Suze Orman has a warning for investors relying too heavily on bonds.

The personal finance expert believes the draw of high interest rates and an aversion to risk taking are preventing too many people from taking a “lifetime opportunity” in the stock market.

“Some of these stocks — how do you pass them up? I mean, you have to go into them. Now, do you go into them with everything that you have? No. Do you dollar-cost average into them, and take advantage of [down] days? … Yes,” the “Women & Money” podcast host told CNBC’s “Fast Money” this week. “You’ll be making a big mistake if you park your money forever in bonds.”

“I have some serious losers at this point. However, I don’t care,” said Orman. “I want to buy a stock, and I hope it goes down. And I hope it goes further down and down so I can accumulate more.”

She does recommend keeping some money in fixed income to mitigate risks in a volatile environment.

At the same time, she still sees a role for bonds in portfolios. She likes the three– and six-month Treasurys and is ready to start looking longer term.

“The play may start to be in long-term Treasurys. So, I’ve started to dip my toe in. Every time the 30-year [yield] crosses five percent, I buy,” said Orman.

The 30-year Treasury yield is still near 2007 highs. It traded above 5% as of Friday’s close.

The Federal Reserve’s flurry of interest rate hikes since March 2022 have taken a toll on home buyers, pushing the typical mortgage rate above 8%, a level not seen since 2000. On Wednesday, the Federal Reserve is set to make another interest rate decision that could impact the home loan market.

The central bank is expected to hold rates steady at its November 1 meeting, according to economists surveyed by FactSet. That comes as credit cards are now charging the highest interest rates on record, and many home buyers have been priced out of the real estate market due to loan costs.

A pause on rate hikes could provide a backstop against higher borrowing costs, yet it might not immediately translate into lower mortgage rates, according to financial experts. That’s partly because mortgage rate hikes don’t always mirror the Fed’s rate increases, but rather tend to track the yield on the 10-year U.S. Treasury note, which recently hit a 16-year high.

“Based on how [mortgage rates] have consistently risen since September, there’s a decent chance that we’ll end 2023 with the average rate on 30-year, fixed mortgages near, or even slightly above, 8%,” said Jacob Channel, a senior economist at LendingTree.

Even so, mortgage rates have climbed this year almost in lockstep with the Fed raising its benchmark rate. Investors’ expectations for future inflation as well as global demand for Treasurys can also influence rates on home loans.

The Federal Reserve has turned to rate hikes as its most potent weapon to battle the highest inflation in four decades. While inflation has eased since last year, Federal Reserve Chair Jerome Powell said last week that inflation remains too high, but he also signaled that the Fed may not need to raise rates again — at least in the short term.

Will mortgage rates go down in 2024?

Still, mortgage rates could ease in 2024, with economists forecasting the Fed could start to cut rates by mid-year, according to FactSet.

“We don’t expect additional Fed rate hikes this year — we think they will pause into next year, and we expect there to be a first rate cut sometime probably toward around the second quarter,” noted Matt Vance, senior director and Americas head of multifamily research for real estate company CBRE.

In the meantime, home buyers are facing an affordability crisis, with home prices climbing along with rates. The national median home price hit $430,000 in September, up from $400,000 in January, according to Realtor.com. Prices have climbed so high that the average down payment is now between $47,900 and $84,983 in the nation’s 50 largest metropolitan areas, LendingTree said in a study this week.

Some would-be buyers have paused their house hunting plans due to higher rates and prices. Meanwhile, many homeowners have decided not to sell their property because they don’t want to purchase a new home at today’s elevated borrowing costs.

Americans may continue to be hesitant to purchase homes next year because of interest rates, analysts at Goldman Sachs said this month.

“Sustained higher mortgage rates will have their most pronounced impact in 2024 on housing turnover,” Goldman Sachs said in a research note this week. “As a result, we expect the fewest annual existing home sales since the early 1990s at 3.8 million.”

The one-two punch of higher interest rates and home prices have caused a slowdown in the housing market this year. Mortgage applications have dipped in recent weeks, according to the latest data from the Mortgage Bankers Association, and existing homes sales fell 2% in September, according to the National Association of Realtors.

Despite those challenges, some Americans were still able to buy a home this year, but “today’s housing market is much less energetic than it was during the height of the pandemic,” Channel said.

Khristopher J. Brooks is a reporter for CBS MoneyWatch covering business, consumer and financial stories that range from economic inequality and housing issues to bankruptcies and the business of sports.

That doesn’t mean everything costs more in Canada, says David Soberman, a professor of marketing and Canadian national chair of strategic marketing at the University of Toronto’s Rotman School of Management. Canadians may pay more than Americans for the same basket of goods, he says, but we pay less than people in some other countries, like Switzerland.

Why do we pay what we do? That’s a difficult question to answer. The reasons are complex and vary depending on the type of good or service. Let’s look at some of the main contributors to Canada’s cost of living, why they are as expensive as they are, and steps you can take to reduce those costs.

Why are groceries so expensive in Canada?

There are a few reasons groceries cost so much in Canada, says Soberman. It’s expensive for companies to ship food products across a country as large as ours, and those costs are reflected in what you pay in stores, he says. But a highly concentrated grocery industry is also a big contributing factor.

Canada’s grocery market is dominated by just a few companies. Domestically, there are three big players: Loblaws, Metro and Sobeys. (Some chains, such as Save-On-Foods in Western Canada, compete on a regional basis.) The next largest retailers for grocery sales are Walmart and Costco. Together, these five companies account for more than three-quarters of all food sales in Canada, according to Canada’s Competition Bureau. In 2023, 49% of Canadians report buying groceries from Loblaws or one of its sister stores.

Critics argue such concentration allows the dominant companies to participate in anti-competitive practices that ultimately harm consumers through higher prices. In grocery, this takes the form of fixing bread prices, preventing competitors from selling certain products, or collectively deciding when to freeze grocery prices—and when to unfreeze them. It’s a problem experts say applies to other industries, such as telecommunications and air travel.

When Canada’s Competition Act was introduced, in 1986, there were at least eight large grocery chains in Canada, each owned by a different company. Since then, more than a dozen major mergers and acquisitions have reduced the level of competition. Today, three big supermarket companies own several smaller chains, including discount brands that could be mistaken for rivals: Loblaws has No Frills, Sobeys has FreshCo and Metro has Food Basics, for example.

How does Canada allow for three big grocers to reign? “The law in Canada typically will not allow the Bureau to intervene in these deals, as they are generally seen as unlikely to have a significant impact on prices and other dimensions of competition,” states a Competition Bureau report. “In the case of a major city or suburb, with five or six different grocery stores nearby, it can be hard to prove that removing one option will cause prices to go up significantly.”

Another underlying issue is that, for many decades, the prevailing view was that “as a small, but large country, we need to accept lower levels of competition to achieve a scale that is necessary to serve the various markets,” says Keldon Bester, executive director of the Canadian Anti-Monopoly Project (CAMP). Over time, that belief has led to fewer and fewer options for consumers, he says.

Most credit cards come with a variable rate, which hasa direct connection to the Fed’s benchmark rate.

After the previous rate hikes, the average credit card rate is now more than 20% — an all-time high. Further, with most people feeling strained by higher prices, balances are higher and more cardholders are carrying debt from month to month.

Even without a rate hike, APRs may continue to rise, according to according to Matt Schulz, chief credit analyst at LendingTree. “The truth is that today’s credit card rates are the highest they’ve been in decades, and they’re almost certainly going to keep creeping higher in the next few months.”

Although 15-year and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed’s policy moves.

The average rate for a 30-year, fixed-rate mortgage is up to 8%, the highest in 23 years, according to Bankrate.

“Rates have risen two full percentage points in 2023 alone,” said Sam Khater, Freddie Mac’s chief economist. “Purchase activity has slowed to a virtual standstill, affordability remains a significant hurdle for many and the only way to address it is lower rates and greater inventory.”

Federal student loan rates are also fixed, so most borrowers aren’t immediately affected by the Fed’s moves. But undergraduate students who take out new direct federal student loans are now paying 5.50% — up from 4.99% in the 2022-23 academic year and 3.73% in 2021-22.

