A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN Business

—

Tuesday’s midterm elections come at a time of economic vulnerability for the United States. Recession predictions have largely turned to “when” not “if” and inflation remains stubbornly elevated. Americans are feeling the pain of rising interest rates and are facing a winter filled with geopolitical tension.

The results of Tuesday’s election will determine the makeup of a Congressional body that holds the potential to enact policies that will fundamentally change the fiscal landscape.

Here’s a look at what policy issues investors will pay particular attention to as they digest election results.

Tax changes: Last week, President Joe Biden suggested he may impose a windfall tax on Big Oil companies after they recorded record profits on high gas prices. Republicans would be less likely to approve that windfall tax on oil company profits and also are generally not in favor of tax hikes on the wealthy, reports my colleague Paul R. La Monica.

“What do midterms mean for the markets? If Republicans get the House, tax hikes are dead in the water,” said David Wagner, a portfolio manager with Aptus Capital Advisors.

What about tax cuts? If Republicans do take control of Congress, it would be difficult to enact any major tax reductions without some backing from Democrats or President Biden, meaning there could be grandstanding without much action.

Debt limit: The federal debt ceiling was last lifted in December 2021 and will likely be hit by the Treasury at some point next year. That means it will need to be raised againin order to ensure that America can borrow the money it needs to run its government and ensure the smooth operation of the market for US Treasuries, totalingroughly $24 trillion.

A fight seems to be brewing between Democrats and Republicans. House Republicans indicate that they may ask for steep spending cuts inexchange for boosting the ceiling.

If the government ends up divided and brinkmanship continues, there could be bad news for markets. The last time such gridlockoccurred, under the Obama administration in 2011, the United States lost its perfect AAA credit rating from Standard & Poor and stocks dropped more than 5%.

Spending: Democrats have indicated that they intend to focus on parts of the fiscal agenda proposed by President Biden in 2021 that have not yet become law, including expanding health coverage and child care tax credits. A Republican win or gridlock could table that. Goldman Sachs economists also note that a Democratic victory could likely increase thefederal fiscal response in the event of recession, while Republicans would be more likely to avoid costly relief packages.

Social Security: Popular programs like Social Security and Medicare face solvency issues long-term and the topic has become a hot-button issue on both sides of the aisle. The topic is so closely watched that even debating changes could impact consumer confidence, say analysts.

Democratic Senator Joe Manchin said last week that spending changes must be made to shore up Social Security and other programs which he said were “going bankrupt.” He said at a Fortune CEO conference that he was in favor of bipartisan legislation within the next two years to confront entitlement programs that are facing “tremendous problems.” Republican Senator Rick Scott has proposed subjecting almost all federal spending programs to a renewal vote every five years. Analysts say that could make Social Security and Medicare more vulnerable to cuts.

The Federal Reserve: Lawmakers have been increasingly speaking out against the pace of the Federal Reserve’s interest rate hikes meantto fight inflation. Democratic Senators Elizabeth Warren, alongside Banking Chair Sherrod Brown, John Hickenlooper and others have called on Fed Chair Jerome Powell to slow the pace of hikes.

Now, Republicans are getting involved. Senator Pat Toomey, the top Republican on the Banking Committee, asked Powell last week to resist buying government debt if market conditions remain subdued. Expect more scrutiny from both parties after the elections.

The stock market under President Biden started with a boom, but as we head into midterm elections, markets are going bust, reports my colleague Matt Egan.

As of Monday, the S&P 500 has fallen by 1.2% since Biden took office in January 2021. That marks the second-worst performance during a president’s first 656 calendar days in office since former President Jimmy Carter, according to CFRA Research.

Out of the 13 presidents since 1953, Biden ranks ninth in terms of stock market performance through this point in office, besting only former Presidents George W. Bush (-32.8%), Carter (-8.9%), Richard Nixon (-17.2%) and John F. Kennedy (-2.1%), according to CFRA.

By contrast, Biden’s two immediate predecessors headed into their first midterm election with stock markets surging. The S&P 500 climbed 52.2% during the first 656 calendar days in office for former President Barack Obama and 23.9% under former President Donald Trump, according to CFRA.

American consumers borrowed another $25 billion in September, according to newly released Federal Reserve data, as higher costs led to further dependence on credit cards and other loans, reports my colleague Alicia Wallace.

In normal economic times, that would be a concerningly large jump, said Matthew Schulz, chief credit analyst for LendingTree, wrote in a tweet. “However, it is actually the second-smallest increase in the past year.” Economists were anticipating monthly growth of $30 billion, according to Refinitiv consensus estimates.

The data is not adjusted for inflation, which is at decade highs and weighing heavily on Americans, outpacing wage gains and forcing consumers to rely more heavily on credit cards and their savings.

In the second quarter of this year, credit card balances saw their largest year-over-year increases in more than two decades, according to separate data from the New York Federal Reserve. The third-quarter household debt and credit report is set to be released Nov. 15.

Correction: A previous version of this article incorrectly stated the number of calendar days in the analysis as well as the stock market performance under various US presidents during that period.

One of the reasons for the record $1.9 billion jackpot for the Powerball drawing Monday night is something you wouldn’t expect — the recent run of steep interest rate hikes from the Federal Reserve.

That’s because the size of the advertised $1.9 billion top prize is the amount winners would get, which involves taking 30 equal payments of about $63 million spread out over the next 29 years. Those payments come from an annuity purchased by the lottery sponsors, and the payments factor in an average rate of return

But the thing is, the real prize is far more likely to be a much smaller lump sum, the “cash value” – in this case $929.1 million – that never gets any attention.

“All anyone ever talks about is the annuity prize,” said Victor Matheson, professor of economics and accounting at the College of the Holy Cross in Massachusetts. “It’s the number the lotteries market. It’s the number in the news story. But it’s the number that almost no one ever takes.”

No Powerball winner since 2014 has chosen the “larger” annuity amount over the cash prize.

The cash value is the amount the prize would actually cost the lottery, either in a lump-sum payment now, or to buy an annuity to make those 29 subsequent payments. The current environment of rising interest rates has opened the door to ever-larger annuity payments.

In the low interest rate environment of recent years, the advertised annuity price was only about 50% or 60% bigger than the cash value, or sometimes less.

The largest Powerball jackpot ever won was in January 2016 when three winners split a prize advertised at $1.586 billion. Each took their share of the cash value, which added up to $983.5 million, which was $54.4 million more than cash prize in Monday’s “record” drawing.

That advertised then-record annuity prize was 61% greater than the cash prize. This time, the estimated annuity prize is 104% greater than the cash prize. If it was the same ratio as in 2016, Monday’s annuity prize would be only $1.5 billion.

And interest rates were as low as they were in January of this year, Monday’s annuity rate would be only $130 million.

The current prize assumes a return on the cash value of about 5.75% a year, Matheson said.

But even a conservative investor in stocks could likely do better by taking the money up front and investing it, not withstanding the swings in the stock market. The Standard & Poor’s 500 has risen 728% in the 29 years since October 1993, or a compounded annual average growth rate of about 7.5%. The larger assumed return associated with Monday’s annuity prize might make it more attractive to the next big winner or winners, said Matheson.

