[ad_1]

Build your retirement savings with 1.50% interest, tax-deferred contributions and zero fees.

Earn a guaranteed 2.75% in your RRSP when you lock in for 1 year.

See our ranking of the best RRSP accounts and rates available in Canada.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Scotiabank reports $2.3B Q1 profit, up from $993M a year earlier

Bank of Nova Scotia (TSX:BNS)

Numbers for its first quarter:

- Profit: $2.30 billion (up from $993 million a year ago)

- Revenue: $9.65 billion (up from $9.37 billion)

The Bank of Nova Scotia reported $2.30 billion in first-quarter net income, up from $993 million a year earlier. The bank says the profit amounted to $1.73 per diluted share for the quarter ended Jan. 31, up from 66 cents per diluted share in the same period a year earlier.

Revenue totalled $9.65 billion, up from $9.37 billion.

Scotiabank says its provision for credit losses was $1.18 billion for the quarter, up from $1.16 billion a year earlier.

On an adjusted basis, Scotiabank says it earned $2.05 per diluted share in its latest quarter, up from $1.76 a year earlier.

The average analyst estimate had been for an adjusted profit of $1.95 per share, according to LSEG Data & Analytics.

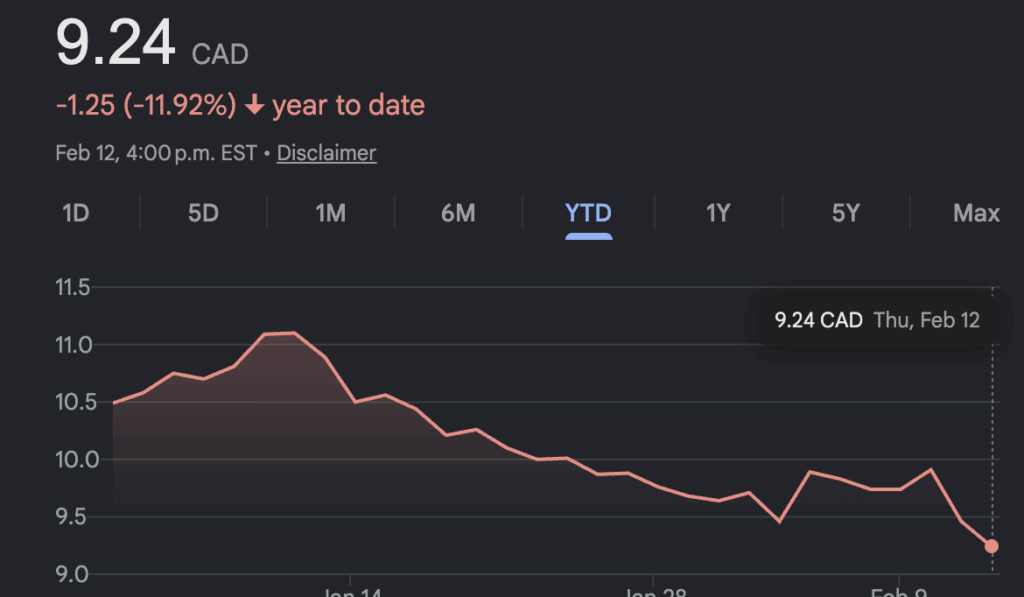

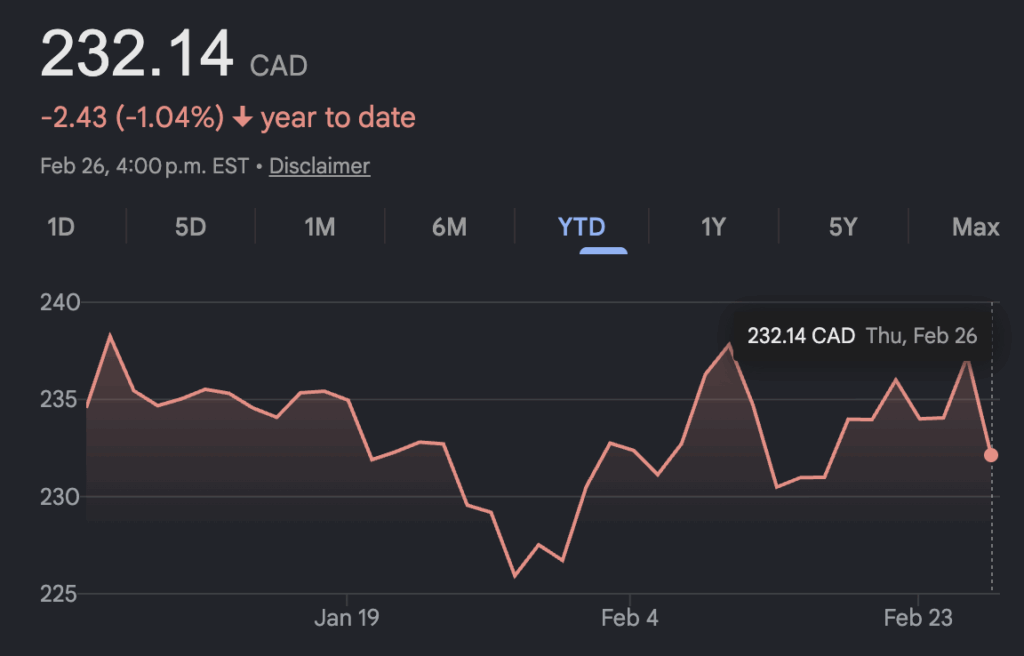

EQB reports lower first quarter adjusted net income of $85.2M, raises dividend

EQB (TSX:EQB)

Numbers for its first quarter:

- Profit: $85.2 million (down from $116.2 million a year ago)

- Revenue: $306.8 million (down from $322.6 million)

EQB Inc. reported adjusted net income of $85.2 million for the first quarter, down from $116.2 million during the same period a year earlier. On a per-share basis, that amounted to adjusted earnings of $2.26, down from $2.98 a year earlier.

The owner of EQ Bank says its adjusted net interest income came in at $263.4 million, down from $270.6 million in the prior year quarter.

EQB says its adjusted revenue was $306.8 million during the period, down year over year from $322.6 million.

Chadwick Westlake, the CEO of EQB, says the company is energized to close its acquisition of PC Financial, announced in December of last year, and partner with Loblaw Companies.

EQB also raised its dividend by 16% year over year, now sitting at 59 cents per common share.

