Walt Disney Co.’s ESPN, Fox Corp. and Warner Bros. Discovery Inc. are teaming to create a joint sports streaming service.

The as-yet unnamed service, which could be available as early as the fall and offer a sort of Hulu model for sports, comes amid an explosion in sports-streaming rights and audiences.

The service would essentially be a skinny bundle of the companies’ linear channels, including ESPN, ESPN2, ESPNU, SECN, ACCN, ESPNEWS, ABC, Fox, FS1, FS2, BTN, TNT, TBS, truTV, as well as the ESPN+ streaming service.

“The launch of this new streaming sports service is a significant moment for Disney DIS, +2.73%

and ESPN, a major win for sports fans, and an important step forward for the media business,” Disney Chief Executive Bob Iger said in a statement late Tuesday. “This means the full suite of ESPN channels will be available to consumers alongside the sports programming of other industry leaders as part of a differentiated sports-centric service.”

Added Warner Bros. WBD,

CEO David Zaslav: “This new sports service exemplifies our ability as an industry to drive innovation and provide consumers with more choice, enjoyment and value and we’re thrilled to deliver it to sports fans.”

Each company will own one-third of the platform, according to Disney, in a deal reminiscent of the original Hulu, which started off as a joint venture between ABC, Fox and NBCUniversal.

The service will have a new brand with an independent management team, and will be available to bundle with Disney+, Hulu and Max subscriptions.

“We’re pumped,” Fox FOX, +0.55%

CEO Lachlan Murdoch said. “We believe the service will provide passionate fans outside of the traditional bundle an array of amazing sports content all in one place.”

More details, including pricing, will be announced later.

Prominently missing from the deal are Comcast Corp. CMCSA, -1.00%,

which owns NBCUniversal and its sports lineup that includes NFL football and the Olympics, and Paramount Global PARA, -0.21%,

which owns CBS — which carries the NFL and college football, among other sports.

The new service will showcase thousands of high-profile sporting events and include all four major sports leagues — the NFL, NBA, MLB and NHL — as well as college football and basketball, golf, tennis, cycling, soccer and UFC.

Shares of Disney were down 1% in extended trading Tuesday, while Fox shares jumped 6% and WBD gained 3%.

Small businesses in sectors like software and manufacturing are panicking over the expiration of a critical tax deduction that they say could lead to mass layoffs and business closures, unless Congress acts quickly to amend the law.

“This is a life-and-death scenario for small software companies,” Michelle Hansen, co-founder of the geocoding company Geocodio, told MarketWatch.

The tax change that Hansen and other software executives are taking issue with was signed into law by President Trump in 2017, as part of a larger tax overhaul that slashed the top corporate tax rate from 35% to 21%.

But in order to satisfy Senate budget rules and pass the law with only Republican votes, the bill could not increase the budget deficit over a 10-year window.

So lawmakers included a provision that, beginning in 2022, drastically reduced how much research-and-development spending a business could deduct from their annual revenue to determine taxable income.

The change penalizes certain industries like software and information technology — where engineer salaries are often classified as R&D expenses — as well as manufacturing and pharmaceuticals IHE.

IntervalZero CEO Jeff Hibbard, whose Massachusetts-based company designs and sells software for installation on precision machines like semiconductor manufacturers, told MarketWatch that he has had to tap into company savings for the past several years in order to avoid laying off engineers.

He said that his firm brings in about $9 million in revenue annually with expenses of $8 million — but 60% of those expenses come in the form of engineer salaries, which can only be deducted from taxable income over a five-year period because the IRS treats it as R&D.

He said that after taxes consumed all his profits in 2022, he had to pay an additional $800,000 to Uncle Sam, and an additional $600,000 for the 2023 tax year.

“We’ve had to do a hiring freeze and postpone projects” in a cutthroat industry where technology progresses rapidly, Hibbard said. “We’ve been in existence for 15 years. For the first 14, we always hired additional people. Now we have a hiring and salary freeze.”

The House of Representatives voted last week 357-70 to restore full expensing for R&D as part of a $79 billion tax package that boosted the child tax credit and extended other business tax breaks.

The bill now heads to the Senate, which already has its hands full debating immigration and national-security issues, and analysts say election-year politics could thwart its passage in 2024.

Henrietta Treyz, director of economic-policy research at Veda Partners, gave just a 10% chance of the bill passing the Senate in a recent note to clients.

“This year’s effort to pass a tax package has been more robust than the effort we saw in 2022 and 2023,” she wrote. Treyz added, however, that “the competing need to pass border reform and Ukraine/Israel aid, and general dysfunction in Washington keep us pessimistic that we’ll see a bipartisan economic-stimulus package come out of Congress this year.”

On top of Republicans not wanting to give President Joe Biden a victory that would provide tax relief for businesses and families, Senate Republicans could decide to drag their feet on the bill in the hope that they’ll retake the chamber next year and can play a bigger role in the process, according to Owen Tedford, policy analyst at Beacon Policy Advisors.

“The critical member to watch is Senator Mike Crapo [of Idaho], the top Republican on the Senate Finance Committee,” Tedford wrote. “Crapo has not outright opposed the bill but has raised policy concerns and has expressed a desire to have a chance to amend it.”

Political considerations may be dictating the bill’s fate in Washington — but some business owners fear they don’t have the wherewithal to wait until next year for the problem to be fixed.

Benjamin Bengfort, co-founder and CEO of Iowa-based software firm Rotational Labs, told MarketWatch that he had to lay off workers last year after his 2022 tax bill rose by 438%.

He noted that even demand for his products has taken a hit because of the change in the law, because his services can count as an R&D expense for his customers, too.

“So it is [between] a rock and a hard place for us, no matter how you look at it,” Bengfort said. “This is an existential threat for software engineering companies.”

McDonald’s Corp.’s stock fell 1.3% in premarket trading on Monday after the fast-food giant missed Wall Street analysts’ estimates for revenue and same-store sales, while citing an impact from war in the Middle East.

The global fast-food giant said it expects “macro challenges” to persist in 2024.

McDonald’s MCD, -0.35%

said its fourth-quarter net income rose by 7% to $2.04 billion, or $2.80 a share, from $1.9 billion, or $2.59 a share, in the year-ago quarter.

McDonald’s said the latest quarter’s results included 15 cents a share in one-time charges.

Breaking those charges out, McDonald’s would have earned $1.95 a share. Analysts expected McDonalds to earn $1.83 a share, according to FactSet data.

