[ad_1]

Getting Ready for a Rate Cut

[ad_2]

[ad_1]

Chalk that up as a win for Canadians. Between the tax-free savings account (TFSA), registered retirement savings plan (RRSP), and first home savings account (FHSA), Canadians have ample room to shelter gains from the Canada Revenue Agency (CRA). These registered accounts offer more flexibility and contribution room than Americans get with comparable 401(k) and Roth IRA plans, and they can go a long way if you use them wisely.

That said, whether from windfalls or diligent saving, some Canadians do manage to max out their registered accounts. Once that happens, and until new room opens up in January, the challenge becomes how to keep more of your investment income and gains from getting taxed in a non-registered account.

Some exchange-traded funds (ETFs) are better than others for this. Here’s a guide to how ETF tax efficiency works in Canada and which types of ETFs work best in taxable accounts.

In a nutshell, ETF taxes work a lot like the taxes on stocks or bonds, because most ETFs are just collections of those underlying investments. If you’ve ever received a T3 or T5 slip, the categories will look familiar.

The easiest way to see how it works in practice is to check the ETF provider’s website for a tax breakdown. We’ll walk through an example using the BMO Growth ETF (ZGRO), a globally diversified asset-allocation ETF that holds about 80% equities and 20% fixed income.

If you scroll down to the “Tax & Distributions” section on ZGRO’s fund page, you’ll see a table that breaks down the composition of distributions by year. The most recent data for 2024 shows the ETF paid out $0.467667 per unit in total distributions, made up of several different tax categories:

All of these get taxed differently, which makes ETFs like ZGRO tricky to manage in a non-registered account. In a TFSA or RRSP, you can ignore this tax complexity because none of it applies. But outside of registered accounts, you’ll need to report this all accurately, which can mean more work at tax time.

ZGRO is still a strong choice overall—it’s diversified, affordable, and well constructed. But for Canadian investors focused on tax efficiency, there are cleaner options. ETFs like ZGRO make the most sense in a registered account where you don’t have to worry about this messy tax mix.

Figuring out which ETFs are more tax-efficient starts with defining your objective. Are you investing for capital appreciation, or are you trying to generate regular income from your portfolio?

If your goal is capital growth and you don’t need to make regular withdrawals, say, for retirement income, the focus should be on ETFs that minimize or avoid distributions. This allows the value of the ETF to grow through share price gains rather than payouts, which can defer your tax burden.

One simple way to do this is to choose growth-focused ETFs. For example, the Invesco NASDAQ 100 ETF (QQC) offers exposure to U.S. tech stocks that typically don’t pay high dividends, since they often reinvest profits into research and development and expansion. QQC’s trailing 12-month yield is just 0.42%, mostly foreign income. That level is low enough to render the tax drag minimal.

If you want to go a step further and avoid distributions altogether, some ETF families are designed specifically to do that. A well-known example is the Global X Canada (formerly Horizons ETFs) suite of corporate class, swap-based ETFs. In simple terms, these ETFs use a different fund structure and derivatives contracts to synthetically replicate exposure to equities while avoiding distributions. This has worked well in practice. You could create a globally diversified equity portfolio using:

But there are trade-offs. These ETFs have seen their fees rise over time. On top of the management fee, they also charge a swap fee and have higher trading expense ratios than traditional index ETFs. This adds to your cost of holding the fund. And because they rely on swaps, you’re exposed to counterparty risk, which is the chance that the other party to the derivative contract (often a big Canadian bank) fails to deliver on its obligation. That’s unlikely but not impossible.

Another caveat is that, while these ETFs are designed to avoid distributions, they can’t guarantee zero payouts. The distribution frequency is listed as “at the manager’s discretion,” largely because of how fund accounting works. And there’s always the risk that tax law changes could alter how these structures are treated, as has happened in the past.

If you’re investing in a taxable account and want to prioritize tax deferral, these ETFs are worth considering, but go in with your eyes open.

Personally, I fall into the camp of just selling ETF shares and paying capital gains tax when I need portfolio withdrawals. But I recognize a lot of investors (especially retirees) have a strong psychological aversion to this. This behaviour is known as mental accounting.

[ad_2]

Tony Dong, MSc, CETF

Source link

[ad_1]

They recognize, too, that there are more fish in the sea than the stock and bond indices represented in core portfolios. They may seek to spice up returns or further diversify with, say, a high-yield bond or crypto fund. There’s no limit to the add-ons you can apply to a couch portfolio.

Second, there are those who get the hang of managing a core portfolio, like the results, and, upon gaining investment knowledge and experience, feel comfortable raising the complexity of their holdings. Couch potato investing offers a good entry level to more sophisticated investing, by which time your nest egg will likely have grown and gained a momentum all its own.