Then again, a disinclination to accept deferred gratification could overcome any investment assumptions or tax planning that goes into the winner’s calculations.

Nick Jones, equity research analyst at JMP securities, joins ‘Power Lunch’ to discuss Opendoor’s warning, the cash needed to navigate near term headwinds and forces needed to normalize the housing market.

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN Business

—

What will the Federal Reserve do at its meeting in December? Analysts can speculate all they want, but Fed officialssay they will be using hard economic data to make their next decision.

That means key housing, labor, and inflation reports will likely have outsized effects on the market as investors speculate about what they might mean for the future of interest rates.

What’s happening: No one can move markets like Federal Reserve Chair Jerome Powell — with just a few words on Wednesday he crushed investors’ hopes of an interest rate pivot and sent stocks plunging. “We have a ways to go,” said Powell of the Fed’s current hiking regime meant to fight persistent inflation. “It’s very premature, in my view, to think about or be talking about pausing.”

But Powell did add an important caveat. The Fedcould start to slow the pace of those painful hikes as soon as December. “Our decisions will depend on the totality of incoming data and their implications for the outlook for economic activity and inflation,” Powell said on Wednesday.

So what will the Fed be looking at between today and itsnext policy decision on December 14?

The labor market: The Fed’s biggest worry is the super-tight US labor market, and Friday’s jobs report isn’t likely to soothe any nerves.

The government report is expected to show the economy added another 200,000 positions in October — down from last month, but still a very solid number as demand for employment continues to outpace the supply of labor.

That means more inflation. Businesses have to pay higher wages to attract employees and are able to charge more for their goods and services. The Fed will be looking closely at hourly wage growth in the report. In September, wages rose by 5% from a year ago.

There is a possible upside: Another jobs report in December is expected ahead of the Fed meeting. If both reports show a downward trajectory in employment, that could be enough to placate Fed officials, even if the unemployment rate remains historically low.

Inflation data: Expect new data from two major indexes that measure the pace of inflation ahead of the next Federal Reserve meeting.

The Consumer Price Index (CPI) for October, which tracks changes in the prices of a fixed set of goods and services, is out on November 10.

Core CPI prices, which exclude oil and food, rose 0.6% in September month-over-month, matching August’s pace and coming in well above expectations of a 0.4% increase, not a great sign for the Fed. And analysts expect to see another large 0.5% increasein October.

The Fed will also get to see October data from its favored measure of inflation, Personal Consumption Expenditures (PCE), on December 1.

PCE reflects changes in the prices of goods and services purchased by consumers in the United States. The Fed believes the measure is more accurate than CPI because it accounts for a wider range of purchases from a broader range of buyers.

Housing: The housing market has been deeply impacted by the Fed’s efforts to fight inflation, and is one of the first areas of the economy to show signs of cooling.

The 30-year fixed-rate mortgage averaged 6.95% last week, up from 3.09% just a year ago, and elevated borrowing costs are leading to a decline in demand.

“The housing market was very overheated for the couple of years after the pandemic as demand increased and rates were low,” said Powell on Wednesday. “We do understand that that’s really where a very big effect of our policies is.”

October’s new and existing home sales numbers, due on November 18 and 23, will show the continued impact of that policy ahead of the next meeting.

The US economy is still standing strong in the face of rising interest rates, but things are softening much more quickly across the pond.

The United Kingdom will face hard economic times and elevated interest rates well into next year, officials warned this week.

The Bank of England raised interest rates by three-quarters of a percentage point on Thursday, the biggest hike in 33 years, as it attempts to fight soaring inflation.

But the bank also issued a stark warning. It said that economic output is already contracting and that it expects arecession to continue through the first half of 2024 “as high energy prices and materially tighter financial conditions weigh on spending.”

A two-year recession would be longer than the one that followed the 2008 global financial crisis, though the Bank of England said that any declines in GDP heading into 2024 would likely be relatively small.

The central bank also doesn’t think inflation will start to fall back until next year. That will require more interest rate hikes in the coming months, warned policymakers.

Elon Musk has been busy over at Twitter HQ. Aside from tweeting and deleting a conspiracy theory, he’s talked about implementing some big changes at his $44 billion acquisition. Here’s what’s happened so far:

Layoffs begin: Elon Musk began laying off Twitter employees on Friday morning, according to a memo sent to staff. The email sent Thursday evening notified employees that they will receive a notice by 12 p.m. ET Friday that informs them of their employment status.

The email added that “to help ensure the safety” of employees and Twitter’s systems, the company’s offices “will be temporarily closed and all badge access will be suspended.”

Twitter had around 7,500 employees prior to Musk’s takeover.

Several Twitter employees have already filed a class action lawsuit claiming that the layoffs violate the federal Worker Adjustment and Retraining Notification Act.

The WARN Act requires any company with over 100 employees to give 60 days’ written notice if it intends to cut 50 jobs or more at a “single site of employment.”

Consolidating strength: In less than a week since Musk acquired Twitter, the company’s C-suite appears to have almost entirely cleared out, through a mix of firings and resignations.

Twitter’s board of directors was also dissolved last week, according to a securities filing.

The company filing states that all previous members of Twitter’s board, including recently ousted CEO Parag Agrawal and chairman Bret Taylor, are no longer directors “in accordance with the terms of the merger agreement.” That makes Musk, according to the filing, “the sole director of Twitter.”

Cashing blue checks’ checks: Musk on Tuesday said he planned to charge $8 a month for Twitter’s subscription service, called “Twitter Blue,” with the promise to let anyone pay to receive a coveted blue check mark to verify their account. That’s a steep haircut from his original plan to charge users $19.99 a month to get or keep a verified account.

In a tweet, the world’s richest man used an expletive to describe his assessment of “Twitter’s current lords & peasants system for who has or doesn’t have a blue checkmark.” He added: “Power to the people! Blue for $8/month.”

Advertisers hit pause: Elon Musk wrote an open letter to advertisers just hours before cementing his acquisition of Twitter, explaining that he didn’t want the platform to become a “free-for-all hellscape.” But that attempt at reassuring the advertising industry, which makes up the vast majority of Twitter’s business, doesn’t appear to be working.

General Mills

(GIS), Mondelez International

(MDLZ), Pfizer

(PFE) and Audi

(AUDVF) have reportedly joined a growing list of companies hitting pause on their Twitter advertising in the wake of Musk’s acquisition.

The Labor Department reported a drop in jobless claims for the week ending Oct. 29. This comes as the Federal Reserve hiked interest rates this week in an effort to tame rising inflation. Nick Bunker, economic research director for the Indeed Hiring Lab, joined CBS News to help bring clarity to the state of the economy and project what could be next.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

Home sales across the country over the last eight months are down as the Federal Reserve raises interest rates. Rising mortgage rates are shrinking the number of people who can get a loan and buy a home. Lilia Luciano takes a look.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

Britain’s central bank warned on Thursday that the U.K. is facing its longest-ever recession, and it predicted the country’s unemployment rate could double by 2025. The Bank of England’s announcement came as it raised the base interest rate from 2.25% to 3%, giving it the most significant hike in 33 years amid dire economic forecasts.

