Budgets are a great tool to help you stay on track with your spending and savings goals, but they need regular updates to maximize their effectiveness. Hopefully, you’ve recorded any changes to your income, expenses, or money objectives throughout the year. If not, now is the time to do a deep update and analyze your progress.

If you find evidence of impulse spending, it’s time to make some adjustments. For example, rather than keeping all of your income in an instant-access chequing or savings account, you could tuck some away in an account like EQ Bank’s high-interest no-fee Notice Savings Account. In exchange for giving advance notice of a withdrawal (10 or 30 days), you get a higher interest rate. It’s a win-win for spur-of-the-moment shoppers who want to hold some of their money at arm’s length.

sponsored

EQ Bank Notice Savings Account

go to site

Monthly fee: $0

Interest rates: 2.60% for 10-day notice, 2.75% for 30-day notice. Read full details on the EQ Bank website.

Minimum balance: n/a

Eligible for CDIC coverage: Yes

go to site

2. Simplify your money management

If you think managing your own spending and saving is a challenge, try doing it with others! For some people—like couples, family members, or even roommates—budgeting can be complicated by shared expenses or joint savings goals. That’s where a joint bank account can make a huge difference.

When you open a joint account, all account holders (you and up to three other people) can deposit, withdraw, and save in the same account. Rather than trying to bookkeep separately, everything is in one place. Make easier money management part of your financial resolutions. Pro-tip: Consider a no-monthly-fee, high-interest bank account like EQ Bank’s Joint Account to keep your money growing.

3. Top-up your retirement funds and get a tax break

Registered retirement savings plans (RRSPs) let you save for retirement in a tax-advantaged account, meaning that every dollar you put away can reduce your taxable income for the following year. Every year, you have a certain amount of contribution room for your RRSP and unused room rolls over into subsequent years.

Taxes on your RRSP savings are only due once you withdraw. The idea is that you will be retired at that point, so your tax rate will be lower than during your working years.

Although the last day to contribute to your RRSP is in March, many Canadians strive to top up earlier. Not only does this give your savings more time to accumulate interest, but it also ensures that your retirement savings don’t end up inadvertently going to holiday expenses.

4. If you need it, consider making a withdrawal from your tax-free savings account (TFSA) before Dec. 31

Similar to the RRSP, a tax-free savings account (TFSA) is a tax-advantaged registered savings account with a certain amount of contribution room added annually. The difference is that when you put money into a TFSA, you don’t get a tax-break on your income tax. Instead, any gains you earn are yours, tax-free.

Article Continues Below Advertisement

The annual deadline for TFSA deposits is December 31, and on January 1, you get your new contribution room. What you may not know is that when you withdraw funds from your TFSA, the amount you withdraw is added back to your contribution room the following calendar year.

So, if you anticipate needing money soon but still want to make use of your full contribution room next year, making a withdrawal before December 31 is a good time to do it because you’ll get that room back quickly.

sponsored

EQ Bank TFSA Savings Account

GO TO SITE

Interest rate: Earn 1.50% on your cash savings. Read full details on the EQ Bank website.

Minimum balance: n/a

Fees: n/a

Eligible for CDIC coverage: Yes, for deposits

GO TO SITE

5. Capitalize on saving for a home

A first home savings account (FHSA) is a tax-advantaged investment that works in a similar way to an RRSP in that the money you deposit can reduce the amount of your taxable income. And, similar to a TFSA, the money you withdraw is tax-free. Each year’s unused contribution room rolls over to the next year, so if you’ve never contributed but open one now, you could deposit up to $16,000 per person (or double that, for a couple) in 2026.

Unlike a TFSA or RRSP, you won’t begin accumulating contribution room until you open the FHSA. So, if you don’t have an FHSA but intend to open one, doing so before Dec. 31 can give you an extra year of contribution room in 2025.

On the other hand, if you have some extra cash (perhaps a year-end bonus!) to allocate to savings, contributing to your existing account by the December 31 deadline can reduce your taxable income for 2025.

Get started on a new year’s financial plan

Year-end is a great time to review your financial health. By choosing the right banking products and making smart investment decisions, you can build momentum toward lasting security and success.

Get free MoneySense financial tips, news & advice in your inbox.

Financial planner Robb Engen recently tackled this puzzle in his Boomer & Echo blog, “Why Canadians avoid one of retirement’s most misunderstood tools.” Engen notes that experts like Finance professor Moshe Milevsky and retired actuary Fred Vettese believe “converting a portion of your savings into guaranteed lifetime income is one of the smartest and most efficient ways to reduce retirement risk.” Vettese has said the math behind an annuity is “pretty compelling,” especially for those without Defined Benefit pensions.

Milevsky and Alexandra Macqueen coined a great term applicable to annuities when they titled their book about the subject Pensionize Your Nest Egg, which I reviewed in the Financial Post in 2010 under the title ”A cure for pension envy?”

Engen observes that a life annuity is “the cleanest version of longevity insurance … You hand over a lump sum to an insurer, and they guarantee you monthly income for life. If you live to 100, the insurer pays you. If stock markets collapse, you still get paid. If you’re 87 and never want to look at a portfolio again, the income keeps flowing.”

In other words, annuities neutralize the two big risks that haunt retirees: longevity risk (the chance of outliving your money) and sequence-of-returns risk, the danger of suffering a stock-market meltdown early in retirement and inflicting irreversible damage on a portfolio.

Despite all the seeming positives about annuities, Engen notes that “almost nobody buys one.” He cites a Vettese estimate that only about 5% of those who could buy an annuity actually do so. Engen suggests there is a behavioural hurdle: fear of losing liquidity and control of the underlying assets. He cites research by the National Institute of Ageing’s Bonnie-Jeanne MacDonald on pooled-risk retirement income, where she wrote that such retirees are “strongly opposed to voluntary annuities, as they want to keep control over their savings.”

Compare the best RRSP rates in Canada

A chance to lock in recent portfolio gains?

Even so, the new Retirement Club created by former Tangerine advisor Dale Roberts earlier this year (see the blog posted on my own site in June) recently featured a guest speaker who extolled the virtues of annuities: Phil Barker of online annuities firm Life Annuities.com Inc.

Barker said many clients tell him they’ve done really well in the markets over the last 20 years and now they’d like to lock in some of those gains. They may be looking for fixed-income strategies, and many were delighted with GIC returns when they were a bit higher than they are now (some in the range of 6-7%). But they are less happy with the new rates on GICs now reaching maturity. Meanwhile, annuities have just come off a 20-year high in November 2023 so the time to consider one has never been better, Barker told the Club in August.

With annuities, you can lock in a rate for the rest of your life—so if your timing is good, it may make sense to allocate some funds to them.

Barker said eight life insurance companies offer annuities in Canada: Desjardins, RBC Life Insurance, BMO Life Insurance, Canada Life, Manulife, Sun Life, Equitable Life and Empire Life. All are covered under Assuris, a third-party organization that guarantees 100% of an annuity up to $5,000 per month. So if one of those companies failed, the annuity would be honored by one of the other firms via Assuris.

Barker described an annuity as simply a “personal-funded pension.” To set one up you can take registered or non-registered funds and send the capital to an insurance company. In return, they give you an income stream for as long as you live: this is the traditional life annuity. Unlike annuities in the U.S., you cannot add funds to an existing annuity, Barker told the club, nor can you co-mingle funds from for example RRSPs and non-registered funds.

However, you can buy a new annuity each time you need to. There is no medical underwriting for annuities, unlike life insurance. Joint annuities for couples are a great value, he said, but the tax slips are sent to the primary annuitant. Nor is income splitting possible under current CRA rules.

When annuities shine

Annuities shine when you are confident about your health and prospects for living a long time. Having $X,000 a month assured income to live on means your other sources of income that fluctuate with stock markets can be weathered, Barker said. “We’re seeing people getting 6.5% to 8.5% a year for the rest of their lives, depending on their age.”

As Dale Roberts commented during Barker’s talk, having enough to live on just from the pension bucket (annuities, pensions, CPP/OAS etc.) frees you up to take some risk in other areas, like stocks and equity ETFs.

Funding by registered vs. non-registered accounts

Registered funds transfer to an annuity tax-free; that’s because money is not being deregistered, but rather going from one registered environment into another registered environment. It will be fully taxed when it comes out. The monthly income from the annuity is then fully taxable in the year it is received.

If you fund with non-registered money, the taxation is considerably different. For one, if your non-registered account has unrealized capital gains you’ll have to realize them and pay tax on them. Other than that, so-called prescribed annuities are relatively tax-efficient. The capital that is used to fund the annuity is not taxed, only the gain is, Barker says. “Therefore, the taxable portion of the annuity income is a very small amount. Prescribed means that the taxation is the same or level for the entire life of the annuity.”

The Club has also covered other retirement income products that may resemble annuities in some respects: the Vanguard Retirement Income Fund (VRIF) and the Purpose Longevity Fund, both of which I have small chunks in. Dale adds that the Longevity Fund has the potential to be a “nice complement to annuities,” as it “is designed to increase payments quite nicely in the later years thanks to the mortality credits. Those with very long lives are subsidized by those who pass away much earlier.”