While the core exposures should always represent a majority of any long-term investment portfolio, here are some asset types available through ETFs that typically aren’t represented in core portfolios:

There may also be segments of the investible universe already embedded within core portfolios that an investor might seek to increase their exposure to:

American investor Ray Dalio famously created an “all-weather portfolio” that he claimed would hold up in almost any market environment. It broke down like this: 30% U.S. stocks, 40% long-term treasury bonds, 15% intermediate bonds, 7.5% commodities, and 7.5% gold. Should you so choose, you could create a reasonable facsimile to the all-weather portfolio using ETFs.

Our MoneySense columnists have likewise illustrated how you can further diversify a core portfolio, reducing the risk of losses.

Here’s one such strategy, augmenting an asset-allocation fund with cash and/or gold bullion that would have held up well through past market downturns. And there’s another that adopts the buzzy 40/30/30 portfolio model that includes exposure to alternative assets along with stocks and bonds.

If you think you might be ready to take the next step beyond investing just in Canadian bonds and the major investible regions for equities, consider one of the advanced portfolios listed below. These are just suggested allocations that we believe won’t lead you too far astray. Feel free to tweak them to better suit your circumstances and build on them over time.

An important note: As your portfolio gets more complex, it will be harder to fill each allocation with index mutual funds and asset-allocation ETFs, which is why index ETFs are the go-to vehicle for building an advanced portfolio. We’ve suggested some funds, but with some 1,500 ETFs trading in Canada, know that there will be comparable competing products out there, possibly with lower fees or other attractive attributes.

Consider our fund picks suggestions only. For up-to-date ETF recommendations from the experts, check out MoneySense’s guide to the best ETFs in Canada, which we update every year in May.

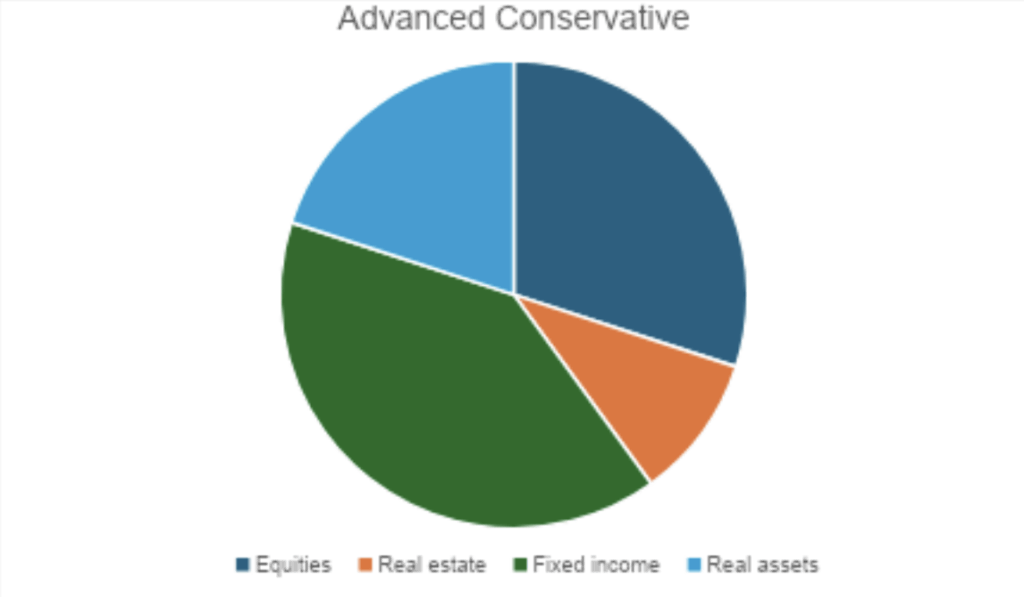

Equities: 30%

Real estate: 10%

Fixed income: 40%

Real assets: 20%

Equities: 50%

Real estate: 10%

[ad_2]

Michael McCullough

Source link

[ad_1]

But before we dive into these further, an important note. The following options are meant to illustrate sample portfolios and do not constitute financial advice. If you haven’t already done so, review the principles behind how to build a couch-potato portfolio and our overview of couch potato investing before committing your hard-earned money to any of the investments indicated.

Most Canadian banks offer a selection of relatively low-cost index mutual funds with which you can build your own balanced portfolio. Depending on your relationship with the institution, they may throw in advice for free.

TD is the best-known provider in this space with its e-Series funds, but Scotiabank, RBC, and CIBC, among others, have similar products.

