Editor’s Note: Sign up to get this weekly column as a newsletter. We’re looking back at the strongest, smartest opinion takes of the week from CNN and other outlets.

CNN

—

“Buy land,” the saying goes, “they’re not making it anymore.”

Variously attributed to Mark Twain and Will Rogers, the advice fits well with the national fixation on real estate, home values and location, location, location. The scarcity of land that can be developed – and surging demand for desirable locations – drove US median home prices over $400,000 for the first time last quarter before interest rate hikes started cooling the market.

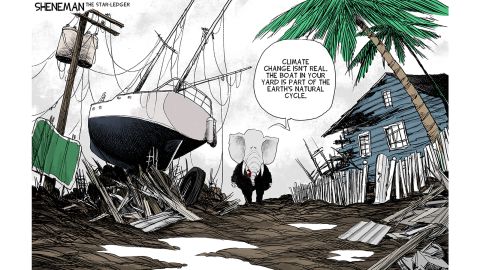

In Florida, a warm climate, expansive coastline and low taxes helped fuel a long-term boom, making it the third most populous state. As Hurricane Ian carved an awful path of destruction through the center of the state last week, the damage to people and property was severe. At least 66 people died, homes and businesses were destroyed and for many people, power may be out for weeks.

Florida tightened its building standards after the devastation wrought by Hurricane Andrew in 1992 but even with stronger structures, there’s little chance of avoiding catastrophic damage when 150 mph winds, torrential rain and steep storm surges hit a populated area.

“The simple fact is that when more people are exposed to a natural hazard such as a hurricane,” wrote Stephen Strader, an associate professor of geography and the environment at Villanova University, “the odds for a major disaster to occur are greater. As our population and built environment grows and expands, we are more readily placing ourselves in harm’s way. The wetlands and mangroves that once acted as natural ‘buffers’ to the rising waters and waves that come with hurricanes are now shrinking or gone. They have been replaced by subdivisions.”

Strader traces Florida’s boom back to the early 1910s, when “a man named Carl Fisher (best known as the automobile magnate responsible for building the Indianapolis Motor Speedway) decided to take a vacation on what is now known as Miami Beach.”

“He quickly realized the moneymaking opportunity at hand, buying, clearing and filling in thousands of acres of swamps and mangroves to make way for new waterfront property where investors would line up for the foreseeable future to build homes and hotels for those seeking a piece of paradise,” wrote Strader.

“There are very few things that test political leaders like natural disasters,” Julian Zelizer pointed out. “When mother nature wreaks havoc, presidents, governors, and legislators are forced to deploy resources to address the dire needs of those affected….”

“At the federal level, President Joe Biden needs to demonstrate he has the leadership and rigorous governing skills that are necessary to help Florida out of this mess,” Zelizer added. “At the state level, Gov. Ron DeSantis, who is billed as a potential Republican presidential nominee for 2024, needs to show that he can achieve more than political stunts like the one he orchestrated earlier this month when he sent migrants from Texas to Martha’s Vineyard.”

As Jack Shafer, writing for Politico, noted, DeSantis sounded a different tone this week, promising to work with the Biden administration to help his battered state recover. “In throttling back on the vitriol, DeSantis proves himself a wiser politician than (former President Donald) Trump, the man who reset politics in 2016 to establish senseless fight-picking and name-calling as part of the normal political arsenal and allowing somebody like DeSantis to rise. Trump, unlike DeSantis, never figured out how to turn off the meshugana theatrics, even when it could have benefited him. Imagine if, for example, Trump had approached the Covid crisis with the reassuring cool of Barack Obama instead of roasting the issue in a bonfire every time he called a presser. He might still be president today.”

Puerto Rico is still recovering from Hurricane Fiona, which was cited as a factor in at least 25 deaths, according to the island’s health department.

“Nearly five years to the day since Maria slammed our island, on September 18 of this year, Hurricane Fiona delivered yet another knockout punch,” wrote Brenda Rivera-García, senior director of Latin America and Caribbean programs for Americares.

“With Maria, we thought we experienced a 100-year flood. But, after only a half-decade later, it seems another century of water has enveloped us: Maria dumped more than three dozen inches of rain in some parts of the island over two days and last week Hurricane Fiona drowned us with 31 inches in a 72-hour period. A week after the storm, nearly 20% of the island was still without potable water, and nearly 60% still had no power, according to Puerto Rico’s government data. Once again, our air is filled with a familiar lullaby — the hum of generators.”

“More and more,” Rivera-Garcia added, “I hear from family, friends, neighbors and people on the street saying, ‘I’m tired. It’s one crisis after another. I can’t take it anymore.’ With multiple generations often living together, family members have always been each other’s rock. But what happens when that rock is shattered?”

Drew Sheneman/Tribune Content Agency

After conducting a series of votes widely viewed as a sham, Russia is moving to annex regions of eastern Ukraine, and President Vladimir Putin is warning that attacks on these territories would be viewed as an assault on Russia itself. He’s raised the fearsome prospect that tactical nuclear weapons could be used to defend what he now claims is part of the homeland.