Revenue rose 8% to $6.41 billion, short of the FactSet consensus estimate of $6.45 billion.

Fourth-quarter global comparable-store sales increased by 3.4%, including a 4.3% rise in the U.S.. Analysts expected same-store sales growth of 4.7%.

McDonald’s said its comparable sales fell in the Middle East as a reflection of war in the region since Oct. 7.

All other same-stores sales rose in international developmental licensed markets.

Total international developmental licensed markets same-store sales rose by 0.7%, well below the result in the previous quarter, which saw a 10.5% increase.

Looking back at the balance of 2023, McDonald’s said its net income rose by 37% to $8.47 billion.

Revenue jumped by 10% in 2023 to $25.49 billion.

Free cash flow for 2023 increased to $7.25 billion from $5.49 billion.

Before Monday’s moves, McDonald’s stock was up by 10.9% in the past year.

While the U.S. stock market has been pricing in a “soft-landing” scenario for the economy, a blowout January jobs report, relatively strong corporate earnings, and Federal Reserve Jerome Powell’s comments during the past week could point to the possibility of “no landing,” where the economy is resilient while inflation stays on target.

Such a scenario could still be positive for U.S. stocks, as long as inflation remains steady, according to Richard Flax, chief investment officer at Moneyfarm. However, if inflation reaccelerates, the Fed may be hesitant to cut its policy interest rate much, which could spell trouble, Flax said in a call.

What the past week tells us

Investors have just gone through the busiest week so far this year for economic data and corporate earnings reports, with stocks ending at or near their record highs.

The Dow Jones Industrial Average DJIA

finished the week with its nineth record close of 2024, according to Dow Jones Market Data. The S&P 500 index SPX

scored its seventh record close this year on Friday, while the Nasdaq Composite COMP

is about 2.7% lower from its peak.

The Fed kept its policy interest rate unchanged in the range of 5.25% to 5.5% at its Wednesday meeting, as expected. However, in the subsequent press conference, Fed Chair Jerome Powell threw cold water on market expectations that the central bank may start cutting its key interest rate in March, and underscored that they want “greater confidence” in disinflation.

Roger Ferguson, former Fed vice chairman, said Powell introduced “a new kind of risk, the risk of no landing.”

In that scenario, inflation will stop falling, while the economy is strong, Ferguson said in an interview with CNBC on Thursday. However, Ferguson said he doesn’t think it is the likely outcome.

Traders were pricing in a 20.5% likelihood on Friday that the Fed will cut its interest rates in its March meeting, according to the CME FedWatch tool and that’s down from over 46% chance a week ago. The likelihood that the Fed will kick off its rate cutting program in May stood at 58.6% on Friday.

The stronger-than-expected January jobs data released on Friday further eliminates the chance of a rate cut in March, said Flax.

The U.S. economy added a whopping 353,000 new jobs in January while economists polled by The Wall Street Journal had forecast a 185,000 increase in new jobs. Hourly wages rose a sharp 0.6% in January, the biggest increase in almost two years.

The past week has also been heavy with earnings reports, as several tech giants including Microsoft MSFT, +1.84%,

Apple AAPL, -0.54%,

Meta META, +20.32%,

and Amazon AMZN, +7.87%

reported their financial results for the fourth quarter of 2023.

Among the 220 S&P 500 companies that have reported their earnings so far, 68% have beaten estimates, with their earnings exceeding the expectation by a median of 7%, analysts at Fundstrat wrote in a Friday note.

While the reported earnings by big tech companies have been “okay,” the guidance was not, said José Torres, senior economist at Interactive Brokers.

What has been driving the tech stocks’ rally since last year was mostly the prospect of sales from artificial intelligence products, but tech companies are not able to monetize the trend yet, Torres said in a phone interview.

Adding to the headwinds is a comeback of concerns around regional banks.

On Thursday, New York Community Bancorp Inc.’s stock triggered the steepest drop in regional-bank stocks since the collapse of Silicon Valley Bank in March 2023. New York Community Bancorp on Wednesday posted a surprise loss and signaled challenges in the commercial real estate sector with troubled loans.

Meanwhile, the Fed’s bank term funding program, which was launched in March last year to bolster the capacity of the banking system, will expire on March 11.

If the Fed could start cutting its key interest rate in March, it would be “sort of like the ambulance that was going to pick regional banks up and save them,” said Torres. “Now the ambulance is coming in May at the earliest, I think that we’re in a particularly risky period from now to May,” Torres said.

What should investors do

Investors should go risk-off before May, according to Torres. “Last year, goods and commodities helped a lot on the disinflationary front. This year for disinflation to continue, we’re going to need services to start contributing to that. Then we’re going to need to see an increase in the unemployment rate,” Torres said.

He said he prefers U.S. Treasurys with a tenor of four years or shorter, as the long-dated ones may be susceptible to risks around the fiscal deficit and government borrowing. For stocks, he prefers the healthcare, utilities, consumer staples and energy sectors, he said.

Keith Buchanan, senior portfolio manager at Globalt Investments, is more optimistic. The slowdown in inflation and the relatively strong economic data and earnings “don’t really paint a picture for a risk-off scenario,” he said. “The setup for risk assets still leans towards the bullish expectation,” Buchanan added.

In the week ahead, investors will be watching the ISM services sector data on Monday, the U.S. trade deficit on Wednesday and weekly initial jobless benefit claims numbers on Thursday. Several Fed officials will speak as well, potentially providing more clues on the possible trajectory of rate cuts.

As the U.S. Federal Reserve’s three-year reign in the headlines potentially comes to an end, an analysis of this year’s market themes can offer valuable insights for predicting trends and ensuring attractive returns in 2024.

Beyond the central bank’s actions, pivotal factors shaping the investment landscape this year include fiscal policies, election outcomes, interest rates and earnings prospects.

Throughout 2023, a prominent theme emerged: that equities are influenced by factors beyond monetary policy. That trend is likely to persist.

A decline in interest rates could significantly increase the relative valuations of equities while simultaneously reducing interest expenses, potentially transforming market dynamics. Contrary to consensus estimates, 2023 brought a more robust earnings rebound, leaving analysts optimistic about 2024.

The 2024 U.S. presidential election, meanwhile, introduces a new element of uncertainty with the potential to cast a shadow over the market during much of the coming year.