The pie chart below illustrates how a typical mid-career investor with a moderate risk tolerance might construct a portfolio using e-Series funds. More conservative investors would typically increase the fixed-income allocation as high as 80%, while more growth-oriented investors might reduce the fixed income component to 20% or less.

Tangerine Bank, the online banking subsidiary of Scotiabank, lets you simplify the process further with a single, all-in-one product—similar to the asset-allocation ETFs described below but marketed as a mutual fund. You can find your choice of Tangerine Core Balanced Portfolio (60% stocks, 40% bonds), Core Balanced Income Portfolio (70% bonds, 30% stocks), Core Balanced Growth Portfolio (75% stocks, 25% bonds), Core Equity Growth Portfolio (100% global stocks), and Core Dividend Portfolio (100% dividend stocks), depending on your risk/return profile and investing style.

While cheaper than actively managed mutual funds, index mutual funds still tend to charge management expense ratios (MERs)—annual fees represented as a portion of your total account, deducted from your returns—that are higher than equivalent exchange-traded funds (ETFs). TD’s e-Series has MERs of 0.25% to 0.5%. Tangerine’s complete portfolios run just over 1%.

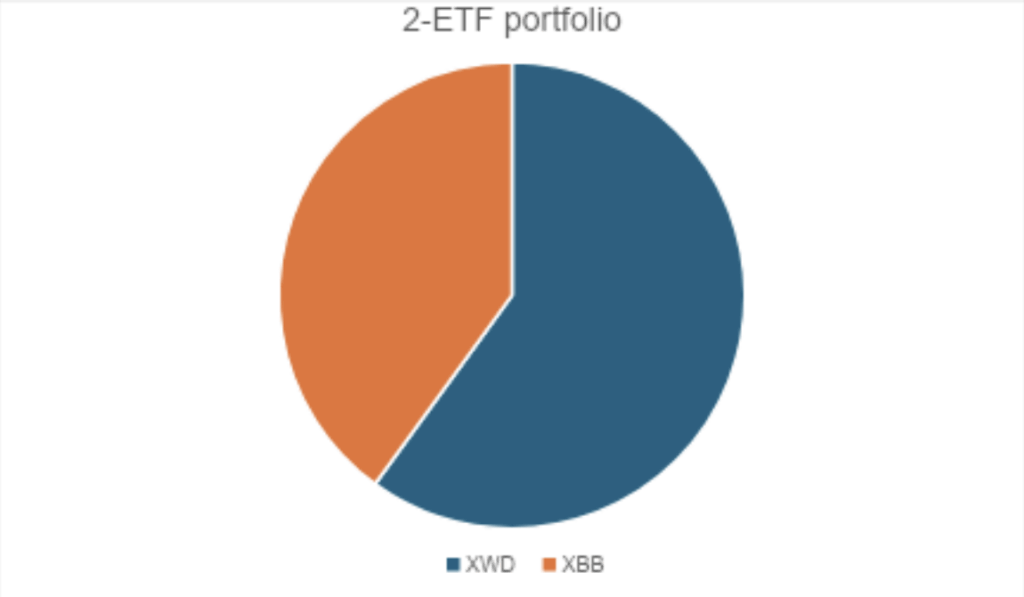

A core index ETF portfolio can consist of as little as two and up to four ETFs. Core exposures required include the U.S., Canadian, and International equities markets and domestic fixed income.

The sample portfolios here are balanced for moderate risk and return potential. More conservative and growth-oriented investors can adjust their portfolios to skew more towards fixed income or equities. See the section on asset-allocation ETFs below for examples.

The simplest approach is to buy a broad bond market fund such as iShares Core Canadian Universe Bond ETF (XBB) or Vanguard Canadian Aggregate Bond ETF (VAB) and a global equity ETF that takes in all geographies such as iShares MSCI World Index ETF (XWD). This will reduce your Canadian equity exposure to just 2% and raise your U.S. stock allocation to almost 40%—a good thing in some investors’ minds, bad in others’. Another potential downside is cost: global funds tend to have MERs of 0.2%, more than U.S. and Canadian equity funds.

We have used iShares funds in the example below, but there are comparable offerings from BMO, Vanguard, TD, and Global X. For specific fund recommendations, check out MoneySense’s annually updated guide to the best ETFs.