Private student loans tend to have a variable rate tied to prime, Treasury bill or another rate index — and that means that those borrowers are already paying more in interest. How much more, however, varies with the benchmark.

“Borrowers are being squeezed but the flipside is that savers are benefiting,” said Greg McBride, chief financial analyst at Bankrate.com.

While the Fed has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate. The savings account rates at some of the largest retail banks, which were near rock bottom during most of the Covid pandemic, are currently up to 0.46%, on average, according to the Federal Deposit Insurance Corp., or FDIC.

However, top-yielding online savings account rates are now paying over 5%, according to Bankrate — which is the most savers have been able to earn in nearly two decades.

“Moving your money to a high-yield savings account is the easiest money you are ever going to make,” McBride said.

“Although relaxation of property restrictions was highly anticipated, the BSD [buyers’ stamp duty] cut from 15.0% to 7.5% surprised us; the other relaxations were in-line,” Citi’s Ken Yeung wrote in a note.

He doesn’t expect the move to reverse downward trend in Hong Kong’s property prices as interest rates remain high.

According to data from real estate agency Midland Realty, the second-hand property market average turnover ratio between 2017 and 2023 stands at 3.7%. That’s compared with 8.7% before the cooling measures took effect in 2010.

Buggle Lau, chief analyst at Midland Realty told CNBC the average turnover ratio in 2022 to 2023 are at historic lows, as property prices have corrected down by nearly 20% since their peak in August 2021.

He expects the policy address will give property prices “a chance to stabilize” and for volumes to pick up.

For the market to fully recover, both in terms of price and volume, interest rates will have to come down next year, the property analyst said.

He expects a further 5% downside on prices in the first half of next year should there be a rate cut.

Hong Kong homeowner KC Mok has been trying to sell his apartment before his family immigrates at the end of the year — a popular reason for people selling their property in recent years.

The 41-year-old told CNBC that his 707 sq. ft. 3-bedroom apartment is currently listing at $9.5 million Hong Kong dollars ($1.21million), 20% lower than his purchase price in 2019.

He said many people have been viewing his place, but the only offer he received so far is a mismatch.

“Now when we come to selling the apartment, we found that the value of the apartment [is] already like $2 million dollars less, so a little bit depressed but we have to leave so it’s the timing maybe,” Mok said, acknowledging that the latest cooling measures “will help a little bit” for his situation.

Meanwhile, 33-year-old Kitty Yiu considers herself “lucky” as she sold her apartment and started renting in February, just before property prices fell and interest rates rose.

Yiu gave birth to her firstborn earlier this year and needed a bigger home to accommodate her growing family.

“To be honest, we are still in a struggle to see whether we should buy a new flat, like to buy a flat again,” she said.

“I think the price at this moment is still high, even if it’s having a downward trend, but for me I think it’s still overpriced,” said Yiu who doesn’t think the latest policy relief would increase her appetite to purchase a house.

Unlike Mok and Yiu, Eugene Law faces the struggle of rising mortgage rates as a new homeowner.

Together with his mother, Law, who is 30, purchased a flat at pre-construction in 2021 and moved in last year. His mortgage rate started at 1.9% and is currently at 3.375%. That means he needs to pay an additional HKD $6,000 ($767.09) per month for the interest, which he says makes him feel “so bad.”

“[It was] unexpected … because I expected the HIBOR may rise but I didn’t expect the prime rate will also rise, and also in a very high percentage.”

Prospective homebuyers in Hong Kong can choose to peg their mortgage rate with HIBOR or prime rate – known as the “H Plan” and “P Plan.” HIBOR refers to the interest rate for interbank borrowing, while prime rate is determined by individual banks.

In a low interest rate environment, the prime rate is usually the more popular choice as it is considered more stable, and easier for the mortgagor to make financial plans.

Despite regretting the timing of his purchase, Law said the latest easing of policy would not have affected the decision.

A recent report from UBS showed Hong Kong is the 6th overvalued city on their Global Real Estate Bubble Index. Zurich, Tokyo and Miami are the top three.

“Biggest risk [to Hong Kong’s property market] will be [a] pro-longed high-rate environment, and hence further mortgage cost increase. Longer run will be geopolitical risk,” said UBS’s china property market Mark Leung in an email to CNBC.

While describing the current sentiment as “a bit weak,” he expects the policy address would release sizable purchasing power from non-local expats who are waiting to become permanent residents.

With the second-hand market bid-ask spread remaining high and many homeowners not willing to sell their properties at a discount, Leung said he expects little room for property prices to reverse the downward trend.

For the primary market, he expects developers will now be more willing to cut prices in order to boost sales and “recycle cash, given higher interest rate environment.”

“Price-wise should be muted, as we think developers may be aggressive in price setting, hence cap the price rebound potential,” he added.

Minister Freeland’s proposal tackles four areas: mortgages, bank account fees, junk fees and dispute resolution. Junk fees include as the cost Canadians pay for non-sufficient funds (NSF), overdraft protection, debit transactions and Interac e-Transfers. Here’s how:

New mortgage guideline for banks

In early October, Minister Freeland met with the CEOs of Canada’s largest banks to discuss the government’s new mortgage guideline, issued by the FCAC, that asks banks to proactively assist Canadian mortgage-holders who are struggling to meet rising costs. In particular, the guideline focuses on home owners who are at risk of defaulting on their mortgage.

The guideline asks that banks identify consumers who are at risk and explore assistance in the form of fee waivers, no-cost financial education, lengthened mortgage amortization periods and mortgage relief measures.

Eliminating some bank account and junk fees

The government has tasked the FCAC with “setting expectations” for banks to provide free or low-cost banking options and with “encouraging” them to remove junk charges.

Although there are numerous no-fee bank accounts available to Canadians, they are typically online-only. For chequing accounts at a Big Six bank, costs can range from $4 to $40 monthly, with extra charges of around $1 to $1.50 for Interac e-Transfers, over limit transactions, and out-of-network ATM use. Penalties for non-sufficient funds can be a whopping $45 to $50. Currently, the big banks offer low- or no-cost options to youth, students and seniors, and Freeland is hoping to expand eligibility to even more Canadians.

Resolving disputes with banks

In a 2020 report, the FCAC identified dispute resolution as a problem for Canadian banking customers, noting that allowing banks to choose between two separate complaint bodies—the Ombudsman for Banking Services and Investments (OBSI) and the ADR Chambers Banking Ombuds Office (ADRBO)—created inefficiencies and delays. So, another government measure seeks to remedy this by designating the OBSI, an independent and transparent non-profit, as the sole complaints body for banking.

Why is the federal government taking these steps?

The housing crisis, the rising costs of living and high interest rates are putting enormous financial pressure on Canadians, many of whom are taking on debt just to get by.

According to the government press release, these measures are intended to “ensure Canadians are treated fairly by their banks,” to make life more affordable and to reduce inflation. Additionally, they are intended to guard against the dangers of the current Canadian housing market by taking action now to avoid mass foreclosures in the future.

New home sales in the United States surged higher in September from the month before, even as mortgage rates remained over 7%, making financing a home costlier and pushing people out of the market.

Sales of newly constructed homes jumped 12.3% in September to a seasonally adjusted annual rate of 759,000, from a revised rate of 676,000 in August, according to a joint report from the US Department of Housing and Urban Development and the Census Bureau. Sales were up 33.9% from a year ago.

This represents the fastest pace of sales since February 2022 and easily exceeds analysts’ expectations of a sales pace of 680,000.

Sales of existing homes have been trending down since February and are down 20% year to date in September from a year ago. There is an ongoing inventory and affordability crunch that has homeowners with mortgage rates of 3% or 4% reluctant to sell and buy another home at a much higher rate. In August, rates topped 7% and have lingered there as the Federal Reserve continues to address inflation.

The average rate for a 30-year, fixed-rate mortgage was 7.63% last week, according to Freddie Mac, and there are indications it could continue to climb.

