Now to your question: Should you contribute to your RRSP or TFSA? I don’t know your circumstances, but I can show you the math. In the table below, you are going to see that there is no real difference if your marginal tax rate is the same at time of contribution and time of withdrawal.

RRSP vs. TFSA comparison on a $10,000 contribution over one year

RRSP

TFSA

Gross contribution

$10,000

$10,000

Income tax (30% tax rate)

$0

$3,000

Net contribution

$10,000

$7,000

5% investment growth

$500

$350

Value of account

$10,500

$7,350

Tax owing

$3,150

$0.00

After tax value

$7,350

$7,350

The math for retires investing in an RRSP and TFSA

The above table shows that all things being equal a dollar invested into a RRSP or TFSA yields the same results. This is why it’s argued that an RRSP provides tax-free growth after all if, dollar for dollar, it gives the same after-tax value as a TFSA.

How could it not?

You may have questions about the table. For example, if you invest $10,000 and end up with $7,350 after one year, how is that a good investment? The $10,000 number is a before-tax figure. Remember, if you’re given $10,000 at the beginning of the year, and have a marginal tax rate of 30%, then you would be left with $7,000. Investing in a RRSP or TFSA leaves you with $7,350 after tax, so you have a gain.

The other thing to remember is that RRSP contributions are made with pre-taxed money and TFSA contributions are made with after-tax money. This is why you see the $3,000 income tax entry under the TFSA column, to make it a fair comparison.

Where should Canadian retirees put their money

Now to your question Gary, should you contribute to your RRSP or TFSA? You see there’s no difference between investing inside an RRSP or a TFSA if your marginal tax rate is the same at time of contribution and withdrawal. If your marginal tax rate is higher at time of withdrawal, then the TFSA has the advantage. Conversely, if your tax rate is lower at time of withdrawal the advantage goes to the RRSP.

Also, consider that RRSPs and TFSAs are both available tax shelters to maximize when sensible and if possible. Canadians are to only contribute to their RRSPs until they turn 71, whereas TFSA contributions can be made right up until death. If there’s a chance you receive a lump sum of money from an inheritance, home sale, and so on, you may want to save your TFSA contribution room and use your RRSP now, while you can.

There are some other finer details to think about. Does the RRSP tax deduction help with your age credit? Will future RRSP withdrawals result in OAS or Guaranteed Income Supplement clawback?

A sharp drop in mortgage interest rates in December may have kickstarted this year’s spring housing market early. Rates are about a full percentage point lower than they were in October, and consumers expect they will fall even more.

Optimism about mortgage rates increased sharply in December, according to a monthly consumer survey by Fannie Mae. For the first time since the survey was launched in 2010, more homeowners on net believe rates will go down rather than up, according to Mark Palim, deputy chief economist at Fannie Mae.

“This significant shift in consumer expectations comes on the heels of the recent bond market rally,” said Palim. “Notably, homeowners and higher-income groups reported greater rate optimism than renters.”

The average rate on the 30-year fixed has been on a wild ride since the start of the Covid pandemic. It hit more than a dozen record lows in 2020 and 2021, below 3%, causing a historic run on homebuying and a sharp rise in prices, only to then more than double in 2022. Rates hit a more than 20-year high in October 2023, hovering around 8% before falling back below 7% in December. Rates, however, are still twice what they were three years ago.

Ryan Paredes (R) and Ariadna Paredes look at a home being shown to them by Ryan Ratliff, a Real Estate Sales Associate with Re/Max Advance Realty, on April 20, 2023 in Cutler Bay, Florida.

Joe Raedle | Getty Images News | Getty Images

Buyers are coming back. Washington, D.C.-area real estate agent Paul Legere hosted two open houses over the weekend — homes in the $1.1 million to $1.2 million price range — and said they were the busiest he’s experienced in the last year.

“Similar report from my co-worker,” he added. “Even on Saturday, during torrential rain, we both had over 10 groups of active shoppers. These were people that had been in the market and had slowed or put their search on hold and are coming back, earnestly looking for a new property.”

Legere said he expects to see “an infusion” of inventory in the next week or two. Tight inventory has helped keep prices higher, another hurdle for potential homebuyers.

“Homeowners have told us repeatedly of late that high mortgage rates are the top reason why it’s both a bad time to buy and sell a home, and so a more positive mortgage rate outlook may [incentivize] some to list their homes for sale, helping increase the supply of existing homes in the new year,” said Palim.

A recent report from Redfin, a national real estate brokerage, found demand starting to pick up in December as rates fell. Redfin’s Homebuyer Demand Index — a seasonally adjusted measure of requests for tours and other homebuying services from Redfin agents — was up 10% from a month ago to its highest level since August, according to the report. Pending sales, which measure signed contracts on existing homes, were down 3% from December 2022, but that was the smallest decline in two years.

Much will depend on both interest rates and home prices in the months to come. Prices continue to rise, due to lack of supply, and if rates continue to drop, price gains could accelerate. The lower the rate, the more potential homebuyers can afford.

While mortgage rates are expected to drop further, that will depend on the strength of the economy and inflation.

“The rate momentum is as good as the trajectory of economic data. So if the data continues to do what it has been doing, there’s no reason rates couldn’t go down into the 5’s, possibly even the high 4’s if some of the talking heads are right about recession in 2024,” Matthew Graham, chief operating officer of Mortgage News Daily, said on CNBC’s “The Exchange.”

The average rate on the 30-year fixed mortgage hit a recent low of 6.61% at the end of December, but is up slightly this month to 6.76%, according to Mortgage News Daily.

Stock investors have gotten off to a wobbly start to the new year, hobbled by shifting expectations on the timing and extent of Federal Reserve interest-rate cuts in 2024.

All three major U.S. stock indexes snapped a nine-week winning streak on Friday, after unexpectedly strong December job gains prompted traders to briefly pull back on the chances of a March rate cut. The S&P 500 SPX

and Nasdaq Composite COMP

also failed to stage a Santa Claus Rally from the five final trading days of 2023 through the first two sessions of 2024, as questions grew about the market’s multiple rate-cuts view.

It all adds up to a glimpse of what might be in store for investors in the year ahead. Already, the so-called “January effect,” or theory that stocks tend to rise by more now than any other month, could be put to the test by headwinds that include stalling progress on inflation. Inflation’s downward trend in recent months had given traders and investors hope that as many as six or seven quarter-percentage-point rate cuts from the Federal Reserve could be delivered in 2024, starting in March.

Over the first handful of days in the new year, however, reality has started to sink in. For one thing, multiple rate cuts tend to be more commonly associated with recessions and not soft landings for the economy.

Moreover, the idea that the Fed could follow through with as many rate cuts as envisioned by traders would significantly increase the probability that policymakers lose their battle against inflation, according to Mike Sanders, head of fixed income at Wisconsin-based Madison Investments, which manages $23 billion in assets. That’s because six or more rate cuts would loosen financial conditions by too much, and boost the risk of another bout of inflation that forces officials to hike again, he said.

Minutes of the Fed’s Dec. 12-13 meeting show that policymakers were uncertain about their forecasts for rate cuts this year and failed to rule out the possibility of further rate hikes. Nonetheless, fed funds futures traders continued to cling to expectations for a big decline in borrowing costs, with the greatest likelihood now coalescing around five or six quarter-point rate cuts that total 125 or 150 basis points of easing by year-end. That’s roughly twice as much as what policymakers penciled in last month, when they voted to keep interest rates at a 22-year high of 5.25% to 5.5%.