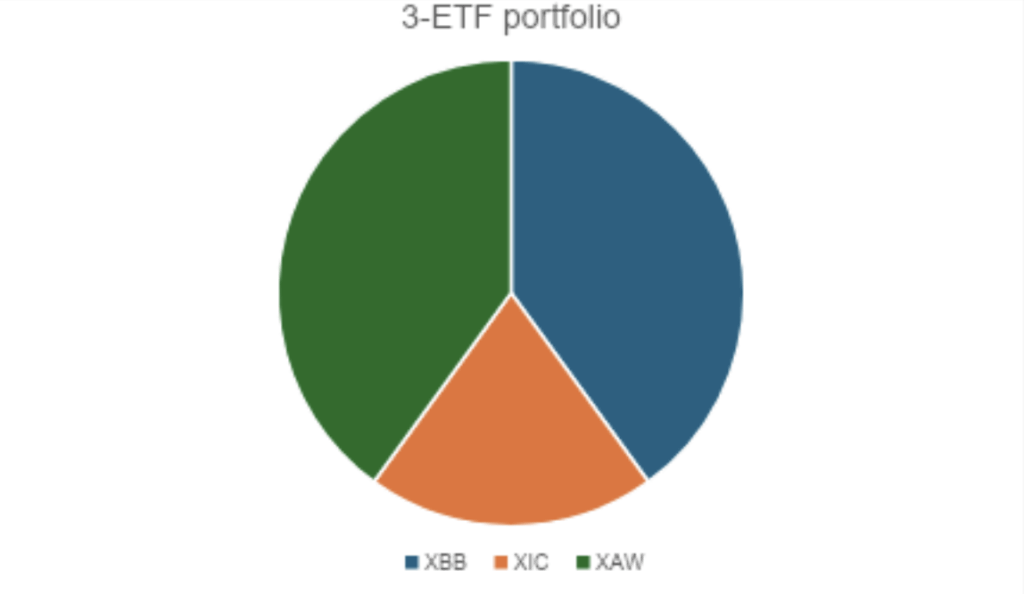

Option 2b (below) features three funds: fixed income, global equities excluding Canada, and Canadian equity. This lets you set your own preferred level of Canadian content, as well as enjoy low Canadian equity ETF fees and tax efficiency if the account is taxable.

For the Canadian equity portion, we have chosen iShares Core S&P/TSX Capped Composite Index ETF (XIC). You can find more good Canadian equity ETF options in our ETFs guide. For Global equity, we used iShares Core MSCI All Cap World ex-Canada Index ETF (XAW). Again, you can find equivalents from rival fund companies such as Vanguard and BMO.

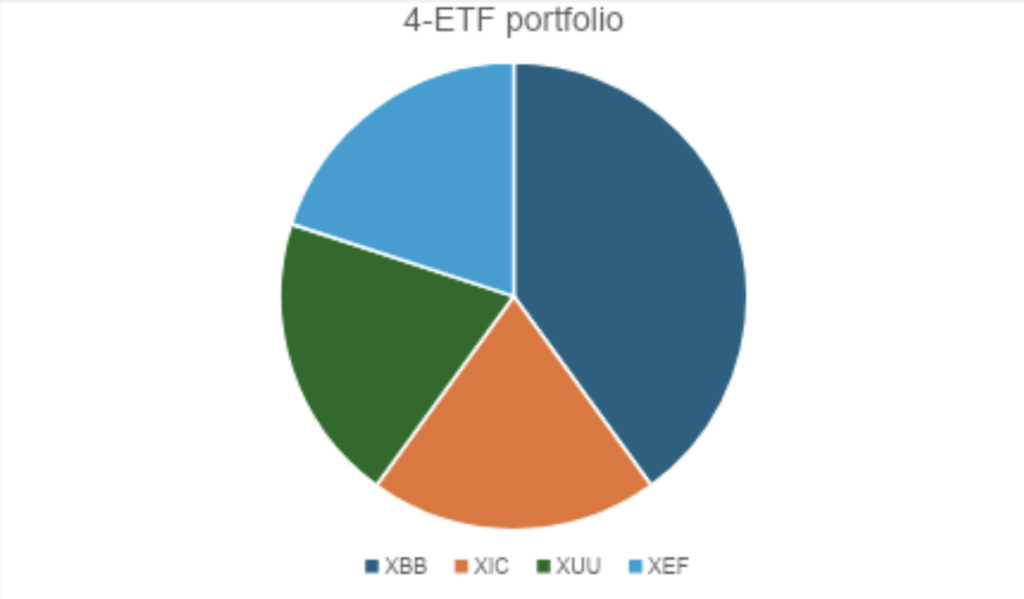

Option 2c takes in separate funds representing fixed income, U.S. equities, Canadian equities, and international equities (developed markets outside North America). The greater complexity brings with it potential cost savings, but also a greater need to monitor the portfolio and rebalance.

Along with XBB and XIC, we have sampled iShares Core S&P US Total Market Index ETF (XUU) and iShares Core MSCI EAFE IMI Index ETF (XEF). Find more suitable funds for these core positions in our most recent best U.S. Equity ETFs and best International Equity ETFs surveys.