“With one more Fed interest rate hike expected for the year, interest rates are not anticipated to drop any time soon,” said Kelly Mangold of RCLCO Real Estate Consulting.

New construction has been an appealing alternative, attracting determined buyers frustrated by the historically low supply of existing homes. Still, affordability concerns remain.

“The constraints in the housing market have created a significant amount of pent-up demand, as more and more households are living in homes they may have outgrown and are deciding to buy despite current market conditions,” said Mangold.

According to the report, new home sales activity increased the most in the south, “a region that continues to outperform due to availability of land, population and job growth, and a relatively lower cost of living,” said Mangold.

While new home sales are a much smaller share of the overall sales market than existing home sales, the inventory picture is rosier for new construction homes.

The seasonally adjusted estimate of new homes for sale at the end of September was 435,000. This represents a supply of 6.9 months at the current sales pace.

By comparison, there were 1.13 million existing homes for sale at the end of September, or the equivalent of 3.4 months’ supply at the current monthly sales pace.

Typically, the ratio of existing homes to new homes has been closer to 5 to 1, but lately it has been closer to 2 to 1, according to the National Association of Realtors.

The U.S. economy has not only defied widespread predictions of a sharp slowdown. It’s grown even faster.

But that doesn’t mean a recession is far away. The U.S. has often experienced fast growth shortly before the bottom fell out.

Let’s start with the good news.

Gross domestic product, the official scorecard of the economy, looks likely to top 4% or even 5% annual growth in the third quarter. The government will release its preliminary estimate on Thursday morning.

Economists polled by The Wall Street Journal predict 4.7% GDP in the third quarter.

Other top forecasters see even faster growth. S&P Global estimates 5.6% GDP and the Atlanta Federal Reserve GDPNow forecast projects 5.4%.

How fast is that? GDP only topped 5% once from 2010 to the start of the pandemic in early 2020.

This is not what was supposed to happen.

After solid 2%-plus growth in the first and second quarters, the economy was widely expected to slow down in response to rapidly rising interest rates.

The Federal Reserve has jacked up borrowing costs in the past year and a half to try to tame inflation, a strategy that typical depresses consumer spending and business investment. Those are the dual engines of the economy.

To some extent the Fed has succeeded. Home sales and construction, for instance, have tumbled due to the highest mortgage rates in decades. And manufacturers have taken a hit as customers curtailed purchases of goods and big-ticket items.

The annual rate of inflation, meanwhile, has tapered to 3.7% as of September from a 40-year high of 9.1% in 2022.

Still, spending and investment have not dropped off nearly as much as expected. And there are two reasons for that.

The first is a strong and ultra-tight labor market, with unemployment hovering just below 4%. Most Americans who want a job have one, and as a result, they have been able to keep spending. Travel, recreation, leisure and hospitality have been the big winners.

S&P Global estimates a flush of consumer spending in the third quarter will account for just over half of the growth.

The industrial side of the economy, for its part, has been the beneficiary of tens of billions of dollars in subsidies from the Biden administration to support green energy and bring home more manufacturing.

The U.S. has also ramped up military aid to Ukraine and has to replace outgoing equipment, weapons and ammunition.

All the government money has helped to keep manufacturers from falling too far down the well. Government outlays could add as much as 0.6 percentage points to third-quarter GDP.

Making the third quarter look even better, the U.S. trade deficit fell sharply and is likely to add 1.0 percentage point or more to GDP.

A small rebound in the production of inventories, or unsold goods, would be the icing on the cake.

So the economy is doing great, right? Maybe not.

Consumers probably can’t keep spending at their current pace since their incomes are barely rising faster than inflation. Businesses are proceeding cautiously because of higher borrowing costs. And banks are more reluctance to lend.

Other restraints on the economy include higher gasoline prices and a surge in long-term interest rates that make it far more expensive to buy houses, cars, appliances and the like.

That’s why many forecasters believe the economy start to soften in final months of 2023. S&P Global, for instance, initially projects 1.7% growth in the fourth quarter.

Nor does the third quarter’s heady growth rate suggest there is no reason to worry about a recession. The economy has expanded rapidly just before the onset of prior recessions.

The economy grew at solid 2.5% pace right before the 2007-2009 Great Recession, for example. And GDP grew a frothy 4.4% in the first quarter of 1990 just several months before a recession started.

Many of the same economic headwinds, it turns out, are still in place that led to widespread Wall Street predictions of recession earlier in the year.

Indeed, some forecasters such as the Conference Board still insist a short recession is likely in 2024. Other economists are also on guard.

“I still believe a recession is coming — though far less severe than the 2008-2009 event,” said chief economist Steve Blitz of TS Lombard.

The cumulative increase of 250 basis points (bps) repo rate by the Reserve Bank of India (RBI) and the reaction of banks in terms of transmission has still not pushed interest cost for borrowers to the pre-pandemic levels, according to a report by Bank of Baroda’s economic research department.

“While borrowers may view this current cycle as imposing an additional burden, this is because abnormal conditions typified by the pandemic had made interest rates come down to the lowest level. Hence, the present level of rates may be viewed as a correction.

“…There is still some room for upward movement in weighted average lending rate, which will keep interest costs of borrowers at the pre-pandemic level,” Dipanwita Mazumdar, economist, BoB.

The economist observed that when the pandemic started in March 2020, there was a dramatic easing in monetary policy, with repo rate hitting record low of 4 per cent. This was also reflected in the Weighted Average Lending rate (WALR), witnessing more than complete pass through in the same period.

Subsequently, the repo rate has been increased by 250 bps to 6.5 per cent. Both these cycles involved lending rates coming down first and then going up, she said.

BoB’s analysis shows that interest cost on outstanding loans as of February 2020 (under certain assumptions) got a benefit of ₹61,000 crore in FY21 and a further ₹53,000 crore in FY22 relative to FY21.

In FY20, based on the WALR, the interest outgo was ₹10.16-lakh crore (applying the the then outstanding WALR of 10.05 per cent) on a sum of ₹101.05-lakh crore (outstanding loans).

“In FY21 the cost came down to ₹9.55-lakh crore and declined further to ₹9.02-lakh crore in FY22. Compared with FY20, the cost was lower by ₹61,000 crore and ₹1.14-lakh crore, respectively. If these two years are combined, the savings in interest costs for borrowers amounted to ₹1.75-lakh crore,” said Mazumdar.

Rise in interest cost

In FY23, as interest costs rose, total interest outgo was ₹9.35-lakh crore, which though higher than that in FY22, is much lower than the FY20 cost. Therefore, as the RBI corrected the repo rate towards normal, borrowers were still not worse off compared to pre-pandemic times, opined the Economist.

She assessed that in FY24, based on assumption of unchanged WALR, the interest cost will go up to ₹9.91-lakh crore, which is again lower than FY20 level by ₹25,000 crore.

(Bloomberg) — After the most aggressive monetary-tightening campaign in four decades, academics and economic practitioners are running autopsies on what could have prevented the cost-of-living crisis and how to ensure the same mistakes won’t be repeated.

Most Read from Bloomberg

Markets have scrambled to price in high-for-longer interest rates, with a new war in the Middle East adding yet more risk to an already uncertain outlook confronting central bankers as they gather for their penultimate meetings of a tumultuous year.

The policy navel-gazing is centering around three debates. How much flexibility central banks can allow in reaching their inflation targets, the effectiveness of asset purchases in the policy mix, and the merits of monetary and fiscal coordination.

Bloomberg surveyed economists from around the world to gather views on those three debates. Their verdict: Central banks won’t break their economies in a rush to hit inflation targets, QE will be used more sparingly in the future, and fiscal policy risks countering the work of monetary authorities.

What Bloomberg Economics Says…

“A long period of galloping price gains, and fears that the last yards back to target could be most painful for workers, have reignited the debate about whether central banks should aim for a higher rate of inflation. That’s a conversation worth having. But for monetary policymakers, the imperative of retaining credibility means the right time for it is after inflation is back at target, not before.”

