Inflation in the eurozone accelerated in October, reaching double digits, with increasing signs that price pressures are broadening beyond food and energy.

The consumer price index–a measure of what consumers pay for goods and services–increased 10.7% in October on year, accelerating from 9.9% in September, preliminary data from the European Union’s statistics agency Eurostat showed Monday.

Economists polled by The Wall Street Journal expected inflation to come in at 10.0%.

The acceleration in inflation was led by higher energy prices, which rose 41.9% on year in October compared with the 40.7% gain registered in September. Food, alcohol and tobacco prices also gained pace, increasing 13.1% on year from an 11.8% rise in September. Price of non-energy industrial goods and of services also accelerated, the data showed.

The core consumer price index–which excludes the more volatile categories of food and energy–increased 5% on year in October, up from 4.8% in September.

The European Central Bank raised interest rates by 75 basis points for the second time in a row on Thursday, but signaled mounting concerns about economic growth in the region.

Data released Friday showed the eurozone economy expanded by 0.2% in the third quarter, beating economists’ expectations but slowing from the 0.8% expansion registered in the previous three-month period.

Write to Xavier Fontdegloria at xavier.fontdegloria@wsj.com

Economists polled by the Wall Street Journal had expected manufacturing to rise to 51.8 in October and for the service sector to rise to 49.7.

Key details: In the service sector, the downturn was fueled by the rising cost of living and tightening financial conditions.

New orders in the manufacturing sector fell back into contraction territory in October. Output remained resilient due to firms eating into backlogs of previously placed orders, S&P Global said.

While price pressures picked up a bit in the service sector, the pace of the gain in inflation in the manufacturing sector was the slowest in almost two years.

Big picture: Talk of a recession sometime in 2023 has picked up in the last week. Many economists are sounding more bearish on the outlook, especially since the Federal Reserve is now seen raising its benchmark rate to 5%. However, on Monday, economists at Goldman Sachs said that talk over a recession was overblown.

What S&P Global said: “The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

“Although price pressures picked up slightly in the service sector due to high food, energy and staff costs, as well as rising borrowing costs, increased competitive forces meant average prices charged for services grew at only a fractionally faster rate. Combined with the easing of price pressures in the goods-producing sector, this adds to evidence that consumer price inflation should cool in coming months,” he added.

America’s high inflation rate will produce a 7% increase in the size of the standard deduction when workers file their taxes on their 2023 income, according to new inflation adjustments from the Internal Revenue Service.

It’s also going to pump up tax brackets by 7% as well, according to the annual inflation adjustments the IRS announced this week.

Many tax code provisions — but not all — are indexed for inflation, so the announcements are a recurring event. But when inflation is persistently clinging to four-decade highs, these annual adjustments carry extra significance.

“When inflation is persistently clinging to four-decade highs, these annual adjustments of approximately 7% for the standard deduction carry extra significance.”

Start with the standard deduction, which is what most people use instead of itemizing deductions.

The standard deduction for individuals and married people filing separately will be $13,850 for the 2023 tax year. That’s a $900 increase from the $12,950 standard deduction for the upcoming tax season.

For married couples filing jointly, the payout climbs to $27,700 for the 2023 tax year. That’s a $1,800 increase from the $25,900 standard deduction set for the upcoming tax year.

The increases in the marginal tax rates reflect the same 7% rise. For example, the 22% tax bracket for this year is over $41,775 for single filers and over $83,550 for married couples filing jointly. Next year, the same 22% bracket applies to incomes over $44,725 and over $89,450 for married couples filing jointly.

MarketWatch/IRS

“The changes seem to be much larger than previous years because inflation is running much higher than it has in previous decades,” said Alex Durante, economist at the Tax Foundation, a right-leaning tax think tank.

The IRS arrives at its inflation adjustments by averaging a slightly different inflation gauge, the so-called “chained Consumer Price Index” instead of the widely-watched Consumer Price Index, Durante noted. That’s an outcome of the Trump-era Tax Cuts and Jobs Act of 2017, he added.

“The reason they do this is because the regular CPI is thought to overstate inflation because it doesn’t take into account the substitution that shoppers can make as cost rise,” Durante said. Shoppers substitute when they swap a more expensive item for cheaper one, and research shows many Americans are using the tactic.

The IRS inflation adjustments come after September CPI data last week showed inflation of 8.2% year-over-year, slightly off from 8.3% in August. Also last week, the Social Security Administration said next year’s payments would include an 8.7% cost of living adjustment.

“The payout on the earned income tax credit — geared at low- and moderate-income working families who have been hit hard by red-hot inflation — is also increasing. ”

The payout on the earned income tax credit is also increasing. The maximum payout for a qualifying taxpayer with at least three qualifying children climbs to $7,430, up from $6,935 for this tax year. The longstanding credit is geared at low- and moderate-income working families who have been hit hard by red-hot inflation.