Inflation has been soaring in the United Kingdom at its fastest rate in decades, with food and energy prices exploding, due in part to Russia’s invasion of Ukraine. The bank believes that by raising its benchmark interest rate, and thus increasing the cost of debt, including mortgages, it will encourage people to stop spending money and contribute to lowering prices.

Bank boss Andrew Bailey acknowledged a “tough road ahead,” and he warned that action had to be taken now by the government or things “will be worse later on.”

The European Union has been hit hard by the energy price hikes caused by the war in Ukraine. Central banks around the world are struggling to contain rising inflation, which has stuck around longer than many pundits predicted and is contributing to demands for wage increases. But the U.K. has fared worse than its neighbors thanks to factors including the ongoing fallout from Brexit, Britain’s break with the European Union and a recent period of political turmoil that sapped investor confidence in the country and devalued the pound.

“The most important thing the British government can do right now is to restore stability, sort out our public finances, and get debt falling so that interest rate rises are kept as low as possible,” said U.K. Finance Minister Jeremy Hunt.

The Bank of England made its largest interest-rate increase in three decades in response to inflation that the central bank still expects to accelerate.

By a 7-to-2 vote, the U.K. central bank voted to lift rates by a three-quarters percentage point to 3%, as inflation hit a 40-year high in September. The central bank said inflation will further accelerate to 11% in the fourth quarter.

There was one vote, from Swati Dhingra, for a half-point increase, and another, from Silvana Tenreyro, for a quarter-point rise. Both are external members of the central bank’s monetary policy committee.

It was the first gyrations since the turmoil in financial markets that prompted the BOE to step in with a temporary bond purchase program.

“These had partly reflected global developments, although U.K.-specific factors had played a very significant role during this period,” the central bank dryly said of the market reaction to the tax-cut proposals produced by Prime Minister Liz Truss and Chancellor of the Exchequer Kwasi Kwarteng, both of whom have resigned.

The U.K. central bank has now started a delayed bond selling program, and Chancellor Jeremy Hunt has backtracked on the tax-cut proposals as he readies a new “autumn statement” due in mid-November.

The pound dropped despite the central bank matching the Fed’s three-quarter point rate hike. That’s because of a comment found within the minutes of the meeting, that a majority felt rates would not have to go as high as the implied 5.25% path in financial markets.

The pound GBPUSD, -1.92%

was weaker on the day at $1.1235 from $1.1392 — though much of that move came before the actual BOE decision — while the 2-year gilt TMBMKGB-02Y, 3.029%

rose 10 basis points to 3.08%.

“This will most likely mark the peak in pace of tightening, especially with the Bank highlighting financial markets are pricing too much too soon. Next up for the U.K. will see the focus shift to the autumn statement to see what the chancellor’s fiscal plans are, but in the meantime the headlines point to gilts being relatively more supported, however the currency less so,” said Edward Hutchings, head of rates at Aviva Investors.

Tim Graf, head of EMEA macro strategy at State Street, said the peak rate is likely to be closer to 4% to 4.25%.

“The accompanying messaging was clearly dovish, with the MPC noting the economy was already in the midst of a recession it expects to last into 2023, that inflation will likely fall sharply over the next two years and citing pricing for terminal rates as likely too high, limiting the need to hike aggressively,” he said.

Inflation in Turkey rose for the 17th consecutive month in October, hitting 85.5% year-on-year as food and energy prices continued to climb, according to official figures.

Food prices were 99% higher than the same period last year, housing rose by 85% and transport was up 117%, the Turkish Statistical Institute reported Thursday.

The domestic producer price index shows a 157.69% increase annually and was up 7.83% on a monthly basis. The monthly rise in consumer prices was 3.54%.

The dramatic rise in living costs for the country of 85 million has continued unabated for nearly two years, in tandem with significant devaluation of Turkey’s currency, the lira.

Controversially, Turkish President Recep Tayyip Erdogan refuses to raise interest rates, insisting that it would harm the economy. Economists and critics say his policies have continued to hurt the lira and push inflation up, fomenting a currency crisis.

Turkey’s central bank on Oct. 20 slashed its key interest rate by 150 basis points for the third consecutive month of cuts, from 12% to 10.5% — despite Turkish inflation at more than 83% at the time.

Erdogan says the cuts are pro-growth, and that they will continue. The president remains determined to get the country’s interest rate down to single digits by the end of this year.

“My biggest battle is against interest. My biggest enemy is interest. We lowered the interest rate to 12%,” the president said during an event in late September. “Is that enough? It is not enough. This needs to come down further.”

Turkey’s central bank “will remain under pressure from President Erdogan for looser policy,” Liam Peach, senior emerging markets economist at London-based Capital Economics, wrote in an analyst note after the data was released.

He added that “although the CBRT [Central Bank of the Republic of Turkey] said it will deliver one more 150bp interest rate cut at its meeting later this month, there is a risk of further easing beyond that, adding more downward pressure onto the lira.”

The lira was trading roughly flat on the day at 18.61 to the dollar. It’s lost more than 28% of its value against the greenback year-to-date and nearly 50% in the last full year.

LIVERPOOL, England — On the long picket line outside the gates of Liverpool’s Peel Port, rain-soaked dock workers warm themselves with cups of tea as they listen to 1980s pop.

Dozens of buses, cars and trucks honk in solidarity as they pass.

Dockers’ strikes are not new to Liverpool, nor is depravation. But this latest walk-out at Britain’s fourth-largest port is part of something much bigger, a great wave of public and private sector strikes taking place across the U.K. Railways, postal services, law courts and garbage collections are among the many public services grinding to a halt.

The immediate cause of the discontent, as elsewhere, is the rising cost of living. Inflation in the United Kingdom breached the 10 percent mark this year, with wages failing to keep pace.

But the U.K.’s economic woes long predate the current crisis. For more than a decade, Britain has been beset by weak economic growth, anaemic productivity, and stagnant private and public sector investment. Since 2016, its political leadership has been in a state of Brexit-induced flux.

Half a century after U.S. Secretary of State Henry Kissinger looked at the U.K.’s 1970s economic malaise and declared that “Britain is a tragedy,” the United Kingdom is heading to be the sick man of Europe once again.

The immediate cause of Liverpool dockers’ discontent that brought them to strike is the rising cost of living. | Christopher Furlong/Getty Images

Here in Liverpool, the “scars run very deep,” said Paul Turking, a dock worker in his late 30s. British voters, he added, have “been misled” by politicians’ promises to “level up” the country by investing heavily in regional economies. Conservatives “will promise you the world and then pull the carpet out from under your feet,” he complained.

“There’s no middle class no more,” said John Delij, a Peel Port veteran of 15 years. He sees the cost-of-living crisis and economic stagnation whittling away the middle rung of the economic ladder.

“How many billionaires do we have?” Delij asked, wondering how Britain could be the sixth-largest economy in the world with a record number of billionaires when food bank use is 35 percent above its pre-pandemic level. “The workers put money back into the economy,” he said.

What would they do if they were in charge? “Invest in affordable housing,” said Turking. “Housing and jobs.”

Falling behind

The British economy has been struck by particular turbulence over recent weeks. The cost of government borrowing soared in the wake of former PM Liz Truss’ disastrous mini-budget on September 23, with the U.K.’s central bank forced to step in and steady the bond markets.