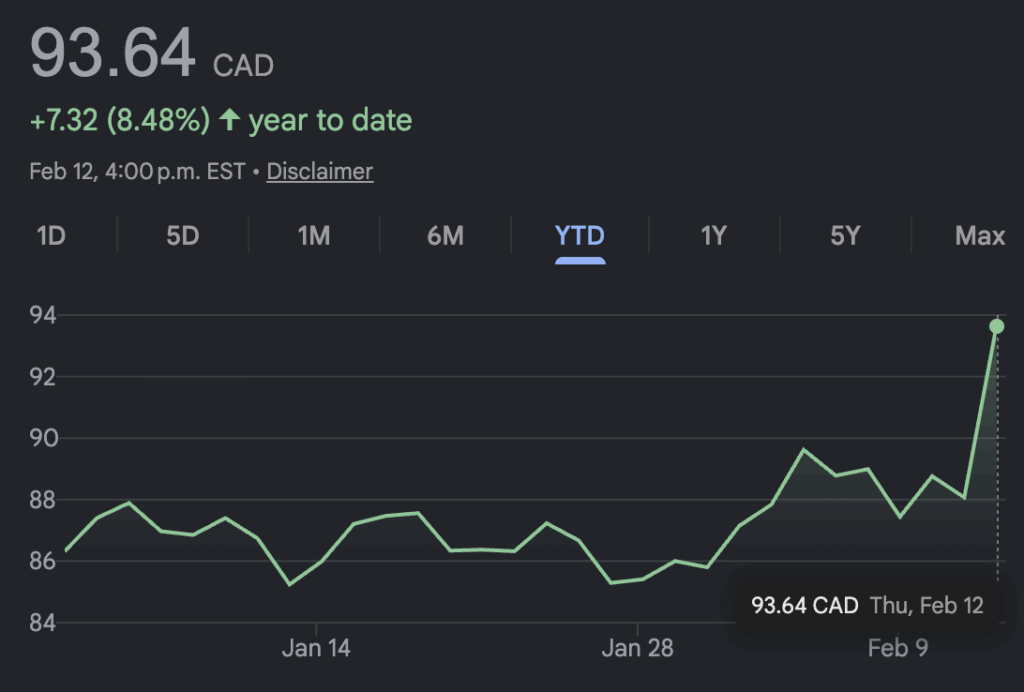

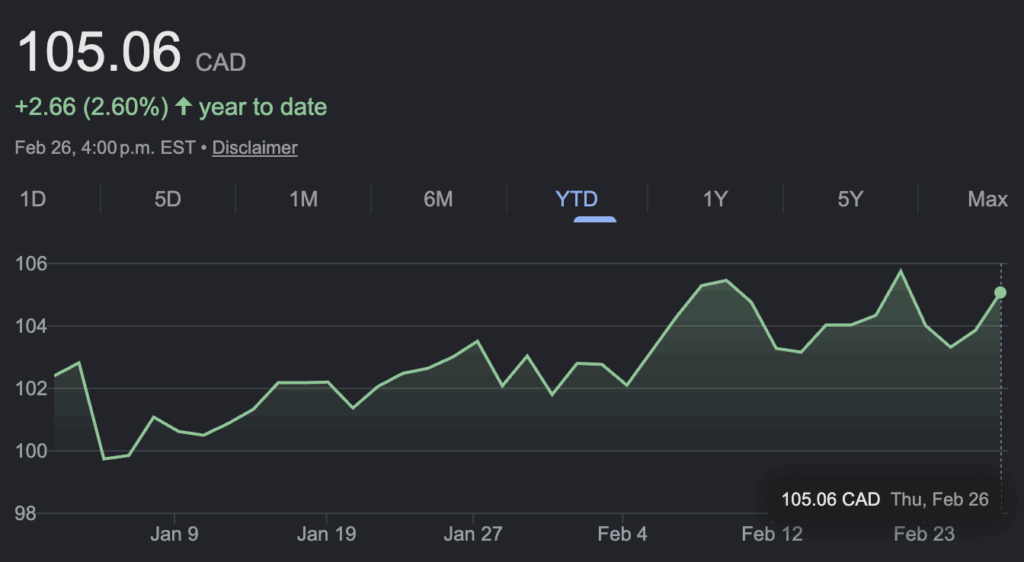

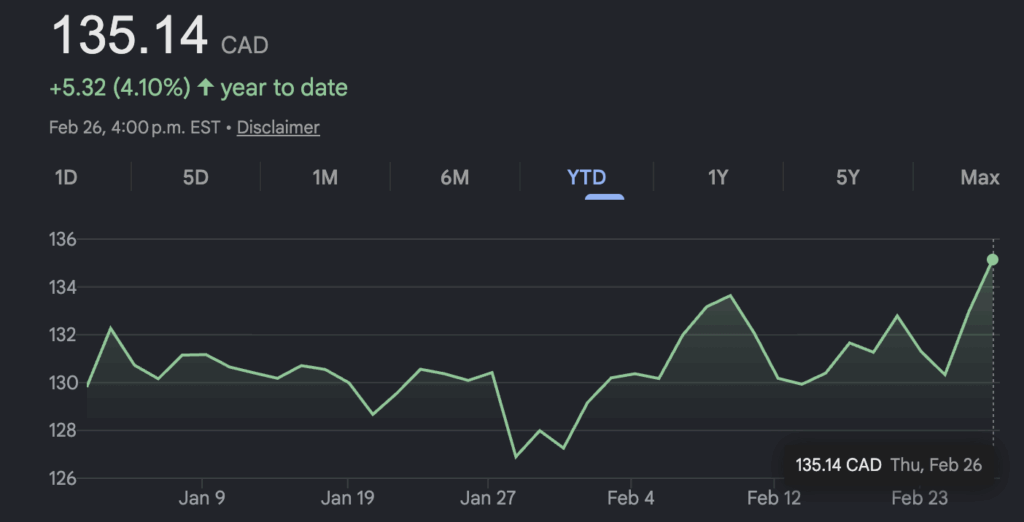

National Bank reports $1.25B Q1 profit, up from $997M a year earlier

National Bank of Canada (TSX:NA)

Numbers for its fourth quarter:

- Profit: $1.25 billion (up from $997 million a year ago)

- Revenue: $3.89 billion (up from $3.18 billion)

National Bank of Canada reported a first-quarter profit of $1.25 billion, up from $997 million a year earlier, helped by its acquisition of Canadian Western Bank. The bank says the profit amounted to $3.08 per diluted share for the quarter ended Jan. 31, up from $2.78 in the first quarter of 2025.

