[ad_1]

Analyst Report: Lennar Corp.

[ad_2]

[ad_1]

The retailer behind the Garage and Dynamite banners says based on the result it now expects comparable store sales growth for its 2025 financial year to be in a range of 26.5% to 27.0%. The new guidance for the year ended Jan. 31 compared with earlier expectations for between 25.5% and 27.5%.

Groupe Dynamite also raised the lower end of its adjusted earnings before interest, taxes, depreciation and amortization margin for its 2025 financial year. The retailer now expects its adjusted EBITDA margin to come in between 36% and 37% compared with earlier expectations for between 35% and 37%.

Capital spending for the year is expected to be in a range of $80 million to $90 million for the year, down from a range of $85 million to $95 million, mainly reflecting payments timing.

Lululemon Athletica Inc. says it expects its net revenue and diluted earnings per share for its fourth quarter to come in at the high end of its guidance for the period. Chief financial officer Meghan Frank says the update is based on the company’s performance over the holiday season.

The retailer had previously guided for revenue in a range of US$3.500 billion to US$3.585 billion and diluted earnings per share between US$4.66 and US$4.76 for the fourth quarter.

The company made no changes to its guidance for gross margin, selling, general and administrative expenses, or the effective tax rate.

The results come as Lululemon CEO Calvin McDonald prepares to step down from his role effective Jan. 31. Founder Chip Wilson, who has been critical of the company, has nominated three director candidates for Lululemon’s board, saying the search for McDonald’s replacement should be led by new, independent directors.

Kinross Gold Corp. says it is going ahead with the construction of three organic growth projects in the U.S. that will cost a total of nearly US$1.4 billion. The company says the initial capital costs of its Round Mountain Phase X project in Nevada are expected to total US$400 million over four years, while the Bald Mountain Redbird 2 project in the state is expected to cost US$490 million over three years. The Kettle River-Curlew project in Washington is expected to cost US$485 million over three years.

Kinross says the projects are expected to meaningfully extend mine life and will benefit long-term costs within its U.S. portfolio.

Chief executive Paul Rollinson says the new growth projects are expected to contribute three million ounces of life-of-mine production to its portfolio. The company says it intends to fund the projects from operating cash flows.

[ad_2]

The Canadian Press

Source link

[ad_1]

2025 was a milestone year for BTC and other cryptocurrencies. The passing of the GENIUS Act in the U.S., which regulates U.S. dollar stablecoins, confirmed crypto’s status as a mainstream asset. Equally important was the proliferation of cryptocurrency exchange-traded funds (ETFs) in Canada, the US, and other countries. Investors no longer need to jump through hoops or navigate the crypto ecosystem to invest in BTC, ethereum (ETH), Solana (SOL) or other cryptocurrencies. Now, getting exposure to crypto is as easy as buying an S&P 500 Index ETF or a S&P/TSX Composite Index ETF.

How did BTC perform as an investment in 2025? Although it was down a relatively modest 7.32% from the beginning to the end of 2025, investors experienced wild up and down swings through the year. Here’s how much BTC gained or lost in each quarter of 2025.

2026 is off to a wild start. The US special forces entered Venezuela, captured the country’s leader Nicholas Maduro and his wife, Cilia Flores, and flew them to New York to face charges.

How does this affect BTC? BTC trades in two ways: sometimes as a safe haven asset like gold, and other times like a technology stock that rips higher in times of market optimism and exuberance. In the weeks since this year began, BTC has traded like a safe haven asset, gaining on the back of rising geopolitical tensions exemplified by the US military action in Venezuela.

We’ve ranked the best crypto exchanges in Canada.

From the beginning of 2026 to now (mid January 2026) BTC has gained over 8% and gold is up about 5%. Why so? Much of the geopolitical uncertainty these days is caused by actions taken by, or statements made by the US government. As a result, investors are on the lookout for assets that are—at least partially—independent of US government influence.

Enter gold and BTC. They’re both globally traded assets that aren’t structurally controlled by the US—or any other country. Further, both are considered by many investors to be alternative forms of money. In fact, gold and BTC are often clubbed together as hard assets; that is, assets the value of which cannot easily be manipulated or inflated by governments, including the US.

Does this mean that the price of BTC will continue to rise this year as long as geopolitical uncertainty persists? It’s not that simple.