Barring frequent trading that incurs brokerage fees, the index ETF portfolio is the lowest-cost approach available to couch-potato investors. Combined, your fixed income and equity allocations will have average MERs around 0.1% per year (slightly higher for international equity). You’ll barely notice it.

“Asset allocation ETF” is the term most often used in the investment industry, but they are variously known as one-ticket, all-in-one, one-decision and multi-asset ETFs. Essentially, they invest usually in the fund company’s own index ETFs to offer a whole portfolio’s worth of exposure in one investment. Just buy one, set your brokerage account preference to DRIP (dividend reinvestment program) so that quarterly distributions get invested in more units, and you really can “set it and forget it.”

There isn’t a lot to separate the major ETF providers in the asset-allocation space. The bigger decision you have to make is where you want to fall on the risk/return spectrum. The most conservative option, for money you might need in the next year or two, is not to use a multi-asset fund at all, but instead one invested in high interest savings accounts (HISAs) or the money market. (See MoneySense’s best cash alternative ETFs for suggestions.)

[ad_2]

Michael McCullough

Source link

[ad_1]

With Bay and Wall Streets trading in record territory, and certain high-flying stocks like Nvidia making headlines for their share price rallies, it’s tempting for investors—especially those who are just starting their investment journey and who might not have a lot of money to invest right off the bat—to want to jump in on the action.

But before the fear of missing out gets the best of you, experts advise taking a moment to ask why you want to invest in that company. “Many investors get caught in the hype,” said Ryan Gubic, certified financial planner and founder of MRG Wealth Management. “When you have high-performing or winning investments, they’ve already gone from potentially a low period to a high period,” he said, which means there could be a chance that the stock might plateau or trade lower going forward.

But investing goes beyond the fear of missing out on gains. It’s more about where an individual is in their financial journey, including their goals and time horizon, and tying that to their investment decisions, experts say.

Gubic said young investors need to consider their experience in investing and the amount of time they’re dedicating to market and economic analysis. He suggests they speak with a financial adviser to get more clarity on their goals, risk tolerance and needs that can be mapped out in a holistic financial plan.

If an investor isn’t doing their homework on what they’re actually investing in, Gubic said, stock picking can quickly turn into speculative betting. “Are you just chasing returns, or do you actually have a strategy and a process that you’re following?” he asked.

There are also risks to buying individual stocks when they’re trading in record territory. “What are you willing to lose, and how will that impact you over the next one, five, 10, and 30 years?” Gubic said. “Be really truthful with yourself: Are you doing speculative gambling or are you doing systematic investing?”

While friends may often talk about their investing wins, few openly discuss their losses, said Mia Karmelic, executive financial consultant at IG Wealth Management. “They don’t always talk about it when they’ve lost money,” she said. “I think it’s important to bring that perspective in too.”

While markets emerged from trade-related volatility earlier this year, the significant drops put many investors on edge. But the markets pulled through and have since delivered several new highs in the months that followed.

“Pullbacks are normal and they happen each year,” Karmelic said. “Markets recover and go on to hit new highs.”

She said investors shouldn’t be hyper-fixated on where markets or individual stocks are at, but focus on growing money in the long run. “I suggest investing in a diversified portfolio—ETFs, mutual funds—rather than individual stocks when there isn’t a large amount of savings to be invested,” she said.

Young investors typically start off with a smaller amount of money and sometimes, they might take on more risk in search of returns.

“It’s really hard to diversify into an individual stock portfolio when there isn’t a substantial amount of money being invested,” Karmelic said. Instead, she recommends investing on a regular basis. “Average yourself into the markets, capture those different prices, and over the long term, you will do very well,” she said.

But that doesn’t mean putting your money to work in a stock that’s trading at an all-time high is out of the question. “There’s certainly space for some of those stocks that are at all-time highs because chances are they can continue to hit new highs,” said Karmelic.

But it’s important to protect your portfolio from significant volatility, she said.

“It’s important to invest in a portfolio of stocks that are diversified, that are not just in a specific industry, in a specific country,” Karmelic said. “I think investors will definitely feel the volatility more if they’re only exposed to three or four individual companies,” Karmelic said.

Even then, if an investor has their heart set on a high-flying stock, it should only make up a small percentage of their portfolio. “When I look at a lot of my clients, an individual public equity holding might be around a one to 2% weight, sometimes a little less,” Gubic said.

[ad_2]

The Canadian Press

Source link

[ad_1]

2025 has been the year of “hard assets,” including gold and bitcoin (BTC), the latter often dubbed “digital gold.” As monetary policy eased, investors rotated into these inflation-hedging assets.

