[ad_1]

Analyst Report: KKR & Co. Inc.

[ad_2]

[ad_1]

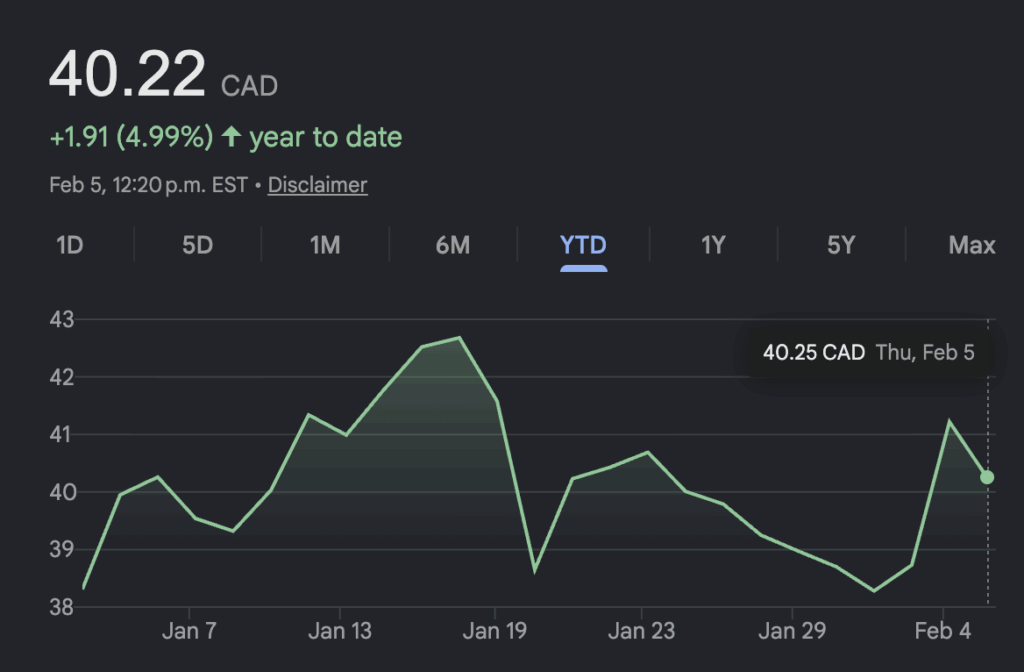

Adjusted operating earnings, which Suncor considers a better gauge of its underlying performance because it filters out the effects of unusual items, were $1.33 billion, or $1.10 per share. That’s a drop from the prior-year quarter, when Suncor had adjusted operating earnings of $1.57 billion, or $1.25 per share.

Operating revenues, net of royalties, were $12.04 billion for the period, down from $12.53 billion. Total upstream production was a record 909,000 barrels per day, up from 875,000 in the same 2024 period.

ATS Corp. reported third-quarter net income of $30.0 million, up from $6.5 million a year ago as its revenue rose nearly 17%. The maker of automation systems says the profit amounted to 30 cents per diluted share for the quarter ended Dec. 28 compared with a profit of seven cents per diluted share a year earlier.

On an adjusted basis, ATS says it earned 48 cents per share in its latest quarter, up from an adjusted profit of 32 cents per share a year earlier.

Revenue for the quarter totalled $760.7 million, up from $652.0 million.

ATS chief executive Doug Wright says the results reflected solid organic revenue growth across its portfolio, including continued momentum in services.

The company’s order backlog stood at $2.05 billion at the end of its most recent quarter, compared with $2.06 billion a year earlier.

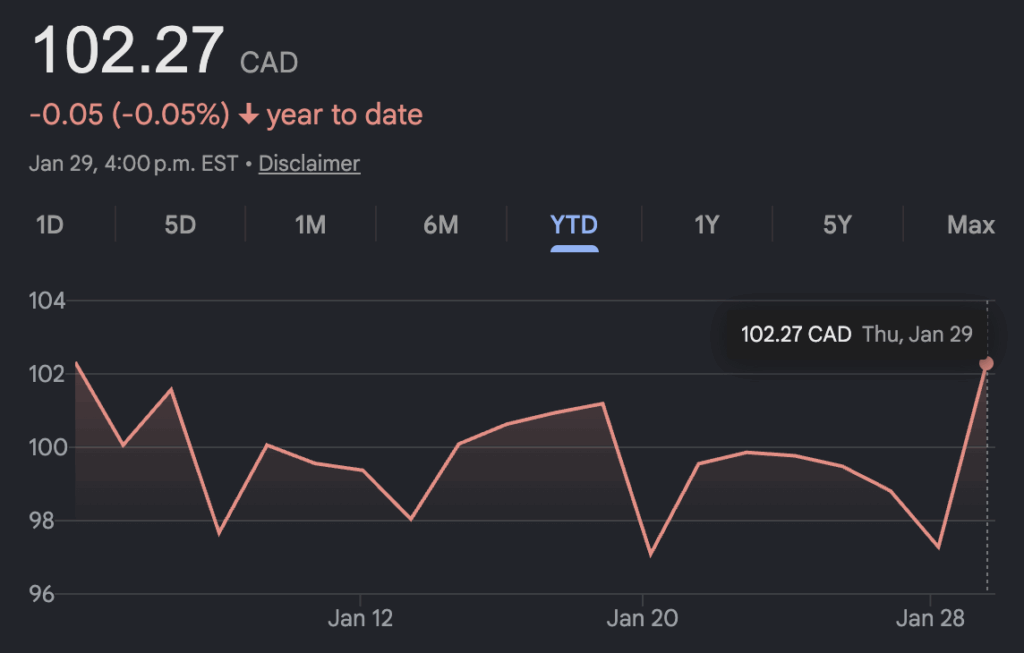

CGI Inc. reported a first-quarter profit of $442.0 million, up from $438.6 million a year earlier, as its revenue rose nearly 8%. The business and technology consulting firm says the profit amounted to $2.03 per diluted share for the quarter ended Dec. 31, up from $1.92 per diluted share a year earlier.