— Tom Orlik, chief economist

Rethinking Targets

So long as people believe prices will get back toward 2%, central bankers have some leeway in deciding how aggressive they need to be in pursuing that goal.

Economists covering 16 of the world’s most important central banks say policymakers will allow more time to bring inflation back to target if it means less damage to their economies. The Bloomberg special survey also shows that a sizable minority sees them going even further, accepting price pressures that are either slightly too strong or too weak — as long as expectations remain anchored.

Olivier Blanchard, a former IMF chief economist, has long argued in favor of raising the inflation target, and former European Central Bank Vice President Vitor Constancio has also embraced the idea. But it’s a controversial view and only possible from a position of credibility, which means central banks would likely have to get inflation back to 2% first.

“It would be a mistake of the first order to think you can change a goal you have set if you can’t achieve it,” according to Bundesbank President Joachim Nagel.

Global trends suggest inflation will be stronger than in the past, with former Bank of England Governor Mark Carney among those saying rates won’t return to pre-pandemic lows.

One lesson Gita Gopinath, the IMF’s No. 2 official, draws from the latest inflation episode is that policymakers mustn’t assume that looking through supply shocks — as text books suggest — is the optimal response. She recommends they be ready to react preemptively, even when inflation hasn’t yet spun out of control.

They may be called into action soon on that front, should an escalation in the conflict in the Middle East hit oil deliveries.

When the next big global slowdown comes, though, flexibility may be needed the other way. Europe’s eight-year experiment with negative rates ended with mixed reviews last summer as to whether it was all worth it.

The Bank for International Settlements argues that there’s room for greater tolerance for moderate shortfalls even if they’re persistent, because “low-inflation regimes, in contrast to high-inflation ones, have self-stabilizing properties.”

Rethinking Quantitative Easing

With a more flexible approach to those 2% targets, monetary policy after the 2008 financial crisis would have looked very different in many parts of the world. Trillions of dollars, euros, yen and pounds of asset purchases did little to raise prices in the face of global disinflationary forces until governments used the money they raised to stuff cash into consumers’ pockets during Covid lockdowns.

But that’s also been blamed for distorting financial markets. Episodes such as the Silicon Valley Bank blow-up are seen by some as a direct result of central bank reserves creation under QE, along with regulatory and supervision failures.

Only 40% of economists surveyed predict central banks will use QE the same way as they did before. A quarter expect them to deploy it more sparingly, about 30% see its only role going forward as a tool to address financial-stability concerns and a small minority doesn’t see it being used again at all.

There are other problems with bond-buying that may affect how it’s used in the future. QE effectively swaps long-term borrowing costs for short-term ones. What’s been a lucrative deal for taxpayers when official interest rates were low has now turned into a disastrous trade.

The clearest depiction of the problem is in the UK, where the BOE secured taxpayer indemnity for any losses on QE. Over the next decade, it estimates, its purchases will cost the government over £200 billion ($243 billion).

And policymakers have little experience in unwinding their balance sheets, where small mistakes can trigger big market turbulence.

The Fed experienced some of that when it tried to shrink bond holdings between 2017 and 2019. More recent efforts to reduce portfolios have progressed rather smoothly, partially because central banks have amassed so much debt over the years that they’re far away from any thresholds that would trigger a squeeze.

But the fact that they’re treating quantitative tightening as a technical adjustment rather than a part of their efforts to conquer inflation raises questions about the future use of a tool that’s only trusted to work one way.

The ECB faces an extra legal burden on bond holdings that comes with operating in a currency union of 20 countries. Concerns around illegally financing governments and debt mutualization have already landed the central bank in court several times.

Mixing Policies

Low interest rates and large-scale QE programs allowed treasuries to borrow on the cheap to finance stimulus campaigns, protecting labor markets, businesses and consumers from collapse. But the spending blowout throughout and since the pandemic — part critical emergency funding, part political need to show an all-hands-on-deck approach in crisis — contributed to the latest outbreak in inflation.

While the same kind of pulling in the same direction is needed to restrain demand, many governments are concerned that if they tighten policy too hard, voters will kick them out and replace them with populists or extremists. That’s reviving questions about whether central banks can deliver price stability all on their own.

“If we were designing optimal policy arrangements from scratch, monetary and fiscal policy would both have a role in managing the economic cycle and inflation, and that there would be close coordination,” Philip Lowe said in his last speech as Australian central bank governor in September.

Economists surveyed by Bloomberg predict fiscal policy will somewhat counteract the Fed’s efforts to rein in inflation in the US.

“It’s true that there are circumstances where working hand in hand and supporting each other has proved helpful,” ECB President Christine Lagarde told a panel discussion in June at the institution’s annual economic forum.

Fed Chair Jerome Powell, who sat to her right, signaled he wasn’t ready to rely on that kind of cooperation. “Our assignment is to deliver price stability kind of regardless of the stance of fiscal policy.”

Central bankers warn that any failure to scale back fiscal spending risks coming at the cost of yet higher interest rates. They also want elected officials to put in place policies that help deliver sustainable growth.

“A change in mindset needs to happen,” said Agustin Carstens, the former governor of the Bank of Mexico who’s now the general manager of the BIS. “Growth needs to depend less on fiscal and monetary policy, it should depend more on structural policies.”

–With assistance from Philip Aldrick, Rich Miller, Harumi Ichikura, Cynthia Li, Sarina Yoo, Andrew Langley and Zoe Schneeweiss.

NEW YORK (Reuters) – Relentless selling of U.S. government bonds has brought Treasury yields to their highest level in more than a decade and a half, roiling everything from stocks to the real estate market.

The yield on the benchmark 10 year Treasury – which moves inversely to prices – briefly hit 5% late Thursday, a level last seen in 2007. Expectations that the Federal Reserve will keep interest rates elevated and mounting U.S. fiscal concerns are among the factors driving the move.

Because the $25-trillion Treasury market is considered the bedrock of the global financial system, soaring yields on U.S. government bonds have had wide-ranging effects. The S&P 500 is down about 7% from its highs of the year, as the promise of guaranteed yields on U.S. government debt draws investors away from equities. Mortgage rates, meanwhile, stand at more than 20-year highs, weighing on real estate prices.

“Investors have to take a very hard look at risky assets,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities in New York. “The longer we remain at higher interest rates, the more likely something is to break.”

Fed Chairman Jerome Powell on Thursday said monetary policy does not feel “too tight,” bolstering the case for those who believe interest rates are likely to stay elevated.

Powell also nodded to the “term premium” as a driver for yields. The term premium is the added compensation investors expect for owning longer-term debt and is measured using financial models. Its rise was recently cited by one Fed president as a reason why the Fed may have less need to raise rates.

Here is a look at some of the ways rising yields have reverberated throughout markets.

Higher Treasury yields can curb investors’ appetite for stocks and other risky assets by tightening financial conditions as they raise the cost of credit for companies and individuals.

Elon Musk warned that high interest rates could sap electric-vehicle demand, which knocked shares of the sector on Thursday. Tesla’s shares closed the day down 9.3%, as some analysts questioned whether the company can maintain the runaway growth that has for years set it apart from other automakers.

With investors gravitating to Treasuries, where some maturities currently offer far above 5% to investors holding the bonds to term, high-dividend paying stocks in sectors such as utilities and real estate have been among the worst hit.

The U.S. dollar has advanced an average of about 6.4% against its G10 peers since the rise in Treasury yields accelerated in mid-July. The dollar index, which measures the buck’s strength against six major currencies, stands near an 11-month high. A stronger dollar helps tighten financial conditions and can hurt the balance sheets of U.S. exporters and multinationals. Globally, it complicates the efforts of other central banks to tamp down inflation by pushing down their currencies. For weeks, traders have been watching for a possible intervention by Japanese officials to combat a sustained depreciation in the yen, down 12.5% against the dollar this year.

“The correlation of the USD with rates has been positive and strong during the current policy tightening cycle,” BofA Global Research strategist Athanasios Vamvakidis said in a note on Thursday.