The tech sector has seen significant volatility recently, as speculation mounts on whether there’s an AI bubble percolating after a major rally. For young investors looking for a piece of the action, experts say with the right strategy, it’s possible to participate without risking it all.

Align AI investing with risk tolerance and goals

Dhanji said he usually begins with the basics—assessing his client’s risk profile and financial goals. “Not everyone can tolerate the risks of AI companies because they are more volatile,” Dhanji said.

Investing in AI no longer has to mean owning shares of big-name tech companies. Nvidia, Meta Platforms, and AMD, among others, have been seen as proxies for the AI sector in recent years, but they are not the only options. Companies across the board have now bet huge sums of money on AI and its productivity promises.

If the client’s goals are long-term, such as retirement savings, then having some AI exposure in their portfolio can complement other asset classes, Dhanji said. The volatility of AI stocks makes them unsuitable for short-term financial goals. For example, if you’re saving money to start a business or buy a house, it’s better to keep AI stocks out of the mix.

Another risk, he said, is that technology is evolving so quickly that what you own today may be outdated in a year’s time. “You have to be careful in terms of what you’re investing in,” Dhanji said.

Balanced approach recommended for investing in AI stocks

Most investors Ryan Lee hears from are aware of the volatility, but they want to buy in anyway. Lee, a certified financial planner and founder of Twain Financial, said picking individual AI stocks to invest in can be an “overly risky” move. He also said it’s important to keep in mind how those AI stocks fit in your long-term investment strategy.

Certain index funds in your portfolio might already have exposure to AI companies—such as an exchange-traded fund (ETF) that tracks the Nasdaq. “When you hold a diversified portfolio, you already have exposure,” he said.

Lee said it’s difficult nowadays to ignore AI stocks. “There is AI in the future … and there is going to be growth,” Lee said. “But we just don’t know when that growth is going to happen or whether or not that growth is going to be higher than other industries.”

Article Continues Below Advertisement

Instead of picking individual stocks, some investors might look to AI-centric ETFs, but Dhanji warned against over-concentration. If a young investor has a long-term time horizon, Dhanji recommends 10% to 15% of their portfolio can be allocated to the AI sector. But if the investor is more conservative, Dhanji suggested capping their AI exposure to 5% of the portfolio—or not holding any AI ETFs or stocks at all if that money will be needed in the next three years or so.

Whatever the financial goal and time horizon may be, Dhanji recommended shying away from AI names that are buzzy social media recommendations. “My advice is to avoid the hype train,” Dhanji said. “I’d rather people focus on the companies themselves, making sure they have strong balance sheets and cash flows.”

Dhanji said investing in quality companies with strong balance sheets will help your portfolio weather extreme fluctuations in the market long term, if the AI bubble were to burst. “My recommendation is to have that financial plan in place, know what your cash flows look like, and instead of investing a lump sum all at once and timing the market, you can then dollar average into the market over time,” he said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Users can make transactions, save, and earn rewards on their stablecoins without the volatility often associated with cryptocurrencies. Some experts even believe that stablecoins and other crypto technologies could compete with, and eventually even displace, today’s traditional payment systems.

Cryptocurrency exchanges allow users to make faster payments, pay low fees, and have better access to financial tools. For example, Coinbase has partnered with Shopify to accept USDC payments on select Shopify stores, giving users a convenient payment option that doesn’t rely on traditional banking networks.

Inside Coinbase’s USDC Rewards (and why it could be a game changer)

Coinbase’s USDC Rewards show how finance is shifting to put consumers first. The platform focuses on customer success, using technology to help Canadians grow and manage their money.

featured

Coinbase

go to site

Account minimum: $1

Trading fees: 0% – 2% per transaction. Varies by transaction amount and type (Simple, Advanced)

Welcome offer: None at this time

go to site

Here’s how it works: you earn 3.85% uncapped rewards* on your daily USDC balance, and the rewards you earn are deposited at the end of the week. Coinbase One members earn 4.25% automatically on their USDC holdings.

With USDC Rewards, you can enjoy more control over your money while being rewarded for your participation.

Higher potential returns come with risks. Stablecoins aren’t covered by CDIC insurance, which means your money isn’t protected like it is in a traditional bank account. The GENIUS Act provides a framework for U.S. financial regulation, and USDC already meets many existing crypto rules—but some risks remain.

If you prefer to play it safe, spreading your money across different accounts or investments can reduce risk. For others, USDC Rewards offers the chance to earn more than a regular savings account and be rewarded for your loyalty. You’ll also have full access to your funds, so you can sell, send, or convert stablecoins anytime without lock-ups.

The bottom line

For Canadians frustrated with low-yield savings accounts, Coinbase’s USDC Rewards program offers a compelling alternative. By paying rewards on USDC, it helps you earn competitive returns while keeping your money accessible—something that’s hard to find with traditional banks.

The chart below compares total returns, which measure both price appreciation and reinvested dividends, across major Canadian and U.S. equity benchmarks since 2016.

While the S&P 500 and S&P/TSX 60 have surged higher, Canadian real estate investment trusts (REITs) have badly lagged. The gap hasn’t narrowed meaningfully either. Even with distributions reinvested, the S&P/TSX Capped REIT Index remains well below its pre-COVID highs, with little evidence of a sustained rebound.

I’m not a value investor by nature, nor a sector picker, but divergences like this give me pause. Canadian REITs may quietly represent one of the few asset classes that aren’t overvalued today—and could offer genuine recovery potential in the years ahead, especially as interest rates fall.

The irony is that many Canadians still see real estate as the path to financial independence after decades of soaring home prices, even with the recent downturn in major cities like Toronto. Yet few consider REITs, which do the same thing at scale, with diversification and liquidity that private property ownership can’t match, especially when packaged into an exchange-traded fund (ETF).

The ABCs of Canadian REIT investing

REITs have their own nuances that make them very different from regular stocks. You can’t analyze them using the same metrics you’d apply to a company like Dollarama. That’s because REITs are pass-through vehicles: they’re exempt from paying corporate income tax as long as they distribute most of their taxable income to unitholders.

Unlike operating companies that make money by selling products or services, REITs earn revenue primarily from rent. They own portfolios of income-producing real estate and pass that rental income on to investors through distributions, which are usually paid monthly and tend to be higher than the average dividend yield from stocks in other sectors.

Canadian REITs span a variety of sub-sectors, including:

Office: properties leased to businesses and professional firms

Retail: shopping centers and standalone stores

Residential: apartment complexes and multi-family housing

Industrial: warehouses, logistics hubs, and distribution centers

Diversified: a mix of several categories above

Because of how REITs operate, you can’t value them using conventional measures like earnings per share (EPS) or price-to-earnings (P/E) ratios. In fact, those figures can be misleading on sites like Yahoo Finance or Google Finance. That’s because REITs use significant non-cash charges such as depreciation, which can artificially depress reported earnings even when cash flow is strong.

Article Continues Below Advertisement

The key metric for REITs is funds from operations (FFO). FFO adjusts net income by adding back depreciation and amortization (which are non-cash expenses) and subtracting any gains or losses from property sales. In simple terms, FFO is a more accurate measure of a REIT’s true cash-generating ability.

Once you know the FFO, you can calculate price-to-FFO, the REIT equivalent of a price-to-earnings ratio. It tells you how expensive a REIT is relative to its cash flow. Comparing a REIT’s price-to-FFO to its own historical average and to peers within the same subsector (e.g., residential vs. residential) gives a much fairer sense of value.

FFO is also used to judge whether a REIT’s distribution is sustainable. Since REITs pay out most of their income, the payout ratio is typically based on the percentage of FFO, not earnings. A lower payout ratio suggests more cushion to maintain distributions through economic downturns.

Supporting FFO is the occupancy rate, which measures how much of a REIT’s property portfolio is currently leased. It’s usually reported quarterly and varies by sector. As of late 2025, occupancy remains strongest in residential REITs, driven by housing demand, while office REITs continue to face pressure from remote work trends. Generally, you want to see occupancy of 95% or higher.

Another useful valuation tool is net asset value (NAV) per unit, which estimates the fair value of a REIT’s underlying real estate after liabilities. NAV divides the total appraised property value minus debt by the number of outstanding share units. The market price of a REIT can trade at a premium or discount to NAV—there’s no guarantee it will converge—but it’s still a good reality check for whether a REIT looks undervalued.

The best place to find these figures is in a REIT’s quarterly reports and audited financial filings. Some data providers, like ALREITs, compile these metrics for most Canadian-listed REITs.

Personally, I prefer REIT ETFs over picking individual REITs. Valuing REITs properly requires a working knowledge of specialized metrics. And while each REIT is diversified internally, most still focus on one property type or region. A REIT ETF spreads that exposure across multiple sectors and issuers, averaging out risks and simplifying portfolio management.

In Canada, REIT ETFs generally fall into two camps: passive index trackers and actively managed funds. Each has its strengths, and I’ll walk through some of the more notable examples in both categories, along with their pros and cons.

Berkshire Hathaway’s third-quarter earnings report on Saturday revealed Warren Buffett continued to sell more stocks than he bought with the legendary investor poised to step down as CEO by year’s end.