Choppy trading, modest earnings growth

Anticipating a choppy first half of the year due to sluggish economic growth, we see a better opportunity for cyclicals and small-cap stocks to rebound in the latter part of the year. As uncertainty around the election and recession fears dissipate, a broad rally that includes previously ignored cyclicals and small-caps should help propel the S&P 500 SPX

higher.

Broader macroeconomic conditions support mid-single-digit growth in earnings per share throughout 2024. Factors such as moderate economic expansion, controlled inflation and stable interest rates are expected to provide a conducive environment for companies, enabling them to sustain and potentially improve their earnings performance. We estimate EPS growth of 6.5%. This projected growth aligns with the broader market sentiment indicating a steady upward trajectory in earnings for the upcoming year, fostering investor confidence and supporting valuation expectations across various sectors.

“ If the economy has not been in recession at the time of the first rate cut but enters one within a year, the Dow enters a bear market.”

When it comes to U.S. stock-market performance around rate cuts, the phase of the economic cycle matters. When there has been no recession, lower rates have juiced the markets, with the Dow Jones Industrial Average DJIA

rallying by an average of 23.8% one year later.

If the economy has not been in recession at the time of the first cut but enters one within a year, the Dow has entered a bear market every time, declining by an average of 4.9% one year later. Our base case is a soft landing, but history shows how critical avoiding recession is for the bull market as the Fed prepares to ease policy.

Big on small-caps

This past year has posed a hurdle for small-cap stocks due to the absence of a driving force. These stocks typically perform better as the economy emerges from a recession. While they are currently undervalued, their earnings growth has been notably lacking. If concerns about a recession diminish, a normal yield curve could serve as a potential catalyst for small-cap stocks.

Growth vs. value

The ongoing outperformance of megacap growth stocks that we saw in 2023 might hinge on their ability to sustain superior earnings growth, validating their current valuations. Defensive sectors in the value category, meanwhile, are notably oversold and might exhibit strong performance, particularly toward the latter part of the first quarter. Should concerns about a recession dissipate, cyclical sectors within the value category could outperform, particularly if broader market conditions turn favorable in the latter half of the year.

Handling uncertainty

The Fed’s enduring influence regarding the prospect of a soft landing in 2024 remains a pivotal point in the market’s focus. Considering the themes of the past year and the multifaceted influences on equities beyond monetary policy, investors are advised to navigate through uncertainties stemming from unintended fiscal shifts, upcoming elections and the impact of fluctuating interest rates. While a potentially choppy start to the year is anticipated, it could create opportunities for cyclical and small-cap stocks later in the year.

Ed Clissold is chief of U.S. strategies at Ned Davis Research.

Mark Zuckerberg delighted Meta shareholders and Wall Street this week with news of the social media giant’s first-ever dividend.

The IRS may also be happy, now that it’s staring at millions in taxes on the Meta stock dividends bound for Zuckerberg’s portfolio.

Zuckerberg, the CEO of Meta Platforms Inc. META, +20.32%,

is poised to make $700 million in dividends yearly. He owns nearly 350 million shares, according to FactSet, and the company will start paying a quarterly dividend of 50 cents a share.

That would yield nearly $167 million in federal taxes yearly, after a qualified-dividend tax of 20% and another 3.8% tax on the investment returns of rich households, two accounting experts said.

California income taxes of 13.3% on the dividends could cost Zuckerberg another $93.1 million, said Andrew Belnap, an accounting professor at the University of Texas at Austin’s McCombs School of Business.

All in, that’s a combined $259.7 million in federal and state taxes annually on the Meta dividends, Belnap estimated.

For context, U.S. taxpayers reported over $285 billion in qualified-dividend income to the IRS though mid-November 2023, according to agency statistics. Nearly 30 million tax returns reported qualified dividends through that time.

Meta said it plans a quarterly cash dividend going forward, with the first such payment in March.

Meta shares soared 20.5% on Friday, ending with a record-high close of $474.99. The Dow Jones Industrial Average DJIA,

S&P 500 SPX

and Nasdaq Composite COMP

all closed higher Friday.

‘Zuck is getting a major break’

Meta announced the dividend payment in its earnings results Thursday, on the same week that Americans began filing their income taxes.

A look at Zuckerberg’s dividends and their tax implications offer a peek at the debate about the varying ways wages and wealth are taxed.

“Zuck is getting a major break,” said Andrew Schmidt, an accounting professor at North Carolina State University’s Poole School of Management who also crunched the numbers for MarketWatch.

Approximately $167 million “seems like a high tax bill,” he said. But if Zuckerberg received the $700 million as a straight salary, Schmidt estimated he’d be looking at a roughly $259 million tax bill on the wages after they were taxed at the top marginal rate of 37%.

For federal and state taxes on the Meta dividends, Zuckerberg would face a combined rate of 37.1%, Belnap noted. “His tax rate on this is actually fairly high,” he said.

The gap in tax rates on income derived from wages and investments “has been a big criticism with U.S. tax policy,” Schmidt said, especially as lawmakers look for ways to come up with more tax revenue.

Regular retail investors enjoy the same preferential rates on capital gains and dividends as the top 1% of taxpayers, Schmidt added. The issue is that those dividends and stock profits are a smaller part of their income while salaries, taxed at higher rates, are a bigger proportion.

Belnap noted that California’s state tax rules don’t provide special treatment to dividends.

Zuckerberg received a $1 base salary in 2022, a figure that hasn’t changed in several years. He is now worth $142 billion, according to the Bloomberg Billionaires Index, making him the fifth-richest person in the world.

Meta did not immediately respond to a request for comment.

Taxes on the Meta dividends will not be something Zuckerberg, or any Meta shareholders big or small, need to deal with until next year’s tax season, Belnap and Schmidt observed.

But as taxpayers amass their 1099-DIV forms on dividend income, IRS figures show that it’s mostly upper-echelon taxpayers reaping the rewards on the preferential rates for qualified dividends.

Households worth at least $1 million accounted for 40% of the approximate $285.3 billion in qualified dividends reported through mid-November, according to agency figures.

For less affluent investors, “it’s usually a nice supplement, but I’d say very few people are living off dividends,” Belnap said.

GOOGL, +0.86%

and become the third-largest U.S. public company upon Friday’s close, after its results were well received by Wall Street and Alphabet’s earlier in the week got panned.

Amazon edged out Alphabet only barely, with a closing market cap of $1.785 trillion compared with $1.777 trillion for Alphabet, according to Dow Jones Market Data.