Source: CME FedWatch Tool, as of Jan. 5.

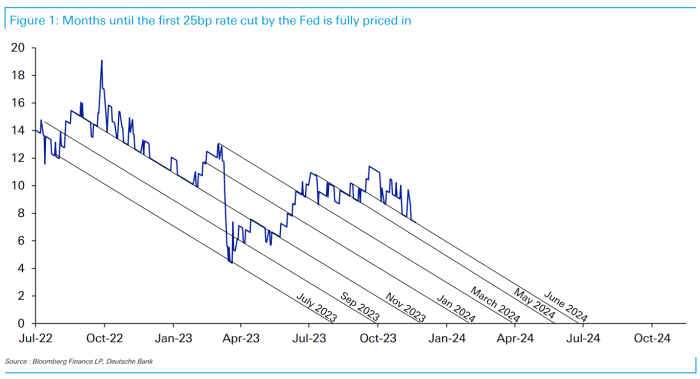

Uncertainty over the path of U.S. interest rates could leave investors flat-footed once again, and damp the optimism that sent all three major stock indexes in 2023 to their best annual performances of the prior two to three years. In November, analysts at Deutsche Bank AG DB, +0.81%

counted seven times since 2021 in which markets expected the Fed to make a dovish pivot, only to be wrong.

Sources: Bloomberg, Deutsche Bank. Chart is as of Nov. 20, 2023.

Financial markets have been operating with “sky-high expectations” for 2024 rate cuts, but the only way to substantiate six cuts this year is with an “abrupt and sharp downturn in the economy,” said Todd Thompson, managing director and portfolio co-manager at Reams Asset Management in Indianapolis, which oversees $27 billion.

Heading into 2024, euphoria over the prospect of lower borrowing costs produced what Thompson calls “an alarming, everything rally,” which he says leaves equities and high-yield corporate debt vulnerable to pullbacks between now and the next six months. Beyond that period, however, “the trend is likely to be lower rates as the economy finally succumbs to tightening conditions at the same time inflation continues to recede.”

The coming week brings the next major U.S. inflation update, with December’s consumer price index report released on Thursday. The annual headline rate of inflation from CPI has slowed to 3.1% in November from a peak of 9.1% in June 2022. In addition, the core rate from the Fed’s favorite inflation gauge, known as the PCE, has eased to 3.2% year-on-year in November from a 4.2% annual rate in July.

The Fed needs to keep interest rates higher because of all the uncertainty around inflation’s most likely path forward, and the U.S. labor market “won’t degrade fast enough in the first quarter to justify a first rate cut in March,” according to Sanders of Madison Investments.

Rate-cut expectations are “going to be the issue for 2024, and a lot of it is going to be revolving around inflation getting back to that 2% target,” Sanders said via phone. “We think somewhere between 75 and 125 basis points of rate cuts make sense, and that the first move is more of a June-type of event. We don’t think it makes sense to have a March rate cut unless the labor market falls off a cliff.”

History shows that Treasury yields tend to fall in the months leading up to the first rate cut of a Fed easing cycle. However, that isn’t happening right now. Yields on government debt have been on an upward trend since the end of December, with 2- BX:TMUBMUSD02Y,

10- BX:TMUBMUSD10Y,

and 30-year yields BX:TMUBMUSD30Y

ending Friday at their highest levels in more than two to three weeks.

While financial markets generally tend to be efficient processors of information, they “haven’t been very accurate in terms of pricing in rate cuts” this time, said Lawrence Gillum, the Charlotte, North Carolina-based chief fixed-income strategist for broker-dealer for LPL Financial. He said the big risk for 2024 is if financial conditions ease too much and the Fed declares victory on inflation too soon, which could reignite price pressures in a manner reminiscent of the 1970s period under former Fed Chairman Arthur Burns.

“We think rate-cut expectations have gone too far too fast, and that the backup in yields we are seeing right now is the market acknowledging that maybe rate cuts are not going to be as aggressive as what was priced in,” Gillum said via phone.

December’s CPI report on Thursday is the data highlight of the week ahead.

On Monday, consumer-credit data for November is set to be released, followed the next day by trade-deficit figures for the same month.

Wednesday brings the wholesale-inventories report for November and remarks by New York Fed President John Williams.

Initial weekly jobless claims are released on Thursday. On Friday, the producer price index for December comes out.

A ‘now hiring’ sign is displayed in a retail store in Manhattan on January 05, 2024 in New York City.

Spencer Platt | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Hot jobs market The U.S. labor market added 216,000 jobs in December. That’s much more than the 170,000 expected by economists surveyed by Dow Jones, and the downwardly revised 173,000 jobs added in November. The unemployment rate held steady at 3.7%, defying estimates of a 10-basis-point rise. Meanwhile, average hourly earnings rose 4.1% from a year earlier, higher than the 3.9% forecast.

Losing week U.S. stocks inched up slightly Friday, but couldn’t reverse a weekly decline. Treasury yields ticked up for the second day, with the 10-year yield closing at 4.051%. The pan-European Stoxx 600 index retreated 0.27%. Retail stocks fell 1.1%, leading sector losses, after data showed German retail sales fell 2.5% for the month, much more than estimates of a 0.1% slide.

Grounded airplanes The U.S. Federal Aviation Administration has ordered a temporary grounding of the Boeing 737 Max 9 aircraft, which means airlines won’t be able to use those particular Boeing models for flying. The directive comes after a piece of the aircraft blew out in the middle of an Alaska Airlines flight, leaving a gaping hole on the side of the plane.

Potential Apple lawsuit Apple just can’t catch a break. Fresh off a downgrade to its shares by Barclays and Piper Sandler, the technology giant is potentially facing an antitrust lawsuit by the U.S. Department of Justice, according to a report from The New York Times. The lawsuit could target how the Apple Watch works exclusively with the iPhone, as well as the company’s iMessage service, which excludes non-Apple devices.

[PRO] Numbers to watch The U.S. consumer price index report comes out Thursday this week, and will be the major catalyst for markets as investors assess if the U.S. Federal Reserve is edging closer to its goal of keeping inflation at 2%. But don’t neglect Friday, which is jam-packed with earnings reports from big banks such as JPMorgan Chase, Citigroup and Bank of America.

The headline number on the U.S. jobs report’s undeniably startling — 216,000 new jobs in December, compared with an expected 170,000. The unemployment rate defied forecasts for it to fall, while average hourly earnings were higher than estimates too.

The data suggests the U.S. labor market’s still running hot despite the 11 interest-rate hikes implemented by the Federal Reserve.

But the numbers aren’t so drastic that rate hikes could be back on the table. Look more closely and you’ll find pockets of weakness in the report.

The headline number, expectation-busting as it is, probably won’t persuade the Fed to resume hiking.

“While the Dow Jones estimate is for a nonfarm payrolls gain of 170,000, Art Hogan, chief market strategist at B. Riley Financial, said the acceptable range is really something like 100,000-250,000,” CNBC’s Jeff Cox noted.