Revenue for the three-month period totalled $4.08 billion, up from $3.79 billion. On an adjusted basis, CGI says it earned $2.12 per diluted share in its most recent quarter, up from $1.97 per diluted share a year earlier.

Earlier this week, CGI announced a collaboration deal with OpenAI that will see it expand the use of artificial intelligence across its business and help clients adopt it in their operations.

CGI has 94,000 consultants and professionals across the globe that provide business and technology consulting services.

Thomson Reuters raised its dividend by 10% as it reported a fourth-quarter profit of US$332 million, down from US$587 million a year earlier.

The company says it will pay a quarterly dividend of 65.5 US cents per share, up from 59.5 cents US per share. The increased payment came as Thomson Reuters says its fourth-quarter profit amounted to 74 cents US per diluted share for the quarter ended Dec. 31, down from US$1.30 per diluted share a year earlier.

Revenue totalled US$2.01 billion, up from US$1.91 billion in the fourth quarter of 2024. On an adjusted basis, Thomson Reuters says it earned US$1.07 per share in its latest quarter, up from an adjusted profit of US$1.01 per share a year earlier.

The average analyst estimate had been for an adjusted profit of US$1.06 per share, according to data compiled by LSEG Data & Analytics.

BCE Inc. reported a fourth-quarter profit attributable to common shareholders of $594 million as its revenue edged lower compared with a year ago. The company says the profit amounted to 64 cents per share for the quarter, compared with a profit of $461 million or 51 cents per share a year earlier.

[ad_2]

The Canadian Press

Source link

[ad_1]

That’s where guaranteed investment certificates (GICs) can quietly shine. When used strategically, GICs can provide balance, certainty, and tax efficiency within an RRSP. And when those RRSP GICs come from a credit-union-backed financial institution offering highly competitive rates, like Achieva Financial, they can be a key building block in your retirement strategy instead of just a supporting piece. RRSP GICs offer a way to reduce your taxes today while adding predictability to your long-term retirement plan.

Discussions about investing often focus on maximizing returns. Mutual funds and exchange-traded funds (ETFs) naturally dominate, especially earlier in an investor’s journey. But while higher-risk growth assets are important, relying on them too heavily can expose your portfolio to more volatility than you might be comfortable with.

Investor behaviour reflects this tendency. A Fair Canada Investor Survey found that more than 80% of investors purchase higher-risk investments like mutual funds and ETFs, but far fewer (only 31%) look to low-risk options like GICs. In other words, many Canadians prioritize growth potential, even when it comes with greater volatility.

What is often missed is the value of certainty. Guaranteed returns can provide stability, predictability, and peace of mind—and this matters when you need to protect your capital.

A GIC is a low-risk investment that offers a fixed rate of return over a set period of time. GICs are available from banks, trust companies, and credit unions, including online divisions like Achieva Financial, including credit unions and their online divisions, like Achieva Financial, which is part of Manitoba-based Cambrian Credit Union.

Unlike market-based investments such as ETFs and mutual funds, GICs protect your principal while delivering a guaranteed return. This makes them especially good options for RRSP investors who value stability alongside growth. Achieva Financial offers among the highest GIC rates in Canada, including a 2-year RRSP GIC currently paying 3.80%, allowing investors to lock in returns with confidence. All deposits are guaranteed without limit by the Deposit Guarantee Corporation of Manitoba.

GICs are typically available with terms ranging from one to five years. While longer terms often offer higher rates, this offers a good opportunity to strategically “ladder” GICs. When you spread your RRSP GICs across different terms, some of your savings mature each year. This gives you steady access to your money, helps you adjust to changing interest rates, and makes retirement income planning more predictable.

If you’re considering RRSP GICs ahead of the March 2, 2026 contribution deadline, a few key factors can help guide your decision:

Once GICs are part of your RRSP, their role will naturally evolve over time.

Early in your career, when retirement is still years (or decades) away, your portfolio may lean heavily into mutual funds or ETFs with a smaller allocation to GICs. That said, GICs can still play an important role for younger investors with a lower risk tolerance, whether due to discomfort with market volatility or a shorter-term goal like saving for a first home. As retirement approaches, you may want to gradually shift towards investments with guaranteed returns that reduce volatility and protect the savings you’ve accumulated.

This gradual transition can help preserve the progress you’ve made, without removing growth from the equation.

GICs aren’t just a conservative choice, they’re a strategic one. Within an RRSP, they combine tax efficiency with guaranteed rate of return, making them particularly valuable as retirement gets closer and priorities begin to shift. They can also make sense earlier on, particularly for younger investors who prefer certainty over volatility or are working toward shorter-term goals within their registered plan.

With competitive rates like Achieva Financial’s 2-year RRSP GIC at 3.80%, term options suited to laddering, and deposits guaranteed without limit by the Deposit Guarantee Corporation of Manitoba, Achieva’s RRSP GICs help create a steady, worry-free approach to planning for retirement. Combining GICs with higher-risk investments is a common way to build a balanced portfolio that will serve you through your golden years.

