[ad_1]

Home-improvement retailer logs sales increase even as it again records fewer transactions

Source link

[ad_1]

[ad_1]

More than 1 million barrels a day of Russian oil exports are set to be upended by Western sanctions expected to come into force within weeks, shipments Moscow will struggle to redirect elsewhere which threatens to further tighten global energy markets, the International Energy Agency said Tuesday.

Russian crude oil exports, including to the European Union, were largely unchanged last month, despite the prospect of an imminent EU ban on Russian crude oil imports and a separate plan to cap prices for Russian crude oil sales, the Paris-based agency said in a monthly report.

Russian exports to the EU were 1.5 million barrels a day in October, of which 1.1 million barrels a day will be halted when the bloc’s ban comes into effect on December 5, the IEA said.

It was unclear how much of those supplies Russia would be able to redirect to customers elsewhere in the world, the IEA said. India, China and Turkey have snapped up discounted Russian crude shipments, but buying from those nations has stabilized in recent months, the IEA said. Meanwhile, the volume would be too large for the remaining nations to absorb, the agency said.

The warning comes as the IEA predicted additional demand this year and next would come from China as the nation slowly eases its Covid-19 lockdown measures–though global demand growth will be sluggish as economies are expected to struggle.

The agency upped its 2022 global oil demand forecasts by 170,000 barrels a day to 99.8 million barrels a day. For 2023, the IEA raised its oil demand forecasts by 130,000 barrels a day to 101.4 million barrels a day.

Russia’s declining oil output will drag on global supplies which will grow at an anemic rate next year, failing to keep pace with growing oil demand. The IEA said global oil supplies would rise to 100.7 million barrels a day in 2023, 100,000 barrels a day more than it was forecasting last month, but still 700,000 barrels a day short of the world’s expected appetite for oil

CL.1,

Write to Will Horner at william.horner@wsj.com

[ad_2]

[ad_1]

Shares of Chinese internet giants jumped in Hong Kong, after official data showed better-than-expected October retail sales in the world’s second-largest economy.

Alibaba Group Holding Ltd.

BABA,

9988,

jumped 9.8%, Kuaishou Technology

1024,

surged 8.7%, Tencent Holdings Ltd.

700,

rose 8.0% and Meituan

3690,

was up 5.8%. The Hang Seng Tech Index

HSXTCHINDXXX,

has gained as much as 7.7% and was last up 6.1%

The sector’s sharp upturn came after China’s National Bureau of Statistics said online retail sales of physical goods rose 7.2% in the first 10 months of the year. The number, closely watched by investors as an indicator of the country’s consumption trends, outpaced a 6.1% rise in the January-to-September period.

Jefferies analysts estimate that online retail sales grew more than 15% in October, accelerating from the three consecutive months of below-10% growth seen since July.

Write to Yifan Wang at yifan.wang@wsj.com

[ad_2]

[ad_1]

The latest message from former FTX chief executive Sam Bankman-Fried left onlookers puzzled and alarmed after the swift decline into bankruptcy for the cryptocurrency exchange he founded.

In successive tweets, Bankman-Fried’s twitter account merely stated, “What,” followed by capital letters H.A.P.P.E.N., unfurled slowly over the span of about 19 hours.

Bankman-Fried has been an active tweeter throughout FTX’s demise, earlier having written that he was “shocked to see things unravel the way they did.”

Twitter and Tesla

TSLA,

CEO Elon Musk, who’s also having some difficulties, tweeted with fire emojis to an attempt at a translation of the cryptic tweet.

Musk also tweeted his amusement at the claim that Bankman-Fried played a “League of Legends” game — the same game the executive infamously was playing when the venture-capital firm Sequoia invested in FTX. Court filings from Musk’s failed attempt to get out of his Twitter purchase show that he doubted that Bankman-Fried ever had $3 billion liquid to co-invest in Twitter.

While the broader social-media sentiment was a wish for Bankman-Fried to be jailed, there also was concern for his health.

FTX has filed for Chapter 11 bankruptcy protection, and over the weekend there also seems to have been a hack of customer funds. The securities regulator in FTX’s headquarters of the Bahamas meanwhile said it had not requested the prioritization for withdrawals of funds for Bahamian clients.

Reuters reported the allegation Bankman-Fried had a “back door” that allowed him to mask the transfer of customer funds to his Alameda hedge fund, which Bankman-Fried told the news agency was just “confusing internal labeling.”

The former FTX CEO couldn’t be reached for comment.

[ad_2]

[ad_1]

CHARLOTTESVILLE, Va. (AP) — The three students killed in a shooting at the University of Virginia were all members of the school’s football team, the school’s president said.

President Jim Ryan told a Monday morning news conference the shooting happened Sunday night on a school bus of students returning from an off-campus trip.

The suspect has been identified as Christopher Darnell Jones Jr., who is also student.

The incident occurred Sunday near a university parking garage. In addition to the three football players killed, two others were reported to have been wounded.

Police went on a manhunt Monday in search of the student suspected in the attack, officials said.

During a press conference in the 11 o’clock hour local time, the university police chief, Tim Longo, was given word that the suspect was in custody. He immediately returned to the microphone and reported that update to the assembled reporters.

Classes at the university were canceled Monday, following the violence Sunday night, and the Charlottesville campus was unusually quiet as authorities searched for the suspect, whom university President Ryan identified as Christopher Darnell Jones Jr.

A shelter-in-place order to the university community had been lifted less than an hour earlier after a law-enforcement search of the campus.

In a letter to the university posted on social media, Ryan said the shooting happened around 10:30 p.m. Sunday.

The university’s emergency management issued an alert Sunday night notifying the campus community of an “active attacker firearm.” The message warned students to shelter in place following a report of shots fired on Culbreth Road on the northern outskirts of campus.

Access to the shooting scene was blocked by police vehicles Monday morning.

Officials urged students to shelter in place and helicopters could be heard overhead as a smattering of traffic and dog-walkers made their way around campus.

The university police department posted a notice online saying multiple police agencies including the state police were searching for a suspect who was considered “armed and dangerous.”

In his letter to campus, the university president said Jones was suspected to have committed the shooting and that he was a student.

“This is a message any leader hopes never to have to send, and I am devastated that this violence has visited the University of Virginia,” Ryan wrote. “This is a traumatic incident for everyone in our community.”

Eva Surovell, 21, the editor in chief of the student newspaper, The Cavalier Daily, said that after students received an alert about an active shooter late Sunday night, she ran to the parking garage, but saw that it was blocked off by police. When she went to a nearby intersection, she was told to go shelter in place.