Consider also how October and November’s jobs numbers were downwardly revised, which point to a weaker-than-expected labor market last quarter. And when viewed on an annual basis, 2023 saw job growth of 2.7 million, dramatically lower than 2022’s addition of 4.8 million jobs.

The theme of growth continuing — but slowing — was also seen in December’s ISM services index, which measures business activity, such as price and inventory levels. The reading came in at 50.6%, indicating growth in the service sector, but that’s nearly two percentage points below expectations as well as November’s reading.

That’s probably why stocks managed to eke out small gains Friday, despite the shock of the headline jobs number.

But those marginal increases couldn’t prevent major indexes from registering their first negative week in 10. For the week, the S&P fell 1.52%, the Dow lost 0.59% and the Nasdaq slumped 3.25%, its biggest decline since September.

Investors hoping for a positive catalyst for markets will be keeping their fingers crossed, hoping December’s consumer price index report comes in cooler than expected.

The Federal Reserve‘s effort to bring down inflation has so far been successful, a rare feat in economic history.

The central bank signaled in its latest economic projections that it will cut interest rates in 2024 even with the economy still growing, which would be the sought-after path to a “soft landing,” where inflation returns to the Fed’s 2% target without causing a significant rise in unemployment.

“Rates are headed lower,” said Tim Quinlan, senior economist at Wells Fargo. “For consumers, borrowing costs would fall accordingly.”

Most Americans can expect to see their financing expenses ease in the year ahead, but not by much, cautioned Greg McBride, chief financial analyst at Bankrate.

“We are in a high interest rate environment, and we’re going to be in a high interest rate environment a year from now,” he said. “Any Fed cuts are going to be modest relative to the significant increase in rates since early 2022.”

Although Fed officials indicated as many as three cuts coming this year, McBride expects only two potential quarter-point decreases toward the second half of 2024. Still, that will make it cheaper to borrow.

From mortgage rates and credit cards to auto loans and savings accounts, here are his predictions for where rates are headed in the year ahead:

Prediction: Credit card rates fall just below 20%

Because of the central bank’s rate hike cycle, the average credit card rate rose from 16.34% in March 2022 to nearly 21% today — an all-time high.

Going forward, annual percentage rates aren’t likely to improve much. Credit card rates won’t come down until the Fed starts cutting and even then, they will only ease off extremely high levels, according to McBride.

“The average rate will remain above the 20% threshold for most of the year,” he said, “and eventually dip to 19.9% by the end of 2024 as the Fed cuts rates.”

But rates are already significantly lower since hitting 8% in October. Now, the average rate for a 30-year, fixed-rate mortgage is 6.9%, up from 4.4% when the Fed started raising rates in March of 2022 and 3.27% at the end of 2021, according to Bankrate.

McBride also expects mortgage rates to continue to ease in 2024 but not return to their pandemic-era lows. “Mortgage rates will spend the bulk of the year in the 6% range,” he said, “with movement below 6% confined to the second half of the year.”

Prediction: Auto loan rates edge down to 7%

When it comes to their cars, more consumers are facing monthly payments that they can barely afford, thanks to higher vehicle prices and elevated interest rates on new loans.

The average rate on a five-year new car loan is now 7.71%, up from 4% when the Fed started raising rates, according to Bankrate. However, rate cuts from the Fed will take some of the edge off of the rising cost of financing a car, McBride said, helped in part by competition between lenders.

McBride expects five-year new car loans to drop to 7% by the end of the year.

Prediction: High-yield savings rates stay over 4%

Top-yielding online savings account rates have made significant moves along with changes in the target federal funds rate and are now paying more than 5% — the most savers have been able to earn in nearly two decades — up from around 1% in 2022, according to Bankrate.

Even though those rates have likely peaked, “yields are expected to remain at the highest levels in over a decade despite two rate cuts from the Fed,” McBride said.

According to his forecast, the highest-yielding offers on the market will still be at 4.45% in the year ahead. “It will still be a banner year for savers when those returns are measured against a lower inflation rate,” McBride said.

It has been a blockbuster year for investors, with the Dow Jones Industrial Average, the S&P 500 and the Nasdaq Composite all up with double-digit gains. However, the Federal Reserve battled the worst inflation in decades with several rate hikes, and 2023 marked the worst banking crisis since 2008, with three major institutions collapsing. Astrid Martinez reports.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

U.S. Treasury yields fell Wednesday, as investors considered the outlook for monetary policy and financial markets for the coming year.

The yield on the 10-year Treasury dropped nearly 10 basis points to 3.789%. The 2-year Treasury yield edged down 4 basis points to 4.246%.

Yields and prices move in opposite directions. One basis point equals 0.01%.

In the last week of trading for 2023, investors considered the path ahead for interest rates and how this could impact the U.S. economy and financial markets.

Earlier this month, the Federal Reserve indicated that interest rates will be cut three times next year, with further reductions expected in 2025 and 2026, as inflation has “eased over the past year.”

Many investors have interpreted recent economic data, including the November U.S. personal consumption expenditure price index, as a sign that the Fed would be able to stick to its monetary policy expectations for next year.

Uncertainty remains about when the central bank will start cutting rates, although traders are pricing in an over 70% chance of rate cuts at its March meeting, according to CME Group’s FedWatch tool.

These became popular following the financial crisis in 2008/2009 to entice investors to buy preferred shares despite low interest rates at that time. They generally “reset” every five years with the dividend rate for the next five years based on a premium over the 5-year Government of Canada bond rate at the time. Rate reset preferred shares currently represent 73% of the Canadian preferred share market.

2. Perpetual preferred shares

These represent 25% of the Canadian preferred share market. Perpetuals have no reset date. Their dividend rate is set when they are issued, and they continue in perpetuity.

3. Floating or variable rate preferred shares

These are like rate resets in that the rate changes, but those changes are more frequent—typically quarterly. The rate is generally based on a premium to the 3-month Government of Canada treasury bill rate. Together, floating/variable rate and convertible preferred shares represent less than 3% of the Canadian preferred share market.

4. Convertible preferred shares

A convertible security can be converted into another class of securities of the issuer. For example, a convertible preferred share may be convertible into common shares of the company that issued the shares.

Preferred shares Indexes for Canadian investors

The S&P/TSX Preferred Share Index is currently 57% financials, 20% energy and 12% utilities. Communication services, real estate, and consumer staples makes up the remainder of the market. The financials are tilted slightly more towards banks than insurance companies.

The current distribution yield of the S&P/TSX Preferred Share Index is about 6.1%. This is the dividend income an investor might anticipate over the coming year. The trailing 12-month yield is about 5.9%. These are attractive rates, Mario, but you can earn comparable rates in guaranteed investment certificates (GICs) with no risk or volatility. So, the high yields need to be put into perspective.

What to do with preferred shares at a loss

One consideration, Mario, is if you own your preferred shares in a taxable non-registered account, you could sell them to trigger a loss, if you have other investments that you have sold or intend to sell for a capital gain.

“Tax loss selling” is when you sell an investment for a loss to harvest the tax benefit of that loss. You can claim capital losses against capital gains in the current year. If you have a net capital loss for all investments sold in your taxable accounts in a given year, you can carry that loss back to offset capital gains income you paid tax on in the previous three years. Or you can carry the loss forward to use in the future against capital gains.