But while the swift installation of Rishi Sunak, the former chancellor, as prime minister seems to have restored a modicum of calm, the economic backdrop remains bleak. Spending and welfare cuts are coming. Taxes are certain to rise. And the underlying problems cut deep.

U.K. productivity growth since the financial crisis has trailed that of comparator nations such as the U.S., France and Germany. As such, people’s median incomes also lag behind neighboring countries over the same period. Only Russia is forecast to have worse economic growth among the G20 nations in 2023.

In 1976, the U.K. — facing stagflation, a global energy crisis, a current account deficit and labor unrest — had to be bailed out by the International Monetary Fund. It feels far-fetched, but today some are warning it could happen again.

The U.K. is spluttering its way through an illness brought about in part through a series of self-inflicted wounds that have undermined the basic pillars of any economy: confidence and stability.

The political and economic malaise is such that it has prompted unwanted comparisons with countries whose misfortunes Britain once watched amusedly from afar.

“The existential risk to the U.K. … is not that we’re suddenly going to go off an economic cliff, or that the country’s going to descend into civil war or whatever,” said Jonathan Portes, professor of economics at King’s College London. “It’s that we will become like Italy.”

Portes, of course, does not mean a country blessed with good weather and fine food — but an economy hobbled by persistently low growth, caught in a dysfunctional political loop that lurches between “corrupt and incompetent right-wing populists” and “well-intentioned technocrats who can’t actually seem to turn the ship around.”

“That’s not the future that we want in the U.K,” he said.

Reviving the U.K.’s flatlining economy will not happen overnight. As Italy’s experience demonstrates, it’s one thing to diagnose an illness — another to cure it.

Experts speak of an unbalanced model heavily reliant upon Britain’s services sector and beset with low productivity, a result of years of underinvestment and a flexible labor market which delivers low unemployment but often insecure and low-paid work.

“We’re not investing in skills; businesses aren’t investing,” said Xiaowei Xu, senior research economist at the Institute for Fiscal Studies. “It’s not that surprising that we’re not getting productivity growth.”

But any attempt to address the country’s ailments will require its economic stewards to understand their underlying causes — and those stretch back at least to the first truly global crisis of the 21st century.

Crash and burn

The 2008 financial crisis hammered economies around the world, and the U.K. was no exception. Its economy shrunk by more than 6 percent between the first quarter of 2008 and the second quarter of 2009. Five years passed before it returned to its pre-recession size.

For Britain, the crisis in fact began in September 2007, a year before the collapse of Lehman Brothers, when wobbles in the U.S. subprime mortgage market sparked a run on the British bank Northern Rock.

The U.K. discovered it was particularly vulnerable to such a shock. Over the second half of the 20th century, its manufacturing base had largely eroded as its services sector expanded, with financial and professional services and real estate among the key drivers. As the Bank of England put it: “The interconnectedness of global finance meant that the U.K. financial system had become dangerously exposed to the fall-out from the U.S. sub-prime mortgage market.”

The crisis was a “big shock to the U.K.’s broad economic model,” said John Springford, from the Centre for European Reform. Productivity took an immediate hit as exports of financial services plunged. It never fully recovered.

“Productivity before the crash was basically, ‘Can we create lots and lots of debt and generate lots and lots of income on the back of this? Can we invent collateralized debt obligations and trade them in vast volumes?’” said James Meadway, director of the Progressive Economy Forum and a former adviser to Labour’s left-wing former shadow chancellor, John McDonnell.

A post-crash clampdown on City practises had an obvious impact.

“This is a major part of the British economy, so if it’s suddenly not performing the way it used to — for good reasons — things overall are going to look a bit shaky,” Meadway added.

The shock did not contain itself to the economy. In a pattern that would be repeated, and accentuated, in the coming years, it sent shuddering waves through the country’s political system, too.

The 2010 election was fought on how to best repair Britain’s broken economy. In 2009, the U.K. had the second-highest budget deficit in the G7, trailing only the U.S., according to the U.K. government’s own fiscal watchdog, the Office for Budget Responsibility (OBR).

The Conservative manifesto declared “our economy is overwhelmed by debt,” and promised to close the U.K.’s mounting budget deficit in five years with sharp public sector cuts. The incumbent Labour government responded by pledging to halve the deficit by 2014 with “deeper and tougher” cuts in public spending than the significant reductions overseen by former Conservative Prime Minister Margaret Thatcher in the 1980s.

The election returned a hung parliament, with the Conservatives entering into a coalition with the Liberal Democrats. The age of austerity was ushered in.

Austerity nation

Defenders of then-Chancellor George Osborne’s austerity program insist it saved Britain from the sort of market-led calamity witnessed this fall, and put the U.K. economy in a condition to weather subsequent global crises such as the COVID-19 pandemic and the fallout from the war in Ukraine.

“That hard work made policies like furlough and the energy price cap possible,” said Rupert Harrison, one of Osborne’s closest Treasury advisers.

Pointing to the brutal market response to Truss’ freewheeling economic plans, Harrison praised the “wisdom” of the coalition in prioritizing tackling the U.K.’s debt-GDP ratio. “You never know when you will be vulnerable to a loss of credibility,” he noted.

But Osborne’s detractors argue austerity — which saw deep cuts to community services such as libraries and adult social care; courts and prisons services; road maintenance; the police and so much more — also stripped away much of the U.K.’s social fabric, causing lasting and profound economic damage. A recent study claimed austerity was responsible for hundreds of thousands of excess deaths.

Under Osborne’s plan, three-quarters of the fiscal consolidation was to be delivered by spending cuts. With the exception of the National Health Service, schools and aid spending, all government budgets were slashed; public sector pay was frozen; taxes (mainly VAT) rose.

But while the government came close to delivering its fiscal tightening target for 2014-15, “the persistent underperformance of productivity and real GDP over that period meant the deficit remained higher than initially expected,” the OBR said. By his own measure, Osborne had failed, and was forced to push back his deficit-elimination target further. Austerity would have to continue into the second half of the 2010s.

Many economists contend that the fiscal belt-tightening sucked demand out of the economy and worsened Britain’s productivity crisis by stifling investment. “That certainly did hit U.K. growth and did some permanent damage,” said King’s College London’s Portes.

“If that investment isn’t there, other people start to find it less attractive to open businesses,” former Labour aide Meadway added. “If your railways aren’t actually very good … it does add up to a problem for businesses.”

A 2015 study found U.K. productivity, as measured by GDP per hour worked, was now lower than in the rest of the G7 by a whopping 18 percentage points.

“Frankly, nobody knows the whole answer,” Osborne said of Britain’s productivity conundrum in May 2015. “But what I do know is that I’d much rather have the productivity challenge than the challenge of mass unemployment.”

‘Jobs miracle’

Rising employment was indeed a signature achievement of the coalition years. Unemployment dropped below 6 percent across the U.K. by the end of the parliament in 2015, with just Germany and Austria achieving a lower rate of joblessness among the then-28 EU states. Real-term wages, however, took nearly a decade to recover to pre-crisis levels.