“A police officer told me that the shooter was nearby and I needed to return home as soon as possible,” she said.

She waited with other reporters, hoping to get additional details, then returned to her room to start working on the story. The gravity of the situation sunk in.

“My generation is certainly one that’s grown up with generalized gun violence, but that doesn’t make it any easier when it’s your own community,” she said.

The Bureau of Alcohol, Tobacco, Firearms and Explosives said agents were responding to the campus to assist in the investigation.

The Virginia shooting came as police were investigating the deaths of four University of Idaho students found Sunday in a home near the campus. Officers with the Moscow Police Department discovered the deaths when they responded to a report of an unconscious person just before noon, according to a news release from the city. Authorities have called the deaths suspected homicides but did not release additional details, including the cause of death.

On April 16, 2007, another Virginia university was the scene of what was then one of the deadliest shootings in U.S. history. Twenty-seven students and five faculty members at Virginia Tech were gunned down by Seung-Hui Cho, a 23-year-old mentally ill student who later died from a self-inflicted gunshot wound.

[ad_2]

[ad_1]

Investors feeling giddy about last week’s sharp rally for stocks might want to give a listen to Tom Waits’ song, “Whistlin’ Past the Graveyard” from 1978, to sober up for the dangers that still lurk ahead.

The surge in stocks catapulted the S&P 500 index

SPX,

almost back to the 4,000 mark on Friday, also lifting it to the biggest weekly gain in roughly five months, according to Dow Jones Market Data.

Investors showed courage on signs of a slight slowing of inflation, but the fortitude also comes as a drearier backdrop for investors has been unfolding in plain sight. Massive layoffs at big technology companies, the dramatic implosion of crypto-exchange FTX, and the day-to-day pain of high inflation and skyrocketing borrowing on businesses and households are all taking a toll.

“We are not convinced this is the beginning of a new bull market,” said Sam Stovall, chief investment strategist at CRFA Research. “We believe that we are headed for recession. That has not been factored into earnings estimates and, therefore, share prices.”

Stovall also said the stock market has yet to see the “traditional shakeout of confidence capitulation that we typically see that marks the end of the bear markets.”

From Meta Platforms Inc.

META,

to Lyft Inc.

LYFT,

to Netflix Inc.

NFLX,

there is a wave of major technology companies resorting to layoffs this fall, a threat that could sweep other sectors of the economy if a recession materializes.

Yet, information technology stocks in the S&P 500 jumped 10% for the week, while financials, which stand to benefit from higher interest rates, rose 5.7%, according to FactSet.

That could reflect optimism about the odds of a slower pace of Federal Reserve rate hikes in the months ahead, after sharp rate rises helped to undermine valuations and pull tech stocks dramatically lower in the past year. However, Loretta Mester, president of the Cleveland Fed, and other Fed officials since the October inflation reading on Thursday have reiterated the need to keep rates high, until 7.7% annual rate finds a clearer path to the central bank’s 2% target.

The stock-market rally also might suggest that investors view continued mayhem in the crypto sector as contained, despite bitcoin

BTCUSD,

trading near its lowest level in two years and the shocking collapse in recent days of FTX, once the world’s third-largest cryptocurrency exchange.

Read: FTX’s fall: ‘This is the worst’ moment for crypto this year. Here’s what you should know.

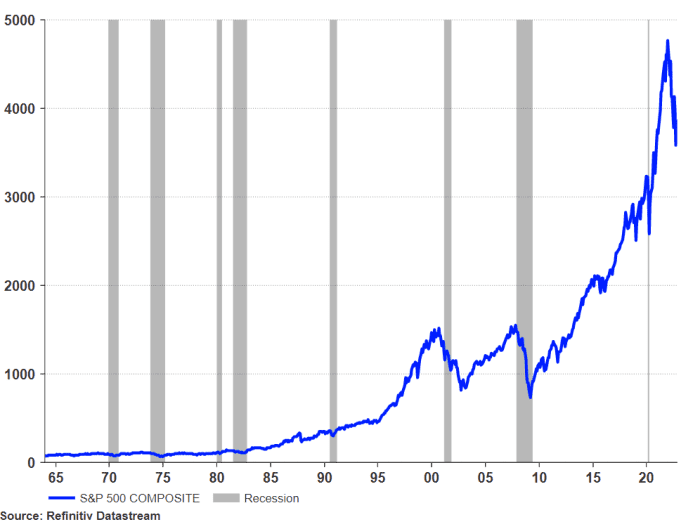

Blows to the American economy rarely have been good for stocks. A look at seven past recessions, starting in 1969, shows declines for the S&P 500 as more typical than gains, with its most violent drop occurring in the 2007-2009 recession.

Refinitiv data, London Stock Exchange Group

While a looming U.S. recession isn’t a foregone conclusion, CEOs of America’s biggest banks have been warning about the risks for months. JP Morgan Chase’s Jamie Dimon said in October that a “tough recession” could drag the S&P 500 down another 20%, even though he also said consumers were doing fine, for now.

Still, the steady stream of warnings about the recession odds have left many Americans confused and wondering if one can even happen without an increase in job losses.

Big moves lately in stocks also have been hard to decode, given the economy was shocked back to life in the pandemic by trillions of dollars in fiscal stimulus and easy-money policies from the Fed that are now being reversed.

“What I think goes unnoticed, certainly by the average person, is that these moves are not normal,” said Thomas Martin, senior portfolio manager at Globalt Investments, about stock swings this week.

“It’s all about who is positioned how — and for what — and how much leverage they’re employing,” Martin told MarketWatch. “You get these outsized moves when people are offside.”

Here’s a view of the sharp trajectory upward of the S&P 500 since 2010, but also its dramatic drop this year.

Refinitiv Datastream

While Martin isn’t ruling out the potential for a seasonal “Santa Claus” rally heading into year-end, he worries about a potential leg lower for stocks next year, particularly with the Fed likely to keep interest rates high.

“Certainly what’s being priced in now is either no recession or a very, very mild recession,” he said .

However, Kristina Hooper, Invesco’s chief global market strategist, said the overarching story might be one of stocks sniffing out the first steps in a path to economic recovery, and the Fed potentially stopping its rate hikes at a lower “terminal” rate than expected.

The Fed increased its benchmark interest rate to a 3.75% to 4% range in November, the highest in 15 years, but also has signaled it could top out near 4.5% to 4.75%.

“If often happens that you can see stocks do well, in a less-than-good economic environment,” she said.