While BTC—like gold—does rise on the back of geopolitical uncertainty, it is also (somewhat paradoxically) considered a risk-on asset. In other words, just like stocks, it gains substantially in low-interest rate regimes when the market is flush with liquidity. Therefore, for BTC to gain substantially in 2026, inflation (especially in the US, which is the world’s largest capital market) would need to be soft and interest rates would need to remain low.

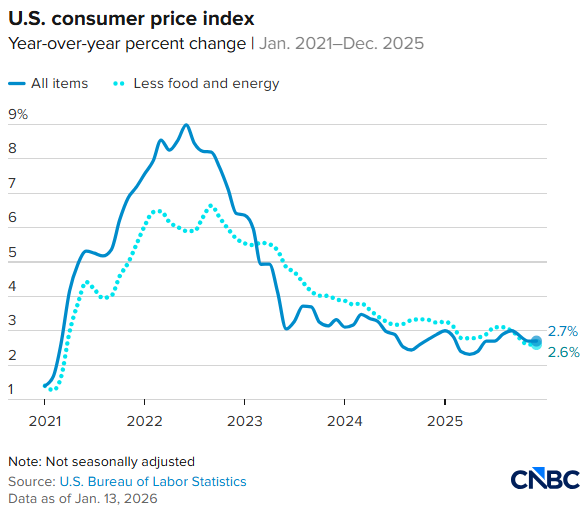

US inflation data right now is encouraging, with the headline U.S. consumer price index (CPI) for December 2025 coming in at 2.7% on an annual basis. This is in line with expectations and within the U.S. Federal Reserve’s (the Fed’s) comfort zone—which means that the Fed may not be in a hurry to raise interest rates. This is positive news for BTC.

The chart below shows the CPI trajectory from 2021 to the latest print for December 2025. As is clear from the chart, CPI has remained relatively low—within the 2% to 3% band—for well over a year on the back of soft crude oil prices and efficiency gains from the adoption of artificial intelligence (AI).

Source: cnbc.com as of January 13, 2026

Where BTC goes in 2026 will in no small part depend on the price of oil, the continued adoption of AI by large global companies, and the effect these will have on inflation.

Cryptocurrencies including BTC, ETH, XRP, SOL, BNB, and others are speculative and highly volatile assets subject to significant price movements. Even stablecoins, which are seemingly “safe,” may be risky if not adequately backed by real-world assets.

Investing in bitcoin and other crypto coins carries significant market, technological, and regulatory risks. Invest in crypto only if it aligns with your broader investment goals, time horizon, and risk profile, and always stay vigilant about crypto scams.

[ad_2]

Aditya Nain

Source link

[ad_1]

If you personally pay for expenses on behalf of your company, it owes you for these personally paid corporate expenses. You can be reimbursed tax-free.

If you deposit money to your corporation, the same situation applies—that is, you are owed money back tax-free. This situation can occur if you have to top up your corporate bank account or deposit money to be used for a real estate down payment for the company.

The rest of this summary will focus on situations where you owe money to your corporation.

Some business owners take withdrawals over the course of the year from their corporation without running them through payroll. At year-end, you can address this by declaring a bonus with payroll withholding tax payable in January. This bonus has the identical tax treatment to salary, as both are reported as employment income on your T4 slip.

The other alternative is to declare a shareholder dividend. This has no withholding tax. The tax implications will instead be a combination of corporate and personal tax. This is because unlike a salary or bonus, dividends are not tax deductible for a corporation. Since a dividend is a distribution of after-tax corporate profits, the personal tax payable is lower than a salary or bonus.

However, the all-in tax is comparable, and in most cases, higher than paying a salary or bonus at most income levels in most provinces and territories.

Deadlines, tax tips and more

If you want to loan money to yourself or a family member from your corporation, this is generally considered taxable income. The default assumption by the Canada Revenue Agency (CRA) is that loans are disguised as compensation unless a specific exemption applies.

The primary exception is if you repay the loan within one year after the corporation’s fiscal year end. For example, a loan outstanding on December 31, 2025 for a corporation with a calendar year-end needs to be repaid by December 31, 2026. If not, it will be considered taxable.

The CRA does not like when you engage in a series of loans and repayments, either, and may treat the original loan as being taxable. So, be careful about back-to-back loans.