Economists like Meadway contend that the rise in employment came with a price, courtesy of Britain’s famously flexible labor market. He points to a Sports Direct warehouse in the East Midlands, where a 2015 Guardian investigation revealed the predominantly immigrant workforce was paid illegally low wages, while the working conditions were such that the facility was nicknamed “the gulag.”

The warehouse, it emerged, was built on a former coal mine, and for Meadway the symbolism neatly charts the U.K.’s move away from traditional heavy industry toward more precarious service sector employment. “It’s not a secure job anymore,” he said. “Once you have a very flexible labor market, the pressure on employers to pay more and the capacity for workers to bargain for more is very much reduced.”

Throughout the period, the Bank of England — the U.K.’s central bank — kept interest rates low and pursued a policy of quantitative easing. “That tends to distort what happens in the economy,” argued Meadway. QE, he said, is a “good [way of] getting money into the hands of people who already have quite a lot” and “doesn’t do much for people who depend on wage income.”

Meanwhile — whether necessary or not — the U.K.’s austerity policies undoubtedly worsened a decades-long trend of underinvestment in skills and research and development (Britain lags only Italy in the G7 on R&D spending). At British schools, there was a 9 percent real terms fall in per-pupil spending between 2009 and 2019, according to the Institute for Fiscal Studies’ Xu. “As countries get richer, usually you start spending more on education,” Xu noted.

Two senior ministers in the coalition government — David Gauke, who served in the Treasury throughout Osborne’s tenure, and ex-Lib Dem Business Secretary Vince Cable — have both accepted that the government might have focused more on higher taxation and less on cuts to public spending. But both also insisted the U.K had ultimately been correct to prioritize putting its public finances on a sounder footing.

It was February 2018 before Britain finally achieved Osborne’s goal of eliminating the deficit on its day-to-day budget.

Austerity was coming to an end, at last. But Osborne had already left the Treasury, 18 months earlier — swept away along with Cameron in the wake of a seismic national uprising.

***

David Cameron had won the 2015 election outright, despite — or perhaps because of — the stringent spending cuts his coalition government had overseen, more of which had been pledged in his 2015 manifesto. Also promised, of course, was a public vote on Britain’s EU membership.

The reasons for the leave vote that followed were many and complex — but few doubt that years of underinvestment in poorer parts of the U.K. were among them.

Regardless, the 2016 EU referendum triggered a period of political acrimony and turbulence not seen in Westminster for generations. With no pre-agreed model of what Brexit should actually entail, the U.K.’s future relationship with the EU became the subject of heated and protracted debate. After years of wrangling, Britain finally left the bloc at the end of January 2020, severing ties in a more profound way than many had envisaged.

While the twin crises of COVID and Ukraine have muddled the picture, most economists agree Brexit has already had a significant impact on the U.K. economy. The size of Britain’s trade flows relative to GDP has fallen further than other G7 countries, business investment growth trails the likes of Japan, South Korea and Italy, and the OBR has stuck by its March 2020 prediction that Brexit would reduce productivity and U.K. GDP by 4 percent.

Perhaps more significantly, Brexit has ushered in a period of political instability. As prime ministers come and go (the U.K. is now on its fifth since 2016), economic programs get neglected, or overturned. Overseas investors look on with trepidation.

“The evidence that the referendum outcome, and the kind of uncertainty and change in policy that it created, have led to low investment and low growth in the U.K. is fairly compelling,” said professor Stephen Millard, deputy director at the National Institute of Economic and Social Research.

Beyond the instability, the broader impact of the vote to leave remains contentious.

Portes argued — as many Remain supporters also do — that much harm was done by the decision to leave the EU’s single market. “It’s the facts, not the uncertainty that in my view is responsible for most of the damage,” he said.

Brexit supporters dismiss such claims.

“It’s difficult statistically to find much significant effect of Brexit on anything,” said professor Patrick Minford, founder member of Economists for Brexit. “There’s so much else going on, so much volatility.”

Minford, an economist favored by ex-PM Truss, acknowledged that “Brexit is disruptive in the short run, so it’s perfectly possible that you would get some short-run disruption.” But he added: “It was a long-term policy decision.”

Where next?

Plenty of economists can rattle off possible solutions, although actually delivering them has thus far evaded Britain’s political class. “It’s increasing investment, having more of a focus on the long-term, it’s having economic strategies that you set out and actually commit to over time,” says the IFS’ Xu. “As far as possible, it’s creating more certainty over economic policy.”

But in seeking to bring stability after the brief but chaotic Truss era, new U.K. Chancellor Jeremy Hunt has signaled a fresh period of austerity is on the way to plug the latest hole in the nation’s finances. Leveling Up Secretary Michael Gove told Times Radio that while, ideally, you wouldn’t want to reduce long-term capital investments, he was sure some spending on big projects “will be cut.”

This could be bad news for many of the U.K.’s long-awaited infrastructure schemes such as the HS2 high-speed rail line, which has been in the works for almost 15 years and already faces a familiar mix of local resistance, vested interests, and a sclerotic planning system.

“We have a real problem in the sense that the only way to really durably raise productivity growth for this country is for investments to pick up,” said Springford, from the Centre for European Reform. “And the headwinds to that are quite significant.”

For dock workers at Liverpool’s Peel Port, the prospect of a fresh round of austerity amid a cost-of-living crisis is too much to bear. “Workers all over this country need to stand up for themselves and join a union,” insisted Delij.

For him, it’s all about priorities — and the arguments still echo back to the great crash of 15 years ago. “They bailed the bankers out in 2007,” he said, “and can’t bail hungry people out now.”

The Federal Open Markets Committee, the U.S. central bank’s body responsible for setting monetary policy, raised interest rates by 75 basis points on Wednesday for the fourth consecutive time as Federal Reserve governors attempt to battle stubborn inflation levels in the country.

Jerome Powell, Chairman of the Federal Reserve and the FOMC, joined a group of journalists for a press conference shortly after the data release, shedding more light on the central bank’s thoughts for future action.

Markets reacted positively to the 0.75% interest rate increase, which came in as expected, but trading became more volatile as the chairman started its speech. While the written statement announcing the interest rate decision showed a new dovish sentence, further fueling the rally, Powell’s press conference combated that feeling as the Fed Chair reiterated previous guidance.

“In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” the FOMC statement read, hinting at a more dovish Fed.

Powell, however, highlighted that the “ultimate level of rates will be higher than previously expected,” triggering an acute market drawdown.

The feeling markets are left with is of confirmation that a slow-down is near but surprise when it comes to the terminal funds rate, something that can be attested by the upswing and consequent downswing in the S&P 500 index.

The S&P 500 shoot up at 14:00 EST (2 p.m.) as soon as the FOMC statement was released with the more dovish language, only to come back down as Powell’s press conference began thirty minutes later. Investors likely left the livestream with a sour taste in their mouths, judging by the continued drawdowns in the index. (Chart/TradingView)

Bitcoin mirrored stock market moves, albeit falling less in percentage terms. At the time of writing, BTC is accumulating a 1% drawdown, while the S&P 500 ended the trading day bleeding by over double that amount (2.39%). The Nasdaq was seeing a similar fate, but extended its losses to 3.15%.