Grocery items are offered for sale at a supermarket on August 09, 2023 in Chicago, Illinois.

Scott Olson | Getty Images

Heading into 2023, the predictions were nearly unanimous: a recession was coming.

As the year comes to a close, the forecasted economic downturn did not arrive.

So what’s in store for 2024?

An economic decline may still be in the forecast, experts say.

The prediction is based on the same factors that prompted economists to call for a downturn in 2023. As inflation has run hot, the Federal Reserve has raised interest rates.

Typically, that dynamic has triggered a recession, defined as two consecutive quarters of negative gross domestic product growth.

Some forecasts are optimistic that can still be avoided in 2024. Bank of America is predicting a soft landing rather than a recession, despite downside risks.

More than three-fourths of economists — 76% — said they believe the chances of a recession in the next 12 months is 50% or less, according to a December survey from the National Association for Business Economics.

“Our base case is that we have a mild recession,” said Larry Adam, chief investment officer at Raymond James.

That downturn, which may be “the mildest in history,” may begin in the second quarter, the firm predicts.

Of the NABE economists who also see a downturn in the forecast, 40% say it will start in the first quarter, while 34% suggest the second quarter.

Americans who have struggled with high prices amid rising inflation may feel a downturn is already here.

Layoffs, which made headlines at the end of 2023, may continue in the new year. While 29% of companies shed workers in 2023, 21% of companies expect they may have layoffs in 2024, according to Challenger, Gray & Christmas, an outplacement and business and executive coaching firm.

To prepare for the unexpected, experts say taking these three steps can help.

More than one third — 34% — of consumers went into debt this holiday season, down from 35% in 2022, according to LendingTree.

The average balance those shoppers are taking away is $1,028, well below last year’s $1,549 and the lowest since 2017.

But higher interest rates mean those debts are more expensive. One-third of holiday borrowers have interest rates of 20% or higher, LendingTree reports.

Certain moves can help control how much you pay on those debts.

First, LendingTree recommends automating your monthly payments to avoid penalties for late payments, including fees and rate increases.

If you have outstanding credit card balances that you’re carrying from month to month, try to lower the costs you’re paying on that debt, either through a 0% balance transfer offer or a personal loan. Alternatively, you may try simply asking your current credit card company for a lower interest rate.

Much of how a recession may affect you comes down to whether you still have a job, Barry Glassman, a certified financial planner and founder and president of Glassman Wealth Services, told CNBC.com earlier this year. Glassman is also a member of CNBC’s Financial Advisor Council.

An economic downturn may also create a situation where even those who are still employed earn less, he noted.

Consequently, it’s a good idea to evaluate how well you could handle an income drop. Consider how long, if you were to lose your job, you could keep up with bills, based on savings and other resources available to you, he explained.

“Stress-test your income against your ongoing obligations,” Glassman said. “Make sure you have some sort of safety net.”

Even having just a little more cash set aside can help ensure an unforeseen event like a car repair or unexpected bill does not sink your budget.

Yet surveys show many Americans would be hard pressed to cover a $400 expense in cash.

Experts say the key is to automate your savings so you do not even see the money in your paycheck.

“Even if we do get through this period relatively unscathed, that’s all the more reason to be saving,” Mark Hamrick, senior economic analyst at Bankrate, recently told CNBC.com.

“I have yet to meet anybody who saved too much money,” he added.

Another advantage to saving now: Higher interest rates mean the potential returns on that money are the highest they have been in 15 years. Those returns may not last, with the Federal Reserve expected to start cutting rates in 2024.

Shoppers weren’t entirely tight fisted during the holiday season, despite the ongoing pressure of inflation on household budgets.

U.S. retail sales grew 3.1% this holiday season, according to a Mastercard poll that tracks in-store and online retail sales. Spending on restaurants increased 7.8% from last year, while apparel and grocery-related purchases were up 2.4% and 2.1%, respectively, according to Mastercard.

Robust consumer spending bodes well for the economy’s present and future, according to Goldman Sachs.

“We continue to see consumer spending as a source of strength in the economy and forecast above-consensus real spending growth of 2.7% in 2023 and 2.0% in 2024 in Q4/Q4 terms,” economists with the investment bank said in a mid-December report.

Consumers proved more willing to shell out on online purchases compared to in-store purchases, with online sales growing 6.3% this holiday season versus a 2.2% increase in sales at brick-and-mortar stores, Mastercard’s data shows.

But not all retailers profited from shoppers’ open wallets.

Pockets of worry

Consumers spent 0.4% less on electronics and 2.0% less on jewelry compared to the 2022 holiday season, as price-conscious consumers cautiously embraced seasonal sales, Mastercard’s data shows.

For many consumers, increased spending over the holidays may also bring more debt. About 2 in 3 Americans say their household expenses have risen over the last year, with only about 1 in 4 saying their income had increased in the same period, according to an October poll from The Associated Press-NORC Center for Public Affairs Research.

The strong holiday shopping turnout reinforces the likelihood the Fed will achieve its goal of so-called soft landing, some analysts say. Even so, some forecasters predict that consumer spending could peter out later next year.

“PNC expects a decline in consumer spending in the second half of 2024 as the U.S. economy enters into a mild recession,” PNC analysts said in a research note. “High interest rates and modest job losses will cause households to turn more cautious. However, there’s still about a 45% probability that the U.S. economy avoids recession and consumer spending growth slows, but does not outright decline.”

The Mastercard SpendingPulse excluded automotive purchases.

Elizabeth Napolitano is a freelance reporter at CBS MoneyWatch, where she covers business and technology news. She also writes for CoinDesk. Before joining CBS, she interned at NBC News’ BizTech Unit and worked on the Associated Press’ web scraping team.

In addition to these three core benefits, a cashable GIC offers investors the option of getting their money back even before the term of the GIC has ended, if they so choose. For example, as of Dec. 14, 2023, you could buy a one-year cashable GIC from Scotiabank at an interest rate of 2.85%. If you need your money back sooner than anticipated, you can redeem the GIC. There is no interest penalty for cashing out early—so you will get the interest earned to date—but you must hold the GIC for at least 30 days before you can do so. Cashable or redeemable GICs offer investors great flexibility but note that banks typically offer higher rates for non-redeemable GICs—currently even 5% for a one-year GIC, as shown in the table below.

1-year non-redeemable GIC (paid annually)

1-year non-redeemable GIC (paid semi-annually)

1-year cashable GIC (paid at maturity)

Interest rate

5%

4.92%

2.85%

Redeemable early

No

No

Yes

Eligible for registered accounts

Yes

Yes

Yes

CDIC-eligible

Yes

Yes

Yes

Rates are provided for information purposes only and are subject to change at any time.

Are cashable GICs a good investment?

Here are some reasons why cashable GICs may be a good investment:

They can be used for tax planning—for example, by buying a GIC in an RRSP account to get a tax deduction, or by holding a GIC in an FHSA to get a deduction and tax-free growth—as long the money is eventually used towards buying a first home.

They are flexible—giving investors the option of fully or partially redeeming their investment, depending on the type of product chosen.

These GICs have a low minimum investment amount of $500 and no investment fees—making them accessible to smaller and newer investors.

Cashable GICs are eligible for CDIC protection, up to $100,000 per depositor, at CDIC member institutions.