The conglomerate sold $12.5 billion of stock in the latest period and bought $6.4 billion, marking the 12th consecutive quarter of net selling. More details on specific stocks will come in a separate regulatory filing later this month.

Meanwhile, Berkshire’s cash hoard swelled to a fresh record high of $382 billion as operating earnings jumped 34% while Buffett held off on buying back stock for the fifth straight quarter.

As the company’s stock portfolio has shrunk, money has been shifting into Treasury debt. But with short-term rates falling recently, Berkshire’s third-quarter net investment income dropped 13% to $3.2 billion.

The cautious stance on stock investing began in 2022, when the Federal Reserve launched its most aggressive rate-hiking campaign in more than 40 years to rein in inflation.

That tightening slammed stock valuations, but apparently not enough to trigger Buffett’s bargain-hunting instincts. The Fed’s subsequent pivot to rate cuts later sparked a rally that sent stocks to new highs.

More recently, the massive market selloff in April, after President Donald Trump unveiled his shocking tariffs, also didn’t get Buffett off the sidelines. In the second quarter, Berkshire sold $3 billion in stocks on net.

Markets quickly bounced back and set new highs just months later with AI-related companies leading the charge. By contrast, Berkshire Hathaway shares have lost 12% since May, when Buffett announced that he will step down as CEO by the end of the year and hand over the role to Greg Abel.

While Buffett is expected to stay on as chairman, he may be staying away from dramatic moves to clear the decks for Abel, who had already been taking on a bigger leadership role before May.

The Oct. 2 acquisition, Berkshire’s largest since buying insurer Alleghany in 2022, was the first-ever Berkshire announcement that quoted Abel and didn’t mention the current chief executive by name.

“It’s genius. It’s certainly a win-plus for Berkshire because it also helps the company that they own 30% of,” Doug Leggate, Wolfe Research energy analyst, told Fortune last month. “It’s completely self-serving, it’s logical, and—not in any nefarious way—definitely helpful.”

It was August 2023, and Matt Swain had five offers on the table for Triago, the company where he’d recently ascended to CEO. He’d built the mightily profitable franchise in an obscure corner of private equity called “directs”—essentially pairing solidly run businesses that wanted to sell, with family offices looking for outsize returns. Now, suitors comprising top banks from Spain and Korea, a leading U.S. private equity firm, a major Midwestern lender, and a giant Asian trading house were circling.

But as Swain weighed the offers, one stood out—from Bob Hotz, chairman of corporate finance and acquisitions chief at mid-market investment banking powerhouse Houlihan Lokey. He felt sure that Houlihan would provide the best home for himself and his team. So he was crushed when an email arrived: “We regrettably will withdraw from considering the purchase of Triago,” wrote Hotz, but noted that “you were the primary reason for our interest,” and graciously suggested they meet for a quick coffee at 9:20 the next morning.

Swain didn’t expect much. “I didn’t even wear socks with my loafers. I never wear socks at any casual, inconsequential meeting,” he recalls. “I just wanted to get veteran Bob’s advice on which offer to pick.” At breakfast, the hyperkinetic youngster quizzed the silver-coiffed, soft-spoken Hotz, who’s a half-century his senior. “Given the time limit, I was talking so fast I didn’t even touch my usual avocado toast. I asked Bob: ‘Which one is the right fit?’ And Bob does a total flip, and says, ‘I think we’re the best partner.’”

At 11 p.m. on Wednesday, Aug. 30, Hotz called Swain to declare he was in—but only on the condition that Swain leave his house full of guests on Nantucket and fly to London the Sunday of Labor Day weekend for a rapid-fire session of due diligence. Swain agreed and boarded the red-eye to Heathrow toting a bulging roller suitcase packed full of financials. By the following Friday, Houlihan Lokey had clinched the whirlwind purchase, reportedly for well over $100 million.

The marriage created a force to watch on Wall Street, between a whiz kid with a knack for dealmaking, and the giant mid-tier investment bank you’ve probably never heard of. In his early twenties, even before joining Triago, Swain beat the Wall Street pros in recognizing that the burgeoning wealth of family offices meant there was high interest in purchasing individual companies, rather than investing in “blind pools” of enterprises assembled by the private equity (PE) giants.

The founders of those family offices had often built and sold their own companies, and they and their heirs relished “kicking the tires,” instead of having a Carlyle or TPG decide for them. To satisfy that appetite among the super-wealthy, Swain developed a wide network of venturesome “independent sponsors,” operators that obtained letters of intent to purchase private, midsize businesses that did everything from making routine airplane parts to marketing Disney-branded souvenirs at a predetermined price.

That process where investors cherry-pick their own deals rather than, say, joining fund No. 7 of a PE colossus, is called “directs.” It’s existed for decades, but in his five years at Triago, Swain has proved the prime mover in taking the sector from backwater to big business, and became king of the realm. By Fortune’s estimates, drawn from industry data, the value of all direct deals, using the broad definition of single investments in private companies, will explode to something like $200 billion this year, multiple the number several years ago.

Still, “directs” have a way to go before they pose any sort of real threat to the PE giants. Though Swain has big plans, there has yet to be mass adoption by the traditional stalwarts of PE—the big pension funds, insurers, and endowments. Those huge institutions still overwhelmingly choose pools, where they can put tons of money to work quickly without specialized teams needed to parse these bespoke deals. Meanwhile success attracts competition—and Swain’s fat returns (garnered by buying and fixing cheap, overlooked, small and midsize companies) are attracting more and more competitors, a trend that could hike prices and reduce profits.

But no challenges seem to faze Swain, who has developed a vast Rolodex featuring the investment arms for the clans of late real estate magnate Sam Zell and ambassador to the U.K. Warren Stephens, plus the Romneys and Bloombergs, among a panoply of luminary names. He proved an expert at curating a cast of top sponsors and identifying the investments that promised—and a few years later delivered—big, PE-beating returns. “Pre-Matt, we had to find the independent sponsors, and it was difficult,” says Duran Curis, founding partner at Ocean Avenue Capital Partners, who manages a $2 billion portfolio of 140 directs. “His big contribution is that he finds them for us, and presents the best opportunities.” Now, paired with the muscle of Houlihan Lokey, Swain has big plans to start selling to pension funds, endowments, and asset managers.

Adds David Feierstein, cofounder of Ronin Equity Partners, an investment firm for which Swain’s raised several hundred million dollars to fund half a dozen purchases, “If you didn’t have someone as aggressive and charismatic as Matt, the directs industry wouldn’t be nearly where it is today. Matt had the first mover advantage. In directs, Matt runs the show.”

The charm offensive

There’s something rare about Swain, who is a young brainiac, but one who has built his business the old-fashioned, pre-quant-trading and Excel models Wall Street way, via charm offensives that weave webs of tight relationships few rivals can match. It’s remarkable that this super-hustler comes from a highly privileged background. He grew up in Greenwich, Conn., son of the CFO of a prominent hedge fund. His ancestors were the original owners of Nantucket island. “Matt tells me his family had been coming to Nantucket for generations. So we’re walking to get coffee and we pass Swain Street, then Swain House, then we go to the Whaling Museum and get greeted by half a dozen portraits of his forbears,” says Rupert Edis, CEO of the Landon family office that includes Landon Capital Partners, a long-standing investor in Swain’s directs.

After graduating from Colgate University, where he served as student body president and starred in squash—he’s still one of the best amateur players in Manhattan—Swain joined Stifel, in a “placement agent” unit that raised money for hedge funds. The managers were amazed that family offices weren’t returning their calls, so they assigned Swain to find takers from a “dead list” of 1,000 mostly wealthy clans. The green recruit got mostly noes, upbraidings, and even a “You’re a midget!” from the respondents who didn’t hang up, but he also learned there was a gap in the market.

Swain played matchmaker. He found that independent sponsor IVEST needed funding for a plush toy purveyor called Dan Dee, and brought their leaders to Solamere, the family office representing the Romneys, former Walmart CEO Lee Scott, and other wealthy investors. Swain raised $100 million to notch the purchase. By 2018, he found a spot that was just small and daring enough to take a flier on his vision of building a whole business around directs: Triago, the firm founded by Frenchman Antoine Dréan that did a thriving trade in a close cousin, finding buyers for limited partners (LPs) that sought to sell their stakes in private equity pools.

Swain quickly turned directs into Triago’s profit driver. Over three years, he raised $3 billion in equity capital for 35 deals that, including debt, backed over $10 billion in purchases. In April 2022, Dréan named his 27-year old comer as CEO.

While Big PE typically delivers twofold returns to investors over a longer holding period, directs aim far higher. “Our investors are looking for returns of 3x or more,” says Patrick Zyla, managing director of Castle Harlan, a firm that Swain has worked with extensively.

Regular PE funds famously charge around 2% a year on all investors’ funds, whether or not they’ve been put to work yet. The directs sponsors typically don’t charge any fees at all, and even better, don’t get paid unless they deliver big-time. The industry’s giants usually get a fixed “carry” of 20% of profits when companies are sold. But directs deals are usually structured so that the sponsors garner zip until they hit a 2x bogey. Over that number, they start collecting 20%, but their take accelerates sharply with each multiple of their investors’ stake they return. If the sponsor-managers hit 5x, they can pocket as much as 40% of the gain.