As the March 2 RRSP deadline approaches, this may be the ideal time to revisit how Achieva RRSP GICs can fit into your long-term plan—and whether your RRSP asset mix could benefit from more certainty.

[ad_2]

Jessica Gibson

Source link

[ad_1]

Young people face many of the same job challenges as older workers, plus some extra ones, like limited work experience. Still, they have one major advantage: time. Younger people have more years to save and invest. If you’re Gen Z and trying to improve your financial future in a shaky economy, starting now can make a big difference.

Gen Z includes people born between 1997 and 2012, which closely matches the 15–24 age group used by Statistics Canada. Here’s a snapshot of their financial situation.

Rising prices affect everyone. Inflation, high rent costs, and expensive groceries are putting pressure on young Canadians, just like older ones.

More than 50,000 young people claimed EI in one year alone. This number doesn’t include gig workers, contractors, part-time workers, or others who don’t qualify for EI. That means the real number of unemployed young people is likely higher.

Even those who are working are struggling. Many hold two or more jobs to keep up with costs. A KOHO survey found that Gen Z’s average monthly income is just $1,083. Nearly half (49%) expect to take on more work in the next year, and 70% say they feel financially unstable or only somewhat stable.

Younger Canadians generally have less debt than older groups, but the average is still close to $8,500 per person. That’s an increase of 3.84% from the year before, according to Equifax.

Gen Z doesn’t have much left over to save. The KOHO study found that end-of-month balances averaged just $9 to $16. Still, savings among this group grew by 23% year over year. That effort to save and invest, even with tight finances, is a positive sign for the future.

When it comes to saving and investing, how long your money stays invested matters just as much as how much you put in. The longer your money sits in an account or investment, the more interest it can earn. This is called a time horizon.

Compound interest means earning interest on both your original money and the interest it has already earned. For example, here’s what happens if you invest $100 at a 2% interest rate:

| Starting amount | Interest earned | Ending amount | |

|---|---|---|---|

| Month 1 | $100 | $2 | $102 |

| Month 2 | $102 | $2.04 | $104.04 |

| Month 3 | $104.04 | $2.08 | $106.12 |

| Month 4 | $106.12 | $2.12 | $108.24 |

| Month 5 | $108.24 | $2.16 | $110.40 |

Savings accounts and GICs are examples of investments that earn compound interest.

Stocks work differently because their value goes up and down. They’re riskier, but they can also offer higher returns. Having a long time horizon gives your investments more time to recover after market drops.

Most people benefit from having different types of savings and investments for different goals. Here are some common options for young Canadians.

Unregistered accounts don’t have limits on deposits or withdrawals. They work like regular savings or chequing accounts.

A high-interest savings account (HISA) is good for emergency savings because you can access your money anytime. A guaranteed investment certificate (GIC) locks your money in for a set period, which can work well for medium-term goals.

These options are low risk because they guarantee your original money plus interest. The downside is lower returns compared to riskier investments.

Registered accounts offer tax benefits that help Canadians save and invest more effectively.

[ad_2]

Keph Senett

Source link

[ad_1]

As your financial needs change from early career to mid-life to pre-retirement to retirement itself, so, too, should the way you approach your investments.

Even though retirement is likely decades away, getting started with investing when you’re in your 20s or early 30s is one of the best money moves you can make. You’re likely embarking on your career, so you’ll have a steady source of income. But more importantly, you’ve got decades to go until you’ll need to access your retirement funds, which gives you more leeway to weather ups and downs in the market.

In this stage, you should consider not only setting up your retirement funds, but also about setting aside money that you may need in the medium term, whether you’re saving for a house or car, or planning for a family.

If you invest early, even with modest contributions, you’ll have a major advantage over people who wait: time.

For your retirement fund, you can get started with an equity-focused mutual fund or exchange-traded fund (ETF). Both options may give you access to a broad swath of the stock market without having to actually buy individual stocks. You can start small and set up pre-authorized contributions that can help your investment grow over time. (At Tangerine, these are called Automatic Purchases, which can be set up for any of their 13 investment portfolios.)

For investments that you expect to use within the next 6–10 years, consider a more conservative approach, with funds that lean more heavily on predictable income such as bonds or GICs, which offer regular interest income and return your initial investment if held to maturity.which offer regular interest income and return your initial investment if held to maturity. These are considered less risky than stocks, though the stock market has historically performed better over time.

As a young adult, you might want investments that offer flexibility and tax-free growth. Take a look at a TFSA to get started. You can contribute up to the federally mandated annual limit (which accumulates each year) and have access to your funds if you need to withdraw them at any point. (Note, however, that if you store something like a GIC in your TFSA, you will still need to wait for the maturity date to access your money.)

The registered retirement savings plan (RRSP, also called an RSP) is the other big one to consider. As the name suggests, it’s designed to be used in retirement. Like the TFSA, there are annual contribution limits. Like the TFSA, there are annual contribution limits. What’s different here is that your contributions are tax-deductible, meaning they can reduce the amount you pay in income taxes today. Instead, you’ll pay tax on the money when you withdraw it, likely in retirement when you will likely be in a lower tax bracket.

Both TFSAs and RRSPs can hold a variety of savings and investing vehicles, including mutual funds, ETFs, stocks, bonds or savings accounts. You can set up and manage your portfolio yourself or have an advisor/portfolio manager handle it for a fee, adjusting as you see fit over time.