The e-commerce giant hadn’t been valued above the Google parent company since Sept. 30, 2022, according to Dow Jones Market Data. That was also the last time Amazon was the third-largest by market cap.

Wall Street found plenty to like in Amazon’s latest report, including drastic improvement in operating income, upbeat commentary on the cloud and momentum within the retail business. Meanwhile, Alphabet’s earnings were met with a chillier reception as the company talked up heavy spending plans linked to its artificial-intelligence ambitions.

The very top of the market-cap ranks has changed up as well lately, though admittedly with less of a tie to earnings. Microsoft Corp.’s MSFT, +1.84%

closing valuation surpassed Apple Inc.’s AAPL, -0.54%

on Jan. 12 for the first time since November 2021. While the two traded around the top spot in January, Microsoft has been sitting there since Jan. 25.

There’s a common belief that “overbought” is a technical condition for a stock, but in practice it seems to be more of an ability.

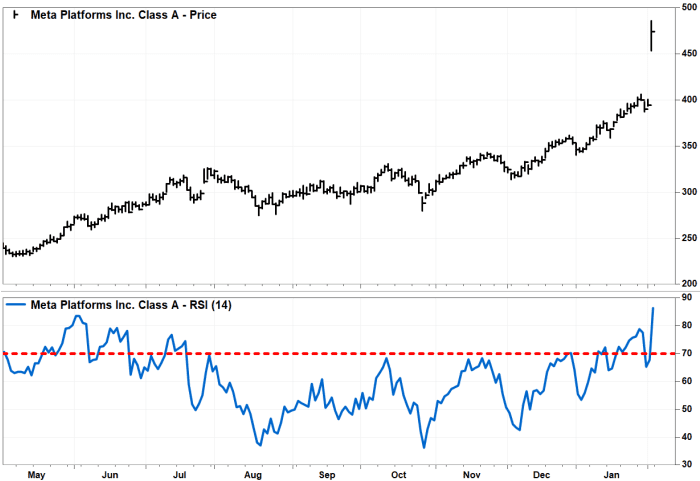

Meta Platforms Inc.’s stock META, +20.32%

soared so much Friday after a blowout earnings report, that some technical readings have reached levels not seen in 11 years.

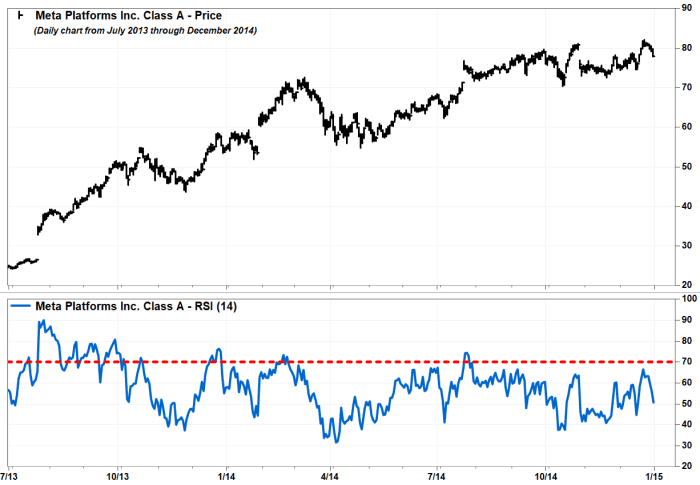

The stock rocketed 20.9% to close at a record $474.99, to book the third-biggest gain since going public in May 2012. The only bigger rallies were 23.3% on Feb. 2, 2023 and 29.6% on July 25, 2013, which were also after earnings reports.

The stock’s Relative Strength Index, which is a momentum indicator that measures the magnitudes of recent gains and losses, climbed to 86.48. That’s the highest level seen since it closed at a record 89.39 on July 30, 2013.

But that shouldn’t scare off Meta bulls.

Many chart watchers believe RSI readings above 70 are signs of “overbought” conditions, which suggests bulls need a breather after running faster and farther than they are used to.

There are also many who believe the ability to become overbought is a sign of underlying strength, since a stock tends to be trending higher when RSI hurdles 70. (Read Constance Brown’s “Technical Analysis for the Trading Professional.”)

For example, the record RSI reading came three days after the record stock-price rally of 29.6% on July 25, 2013. Even though RSI closed at what was then a record of 88.27 after a record price gain on the 25th, the stock continued to rally and become even more overbought.

It was that spike that snapped the stock out of the year-long doldrum that followed the initial public offering, and flipped the long-term narrative on the stock to bullish. (Read “Facebook’s ‘breakaway gap’ is a bullish game changer,” from The Wall Street Journal.)

FactSet, MarketWatch

And while the record RSI readings in July 2013 did lead to a minor short-term pullback, it didn’t stop the stock from embarking on a long-term uptrend, in which RSI made multiple forays above 70.

FactSet, MarketWatch

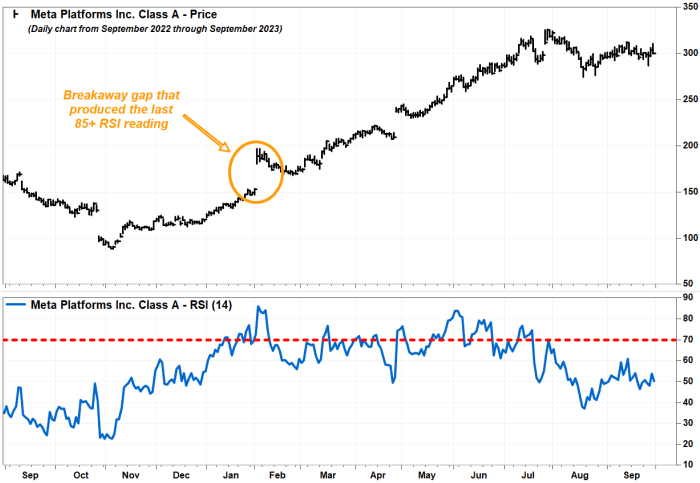

And the last time RSI closed above 85 was Feb. 2, 2023, when it closed at 86.07, also after a blowout earnings report.

And similar to 10 years earlier, that historically high overbought reading helped launch another long-term rally.

FactSet, MarketWatch

So yes, Meta’s stock is now facing historically high overbought conditions. But as many chart watchers like to say, overbought doesn’t mean over.

One thing to consider, however, is that the two prior times RSI spiked above 85 were while the long-term fates of the stock were still in question — the stocks were working on short-term bounces following long-term downtrends.