The S&P 500 rose 4.2% for the week, while the Dow Jones Industrial Average

DJIA,

gained 5.9%, posting its best weekly gain since late June, according to Dow Jones Market Data. The Nasdaq Composite Index shot up 8.1% for the week, its best weekly stretch in seven months.

In U.S. economic data, investors will get an update on household debt on Tuesday, retail sales and homebuilder data on Wednesday, followed by jobless claims and housing starts data Thursday. Friday brings existing home sales.

[ad_2]

[ad_1]

President Joe Biden addressed the U.N. climate summit Friday with his Democratic party having survived a projected Republican “red wave” in the midterm elections — and in doing so protecting at least the bulk of a landmark climate-change spending law he signed this year.

Biden addressed the U.N.’s Conference of the Parties (COP27) climate summit in Egypt on his way to Bali, Indonesia, for the Group of 20 meeting and a planned sit-down with China’s Xi Jinping.

In August, Biden signed the largest U.S. investment in fighting climate change ever, the Inflation Reduction Act (IRA). That puts him on stronger footing on the global stage than at last year’s COP26 gathering in Scotland, when American commitments to carbon reduction weren’t backed by law.

Four themes color Biden’s trip: Russia’s war in Ukraine, escalating trade and security tensions with China, the potential for a global recession in the coming months and the existential problem of climate change.

“The climate crisis is about human security, economic security, environmental security, national security and the very life of the planet,” Biden said in his address to the summit.

Biden apologized to the group for the U.S. pulling out of the Paris Climate Accord — and its global-warming limit of 1.5 degrees Celsius (equivalent to 2.7 degrees Fahrenheit) — which the country did briefly under President Donald Trump. In a remark that garnered speech-pausing applause from the audience, Biden said the U.S. commitment to the global effort, struck in Paris in 2015 and reaffirmed each year, is apparent in the climate-focused IRA.

Biden also highlighted a proposal that would require large federal contractors to develop carbon-reduction targets and disclose their greenhouse gas emissions, by which the administration hopes to use the federal government’s purchasing power to slow the impacts on climate from the private sector and bolster vulnerable supply chains.

“As the world’s largest customer, with more than $650 billion in spending last year, the United States government is putting our money where our mouth is to strengthen accountability for climate risk and resilience,” he said.

Biden’s other task is to convince the summit participants of the U.S. commitment to engage with China, not only on trade and security matters, but also as part of an alliance between the world’s two top polluters to deliver on their carbon-reduction plans and show measurable progress. The U.S. has said it can reach net-zero emissions by 2050; China’s target date is 2060. Both countries have said they can show progress as soon as 2030, but some observers say time may be running out to hit that marker.

At the start of the COP27 summit, U.N. chief Antonio Guterres called for a historic agreement — or “climate solidarity pact” — between developed and emerging economies. The flagship climate conference runs Nov. 6-18.

The U.S. and China, the world’s two largest economies and top greenhouse-gas emitters, “have a particular responsibility to join efforts to make this pact a reality,” Guterres said earlier this week.

Biden used Democrats’ better-than-projected midterm-election results as an opportunity to reassure the world that the U.S. is committed to doing its part to address threats to the planet as a whole, including climate change.

“If the United States tomorrow were to, quote, withdraw from the world, a lot of things would change around the world. A whole lot would change,” Biden said in remarks at a press conference on Nov. 9, the day after the election.

The IRA’s $375 billion commitment to climate efforts, including manufacturing and purchasing incentives for electric vehicles

GM,

F,

tax breaks for home solar and a boost to manufacturers who green up their operations, will provide Biden with leverage as he works to convince other countries to strengthen their own efforts to reduce greenhouse-gas emissions.

Current and former Biden climate officials told the Associated Press that the IRA was crafted in a way that will make it difficult for a future Republican Congress or president to reverse it. That’s in part because of the law’s tax incentives, which are the sort of low-tax strategies normally favored by Republicans, and because much of the advancing green technology would bring jobs to strongly Republican states.

Republicans won’t have a veto-proof majority in the new Congress, even if the GOP ends up with an advantage of a few seats. And even if a Republican wins the White House in 2024, the tax credits will be in place and will already be spurring industry, said Samantha Gross, head of climate and energy studies at the centrist Brookings Institution.

“It’s a lot of tax credits and goodies that make it hard to repeal,” Gross said.

At the climate negotiations in Egypt, Biden’s special climate envoy, John Kerry, said, “Most of what we’re doing cannot be changed by anyone else who comes to Washington, because most of what we do is in the private sector. The marketplace has made its decision to do what we need to do.”

Still, it won’t be all smooth sailing for Biden. Republicans, who as of Friday were close to clinching a modest advantage in the House (control of the Senate will likely hinge on a runoff election in Georgia), have said they will work to repeal parts of the law and advance their own climate and energy bill. They have accused Biden of contributing to rising energy prices by blocking more drilling of U.S. fossil fuels

CL00,

Those fossil fuels are the major contributor to climate change.

While Biden may be moving slower than Republicans would like when it comes to permitting, he has in fact called for more oil drilling to help calm energy markets during the Russia-Ukraine crisis and has even chastised profitable oil companies for not releasing more product. It’s a narrow line for the president to walk and in doing so, he has raised the ire of some environmental groups.

Related: Biden tightens methane emissions rule, but still wants more U.S. oil for now

Still, Biden argues there is scope for both near-term emergency energy policies and a long-term commitment to the transition from oil and gas.

“Russia’s war only enhances the urgency of the need to transition the world off its dependence on fossil fuels,” Biden said Friday. “[N]o action can be taken without a nation understanding that it can’t use energy as a weapon and hold the global economy hostage.”

Outside the U.S., there are also concerns that rising energy costs and a looming recession could dampen resolve to transition to cleaner energy. Germany has dipped back into heavy-polluting coal markets to ensure it has enough power for the cold winter ahead.

Efforts are under way at the COP27 summit to keep attention on methane, a more intense but shorter-lasting greenhouse gas than carbon emissions.

On Friday, the Biden administration detailed what it calls a “super-emitter response program” that would require oil and natural-gas

NG00,

operators to respond to credible third-party reports of high-volume methane leaks.

With an updated methane initiative, proposed Environmental Protection Agency rules first floated last year now target all drilling sites, including smaller wells.

The EPA estimates that in 2030, the proposal would reduce methane from covered fossil-fuel sources by 87% from 2005 levels.