“If you didn’t have someone as aggressive and charismatic as Matt, the directs industry wouldn’t be nearly where it is today.”David Feierstein, cofounder of Ronin Equity Partners

Sam Zell, who along with his team funded a number of Swain’s deals, absolutely loved this ultra-“skin in the game” aspect of directs. (Swain relates that Zell liked having his photo snapped alongside the youngster, as Swain was only slightly taller than the late bantam tycoon.) Zell and the president of the Zell family office EGI, Mark Sotir, would push Swain to arrange transactions that raised the bar for capturing a share of the profits, but gave the management teams an even bigger score for fabulous results.

That makes Houlihan Lokey’s pitch particularly appealing right now, given that PE has seen a sharp drop-off in exits: According to Hamilton Lane, a firm that invests on behalf of pension funds, as of 2021 PE firms were still holding 45% of their buyout deals five years following their purchase; last year, around 65% were still sitting unsold after a half-decade.

Meanwhile Swain’s model thrives on speed. With directs, the money comes fast, and so do the fees. It typically takes placement agents working on behalf of PE firms nine to 18 months to raise a full fund. But once the Swain gang gets a mandate from a sponsor, he and his bankers regularly make the rounds and secure the funding in eight to nine weeks. His team of 40 also concentrates on bigger and bigger deals that swell their take from the average directs transaction. This year, he expects to do around a dozen deals at an average enterprise value of $200 million to $400 million. “That’s much, much bigger than the average in the industry,” he avows. “We’re now working on one worth $2 billion, and the numbers will keep climbing.”

That expanded holding time, and LP thirst for liquidity, should especially benefit the first field where Swain and Houlihan Lokey envisage big expansion beyond traditional directs: so-called continuation vehicles, or CVs, where a fund tags an outstanding company promising great things, and doesn’t want to sell as it exits the other holdings. Today, Evercore is the biggest player, but Houlihan is rising. CVs cash out most of the existing LPs in that star “keeper” at a good return, and replace them with a fresh crop that sees big gains ahead by keeping and growing the standout for another, say, three or four years. The company spins off from the fund and continues as a stand-alone. The newcomers are once again going “direct” since they’re shopping on a deal-by-deal basis.

The second offshoot is what’s known as “co-investment.” PE firms increasingly seek to raise money beyond what the original investors contributed to a given fund. Say the managers see a software provider on the block at a bargain price, and want to add it to a tech portfolio. Or the “concentration limit” on any one purchase is $300 million, and they’d hate to miss out on a perfect fit at $450 million. Or the goal may be clinching a big add-on acquisition, or satisfying an unforeseen surge in sales by constructing new plants. In all those cases, the fund may lack the capital for seizing the opportunity. It may have $300 million still in its coffers and need a couple of hundred million more.

Swain and the Houlihan Lokey team view the area, still in its infancy, as a huge field for lucrative fundraising and investment-banking business. It’s a good deal for the fund LPs because they pay no fee or carry on the additional capital. The new investors pay carry at a rate that’s closely tied to performance: The percentage starts low and rises depending on the level of profit achieved. The arrangement empowers the co-investors to pick and choose their own individual deals, the great lure of directs in general.

Instead of coming from the small sponsors that Swain has mainly represented in the past, these opportunities are flowing from big, established PE outfits that have run these candidates for years, and can show impressive track records, both for the co-invest property and the firm’s overall performance. That imprimatur greatly heightens their appeal.

“A commercial thought every minute of every day”

At Houlihan Lokey, Swain persists in the headlong roundelay of networking that’s his calling card. He does most of his business in a five-block radius of Midtown Manhattan. He resides in a Moorish-themed, Park Avenue high-rise, where he rents an apartment from Eric Trump; Ivanka Trump is his neighbor. Swain does his primary dealmaking at two nearby eateries, tony French venue Le Bilboquet and the LoewsRegency Bar & Grill. “I do back to back breakfasts at Loews, then a lunch at Bilboquet,” he avows. “Then in the evening it’s three chapters. First a cocktail at Bilboquet, then a real dinner, then an elongated catch-up over drinks. Before I hit 30, it would stop at midnight. Now that I’m 30, it’s over by 11:00 or midnight.” In the interests of efficiency, Swain changes tables when the new guest arrives, even if the old guest is still sitting there. Notes Tom Burchill, managing partner of PE firm Seven Point: “He bounces from one pole to another. Once, I got him for 45 minutes at Bilboquet. Lucky me.” When on Nantucket, Swain zooms around the island in a hard-bottom, Navy SEAL–style, super-high-speed raft, a type deployed by the military in Ukraine. He had it imported, and the money went to a manufacturer looking to support jobs in the beleaguered nation.

His business associates view him as both blithely charming and, in a word, obsessed. “Matt thinks a commercial thought every minute of every day,” observes Hotz, whom Swain reveres as “Uncle Bob.” Adds Mike DiPiano, managing general partner at tech PE firm NewSpring Capital: “He’s a young man selling at all times.” His ability to attract top older notables is remarkable. “He’s got this old soul for a young guy, and it’s infectious,” says Kevin Wilcox of the Stephens family office. Edis, of the Landon family office, praises Swain’s knack for “attracting powerful mentors and allies” and calls his ability to accomplish tasks in a jiffy as “Napoleonic”—at 5-foot-8, by the way, Swain is midsize, like the companies he markets.

Though Houlihan Lokey bought Triago 18 months ago, each side is already bringing the other big benefits. It’s astounding that the firm is so little known. Houlihan ranks as the world’s largest investment bank for midsize private companies. It’s also been the top performer on Wall Street for rewarding investors over the past decade, and by a lot. In that span, it’s delivered total shareholder returns of 26.4% a year, beating such fellow boutiques as Lazard (5.9%), Jefferies (13.2%), Moelis (17.2%), and Evercore (22%), while also waxing big guys Citigroup (9.3%), Bank of America (14.5%), Goldman Sachs (18.0%), Morgan Stanley (19.9%), and J.P. Morgan (20.3%). Back in the fall of 2015, Houlihan’s market cap trailed those of Jefferies, Lazard, and Evercore. Now at $13.6 billion, it’s bigger than all three.

A major plus in terms of the synergy at the newly combined company: the directs investment, fund investment, CVs, and co-investments originating from Houlihan Lokey’s PE clients. In 2023 Atlas Merchant Capital, a combined hedge and PE fund headed by former Barclays CEO Bob Diamond, worked with Houlihan as its advisor to MarshBerry, in a significant fund investment for that leading platform in the insurance brokerage space. Diamond is a Swain fan and was one of the Triago bidders. Now that Swain has joined Houlihan, Diamond is giving the firm business on both the fund investment and directs sides; he’s recently engaged the Swain team on securing follow-on capital for Atlas portfolio companies.

The CV connection is also spouting advisory fees for Houlihan Lokey. Last October, Swain raised the money for PE fund NewSpring, renowned for scoring big from buying Nutrisystem in the 2000s, for a vehicle that combined two of its star portfolio holdings. “You realize that if you could just hold these investments longer you’ll get much more out of them,” says cofounder DiPiano. Over sundry phone calls, Houlihan provided investment banking guidance to the family office investors, parsing the transactions’ pros and cons.

In co-invests, Riverside, a $14 billion PE firm that had been a Houlihan Lokey client for years but never worked with Triago, was seeking additional co-investment equity as a way to attract new limited partners and close on two fresh investments. Via the Houlihan connection, in stepped the Swain team. “We were introduced to dozens of LPs in short order, and secured investments from a number of them,” says Peggy Roberts, a managing partner at the firm. “Partnering with Houlihan has helped us forge sustained relationships with firms we would not have met otherwise.”

In the past nine months, Houlihan has raised over $500 million to secure three purchases for Swain’s stalwart customer Ronin. In June, the Swain contingent provided Ronin the funding to buy a company that repairs and overhauls systems for commercial aircraft. Houlihan conducted analysis on behalf of the family office investors. In April, Landon Capital Partners (LCP) scored a big hit via the sale of its portfolio holding, Wisconsin cheesemaker Heartisan Foods, where it partnered with Ronin on a deal in which Triago had raised the money. Through the Swain link, LCP has awarded Houlihan two mandates, one for a debt financing of a portfolio company, and another to explore a sale.

Early this year, the directs franchise collected $75 million in equity and debt for Seven Point to buy Frazier Aviation, producer of structural parts for military aircraft. Now, Seven Point is strongly considering Houlihan Lokey to provide the mark-to-market valuation analysis of its portfolio holdings to deliver to investors.

The rewards also go the other way. Liberty Hall, a PE sponsor focused exclusively on aerospace and defense, is a long-standing Houlihan Lokey client, and had hired Triago before the acquisition to lead a CV. The tie-up has further deepened its Houlihan relationship. Liberty Hall hired Houlihan to raise the capital for a classic direct that closed earlier this year. Between the CV and direct, Houlihan secured $250 million for Liberty. It’s also working with the Houlihan M&A group to seek new purchases.