FactSet, MarketWatch

But Friday’s blast off happened just days after the stock closed at a record high. There was no resistance to hurdle, so rather than a bullish “breakaway gap,” Friday’s jump could be considered more a bullish leap of faith.

Former President Donald Trump on Friday criticized Federal Reserve Chair Jerome Powell and said he’s playing politics with interest-rate policy.

“It looks to me like he’s trying to lower interest rates for the sake of maybe getting people elected,” Trump said, in an interview on the Fox Business Network.

“I think he’s political,” added Trump, the likely 2024 Republican nominee for president.

Asked if he would reappoint Powell to a third four-year term, Trump replied “no.”

Trump said he has a couple of choices in mind to replace Powell, but wouldn’t say who.

Trump said he thinks lowering interest rates would lead to massive inflation. The conflict in the Middle East is likely to lead to “big inflation” from a spike in oil prices, he added.

“Trump said he thinks lowering interest rates would lead to massive inflation. The conflict in the Middle East is likely to lead to “big inflation” from a spike in oil prices, he added.”

Powell “is not going to be able to do anything,” Trump said.

On Wednesday, Powell said he wasn’t giving a potential third term any thought. Powell’s current term expires in early 2026.

Speculation on a third term “is not something I’m focused on,” Powell said.

“We’re focused on doing our jobs. This year is going to be a highly consequential year for the Fed and monetary policy. We’re, all of us, very buckled down, focused on doing our jobs,” Powell said.

Analysts say that the Fed will be criticized by both parties in the election year.

On Sunday, Powell will appear on the CBS News program “60 Minutes” and will likely face more questions about the election.

Earlier this week, top Democrats on the Senate Banking Committee urged the Fed to cut rates quickly, saying they were too high and hurting the housing market.

“Keeping interest rates high will be detrimental to American workers and their families and do little to bring down prices or promote moderate economic growth,” said Sen. Sherrod Brown, a Democrat from Ohio, and the chairman of the Banking Committee, in a letter to Powell prior to Wednesday’s Fed meeting.

At the meeting on Wednesday, the Fed kept its benchmark interest rate unchanged in a range of 5.25%-5.5%.

Asked about the letter from the Democrats on Wednesday, Powell said Congress has given the Fed the job of stable prices. High inflation hurts people at the lower end of the income spectrum, he added.

“It’s what society has asked us to do is to get inflation down. The tools we use to do it are interest rates,” he said.

The Fed has penciled in three rate cuts for 2024. Powell said that a cut at the Fed’s next meeting in March was unlikely. He said the Fed wants to see more good inflation reports so it can have greater confidence that inflation is coming down to the 2% target.

Tesla Inc. will pay $1.5 million to settle a lawsuit filed earlier this week by 25 California counties accusing the electric-vehicle maker of mishandling hazardous waste.

San Francisco District Attorney Brooke Jenkins announced the settlement late Thursday.

“While electric vehicles may benefit the environment, the manufacturing and servicing of these vehicles still generates many harmful waste streams,” Jenkins said in a statement. “Today’s settlement against Tesla, Inc. serves to provide a cleaner environment for citizens throughout the state by preventing the contamination of our precious natural resources when hazardous waste is mismanaged and unlawfully disposed.”

The lawsuit, filed Tuesday, accused Tesla TSLA, +0.84%

of improperly handling, transporting and disposing hazardous materials including oil, lead acid batteries, antifreeze and diesel fuel at as many as 101 sites across the state.

As part of the settlement, Tesla was ordered to pay $1.3 million in civil penalties, and $200,000 to reimburse the cost of the investigation, which began in 2018. Tesla also must comply with an injunction for five years to properly dispose of its hazardous materials.

Investors bought up shares of Etsy Inc. on Thursday after the online crafts marketplace added to its board of directors a partner of hedge fund Elliott Investment Management L.P., which recently acquired a “sizable” stake in the company.

Etsy ETSY, +9.31%

said Marc Steinberg, who is responsible for public- and private-equity investments at Elliott, has been appointed to the board, effective Feb. 5, and will also join the board’s audit committee.

“Etsy has a highly differentiated position in the e-commerce landscape and a uniquely attractive business model, supported by a distinctive and engaged community,” Steinberg said. “We became a sizable investor in Etsy and I am joining its board because I believe there is an opportunity for significant value creation.”

Etsy’s stock shot up 8% in afternoon trading, to pare earlier gains of as much as 14.2%. The stock was headed for its best one-day gain since it climbed 9.2% on July 11.

Elliott’s stake was acquired in recent months, as the fund’s disclosure of equity holdings through the third quarter did not list Etsy shares.

“Marc’s appointment reflects our ongoing commitment to enhance the perspectives and expertise on the Etsy Board,” said Etsy Chairman Fred Wilson. “We look forward to benefiting from his voice in the boardroom as a seasoned and experienced investor as we continue our journey of creating a leading global e-commerce platform.”

Etsy’s stock has run up 18.6% over the past three months, but has tumbled 48.5% over the past 12 months. That’s compared with the S&P 500 index’s SPX

18.7% rally over the past year.

At an investor conference in December, Chief Executive Josh Silverman said business has slowed since the post-pandemic boom, as people have “had enough of buying things” and are now spending primarily on eating out and travel. Inflation and the loss of government subsidies was also weighing on spending.

Still, Silverman said, Etsy is now about two and a half times bigger than it was before the pandemic, and the company has more active buyers than it did at the peak of the pandemic.

Shell’s annual profits fell last year, although by less than the market had expected, as the European energy sector grapples with lower oil and gas prices and weaker refining margins.

Still, the London-based energy giant said Thursday that it would buy back $3.5 billion in shares this quarter and hiked its fourth-quarter dividend by 20% to 34.40 cents a share, in line with its promise of lofty shareholder returns despite slipping commodity prices.

The oil-and-gas major posted $20.28 billion in full-year profit measured on a net current-cost-of-supplies basis–a metric similar to the net income that U.S. oil companies report. This compares with $41.56 billion in 2022 when oil and gas prices soared after Russian invaded Ukraine.

For the fourth quarter, Shell’s profit on a net current-cost-of-supplies basis dropped to $1.38 billion from $6.15 billion in the preceding three-month period, reflecting lower refining margins, margins from crude and oil products trading, and higher operating expenses.