The fact that Bitcoin has been the least volatile of the three is quite remarkable as it defies history and mainstream media narratives altogether. While the peer-to-peer currency is still correlated with stocks, it isn’t the one doing the most severe swings, and that is going by unnoticed.

The Federal Reserve on Wednesday approved a fourth consecutive three-quarter point interest rate increase and signaled a potential change in how it will approach monetary policy to bring down inflation.

In a well-telegraphed move that markets had been expecting for weeks, the central bank raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high.

Along with anticipating the rate hike, markets also had been looking for language indicating that this could be the last 0.75-point, or 75 basis point, move.

The new statement hinted at that policy change, saying when determining future hikes, the Fed “will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Economists are hoping this is the much talked about “step-down” in policy that could see a rate increase of half a point at the December meeting and then a few smaller hikes in 2023.

This week’s statement also expanded on previous language simply declaring that “ongoing increases in the target range will be appropriate.”

The new language read, “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

On balance, Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

He also reiterated that it may take resolve and patience to get inflation down.

“We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,” he said.

Still, Powell repeated the idea that there may come a time to slow the pace of rate increases. He has said this at recent news conferences

“So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made,” he said.

The chairman also expressed some pessimism about the future. He noted that he now expects the “terminal rate,” or the point when the Fed stops raising rates, to be higher than it was at the September meeting. With the higher rates also comes the prospect that the Fed will not be able to achieve the “soft landing” that Powell has spoken of in the past.

“Has it narrowed? Yes,” he said in response to a question about whether the path has narrowed to a place where the economy doesn’t enter a pronounced contraction. “Is it still possible? Yes.”

However, he said the need for still-higher rates makes the job more difficult.

“Policy needs to be more restrictive, and that narrows the path to a soft landing,” Powell said.

Along with the tweak in the statement, the Federal Open Market Committee again categorized growth in spending and production as “modest” and noted that “job gains have been robust in recent months” while inflation is “elevated.” The statement also reiterated language that the committee is “highly attentive to inflation risks.”

The rate increase comes as recent inflation readings show prices remain near 40-year highs. A historically tight jobs market in which there are nearly two openings for every unemployed worker is pushing up wages, a trend the Fed is seeking to head off as it tightens money supply.

Concerns are rising that the Fed, in its efforts to bring down the cost of living, also will pull the economy into recession. Powell has said he still sees a path to a “soft landing” in which there is not a severe contraction, but the U.S. economy this year has shown virtually no growth even as the full impact from the rate hikes has yet to kick in.

At the same time, the Fed’s preferred inflation measure showed the cost of living rose 6.2% in September from a year ago – 5.1% even excluding food and energy costs. GDP declined in both the first and second quarters, meeting a common definition of recession, though it rebounded to 2.6% in the third quarter largely because of an unusual rise in exports. At the same time, housing demand has plunged as 30-year mortgage rates have soared past 7% in recent days.

On Wall Street, markets have been rallying in anticipation that the Fed soon might start to ease back as worries grow over the longer-term impact of higher rates.

The Dow Jones Industrial Average has gained more than 13% over the past month, in part because of an earnings season that wasn’t as bad as feared but also due to growing hopes for a recalibration of Fed policy. Treasury yields also have come off their highest levels since the early days of the financial crisis, though they remain elevated. The benchmark 10-year note most recently was around 4.09%.

There is little if any expectation that the rate hikes will halt anytime soon, so the anticipation is just for a slower pace. Futures traders are pricing a near coin-flip chance of a half-point increase in December, against another three-quarter point move.

Current market pricing also indicates the fed funds rate will top out near 5% before the rate hikes cease.

The fed funds rate sets the level that banks charge each other for overnight loans, but spills over into multiple other consumer debt instruments such as adjustable-rate mortgages, auto loans and credit cards.

The U.S. central bank has raised the benchmark short-term borrowing rate a total of six times this year, including 75 basis point increases in June, July and September, in an effort to cool down inflation, which is still near 40-year highs and causing most consumers to feel increasingly cash strapped. A basis point is equal to 0.01 of a percentage point.

A policy statement after the announcement noted that the Fed is considering the “cumulative” impact of its hikes so far when determining future rate increases. Economists are hoping this signals plans to “step-down” the pace of increases going forward, which could mean a half point hike at the December meeting and then a few smaller raises in 2023. Still, stocks tumbled after Federal Reserve Chair Jerome Powell said there were more rate hikes ahead.

“Americans are under greater financial strain, there’s no question,” said Chester Spatt, professor of finance at Carnegie Mellon University’s Tepper School of Business and former chief economist of the Securities and Exchange Commission.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and saving rates they see every day.

By raising rates, the Fed makes it costlier to take out a loan, causing people to borrow and spend less, effectively pumping the brakes on the economy and slowing down the pace of price increases.

“Unfortunately, the economy will slow much faster than inflation, so we’ll feel the pain well before we see any gain,” said Greg McBride, Bankrate.com’s chief financial analyst.

Already, “mortgage rates have rocketed to 16-year highs, home equity lines of credit are the highest in 14 years, and car loan rates are at 11-year highs,” he said.

• Mortgage rates are already higher. Even though 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a home has lost considerable purchasing power, in part because of inflation and the Fed’s policy moves.

Along with the central bank’s vow to stay tough on inflation, the average interest rate on the 30-year fixed-rate mortgage hit 7%, up from below 4% back in March.

On a $300,000 loan, a 30-year, fixed-rate mortgage at December’s rate of 3.11% would have meant a monthly payment of about $1,283. Today’s rate of 7.08% brings the monthly payment to $2,012. That’s an extra $729 a month or $8,748 more a year, and $262,440 more over the lifetime of the loan, according to LendingTree.

The increase in mortgage rates since the start of 2022 has the same impact on affordability as a 35% increase in home prices, according to McBride’s analysis. “If you had been approved for a $300,000 mortgage in the beginning of the year, that’s the equivalent of less than $200,000 today.”

For home buyers, “adjustable-rate mortgages may continue to be more popular among consumers seeking lower monthly payments in the short term,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion. “And consumers looking to tap into available home equity may continue to look towards HELOCs,” she added, rather than refinancing.

Yet adjustable-rate mortgages and home equity lines of credit are pegged to the prime rate, so those will also increase. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.3% from 4.24% earlier in the year.

• Credit card rates are rising. Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does as well, and your credit card rate follows suit within one or two billing cycles.

That means anyone who carries a balance on their credit card will soon have to shell out even more just to cover the interest charges. “This latest interest rate hike will most acutely impact those consumers who do not pay off their credit card balances in full through higher minimum monthly payments,” Raneri said.

Because of this rate hike, consumers with credit card debt will spend an additional $5.1 billion on interest, according to an analysis by WalletHub. Factoring in the rate hikes from March, May, June, July, September and November, credit card users will wind up paying around $25.6 billion more in 2022 than they would have otherwise, WalletHub found.

Already credit card rates are near 19%, up from 16.34% in March. “That’s the highest since the Fed began tracking in 1994 and is more than a full percentage point higher than the previous record set back in 2019,” according to Matt Schulz, chief credit analyst at LendingTree. And rates are only going to continue to rise, he said. “We’ve still got a ways to go before those rates hit their peak.”