There is a very narrow exemption for loans to employees for specific purposes like buying a work vehicle for employment duties, a home, or shares of the employer. It does not happen often in real life, and owner-managers who think they can loan money to themselves under this exception are probably out of luck. Specified employees who own 10% or more of a company cannot qualify.

Business owners and their accountants often overlook the deemed interest benefit of a shareholder loan. There should be an income inclusion for the notional interest on the loan. The rate applied is CRA’s prescribed rate. As of Q1 2026, the rate used to calculate taxable benefits for employees and shareholders from interest-free and low-interest loans is 3%.

If a loan is forgiven, the principal may be considered a taxable benefit to the owner-manager. The problem is that the corporation may not get a tax deduction, so there is an element of double taxation that may apply.

If an owner-manager owns more than one corporation, they sometimes lend money between two companies. You may be able to loan money between two companies you own without triggering tax.

If you are loaning money between an operating company that is a going concern and an investment holding company, be careful about exposing shareholder loan assets owned by the operating business to company creditors. In some cases, it may be better to ensure that dividends can be paid from one company to another, either directly with the second company as a shareholder or indirectly using a trust.

Shareholder loans should usually be temporary as opposed to permanent. They can have unexpected tax implications, so proper planning is key.

Owner-managers should discuss shareholder loans with their tax accountant with a proactive planning-first approach rather than after year-end when filing their tax return.

[ad_2]

Jason Heath, CFP

Source link

[ad_1]

Kelly Ho, a certified financial planner at DLD Financial Group, says you should start by identifying your fixed costs such as rent, mortgage, utilities or car payments followed by figuring out how much you make. “Sometimes when I ask clients, ‘What is your income?’ Not everyone can give me a straight answer,” she says.

From there, she says, take at look at the rest of your spending and see how it compares with your budget to see where the differences are. If you pay by credit or debit card, your monthly statement will help show where the money is going. “It’s just a matter of really understanding how much money is coming in and how much is going out,” Ho says.

Subscriptions can be a stealthy way to lose track of costs. The cost of subscriptions for not just shows and music, but other services can pile up over time. With apps offering easy sign-ups and free trial periods, it can add up before you realize, unless you keep careful track of your spending.

“Everything costs money and sometimes in the spur of the moment, we’ll subscribe with the intent of unsubscribing at some point. But again, life gets busy, so therefore we leave it on and we’re wondering why our credit card bill is so high every month,” Ho says.

Ho says finding savings of $10 a month here and there can quickly add up if you are cancelling more than one subscription or service you don’t need or use. “You multiply that by 12 months, multiply that over several years, plus, you know, potential investment growth. That’s a lot money on the table,” she said.

Find the best and most up-to-date savings rates in Canada using our comparison tool

Ho says travel is another area where your budget may not match reality.

“Every single individual I’ve spoken to has underestimated the cost of travel,” she says. “I don’t know if many people actually keep track of what they’re spending when they’re there at their destination.” An extra round of drinks, a pricey souvenir or an extra excursion while on vacation can add up to blow past a planned budget. “I encourage people to be more intentional about saving for travel as opposed to simply lumping travel in with everyday costs,” Ho says.

Becky Western-Macfadyen, manager of financial coaching at non-profit credit counselling agency Credit Canada, says when reviewing spending on things like wireless plans that can include all sorts of bells and whistles, it is important to understand what you need. “You want to make sure you’re paying for what you actually will use in your plan,” she said.

Western-Macfadyen also says deleting apps like food delivery services from your phone might make it less convenient, but stopping regular spending on takeout or at least making it a littler harder will add up.

She said the payoff of having a little savings put aside for an emergency can even help you save in the future by avoiding taking on debt. But, she acknowledged that changing spending habits can be hard and sometimes the reality is you can’t find areas to cut.

“If someone looks at their budget and thinks there’s nowhere to cut, that doesn’t mean they’ve failed,” she said. “It means the budget is just telling you the truth. It’s information. And savings comes from understanding your cash flow and sustainable change. So you want to just tell yourself the truth so you can make decisions based on that.”

[ad_2]

The Canadian Press

Source link

[ad_1]

Speed is also a problem. Traditional payment systems can take days to process cross-border transfers. Reducing this friction could boost productivity and strengthen Canada’s economy at a time when both are desperately needed.