But that’s not the whole story. If you were laser-focused on gold and BTC this year, you may have missed two even stronger performers: silver and ethereum (ETH). As gold and BTC cooled in recent months, silver and ETH stole the spotlight.

The chart below compares the year-to-date price appreciation of these four assets. It’s clear that while ETH lagged the others until April, it’s since shot up to overtake them.

While gold and BTC get most of the press and the spotlight, it’s not surprising that the second-largest assets in their respective asset classes (precious metals and crypto) have outperformed this year. In fact, in an earlier edition of this column, I’d written that based on earlier crypto market patterns, ETH could well outperform BTC in 2025—and so far, that’s been the case.

In my previous column, I’d written that it would be reasonable to expect BTC to possibly hit $160,000 (all figures in U.S. dollars unless otherwise specified). Other major Wall Street analysts, including Citigroup and FundStrat’s Tom Lee, have suggested that BTC could reach about $200,000 or more before this bull market is over. So, what does that mean for ETH?

If past cycles are any guide, this crypto bull market could still have legs.

ETH is currently trading at $4,496, but a move to $8,000 wouldn’t be unreasonable. That would represent a 64% gain from today and would still be less than 2x its previous all-time high of $4,878 (set in November 2021). In every prior bull market since ETH’s launch in 2015, it has set a new all time high with gains of at least 270% from the previous one. An approximately 100% gain from its last peak would actually be relatively conservative.

We’ve ranked the best crypto exchanges in Canada.

ETH ETFs did for ethereum in 2025 what BTC ETFs did for BTC in 2024: provided the legitimacy and means for institutions and other large investors to allocate a percentage of their capital to ETH without exposing themselves to the risks associated with direct exposure to the cryptocurrency itself.

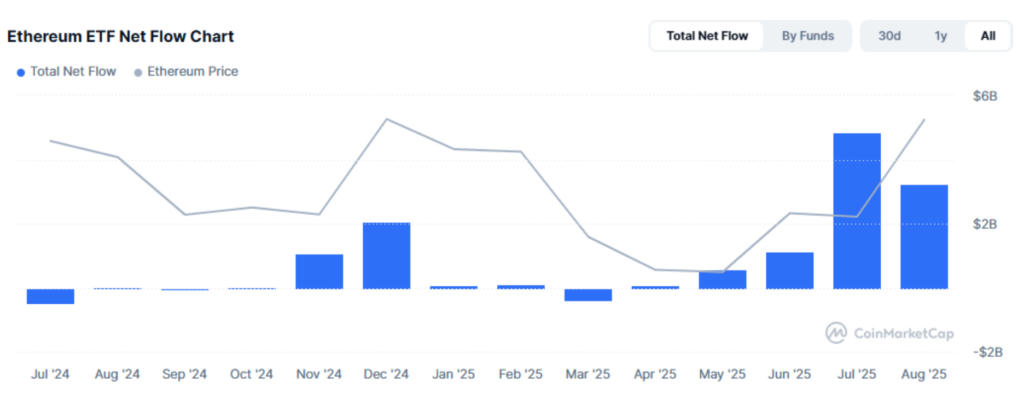

The chart below clearly shows how inflows to ETH ETFs picked up in April-May 2025—coinciding with the beginning of ETH’s 2025 bull run. July and August were bumper months for ETH ETFs with net inflows of $4.86 billion and $3.23 billion, respectively.

Canadian investors who’re bullish on ETH are spoiled for choice with regard to ETH ETFs. These ETFs are attractive to investors because they can be held in registered accounts like tax-free savings accounts (TFSAs), registered retirement savings plans (RRSPs), first home savings accounts (FHSAs), and others.

Learn more: How to invest tax-free in a bitcoin ETF

After the success of Strategy (MSTR), Michael Saylor’s Nasdaq-listed BTC treasury company, a new class of ETH-focused treasury companies have emerged. These companies follow a similar playbook to MSTR: holding a significant portion of their corporate reserves in ETH, aiming to accumulate more over time through both price appreciation and staking rewards.

Ethereum staking involves locking up ETH to help secure the network and validate transactions. In return, stakers earn additional ETH—somewhat like dividends in traditional equity investing.

Here’s a comparison of the two most prominent ETH treasury companies currently trading on public markets that Canadian investors can buy:

So, should you invest in an ETH treasury company? It’s still far too early to tell how this new category of ETH-focused treasury companies will perform. Both BMNR and SBET only announced their treasury strategies in June or July 2025—that’s hardly enough time for meaningful price discovery. Most individual investors in Canada may want to stick to ETH itself or to ETH ETFs, of which Canada has many to offer.

[ad_2]

Aditya Nain

Source link

[ad_1]

The bank says it earned a net income of $2.33 billion or $3.14 per diluted share for the quarter which ended July 31. The result for the quarter compared with a profit of $1.87 billion or $2.48 per diluted share in the same quarter last year.