By the time you’re in your 30s and 40s, your income may have risen, but you may also have taken on more debt and may even be caring for older relatives. At this point, you’ve got competing priorities: saving for retirement, putting down money on housing or paying down a mortgage, and supporting family.

Because of these demands, you may be a bit more risk-averse with your investments than you were in your 20s. Instead of taking chances on investments with large growth potential, you might favour moderate-risk investments with steady returns or even an additional source of income, such as bond interest or stock dividends.

Your primary goal during this stage of life may be maintaining your portfolio’s growth while starting to reduce risk. Instead of relying primarily on high-growth (and higher-risk) investments, consider introducing more moderate-risk options, balancing out your stock portfolio with bonds, money market funds, and other less volatile investments.

In other words, you may want to adjust your mindset from chasing returns to balancing your portfolio.

You may already have an RRSP that you’re contributing to (perhaps in addition to a TFSA). During this stage of your life, consider prioritizing your contributions so the account becomes the backbone of your retirement savings. This means contributing the maximum amount allowed each year if you’re able.

If you’re also at the point where you’re buying a home, look into a first home savings account (FHSA). This registered savings account allows you to contribute up to $8,000 per year to a maximum lifetime limit of $40,000. Your contributions are tax-deductible and eligible withdrawals are tax-free, giving you a nice lump sum towards a down payment.

What about the Home Buyers’ Plan?

The Home Buyers’ Plan allows you to withdraw funds from your RRSP, up to a maximum of $60,000 tax free, if you’re a first-time homebuyer or haven’t purchased or owned a property in the last four years. This can be a useful strategy if timing, eligibility, or cash-flow constraints make the FHSA less practical, or when you already have money sitting in an RRSP.

As you enter your 50s and 60s, retirement is likely on the horizon. You may be thinking more about protecting your investments and trying to figure out how your savings will translate to actual income once you retire. At the same time, you may also be in your peak earning years, so protecting your money from taxes is still important.

[ad_2]

Jessica Gibson

Source link

[ad_1]

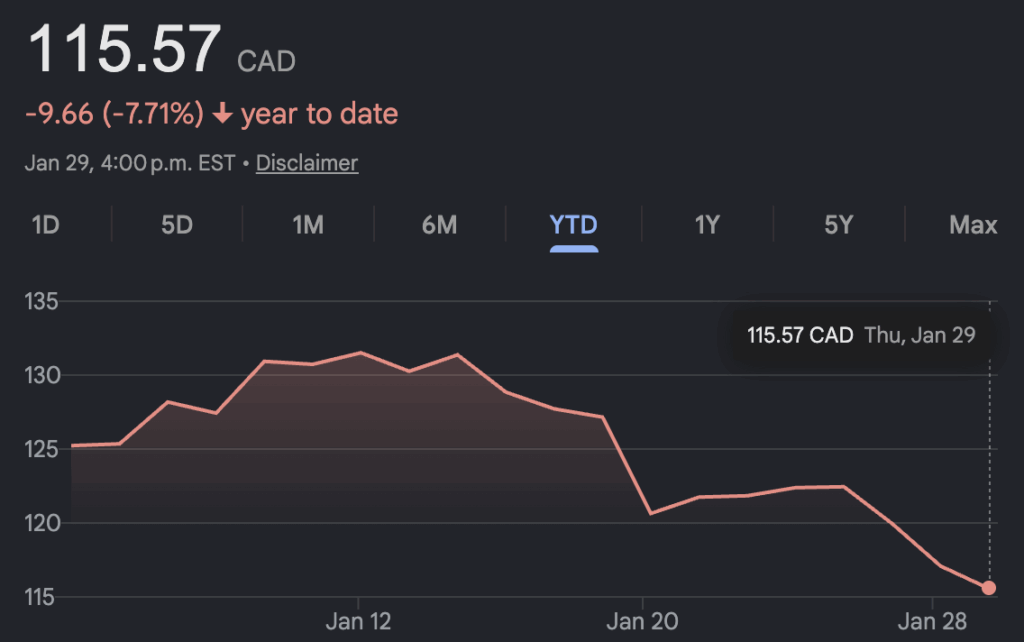

The cable and wireless company, which also owns the baseball team, says it earned a profit attributable to shareholders of $743 million or $1.37 per diluted share for the quarter ended Dec. 31. The result was up from a profit of $558 million or $1.02 per diluted share in the last three months of 2024. On an adjusted basis, Rogers says it earned $1.51 per diluted share in its latest quarter, up from an adjusted profit of $1.46 per diluted share a year earlier.

Revenue totalled $6.17 billion, up from $5.48 billion in the same quarter as year earlier. The increase came as media revenue at Rogers, which includes the Jays, rose to $1.24 billion for the quarter, up from $547 million a year earlier. Wireless revenue for the quarter totalled $2.97 billion, compared with $2.98 billion a year earlier, while cable revenue held steady at $1.98 billion.

The Jays took the Los Angeles Dodgers to extra innings of Game 7 before losing the baseball championship.