More than 60 provisions are slated for an increase inline with inflation, but many portions of the tax code are not indexed for inflation. Depending on the circumstances, the taxes or the tax breaks kick in sooner.

Capital gains tax rules one example. The IRS lets a taxpayer use capital losses to offset capital gains taxes. If losses exceed gains, the IRS allows a taxpayer to deduct up to $3,000 in excess loses. They can then carry the remainder of the capital loses to future tax years. It’s been more than four decades since lawmakers last set the limit, according to Durante.

“While more than 60 provisions are slated for an increase inline with inflation, many portions of the tax code are not indexed for inflation. They include capital gains tax. ”

Given the stock market’s rocky downward slide this year, many investors might welcome a fast-approaching tax break — even if it only enables a $3,000 deduction.

At the same time, a married couple selling their home can exclude the first $500,000 of the sale from capital gains taxation, and it’s $250,000 for a single filer. It’s been that way since the exclusion’s 1997 establishment.

The once white-hot housing market may be cooling, but many sellers may still be facing the point when taxes kick in. The median home listing was over $367,000 as of early October, according to Redfin RDFN, +2.29%.

The child tax credit is another example. After the payout to parents last year jumped to $3,600 for children under age 6 and $3,000 per child age 6 to 17, it’s back to a maximum $2,000. The credit’s refundable portion climbs from $1,500 to $1,600 during tax year 2023, the IRS notes.

Proponents of the boosted payouts and some Congressional Democrats want to revive the larger payments in negotiations tied to corporate taxes. The high costs of living are a strong reason to bring back the boosted credit, they say.

Some investors are on edge that the Federal Reserve may be overtightening monetary policy in its bid to tame hot inflation, as markets look ahead to a reading this coming week from the Fed’s preferred gauge of the cost of living in the U.S.

“Fed officials have been scrambling to scare investors almost every day recently in speeches declaring that they will continue to raise the federal funds rate,” the central bank’s benchmark interest rate, “until inflation breaks,” said Yardeni Research in a note Friday. The note suggests they went “trick-or-treating” before Halloween as they’ve now entered their “blackout period” ending the day after the conclusion of their November 1-2 policy meeting.

“The mounting fear is that something else will break along the way, like the entire U.S. Treasury bond market,” Yardeni said.

Treasury yields have recently soared as the Fed lifts its benchmark interest rate, pressuring the stock market. On Friday, their rapid ascent paused, as investors digested reports suggesting the Fed may debate slightly slowing aggressive rate hikes late this year.

Stocks jumped sharply Friday while the market weighed what was seen as a potential start of a shift in Fed policy, even as the central bank appeared set to continue a path of large rate increases this year to curb soaring inflation.

The stock market’s reaction to The Wall Street Journal’s report that the central bank appears set to raise the fed funds rate by three-quarters of a percentage point next month – and that Fed officials may debate whether to hike by a half percentage point in December — seemed overly enthusiastic to Anthony Saglimbene, chief market strategist at Ameriprise Financial.

“It’s wishful thinking” that the Fed is heading toward a pause in rate hikes, as they’ll probably leave future rate hikes “on the table,” he said in a phone interview.

“I think they painted themselves into a corner when they left interest rates at zero all last year” while buying bonds under so-called quantitative easing, said Saglimbene. As long as high inflation remains sticky, the Fed will probably keep raising rates while recognizing those hikes operate with a lag — and could do “more damage than they want to” in trying to cool the economy.

“Something in the economy may break in the process,” he said. “That’s the risk that we find ourselves in.”

‘Debacle’

Higher interest rates mean it costs more for companies and consumers to borrow, slowing economic growth amid heightened fears the U.S. faces a potential recession next year, according to Saglimbene. Unemployment may rise as a result of the Fed’s aggressive rate hikes, he said, while “dislocations in currency and bond markets” could emerge.

U.S. investors have seen such financial-market cracks abroad.

The Bank of England recently made a surprise intervention in the U.K. bond market after yields on its government debt spiked and the British pound sank amid concerns over a tax cut plan that surfaced as Britain’s central bank was tightening monetary policy to curb high inflation. Prime minister Liz Truss stepped down in the wake of the chaos, just weeks after taking the top job, saying she would leave as soon as the Conservative party holds a contest to replace her.

“The experiment’s over, if you will,” said JJ Kinahan, chief executive officer of IG Group North America, the parent of online brokerage tastyworks, in a phone interview. “So now we’re going to get a different leader,” he said. “Normally, you wouldn’t be happy about that, but since the day she came, her policies have been pretty poorly received.”