The interest rate on the 30-year fixed-rate mortgage – the most popular U.S. home loan – has shot to the highest since 2000, hurting homebuilder confidence and pressuring mortgage applications. In an otherwise resilient economy featuring a strong job market and robust consumer spending, the housing market has stood out as the sector most afflicted by the Fed’s aggressive actions to cool demand and undercut inflation.

U.S. existing home sales dropped to a 13-year low in September.

As Treasury yields surge, credit market spreads have widened with investors demanding a higher yield on riskier assets such as corporate bonds. Credit spreads blew out after a banking crisis this year, then they narrowed in subsequent months.

The rise in yields, however, has taken the ICE BofA High Yield Index near a four-month high, adding to funding costs for prospective borrowers.

Volatility in U.S. stocks and bonds has bubbled up in recent weeks as expectations have shifted for Fed policy. Anticipation of a surge in U.S. government deficit spending and debt issuance to cover those expenditures has also unnerved investors.

The MOVE index, measuring expected volatility in U.S. Treasuries, is near its highest in more than four months. Volatility in equities has also picked up, taking the Cboe Volatility Index to a five-month peak.

(This story has been refiled to add the dropped word ‘briefly’ in paragraph 2)

(Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates)

The numbers: Home sales in September fell to the lowest level since 2010, as high mortgage rates continue to hammer the housing market.

Aside from low inventory, rising rates are eroding buyers’ purchasing power, and drying up demand. Sales of previously owned homes fell by 2% to an annual rate of 3.96 million in September, the National Association of Realtors said Thursday.

That’s the number of homes that would be sold over an entire year if sales took place at the same rate every month as they did in September. The numbers are seasonally adjusted.

The drop in sales was slightly better than what Wall Street was expecting. They forecasted existing-home sales to total 3.9 million in September.

Compared to September 2022, home sales are down by 15.4%.

Key details: The median price for an existing home in September rose for the third month in a row to $394,300. Prices are up 2.8% from a year ago. That was the highest price for the month of September since NAR began tracking the data.

Home prices peaked in June 2022, when the median price of a resale home hit $413,800.

Around 26% of properties are being sold above list price, the NAR noted.

The total number of homes for sale in September fell by 8.1% from last year, to 1.13 million units. Housing inventory for the month of September was the lowest since 1999, when the NAR began tracking the data.

Homes listed for sale remained on the market for 21 days on average, up from the previous month. Last September, homes were only on the market for 19 days.

Sales of existing homes rose only in the Northeast in September, as compared with the previous month, by 4.2%. The median price of a home in the region was $439,900.

All-cash buyers made up 29% of sales, highest since January 2023. The share of individual investors or second-home buyers was 18%. About 27% of homes were sold to first-time home buyers.

Big picture: The U.S. housing market is in the midst of a serious slowdown that is primarily driven by high mortgage rates. High rates spook home buyers, drying up demand, and high rates also deter homeowners from selling since they may have to purchase another home. For a homeowner with a 3% mortgage rate for the next few decades, there’s little incentive to move.

And the residential sector is likely to see sales fall further in October’s data, as the 30-year mortgage inches even higher. Demand for mortgages has collapsed, and some outlets like Mortgage News Daily are quoting a rate of 8% for the 30-year.

Existing-home sales in 2023 could fall to the slowest pace since the housing bubble burst in 2008, real-estate brokerage Redfin said on Thursday, at a 4.1 million pace.

What the realtors said: “Mortgage rates and limited inventory has been the story throughout this year — no different this month, other than the fact that interest rates are moving higher,” said Lawrence Yun, chief economist at the National Association of Realtors.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” he added. “We don’t want the Fed to overdo it and cause great harm to real estate.”

Yun also questioned whether there will be a “fundamental change” or a temporary one to the “American way of life” due to the slowdown in sales.

Market reaction: Stocks were down in early trading on Thursday. The yield on the 10-year note BX:TMUBMUSD10Y

rose above 4.9%.

U.S. Federal Reserve Chairman Jerome Powell holds a press conference after the release of the Fed policy decision to leave interest rates unchanged, at the Federal Reserve in Washington, U.S, September 20, 2023.

Evelyn Hockstein | Reuters

Federal Reserve Chair Jerome Powell is set to deliver what could be a key policy address Thursday, in which he will be tasked with convincing markets the central bank is committed to keep hammering away at inflation, but perhaps now needs a little less force.

The top monetary policymaker will speak at noon ET to the Economic Club of New York at a critical time for the U.S. economy.

Inflation numbers have been improving lately, but Treasury yields have been surging, sending conflicting messages about where monetary policy might be headed. Markets largely expect the Fed to stay on hold with rates, but they will be looking to Powell for confirmation and clarification on how officials view both current conditions and longer-term trends.

“Powell is always tacking back to whatever helps feed the narrative that they need to stay vigilant, and for understandable reasons,” said Luke Tilley, chief economist at Wilmington Trust. “I just expect him to keep talking about the strength of the economy and the surprising strength of the consumer in the third quarter as a risk for inflation. That is enough ammunition to keep talking about staying vigilant.”

Essentially, Tilley expects the Powell message to break into three parts: The Fed needed to get rates high quickly, which it did; that it had to find a peak level, which is part of the current debate; and that it needs to figure out how long rates need to stay this high to get inflation back to its 2% target.

“Really, their ultimate goal is to keep financial conditions tight so inflation comes down,” he said. “He’s going to use that framework, even if he’s dovish about Nov. 1 [the next Fed rate decision] or December to shift the hawkishness to that third question of how long to keep them this high.”

“Higher for longer” has become an unofficial mantra in recent days, with Philadelphia Fed President Patrick Harker earlier this week mentioning the term specifically for how he feels about policy.

Harker was one of several Fed officials, including governors Philip Jefferson, who spoke earlier this month, and Christopher Waller, who spoke Wednesday, to advocate holding off on rate hikes at least in the immediate future while they weigh the impact of incoming data. Waller said the Fed can “wait, watch and see” before it moves on rates.

Powell is expected to join the chorus Thursday, even if his message is filled with caveats about not becoming complacent in the fight against inflation.

“Powell has to present himself to investors as the dispassionate neutral leader and allow [others] to be more aggressive,” said Jeffrey Roach, chief economist for LPL Financial. “They’re not going to declare victory, and that is one reason why Powell is going to continue to talk somewhat hawkish.”

To that point, New York Fed President John Williams on Wednesday moved some of the way there, when he repeated another familiar mantra, that the Fed will have to keep the “restrictive stance of policy in place for some time” to deal with inflation, according to a Reuters report.

Like the other speakers, Powell likely will reiterate a data-dependent focus for the Fed after a much more aggressive path in which it has raised its benchmark borrowing rate 11 times for a total of 5.25 percentage points, its highest level in 22 years. The Fed opted not to hike in September.

He also, though, will be looked to for some guidance as to how he feels about rising yields, in light of the 10-year Treasury having inched closer to 5% — its highest point in 16 years.

The chair “will stick to the message … that the data has been coming in stronger than expected, but there has also been a big move in yields, which has tightened financial conditions, so no urgency for a policy response in November and the Fed can adopt a wait-and-see approach,” Krishna Guha, head of global policy and central bank strategy at Evercore ISI, said in a client note.

Guha said that a Fed on hold now will only be a “down payment” on “extra cuts” in rates for 2024 as inflation and economic growth both weaken.

U.S. Treasury yields rose on Wednesday with the 10-year hitting a fresh multiyear high as investors digested the latest economic data and considered the outlook for Federal Reserve interest rates.

The 10-year Treasury yield gained nearly 7 basis points to 4.911%, putting it above 4.9% for the first time since 2007. Meanwhile, the 2-year Treasury yield was trading almost 2 basis points up at 5.231%, around levels last seen in 2006.

Also notably, the 5-year Treasury moved as high as 4.937%, its top level since 2007.

Yields and prices move in opposite directions and one basis point equals 0.01%.

Investors considered fresh economic data as uncertainty about the path ahead for Fed monetary policy grew in recent weeks.