Given these benefits, a cashable GIC may be suitable for an investor who wants to combine the benefits of traditional GICs—like principal protection and a guaranteed interest rate—with the flexibility of cashing out anytime. (Note, however, that if you redeem within 30 days of the GIC’s issuance, you will forfeit the accumulated interest.)

If you’re saving up to buy a car or a home, for example, GICs are a safe and reliable way to grow your money and access it when you need it.

Can I transfer my GIC?

Canadians are accustomed to transferring their investments from one institution to another if needed—say, from one bank to another. However, unlike mutual funds, exchange-traded funds (ETFs) and stocks, GICs typically cannot be transferred. This is because a GIC is a contract between you and the institution, and each institution offers its own GIC interest rates, terms and conditions. So, if you’re buying a GIC, be prepared to hold it at the financial institution where you bought it. If you have a cashable GIC and you need to move your investments to another institution, you could cash in the GIC and reinvest the cash in a GIC at the new institution.

How to buy Scotiabank cashable GICs

If the ability to access your cash early is what you need, here are two options available through Scotiabank:

Cashable GIC

Personal redeemable GIC

Minimum investment amount

$500

$500

Term

1 year

2 years

Annual interest rate

2.85%

4.75%

Partially or fully redeemable

Fully or partially

Fully or partially

Investment fees

No

No

Principal protection

Yes

Yes

Guaranteed interest rate

Yes

Yes

Eligible for registered accounts

Yes

Yes

CDIC-eligible

Yes

Yes

Rates are provided for information purposes only and are subject to change at any time.

How do you buy a cashable GIC?

Cashable GICs are typically available wherever you buy your other GICs. For example, you can purchase Scotiabank GICs, including cashable/redeemable GICs, through a Scotiabank advisor. Book an appointment with an advisor online or by phone. Read more about Scotiabank GICs.

First, there was the trend of “quiet quitting”: a disgruntled employee doing the bare minimum required for their role. Then there was “quiet firing”: an employer reducing a worker’s duties and training, subtly nudging them to quit. And then, in 2023, we saw the rise of “quiet hiring”: an employer looking to its existing employees to fill a skills gap or take on more responsibilities, rather than hiring someone new. Quiet hiring is typically a cost-cutting or cost-saving measure, but it can also be an opportunity for a staffer who wants to try something new, move up to a new role or stack their case to ask for a raise. Quiet hiring can also refer to outsourcing work to short-term contractors instead of hiring new workers. —Jaclyn Law

2. Soft saving

Facing high inflation, high interest rates, expensive housing and mounting debt, many young people are unsure if they’ll ever be able to retire. So, many Gen Zers are rejecting aggressive saving (see: the FIRE movement) and embracing “soft living”—prioritizing things like comfort, balance, personal growth and wellness. “Soft saving” is part of that. It’s a lower-stress approach to personal finance and investing that focuses on the present. That doesn’t mean Gen Z is spending recklessly—but some might see saving for retirement as more of a nice-to-have than a need. —J.L.

Recommended savings reads

3. Inflation isolation

Is inflation dampening your social life? A November 2023 Ipsos poll found that the rising cost of living is causing “inflation isolation.” Half of Canadians are staying at home more often, and a third of us are socializing less to avoid spending money. As a result, 20% of us are feeling isolated. Pretty bleak, right? Plus, those of us who are struggling with debt are more likely to feel stress and anxiety, as well as cut back on seeing friends and family. If you’re experiencing feelings of anxiety, stress or depression, read our guide to finding free and low-cost mental health resources in Canada. —Margaret Montgomery

Recommended inflation reads

4. Housing-market nepo baby

When I first saw this term in a recent Wealthsimple newsletter, I couldn’t help but laugh… and then I wanted to cry. “Nepo baby” refers to the child of a celebrity who has benefited from their parent’s success, wealth and name recognition. A nepo home buyer in Canada is someone whose parents already own a home and can help their kids afford a down payment for a home, according to some sources. Statistics Canada reports that “in 2021, the adult children (millennial and Generation Z tax filers born in the 1990s) of homeowners were twice as likely to own a home as those of non-homeowners.” Adult children whose parents owned multiple properties were three times as likely to own a home than those whose parents were non-home owners. —M.M.

Recommended real estate and mortgage reads

5. Recession core

Move over, minimalism—recession core is here. Yep, that’s right, there’s a whole aesthetic inspired by living in a recession. Basically, this means going back to simpler styles and using items already in your wardrobe. Look, I get it. Minimalism might actually require you to spend lots of money on “clean” and refined-looking items, so that’s out of the question for many right now. Instead, many of us are looking for greater value when we shop—a habit that could pay off even after the economy improves. —M.M.

Recommended thrifty reads

We can think of several more financial buzzwords that were popular this year, from “tip-flation” to “funflation.” Will they still be talked about in 2024, or will they go the way of “YOLO,” “the new normal” and “The Great Resignation”? Only time will tell. We want to know which trendy money words you love and hate. Share your picks in the comments below, and then boost your financial vocabulary by checking out the MoneySense Glossary.

Margaret Montgomery is MoneySense’s editorial assistant and MoneyFlex columnist. She studied business administration at Wilfrid Laurier University and journalism at Centennial College.

Jaclyn Law is MoneySense’s managing editor. She has worked in Canadian media for over 20 years, including editor roles at Chatelaine and Abilities and freelancing for The Globe and Mail, Report on Business, Profit, Reader’s Digest and more. She completed the Canadian Securities Course in 2022.

Makoto Kuroda of Goldman Sachs says “there are positives to potentially lower Fed rates, such as lower dollar funding costs or lower unrealized loss on U.S. Treasurys.”

U.S. stock index futures were hovering around their highs of the year and just shy of record levels as investors continued to revel in an expected loosening of monetary policy by the Federal Reserve in 2024 amid a ‘soft landing’ for the U.S. economy.

How are stock-index futures trading

S&P 500 futures ES00, +0.05%

rose 3 points, or less than 0.1% to 4796

Dow Jones Industrial Average futures YM00, +0.01%

added 10 points, or less than 0.1% to 37688

Nasdaq 100 futures NQ00, +0.02%

were unchanged at 16940

On Monday, the Dow Jones Industrial Average DJIA

rose 1 points, or 0%, to 37306, the S&P 500 SPX

increased 21 points, or 0.45%, to 4741, and the Nasdaq Composite COMP

gained 91 points, or 0.62%, to 14905.

What’s driving markets

The S&P 500 was set to open Tuesday’s session only about 1% below its record close as traders remained energized by the prospect of the Federal Reserve starting to cut interest rates by the spring of next year.

Some Fed officials in recent days pushed back against the market’s hopes for lower borrowing costs as early as March, but equity investors seem to have shrugged off those comments, for now.

Meanwhile, the Bank of Japan on Tuesday reminded traders that an important spigot of cheap money still remains open. The BOJ left its main interest rate at minus 0.1%, and in the accompanying news conference, Governor Kazuo Ueda provided little evidence he was minded to exit the central bank’s ultra-loose monetary policy anytime soon, despite inflation running above its 2% target for 19 consecutive months.

The Japanese yen USDJPY, +1.32%

fell 1.2% and the Nikkei 225 stock index JP:NIK

rose 1.4% as 10-year government bond yields BX:TMBMKJP-10Y

fell 3.6 basis points to 0.634%, the lowest in nearly four months.