Revenue totalled $3.89 billion, up from $3.18 billion a year earlier.

National Bank’s provision for credit losses amounted to $244 million for the quarter, down from $254 million a year earlier.

On an adjusted basis, National Bank says it earned $3.25 per diluted share in its latest quarter, up from an adjusted profit of $2.93 a year earlier.

Analysts on average had expected an adjusted profit of $2.99 per share, according to LSEG Data & Analytics.

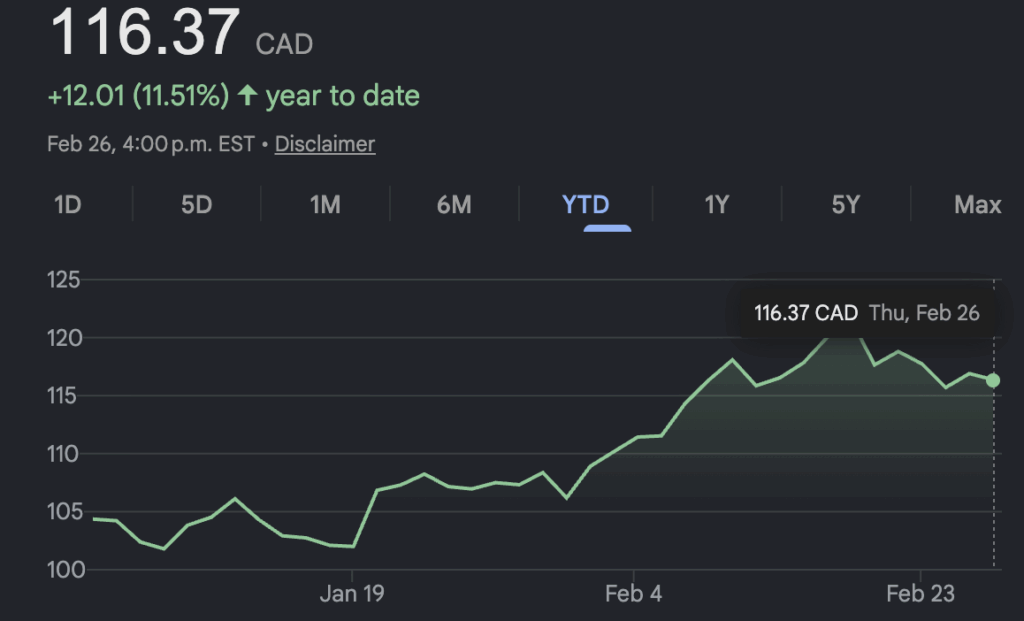

BMO Financial Group reports $2.49B Q1 profit, up from $2.14B a year earlier

BMO Financial Group (TSX:BMO)