Related: Jeff Bezos helping fund U.N. effort to tag and alert methane emitters with data from space

The U.S. government also released a new draft report this year about how climate change is affecting America. The report determined that over the past 50 years, the U.S. has warmed 68% faster than the planet as a whole.

Since 1970, the continental U.S. has experienced 2.5 degrees Fahrenheit of warming, well above the average for the planet, according to a draft of the National Climate Assessment, which is the U.S. government’s definitive report on the effects of climate change and represents a range of federal agencies.

The effects of human-caused climate change on the United States “are already far-reaching and worsening,” the draft report says, but every added amount of warming that can be avoided or delayed will reduce harmful effects.

The Associated Press contributed.

[ad_2]

[ad_1]

Sam Bankman-Fried, co-founder at crypto exchange FTX, tweeted Friday that he was “shocked to see things unravel the way they did,” after he quit as chief executive and the company and its related entities filed for bankruptcy.

The bankruptcy “doesn’t necessarily have to mean the end for the companies or their ability to provide value and funds to their customers chiefly, and can be consistent with other routes,” Bankman-Fried tweeted Friday.

Bankman-Fried has seen his net worth plunge to almost zero from $16 billion in less than a week, according to Bloomberg Billionaires index.

FTX was once the third largest cryptocurrency exchange by trading volume. Bitcoin

BTCUSD,

fell 3.4% Friday to around $16,838, hovering at around a two-year low, according to the CoinDesk data.

A representative at FTX didn’t respond to a request seeking comment.

[ad_2]

[ad_1]

FTX, the crypto exchange, filed for voluntary Chapter 11 bankruptcy in a Delaware court on Friday, and chief executive Sam Bankman-Fried has resigned.

Following the news, here is how prices are doing for major cryptocurrencies, according to CoinDesk data.

Bitcoin BTCUSD, -4.92% The price for Bitcoin was around $19,350 before the announcement of the potential FTX/Binance deal on Tuesday. The price jumped to $20,590 in less than an hour after the announcement. But dropped to a 2-year low of $17,484. Currently, the Bitcoin price is $16,907.19, a change of -5.04% over the past 24 hours.

Ethereum ETHE, -9.66% Currently, the Ethereum price is $1,252.60, a change of -6.60% over the last 24 hours. The price of Ethereum was around $1,438 before the announcement, and peaked at $1,562 under an hour after. Later on Nov 8, the price dropped to $1,289.

FTT: Today the price of FTT, which is the FTX token, is $2.74, down 20.37% in the last 24 hours, according to CoinMarketCap data. At the beginning of the week, on Nov 7, the price was around $22.06.

Solana: Currently, the price is $17.34, a change of 2.91% over the past 24 hours. The price of Solana before the announcement was around $27.69, and peaked at $31.29 shortly after the announcement.

Binance Coin: The Binance Coin price is $285.74, a change of -7.02% over the past 24 hours. The Binance Coin price was around $322 before the announcement that Binance might acquire FTX on Nov 8.

[ad_2]

[ad_1]

Crypto lending platform BlockFi announced it was halting withdrawals Thursday night in the wake of the collapse of crypto exchange FTX.

“We are shocked and dismayed by the news regarding FTX and Alameda,” BlockFi said in a tweet. “We, like the rest of the world, found out about this situation through Twitter.”

BlockFi said that due to the “lack of clarity” regarding FTX and Alameda, “we are not able to operate business as usual,” and that until there is “further clarity, we are limiting platform activity, including pausing client withdrawals.”

The company asked clients not to deposit into BlockFi Wallet or Interest Accounts at this time, and said it will share more specifics “as soon as possible,” though it warned it likely would communicate “less frequently” than what its clients and stakeholders are used to.

In June, BlockFi received a $250 million bailout from FTX to help keep it afloat.

FTX, once valued at $32 billion, collapsed this week under a liquidity crisis, and faces a shortfall of up to $8 billion, according to several media reports. Without a cash injection, the company might plunge into bankruptcy, according to a Bloomberg report.

Also see: ‘Bedazzled by money’: Democratic ties to Sam Bankman-Fried under scrutiny after FTX collapse

FTX founder and CEO Sam Bankman-Fried reportedly extended about $10 billion in loans to its affiliated trading firm Alameda Research — amounting to about half of FTX’s customer assets of $16 billion, according to the Wall Street Journal.

“I fucked up, and should have done better,” Bankman-Fried said in a tweet Thursday, saying he had, among other things, misread the use of margin on the platform.

More: The $26 billion rise and fall of FTX crypto king Sam Bankman-Fried

Late Thursday, it was revealed that Alameda appeared to have shorted the stablecoin Tether, according to blockchain data.

The FTX fiasco has spread fear of a “contagion” across the broader crypto industry, and sent the price of bitcoin

BTCUSD,

at one point to its lowest level since November 2020.

[ad_2]

[ad_1]

A federal judge in Texas on Thursday struck down the Biden administration’s student-debt forgiveness plan, imperiling a key administration priority that would have canceled up to $20,000 in student loans for tens of millions of borrowers.

The Biden administration’s plan is an “unconstitutional exercise of Congress’s legislative power” that also failed to go through normal regulatory processes, Judge Mark Pittman of the Northern District of Texas wrote in a 26-page opinion.

“No one can plausibly deny that it is either one of the largest delegations of legislative power to the executive branch, or one of the largest exercises of legislative power without congressional authority in the history of the United States,” Pittman, an appointee of former President Donald Trump wrote.

The Biden administration can appeal the verdict. The White House didn’t immediately respond to a request for comment.

Two borrowers—supported by the Job Creators Network, a conservative group—were granted standing in the case because they didn’t qualify for the program. One plaintiff had private student loans that weren’t eligible for forgiveness, while the other wasn’t the recipient of a Pell Grant, meaning he didn’t qualify for an extra $10,000 in forgiveness for which only Pell Grant recipients are eligible. The court ruled that they had been deprived of their right to voice their disagreement with the contours of the program through the usual regulatory process.

An expanded version of this report appears on WSJ.com.

Also popular on WSJ.com:

FTX tapped into customer accounts to fund risky bets, setting up its downfall.

Frustrated Republicans try to explain lack of midterm ‘red wave.’

[ad_2]

[ad_1]

Just six months ago, CEOs, celebs and world leaders like Bill Clinton and Tony Blair flocked to him, gathering at a Davos-like conference he hosted in the Bahamas where he lives as one of the most outspoken evangelists for the power of the blockchain.