“Whenever central banks take positions that the market thinks are unsustainable, it’s always the currencies that play the role of the canary in the coal mine. No surprise then to see the Yen weakening by around 1% against every major currency overnight as investors vote with their feet,” said Steve Clayton, head of equity funds at Hargreaves Lansdown.

Traders were also warily eyeing the oil market, after benchmark Brent crude BRN00, +0.06%

jumped on Monday following BP’s statement it was halting shipments through the Red Sea, and thus the Suez Canal, because of attack’s by the Houthi in Yemen.

Many of the world’s biggest shipping companies have said they also will steer clear of the region, prompting concerns about rising costs that may build inflationary pressures.

“An extended period of disruption in global trade ways should not only sustain energy prices, but also put a renewed pressure on global supply chains and shipping prices,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank.

“The latter is a threat to inflation. Remember, the pandemic-related supply chain disruptions were the major reason that sent inflation to almost 10% in the U.S.,” Ozkardeskaya added.

However, there was little evidence early Tuesday that investors were overly concerned by that narrative, with 10-year U.S. Treasury yields BX:TMUBMUSD10Y

dipping 2.7 basis points to 3.912%.

U.S. economic updates set for release on Tuesday include November housing starts and building permits at 8:30 a.m. Eastern.

Atlanta Fed President Raphael Bostic is due to speak at 12:30 p.m.

Wall Street seems to agree that U.S. stocks will climb to fresh record highs in 2024. But the most important question for investors may still be the direction and speed of interest-rate moves.

Rate-sensitive groups of stocks with lackluster fundamentals, such as financials, utilities, staples, “may be able to outperform, at least early in the year,” if one expects interest rates “to come down quickly and permanently,” said Nicholas Colas, co-founder of DataTrek Research.

But if “one expects a bumpier ride on the rate front,” then stronger groups, like technology and tech-adjacent sectors “should do better,” Colas said in a Monday client note.

The S&P 500’s utilities, consumer staples and energy sectors have been the worst performing parts of the large-cap benchmark index so far in 2023, according to FactSet data.

With an over 10% year-to-date decline, the S&P 500’s utilities sector XX:SP500.55

has significantly underperformed the broader index’s SPX

23.6% advance.

The S&P 500’s best performing information technology sector XX:SP500.45

was up 56.5% for the same period. But its consumer staples XX:SP500.30

and energy XX:SP500.10

sectors have slumped by 2.6% and 4.1% so far this year, respectively, according to FactSet data.

Utilities and consumer staples are usually considered defensive investment sectors, or “bond proxies,” because they can help investors minimize stock-market losses in any economic downturn. Companies in these sectors usually provide electricity, water and gas, or they sell products and services that consumers regularly purchase, regardless of economic conditions.

However, utilities and consumer staples stocks were under a lot of pressure this year. A relentless climb in U.S. Treasury yields in October made defensive stocks less attractive compared with government-issued bonds, or money-market funds offering 5%, especially as the economy remained strong, pushing recession expectations out further.

Colas expects “weaker groups” to catch a stronger tailwind if rates continue to decline.

The S&P 500’s utilities and consumer staples sectors rose 0.9% and 1.6% last week, respectively, compared with the information technology sector’s 2.5% advance and communication services sector’s XX:SP500.50

0.1% decline, according to FactSet data.

Earnings growth expectations for each S&P 500 sector in 2024 are indicated below. Sectors to the left of the dotted black line are expected to show better bottom-line results than the S&P 500 as a whole, while those to the right are expected to show weaker earnings growth.

SOURCE: FACTSET, DATATREK RESEARCH

Wall Street expects next year to see 11.5% growth in S&P 500 earnings-per-share (EPS), to $244, and 5.5% revenue growth, according to FactSet data.

However, there is a wide dispersion across S&P 500 sectors. The range goes from 2% revenue and 3% earnings growth for the energy sector, to 9% revenue and 17% earnings growth for the information technology sector, according to data compiled by DataTrek Research.

“Playing fundamentally weaker sectors therefore assumes even more good news on the rate front,” Colas said, adding that it still is riskier than sticking with “tried and true groups” like technology.

Moreover, sectors such as utilities, financials and consumer staples are not expected to show 10% earnings growth next year, while health care and big tech-dominated groups like communication services, technology and consumer discretionary, are expected to show much better than average revenue and earnings growth in 2024, said Colas, citing FactSet data.

U.S. stocks closed higher on Monday, with the Dow Jones Industrial Average DJIA

building on its all-time high set last week. The S&P 500 gained 0.5% and the Dow Industrials closed fractionally higher. The Nasdaq Composite COMP

finished up 0.6%, according to FactSet data.

Back in January, Bank of America was one of many investment banks that believed the U.S. economy was barreling toward recession. With the Federal Reserve raising interest rates at a breakneck pace to fight inflation, the economy would eventually slow to standstill, the bank warned. But as the year went on, economic data pleasantly surprised Wall Street, leading Bank of America’s chief U.S. economist Michael Gapen to begin shifting his recession forecast.

In June, Gapen argued that instead of facing a mild recession as early as the fourth quarter of 2023, the U.S. was likely to fall into an even more tame “growth recession” in 2024. Then, in August, he scrapped the recession call altogether due to the resilience of the labor market and consumer spending amid the Fed’s aggressive rate hikes. Parroting some Beatles lyrics, Gapen titled the note where he detailed his new, more optimistic forecast: “Imagine no recession, it’s easy if you try.”

Now, the veteran economist has turned even more bullish after multiple positive GDP, inflation, and retail sales reports. Consumers’ ability to keep spending even amid rising borrowing costs has convinced Gapen that the vaunted “soft landing”—where the Fed is able to tame inflation without sparking a job-killing recession—is becoming a reality.

“While there are many ways the U.S. economy can evolve, the Fed appears closer to ‘sticking the landing’ than ever,” he wrote in a note to clients Monday.

‘An even softer landing’

Gapen explained Monday that his initial call was based simply on history. At the beginning of the year, “surging inflation” and “a Fed that was prepared to err on the side of doing more than less in its fight to bring inflation down” convinced him there would be economic pain ahead. Over 11 periods of rapidly rising interest rates in a 60-year span, only one has resulted in a “soft landing,” making its odds this time around very slim.

Now, though, Gapen says his economic outlook was “too negative,” as both consumers and business have shown “significant resilience” to higher rates.

“As the calendar turns to 2024, we make further revisions to our outlook for the US in the direction of an even softer landing,” he wrote Monday, arguing that the Fed’s indicating “the potential beginnings of a rate cut cycle” could boost the economy in 2024.

Bank of America’s new outlook for the U.S. economy includes increased economic growth as well as lower inflation and unemployment. The bank expects GDP growth of 1.2% in 2024, 0.6 percentage points above its prior forecast; an unemployment rate of 4.2%, down from 4.4%; and inflation, as measured by the personal consumption expenditures price index, of 2.2%, down from 2.4%.

Gapen said that the strength of the economy in 2024 will be driven by consumer spending, which accounts for roughly 70% of U.S. GDP. Even though many consumers are pessimistic about their prospects, they continue to spend this holiday season. Retail sales shot up 4.1% from a year ago in November as shoppers splurged on Black Friday and Cyber Monday discounts.