Enter stablecoins: regulated digital currencies that combine the reliability of traditional money with the efficiency of modern technology.

A stablecoin is a digital currency pegged 1:1 to a traditional currency, such as the Canadian dollar. Unlike Bitcoin or other cryptocurrencies whose values can vary wildly, stablecoins (true to their name) are designed to hold stable value. This makes them practical for everyday or recurring payments.

Think of stablecoins as the digital equivalent of cash: familiar and stable in value, but built on blockchain technology. This allows money to move instantly, securely, and across borders without relying on slow intermediaries.

We’ve ranked the best crypto exchanges in Canada.

Stablecoins could change how Canadians send and receive money. Each year, Canadians send roughly US$8 billion abroad. Families that depend on remittances could save significant amounts annually, while businesses could recoup lost funds from cross-border transactions.

Beyond individual savings, a more efficient payment system strengthens the economy; it supports innovation, improves competitiveness, and makes it easier for Canadian companies to engage in global trade.

Global regulators are taking notice. The U.S. is moving forward with the GENIUS Act, and the European Union has its Markets in Crypto-Assets Regulation. Canada is keeping pace with a recently announced national stablecoin framework that, when in place, will ensure stablecoins meet strict standards, similar to traditional financial tools.

These regulations help ensure that stablecoins are backed by high-quality reserves, so each digital dollar equals a real one. Strong regulation builds confidence and allows Canadians to feel more secure using new payment tools. In 2023, Coinbase research showed that 72% of Canadians say regulation is important, and 29% of non-owners say they would purchase crypto if the industry were better regulated.

Canadian dollar-backed stablecoins like QCAD are already in development. With the regulatory framework in place, stablecoins could soon start showing up in everyday life—starting with business payment processors and e-commerce platforms.

Canada has long been a hub for innovation, but it has lagged in integrating the advances into practical financial tools. Stablecoins give Canadians a chance to embrace faster, cheaper, and more efficient payments that are better suited to digital life and keep pace with trends in the global financial system.

By modernizing the backbone of our financial system, stablecoins could help families and businesses save money, strengthen productivity, and expand participation in the digital economy. Faster, smarter payments aren’t just convenient—they’re essential for Canada’s economic future.

Information is provided for informational purposes only and is not investment advice. This is not a recommendation to buy or sell a particular digital asset or to employ a particular investment strategy. Coinbase Canada, Inc. is registered as a Restricted Dealer in all provinces and territories of Canada. Trading in crypto assets may result in the loss of invested capital.

Although the term “stablecoin” is commonly used, there is no guarantee that the asset will maintain a stable value in relation to the value of the reference asset when traded on secondary markets or that the reserve of assets, if there is one, will be adequate to satisfy all redemptions.

[ad_2]

Jessica Barrett

Source link

[ad_1]

Over the same time, equity markets have provided returns well above historical averages, which can lead people to take more risk than they normally would by reducing their bond holdings.

Adding to that, if you look at pre-tax historical bond returns, there have been some long stretches when returns have been really bad as you can see in the table below.

U.S. government bond returns

| Time Period | Annualized Return | |

| Before Inflation | After Inflation | |

| 1926–2024 | 4.9% | 1.9% |

| 1926–1980 | 3% | 0.1% |

| 1980–2020 | 9.1% | 5.9% |

| 2020–2024 | -5.8% | -9.6% |

Given that historical context and the knowledge that from 1980 to 2020 we were in a decreasing interest rate environment, ideal for bonds, why would you invest in bonds today?

Your question reminds me of a book I read about 10 years ago, Why bother with bonds? The author, Rick Van Ness, suggests there are four reasons to consider bonds: 1. Stocks are risky, 2. Bonds make risk more palatable, 3. Bonds can be a safe bet, and 4. Bonds can be an attractive diversifier in your portfolio. I’ll walk through each of these but, as I do, consider how each of these would apply to your portfolio needs.

1. Stocks are risky

I am guessing you have read that equities become safer over time. That is true and false. Sure, if you invest $1 today in equities, the longer you hold it the more likely you are to enjoy positive returns. You can see this looking at the historical data. Great! But does that mean equities became safer? No!