The best thing you can do now is pay down high-cost debt — “0% balance transfer credit cards are still widely available, especially for those with good credit, and can help you avoid accruing interest on the transferred balance for up to 21 months,” Schulz said.

“That can be an absolute godsend for folks struggling with card debt,” he added.

Otherwise, consolidate and pay off high-interest credit cards with a lower-interest home equity loan or personal loan, Schulz advised.

• Auto loans are more expensive. Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans, so if you are planning to buy a car, you’ll pay more in the months ahead.

The average interest rate on a five-year new car loan is currently 5.63%, up from 3.86% at the beginning of the year and could surpass 6% with the central bank’s next moves, although consumers with higher credit scores may be able to secure better loan terms.

Paying an annual percentage rate of 6% instead of 5% would cost consumers $1,348 more in interest over the course of a $40,000, 72-month car loan, according to data from Edmunds.

Still, it’s not the interest rate but the sticker price of the vehicle that’s causing an affordability problem, McBride said. “Rising rates doesn’t help, certainly.”

• Student loans vary by type.Federal student loan rates are also fixed, so most borrowers won’t be affected immediately. But if you are about to borrow money for college, the interest rate on federal student loans taken out for the 2022-2023 academic year are up to 4.99%, from 3.73% last year and 2.75% in 2020-2021.

If you have a private loan, those loans may be fixed or have a variable rate tied to the Libor, prime or T-bill rates, which means that as the Fed raises rates, borrowers will likely pay more in interest, although how much more will vary by the benchmark.

Currently, average private student loan fixed rates can range from 3.22% to 14.96%, and from 2.52% to 12.99% for variable rates, according to Bankrate. As with auto loans, they vary widely based on your credit score.

• Only some savings account rates are higher. The silver lining is that the interest rates on savings accounts are finally higher after several consecutive rate hikes.

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 3.5%, according to Bankrate, much higher than the average rate from a traditional, brick-and-mortar bank.

“Savers are seeing the best yields since 2009 — if they’re willing to shop around,” McBride said. Still, because the inflation rate is now higher than all of these rates, any money in savings loses purchasing power over time.

Now is the time to boost that emergency savings, McBride advised. “Not only will you be rewarded with higher rates but also nothing helps you sleep better at night than knowing you have some money tucked away just in case.”

“More broadly, it makes sense to be more cautious,” Spatt added. “Recognize that employment is maybe less secure. It’s reasonable to expect we’ll see unemployment going up, but how much remains to be seen.”

It is three weeks before Black Friday, but the Federal Reserve is about to make the post-holiday debt hangover a little more intense.

By the time the latest rate hikes filter through the very rate-sensitive credit card industry and pump up customers’ annual percentage rates a little more, experts say it will be some point in December 2022 or January 2023. Right in time for many holiday gifts and expenses to post on credit cards bills — and there to make the costs of a carried balance a little extra expensive.

What’s different now is the presence of four-decade high inflation, coupled with fast-rising interest rates that the Fed hopes will ultimately cool those rising prices, although without sending the economy to a recessionary thud.

Wednesday’s rate move is the fourth straight 75-basis-point rate hike to the federal funds rate, taking it to the 3.75% -4% range, when it was near zero last year’s holiday season. By now, Americans are all too acquainted with 2022’s fast-rising interest rates. They just haven’t gone through a Christmas and Hanakkuh with it yet.

“It’s not the time to overspend and have a problem with paying your bills later. We know the economy is sending mixed messages,” said Michele Raneri, vice president of financial services research and consulting at TransUnion TRU, -4.31%,

one of the country’s three major credit reporting companies.

It’s extra important to think through a holiday budget and how much relies on credit, she said. “People need to think about how much they can afford to repay and how long it will take to repay it.”

Holiday spending could be the same as 2021 for many people — but not everyone

Now, two forecasts suggest many people ready to spend the same amount for this year’s holiday cheer as they did last year.

People are planning to spend an average $1,430 on gifts, travel and entertainment this year, which is around the $1,447 spent last year, according to PwC researchers. Three-quarters of people said they were planning to spend the same or more than last year and respondents said credit cards were one of their top ways to pay.

“ Compared to last year, credit card balances are getting bigger, more people are sitting on balances and debt costs are getting pricier.”

By another measure, Americans will pay an average $1,455 on holiday-related gifts and experiences, essentially flat from last year, say Deloitte researchers.

More than one-third of surveyed consumers say their financial outlook is worse than the same point last year. Nearly one-quarter of people were concerned about credit card debt as of late September, Deloitte’s numbers show in an ongoing tracking of consumer mood.

It’s understandable to see the concern with households amassing a collective $890 billion in credit card debt through the second quarter. Compared to last year, balances are getting bigger, more people are sitting on balances and debt costs are getting pricier because the interest rates applied to those balances are rising.

When people were carrying a credit card balance month to month, the sum was $5,474 on average, according to Raneri. That’s through the end of September and it’s a nearly 13% rise year over year, she said. The 164 million people carrying a balance is a 5% increase from last year, she noted.

Credit cards carrying a balance during the third quarter had an average 18.43% APR, Federal Reserve data shows. That’s up from 16.65% in the second quarter and up from 17.13% in 2021’s third quarter.

How the Fed influences credit card rates

Credit card issuers typically determine their rates by applying a “prime rate” — typically three percentage points on top of the federal funds rate — and the issuer’s profit margin, said Ted Rossman, senior industry analyst at Bankrate.com.

By late October, the rate on new card offers was 18.73%, according to Bankrate data. At this point last year, it was 16.31%, Rossman said. In a few weeks, the rates on new offers should beat the all-time record of an average 19% APR, exclusive to new offers, he added.

While it can take a billing cycle or two for a higher APR to make its way to an existing credit card account, Rossman noted the APRs on new offers could rise in a matter of days.

Here’s a hypothetical to show how much more expensive credit card debt becomes with every extra hike. Suppose the $5,474 balance is on a credit card with the current 18.73% average. If a person has to resort to minimum payments, Rossman said, they’d be paying $7,118 just in interest to pay off the debt.

“ In a few weeks, the rates on new credit card offers should beat the all-time record of an average 19% APR.”

What if the 18.73% APR gets kicked up 75 basis points to 19.48%? If that same borrower has to pay minimums, they are now paying $7,417 in interest to snuff the principal debt of $5,474, Rossman said.

The example has its limits because people may pay more than the minimum and they may incur more credit card debt as they pay off the old one. But it shows a bigger point: “Unfortunately, anybody dealing with credit card debt is a loser from the series of rate hikes. It was already expensive. It’s getting more so,” Rossman said.

When do rate hikes stop?

While decisions during the Fed’s November meeting can have a ripple effect on holiday-time borrowing costs, observers say the real question about Wednesday is the clues Federal Reserve Chairman Jerome Powell drops for what’s next. The central bank’s committee voting on interest rate increases reconvenes in mid-December.

On Wednesday, the Fed said in a statement it expected further rate increases, but also said it would be watching to see if there were lag effects with its tightening policies, which could slow or limit the total amount of increases.