Edis, chief of the Landon family office and a protégé of its founder, the late swashbuckling billionaire Timothy Landon, who’s legendary as the chief political advisor to his military school chum, the sultan of Oman, notes that Swain gives Houlihan Lokey an extra edge. “Matt’s been crucial in upselling Houlihan’s other services. As investments move through their life cycle, they need M&A, debt refinancing, and finding buyers for the final sale, and the natural thing for one of Matt’s companies is for Houlihan to take on that work,” says Edis. “We’re doing a new refi with Houlihan because of the cycle that began with Matt.”

In April 2025, the firm promoted Swain as co-head of its equity capital solutions group. The unit encompasses both the equity and debt fundraising franchises; according to sources on Wall Street the group generates $400 million to $500 million a year in revenue—that’s as much as a quarter of the $2.4 billion the firm posted in fiscal year 2025, ended in March.

Swain’s section is highly lucrative. From industry sources, Fortune estimates that at an annual run rate, the three directs areas combined—the traditional variety, CVs, and co-invests—are raising well over $5 billion a year. From studying this highly fragmented industry, Fortune concludes that Houlihan Lokey leads the field in combined classic directs and CVs; in directs alone, it holds a market share of around 10%.

For Swain, the rise of directs presages nothing less than a revolution in the world’s financial markets. “In the future, more and more institutional investors like pension funds and endowments will follow the family offices in buying individual companies, just as investors pick stocks. Instead of investing in a pool, they’ll invest directly into a company’s equity,” he declares. “In other words, directs will make the private market for companies much more liquid so that it looks like the public market for stocks.” Swain predicts that within a decade, the total size of the three classes of directs will be attracting the same annual volume of new funds as traditional PE commands today.

“In the future, directs will make the private market for companies much more liquid so that it looks like the public market for stocks.”Matt Swain

Already the Ventura County Employees’ Retirement Association is launching a program that will spend up to $20 million on directs co-investment this year, and the Texas Municipal Retirement System plans to dedicate as much as $15 billion over the next five years, adding extra growth capital to individual holdings in PE funds. “The large pension funds are migrating to smaller managers in the lower-middle-market and middle-market space because that’s where they’re seeing the highest returns,” says a leading investment advisor to the PE industry.

Swain’s PE customers praise his analytical skills in identifying the most promising deals. “He did intense due diligence on the Frazier Aviation deal, where we’re sponsor,” recalls Burchill of Seven Point. “When Matt goes in front of investors and says it will be good, they listen to him. His credibility helped give us our choice of investors.”

The golden child has developed his own highly original approach in trawling for profit—even on the streets of Manhattan, where you’ll never find him inside a taxi. “No matter how hot or cold it may be, Matt will say, ‘Let’s walk. It’s better for networking,’” marvels Hotz. One day in September, this writer joined Swain on one of his excursions down Park Avenue, and on cue, he ran into Jack Oliver, who heads the PE firm Finback, alongside former Florida Gov. Jeb Bush. Two of the most outsize personas in private equity held their own little curbside summit, rapping on how they might connect on deals. I later asked the super-personable Oliver whether he or Swain is the more magnetic presence. Riposted Oliver: “I’d have to say I have the bigger personality. But he’s more successful.” One thing’s for sure, in a business that thrives on relationships, Swain will never stop working the room, the block, the island, the world, to bring deep-pocketed investors into his own corner of Wall Street.

The first can be regarded by retirees and those on the cusp of retirement as a must read: William Bengen’s A Richer Retirement, the long-awaited update of his classic book on the much-cited 4% Rule: Conserving Client Portfolios During Retirement. First published in 2006, that book was really aimed at financial advisors but became popular with the general investing public after it got extensive press exposure over the years.

The 4% Rule—which is actually closer to a 4.7% Rule depending how you interpret it—refers to the “safe” percentage of a portfolio that retirees can withdraw each year without running out of money in 30 years, net of inflation. Bengen’s term for this is “SAFEMAX.”

The new book is supposedly aimed at average investors. Still, I found it pretty technical, filled chock-a-block with charts and tables that are probably more accessible to the original audience of financial professionals. Counting some useful appendices, the book is just under 250 pages.

After wading through all Bengen’s tweaks meant to minimize the impact of inflation, bear markets, and unexpected longevity, I was left with the impression the original 4% Rule remains a pretty good initial guestimate for what retirees can safely withdraw in any given year.

Sure, 3.5% or 3% may be technically “safer,” especially if you expect to live a very long life or want to leave an estate for your heirs. I’ve even seen arguments that a 2% retirement rule may be appropriate for extremely risk-averse retirees.

On the other hand, it’s not too dangerous to withdraw 6% or 7% or more as long as stock markets and interest rates cooperate. That’s what many retirees intuitively do anyway; they reduce withdrawals in bear markets, and splurge a bit in raging bull markets.

It’s also worth noting that whether you choose 3%, 5%, or larger percentages, that guideline really just applies to your investment portfolios, whether held in tax-deferred or tax-exempt accounts or taxable ones. Most Canadian retirees can also count on the Canada Pension Plan (CPP) and Old Age Security (OAS), not to mention employer pensions. Those lacking big defined-benefit pensions but who have plenty saved in RRSPs and TFSAs can choose to pensionize or partially pensionize their nest eggs by buying annuities. (For timing, see this piece published recently on my blog.) For that concept, refer to Professor Moshe Milevsky’s excellent book, Pensionize Your Nest Egg.

Making money in any market

More controversial is Jim Cramer’s How to Make Money in Any Market. I know it’s fashionable for some mainstream financial journalists to disparage the long-time host of Mad Money and in-house stock-picking guru on Squawk on the Street. I never watch him on TV (MSNBC) but often listen to his podcasts while walking or at the gym, usually at 1.5x speed and skipping over interviews with the CEOs of more speculative stocks I have no interest in. Cramer’s critics tend to be diehard indexers who swear it’s impossible to consistently pick stocks and “beat” the market over the long run. I tend to side with them, but more on that below.

Article Continues Below Advertisement

Obviously, Cramer begs to differ, often trotting out testimonials from Nvidia millionaires who bought that spectacular artificial intelligence (AI) chip stock the moment he named his dog after it (sadly now deceased). Cramer devotes an entire chapter to that call, which he mentions every chance he gets. I did buy that stock too, although I was too late and risk-averse to bet the farm enough to change my life with it.

What his critics may not realize is that even Cramer believes in indexing at least 50% of a portfolio. In fact, he tells newcomers to stocks that their first $10,000 (US) should go in an S&P500 index fund. Hard to argue with that.

Where I part ways is his book’s recommendation of holding just five stocks for the 50% of a portfolio that is not indexed. That would mean holding around 10% of your total portfolio in each such stock, which is way more concentrated than most investors would countenance. Much of the book goes into how to choose the kind of secular growth stocks he prefers, with the help of modern AI tools like ChatGPT, Grok, and all the rest.

I used to wonder about his show’s regular segment, Am I diversified?, where readers submit their five picks for Cramer’s consideration. I’d be surprized if there is an investor anywhere whose portfolio is that concentrated. Even Cramer’s much-cited Charitable Trust holds many more than five stocks.

Canada’s best dividend stocks

How not to invest

This leads me to the third book I ordered from Amazon, recently reviewed by Michael J. Wiener of the Michael James on Money blog: Barry Ritholtz’s book How Not to Invest. Cramer cynics might quip that would have been a better title for How to make money in any market had it not already been taken by Ritholtz; Cramer has after all famously inspired some ETF companies to provide “reverse Cramer” funds that short his major long recommendations.

Ritholtz’s book clocks in at almost 500 pages but is quite readable. It has attracted multiple testimonials ranging from William Bernstein (“Destined to become a classic.”) to DFA’s David Booth, Shark Tank’s Mark Cuban and author Morgan Housel, known through The Motley Fool, and who penned the foreword.

Ritholtz organizes his book in four parts: Bad Ideas, Bad Numbers, Bad Behavior, and Good Advice. While Cramer tempts us into individual stock-picking, Ritholtz reminds us that few can do it well; nor can most of us successfully pull off market timing. He devotes a fair bit of space to how badly some pundits’ predictions have panned out in the past. I was left with a renewed appreciation for the benefits of indexing, certainly for the core of portfolios if not for their entirety. As he puts it: “Index (mostly). Own a broad set of low-cost equity indices for the best long-term results.” He lists five advantages to indexing: lower costs and taxes, you own all the winners, better long-term performance, simplicity and less bad behaviour.

Fortunately, ordinary investors have many advantages over the pros, such as not having to benchmark against indices or worry about investors who sell a fund, the ability to keep costs low, and in theory a much longer time horizon. But the clincher is that “indexing gives you a better chance to be ‘less stupid.’”

The decline in RI usage was driven by fewer new advisors offering RI to clients, the 2025 Advisor RI Insights Study said. The proportion of clients using a responsible methodology was roughly steady at 18%, however, compared to 19% recorded two years ago. Increasingly, it is clients initiating conversations about responsible strategies (41%) over advisors (28%). Still, nearly half of advisors (46%) agree that questions about RI should be included in Know Your Client forms used with new clients.