Numbers for its fourth quarter:

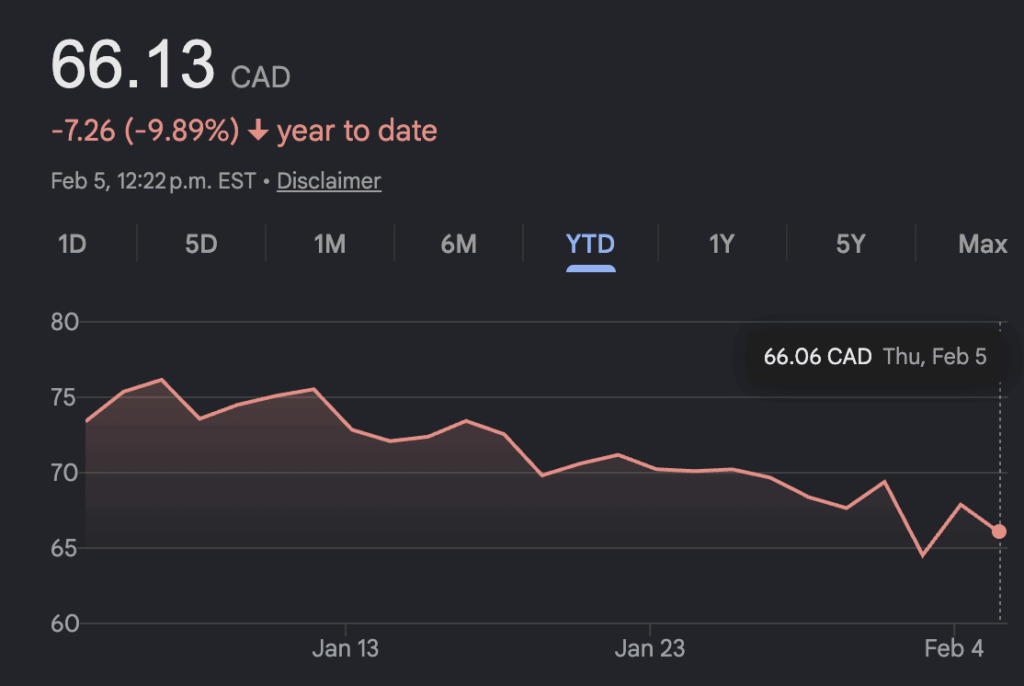

Canadian Pacific Kansas City Ltd. says profits fell 10% in its latest quarter, despite an uptick in revenues that capped off a year of solid earnings growth. CPKC says net income declined to $1.08 billion in the quarter ended Dec. 31 from $1.20 billion in the same period a year earlier.

The Calgary-based railway says fourth-quarter revenues rose 1% to $3.92 billion from $3.87 billion the year before amid a 3% boost in grain and container revenue.

It says core adjusted diluted earnings rose 3% to $1.33 per share from $1.29 per share.

For the full year, CPKC says net income jumped 11% to $4.14 billion and revenues climbed almost 4% to $15.08 billion.

For 2026, the company is predicting low double-digit growth in core adjusted diluted earnings per share, volume growth in the mid-single digits and a 15% reduction in capital expenditures to $2.65 billion.

Numbers for its first quarter:

CGI Inc. reported a first-quarter profit of $442.0 million, up from $438.6 million a year earlier, as its revenue rose nearly 8%. The business and technology consulting firm says the profit amounted to $2.03 per diluted share for the quarter ended Dec. 31, up from $1.92 per diluted share a year earlier.

Revenue for the three-month period totalled $4.08 billion, up from $3.79 billion. On an adjusted basis, CGI says it earned $2.12 per diluted share in its most recent quarter, up from $1.97 per diluted share a year earlier.

Earlier this week, CGI announced a collaboration deal with OpenAI that will see it expand the use of artificial intelligence across its business and help clients adopt it in their operations.

CGI has 94,000 consultants and professionals across the globe that provide business and technology consulting services.

Cascades Inc. has agreed to sell a packaging plant to Crown Paper Group, located in Richmond, B.C.

The transaction is valued at $65.5 million, including real estate assets, and is expected to close in the coming days, subject to closing conditions. Cascades says the plant offered limited integration within its operational network due to its geographic position.

Hugues Simon, the Cascades CEO, says in a news release that the move comes amid a commitment from the company to improve its profitability and optimize operations. The transaction comes after Cascades signed a deal to sell a flexible packaging plant to Texas-based Five Star Holding for $31 million.

Cascades makes cardboard packaging, toilet paper, paper towels and other products.

[ad_2]

The Canadian Press

Source link

[ad_1]

Bank advisors know this rhythm well. If you have cash sitting idle, there is a good chance you have received a call inviting you to review your financial plan or come into a branch. The objective is usually the same: get that cash invested into one of the bank’s in-house products.

For older clients, or those flagged through the know-your-client process as having a lower risk tolerance, the conversation often shifts toward market-linked guaranteed investment certificates (GICs). These products are typically presented as a way to participate in stock market gains while keeping your principal protected.

That pitch has worked for decades. But in 2026, market-linked GICs are no longer the only way to get that type of payoff. Exchange-traded funds (ETFs) have entered the same territory with products commonly called buffer ETFs. Like market-linked GICs, buffer ETFs are designed to limit downside risk while offering some participation in market gains.

As a retail investor, it is reasonable to be cautious here. Added complexity often comes with higher costs, more fine print, and a steep learning curve. When investors own products they do not fully understand, it becomes harder to stay invested through normal market ups and downs, regardless of how the product is designed to work.

Here is what you need to know about buffer ETFs and market-linked GICs in 2026. That includes the key trade-offs, the costs that are easy to overlook, and my honest take on whether either option makes sense for risk-averse investors, beginners and veterans alike.

A market-linked GIC’s principal is protected if you hold the investment to maturity, and it is typically eligible for Canada Deposit Insurance Corporation (CDIC) coverage, subject to the usual limits. The difference shows up in how your return is calculated.