If you have a $100,000 portfolio and equities drop 40%, taking your portfolio to $60,000, are you feeling good that the $1 you invested 10 or 20 years ago may still have a positive return? No, you are thinking you just lost $40,000. Will it get worse, will you get your money back, and how long will it take? What if you had a million-dollar portfolio that went to $600,000?

Equity markets are always at risk of dropping. What if they drop while you are drawing an income or spending money from your portfolio? The reason for holding bonds or an alternative to bonds is to protect the money you plan to spend in the short term from market declines and provide liquidity for spending needs.

2. Bonds make risk more palatable

Holding bonds may prevent you from buying high and selling low. Imagine you have a $1-million portfolio rapidly dropping to $600,000; what are you going to do? Buy, sell, or hold? Some people will panic and sell, which is the real threat to investment success. Volatility on its own is not a problem. It only becomes a problem when it is combined with a withdrawal.

What typically happens when a panic sell occurs? You wait for the right time to get back into the market, if you ever get back into the market. A scared investor doesn’t wait until things get even worse to invest so they can buy low. Instead, they wait until markets recover, things feel good, and then they buy high.

In this case the reason for holding bonds or an alternative to bonds is to anchor your portfolio so that it only drops to an amount you can tolerate before panic selling. Liquidity is not necessarily a requirement to make risk more palatable.

3. Bonds can be a safe bet

In its basic form, a bond is a simple interest-only loan. You lend money to a government or company and in return, they promise to pay you a rate of return. At the end of the term, they give you back your money. There are some risks with bonds, often associated with changes in interest rates, the length of the term, the strength of the originator, and the ability to buy and sell bonds. However, in general they are safer than equities at protecting your capital—capital you can use for spending. Equities are for protecting your long-term purchasing power, matching or beating the rate of inflation.

If you are considering an alternative to bonds, ask yourself: is the investment as safe as a bond?

[ad_2]

Allan Norman, MSc, CFP, CIM

Source link

[ad_1]

Toronto-based Sigma Lithium Corp., which operates lithium mines in Brazil, led the pack, nearly doubling in value over the three months to December 31, 2025. Its performance testified to strong execution—net revenues rose 69% quarter-over-quarter and 36% year-over-year—but also to resumed investor interest in lithium, a key component in rechargeable batteries essential for the energy transition.

Aris Mining of Vancouver came in a distant second, with a 61.9% return, followed by Toronto-headquartered Discovery Silver Corp., at 58.9%. Aris is a miner of gold in Colombia that counts mining tycoons Frank Giustra, Ian Telfer, and Neil Woodyer among its shareholders; it consolidated its stake in the Soto Norte property during the quarter and was added to the S&P/TSX Composite in September.

Backed by mining investor Eric Sprott, Discovery Silver acquired the Porcupine Complex near Timmins, Ont., from Newmont Corp., in 2025, adding to a roster of promising assets that includes the Cordero project in Mexico. Discovery and Aris were among seven of the top 10 stocks last quarter tied to precious metals, including six miners and the Sprott Physical Silver Trust, an investment vehicle for investors seeking exposure to silver bullion.

By comparison, the cap-weighted, 218-member S&P/TSX Composite, the standard benchmark of Canadian stocks, rose 5.6% over the period; its total return, including dividends, was 6.25%. Though down from the third quarter, these numbers still bested the S&P 500 in the U.S., which returned 2.35% (2.7% total return) in Q4.

Here are Canada’s top 10 best performing mid- to large-cap momentum stocks for Q4 2025:

There was significant overlap between the top performers for the fourth quarter and the 10 best Canadian mid- and large-cap performers (market capitalization of $2 billion or more) for the year. Seven of the top stocks of the past three months turned up in the top 10 for all of 2025. Discovery Silver shot out the lights with a more than 10 times return for the year. The next-best stock to have in your portfolio was tungsten miner Almonty Industries, with an 859% annual return, trailed by Americas Gold and Silver Corp. at 450%. Here again, mining stocks dominated, with the sole exception of Groupe Dynamite.

Here are the top 10 best-performing mid- and large-cap Canadian stocks for 2025:

Though momentum is a demonstrated factor in equities investment, past performance is not an indicator of future returns.

[ad_2]

Michael McCullough

Source link