However, adjusted fourth-quarter earnings–which strip out certain commodity-price adjustments and one-time charges–rose to $7.31 billion from $6.22 billion in the third quarter, beating a consensus forecast of $6.04 billion, based on a poll of 24 analysts compiled by Vara Research. The increase was driven by higher trading gains from liquefied natural gas, favorable tax movements, and higher production, Shell said.

Market watchers had expected a dip in quarterly earnings, forecasting results across the integrated energy sector to have been hit by lower oil prices and refining margins.

But despite the weaker market environment, Shell’s key integrated-gas unit, which includes its leading LNG business, posted adjusted fourth-quarter earnings of $3.96 billion, up from $2.53 billion in the preceding three months.

“As we enter 2024 we are continuing to simplify our organization with a focus on delivering more value with less emissions,” Chief Executive Wael Sawan said.

The company, the second-biggest by market cap on the FTSE 100 index, also booked a $3.9 billion impairment charge, dragging quarterly net profits, which fell to $474 million from $7.04 billion. This was flagged by the company in January.

Cash flow from operations–a measure of the cash a company generates from normal business operations–rose to $12.575 billion in the quarter, topping a consensus forecast of $11.59 billion, from $12.33 billion in the third quarter.

During the fourth quarter, Shell–Europe’s biggest integrated oil company–produced 901,000 oil-equivalent barrels a day, in line with its targeted range, and 7.1 million metric tons of LNG, likewise in line with its guidance.

Upstream production–the extraction of crude oil and natural gas–also met the targeted range at 1.87 million BOE a day.

For the current quarter, Shell expects an output between 930,000 and 990,000 BOE a day of integrated gas, 7.0 million-7.6 million tons of LNG and an upstream production of 1.73 million-1.93 million BOE a day.

Write to Christian Moess Laursen at christian.moess@wsj.com

Walt Disney Co.’s lawsuit against Florida’s Republican Gov. Ron DeSantis and others, alleging they retaliated against the company for publicly criticizing a controversial parents-rights education law backed by DeSantis, was dismissed by a federal judge on Wednesday.

Shares of Disney DIS, -0.92%

fell about 1% Monday.

Judge Allen Winsor ruled Disney lacked legal standing to sue DeSantis. He added that Disney’s charges “fail on the merits” against members of the Florida board of a special improvement district in which the company operates its parks and resort.

In his ruling, Winsor said Disney “has not alleged any specific actions the new board took (or will take) because of the governor’s alleged control.” He added the company “has not alleged any specific injury from any board action.”

“Its alleged injury … is its operating under a board it cannot control. That injury would exist whether or not the governor controlled the board,” he wrote.

Disney strongly suggested it will appeal Winsor’s ruling.

“This is an important case with serious implications for the rule of law, and it will not end here,” the company said in a statement. “If left unchallenged, this would set a dangerous precedent and give license to states to weaponize their official powers to punish the expression of political viewpoints they disagree with. We are determined to press forward with our case.”

The controversial legislation, dubbed “Don’t Say Gay” by critics, was passed in 2022.

Total revenue was $86.3 billion, up 13% from $76 billion a year ago. Sales minus total acquisition costs (TAC) came in at $72.3 billion, compared with $63.1 billion a year ago.

Alphabet reported fourth-quarter net income of $20.7 billion, or $1.64 a share, compared with net income of $13.6 billion, or $1.05 a share, in the year-ago quarter.

“We are pleased with the ongoing strength in Search and the growing contribution from YouTube and Cloud. Each of these is already benefiting from our AI investments and innovation. As we enter the Gemini era, the best is yet to come,” Alphabet Chief Executive Sundar Pichai said in a statement announcing the results.

Analysts surveyed by FactSet had expected on average net earnings of $1.59 a share on revenue of $85.3 billion and ex-TAC revenue of $71.2 billion.

Google’s total advertising sales climbed to $65.5 billion from $59 billion a year ago, edging analysts’ average expectations of $65.8 billion. YouTube ad sales rose to $9.2 billion from $7.96 billion a year. Google Cloud rang up $9.2 billion in sales, up from $7.3 billion.

Alphabet is also ramping up AI initiatives to improve operational efficiency and productivity for 2023 and beyond. The company is using AI in its finance organization and analytics, but Alphabet did not break out AI revenue in Tuesday’s earnings report.

Alphabet Chief Financial Officer Ruth Porat told CNBC that gen-AI will be a focus of the call with analysts now taking place.

Shares of Google have climbed 53% over the past 12 months. The S&P 500 index SPX

has risen 21% the past year.

Saudi Arabian Oil Co., commonly known as Saudi Aramco, said that it has been ordered by the Saudi government to keep its oil production capacity at 12 million barrels a day.

The oil and gas company said it received the instruction while it was working to increase production to 13 million barrels per day.

“Aramco announces that it has received a directive from the Ministry of Energy to maintain its Maximum Sustainable Capacity (MSC) at 12 million barrels per day,” it said in a statement.

Write to Pierre Bertrand at pierre.bertrand@wsj.com

Flutter Entertainment, the parent company of FanDuel, started trading on the New York Stock Exchange for the first time Monday, as the company tries to narrow the valuation gap between it and rivals including DraftKings.

Flutter said Monday that it’s planning to make the New York Stock Exchange its primary listing and will put that to a vote of its shareholders in May. Making the NYSE its home, rather than London, will help it get included in important U.S. indexes, the company said.

Launching Monday with the ticker FLUT, it’s targeting New York as its primary listing late in the second quarter and early in the third quarter.

Having a New York listing will also boost its profile in the U.S., help with recruitment and retention, and access “much deeper” capital markets.

Flutter CEO Peter Jackson spoke with Yahoo Finance about the company after it started trading on Monday. The total addressable U.S. sports betting market is expected to reach $40 billion by 2023 — but Jackson thinks that’s lowballing it. “I expect [$40 billion] will turn out to be conservative, because everything in America turns out bigger than you expect,” he said.

Ryanair Holdings said third-quarter adjusted profit after tax fell as higher fuel costs offset revenue gains, and narrowed its guidance for the year.

The Irish budget airline said Monday that for the quarter ended Dec. 31 adjusted post-tax profit–its preferred metric–was 15 million euros ($16.3 million) compared with EUR211 million the year before.

Revenue for the quarter was EUR2.70 billion, compared with EUR2.31 billion a year ago.

The company said revenue per passenger rose 9%, with ancillary revenue up 2% to around EUR23 and average fares up 13% to over EUR42.