Meanwhile, the U.S. Treasury market is “fragile” and “vulnerable to shock,” strategists at Bank of America warned in a BofA Global Research report dated Oct. 20. They expressed concern that the Treasury market “may be one shock away from market functioning challenges,” pointing to deteriorated liquidity amid weak demand and “elevated investor risk aversion.”

“The fear is that a debacle like the recent one in the U.K. bond market could happen in the U.S.,” Yardeni said, in its note Friday.

“While anything seems possible these days, especially scary scenarios, we would like to point out that even as the Fed is withdrawing liquidity” by raising the fed funds rate and continuing quantitative tightening, the U.S. is a safe haven amid challenging times globally, the firm said. In other words, the notion that “there is no alternative country” in which to invest other than the U.S., may provide liquidity to the domestic bond market, according to its note.

YARDENI RESEARCH NOTE DATED OCT. 21, 2022

“I just don’t think this economy works” if the yield on the 10-year Treasury TMUBMUSD10Y, 4.228%

note starts to approach anywhere close to 5%, said Rhys Williams, chief strategist at Spouting Rock Asset Management, by phone.

Ten-year Treasury yields dipped slightly more than one basis point to 4.212% on Friday, after climbing Thursday to their highest rate since June 17, 2008 based on 3 p.m. Eastern time levels, according to Dow Jones Market Data.

Williams said he worries that rising financing rates in the housing and auto markets will pinch consumers, leading to slower sales in those markets.

“The market has more or less priced in a mild recession,” said Williams. If the Fed were to keep tightening, “without paying any attention to what’s going on in the real world” while being “maniacally focused on unemployment rates,” there’d be “a very big recession,” he said.

Investors are anticipating that the Fed’s path of unusually large rate hikes this year will eventually lead to a softer labor market, dampening demand in the economy under its effort to curb soaring inflation. But the labor market has so far remained strong, with an historically low unemployment rate of 3.5%.

George Catrambone, head of Americas trading at DWS Group, said in a phone interview that he’s “fairly worried” about the Fed potentially overtightening monetary policy, or raising rates too much too fast.

The central bank “has told us that they are data dependent,” he said, but expressed concerns it’s relying on data that’s “backward-looking by at least a month,” he said.

The unemployment rate, for example, is a lagging economic indicator. The shelter component of the consumer-price index, a measure of U.S. inflation, is “sticky, but also particularly lagging,” said Catrambone.

At the end of this upcoming week, investors will get a reading from the personal-consumption-expenditures-price index, the Fed’s preferred inflation gauge, for September. The so-called PCE data will be released before the U.S. stock market opens on Oct. 28.

Meanwhile, corporate earnings results, which have started being reported for the third quarter, are also “backward-looking,” said Catrambone. And the U.S. dollar, which has soared as the Fed raises rates, is creating “headwinds” for U.S. companies with multinational businesses.

“Because of the lag that the Fed is operating under, you’re not going to know until it’s too late that you’ve gone too far,” said Catrambone. “This is what happens when you’re moving with such speed but also such size, he said, referencing the central bank’s string of large rate hikes in 2022.

“It’s a lot easier to tiptoe around when you’re raising rates at 25 basis points at a time,” said Catrambone.

‘Tightrope’

In the U.S., the Fed is on a “tightrope” as it risks over tightening monetary policy, according to IG’s Kinahan. “We haven’t seen the full effect of what the Fed has done,” he said.

While the labor market appears strong for now, the Fed is tightening into a slowing economy. For example, existing home sales have fallen as mortgage rates climb, while the Institute for Supply Management’s manufacturing survey, a barometer of American factories, fell to a 28-month low of 50.9% in September.

Also, trouble in financial markets may show up unexpectedly as a ripple effect of the Fed’s monetary tightening, warned Spouting Rock’s Williams. “Anytime the Fed raises rates this quickly, that’s when the water goes out and you find out who’s got the bathing suit” — or not, he said.

“You just don’t know who is overlevered,” he said, raising concern over the potential for illiquidity blowups. “You only know that when you get that margin call.”

U.S. stocks ended sharply higher Friday, with the S&P 500 SPX, +2.37%,

Dow Jones Industrial Average DJIA, +2.47%

and Nasdaq Composite each scoring their biggest weekly percentage gains since June, according to Dow Jones Market Data.

Still, U.S. equities are in a bear market.

“We’ve been advising our advisors and clients to remain cautious through the rest of this year,” leaning on quality assets while staying focused on the U.S. and considering defensive areas such as healthcare that can help mitigate risk, said Ameriprise’s Saglimbene. “I think volatility is going to be high.”

U.K. inflation accelerated slightly in September, returning to the four-decade high reached in July, amid further signs that price pressures are broadening beyond the more-volatile categories of food and energy.