Housing starts accelerated in September, but rose as a slower-than-expected rate, according to data released Wednesday. Building permits fell in the month, but lost less than economists anticipated.

Retail sales figures for September, which were published Tuesday, increased by 0.7% for the month. That’s far higher than the 0.3% anticipated by economists surveyed by Dow Jones, and indicates resilience from consumers in light of higher interest rates and other economic pressures.

The data brought up renewed concerns over the outlook for interest rates, with some investors viewing it as an indication that rates may be hiked further or at least kept elevated for longer.

Markets are still pricing in a 90% chance that rates will remain unchanged when the Fed announces its next monetary decision on Nov. 1, but the probability of a December rate increase rose after Tuesday’s data, according to the CME Group’s FedWatch tool.

In recent days and weeks, various Fed officials have indicated that the central bank may be done hiking, especially as higher Treasury yields are contributing to tighter economic conditions. Further comments from policymakers are expected this week, including by Fed Chairman Jerome Powell, and investors are looking to their comments for hints about their policy expectations.

Upcoming economic data may also influence opinion among both investors and Fed officials.

The numbers: Sales at U.S. retailers jumped a bigger-than-expected 0.7% in September in a sign households have enough buying power to keep the economy expanding.

The increase was spurred by strong demand at auto dealers and Internet stores. Higher gas prices also played a role, however.

Economists polled by The Wall Street Journal had forecast a 0.2% increase in sales.

Retail sales represent about one-third of all consumer spending and usually offer clues on the strength of the economy.

Yet September also falls between the busy back-to-school and holiday-shopping seasons and tends to reveal less about how consumers are doing.

Key details: Auto dealers posted a 1% gain in sales and helped to inflate the headline number. Auto sales account for about 20% of all retail sales.

Receipts at gas stations also rose nearly 1%, but that largely reflected higher gas prices. That’s not a good thing for households.

Retail sales advanced a still-robust 0.6% when car dealers and gas stations are set aside, which gives a better idea of consumer demand.

Sales at internet retailers stayed on a hot streak. They rose 1.1%.

Sales climbed 0.9%% at bars and restaurants. Restaurant sales tend to rise when the economy is healthy and Americans feel secure in their jobs. Sales decline during times of economic stress.

Over the past year, restaurant sales have surged 9.2% — more than twice as fast as inflation.

On the negative side of the ledger, sales fell at big-box electronics stores, clothing stores and home centers such as Home Depot HD, +1.85%

and Lowe’s LOW, +1.28%.

Sales in August were also revised up to show a 0.8% increase instead of 0.6%.

Big picture: The retail sales report is the latest to suggest the economy is still expanding at solid pace and perhaps not decelerating as much as the Federal Reserve would like to help slow the rate of inflation.

Consumer spending has stayed fairly healthy because of rising wages and the lowest unemployment rate in decades. What’s more, incomes are finally increasing faster than inflation for the first time in a few years.

Yet higher interest rates are pinching households and businesses and are bound to slow the economy in the months ahead. If so, retail spending is also likely to soften.

Looking ahead: “Consumer spending shows little sign of flagging, especially when purchases increased on everything from durable goods, such as autos, to the least durable goods, food and drink at bars and restaurants,” said Robert Frick, corporate economist at Navy Federal Credit Union.

“As long as the jobs market remains healthy, consumers should have the cash and confidence to maintain spending.”

Market reaction: Before the markets opened, the Dow Jones Industrial Average DJIA

and S&P 500 SPX

were set to open lower in Tuesday trades.

The volatility in the world’s biggest bond market in recent weeks has been too much for U.S. stocks to handle as investors come to terms with the likelihood that interest rates will remain high deep into 2024 until underlying inflationary pressures ease.

The U.S. Treasury market, the bedrock of the global financial system, has been hammered by repeated selling since late September, sending the yields on the 10-year and 30-year Treasurys to levels last seen when the economy was moving toward the financial crisis in 200, before yields fell again in the past week.

Back in September a bond market selloff was fueled by a hawkish outlook from the Federal Reserve, along with mounting concern about the U.S. fiscal deficit and federal debt amid the potential for a government shutdown if a budget for the 2024 fiscal year is not settled by mid-November.

Earlier this week though, increased uncertainty about the conflict in the Middle East propelled demand for safer assets and caused longer-term bond prices to jump and their yields to fall.

Investors are now wondering what it will take for interest rates and bond yields to fall in the months ahead and whether a retreat in yields could eventually push stocks higher to rally into the year-end.

Tim Hayes, chief global investment strategist at Ned Davis Research, said “excessive pessimism” in the bond market is setting up for a relief rally both in stock and bond prices as “there’s not as much inflationary pressures as the market has been pricing in,” he told MarketWatch in a phone interview on Thursday.

Hayes said his team found the bond sentiment data has started to reflect a “decisive reversal” away from too much pessimism in the Treasury market which could send bond yields lower and boost equities given the inverse correlations between the S&P 500 SPX

and the 10-year Treasury note yield BX:TMUBMUSD10Y.

Meanwhile, some analysts said disinflation may not be enough for the Federal Reserve to drop its “higher-for-longer” interest rate narrative which was primarily responsible for the big spike in yields since September.

The economy needs a slowdown in the consumer sector for some relaxation in the Fed’s “higher-for-longer” narrative and to maybe push policymakers to adopt a more flexible outlook for its long-term guidance, said Thierry Wizman, global FX and interest rates strategist at Macquarie.

“Of course, the Fed right now is certainly not saying anything that’s remotely suggestive of ‘high-for-long’ being taken away or being removed or negated, so I don’t expect yields to fall a lot unless we start to get reasons to believe the Fed is going to remove that narrative based on the economic data,” Wizman told MarketWatch via phone.

However, Wizman said he is confident that the U.S. consumption data will weaken over the next few months when major consumer-product and -service companies start to provide guidance for the fourth quarter, and when U.S. consumers, which have been trapped in a web of conflicting signals on the health of the economy, open their wallet for the holiday shopping season.

“This will produce some weakness on the consumer side of the market and there’s no doubt the slowdown will be more pronounced than most people expect in the economy, [but] that will be the positive scenario for bonds,” said Marco Pirondini, head of U.S. equities at Amundi U.S., in an interview with MarketWatch.

However, that also means investors should not be “too anxious to buy dips in the stock market” because it would be very unusual if the stock market doesn’t see “multiple compression” with Treasury yields at 16-year highs, Wizman said. “Stocks would still look too rich even if the Fed drops the ‘higher-for-longer’ narrative in the first quarter of 2024.”

The “higher-for-longer” mantra is an idea Fed officials have tried to get the market to absorb in recent months, with Fed Chair Powell hardening his rhetoric at the September FOMC meeting, pointing potentially to more rate hikes or, more importantly, interest rates that stay higher for longer.

Fed officials saw interest rates coming down to 5.1% in 2024, higher than June’s outlook for rates to finish next year at 4.6%, according to the latest Summary of Economic Projections at the September policy meeting.

However, Wizman characterized the “higher-than-longer” narrative as a “publicity stunt,” as he thought Fed officials simply wanted to signal to the market that they were frustrated that financial conditions hadn’t measurably tightened enough in 2023, so they utilized the narrative to get rising Treasury yields to do some of the “heavy lifting.”

“… Fed officials are not really serious about ‘higher-for-longer’ – they just did it to drive long-term yields higher for now,” he added.

If a slowdown in the consumer sector of the economy and ongoing disinflation are powerful enough to sap Fed’s rate expectations, Treasury yields could continue to decline without having to have a calamity or big recession in the U.S. economy to drive investors back to the safe-haven assets like Treasurys, strategists said.

Meanwhile, stock-market seasonality may also help lift sentiment. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the large-cap S&P 500 index up nearly 80% of the time dating back to 1950 and gaining more than 4% on average.

The S&P 500 has risen 0.9% so far in the fourth quarter, while the Dow Jones Industrial Average DJIA

is up 0.5% and the Nasdaq Composite COMP

has advanced 1.4% in October, according to FactSet data.