Revenue for the quarter totalled $8.99 billion in the quarter, up from $8.19 billion a year earlier.

BMO’s provision for credit losses amounted to $797 million for the quarter, compared with $906 million a year earlier.

On an adjusted basis, BMO says it earned $3.23 per diluted share in its latest quarter, up from an adjusted profit of $2.64 a year earlier.

The average analyst estimate had been for earnings of $2.95 per share, according to LSEG Data & Analytics.

“BMO delivered another quarter of strong earnings growth, with solid revenue performance and good expense management,” BMO chief executive Darryl White said in a statement.

“We continue to invest to drive sustainable growth across our businesses, including our recently announced acquisition of Burgundy Asset Management Ltd., adding talent and advancing digital and AI capabilities to deliver a differentiated client experience.”

The bank said its Canadian personal and commercial banking business earned $867 million in its latest quarter, down from $914 million a year ago, as higher revenue was more than offset by higher expenses and a higher provision for credit losses for the quarter.

In the U.S., BMO said its personal and commercial banking business earned $709 million, up from $470 million in the same quarter last year.

The bank said its wealth management business earned $436 million, up from $362 million a year ago, while BMO’s capital markets business earned $438 million, up from $389 million in the same quarter last year.

BMO’s corporate services group reported a net loss of $120 million, compared with reported net loss of $270 million a year earlier.

Numbers for its third quarter of 2025 (all figures in USD).

The Bank of Nova Scotia reported a third-quarter profit of $2.53 billion, up from $1.91 billion a year ago.

The bank says the profit amounted to $1.84 per diluted share for the quarter ended July 31, up from $1.41 per diluted share in the same period a year ago.

Revenue totalled $9.49 billion for the quarter, up from $8.36 billion in the same quarter last year.

Scotiabank’s provision for credit losses for the quarter amounted to $1.04 billion, down from $1.05 billion a year earlier.

[ad_2]

The Canadian Press

Source link

[ad_1]

The results announced Wednesday were hotly anticipated because Nvidia has emerged as key barometer of a two-year-old AI boom that has been propelling the stock market to new heights. The Silicon Valley chipmaker also became the first publicly traded company to achieve a $4 trillion market value. (All figures in U.S. dollars.)

In recent weeks, though, research reports and comments by prominent tech executives have raised investor fears that the AI mania has been overblown.

And now Nvidia’s latest numbers covering the May-July period may feed those perceptions because the sales of the company’s processors—indispensable components in the AI data centres being built around the world—aren’t growing as robustly as they once were. The late 2022 release of OpenAI’s ChatGPT unleashed a technological phenomenon that is starting to reshape society.

The AI chips are part of Nvidia’s data centre division, which posted revenue of $41.1 billion, a 56% increase from the same time last year, but below the analyst forecast of $41.3 billion, according to FactSet Research. Even so, Nvidia’s profit of $26.4 billion, or $1.08 per share, was higher than analysts predicted, as was its total revenue of $46.7 billion—also a 56% increase from the last year.

Nvidia signalled it believes more good things are still to come by forecasting revenue of $54 billion for the August–October period, slightly above what analysts had been envisioning for the quarter. “We are in the beginning of the buildout,” Nvidia CEO Jensen Huang told analysts during a Wednesday conference call in which the company predicted another $3 trillion to $4 trillion will be spent on AI initiatives by the end of this decade.

But Nvidia’s stock still slipped 3% in extended trading after the fiscal second quarter report came out, indicating the performance wasn’t enough to allay investors’ fears. A letdown was almost inevitable, given the stock price has increased by more than 10-fold during the past two and a half years.

“Saying the stock was priced for perfection would be an enormous understatement,” said Investing.com analyst Thomas Monteiro.

Delivering the kind of growth to push Nvidia toward a $5 trillion market value has become more daunting as Nvidia’s annual sales have ballooned from $44 billion in its fiscal 2024 to a projected $204 billion in the company’s current fiscal year that ends in January. That has translated into progressively slower rates of year-over-year revenue growth. After Nvidia’s revenue at least doubled or tripled from the previous year in five consecutive quarters during 2023 and 2024, the growth has been tapering off the past four quarters.

Nvidia would have fared better in the most recent quarter if President Donald Trump hadn’t imposed a ban that prevented Nvidia from selling its AI chips in China during the quarter. But investors had already been forewarned the restrictions would cost the company about $8 billion in sales from May through July, so that challenge was already in reflected in Nvidia’s stock price.