The consumer-price index–which measures what people pay for goods and services–increased 10.1% in September on year, up from 9.9% in August, according to data from the U.K.’s Office for National Statistics published Wednesday.

Economists polled by The Wall Street Journal expected inflation to come in at 10.0%.

The rise in inflation was driven by higher food and non-alcoholic beverage prices, which increased by 14.5% on year compared with 13.1% in August. Meanwhile, the continued fall in the price of motor fuels made the largest downward contribution, the ONS said.

Core consumer prices–a measure that excludes the volatile categories of food and energy–accelerated to 6.5% in September from 6.3% in August, signaling that inflation pressures are broadening and remain strong.

Inflation quickened in categories such as clothing and footwear, to 8.5% from 7.6%, furniture and household goods, to 10.7% from 10.1%, and hotels and restaurants, to 9.7% from 8.7%.

“[Wednesday’s] release highlights the danger that underlying inflation remains strong even as the economy weakens,” Capital Economics’ chief U.K. economist Paul Dales said in a note.

Economists expect U.K. inflation to remain high in the months ahead, even as the government’s cap on household energy bills is likely to prevent it from rising further.

Write to Xavier Fontdegloria at xavier.fontdegloria@wsj.com

Rent growth is beginning to cool. But it’s descending from a heck of a peak.

Rental prices climbed 7.2% between September 2021 to September of this year, the largest annual increase since 1982, according to consumer price data released Thursday. Overall, shelter costs were also among the most significant drivers in rising consumer prices, along with the cost of food and medical care, the Labor Department said.

Still, it’s not all bad news for tenants. A new report from Realtor.com out Thursday found that nationwide, median rental prices in 50 large metros grew at their slowest annual pace in 16 months in September — at 7.8%. That marked the second consecutive month of single-digit year-over-year growth for 0-2 bedroom properties, and it meant that median asking rents fell by $12 in a month, Realtor.com said.

Housing inflation in the Consumer Price Index lags trends in the rental market, though, meaning the slowdown in rent growth might not register in the data for a while.

While median rental prices are still nearly 23% higher than they were two years ago, they’re no longer climbing at breakneck speeds with no end in sight. These days, economists say, that counts as a silver lining.

“After more than a year of double-digit yearly rent gains and nearly as many months of record-high rents, it’s especially important to see consistency before we confirm a major shift like the recent rental market cool-down,” Realtor.com Chief Economist Danielle Hale said in a statement. “But September data provides that evidence, as national rents continued to pull back from their latest all-time high registered just two months ago.”

“This return of more seasonal norms indicates that rental markets are charting a path back toward a more typical balance between supply and demand, compared to the previous year,” Hale added. “We expect rent growth to keep slowing in the months ahead, partly driven by the impact of inflation on renters’ budgets.”

(Realtor.com is operated by News Corp NWSA, +1.64%

subsidiary Move Inc., and MarketWatch is a unit of Dow Jones, which is also a subsidiary of News Corp.)

A Redfin RDFN, -3.55%

report out Thursday, meanwhile, said rents grew 9% year-over-year in September — the slowest pace since August 2021. Rents were still way up year-over-year in cities like Oklahoma City (24.1%), Pittsburgh (20%), and Indianapolis (17.9%.)

Calling inflation “unacceptably high,” Federal Reserve leaders saw their strategy of fighting price pressures aggressively as less risky to the economy than doing too little, minutes of the bank’s last meeting show.

The Fed approved another jumbo-size increase in U.S. interest rates at its Sept. 21-22 meeting. It also signaled plans for another pair of big increases before year-end in a surprise to Wall Street DJIA, -0.10%.

The minutes of the Fed’s meeting underscore that top officials were disappointed and worried about persistently high inflation.

“A sizable portion of the economic activity has yet to display much response,” the Fed minutes said. “Inflation had not yet responded appreciably to a policy tightening.”

While some senior Fed officials also worried the bank could go too far and damage the economy, the majority appeared to believe it was vital for the central bank to squelch inflation, even if that meant keeping rates high for a prolonged period.

“Many participants emphasized that the cost of taking too little action to bring down inflation likely outweighed the cost of taking too much action,” the minutes said.

The Fed predicts the economy will eventually slow as rates rise, but it noted the labor market remains extremely tight.

Fed officials also expressed concern that oil prices could rise again, supply chains would not heal as quickly as expected and that rising wages could exacerbate inflation.

“Inflation was declining more slowly than [Fed officials] had been anticipating,” the minutes said.

The internal Fed debate has also playing out publicly since the last meeting.

Some senior officials such as Atlanta Federal Reserve President Raphael Bostic hope the bank will make enough progress in its fight against inflation to “pause” rate hikes at the end of this year.