Part of the reason for the resilient consumer spending is “elevated net wealth,” according to Gapen. The stock market’s 23% surge so far this year, as well as years of booming home prices, have made many Americans far richer. The median net worth of U.S. households jumped 37% to $192,900 between 2019 and 2022, according to the Federal Reserve’s Survey of Consumer Finances.

The rise in Americans’ wealth means that, as long as the labor market remains strong, consumers are likely to continue their spending spree, Gapen said. And with inflation cooling from its four-decade high of over 9% in June 2022 to just 3.1% in November, a soft landing is likely.

“Incoming data is signaling the U.S. economy can enjoy both modest growth and disinflation simultaneously,” the veteran economist wrote.

The U.S. economy is built different

Falling inflation and resilient growth are not a common combination for most economies, but Gapen believes the U.S. has “structurally changed” over the past decade or so, making it more resilient to higher interest rates. In the housing market, for example, lending standards have improved and the number of adjustable rate mortgages has plummeted since the Global Financial Crisis (GFC) of 2008. These, often risky, interest-rate-sensitive mortgages now make up just 9.2% of the market, compared to roughly 35% during the housing boom that led up to the GFC.

At the same time, Gapen noted that many of the drivers of the rise of U.S. inflation over the past few years have been related to supply shocks during the pandemic era, which are now fading.

“Supply-side improvements have helped bring inflation down more rapidly than we and the Fed had assumed previously,” he explained. “It opens the door for inflation to decelerate without putting policymakers in the position of implementing significant demand destruction.”

Subscribe to the CFO Daily newsletter to keep up with the trends, issues, and executives shaping corporate finance. Sign up for free.

Market optimism over the potential for interest rate cuts next year is dangerously overdone, according to former FDIC Chair Sheila Bair.

Bair, who ran the FDIC during the 2008 financial crisis, suggests Federal Reserve Chair Jerome Powell was irresponsibly dovish at last week’s policy meeting by creating “irrational exuberance” among investors.

“The focus still needs to be on inflation,” Bair told CNBC’s “Fast Money” on Thursday. “There’s a long way to go on this fight. I do worry they’re [the Fed] blinking a bit and now trying to pivot and worry about recession, when I don’t see any of that risk in the data so far.”

The Dow hit all-time highs in the final three days of last week. The blue-chip index is on its longest weekly win streak since 2019 while the S&P 500 is on its longest weekly win streak since 2017. It’s now 115% above its Covid-19 pandemic low.

Bair believes the market’s bullish reaction to the Fed is on borrowed time.

“This is a mistake. I think they need to keep their eye on the inflation ball and tame the market, not reinforce it with this … dovish dot plot,” Bair said. “My concern is the prospect of the significant lowering of rates in 2024.”

Bair still sees prices for services and rental housing as serious sticky spots. Plus, she worries that deficit spending, trade restrictions and an aging population will also create meaningful inflation pressures.

“[Rates] should stay put. We’ve got good trend lines. We need to be patient and watch and see how this plays out,” Bair said.

A trader works, as a screen displays a news conference by Federal Reserve Board Chairman Jerome Powell following the Fed rate announcement, on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., December 13, 2023.

Brendan Mcdermid | Reuters

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Asia markets fall U.S. markets mostly rose Friday amid a tumultuous day of trading, giving major indexes their seventh consecutive week of gains. However, Asia-Pacific markets slumped Monday, with Hong Kong’s Hang Seng index falling around 1%. It was dragged down by shares of SenseTime, which plunged as much as 18.25% to its all-time low on news the company’s founder had passed away.

Lowered risk appetite For the first half of the year, family offices in Asia had bet big on risky assets, said Hannes Hofmann of Citi Private Bank. That’s because Asian family offices were anticipating a rebound in China’s economy. But as the country’s economy slows down and Asian stock markets lag behind that of the U.S., that appetite for risk’s dwindling, according a Citi Private Bank global survey.

AI job losses There are signs humans are losing jobs to artificial intelligence. According to a recent report from ResumeBuilder, 37% of respondents say AI has replaced workers this year, while 44% report AI will result in layoffs in 2024. But experts say this trend isn’t a wholesale replacement of humans — but a redefinition of the sort of jobs we can do.

[PRO] ‘Poised to pounce’ Jefferies is “poised to pounce” on several global stocks next year, the investment bank’s analysts wrote. Three stocks, which include companies with strong cash flows and attractive risk-reward ratios, made it to Jefferies’ top choices for 2024. And all of them have at least a 60% potential upside.

The “everything rally” spurred by Wednesday’s Federal Reserve meeting appears to have lost its legs — not least because the Fed itself seemed slightly spooked by how aggressively markets are pricing in rate cuts for next year.

According to the dot plot, which is a projection of where Fed officials expect interest rates to be in the future, there could be three 25-basis-point cuts next year. But markets think there’s more than a 38% chance rates will plummet to a range of 3.75% to 4% — that’s six 25-basis-point cuts — by December next year, according to the CME FedWatch Tool.

On Friday, New York Federal Reserve President John Williams tried to rein in some of that exuberance.

“I just think it’s just premature to be even thinking about that,” Williams said, when asked about futures pricing for a rate cut in March.

Williams even warned rates might go up.

“One thing we’ve learned even over the past year is that the data can move and in surprising ways, we need to be ready to move to tighten the policy further, if the progress of inflation were to stall or reverse.”

That said, Friday also saw a quarterly event known as “triple witching,” the confluence of expiring stock index futures and options, as well as individual stock options. Furthermore, the S&P and Nasdaq-100 rebalanced their indexes, meaning the weight of some stocks on the index was changed. That could have exaggerated price moves and increased volatility as investors, accordingly, rebalanced their portfolios.

Finally, perhaps investors shouldn’t be surprised or disappointed the rally’s subsiding. “The market doesn’t go up every day, no matter how strong a trend is,” Chris Larkin, managing director of trading and investing at E-Trade points out. “Pullbacks and pauses are inevitable, regardless of how big they are or how long they last.”

The corollary to that is even a decline won’t last. Barring any shocks, signs are pointing to Santa spreading cheer in markets as the year wraps up.

Yields on 3-month BX:TMUBMUSD03M

and 6-month BX:TMUBMUSD06M

Treasury bills have been seeing yields north of 5% since March when Silicon Valley Bank’s collapse ignited fears of a broader instability in the U.S. banking sector from rapid-fire Fed rate hikes.

Six months later, the Fed, in its final meeting of the year, opted to keep its policy rate unchanged at 5.25% to 5.5%, a 22-year high, but Powell also finally signaled that enough was likely enough, and that a policy pivot to interest rate cuts was likely next year.

Importantly, the central bank chair also said he doesn’t want to make the mistake of keeping borrowing costs too high for too long. Powell’s comments helped lift the Dow Jones Industrial Average DJIA

above 37,000 for the first time ever on Wednesday, while the blue-chip index on Friday scored a third record close in a row.

“People were really shocked by Powell’s comments,” said Robert Tipp, chief investment strategist, at PGIM Fixed Income. Rather than dampen rate-cut exuberance building in markets, Powell instead opened the door to rate cuts by midyear, he said.