Trump took the China handcuffs off of Nvidia earlier this month in return for a 15% cut of the company’s sales in that country—a compromise that is expected to help boost revenue during the upcoming months although it’s unclear how quickly that will happen. In the best case scenario, Nvidia may be able to bring in $2 billion to $5 billion in AI chip sales to China, according to Colette Kress, the company’s chief financial officer.

While the technology industry has been the biggest beneficiary of the AI frenzy, it’s also been a boon for the overall stock market. The benchmark S&P 500 has gained 69% since the end of 2022, with AI fervour fuelling much of the investor optimism.

But even amid the general euphoria, there recently have been murmurs about whether AI mania will prove to be an echo of the late 1990s dot-com boom and meltdown that plunged Silicon Valley into a funk that lasted several years.

[ad_2]

The Associated Press

Source link

[ad_1]

As a starting point, I like to look at the big picture to see where you are headed. This involves modelling all your current and future financial resources, including your cash flow and the activity in your holding company. This provides a clear picture of what you have today and gives you a general sense of your asset growth or decline over time, future annual and final taxes, and estate values. With that backdrop you can experiment to see which options are available to you and which ones you want to act on, in terms of spending, lifestyle, gifting, and leaving a bequest.

With that background, which I refer to as lifestyle planning, financial planning begins, and this is the nature of your question. From the tax side it is about understanding what tax credits and deductions are available to you, and how to take advantage of them in a way that aligns with your personal values, beliefs, and lifestyle.

You will also need to understand how your individual investments are taxed in your non-registered and registered accounts and your holding company. You also need to be aware of the three different dividend options you have when drawing from your holdco, and the impact that investment tax and dividends have on tax credits and benefits. Old Age Security (OAS) is a good example of a benefit that begins to be clawed back once your income exceeds about $93,500.

I suspect through experience you are aware of the things I have discussed so far and some of the planning solutions you can use to reduce the tax owing such as pension splitting, donating shares to charity, and tax-free savings account (TFSA) contributions. Rather than rehash those strategies, I will briefly touch on a few others you may not be so familiar with, such as a donor-advised fund, immediate flow-through shares, insurance and investment selection.

You are already donating to charity, but have you ever thought of setting up a donor-advised fund (DAF)? You can add as much money as you like to the fund, in your case maybe $200,000 of your non-registered money. Once it is there, you can manage the money your way and the investment will grow tax-free, so you are not paying tax on the distributions. When you make the deposit, you can claim the charitable tax credit all at once or defer it over five years. It is also at your discretion when you give money to the charities of your choice from the DAF. One catch is you can’t change your mind and take the money back once it is in the DAF.

Have you heard of flow-through shares with an immediate liquidity provider? You buy the shares and then immediately sell them to a waiting buyer for less than what you paid. It is the tax credit that makes this work. Ottawa-based planning firm WCPD provides the following simple explanation of how this can work both personally, making a charitable contribution, or a combination for a person with a marginal tax rate of 50%.

You pay $1.50 for a flow-through share and immediately sell it for $1. The flow-through tax credit and deduction will save you $0.75 in tax which, when combined with the $1 you sold the share for, puts you up $0.25. If you want to make a charitable contribution, you could donate the $1 you sold the share for and get a tax savings of $0.50. With the combined tax savings of $1.25 ($0.75 + $0.50), your charitable contribution will only cost you $0.25, rather than $0.50 if you didn’t purchase a flow-through share. WCPD also provides a strategy where you go two parts personal and one part charity, resulting in a zero-cost way to donate to charity.

As mentioned, this is a very simplified example, and you will want to talk to a professional before doing this on your own.

A second-to-die permanent life insurance policy held in your holding company is another tax-saving strategy. Money invested within the policy grows virtually tax-free, and when it pays out, a capital dividend account (CDA) is created equal to or almost equal to the full value of the death benefit. You are then able to pay a tax-free dividend equal to the CDA out of the holdco. While you own the policy, there may be other ways to use the policy, such as borrowing for tax-free income or investing. Have you had a discussion with your accountant about the wind-up of your holdco on your deaths, i.e, the tax, time, and fees? Insurance may ease some of those issues.

Finally, and probably more familiar, have you thought about how your investment approach is affecting your annual tax? I have the impression you are a successful DIY dividend investor. You are receiving taxable dividends each quarter and possibly buying and selling stocks, subjecting you to capital gains and higher corporate accounting fees. For your non-registered and corporate accounts, consider a long-term, buy-and-hold portfolio made up of simple low-cost index ETFs that will be more tax-efficient.

Mike, there is probably a lot you can do to make things more tax-efficient. It is something you should look at on an annual basis as your spending and income will likely change from year to year.

[ad_2]

Allan Norman, MSc, CFP, CIM

Source link