“While adoption has steadied, investor demand for RI remains strong and advisors remain open to closing the service gap,” Patricia Fletcher, CEO of the RIA, said in a release. “Mobilizing wholesalers and equipping advisors with tools and training, we can empower advisors to align portfolios with their clients’ values.”

Compare the best TFSA rates in Canada

The reasons for the RI pullback could be related to economic headwinds, the backlash against environmental, social, and governance (ESG) criteria in the U.S., or the maturation of the RI niche, with fewer new investment products coming on the market, the study’s authors speculated.

This reversal is consistent with public attitudes reflected in President Donald Trump’s recent dismissal of climate change as a “con job” and Canada’s withdrawal of carbon taxes and electric vehicle subsidies.

But it may also be rooted in the relatively poor performance of RI investments in recent years.

In the early years of what was then called “ethical investing”—in the 1990s and early 2000s—many RI funds could boast superior returns to broad index funds. RI advocates pointed to the way ESG criteria served as a force for risk mitigation, steering clients away from potentially unsustainable industries (tobacco, coal) and companies at greater risk of lawsuits and increased regulation.

The last decade, by contrast, has been marked by strong performance of major indices like the S&P 500 and underperformance by sectors commonly overweighted in RI portfolios, such as renewable energy. In the RIA survey, “Concerns about returns” ranked as the second most common reason advisors cited for not including RI in client portfolios (47%), after “Lack of client interest/demand” (61%).

Other factors possibly contributing to the RI pause include the rising market share of exchange-traded funds (ETFs) over mutual funds—76% of advisors offering RI said they predominantly use mutual funds, compared to just 8% using ETFs—and skepticism fed by so-called “greenwashing.” Thirty-five percent of advisors polled by RIA cited “Concerns about the validity of ESG benefits” among their reasons for not offering RI portfolios.

Article Continues Below Advertisement

Get free MoneySense financial tips, news & advice in your inbox.

On an adjusted basis, BlackBerry says it earned four cents US per share for the quarter compared with zero cents US per share a year earlier.

Revenue for the company’s latest quarter totalled US$129.6 million, up from US$126.2 million a year earlier. The increase came as its QNX segment revenue rose to US$63.1 million, up from US$54.7 million a year ago, while secure communications revenue fell to US$59.9 million compared with US$66.5 million. Licensing revenue amounted to US$6.6 million, up from $5.0 million a year earlier.

In its outlook for its full year, BlackBerry says it now expects full year revenue of US$519 million to US$541 million, up from earlier guidance for US$508 million to US$538 million.

The company also raised its guidance for its adjusted earnings per share for its full year to between 11 cents US and 15 cents US, up from earlier expectations for between eight cents US and 10 cents US.

Air Canada lowers full-year guidance as hit from strike estimated at $375M

Air Canada (TSX:AC)

Adjusted guidance for the year:

Previous: $3.2 billion to $3.6 billion

Adjusted: $2.9 billion to $3.1 billion

Source Google

Air Canada has lowered its guidance for the year after taking a hit from the flight attendant strike that took place earlier this summer. The Montreal-based airline said in a press release that it estimates the cost of the labour disruption was $375 million on operating income and adjusted earnings before interest, taxes, depreciation and amortization.

Air Canada said that it now expects to make between $2.9 billion and $3.1 billion in adjusted EBITDA for the full year. This is in comparison to the airline’s previous 2025 guidance that it suspended in August, which had projected adjusted EBITDA between $3.2 billion and $3.6 billion.

For the third quarter, Air Canada said it expects operating capacity to decline by around 2% from the same period last year, due to the cancellation of more than 3,200 flights. It also expects operating income between $250 million and $300 million during the quarter.

Article Continues Below Advertisement

The airline said three factors combined for the $375 million financial impact of the strike. The first is an estimated $430 revenue hit from refunds, customer compensation and lower travel bookings. It also had about $90 million in incremental costs associated with reimbursements for customers and some labour operating costs. However, the company also saved $145 million, primarily due to lower fuel costs, which reduced the loss.

The Air Canada flight attendant strike lasted three days and ended on Aug. 19, though it took longer to ramp up to full operations.

Earlier this month, Air Canada flight attendants massively rejected the employer’s wage offer, with the airline saying the wage portion will now be referred to mediation as previously agreed to by both sides.

The tentative deal that was voted down raised wages for workers and established a pay structure for time worked when aircraft are on the ground.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

President Donald Trump wants corporations to “no longer be forced” to report earnings every quarter.

In a Truth Social post on Monday, he said companies should instead only be required to post earnings every six months, pending the U.S. Securities and Exchange Commission’s approval. This change would break a quarterly reporting mandate that’s been in place since 1970.

“This will save money, and allow managers to focus on properly running their companies,” Trump wrote.

Trump added that China has a “50 to 100 year view on management of a company,” as opposed to U.S. companies required to report four times in a fiscal year. China’s Hong Kong Stock Exchange (HKEX) allows companies to submit voluntary quarterly financial disclosures, but only requires them to report their financial results twice a year.

During his first term, Trump publicly asked the SEC on X, then still known as Twitter, to study shifting company disclosures from a quarterly to semiannual basis, stating business leaders felt less frequent reporting would allow for greater flexibility and long-term planning.

He told reporters at the time that he got the idea from CEOs.

“It made sense to me because, you know, we are not thinking far enough out,” Trump said in 2018. “We’ve been accused of that for a long time, this country. So we’re looking at that very, very seriously.”

No change came from the SEC.

A revived debate

“President Trump has revived an old idea emphasizing the costs of quarterly filings, the distraction from long-term goals, and how they reinforce Wall Street’s obsession with beating short-term expectations,” Usha Haley, a professor at the Barton School of Business at Wichita State University, told Fortune.

For his part, SEC Chair Paul Atkins has explicitly called for more transparency as he’s taken control of the regulatory body this year.

But companies keep pushing back. Last week, the San Francisco-based Long Term Stock Exchange said it planned to petition the SEC to end its quarterly reporting requirement. The exchange lists companies focused on long-term goals.

Critics of the move argue that it might reduce transparency for investors.

Chad Cummings, a CPA and attorney at Cummings & Cummings Law, told Fortune semiannual reporting enables companies to hide “red flags” like deteriorating cash flows or abrupt changes in auditor language, which can lead to unsavory practices like concealment of liquidity crises, accounting fraud, and whistleblower retaliation.

“Removal of quarterly earnings sabotages valuation models and tilts power to insiders,” Cummings, who has active bar admissions in the U.S. Tax and Bankruptcy courts, added.

SEC approval would face internal resistance, statutory barriers, and potential litigation, as the SEC’s investor protection mandate requires “reasonably current” disclosure, Cummings said.

If regulators stopped requiring companies to report earnings every quarter without having clear legal authority, the decision could be challenged in court under the Administrative Procedure Act, a federal law that governs how U.S. administrative agencies create regulations, he warned.

Meanwhile, Haley also said Trump’s nod to China’s financial disclosure mandates misses the point.

“The United States is not China,” she said. “Our markets derive their strength and global dominance through transparency, investor protections, and a long tradition of disclosures… Weakening those guardrails, while invoking efficiency risks, undermines investors’ confidence, the foundation of U.S. capital markets, which China does not have.”

Fortune Global Forum returns Oct. 26–27, 2025 in Riyadh. CEOs and global leaders will gather for a dynamic, invitation-only event shaping the future of business. Apply for an invitation.

The fashion retailer, which operates under the Garage and Dynamite banners, says its profit amounted to 56 cents per diluted share for the quarter ended Aug. 2, up from 38 cents per diluted share in the same quarter last year. On an adjusted basis, Groupe Dynamite says it earned 57 cents per diluted share, up from an adjusted profit of 40 cents per diluted share a year earlier.

Revenue for the 13-week period totalled $326.4 million, up from $239.1 million a year ago, while its comparable store sales rose 28.6%.

In its outlook, Groupe Dynamite says it now expects comparable store sales growth between 17.0% and 19.0% for its full year, up from earlier expectations for between 7.5 and 9.0%. It also raised its expectations for its adjusted earnings before interest, taxes, depreciation and amortization margin to between 32.0% and 33.5%, up from earlier guidance for between 30.3% and 32.3%.

Roots Corp. offered some buzzy marketing campaigns and brand collaborations over the summer in hopes of driving traffic to the retailer but still wound up reporting a loss during the period.

The Toronto-based apparel maker said Wednesday its second-quarter net loss narrowed to $4.4 million compared with a $5.2-million loss a year earlier. The result for the period ended Aug. 2 amounted to a loss of 11 cents per share for the quarter compared with a loss of 13 cents per share a year prior. Meanwhile, second-quarter sales reached $50.8 million, up from $47.7 million.

Roots CEO Meghan Roach told financial analysts on a conference call Wednesday that it is typical for the company to generate about 30% of its sales in the first half of the year, often leaving it with a loss as it heads into the fall and winter.