The airline carried 41.4 million passengers in the quarter compared with 38.4 million a year ago. Load factor–a measure of how full a plane is–for the period fell one percentage point to 92%.

The company narrowed its profit after tax guidance for the year to between EUR1.85 billion and EUR1.95 billion, from prior guidance of between EUR1.85 billion and EUR2.05 billion.

The company said that although it will benefit from the first half of Easter traffic falling in late March, this was unlikely to fully offset weaker-than-previously-expected load factors and yields in late third quarter and early fourth quarter.

Write to Anthony O. Goriainoff at anthony.orunagoriainoff@dowjones.com

By Anthony O. Goriainoff

Ryanair Holdings said third-quarter adjusted profit after tax fell as higher fuel costs offset revenue gains, and narrowed its guidance for the year.

The Irish budget airline said Monday that for the quarter ended Dec. 31 adjusted post-tax profit–its preferred metric–was 15 million euros ($16.3 million) compared with EUR211 million the year before.

Revenue for the quarter was EUR2.70 billion, compared with EUR2.31 billion a year ago.

The company said revenue per passenger rose 9%, with ancillary revenue up 2% to around EUR23 and average fares up 13% to over EUR42.

The airline carried 41.4 million passengers in the quarter compared with 38.4 million a year ago. Load factor–a measure of how full a plane is–for the period fell one percentage point to 92%.

The company narrowed its profit after tax guidance for the year to between EUR1.85 billion and EUR1.95 billion, from prior guidance of between EUR1.85 billion and EUR2.05 billion.

The company said that although it will benefit from the first half of Easter traffic falling in late March, this was unlikely to fully offset weaker-than-previously-expected load factors and yields in late third quarter and early fourth quarter.

Write to Anthony O. Goriainoff at anthony.orunagoriainoff@dowjones.com

With a rough 2023 in the rearview mirror, Levi Strauss & Co. this year is trying to tackle its problems with new pants.

That includes pants with lighter-weight denim; pants for women that can be worn as high-rise or low-rise; and even nondenim pants that management, during Levi’s LEVI, +1.27%

earnings call on Thursday, referred to as a “tech pant” for men with “moisture control and 360 mobility.” The company also plans to expand its offerings of Performance Cool pants intended to keep the wearer cool and dry on hotter days.

But as those products roll out, the retailers that account for most of Levi’s sales are still cautious about packing their shelves with new apparel — even though Levi’s executives pointed to slightly better demand from clothing stores during the fourth quarter and holiday period. And as the denim pioneer cuts costs, brings in new leadership and tries to be a bigger e-commerce player, Wall Street will now be digging around for signs of a payoff.

“Ultimately, the market will be looking for evidence new strategies can drive accelerated growth,” Stifel analyst Jim Duffy said in a research note on Thursday.

“We continue to believe in brand vitality and opportunities for extension. With product reflective of new direction arriving in the marketplace across 2024, the proof will be in consumer response,” he continued.

In an interview with MarketWatch on Friday, Duffy said he was optimistic about Levi’s standing as an established brand and stronger demand for its dresses, skirts and other women’s clothing items. But the more products a company rolls out, he suggested, the more it has to invest to make them work — and the more it needs to manage if sales falter.

“The risk, as I see it, is that more categories means more SKUs and more product that is fashion rather than core basic styles, and more investment and inventory that, if it doesn’t translate to the marketplace, could result in higher markdowns,” he said, referring to the stock-keeping units by which retailers track inventory.

Levi’s on Thursday said it would lay off between 10% and 15% of its global corporate staff in the first half of this year, a move intended to save $100 million in costs over that period. The layoffs are part of a two-year plan, called Project FUEL, intended to save money and strengthen the part of Levi’s business that sells directly to consumers via its own e-commerce network and its physical stores, as opposed to third-party retail operations.

The layoff announcement arrived days ahead of Chief Executive Chip Berg’s departure from that role, with Michelle Gass taking over on Jan. 29. As the company tries to be bigger than men’s jeans, Gass, in Levi’s earnings release on Thursday, said she saw an opportunity to grow internationally, make Levi’s own online and bricks-and-mortar sales a greater priority, and turn the brand into a larger “denim apparel lifestyle business.”

Levi’s shares fell after hours Thursday, after the company’s full-year profit forecast came in below expectations. The stock rebounded 1.3% on Friday but is still down 10.3% over the past 12 months.

Still, Levi’s direct-to-consumer sales jumped 11% during the fourth quarter, and accounted for 42% of sales overall. Duffy said that the company has pushed deeper into its direct-sales business because it gives executives greater insight into what consumers want, as well as more control over how it markets and sells its clothing. Cutting out other retailers also widens margins on sales, he noted.

Levi’s operating margins were higher in the fourth quarter. It also declared a dividend of 12 cents per share, payable in cash on Feb. 23.

But sales in Levi’s wholesale segment — the sales it gets from retailers who buy Levi’s product, then sell it to consumers — fell 2%. Better results in the U.S. and Asia were offset by a drop in Europe, the company said.

Retailers have spent the past two years trying to clear unwanted clothes from their stockrooms, and cutting prices in the process, after spiking inflation restricted many shoppers’ appetites to basics.

As Gass prepares to take the reins, she sought to put a positive spin on retail-chain sentiment. “So net-net, overall, as a company, we’re exiting the year on a strong note,” Gass said on the earnings call. “And U.S. wholesale, we’re encouraged. But as it relates to that channel, we’re not declaring victory yet. There’s been a lot of volatility this past year, some in our control, some outside. And so we are taking a cautious approach as we look forward.”

The U.S. dollar has had a relatively strong start to 2024 — but some analysts believe the greenback is still more likely than not to depreciate over the course of this year.

The ICE U.S. Dollar Index DXY,

which tracks the currency against a basket of six major rivals, has climbed about 2.1% so far this year, per Dow Jones Market Data.

As recently as late December, traders were pricing a likelihood as high as 90% for a rate cut in March — but those chances have since fallen to around 46% as of Friday, according to the CME FedWatch Tool. Meanwhile, the total amount of rate cuts priced in for this year, which reached as high as 170 basis points in mid-January, has now slipped to around 135 to 150 basis points.

However, the greenback is likely to see depreciation throughout the rest of this year, analysts at the investment bank wrote in a Thursday note, adding that much of the retreat would likely happen in the second half of 2024.

The BofA analysts said expect no recession this year and anticipate that the Federal Reserve will start cutting its key policy rate in March. Such a scenario is negative for the dollar, as the Fed’s easing would likely support risk assets with U.S. economic growth remaining resilient, according to the analysts.