“So you have this situation where sentiment got stretched and now sentiment is reversing with more confidence that bond yields have reached their peak, so equities can rally moving into the end of the year, and that should start to become increasingly evident,” said Hayes.

The yield on the 10-year Treasury note dropped 8.2 basis points to 4.628% on Friday, while the yield on the 30-year Treasury BX:TMUBMUSD30Y

declined by 9.2 basis points to 4.777%. The 30-year yield fell 16.4 basis points this week, its largest weekly drop since the period that ended March 10, according to Dow Jones Market Data.

Investor and personal finance author Ric Edelman believes it’s a practical strategy to take chips off the table right now.

“It comes down to behavioral finance. It comes down to human emotion,” the Edelman Financial Engines founder told CNBC’s “ETF Edge” this week. “Do you have the stomach? Does your spouse have the stomach to hang in there if things get ugly like they did in ’01, ’08, 2020? Can you hang in there?”

Edelman added there’s a “laundry list of reasons” to be cynical right now. He includes struggles in the real estate market, high interest rates, government shutdown risks and the Israel-Hamas war.

“It’s easy to be negative and that can cause you to say, ‘Why do I want to put myself in a position of maybe losing another 20% or 30% of my money when I’ve already amassed an awful lot of money and I am already in my ’60s or ’70s and I need the safety and protection and by the way get five percent in my bonds or U.S. Treasury or my bank CD? Why don’t I just park it? Earn 5%. Call it a day,’ he said.

Edelman acknowledges the strategy could be less profitable, but he suggests it’s important to sleep better at night.

“I’m not sure everybody in the investment world is acting logically as opposed to emotionally. You’ve got to know yourself,” said Edelman.

The Capital Group’s Holly Framsted is also seeing investors de-risk, and her firm is trying to cater to them by offering a new batch of exchange-traded funds focused on fixed income.

“We’re seeing increased interest in short-duration fixed income,” said the firm’s head of global product strategy and development.

Framsted speculates the investors are making the move to short-duration funds in response to the volatility of today’s market.

“[The Capital Group Core Bond ETF] was among the original six funds that we launched,” Framsted said. “We’re seeing interest among our client base who tend to be longer-term oriented in nature across the full spectrum. But certainly, a lot of conversations in the short-duration space given the environment that we’re in.”

The firm’s bond ETF is virtually flat since its Sept. 28 launch. The Capital Group managed more than $2.3 trillion as of June 30, according to the firm’s website.

Megabanks like JPMorgan Chase and Wells Fargo have an edge in net interest income over their regional-bank rivals, according to Brian Mulberry at Zacks Investment Management. “If it’s David versus Goliath, Goliath is only getting bigger, and it seems like they’re winning more at this point in time,” he says.

Bloomberg

Two of the country’s biggest banks continue to rake in profits as the costs of their deposits rise less than expected, but it’s unclear how long the good times will last, or whether smaller competitors can pull off the same trick.

During the third quarter at JPMorgan Chase, net interest income increased 30% year over year, while it rose by 8% at Wells Fargo, as the interest the two megabanks charged on loans outstripped what they had to pay their depositors.

But executives at both companies were uncertain about whether their outperformance will continue, underlining an industrywide challenge if interest rates stay high longer than previously anticipated.

“We’re all in a bit of uncharted territory at this point with rates being where they are and the pace at which they got there,” Michael Santomassimo, chief financial officer at the $1.9 trillion-asset Wells Fargo, said Friday on an earnings call.

Interest expenses in the banking industry have jumped sharply, thanks to the Federal Reserve hiking rates from near 0% to more than 5% since March 2022. JPMorgan and Wells haven’t been immune to rising deposit costs, but the two banking giants have been able to keep a tighter lid on them than some competitors.

Still, JPMorgan Chase CFO Jeremy Barnum said Friday that the $3.9 trillion-asset bank has been “cautious about recognizing” that current levels of deposit costs don’t seem sustainable.

The growing likelihood of the Fed keeping rates higher for longer has clouded the profitability outlook for banks of all sizes — an issue that analysts will watch closely when regional banks begin to report their earnings next week. Industrywide net interest income is expected to decline in 2024 before picking back up in 2025, according to Jefferies research published this week.

Stronger-than-expected net interest income figures at JPMorgan Chase and Wells Fargo helped boost their stock prices on Friday by 1.50% and 2.99%, respectively. Shares in Citigroup, which reported a 10% pickup in net interest income, were roughly flat on Friday. Bank of America, the other of the four largest U.S. banks, is scheduled to report results on Tuesday.

Pittsburgh-based PNC Financial Services Group on Friday reported slightly lower net interest income for the third quarter, and its stock price fell by 2.62%. Executives at the $557 billion-asset bank said deposit-cost pressures have slowed, but they noted that the outlook on Fed policy is unclear. PNC said Friday its layoffs reported this week would affect about 4%, or 2,400, of its more than 60,000 employees.

JPMorgan revised higher its estimate of full-year net interest income, a key revenue driver in 2023. America’s largest bank now expects $88.5 billion of net interest income, up more than $2 billion from guidance released earlier this year.

While big banks are enjoying net interest income strength, analysts expect the comparable figures at regional banks to come under pressure in the coming months, thanks in part to rising deposit costs. Net interest income measures the difference between a bank’s lending revenue and its deposit costs.

Megabanks have more diversified streams of revenue than their smaller competitors, plus a broader footprint to pull in deposits, said Brian Mulberry, a portfolio manager at Zacks Investment Management.

“If it’s David versus Goliath, Goliath is only getting bigger, and it seems like they’re winning more at this point in time,” Mulberry said.

Still, even the largest banks have been forced to pay customers higher interest rates on deposit accounts. During the third quarter, interest expenses at JPMorgan rose 170% from the same period a year earlier to $21.8 billion. At Wells Fargo, interest-related expenses totaled nearly $9 billion between July and September, 275% higher than in the third quarter of 2022.

Total profit at JPMorgan rose 35% year over year to $13.2 billion in the third quarter. Wells Fargo’s earnings increased 61% from the third quarter of 2022, when it reported unusually high expenses tied to its regulatory troubles, to $5.8 billion in the latest quarter. At JPMorgan, revenue increased 22% to $39.9 billion during the same period, while it rose 7% to $20.9 billion at Wells.

JPMorgan said that its purchase of part of First Republic Bank drove about $1.1 billion of profit and $2.2 billion in revenue during the third quarter. But it also said that those metrics would have risen even without the acquisition, which was arranged by the Federal Deposit Insurance Corp. after First Republic failed.

Growing credit card balances helped drive loan growth at JPMorgan, which saw an 18% increase in total loans. Wells Fargo, which has been revamping its credit card portfolio under CEO Charlie Scharf, also reported double-digit growth in its consumer card business. In the San Francisco bank’s auto and home lending portfolios — two areas where it has been scaling back — loan volumes declined.

Wells Fargo’s overall loan totals were down slightly from the third quarter of last year, with Scharf citing weaker loan demand and tighter underwriting criteria amid a more uncertain economic outlook.

The economic environment will drive the direction of loan growth moving forward, JPMorgan CEO Jamie Dimon said on a call with analysts.

“Depending on what you believe about a soft landing, mild recession, no landing, you have slightly lower or slightly higher loan growth,” Dimon said. “But in any case, I would expect it to be relatively muted.”

A construction in a multifamily and single family residential housing complex is shown in the Rancho Penasquitos neighborhood, in San Diego, California, September 19, 2023.

Mike Blake | Reuters

In theory, getting inflation closer to the Federal Reserve’s 2% target doesn’t sound terribly difficult.

The main culprits are related to services and shelter costs, with many of the other components showing noticeable signs of easing. So targeting just two areas of the economy doesn’t seem like a gargantuan task compared to, say, the summer of 2022 when basically everything was going up.

In practice, though, it could be harder than it looks.

Prices in those two pivotal components have proven to be stickier than food and gas or even used and new cars, all of which tend to be cyclical as they rise and fall with the ebbs and flows of the broader economy.

Instead, getting better control of rents, medical care services and the like could take … well, you might not want to know.