Fast forward to Sunday and Bankman-Fried’s crypto empire came crashing down, the victim of an old-fashioned bank run that quickly exposed the weaknesses of the new finance system he had championed.

Almost overnight, Bankman-Fried’s cryptocurrency exchange, FTX, had gone from being valued at $32 billion to worthless, leaving scores of investors scrambling to get their deposits back and triggering probes in the U.S. by the Securities and Exchange Commission, the Commodities Futures Trading Commission and the Department of Justice, according to reports.

On Thursday, the 30-year-old Bankman-Fried took to Twitter to level with his clients.

“I fucked up, and should have done better,” he wrote.

It took less than five years for Bankman-Fried to build a personal fortune that was estimated at its highest point to be more than $26 billion, making him among the richest people in the world.

His schlubby, boyish appearance — ill-fitting t-shirts, gym shorts and a mop of curly hair — made him look more like a college student ripping bong hits in the basement of a frat house than a finance guru, but fit nicely with the anti-establishment ethos that appealed to crypto enthusiasts.

The son of law professors at Stanford University, Bankman-Fried was a wunderkind from an early age. He studied physics and mathematics at the Massachusetts Institute of Technology.

After a stint as an ETF trader for Jane Street Capital, a highly respected Wall Street firm that is known for attracting genius quantitative traders, Bankman-Fried became interested in the concept of effective altruism, a philosophy that focuses on using reason and evidence to find solutions that benefit the most people possible. In 2017, he launched Alameda Research, a quantitative trading firm focused on digital currencies.

Over the next year, he began building his fortune through arbitrage trading of Bitcoin

BTCUSD,

between exchanges in the U.S. and Japan, where prices were often slightly higher. In 2019, Bankman-Fried launched the crypto exchange FTX.

The timing was fortuitous: as the COVID-19 pandemic spread across the globe the following year, interest in cryptocurrencies among people exploded. FTX took off and brought in the big-name celebrity endorsers and partners, like professional athletes Tom Brady and Steph Curry.

Bankman-Fried soon found himself feted by some of the biggest institutions in finance, attracting investment from the biggest names on Wall Street and beyond like Softbank

9984,

Group, Sequoia Capital, Blackrock

BLK,

Tiger Global Management and Thoma Bravo. He even raised money from billionaire hedge fund legends Paul Tudor Jones and Israel Englander.

Soon, FTX was among the biggest players in the industry.

Despite his ballooning wealth, Bankman-Fried maintained the appearance and lifestyle of a teenage gamer. He moved to the Bahamas, where he reportedly lived in a penthouse apartment with 10 roommates.

On Zoom calls, he would often play video games while talking — his favorite game being League of Legends. Profiles of him often noted that he kept a bean bag just feet from his desk to sleep on.

What set Bankman-Fried apart from other crypto tycoons, was his professed interest in working with regulators to create a more robust framework around the nascent industry and treat it more like a traditional finance network.

To that end, Bankman-Fried appeared before Congress to try to explain to skeptical U.S. lawmakers how the crypto industry worked. He also said he welcomed regulation, not always a popular position in the crypto world.

“FTX believes [government agencies] could play an even more prominent role in the digital-asset ecosystem and bring greater investor protections by closing some regulatory gaps,” he said before a senate panel in February. “FTX believes that such efforts would combine the best aspects of traditional finance and digital-asset innovations.”

Bankman-Fried even put his great wealth to play in politics, becoming a major campaign donor for the Democratic party. In 2020, he was one of President Joe Biden’s largest single donors and spent nearly $40 million on political campaigns this year for the midterm elections, according to campaign filings.

As cryptocurrencies have experienced significant declines in prices this year, triggering the collapse of several operations, Bankman-Fried arose as a savior, buying up several failing partners as positioning himself as a kind of Robin Hood for the industry.

For as fast a rise to the top of the world that Bankman-Fried enjoyed, the fall was just as rapid.

On Sunday, Changpeng Zhao, the CEO of FTX’s competitor, Binance, and an archrival of Bankman-Fried’s, announced on Twitter that his firm, the world’s biggest cryptocurrency exchange, was liquidating its sizable holdings of FTT, the coin issued by FTX, “due to recent revelations that have come to light.”

Bankman-Fried accused Zhao of spreading false rumors. But the damage was done.

Binance’s move triggered a massive selloff with customers seeking to redeem some $5 billion in deposits. FTX didn’t have it and redemptions froze up.

On Tuesday, Bankman-Fried announced that FTX had reached a tentative agreement to be acquired by Binance, due to a “significant liquidity crunch.” The turmoil set off broad declines among several of the most popular cryptocurrencies and even spilled into the world of traditional finance, sending markets tumbling.

The next day, the chaos increased, with reports that FTX and Bankman-Fried were under investigation by several U.S. agencies. By the end of the day, Binance said it was walking away from the deal because due diligence had revealed that “the issues are beyond our control or ability to help.”

Binance’s deal seemed like the only thing preventing FTX from potentially collapsing. “At some point I might have more to say about a particular sparring partner,” Bankman-Fried tweeted on Thursday. “For now, all I’ll say is: well played; you won.”

Also on Thursday, the Wall Street Journal reported that Bankman-Fried had been using some customer deposits to fund risky bets by his Alameda Research firm, setting FTX up for collapse.

With the Binance lifeline gone and with few options available, Bankman-Fried told investors he needed $8 billion or more to plug the hole in FTX’s books, according to reports.

On Twitter, Bankman-Fried said he would focus all his efforts on making sure depositors got their money back. He also tried to explain FTX’s collapse, saying “a poor internal labeling of bank-related accounts meant that I was substantially off on my sense of users’ margin. I thought it was way lower.”

Said Bankman-Fried: “My #1 priority–by far–is doing right by users,” he wrote. “Right now, we’re spending the week doing everything we can to raise liquidity. I can’t make any promises about that.”

[ad_2]

[ad_1]

The head of the World Health Organization said a close to 90% decline in COVID deaths globally compared to nine months ago is “cause for optimism,” but urged leaders to remain vigilant as new variants continue to emerge.

Tedros Adhanom Ghebreyesus told reporters on Wednesday that there were just 9,400 COVID deaths last week, compared with more than 75,000 in February, the Associated Press reported.

“Almost 10,000 deaths a week is 10,000 too many for a disease that can be prevented and treated,” he said.

Testing and sequencing rates remain low globally, vaccination gaps between rich and poor countries are still wide, and new variants continue to proliferate.

In its weekly epidemiological update, the agency said the global tally of cases fell 15% in the week through Nov. 6 from the previous week with over 2.1 million new cases counted.