Fed critics contend the bank is going to go too far and could plunge the economy into a second recession in four years. A pause would allow the Fed to see how much its prior rate hikes have succeeded in lowering the rate of inflation, they say.

Failing to do so, they contend, would make it even harder to get prices back under control if Americans come to view high inflation as the norm. That would do even more damage to the economy in the long run.

Jennifer Lee, senior economist at BMO Capital Market, downplayed the debate and said the Fed in unified on its next few steps.

“The Federal Reserve is pretty much in sync and is not going to be easing anytime soon,” she said.

Since March the Fed has lifted a key short-term interest rate from near zero to an upper end of 3.25%. And the central bank has telegraphed plans to raise the so-called fed funds rate to as high as 4.75% by next year.

Rising U.S. interest rates has done little so far to douse inflation.

The rate of inflation, using the Fed’s preferred PCE price index, rose at a yearly rate of 6.2% as of August. That’s a long way off from the Fed’s forecast for inflation to fall to 2.8% in 2023 and 2.3% by 2024.

The higher cost of borrowing has only chilled a few parts of the economy, most notably housing.

The rate on a 30-year mortgage has surged above 7% to a 16-year high from less than 3% one year ago. The result has been a slowdown in home buying and construction and softer sales of home furnishings.

Most consumer and business loans are influenced by the fed funds rate.

U.S. stock indexes edged higher on Wednesday, while hotter-than-expected producer price inflation data deepened concerns that the Federal Reserve may continue its aggressive interest rate hikes.

How are stock-index futures trading

The Dow Jones Industrial Average DJIA, +0.50%

was up 120 points, or 0.4% to around 29,355

The S&P 500 SPX, +0.35%

gained 5.3 points, or 0.2% to about 3,594

The Nasdaq Composite COMP, -6.31%

traded 5.1 points, or 0.1% higher to 10,430

On Tuesday, the Dow Jones Industrial Average rose 36 points, or 0.12%, to 29239, the S&P 500 declined 24 points, or 0.65%, to 3589, and the Nasdaq Composite dropped 116 points, or 1.1%, to 10426. The S&P 500 closed down 1,177 points, or 24.7% for the year to date.

What’s driving markets

The 12-month rate of producer price inflation slowed to to 8.5% from 8.7% while the annual core rate, excluding food and energy, was unchanged at 5.6%, but the monthly rate rose 0.4% in September, above forecast, and the monthly core PPI was also up 0.4% in September.

Such data has worsened fears that to curb inflation, the Fed will continue its aggressive rate hikes, which may steer the U.S. economy into a recession.

“We believe the odds of a recession in 2023 are now better than 50%,” Greg Bassuk, chief executive at AXS Investments, wrote in a Wednesday note. “Last week’s market turbulence saw volatility at levels we have not seen since July, and we believe investors should brace for ongoing market volatility and uncertainty throughout Q4, in concert with another likely Fed interest rate hike to the tune of 0.75% in November,” according to Bassuk.

The 10-year Treasury yield BX:TMUBMUSD10Y, which started the year around 1.65% was trading at 3.931% on Wednesday, off 1.3 basis points, after the producer price inflation data.

Traders are also awaiting U.S. September consumer prices data on Thursday due at 8:30 am Eastern Time.

“Inflation has proven to be difficult to forecast and given the negative ‘shock’ from the August CPI, it would be difficult for any investor to have conviction going into this report,” according to Tom Lee, head of research at Fundstrat.

“For us, analyzing the month over month numbers is much more important than looking at the headline,” Zachary Hill, head of portfolio management at Horizon Investments, said in an interview.

“The way we’ve been thinking about it, the last three months annualized [inflation] gives you a kind of a decent idea of where the shorter term trends are around inflation,” Hill said. “We think that’s what the Fed is going to be looking at to see progress towards their 2% goal. And unfortunately, based on various measures, we’re nowhere near that today.”

Investors have become increasingly concerned of late that severe stresses in the financial system may emerge as central banks switch from the era of zero or negative interest rates to sharply higher borrowing costs as they try to tackle inflation at multi-decade highs.

“[G]lobal financial conditions have tightened as central banks continue to raise interest rates. Our latest Global Financial Stability Report shows that financial stability risks have increased since our last report, with the balance of risks tilted to the downside,” said the International Monetary Fund in a report released on Tuesday.

“The mood of global investors was gloomy enough and hardly needed yesterday’s reminder from the IMF that the risks to financial stability have increased,” Ian Williams, strategist at Peel Hunt, noted. “Its report highlighted specifically (if obviously) the threats from persistent inflation, China’s slowdown and the war in Ukraine. The highlighted ‘disorderly repricing of risk’ is arguably already underway.”