Instead of earning a fixed interest rate for the full term, the return on a market-linked GIC depends on the performance of a specific market benchmark. That benchmark could be a stock index or another predefined group of securities. If the benchmark performs well, your return increases. If it performs poorly, your return falls back to a guaranteed minimum.

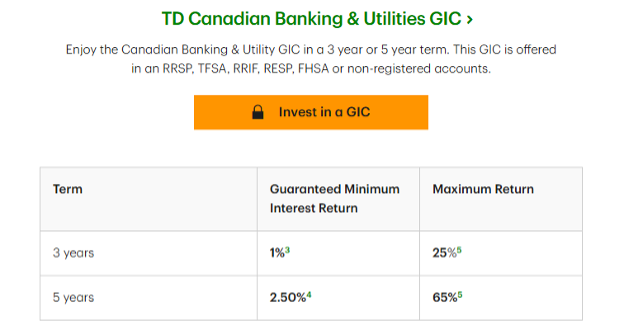

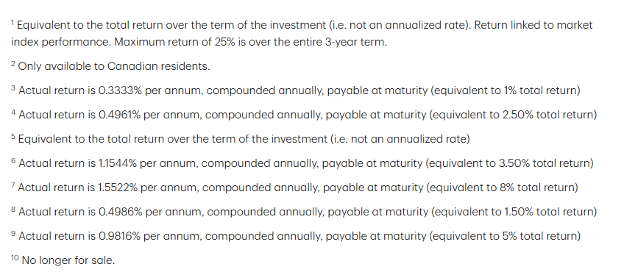

To see how this works in practice, consider the market growth GICs offered by TD Bank. One option is linked to a basket of major Canadian banks and is available in three-year and five-year terms in most registered accounts.

Source: TD, January 2026

For the three-year version, the guaranteed minimum return is 3.5%. For the five-year version, the guaranteed minimum return is 8%. If the linked bank basket performs poorly, that minimum is what you receive at maturity. You cannot lose money as long as you hold the GIC to the end of the term.

However, the upside participation is capped. Over three years, the maximum cumulative return is 18%. Over five years, the maximum cumulative return is 32%. Importantly, these figures are not annualized. They represent the total return over the entire life of the investment.

The fine print matters here. TD discloses that the 8% minimum return over five years works out to about 1.55% per year. The same logic applies to the maximum return. A 32% total return over five years sounds attractive, but once translated into an annualized figure, it looks far more modest.

Source: TD, January 2026

This structure highlights the core trade-off. You are free of downside risk, but you also give up a large portion of the upside. If the underlying market performs exceptionally well, the return above the cap does not accrue to you.

That leads to the obvious question of incentives. Banks earn fees for structuring and distributing these products. This is part of the reason market-linked GICs can be attractive for issuers even when they appear conservative on the surface.

Another common issue is investor misunderstanding. Many people confuse cumulative returns with annualized returns and assume the headline numbers are yearly figures; others assume the maximum return is what they are likely to receive, when in reality it is simply the upper boundary. Actual outcomes can land anywhere between the guaranteed minimum and the cap, depending entirely on how the underlying benchmark performs over the term.

[ad_2]

Tony Dong, MSc, CETF

Source link

[ad_1]

When you have a limited budget, every dollar has to work harder. The margin for error is slimmer, and the overwhelming number of financial products, from ETFs to individual stocks, can lead to analysis paralysis. Experts say there is no bulletproof way to stock pick in the early stages. Instead, focus on structure, simplicity, and consistency.

Before browsing the stock market, young investors need to decide where their money will live. There are a number of options including the tax-free savings account (TFSA), registered retirement savings plan (RRSP), first home savings account (FHSA), or an unregistered account.

Diandra Camilleri, associate portfolio manager at Verecan Capital Management Inc., noted that many young Canadians rush to buy a product without considering the tax implications or accessibility of the account they are using. “Asset location, which is about deciding which accounts hold which investments, is often framed as a tax decision, yet it also affects how accessible your money is and what it can realistically do for you over time,” said Camilleri.

She warned that investors often reach their thirties and forties only to realize they’ve been saving in the wrong vehicle. Whether it is a TFSA for flexibility or an RRSP for long-term growth, getting advice on the “where” you should put your money is just as vital as the “what.”

Once the account is open, how should a beginner deploy a lump sum of $500 or $1,000?

Robert Gill, a portfolio manager at Fairbank Investment Management, said simplicity is paramount. While his firm generally favours other investment strategies for larger portfolios, he notes that a small capital base presents a practical exception for using exchange-traded funds (ETFs).

“With a limited amount to invest, allocating capital across multiple ETFs may introduce unnecessary complexity and excessive diversification,” Gill said. “One broad-based ETF is typically sufficient to provide the diversification and growth potential a new investor requires.”

Gill suggests focusing on those tracking the TSX, S&P 500, or MSCI World, rather than niche sectors. This allows a young investor to participate in the growth of top-tier companies without the fees and complexity of managing a multi-asset portfolio.

Shane Obata, portfolio manager at Middlefield, echoes Gill’s belief of building a broad, diversified global equity base as a stable foundation. Once you’ve done that, he suggests you consider a slightly more active, prudent approach, called a “core and satellite” strategy. “You can layer in specific thematic investments that you believe have long-term durability … to capture higher growth potential,” said Obata.

However, he advises caution when buying passive indices for complex sectors, such as technology. In fast-moving industries, a passive index forces investors to own the “losers” alongside the “winners,” exposing them to unnecessary risk.