The highest number of new cases was reported from Japan, at 401,693, followed by Korea at 299,440 and the U.S. at 266,104. The agency again cautioned that the numbers may be undercounted, given the changes in testing strategies and overall surveillance in many countries, including the U.S.

As for new variants, the update found BA.5, an omicron subvariant, remained dominant globally, accounting for 74.5% of sequences submitted to a central database. But newer ones, including BQ.1 and XBB, are on the rise.

BQ.1 sequences rose to 13.4% of the total from 9.4% a week ago. XBB rose to 2.0% from 1.1%. The WHO is still closely monitoring newer sublineages but called on countries to also track them closely.

In the U.S., known cases of COVID are climbing again for the first time in a few months. The daily average for new cases stood at 40,189 on Wednesday, according to a New York Times tracker, up 7% versus two weeks ago.

Cases are rising extremely sharply in some states, led by Nevada, where they are up 96% from two weeks ago. New Mexico’s case tally has climbed 64% from two weeks ago and Utah is up 61%. Overall, cases are rising in 32 states and are flat in Delaware. They are also rising in Washington, D.C., Guam, Puerto Rico and the U.S. Virgin Islands.

The daily average for hospitalizations was up 3% at 28,003, while the daily average for deaths is down 13% to 316.

Coronavirus Update: MarketWatch’s daily roundup has been curating and reporting all the latest developments every weekday since the coronavirus pandemic began

Other COVID-19 news you should know about:

• China’s new top leadership body reaffirmed Beijing’s “dynamic-zero” COVID-19 policy on Thursday, as case numbers rose and authorities in the city of Guangzhou urged residents to work from home but stopped short of a citywide lockdown, Reuters reported. In its first meeting since being formed last month after the ruling Communist Party’s twice-a-decade congress, the Politburo Standing Committee said China’s epidemic prevention measures must not be relaxed, according to state media.

• AstraZeneca PLC on Thursday lifted its guidance for the full year after reporting a swing to net profit and higher sales for the third quarter of the year, which both beat consensus expectations, Dow Jones Newswires reported. The Anglo-Swedish drug company dropped its submission for U.S. regulatory approval for its COVID vaccine, saying it has decided to focus instead on areas with greater unmet medical needs. The vaccine was initially approved in the U.K. and Europe about two years ago. CEO Pascal Soriot said the submission in the U.S. was becoming “very complicated and very large,” as it had to gather data from around the world.

• Pfizer

PFE,

and German partner BioNTech

BNTX,

said Thursday that their booster dose of the omicron BA.4/BA.5-adapted bivalent COVID vaccine for 5-to-11 year olds was recommended for marketing authorization in the European Union. The EU will review the recommendation from the European Medicines Agency (EMA) Committee for Medicinal Products for Human Use (CHMP), and is expected to make a decision “soon.” The companies’ bivalent booster is already authorized in the EU for people at least 12 years old.

Here’s what the numbers say:

The global tally of confirmed cases of COVID-19 topped 633.9 million on Monday, while the death toll rose above 6.60 million, according to data aggregated by Johns Hopkins University.

The U.S. leads the world with 97.9 million cases and 1,073,934 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 227.3 million people living in the U.S., equal to 68.5% of the total population, are fully vaccinated, meaning they have had their primary shots.

So far, just 26.3 million Americans have had the updated COVID booster that targets the original virus and the omicron variants, equal to 8.4% of the overall population.

[ad_2]

[ad_1]

Binance, the world’s largest crypto exchange, is abandoning its proposed acquisition of the non-U.S. assets of rival FTX, amid the latter’s liquidity crunch.

“As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com,” according to a tweet by Binance’s official account Wednesday.

“Our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help,” Binance wrote.

Executives at Binance have found a gap, likely in billions and possibly more than $6 billion, between the liabilities and assets of FTX, Bloomberg reported Wednesday, citing an anonymous source familiar with the matter.

Representatives at Binance and FTX didn’t immediately respond to a request seeking comments.

On Tuesday, Changpeng Zhao, Binance’s chief executive, said the exchange had signed a letter of intent to acquire FTX.com, a separate entity from FTX.US, after FTX “asked for help.”

Read: Bitcoin falls to two-year low after crypto exchange Binance proposed to buy rival FTX

Investors are worried about any contagion, as concerns over FTX’s solvency spilled over to the already battered crypto market. BitcoinBTCUSD plunged Wednesday to as low as $16,863, the lowest level since November 2020.

FTX is the third largest crypto exchange by trading volume, according to CoinMarketCap.

Also read: Crypto billionaire Sam Bankman-Fried’s net worth could shrink by over $13 billion

See also: FTX problems mean big headaches for its private equity investors

[ad_2]

[ad_1]

The southern Chinese manufacturing hub of Guangzhou is the latest to see lockdowns amid a surge in COVID-19 cases, as the government presses ahead with the strict zero-COVID policy that has frustrated citizens.

The latest lockdowns have further disrupted global supply chains and sharply slowed growth in the world’s second-largest economy, as the Associated Press reported.

Residents in districts encompassing almost 5 million people have been ordered to stay home at least through Sunday, with one member of each family allowed out once a day to purchase necessities, local authorities said Wednesday.

The order came after the densely populated city of 13 million reported more than 2,500 new cases over the previous 24 hours.

China has retained its strict zero-COVID policy despite relatively low case numbers and no new deaths. The country’s borders remain largely closed, and internal travel and trade is complicated by ever-changing quarantine regulations.

Apple

AAPL,

and iPhone manufacturer Foxconn

2317,

said over the weekend that restrictions are crimping production and will delay shipments of the high-end iPhone 14.

For more, read: All eyes on China as Apple and Foxconn outline zero-COVID issues. Meanwhile, cases are rising again in the U.S.

In the U.S., known cases of COVID are climbing again for the first time in a few months. The daily average for new cases stood at 39,578 on Tuesday, according to a New York Times tracker, up 5% versus two weeks ago.

As always, the increase in cases is not uniform across the nation. Some states are seeing sharp spikes, led by Nevada, where cases are up 96% from two weeks ago. Tennessee is second with cases up 69%, followed by Louisiana with cases up 68%, New Mexico, where they are up 62%, and Utah, where they have climbed 61%.

Cases are up by a double-digit percentage in 22 states.

The daily average for hospitalizations was up 3% to 27,713, while the daily average for deaths was down 14% to 308.