The Fed may offer its view on the topic as a number of officials are due to give comments on Wednesday. Minneapolis Fed President Neel Kashkari said the Fed is “dead serious” about getting inflation down. Fed vice chair Michael Barr will speak at 1:45 p.m. The minutes of the Fed’s previous monetary policy setting meeting will be released at 2 p.m. ET and Fed governor Michelle Bowman will deliver comments at 6.30 pm.

PHG, -11.33%

plunged 12% after the Dutch tech company issued its second profit warning this year, forewarning that supply chain problems will impact sales and third-quarter profits.

Intel Corp. INTC, +1.50%

may fire thousands of workers by the end of the month, around the same time the chip manufacturer reports quarterly results amid a tough year for semiconductor makers, Bloomberg reported late Tuesday. The company’s shares rose 1% Wednesday.

Shares of PepsiCo Inc. climbed 4.6% Wednesday, after the beverage and snack giant reported third-quarter profit and revenue that rose above expectations and raised its full-year outlook, as higher prices helped offset some volume weakness.

Hotter-than-expected consumer-price index readings have triggered some of the stock market’s biggest one-day selloffs in 2022, serving to focus investor attention ahead of the latest measure of retail inflation on Thursday.

The September CPI reading from the Bureau of Labor Statistics, which tracks changes in the prices paid by consumers for goods and services, is expected to show an 8.1% rise from a year earlier, slowing from an 8.3% year-over-year rise seen in August, according to a survey of economists by Dow Jones.

The S&P 500 SPX, +0.23%

is down 24.7% year to date through Tuesday, according to Dow Jones Market Data. Most of the single days that are responsible for the decline occurred on or around CPI reports or Fed-related events, said Nicholas Colas,co-founder of DataTrek Research, in a note on Monday. Two of the S&P 500’s nine largest down days this year have come on days when CPI data was released, he noted.

Without those nine down days, the S&P 500 would have been up 8.6% year-to-date through the end of last week, Colas wrote.

For example, the S&P 500 recorded its biggest daily percentage fall since June 2020 last month on CPI reporting day, when the large-cap index shed 177.7 points, or 4.3%. On June 13, the S&P slid 3.9% and ended in a bear market after the May inflation report came in hotter than expected, with CPI hitting a 40-year high. Three days later, the index dropped 3.3% following what was then the Federal Reserve’s largest rate hike since 1994.

“Every time we see large selloffs it means investor confidence has collided with macro uncertainty,” warned Colas. “History shows that valuations suffer when this happens repeatedly. As we see further equity market volatility, keep your expectations for valuations modest. They will bottom when macro news is greeted with a rally that sticks, not one that fades away a few days later.”

Bloomberg reported that JPMorgan’s analysts led by Andrew Tyler expect the stock market to tumble by 5% on Thursday if the inflation gauge comes in above August’s 8.3%. If the result is in line with the consensus, the S&P 500 would fall about 2%. On the flip side, the team forecast any softening inflation below 7.9% will spark an equity rally where the index may jump at least 2%.

However, Aoifinn Devitt, chief investment officer at Moneta, said the market would take the top-line number and react to it.

“I would expect to see a similar reaction to what we saw from Friday’s jobs report, which was a positive number that translates into a negative stock-market reaction,” Devitt told MarketWatch via phone. “Stock prices have adjusted. Earnings have adjusted, so there’s already been this kind of managing of expectations (which) leads me to take up some of this and try to be on the upside for some of these stocks, just because so much of the bad news is already there.”

The September inflation report is expected to show the headline CPI continued moderating as gasoline and commodity prices fell to the February level. But future expectations may have changed after OPEC+ announced last week its decision to cut production by 2 million barrels a day, which may have “lagging effect (on inflation data)“, according to Devitt.

Meanwhile, shelter costs and medical care services, which have been at the core of inflationary pressures and are sticky, are expected to increase by 0.7% on a monthly basis. The core CPI is expected to be running at a year-over-year pace of 6.5%, up from 6.3% in August.

“The bulls are desperate for signs that inflation is set to roll back to the Fed’s target — they may be mistaken, and while headline inflation is expected to fall thanks to a decline in energy, the Fed’s focus has shifted towards core CPI,” said Chris Weston, head of research of Pepperstone, in a Tuesday note.

“This is why core CPI will unlikely roll over anytime soon and why the Fed has made it clear they will hike further and leave the fed fund rate in restrictive territory for an extended period,” he wrote.

U.S. stocks finished mostly lower on Tuesday with the Nasdaq Composite dropping 1.1%, while the S&P 500 shed 0.6% and the Dow Jones Industrial Average DJIA, +0.38%

edged up 0.1%. Stock-index futures pointed to a higher start Wednesday.

Don’t assume the worst is over, says investor Larry McDonald.

There’s talk of a policy pivot by the Federal Reserve as interest rates rise quickly and stocks keep falling. Both may continue.

McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, expects more turmoil in the bond market, in part, because “there is $50 trillion more in world debt today than there was in 2018.” And that will hurt equities.

The bond market dwarfs the stock market — both have fallen this year, although the rise in interest rates has been worse for bond investors because of the inverse relationship between rates (yields) and bond prices.

About 600 institutional investors from 23 countries participate in chats on the Bear Traps site. During an interview, McDonald said the consensus among these money managers is “things are breaking,” and that the Federal Reserve will have to make a policy change fairly soon.

Pointing to the bond-market turmoil in the U.K., McDonald said government bonds that mature in 2061 were trading at 97 cents to the dollar in December, 58 cents in August and as low as 24 cents over recent weeks.

When asked if institutional investors could simply hold on to those bonds to avoid booking losses, he said that because of margin calls on derivative contracts, some institutional investors were forced to sell and take massive losses.

And investors haven’t yet seen the financial statements reflecting those losses — they happened too recently. Write-downs of bond valuations and the booking of losses on some of those will hurt bottom-line results for banks and other institutional money managers.

Interest rates aren’t high, historically

Now, in case you think interest rates have already gone through the roof, check out this chart, showing yields for 10-year U.S. Treasury notes TMUBMUSD10Y, 3.898%

over the past 30 years:

The yield on 10-year Treasury notes has risen considerably as the Federal Reserve has tightened during 2022, but it is at an average level if you look back 30 years.

FactSet

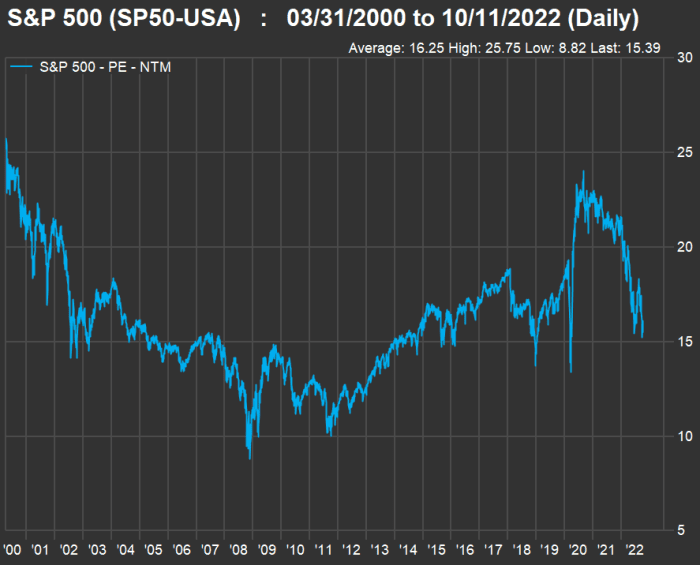

The 10-year yield is right in line with its 30-year average. Now look at the movement of forward price-to-earnings ratios for S&P 500 SPX, -0.03%

since March 31, 2000, which is as far back as FactSet can go for this metric:

FactSet

The index’s weighted forward price-to-earnings (P/E) ratio of 15.4 is way down from its level two years ago. However, it is not very low when compared to the average of 16.3 since March 2000 or to the 2008 crisis-bottom valuation of 8.8.

Then again, rates don’t have to be high to hurt

McDonald said that interest rates didn’t need to get anywhere near as high as they were in 1994 or 1995 — as you can see in the first chart — to cause havoc, because “today there is a lot of low-coupon paper in the world.”

“So when yields go up, there is a lot more destruction” than in previous central-bank tightening cycles, he said.

It may seem the worst of the damage has been done, but bond yields can still move higher.

Heading into the next Consumer Price Index report on Oct. 13, strategists at Goldman Sachs warned clients not to expect a change in Federal Reserve policy, which has included three consecutive 0.75% increases in the federal funds rate to its current target range of 3.00% to 3.25%.

The Federal Open Market Committee has also been pushing long-term interest rates higher through reductions in its portfolio of U.S. Treasury securities. After reducing these holdings by $30 billion a month in June, July and August, the Federal Reserve began reducing them by $60 billion a month in September. And after reducing its holdings of federal agency debt and agency mortgage-backed securities at a pace of $17.5 billion a month for three months, the Fed began reducing these holdings by $35 billion a month in September.

Bond-market analysts at BCA Research led by Ryan Swift wrote in a client note on Oct. 11 that they continued to expect the Fed not to pause its tightening cycle until the first or second quarter of 2023. They also expect the default rate on high-yield (or junk) bonds to increase to 5% from the current rate of 1.5%. The next FOMC meeting will be held Nov. 1-2, with a policy announcement on Nov. 2.

McDonald said that if the Federal Reserve raises the federal funds rate by another 100 basis points and continues its balance-sheet reductions at current levels, “they will crash the market.”