That poses the huge question of how NATO should react. Hamish De Bretton-Gordon, former commander of the UK & NATO Chemical, Biological, Radiological and Nuclear (CBRN) Forces, said that “the West must make it absolutely clear to Putin that any use of nuclear, or chemical or biological weapons is a real redline issue. That said, I don’t think all-out nuclear war is at all likely.”

“NATO must direct that it will take out Russia’s tactical nuclear weapons if they move out of their current locations to a position where they could threaten Ukraine, and must also make clear that any deliberate attacks on nuclear power stations will exact an equal and greater response from NATO.”

“This is the time to call Putin’s bluff. He’s hanging on by his fingertips, and we must give him no chances to regain his hold. Russia’s forces are now so degraded that they are no match for NATO and we should now negotiate, with this in mind, from this position of strength.”

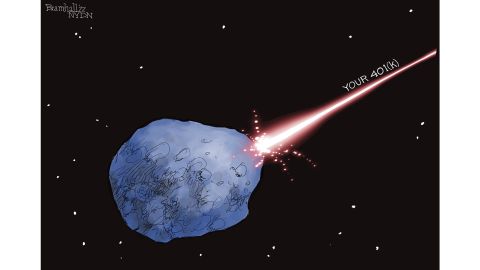

The UK’s new prime minister, Liz Truss, and the Chancellor of the Exchequer Kwasi Kwarteng played starring roles in a week of market turmoil around the globe.

As Frida Ghitis observed, “In the midst of a wave of inflation that is battering the world and prompting central banks to raise interest rates in hopes of cooling inflationary pressures, Truss’ plan to slash taxes, especially for the wealthiest, amounted to opening a firehose filled with gasoline into that raging economic fire.” The pound tumbled, nearly reaching parity with the dollar, and the Bank of England had to announce it would buy bonds to restore confidence.

“Economists and politicians left and right largely agreed that, if not the policy itself, the abrupt rollout and the timing could not have been worse…”

“They came at a moment when the world – and the West – stands on a knife’s edge, with Russian President Vladimir Putin annexing large pieces of Ukraine and hinting at using nuclear weapons as his invasion falters. With mysterious explosions causing leaks in the Nordstream pipeline applying further anxiety just ahead of a dreaded winter with gas supply shortages across Europe, all of this is happening when democracy finds itself under pressure the world over.”

The prime minister’s policy is far from the only thing unsettling investors, as central banks around the world aim to tame inflation with rising interest rates, a strategy that risks choking off economic growth.

Bill Bramhall/Tribune Content Agency

Bill Carter has a confession to make: he has not read all the books about Donald Trump.

“I can’t even remember all the books about Donald Trump,” he wrote.

“I know Bob Woodward has written three. So has Michael Wolff. Sean Spicer wrote one (or was it two?). “Mooch” – that is, Anthony Scaramucci, Trump’s White House communications director ever so briefly – wrote one. So did Omarosa, for heaven’s sake.”

“This week marks the release of yet another: New York Times journalist Maggie Haberman’s ‘Confidence Man: The Making of Donald Trump and the Breaking of America.’” Carter cited a New York Times reference to an analysis by NPD BookScan, which found more than 1,200 titles about Trump were released over four years – not including the avalanche of books published since the 2020 election.

“The robust sales for many of these books attest to the hunger among readers to hear every gobsmacking detail about a real-life character who is beyond the imagination of most fever-dreaming fiction writers.”

“But even ravenous levels of hunger can be sated – eventually. After seven or eight – or 12 – courses, a bit of bloat is likely to set in … Every book seems to contain a sufficient number of ‘bombshell revelations’ to drum up media coverage, along with some combination of amusing, enraging or revolting personal details (previously unreported, of course, and almost always disputed by the former president)…”

But do they have an impact anymore? A “defining aspect of the collected works on Trump,” Carter concluded, “is that virtually nothing in any of them – none of the ‘bombshells’ or details about his character – seems to have substantially changed people’s minds about him. That may be because Trump acolytes don’t tend to read critical accounts about him – and his opponents aren’t likely to read the hagiographies.”

SE Cupp noted a Vanity Fair report that lifted the curtain on the rivalry between DeSantis and Trump, which included this description of Trump attributed to the governor: “A TV personality and a moron, who has no business running for president.”

“The love loss seems to go both ways. According to reporting by Maggie Haberman, Trump has called DeSantis ‘fat,’ ‘phony,’ and ‘whiny.’”

“As is often the case,” Cupp observed, “the courage to criticize Trump – even among Republicans who might want to run against him – is almost always reserved for private conversations. When will DeSantis get the spine to attack Trump frontally?”

As the Supreme Court begins its new term Monday, the reverberations of its June decision on abortion are still playing out. As Fareed Zakaria wrote, “The Court has been growing more ideologically predictable – that is, politically partisan – in recent years. Judges appointed by Republicans now almost always rule in ways that Republicans want them to. Ditto for judges appointed by Democrats. It is all part of the hyper-polarization of American life.”