Numbers for its fourth quarter:

- Profit: $2.49 billion (up from $2.14 billion a year ago)

- Revenue: $9.82 billion (up from $9.27 billion)

BMO Financial Group reported a first-quarter profit of $2.49 billion, up from $2.14 billion a year earlier. The bank says its profit amounted to $3.39 per diluted share for the quarter ended Jan. 31, up from $2.83 per diluted share in the same quarter last year.

Revenue for the quarter totalled $9.82 billion, up from $9.27 billion a year earlier.

The bank’s provisions for credit losses for the quarter amounted to $746 million, down from $1.01 billion.

On an adjusted basis, BMO says it earned $3.48 per diluted share in its latest quarter, up from an adjusted profit of $3.04 per diluted share a year earlier.

Analysts on average had expected an adjusted profit of $3.20 per share in the quarter, according to LSEG Data & Analytics.

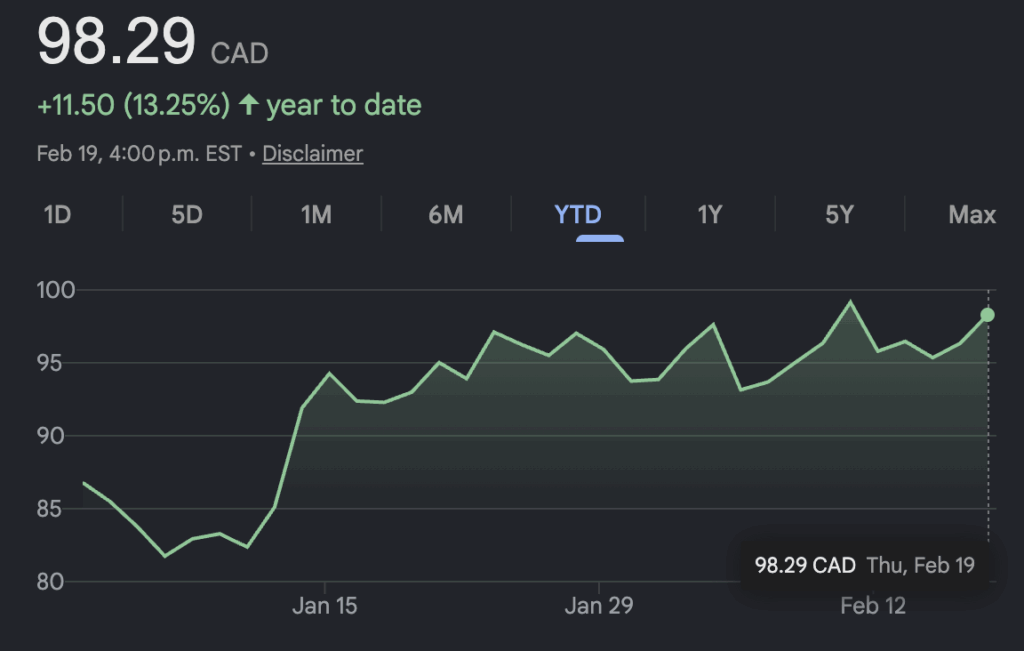

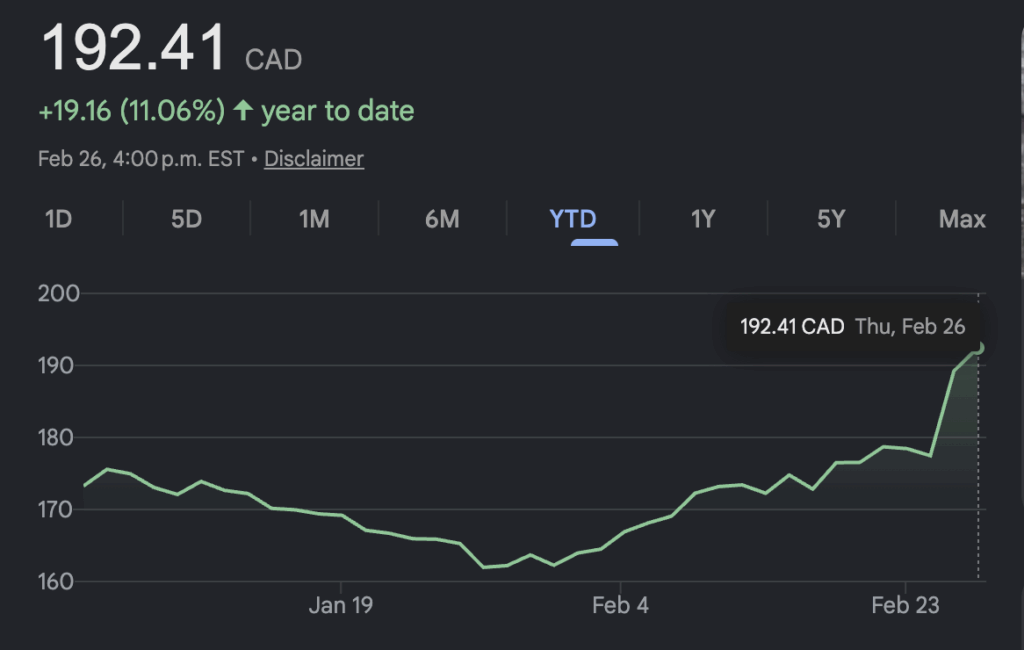

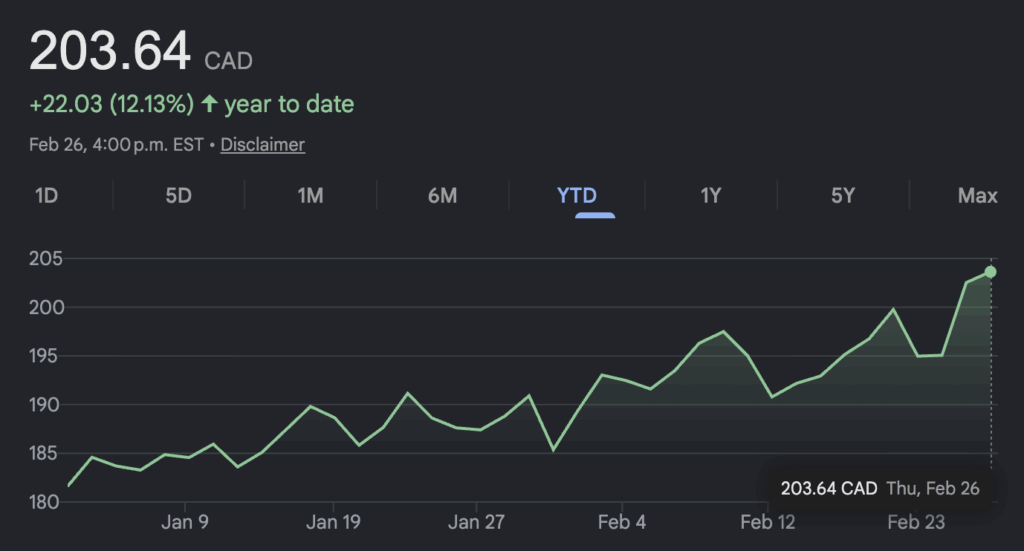

RBC reports $5.79B first-quarter profit, up from $5.13B a year earlier

Royal Bank of Canada (TSX:RY)

Numbers for its fourth quarter:

- Profit: $5.79 billion (up from $5.13 billion a year ago)

- Revenue: $17.96 billion (up from $16.74 billion)

Royal Bank of Canada reported a first-quarter profit of $5.79 billion, up from $5.13 billion a year earlier. The bank says the profit amounted to $4.03 per diluted share for the quarter ended Jan. 31, up from $3.54 per diluted share a year earlier.