However, the second-quarter results this year came in spite of tense trade relations between Canada and the U.S., which have made shoppers more cautious. “Despite the dynamic global operating environment, Roots continues to build positive momentum as we head into the second half of the year,” Roots chief financial officer Leon Wu said on the same call as Roach.

Article Continues Below Advertisement

Much of that momentum has come from direct-to-consumer sales, which include corporate retail store and e-commerce sales. In the second quarter, direct-to-consumer sales totalled $41 million, up 12.7% from the year before. Direct-to-consumer comparable sales growth was 17.8%.

Wu saw the increase as a reflection of customers responding well to the company’s spring and summer collections as well as its recent marketing campaigns. The campaigns helped Roots increase engagement and made the brand feel more accessible, Roach said. Included in the campaigns were instances where Roots transformed a parking lot into nature-inspired spaces for golf and tennis.

The company also hosted a pop-up in Toronto to promote a summer capsule collection with ginger ale maker Canada Dry. The collection included hoodies and graphic tees featuring Canada Dry’s logo and vintage advertisements.

“Together, these collaborations amplified brand heat, reinforced our heritage positioning, and extended our reach for authentic Canadian cultural moments,” Roach said. “We will continue to use selective partnerships and experiences to build that brand perception and support full-price sell through into fall.”

Transat A.T. Inc. reported a net income of $399.8 million in its latest quarter compared with a loss of $39.9 million in the same quarter last year, as its revenue rose 4.1%.

The parent company of Air Transat says the profit amounted to $9.97 per share for the quarter ended July 31, compared with a loss of $1.03 per share a year earlier.

On an adjusted basis, Transat says it had a loss of 28 cents per share in its latest quarter, compared with an adjusted loss of 93 cents per share in the same quarter last year.

They recognize, too, that there are more fish in the sea than the stock and bond indices represented in core portfolios. They may seek to spice up returns or further diversify with, say, a high-yield bond or crypto fund. There’s no limit to the add-ons you can apply to a couch portfolio.

Second, there are those who get the hang of managing a core portfolio, like the results, and, upon gaining investment knowledge and experience, feel comfortable raising the complexity of their holdings. Couch potato investing offers a good entry level to more sophisticated investing, by which time your nest egg will likely have grown and gained a momentum all its own.

While the core exposures should always represent a majority of any long-term investment portfolio, here are some asset types available through ETFs that typically aren’t represented in core portfolios:

Money markets and high-interest savings accounts (HISAs)

Gold and other commodities

Cryptocurrency

Alternative strategies (leveraged, inverse and hedge funds)

Private assets

There may also be segments of the investible universe already embedded within core portfolios that an investor might seek to increase their exposure to:

Sector-specific equities (e.g. REITs)

Country-specific equities (e.g. India)

Dividend stocks

Corporate bonds

Short- or long-duration bonds

Compare the best TFSA rates in Canada

American investor Ray Dalio famously created an “all-weather portfolio” that he claimed would hold up in almost any market environment. It broke down like this: 30% U.S. stocks, 40% long-term treasury bonds, 15% intermediate bonds, 7.5% commodities, and 7.5% gold. Should you so choose, you could create a reasonable facsimile to the all-weather portfolio using ETFs.

Our MoneySense columnists have likewise illustrated how you can further diversify a core portfolio, reducing the risk of losses.

Here’s one such strategy, augmenting an asset-allocation fund with cash and/or gold bullion that would have held up well through past market downturns. And there’s another that adopts the buzzy 40/30/30 portfolio model that includes exposure to alternative assets along with stocks and bonds.

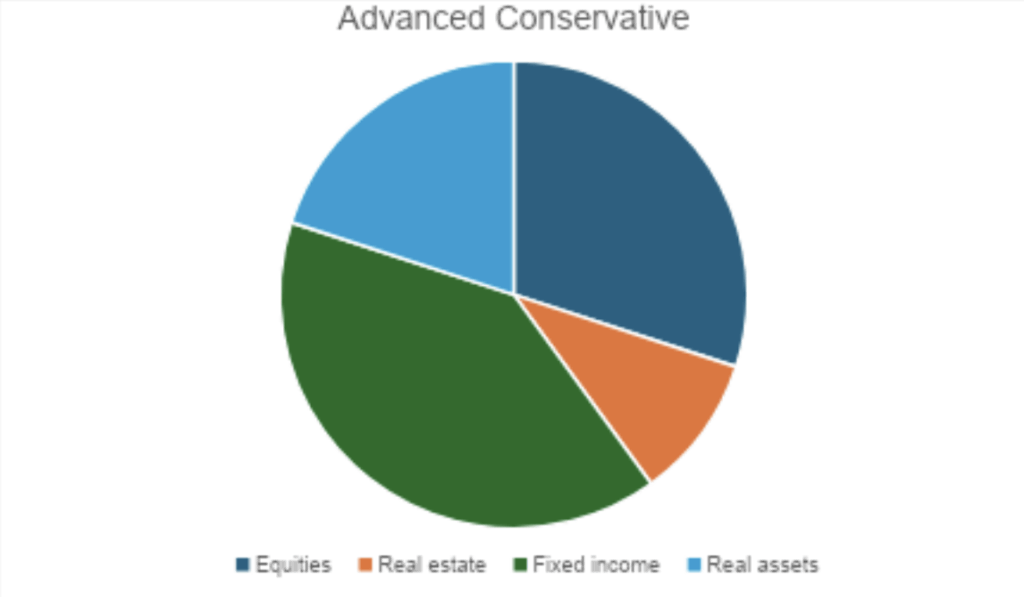

If you think you might be ready to take the next step beyond investing just in Canadian bonds and the major investible regions for equities, consider one of the advanced portfolios listed below. These are just suggested allocations that we believe won’t lead you too far astray. Feel free to tweak them to better suit your circumstances and build on them over time.

Article Continues Below Advertisement

An important note: As your portfolio gets more complex, it will be harder to fill each allocation with index mutual funds and asset-allocation ETFs, which is why index ETFs are the go-to vehicle for building an advanced portfolio. We’ve suggested some funds, but with some 1,500 ETFs trading in Canada, know that there will be comparable competing products out there, possibly with lower fees or other attractive attributes.

Consider our fund picks suggestions only. For up-to-date ETF recommendations from the experts, check out MoneySense’s guide to the best ETFs in Canada, which we update every year in May.

But before we dive into these further, an important note. The following options are meant to illustrate sample portfolios and do not constitute financial advice. If you haven’t already done so, review the principles behind how to build a couch-potato portfolio and our overview of couch potato investing before committing your hard-earned money to any of the investments indicated.

Option 1: Build a mutual fund portfolio

Most Canadian banks offer a selection of relatively low-cost index mutual funds with which you can build your own balanced portfolio. Depending on your relationship with the institution, they may throw in advice for free.

Your mutual fund options

TD is the best-known provider in this space with its e-Series funds, but Scotiabank, RBC, and CIBC, among others, have similar products.

The pie chart below illustrates how a typical mid-career investor with a moderate risk tolerance might construct a portfolio using e-Series funds. More conservative investors would typically increase the fixed-income allocation as high as 80%, while more growth-oriented investors might reduce the fixed income component to 20% or less.

Tangerine Bank, the online banking subsidiary of Scotiabank, lets you simplify the process further with a single, all-in-one product—similar to the asset-allocation ETFs described below but marketed as a mutual fund. You can find your choice of Tangerine Core Balanced Portfolio (60% stocks, 40% bonds), Core Balanced Income Portfolio (70% bonds, 30% stocks), Core Balanced Growth Portfolio (75% stocks, 25% bonds), Core Equity Growth Portfolio (100% global stocks), and Core Dividend Portfolio (100% dividend stocks), depending on your risk/return profile and investing style.

Mutual fund fees

While cheaper than actively managed mutual funds, index mutual funds still tend to charge management expense ratios (MERs)—annual fees represented as a portion of your total account, deducted from your returns—that are higher than equivalent exchange-traded funds (ETFs). TD’s e-Series has MERs of 0.25% to 0.5%. Tangerine’s complete portfolios run just over 1%.