“You need a recession,” said Steven Blitz, chief U.S. economist at GlobalData TS Lombard. “You’re not going to magically get down to 2%.”

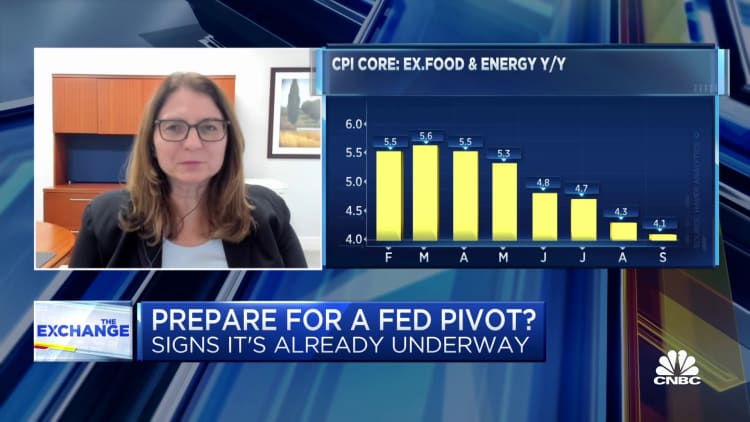

Annual inflation as measured by the consumer price index fell to 3.7% in September, or 4.1% if you kick out volatile food and energy costs, the latter of which has been rising steadily of late. While both numbers are still well ahead of the Fed’s goal, they represent progress from the days when headline inflation was running north of 9%.

The CPI components, though, told of uneven progress, helped along by an easing in items such as used-vehicle prices and medical care services but hampered by sharp increases in shelter (7.2%) and services (5.7% excluding energy services).

Drilling down further, rent of shelter also rose 7.2%, rent of primary residence was up 7.4%, and owners’ equivalent rent, pivotal figures in the CPI computation that indicates what homeowners think they could get for their properties, increased 7.1%, including a 0.6% gain in September.

Without progress on those fronts, there’s little chance of the Fed achieving its goal anytime soon.

“The forces that are driving the disinflation among the various bits and micro pieces of the index eventually give way to the broader macro force, which is rising, which is above-trend growth and low unemployment,” Blitz said. “Eventually that will prevail until a recession comes in, and that’s it, there’s nothing really much more to say than that.”

On the bright side, Blitz is among those in the consensus view that see any recession being fairly shallow and short. And on the even brighter side, many Wall Street economists, Goldman Sachs among them, are coming around to the view that the much-anticipated recession may not even happen.

In the interim, though, uncertainty reigns.

“Sticky-price” inflation, a measure of things such as rents, various services and insurance costs, ran at a 5.1% pace in September, down a full percentage point from May, according to the Cleveland Fed. Flexible CPI, including food, energy, vehicle costs and apparel, ran at just a 1% rate. Both represent progress, but still not a goal achieved.

Markets are puzzling over what the central bank’s next step will be: Do policymakers slap on another rate hike for good measure before year-end, or do they simply stick to the relatively new higher-for-longer script as they watch the inflation dynamics unfold?

“Inflation that is stuck at 3.7%, coupled with the strong September employment report, could be enough to prompt the Fed to indeed go for one more rate hike this year,” said Lisa Sturtevant, chief economist for Bright MLS, a Maryland-based real estate services firm. “Housing is the key driver of the elevated inflation numbers.”

Higher interest rates’ biggest impact has been on the housing market in terms of sales and financing costs. Yet prices are still elevated, with concern that the high rates will deter construction of new apartments and keep supply constrained.

Those factors “will only lead to higher rental prices and worsening affordability conditions in the long run,” wrote Christopher Bruen, senior director of research at the National Multifamily Housing Council. “Rising rates threaten the strength of the broader job market and economy, which has not yet fully digested the rate hikes already enacted.”

The notion that rate increases totaling 5.25 percentage points have yet to wind their way through the economy is one factor that could keep the Fed on hold.

That, however, goes back to the idea that the economy still needs to cool before the central bank can complete the final mile of its race to bring down inflation to the 2% target.

One positive in the Fed’s favor is that pandemic-related factors largely have washed out of the economy. But other factors linger.

“Pandemic-era effects have a natural gravitational pull and we’ve seen that take place over the course of the year,” said Marta Norton, chief investment officer for the Americas at Morningstar Wealth. “However, bringing inflation the remainder of the distance to the 2% target requires economic cooling, no easy feat, given fiscal easing, the strength of the consumer and the general financial health in the corporate sector.”

Policymakers have been banking on the notion that when existing rental leases expire, they will be renegotiated at lower prices, bringing down shelter inflation. However, the rising shelter and owners’ equivalent rent numbers are running counter to that thinking even though so-called asking rent inflation is easing, said Stephen Juneau, U.S. economist at Bank of America.

“Therefore, we must wait for more data to see if this is just a blip or if there is something more fundamental driving the increase such as higher rent increases in larger cities offsetting softer increases in smaller cities,” Juneau said in a note to clients Thursday. He added that the CPI report “is a reminder that we do not have good historic examples to lean on” for long-term patterns in rent inflation.

The Federal Reserve is expected to further hike interest rates before the end of the year, and the average credit card interest rate is already at an all-time high. The average rate for existing accounts is at 22.77%, the highest it has been in 30 years, according to WalletHub.

Automated payment options can help credit card holders bypass late payment fees. While cardholders who use automated payment features typically set them for more than the minimum due, they also tend to pay off less of their monthly balance than customers making manual payments, according to a 2022 study.

Such cardholders will end up paying more in interest in the long run if they don’t pay their statement balance in full each month, experts say.

“You can set it up for a lower payment,” said Sara Rathner, credit cards expert and writer at NerdWallet, referring to a monthly automated card payment. “If you still have a balance, [that] will roll over as long as it’s unpaid.” But that unpaid balance will be subject to interest charges.

Avoid paying more in interest and fees by setting up your credit card automated payments to cover the entire statement balance, experts say. If you check your account online, you may also see a “current” balance that includes newer charges, but you only have to pay the statement balance in full each month to avoid interest charges.

If you can’t pay your statement balance in full, be sure to make smaller payments on a regular basis to keep current and chip away at your overall balance, said Nick Ewen, director of content at The Points Guy. Not doing so can mean hefty late fees in addition to accrued interest.

You usually can pay off your statement or current balance whenever you like. “There’s no penalty charge on your card if you pay your statement balance before the due date,” Ewen added.

Here are some of the best practices cardholders should consider:

Ask your lender if you can change your card payment due date to a few days after your paycheck is deposited, said Rathner. This way, you’re aware of how much money is available in your checking account before a scheduled automatic card payment goes through and you won’t overdraft your account, she added.

Log into your credit card account online or call a customer service agent to find out what features you have available to facilitate this.

Zero percent annual percentage rate offers are usually good for 12 to 18 months. However, if a cardholder does not make a minimum payment, the card issuer can revoke the 0% APR offer and push the customer into an APR of 29% or higher, said Ewen.

Make sure to read the fine print and make all the payments to keep the offer rate. Additionally, pay off the full balance before the promotion expires. Otherwise, you will be hit with interest charges at that point, he added.

If you’re carrying credit card debt, consider doing a balance transfer, said Ewen. Some credit cards offer a 0% APR for balance transfers for, as an example, a one-time fee of 3% to 5% or $5, he said. If you transfer a balance from one card to another for a 12-month 0% APR, you have a year to pay off the balance as long as you pay it off by the time the introductory special is over.

Additionally, if the terms change with one of your existing credit cards, most larger credit card companies will offer you a product change, said Winnie Sun, co-founder and managing director of Sun Group Wealth Partners in Irvine, California.

Instead of closing the affected card, move to another card from the issuer that has no annual fee, she added. This is helpful if you have a high-fee credit card and want to keep the overlying credit line high.

“It doesn’t require credit pool and reduces credit card expenses,” said Sun, a member of CNBC’s Advisor Council. Call the provider and see if a product change is available.