Revenue totalled $17.96 billion, up from $16.74 billion.

RBC’s provision for credit losses for the quarter amounted to $1.09 billion, up from $1.05 billion a year earlier.

On an adjusted basis, the bank says it earned $4.08 per diluted share in its latest quarter, up from an adjusted profit of $3.62 per diluted share a year earlier.

The average analyst estimate had been for an adjusted profit of $3.85 per share, according to LSEG Data & Analytics.

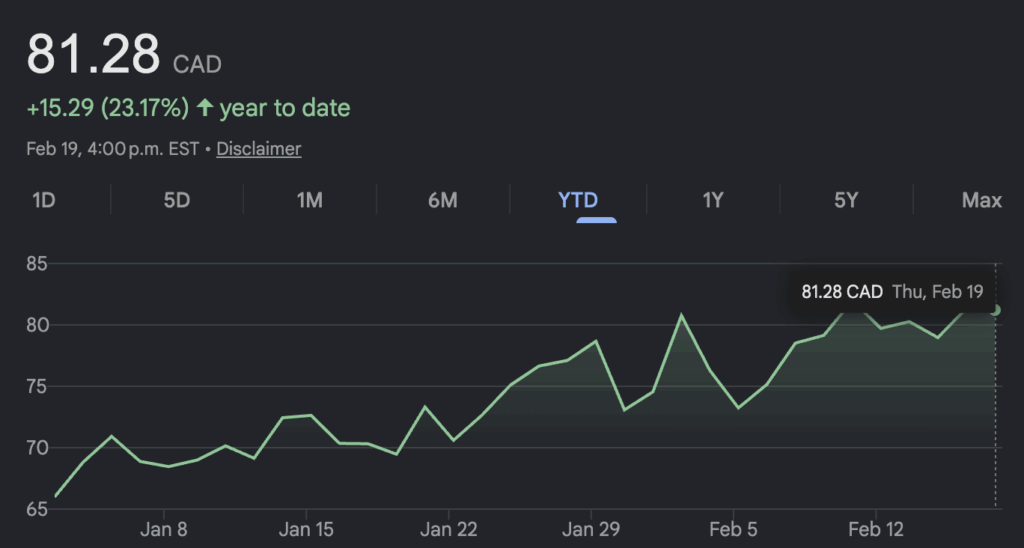

TD reports $4.04B Q1 profit, up from $2.79B a year earlier

TD Bank Group (TSX:TD)

Numbers for its fourth quarter:

- Profit: $4.04 billion (up from $2.79 billion a year ago)

- Revenue: $16.59 billion (up from $14.05 billion)

TD Bank Group reported a first-quarter profit of $4.04 billion, up from $2.79 billion a year earlier. The bank says the profit amounted to $2.34 per diluted share for the quarter ended Jan. 31, up from $1.55 per diluted share last year.

Revenue totalled $16.59 billion, up from $14.05 billion.

TD’s provision for credit losses amounted to $1.04 billion, down from $1.21 billion a year ago.

On an adjusted basis, TD says it earned $2.44 per diluted share in its latest quarter, up from $2.02 per diluted share a year earlier.

The average analyst estimate had been for a profit of $2.26 per share, according to LSEG Data & Analytics.

Tools

MoneySense’s ETF Screener Tool

Read more news:

- Stock news for investors: Mixed Q4 results with big profit gains for Enbridge, Nutrien, and Cenovus

- How often should you rebalance?

- What happens when you inherit an IRA or 401(k)?

- What replacing my tires taught me about planning for retirement

The post Stock news for investors: Big gains for Canada’s banks in Q1 appeared first on MoneySense.

[ad_2]

The Canadian Press

Source link