A pivot may not prevent pain

McDonald expects the Federal Reserve to become concerned enough about the market’s reaction to its monetary tightening to “back away over the next three weeks,” announce a smaller federal funds rate increase of 0.50% in November “and then stop.”

He also said that there will be less pressure on the Fed following the U.S. midterm elections on Nov. 8.

Eurozone inflation hit a new record in September and is expected to rise further in the coming months amid higher energy prices, increasing the likelihood of a lengthier and deeper economic contraction at year-end.

The consumer price index–a measure of what consumers pay for goods and services–increased 10.0% in September compared with the same month a year earlier after climbing 9.1% in August, according to preliminary data from Eurostat, the European Union’s statistics agency.

The reading beats the 9.7% consensus forecast from economists polled by The Wall Street Journal.

September’s rise in the inflation rate was driven by energy prices, with prices up 40.8% year-on-year in September after a 38.6% increase in August.

There was also an acceleration of food, alcohol and tobacco prices, which rose 11.8% on year compared with a 10.6% rise in August, data from Eurostat showed.

The core consumer price index–which excludes the more volatile categories of food and energy–rose 4.8% on year in September, up from 4.3% in August.

Economists expect eurozone inflation to increase further in the coming months, remaining above double digits. Elevated inflation adds pressure on the European Central Bank, which raised key interest rates by 75 basis points in September and is expected to increase rates again by 75 basis points at its next meeting in October.

U.S. stocks dropped sharply Friday, with major indexes posting their lowest finishes since 2020 and logging a third straight quarterly decline as investors grew more fearful that aggressive interest rate hikes by the Federal Reserve will drive the economy into a downturn in an attempt to quell inflation.

What’s happening

The Dow Jones Industrial Average DJIA, -1.71%

dropped 500.10 points, or 1.7%, to close at 28,725.51.

The S&P 500 SPX, -1.51%

dropped 54.85 points, or 1.5%, to end at 3,585.61.

The Nasdaq Composite COMP, -0.43%

shed 161.88 points, of 1.5%, finishing at 10,575.61.

The drop left the Dow and S&P 500 at their lowest since November 2020, while the Nasdaq posted its lowest close since July 29, 2020. The Dow dropped 8.8% in September, while the S&P 500 tumbled 9.3% and the Nasdaq lost 10.5%.

For the quarter, the Dow dropped 6.7%, the S&P 500 declined 5.3% and the Nasdaq gave up 4.1%.

What’s driving the market

In keeping with the historical pattern, U.S. stocks suffered during the month of September as an assertive Federal Reserve helped push Treasury yields and the dollar higher, which in turn undermined equity valuations.

Investors on Friday digested a reading from the personal consumption expenditure inflation index for August, which showed that core consumer prices climbed by 0.6% last month, more than Wall Street’s forecast of 0.5%. The core inflation measure excludes volatile food and energy prices.

“That means the Fed will remain hell-bent on killing inflation. And the best way to do that is to increase rates, kill the housing market, and get rental costs down. The PCE doesn’t have housing and rents as a big component as the CPI does, so the fact that it is rising is a warning sign,” said Louis Navellier, founder of Navellier & Associates, in emailed comments.

The reading largely confirmed similar data from the consumer-price index, another closely watched inflation barometer, which sent stocks lower earlier this month. Since that report was released just over two weeks ago, the S&P 500 has fallen more than 10%.

Helping to underscore this point, data out of the eurozone showed inflation accelerated at a record pace last month.

In other news, investors also heard from Fed Vice Chair Lael Brainard, who reiterated that the central bank would keep interest rates elevated to combat inflation, even if it harms the economy.

Since it will take time for high interest rates to bring inflation down, Brainard said the Fed is “committed to avoiding pulling back prematurely.”

Investors were also keeping an eye on megacap tech stocks. Apple Inc. AAPL fell 3% on Friday after leading markets lower a day earlier following a downgrade by Bank of America.

A final reading on the University of Michigan consumer-sentiment index for September showed consumers’ view of the economy improved somewhat during the month due to falling gas prices, even as their outlook remained broadly pessimistic.

Investors are now facing “what may be one of the most important earning seasons in a very long time, with a major rally in the cards if earnings don’t disappoint, and if the bears are right, lead to a further leg down if earnings disappoint and 4th quarter estimates are cut,” Navellier said.

Micron Technology MU, +0.18%

stock rose 0.2% after a report that Japan will grant it a $320 million subsidy to make advanced memory chips at its Hiroshima plant. That came a day after Micron posted quarterly earnings that included a forecast for a loss in the coming quarter and plans to scale back a build out of capacity.

— Steve Goldstein and Barbara Kollmeyer contributed to this article