“Eventually, you end up with a lower fed-funds rate,” Tipp said in an interview. The risk is that cuts come suddenly, and can erase 5% yields on T-bills, money-market funds and other “cash-like” investments in the blink of an eye.

Swift pace of Fed cuts

When the Fed cut rates in the past 30 years it has been swift about it, often bringing them down quickly.

Fed rate-cutting cycles since the ’90s trace the sharp pullback also seen in 3-month T-bill rates, as shown below. They fell to about 1% from 6.5% after the early 2000 dot-com stock bust. They also dropped to almost zero from 5% in the teeth of the global financial crisis in 2008, and raced back down to a bottom during the COVID crisis in 2020.

Rates on 3-month Treasury bills dropped suddenly in past Fed rate-cutting cycles

FRED data

“I don’t think we are moving, in any way, back to a zero interest-rate world,” said Tim Horan, chief investment officer fixed income at Chilton Trust. “We are going to still be in a world where real interest rates matter.”

Burt Horan also said the market has reacted to Powell’s pivot signal by “partying on,” pointing to stocks that were back to record territory and benchmark 10-year Treasury yield’s BX:TMUBMUSD10Y

that has dropped from a 5% peak in October to 3.927% Friday, the lowest yield in about five months.

“The question now, in my mind,” Horan said, is how does the Fed orchestrate a pivot to rate cuts if financial conditions continue to loosen meanwhile.

“When they begin, the are going to continue with rate cuts,” said Horan, a former Fed staffer. With that, he expects the Fed to remain very cautious before pulling the trigger on the first cut of the cycle.

“What we are witnessing,” he said, “is a repositioning for that.”

Pivoting on the pivot

The most recent data for money-market funds shows a shift, even if temporary, out of “cash-like” assets.

The rush into money-market funds, which continued to attract record levels of assets this year after the failure of Silicon Valley Bank, fell in the past week by about $11.6 billion to roughly $5.9 trillion through Dec. 13, according to the Investment Company Institute.

Investors also pulled about $2.6 billion out of short and intermediate government and Treasury fixed income exchange-traded funds in the past week, according to the latest LSEG Lipper data.

Tipp at PGIM Fixed Income said he expects to see another “ping pong” year in long-term yields, akin to the volatility of 2023, with the 10-year yield likely to hinge on economic data, and what it means for the Fed as it works on the last leg of getting inflation down to its 2% annual target.

“The big driver in bonds is going to be the yield,” Tipp said. “If you are extending duration in bonds, you have a lot more assurance of earning an income stream over people who stay in cash.”

Molly McGown, U.S. rates strategist at TD Securities, said that economic data will continue to be a driving force in signaling if the Fed’s first rate cut of this cycle happens sooner or later.

With that backdrop, she expects next Friday’s reading of the personal-consumption expenditures price index, or PCE, for November to be a focus for markets, especially with Wall Street likely to be more sparsely staffed in the final week before the Christmas holiday.

The PCE is the Fed’s preferred inflation gauge, and it eased to a 3% annual rate in October from 3.4% a month before, but still sits above the Fed’s 2% annual target.

“Our view is that the Fed will hold rates at these levels in first half of 2024, before starting cutting rates in second half and 2025,” said Sid Vaidya, U.S. Wealth Chief Investment Strategist at TD Wealth.

U.S. housing data due on Monday, Tuesday and Wednesday of next week also will be a focus for investors, particularly with 30-year fixed mortgage rate falling below 7% for the first time since August.

The major U.S. stock indexes logged a seventh straight week of gains. The Dow advanced 2.9% for the week, while the S&P 500 SPX

gained 2.5%, ending 1.6% away from its Jan. 3, 2022 record close, according to Dow Jones Market Data.

The Nasdaq Composite Index COMP

advanced 2.9% for the week and the small-cap Russell 2000 index RUT

outperformed, gaining 5.6% for the week.

Traders work on the floor of the New York Stock Exchange (NYSE) during morning trading on December 14, 2023, in New York City.

Angela Weiss | Afp | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Triple witching U.S. markets mostly rose Friday amid a tumultuous day of trading, which could have been triggered by an event known as “triple witching” — the simultaneous expiration of stock options, and stock index futures and options. Europe’s Stoxx 600 index ended the day flat, giving away earlier gains of around 0.5%. But it rose 0.91% last week, its fifth week of wins.

Cooling the heat Following the euphoria markets experienced after the U.S. Federal Reserve’s last meeting, during which it indicated three rate cuts for 2024, Fed officials seem to be dampening the enthusiasm. “We aren’t really talking about rate cuts right now,” New York Federal Reserve President John Williams told CNBC. “We need to be ready to move to tighten the policy further, if the progress of inflation were to stall.”

Citi works remotely Citigroup employees were told they can work remotely in the final two weeks of December, CNBC has learned, making last week the final in-person experience of this year for many staffers. But this perk comes at a tense moment. Some employees expressed concern over whether their job will still exist next year as CEO Jane Fraser finalizes her sweeping corporate reorganization — one that’s already resulted in layoffs.

AI job losses There are signs humans are losing jobs to artificial intelligence. According to a recent report from ResumeBuilder, 37% of respondents say AI has replaced workers this year, while 44% report AI will result in layoffs in 2024. But experts say this trend isn’t a wholesale replacement of humans — but a redefinition of the sort of jobs we can do.

[PRO] Focus on PCE In comparison to last week, this week’s relatively light on economic data and market-moving events. But investors should keep an eye on the personal consumption expenditure index, out Friday. Economists expect the PCE to show inflation’s receding. But if it surprises to the upside, it’ll throw a wrench into the Fed’s plan to pivot — and possibly halt the ferocious market rally.

The “everything rally” spurred by Wednesday’s Federal Reserve meeting appears to have lost its legs — not least because the Fed itself seemed slightly spooked by how aggressively markets are pricing in rate cuts for next year.

According to the dot plot, which is a projection of where Fed officials expect interest rates to be in the future, there could be three 25-basis-point cuts next year. But markets think there’s a 34.7% chance rates will plummet to a range of 3.75% to 4% — that’s six 25-basis-point cuts — by December next year, according to the CME FedWatch Tool.

On Friday, New York Federal Reserve President John Williams tried to rein in some of that exuberance.

“I just think it’s just premature to be even thinking about that,” Williams said, when asked about futures pricing for a rate cut in March.

Williams even warned rates might go up.

“One thing we’ve learned even over the past year is that the data can move and in surprising ways, we need to be ready to move to tighten the policy further, if the progress of inflation were to stall or reverse.”

That said, Friday also saw a quarterly event known as “triple witching,” the confluence of expiring stock index futures and options, as well as individual stock options. Furthermore, the S&P and Nasdaq-100 rebalanced their indexes, meaning the weight of some stocks on the index was changed. That could have exaggerated price moves and increased volatility as investors, accordingly, rebalanced their portfolios.

Finally, perhaps investors shouldn’t be surprised or disappointed the rally’s subsiding. “The market doesn’t go up every day, no matter how strong a trend is,” Chris Larkin, managing director of trading and investing at E-Trade points out. “Pullbacks and pauses are inevitable, regardless of how big they are or how long they last.”

The corollary to that is even a decline won’t last. Barring any shocks, signs are pointing to Santa spreading cheer in markets as the year wraps up.