A popular option for beginners is the “all-in-one” asset allocation ETF, which holds global stocks and bonds. While convenient, Obata warned they can be a “one-size-fits-most” solution that lack flexibility in response to market conditions. “By bundling everything together, investors lose some flexibility to adjust their asset allocation based on market conditions,” Obata said.

He also notes that in taxable accounts, these funds limit tax-efficiency strategies, such as tax-loss harvesting, because you cannot selectively sell the underlying holdings.

After the initial investment, the next step is monthly contributions. If you only have $200 a month to spare, should you spread it around?

Gill advises against it. “A monthly contribution of $200 is well-suited to investing in a single, diversified ETF, but is generally insufficient to be effectively allocated across multiple investment products,” he said.

Young investors also shouldn’t fret that their monthly contribution is on the smaller side. Camilleri said consistency matters far more than the dollar figure. She recommends setting up automatic contributions to build discipline without having to think about it.

Finally, both Gill and Obata said beginners should avoid the temptation of picking individual stocks. “Picking individual stocks is a difficult proposition that requires a significant time commitment to research and track companies, which most beginners simply do not have,” said Obata.

[ad_2]

The Canadian Press

Source link

[ad_1]

Or, as U.S. retirement guru Wade Pfau recently put it, “A retirement income plan should be based on planning to live, rather than planning to die.” The Michael James blog recently highlighted that quote.

Retirement is usually about planning for unexpected longevity, often exacerbated by inflation. After all, a 65-year-old Canadian woman can expect to live to 87—but there’s an 11% chance she’ll live to 100.

That fact was cited by Fraser Stark, President of Longevity Retirement Platform at Toronto-based Purpose Investments Inc., at a September presentation to the Retirement Club, which we described this past summer. Stark’s presentation was compelling enough that I decided to invest a chunk of my recently launched RRIF into the Purpose Longevity Pension Fund (LPF). A version of Stark’s presentation may be available on YouTube, or you can get the highlights from the Purpose brochure.

Stark confirms that LPF, launched in 2021, is currently the only retail mutual fund or ETF offering longevity-protected income in Canada. Note that LPF is not an ETF but a traditional mutual fund. It aims to generate retirement income for life; to do so, it has created what it describes as a “unique longevity risk pooling structure.”

This reflects what noted finance professor Moshe Milevsky has long described as “tontine thinking.” See my Retired Money column on this from 2022 after Guardian Capital LP announced three new tontine products under the “GuardPath” brand. However, a year ago Guardian closed the funds, so is effectively out of the tontine business. Apparently, it’s a tough slog competing with life annuities.

Here’s the full list of wealth advisors and full-service brokers that offer it. Included are full-service brokerages (and/or their discount brokerage units) of the big banks, including Bank of Montreal, National Bank, and recently Royal Bank on a non-solicited basis. Among many independents offering it are Questrade and Qtrade. In addition, Stark says iA Financial allows investments in LPF on a non-solicited basis.

Purpose doesn’t use the term tontine to describe LPF, but it does aim to do what traditional employer-sponsored defined benefit (DB) pensions do: in effect, those who die early subsidize the lucky few who live longer than expected.

LPF deals with the dreaded inflation bugaboo by aiming to gradually raise distribution levels over time. It recently announced it was boosting LPF distributions by 3% for most age cohorts in 2026, following a similar lift last year.

Here’s how Purpose’s actuaries describe LPF:

“The Longevity Pension Fund is the world’s first mutual fund that offers income for life by incorporating longevity risk pooling, a concept similar to that utilized by defined benefit pension plans and lifetime annuities, to provide lifetime income.”

Purpose envisages LPF working alongside annuities for some retirees (see my last column on why annuities aren’t as popular as some think they should be). LPF is not registered as a pension, but it’s described as one because it’s structured to provide income for life, no matter how long you live. It’s offered as a mutual fund rather than an ETF because it’s not designed to be traded, Stark said in one podcast soon after the launch.

Age is a big variable. Purpose created two classes of the Fund: an “Accumulation” class for those under age 65, and a “Decumulation” class for those 65 or older. You cannot purchase it once you reach 80. LPF promises monthly payments for life but the structure is flexible enough to allow for either redemptions or additional investments in the product—something traditional life annuities do not usually provide. When moving from the Accumulation to the Decumulation product at age 65, the rollover is free of capital gains tax consequences.

The brochure describes six age cohorts, 1945 to 1947, 1948 to 1950 etc., ending in 1960. Yield for the oldest cohort as of September 2025 is listed as 8.81%, falling to 5.81% for the 1960 cohort. My own cohort of 1951–1953 has a yield of 7.24%.

How is this generated? Apart from mortality credits, the capital is invested like any broadly diversified Asset Allocation fund. The long-term Strategic Asset Allocation is set as 49% equity, 41% fixed income and 10% alternatives. As of Sept. 30, Purpose lists 38.65% in fixed income, 43.86% in equities, 12.09% in alternatives, and 4.59% in cash or equivalents. Geographic breakdown is 54.27% Canada, 30.31% the United States, 10.84% international/emerging, and the same 4.59% in cash. MER for the Class F fund (which most of its investors are in) is 0.60%.

Stark says LPF has accumulated $18 million since its launch, with 500 investors in either the Accumulation or Decumulation classes. He also referred me to the recently released actuarial review on LPF.