“People, when they hear lags, they think about a pause. It’s very premature, in my view, to think about or be talking about pausing our rate hike. We have a ways to go,” Powell told reporters at a Wednesday afternoon press conference.

The economy is strong enough to handle higher rates, Powell said. For one thing, households have “strong balance sheets” and “strong spending power,” he noted.

Stock markets first jumped higher after the latest interest rate announcement. But they gave up the gains — and then some — by the end of the day. The Dow Jones Industrial Average DJIA, -1.55%

was down more than 500 points, or 1.6% while the S&P 500 SPX, -2.50%

was down 2.5% and the Nasdaq Composite COMP, -3.36%

closed 3.4% lower.

Top economists in major North American-based banks forecasted the Fed will keep raising interest rates “until the first quarter of next year before potentially lowering rates through the end of 2023,” Sayee Srinivasan, chief economist at the American Bankers Association, the banking sector’s trade association, said ahead of Wednesday’s latest rate hike.

“Top economists polled as part of a banking industry panel expect Fed rate increases through at least the first quarter of 2023.”

The forecast, coming through an ABA advisory committee, is no sure thing. “Everything depends on the ability of the Fed to bring inflation down, so that will remain their clear priority,” said Srinivasan.

Meanwhile, rising costs may cause more people to put the holiday cheer on plastic, even their decorations. The majority of Christmas tree growers in one poll are expecting wholesale prices to climb 5% to 15% for this season.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

November FOMC Meeting

All eyes across global markets are on the November FOMC meeting. At this point in the global liquidity cycle, seemingly every asset class is part of the same implicit trade. The tough talk from the Fed, the central bank of the dollar indebted world, has held up so far in 2022, as they embark upon the fastest tightening cycle in modern history.

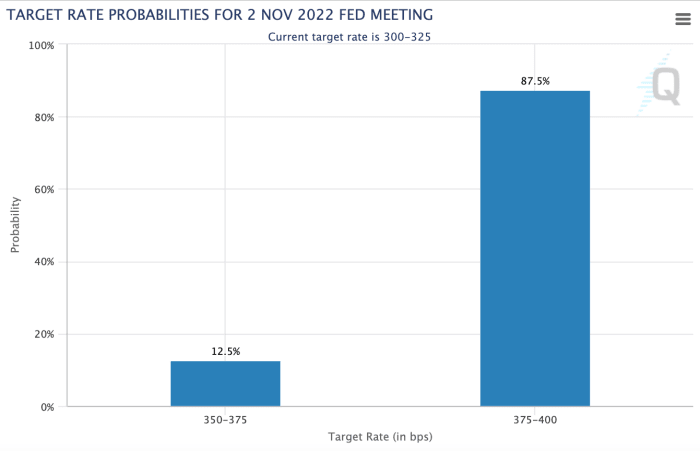

Consensus for the size of the rate hike is 75bps, which would raise the policy rate to 4.00%.

Consensus for the size of the rate hike is 75bps, which would raise the policy rate to 4.00%.

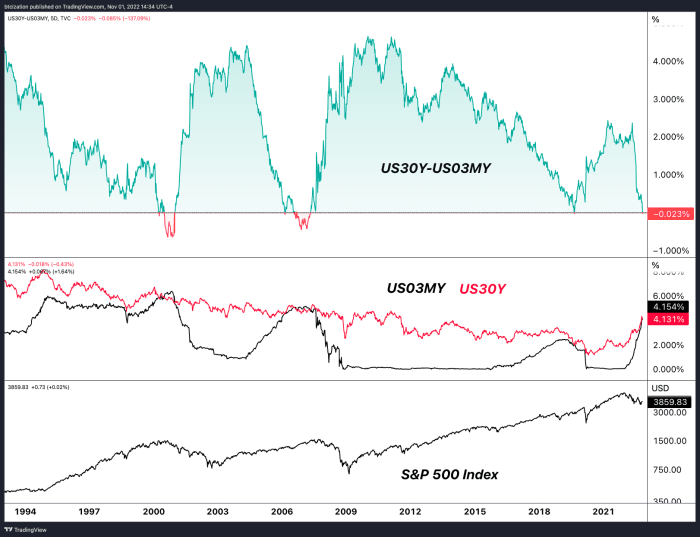

Much of this hiking has already priced itself into the front end of the U.S. Treasury curve, which has led to all sorts of inversions across various maturities.

In terms of the yield curve, across any duration that matters, an inversion has happened — a phenomenon that typically occurs before an economic slowdown, as short term yields rising disincentivizes the investment of capital over long durations due to “attractive” short end yields. Lend your money to the U.S. government for 30 years and lock in 4.13% or for three months at 4.13% and reevaluate then? Duration risk is real and the pace of this tightening cycle on the backs of record inflationary conditions across the globe has left investors uneasy on the long-term prospect of government paper. No kidding.

U.S. Treasury yield curve inversion with short-term yields higher than long-term yields.

Arguably, the Fed is still behind the curve and, per their mandate, shouldn’t have “let” inflationary pressures get this out of control while still stoking the flames with zero-interest rate policy and $120B/month of quantitative easing bond purchases. Due to the blunder and subsequent hit to their credibility, the Fed is attempting to induce pain in the labor market and in asset prices until inflationary concerns abate.

It’s a bold strategy and it’s one that is entirely destined to fail. But they’ll likely end up crashing everything while trying. However, the nominal economy — meaning gross domestic product expectations (not inflation adjusted) and the labor market — is still piping hot. The market looks to be believing that Fed policy is in an entirely new regime going forward.

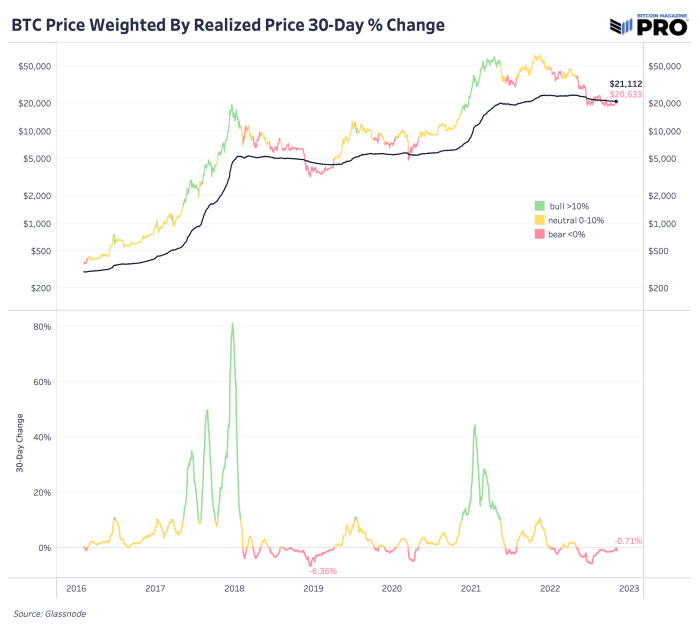

Shown below is the bitcoin price with its average on-chain holder cost basis (realized price). Bitcoin is in a classic bear market consolidation phase, that many may not have more pain ahead. These periods, where panicked/leveraged investors transfer their holdings to the prudent and well capitalized, are what create the conditions for the next bull run.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.046%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.