Mutual fund pros and cons

Compare the best TFSA rates in Canada

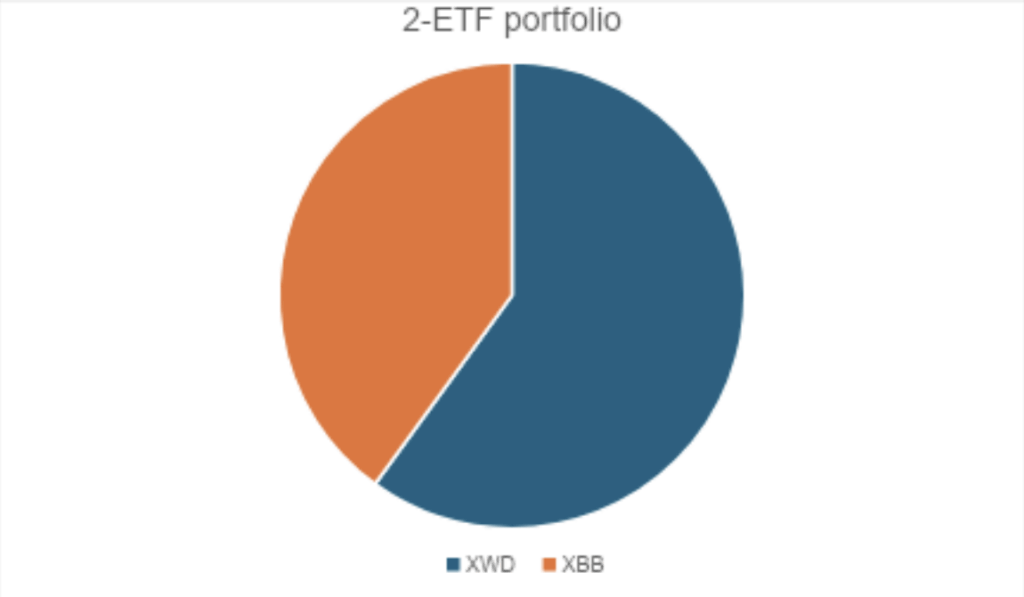

Option 2: Build an ETF portfolio

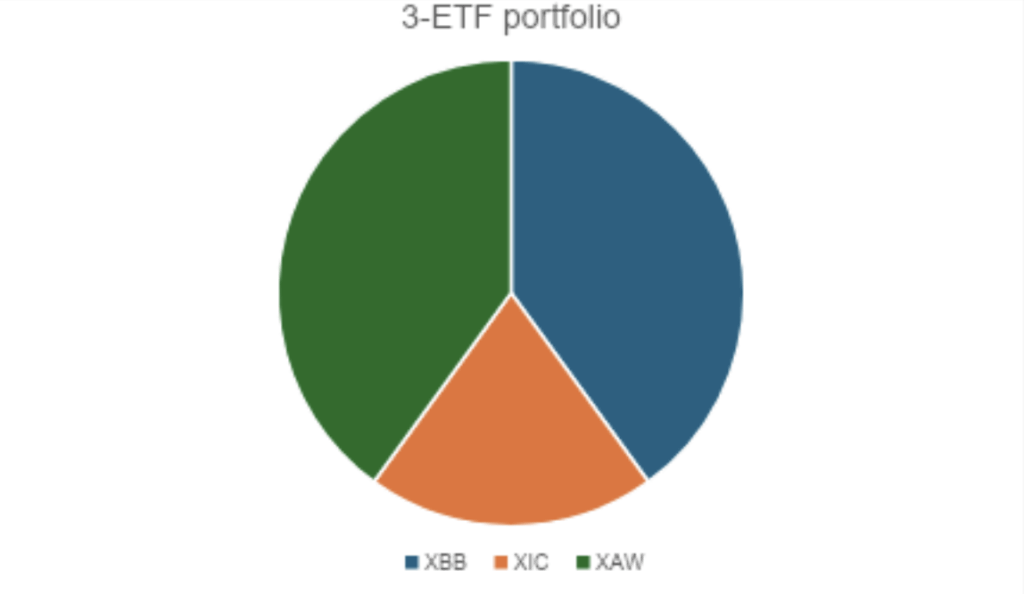

A core index ETF portfolio can consist of as little as two and up to four ETFs. Core exposures required include the U.S., Canadian, and International equities markets and domestic fixed income.

The sample portfolios here are balanced for moderate risk and return potential. More conservative and growth-oriented investors can adjust their portfolios to skew more towards fixed income or equities. See the section on asset-allocation ETFs below for examples.

Article Continues Below Advertisement

Your ETF options

The simplest approach is to buy a broad bond market fund such as iShares Core Canadian Universe Bond ETF (XBB) or Vanguard Canadian Aggregate Bond ETF (VAB) and a global equity ETF that takes in all geographies such as iShares MSCI World Index ETF (XWD). This will reduce your Canadian equity exposure to just 2% and raise your U.S. stock allocation to almost 40%—a good thing in some investors’ minds, bad in others’. Another potential downside is cost: global funds tend to have MERs of 0.2%, more than U.S. and Canadian equity funds. We have used iShares funds in the example below, but there are comparable offerings from BMO, Vanguard, TD, and Global X. For specific fund recommendations, check out MoneySense’s annually updated guide to the best ETFs.

Option 2b (below) features three funds: fixed income, global equities excluding Canada, and Canadian equity. This lets you set your own preferred level of Canadian content, as well as enjoy low Canadian equity ETF fees and tax efficiency if the account is taxable.

For the Canadian equity portion, we have chosen iShares Core S&P/TSX Capped Composite Index ETF (XIC). You can find more good Canadian equity ETF options in our ETFs guide. For Global equity, we used iShares Core MSCI All Cap World ex-Canada Index ETF (XAW). Again, you can find equivalents from rival fund companies such as Vanguard and BMO.

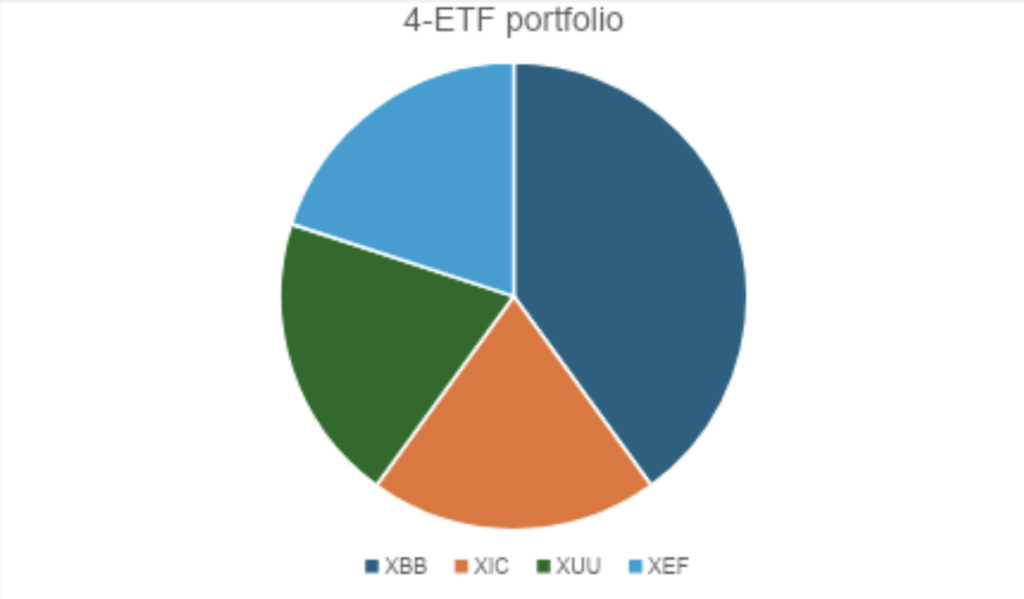

Option 2c takes in separate funds representing fixed income, U.S. equities, Canadian equities, and international equities (developed markets outside North America). The greater complexity brings with it potential cost savings, but also a greater need to monitor the portfolio and rebalance.

Along with XBB and XIC, we have sampled iShares Core S&P US Total Market Index ETF (XUU) and iShares Core MSCI EAFE IMI Index ETF (XEF). Find more suitable funds for these core positions in our most recent best U.S. Equity ETFs and best International Equity ETFs surveys.

ETF fees

Barring frequent trading that incurs brokerage fees, the index ETF portfolio is the lowest-cost approach available to couch-potato investors. Combined, your fixed income and equity allocations will have average MERs around 0.1% per year (slightly higher for international equity). You’ll barely notice it.

ETF pros and cons

Option 3: Buy an asset-allocation ETF

“Asset allocation ETF” is the term most often used in the investment industry, but they are variously known as one-ticket, all-in-one, one-decision and multi-asset ETFs. Essentially, they invest usually in the fund company’s own index ETFs to offer a whole portfolio’s worth of exposure in one investment. Just buy one, set your brokerage account preference to DRIP (dividend reinvestment program) so that quarterly distributions get invested in more units, and you really can “set it and forget it.”

Your asset-allocation ETF options

There isn’t a lot to separate the major ETF providers in the asset-allocation space. The bigger decision you have to make is where you want to fall on the risk/return spectrum. The most conservative option, for money you might need in the next year or two, is not to use a multi-asset fund at all, but instead one invested in high interest savings accounts (HISAs) or the money market. (See MoneySense’s best cash alternative ETFs for suggestions.)

An option is a contract to buy or sell a security for a specific price, called the strike price, on or before the option’s expiration date. Options are available for individual stocks, stock indexes, commodities and other securities. They trade on stock exchanges and can be bought and sold both through brokers and self-directed investing platforms.

Combined with more stock market chatter on social media and market volatility, options trading has gained steam with mom and pop Canadian investors. The trend truly picked up during the pandemic when many were stuck at home and has since continued, with options trading surging 89.4 per cent in 2023 compared with the year before, a World Federation of Exchanges report shows.

Social media and online commentary have pushed demand for options trading, said Josh Sheluk, portfolio manager at Verecan Capital Management. “People hear about how great somebody on Reddit has done with a specific options trade and they want to try to do the same thing and get very, very rich, very, very quickly,” Sheluk said. “It’s become very appealing.”