“But it is also partly because of the strange way in which America’s highest court is structured,” observed Zakaria, who noted that “no other major democracy gives members of its highest court life tenure.”

The court “has moved in a direction that has weakened its own legitimacy. It might be an occasion to begin a national conversation about what reforms could be put in place to make it less partisan, less divisive and more trusted by the vast majority of citizens. After all, that is the only way its rulings will be truly accepted in a diverse democracy of more than 330 million people.” (Watch Fareed Zakaria’s special report Sunday at 8 p.m. ET and PT: “Supreme Power: Inside the Highest Court in the Land.”)

For more:

Jill Filipovic: This Texas Republican in full sprint is a metaphor for the GOP’s stance on abortion

Steve Vladeck: America’s most powerful court owes the public an explanation

One morning in 2016, Eric Adams, a former police officer turned politician – and now New York’s mayor – couldn’t see the numbers on his alarm clock.

“I went to the doctor, who diagnosed me with Type 2 diabetes. He told me I might have my driver’s license revoked due to vision loss, and I might have permanent nerve damage in my fingers and toes.”

After googling “reversing diabetes,” he connected with “Dr. Caldwell Esselstyn at the Cleveland Clinic, who told me I could treat my diabetes with lifestyle changes, including overhauling my diet and exercising.

“I was skeptical at first. But reducing meat and dairy consumption in favor of fresh produce and grains made an immediate difference in my health … Within three months, I lost significant weight, lowered my cholesterol, restored my vision and reversed my diabetes.” But not everyone has the resources to get expert medical advice and turn their health around so dramatically.

“The disproportionate effect of Covid-19 on Black and brown communities was tragically compounded by existing diet-driven health disparities. While higher-income neighborhoods have overwhelming options when it comes to fresh fruits and vegetables, low-income communities of color often live in nutritional deserts with fewer grocery stores and a higher concentration of processed foods, sugary drinks, and shelf-stable products…”

“Now is the time for our country to make the shift from treatment to prevention, from feeding the illness to giving people the tools to build sustainable lifestyles and healthier, stronger communities.”

Dana Summers/Tribune Content Agency

Michael Fanone: What my January 6 assailant deserves

Ruth Ben Ghiat: Casting doubt on Brazil’s election, Bolsonaro follows Trump’s lead

Matthew Bossons: My 5-year-old just confirmed our decision to leave China

Peter Bergen: The British Empire – A legacy of violence?

AND…

Bill Bramhall/Tribune Content Agency

To fans of the New York Yankees, there’s an almost mystical connection uniting the team’s pantheon of heroes – including Babe Ruth, Lou Gehrig, Joe DiMaggio, Mickey Mantle, Roger Maris and Derek Jeter. And now by hitting 61 homers in a single season – tying Maris, who bested Ruth’s record of 60 home runs – Aaron Judge has arguably joined those ranks.

As Billy Crystal’s 2001 movie, “61*” made clear, though, those ties have long been frayed – Mantle and DiMaggio had a frosty relationship and there were tensions between Mantle and Maris. But if you widen the lens beyond the Yankees and look at the entire history of Major League Baseball, as Jeff Pearlman wrote, the picture surrounding Judge’s achievement is even more clouded.

“By allowing rampant steroid and human growth hormone usage throughout the 1990s and early 2000s,” Pearlman observed, “Major League Baseball ruined and disgraced its own record book, and Judge’s shot merely (yawn) tied the American League home run mark.”

“When, in 2001, San Francisco’s Barry Bonds broke (Mark) McGwire’s record with 73 homers, we all knew it was nonsense. Not some of us – all of us. Here was a man, at age 36, with muscles growing atop muscles and a skull size that – as I reported in my Bonds biography, “Love Me Hate Me” – had actually increased in recent years (this is physically impossible without the help of HGH). I was in San Francisco the night Bonds passed McGwire, and it was…stupid. Just so damn stupid. The local fans stood and cheered, but it felt flat and meaningless and a bit embarrassing. Like spotting a magician’s fake thumb.”

“All the while, Major League Baseball and the Major League Baseball Players Association did … nothing. Home runs were great business, so team owners shrugged off PED suspicions while the union made clear it would refuse to have its players be tested in any sort of methodical, impactful manner. The result was temporary long ball excitement, followed by the quiet-yet-crushing realization (by most involved in the game) that the record book had been rendered meaningless.” Eventually, baseball woke up and instituted testing for performance enhancing drugs.

As for Aaron Judge, according to Pearlman, “the 30-year-old slugger has had a season for the ages – he’s all but locked up the AL MVP award, and at this moment is in line to become the Yankees’ first triple crown winner since Mickey Mantle in 1956.

“This should be an historic time for baseball.

“This should be an historic time for Aaron Judge.

“Instead, greed destroyed baseball – and took its history with it.”