While LPF (and formerly) Guardian are the two main longevity product suppliers in Canada of which I’m aware, several products in the United States attempt to tackle the same problem in different ways. A few weeks ago, I did a roundup of the major U.S. offerings by contacting various U.S. and Canadian retirement experts through Featured.com and LinkedIn. The resulting blog covers products like Vanguard Target Retirement Income Fund, Fidelity Strategic Advisors Core Income Fund, Stone Ridge LifeX Longevity Income ETFs, and others.

For now, it appears Purpose is alone in this space in Canada, apart from fixed life annuities offered by insurance companies. The U.S. market is different because of Variable Annuities with income options.

[ad_2]

Jonathan Chevreau

Source link

[ad_1]

Common examples include American mortgage real estate investment trusts (mREITs) and business development companies (BDCs). Both tend to be highly leveraged and structurally complex, and the headline yield rarely tells the full story. The same applies to Master Limited Partnerships, or MLPs.

MLPs occupy the midstream segment of the energy sector. This part of the industry focuses on transporting, storing, and processing oil and gas rather than producing or retailing it. Canadian investors are already familiar with midstream businesses through TSX-listed companies like TC Energy and Enbridge. The difference is that these Canadian firms are conventional corporations, not partnerships.

An MLP is a U.S.-specific pass-through structure designed to generate income from energy-related assets. By operating as a partnership rather than a corporation, an MLP avoids corporate-level tax and distributes most of its cash flow directly to unitholders. That structure is the reason for the eye-catching yields. It is also why MLPs have long been popular with income-focused investors stateside.

From a distance, it is easy for Canadians to assume these investments should translate well across the border. Capital markets are similar, the businesses are familiar, and the income looks appealing.

The sticking point is taxation. Differences between Canadian and U.S. tax rules turn MLP ownership into a complicated exercise for Canadian investors, often reducing after-tax returns and creating ongoing administrative headaches. Those frictions matter more than most investors realize.

Here is what Canadian investors need to know about U.S. MLPs, why they are usually best avoided, and which alternatives offer exposure to similar businesses without the same tax complications.

For Canadian investors, the problems with U.S. master limited partnerships come down to two main issues: withholding tax and reporting requirements.

Most Canadians are already familiar with how U.S. withholding works. When you own U.S.-domiciled stocks or exchange traded funds (ETFs), 15% of dividends are typically withheld at source. That withholding can be avoided by holding those securities inside a Registered Retirement Savings Plan (RRSP), thanks to the Canada-U.S. tax treaty.

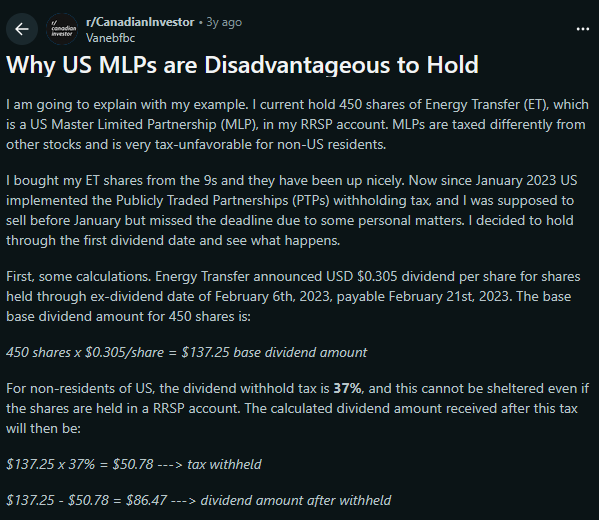

MLPs are treated very differently. They do not benefit from that treaty treatment. Distributions from MLPs are fully subject to U.S. withholding tax. Worse, the rate is not 15%. It is up to 37%. This withholding applies even inside registered accounts, including RRSPs.

Source: r/CanadianInvestor

That means more than one third of each distribution can disappear before it ever reaches your account. This is especially damaging because most of the long-term return from MLPs comes from reinvested distributions rather than price appreciation.

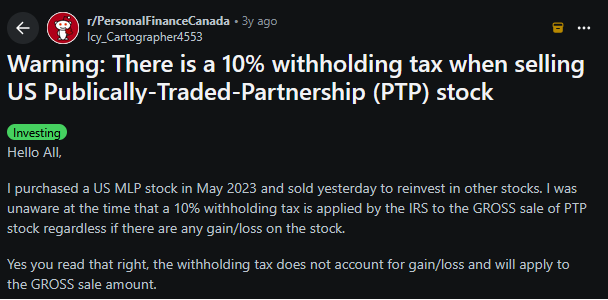

It does not stop there. When you sell an MLP, there is an additional 10% withholding tax applied to the gross proceeds by the Internal Revenue Service (IRS), because MLPs are classified as publicly traded partnerships. This is not a capital gains tax. It is withheld regardless of whether you are selling at a gain or a loss.

There are numerous real-world examples of Canadian investors discovering this the hard way. Some have bought and sold the same MLP multiple times, only to find that 10% was withheld on each transaction.

Source: r/PersonalFinanceCanada

The final complication is tax reporting requirements. When you own a typical U.S. stock, you receive a 1099-DIV form that summarizes your income. With an MLP, you are not a shareholder. You are a partner. That means you receive a Schedule K-1.

A K-1 reports your share of the partnership’s income, deductions, and credits. It is far more complex than a standard dividend slip, and it creates a U.S. tax filing obligation. In theory, you are required to file a U.S. tax return to properly report this income to the IRS.

[ad_2]

Tony Dong, MSc, CETF

Source link