Coronavirus Update: MarketWatch’s daily roundup has been curating and reporting all the latest developments every weekday since the coronavirus pandemic began

Other COVID-19 news you should know about:

• Novavax Inc.

NVAX,

on Tuesday tweaked its full-year sales outlook to the low end of its expected range and reported a surprise quarterly loss, but sales for the COVID-19 vaccine maker were far better than expected. The company reported a net loss of $168.6 million, or $2.15 a share, compared with a loss of $322.4 million, or $4.31 a share, in the same quarter a year ago. Sales were $735 million, compared with $178.8 million in the prior-year quarter. Analysts polled by FactSet expected Novavax to earn $1.57 a share on revenue of $586 million.

• A Food and Drug Administration advisory committee said this week that Veru Inc.’s

VERU,

COVID treatment Sabizabulin demonstrated a clear clinical benefit with a favorable benefit-to-risk profile. Veru is seeking emergency-use authorization for treatment of hospitalized COVID-19 patients at high risk for acute respiratory distress syndrome.

• A Massachusetts man who admitted to lying on his application for federal coronavirus business stimulus funds and using some of the $400,000 he received to pay his mortgage has been sentenced to 15 months in prison, federal prosecutors said, as the AP reported. In addition to the time behind bars, Adley Bernadin, 44, of Stoughton, was sentenced last week to three years of supervised release and ordered to forfeit more than $280,000, according to a statement from the U.S. attorney’s office.

Here’s what the numbers say:

The global tally of confirmed cases of COVID-19 topped 633.5 million on Monday, while the death toll rose above 6.60 million, according to data aggregated by Johns Hopkins University.

The U.S. leads the world with 97.8 million cases and 1,072,943 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 227.3 million people living in the U.S., equal to 68.5% of the total population, are fully vaccinated, meaning they have had their primary shots.

So far, just 26.3 million Americans have had the updated COVID booster that targets the original virus and the omicron variants, equal to 8.4% of the overall population.

[ad_2]

[ad_1]

[ad_1]

Walt Disney Co. wrapped up its fiscal year with record sales and its best revenue growth in more than 25 years, but executives predicted much slower sales increases in the year ahead while missing expectations for fourth-quarter earnings and sales, sending shares down more than 10% Tuesday afternoon.

Disney

DIS,

reported fiscal fourth-quarter net income of $162 million, or 9 cents a share, on sales of $20.15 billion, up from $18.53 billion a year ago but more than $1 billion short of expectations. After adjusting for amortization and certain investment changes, Disney reported earnings of 30 cents a share, down from 37 cents a share a year ago.

Analysts surveyed by FactSet had on average expected adjusted earnings of 56 cents a share on revenue of $21.27 billion.

Disney executives blamed a number of factors for the revenue miss, including lower content sales because they had fewer theatrical films on the calendar; underperformance of the parks and media divisions; and seasonality of its fourth quarter, which tends to be the lowest for margins.

For the full fiscal year, Disney reported record sales of $82.72 billion, more than 22% higher than the previous year, the strongest annual sales growth for Disney since the 1996 fiscal year, according to FactSet records. Profit grew to $3.19 billion from $2.02 billion the year before, but is nowhere close to prepandemic Disney earnings, which hit eight figures in both 2019 and 2018.

In a conference call Tuesday afternoon, though, Chief Financial Officer Christine McCarthy suggested that revenue and profit growth will slow to single digits on a percentage basis in the current fiscal year, missing Wall Street’s expectations. Analysts’ average revenue projection for Disney in the new fiscal year suggested revenue growth of about 13.9% and operating-income growth of roughly 17.4%, according to FactSet.

“Putting this all together, assuming we do not see a meaningful shift in the macroeconomic climate, we currently expect total company fiscal 2023 revenue and segment operating income to both grow at a high-single-digit percentage rate versus fiscal 2022,” McCarthy said.

Disney shares initially fell more than 6% in after-hours trading following the release of the results, but plunged anew to a decline of more than 10% after closing with a 0.5% decline at $99.94.

Disney has been helped by the return of visitors to its theme parks in the third year of the COVID-19 pandemic, as well as a recovering movie business. The main attraction for investors, though, has been growing Disney’s streaming efforts — total streaming subscribers topped Netflix Inc.’s

NFLX,

subscriber total last quarter, and grew its lead in Tuesday’s report, with Disney adding 12.1 million net new subscribers, while analysts on average expected 10.4 million.

Disney’s streaming growth has hampered its profitability, however, as the company spends to add content to its streaming services in order to compete with Netflix. Those days appear to be coming to an end as Disney struggles with profit.

“The rapid growth of Disney+ in just three years since launch is a direct result of our strategic decision to invest heavily in creating incredible content and rolling out the service internationally, and we expect our DTC operating losses to narrow going forward and that Disney+ will still achieve profitability in fiscal 2024, assuming we do not see a meaningful shift in the economic climate,” Disney Chief Executive Bob Chapek said in a statement announcing the results. “By realigning our costs and realizing the benefits of price increases and our Disney+ ad-supported tier coming December 8, we believe we will be on the path to achieve a profitable streaming business that will drive continued growth and generate shareholder value long into the future.”

Disney’s largest business segment, media and entertainment distribution, reported sales of $12.73 billion in the quarter, down from $13.08 billion a year ago; analysts on average predicted $13.86 billion. Direct-to-consumer sales, which includes streaming services as well as some international products, hauled in $4.9 billion, compared with analysts’ forecast of $5.4 billion on average.

The trajectory of Disney’ meteoric rise as video-streaming market leader is likely to continue once its advertising-supported service debuts in the U.S. next month, according to Wall Street analysts, after Netflix launched its rival offering on Nov. 3. Disney has leaned heavily on its stable of mega-franchises such as “Star Wars” and the Marvel Cinematic Universe to outpace Netflix Inc.

NFLX,

Apple Inc.

AAPL,

Comcast Corp.

CMCSA,

Warner Bros. Discover Inc.

WBD,

Amazon.com Inc.

AMZN,

Paramount Global

PARA,

and others.

Read more: Disney overtook Netflix as the streaming leader, and is expected to widen its lead

Disney’s television networks generated sales of $6.34 billion, while analysts’ average estimates called for $6.64 billion. Content sales and licensing, a category that includes Disney’s film business, registered revenue of $1.74 billion vs. analysts’ expectations of $2.08 billion.

The company’s signature theme parks and product sales business increased to $7.43 billion in revenue from $5.45 billion a year ago. The average analyst estimate was $7.46 billion.

Shares of Disney are down 35.5% this year, while the broader S&P 500 index

SPX,

has dropped 20%.

[ad_2]

[ad_1]

China’s strict zero-COVID policy was making headlines Monday after Apple and iPhone manufacturer Foxconn said over the weekend that restrictions are crimping production and will delay shipments of the high-end iPhone 14.

“We continue to see strong demand for iPhone 14 Pro and iPhone 14 Pro Max models,” Apple

AAPL,

announced in a Sunday evening press release. “However, we now expect lower iPhone 14 Pro and iPhone 14 Pro Max shipments than we previously anticipated and customers will experience longer wait times to receive their new products.”

Also read: Will Apple’s latest production issues destroy demand?

Foxconn, meanwhile, which trades as Hon Hai Precision Industry Co.

2317,

lowered its fourth-quarter guidance and said anti-COVID measures were affecting some of its operations in Zhengzhou, China, as Dow Jones Newswires reported.

Foxconn said that the Henan provincial government had made it clear that it would fully support the company. Foxconn’s most advanced iPhone plant, located in the provincial capital of Zhengzhou, has been battling a COVID outbreak.

Foxconn said it is working with the government to halt the outbreak and resume production at full capacity as quickly as possible.

Investors have been closely watching China for signs that its government would start to lift the tough pandemic restrictions that have been in place for almost three years. The Wall Street Journal reported Monday that the country’s leaders are considering steps but have not yet set a timeline.

Chinese officials have become concerned about the costs of their zero-tolerance approach to COVID, which has resulted in lockdowns of cities and whole provinces, crushing business activity and confining hundreds of millions of people to their homes for weeks and sometimes months on end.

But they are weighing those concerns against the potential costs of reopening on public health and on support for the Communist Party. On Saturday, officials from China’s National Health Commission again reaffirmed their commitment to a firm zero-COVID strategy, which they described as essential to “protect people’s lives.”

Still, there are plans in Beijing to further cut the number of days incoming travelers must quarantine in hotels from 10 to seven, followed by three days of home monitoring, the paper reported, citing people involved in the discussions.

And officials have told retail businesses that they intend to reduce the frequency of PCR testing as soon as this month, partly because of the cost.

In the U.S., known cases of COVID and hospitalizations are climbing again for the first time in a few months.

The daily average for new cases stood at 39,954 on Sunday, according to a New York Times tracker, up 6% compared with two weeks ago. But cases are sharply higher in several states, led by Nevada, where they are up 96% from two weeks ago, followed by Tennessee, where they are up 69%; Louisiana, where they are up 68%; Utah, where they have climbed 61%; and New Mexico, where they are up 56%.

Cases are climbing in 30 states and in Washington, D.C.

The daily average for hospitalizations was up 2% to 27,419, while the daily average for deaths was down 11% to 320.

The Centers for Disease Control and Prevention said the BQ.1 and BQ.1.1 variants accounted for 35.3% of new cases in the week through Nov. 5, up from 27.1% a week ago.

The two variants accounted for 52.3% of all cases in the New York region, which includes New Jersey, Puerto Rico and the Virgin Islands, up from 42.5% the previous week. That was more than the BA.5 omicron subvariant, which accounted for 24.9% of new cases in the New York area in the latest week.

The BA.5 omicron subvariant accounted for 39.2% of all U.S. cases, the data show.

BQ.1 and BQ.1.1 were still lumped in with BA.5 variant data as recently as three weeks ago, because at that time, their numbers were too small to break out. BQ.1 was first identified by researchers in early September and has been found in the U.K. and Germany, among other places.

Coronavirus Update: MarketWatch’s daily roundup has been curating and reporting all the latest developments every weekday since the coronavirus pandemic began

Other COVID-19 news you should know about:

• BioNTEch SE

BNTX,

the German biotech that has partnered with Pfizer

PFE,

on a COVID vaccine, posted earnings early Monday, showing a roughly 50% drop in profit that sent its stock lower, despite beating consensus estimates. The Mainz-based company said it had invoiced about 300 million doses of its bivalent vaccine, which targets the omicron variant as well as the original virus. The company chalked up €564.5 million ($563.9 million) in direct COVID vaccine sales in the quarter, down from €1.351 billion a year ago. BioNTech raised the lower end of its full-year COVID vaccine revenue range to €16 billion to €17 billion, from a previous €13 billion to €17 billion.

• Thousands of runners took to the streets of the Chinese capital on Sunday for the return of Beijing’s annual marathon after a two-year hiatus, the Associated Press reported. However, the good news was offset by anger about another death related to COVID restrictions, this time of a 55-year-old woman in a sealed building. An investigation report released Sunday in Hohhot, the capital of China’s Inner Mongolia region, blamed property management and community staff for not acting quickly enough to prevent the death of the woman after being told she had suicidal tendencies.

• The U.S. flu season is off to an unusually fast start, contributing to an autumn mix of viruses that have patients filling hospitals’ and physicians’ waiting rooms, the AP reported separately. Reports of flu are already high in 17 states, and the hospitalization rate hasn’t been this high this early since the 2009 swine flu pandemic, according to the Centers for Disease Control and Prevention. So far, there have been an estimated 730 flu deaths, including at least two children. The winter flu season usually ramps up in December or January.

Here’s what the numbers say:

The global tally of confirmed cases of COVID-19 topped 632.6 million on Monday, while the death toll rose above 6.60 million, according to data aggregated by Johns Hopkins University.

The U.S. leads the world with 97.7 million cases and 1,072,598 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 227.3 million people living in the U.S., equal to 68.5% of the total population, are fully vaccinated, meaning they have had their primary shots.

So far, just 26.3 million Americans have had the updated COVID booster that targets the original virus and the omicron variants, equal to 8.4% of the overall population.

[ad_2]

[ad_1]

By Michael Susin

GSK PLC said Monday that its Dreamm-3 Phase 3 study in patients with relapsed or refractory multiple myeloma didn’t meet its primary endpoint of progression-free survival.

The pharmaceutical giant said that the study compared its monotherapy Blenrep versus pomalidomide in combination with low dose dexamethasone and observed median progression-free survival was longer for Blenrep.

“These trials are designed to demonstrate the benefit of Blenrep in combination treatment with novel therapies and standard-of-care treatments in earlier lines of therapy and dosing optimization to maintain efficacy while reducing corneal events,” it added.

The company said additional trials will continue and further data from the studies are anticipated in the first half of 2023.

Write to Michael Susin at michael.susin@wsj.com

[ad_2]