Based on historical data, the ICE U.S. Dollar Index’s performance has been mixed from the onset of the Fed’s first rate cut over the past six cycles, and has been relatively flat on average over the following quarters, the analysts said.

“This is due in large part to the USD’s perceived ‘safe haven’ status and its negative correlation to risk, as cutting cycles have often been associated with recessions,” they wrote.

Jonathan Petersen, senior market economist at Capital Economics, echoed that point in a Thursday note. He expects the dollar to face headwinds from strong risk appetite in global markets and falling bond yields in the U.S. over the course of the year, and anticipates the greenback will remain rangebound against most major currencies for most of 2024.

The Biden administration’s announcement Friday that it’s pausing liquefied natural gas export approvals sparked political backlash, drew cheers from climate activists and stoked uncertainty in energy markets, but is unlikely to see the U.S. give up its title as the world’s top LNG exporter.

The U.S. will delay its decisions on new LNG exports to non-free trade agreement countries, allowing time for the Energy Department to update the underlying analyses for LNG export authorizations, the White House said.

Those analyses are roughly five years old and “no longer adequately account for considerations” such as potential cost increases for American consumers and manufacturers or the “latest assessment of the impact of greenhouse gas emissions,” it said.

The Biden administration likely “realizes the role of LNG in foreign policy, but at the same time it needs to show the Democrat base that it is doing something for climate change,” said Anas Alhajji, an independent energy expert and managing partner at Energy Outlook Advisors, pointing out that the announcement comes during a presidential election year.

“Delaying one project or stopping it may not be a big deal, but it is a problem if it becomes a trend,” he said in emailed commentary.

Environmental groups, which have pushed for action, cheered the decision.

The 12 impacted projects in the U.S. “would spew out as much climate-warming pollution as 223 coal plants per year, and they present explosion risks to the communities where they’re located and emit other health-harming chemicals,” the Sierra Club, an environmental group, said in a statement welcoming the decision.

Top exporter

The announcement is particularly important for a nation that became the world’s biggest LNG exporter in the span of less than a decade.

The U.S. became the world’s largest LNG exporter during the first half of 2022 on the back of increases in LNG export capacity, international natural gas and LNG prices, and global demand, particularly in Europe, according to the Energy Information Administration.

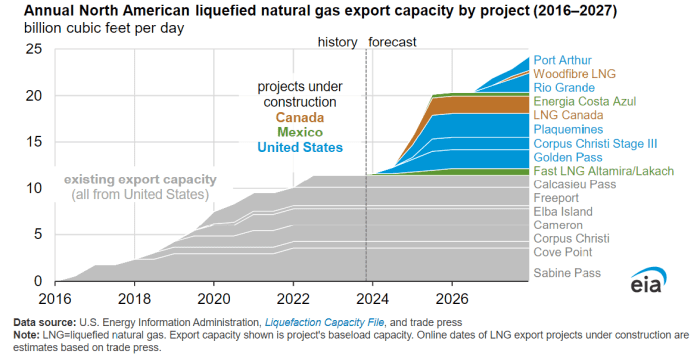

The country’s exports of LNG climbed to a fresh record in November 2023, with the EIA reporting domestic exports of 386.2 billion cubic feet, up from 384.4 bcf a month earlier. Exports in December 2016 were at just 41.8 bcf.

U.S. LNG exports soared after 2016.

EIA

With 90% of U.S. LNG going to non-free trade agreement destinations, withholding licensing effectively “halts project development,” John Miller, managing director, ESG and sustainability policy at TD Cowen wrote in a Friday note.

Equities

LNG equities with operating facilities likely won’t benefit from the administration’s announcement, at least not immediately, until the impacts of this pause in export approvals to non-FTA countries becomes more clear, Jason Gabelman, director, sustainability & energy transition at TD Cowen said.

U.S. companies with government approvals that have not been sanctioned, “could have a higher probability of moving forward this year, albeit modestly” as offtakers may be hesitant to sign up to new U.S. projects with LNG development getting “politicized,” he said. Among those, he pointed out approvals for proposed liquefaction units at NextDecade Corp.’s NEXT, +2.30%

Rio Grande LNG export facility project in Brownsville, Texas.

At the same time, it would not be a surprise if U.S. LNG companies pursuing growth that do not yet have non-FTA approval see downside pressure, said Gabelman.

LNG projects take around 4 years to build and any delays to project sanctions today will take “multiple years to manifest in the market,” he said.

Still, the U.S. announcement “introduces the risk of more stringent oversight that could limit new U.S. capacity” more than four years out, Gabelman said.

Companies that supply equipment to LNG liquefaction projects include Baker Hughes Co. BKR, +0.59%

and Chart Industries Inc. GTLS, -7.54%,

said Marc Bianchi, a senior energy analyst at TD Cowen.

Any slowing of approval would create “overhand on order growth,” he said.

Climate change

The White House said Friday that its decision will not impact the ability of the U.S. to continue supplying LNG to its allies in the near term but also acknowledged environmental concerns.

“I think we’ve got to be clear eyed about the challenges that we face. The climate crisis is an existential crisis, and we’ve got to be, I think, really forward leaning into making sure that we’re taking that head on,” said Ali Zaidi, the White House national climate adviser, told reporters Friday.

He added that given the number of approvals already completed, the number of projects under construction are set to double existing capacity with approvals beyond that set to double capacity yet again.

“So there’s a long runway here, and we’re taking a step back and thinking, OK, let’s take a hard look before that runway continues to build out,” he said.

Rob Thummel, senior portfolio manager at Tortoise, argued that U.S. LNG exports actually reduce global carbon emissions as natural gas typically “displaces coal to generate electricity in countries such as China and India.”

They also improve global energy security as U.S. natural gas is becoming Europe’s primary energy supplier, replacing Russia, he said.

In a statement Friday, Sen. Joe Manchin, a West Virginia Democrat and chairman of the U.S. Senate Energy and Natural Resources Committee, said that if the Biden administration has facts to prove that additional LNG export capacity would hurt Americans, it needs to make that information public. But if the pause is “another political ploy to pander to keep-it-in-the-ground climate activists,” he said he would “do everything in my power to end this pause immediately.

Manchin plans to hold a hearing on the decision in the coming weeks.

Market impact

The U.S. decision to delay new LNG export permits is unlikely to have an impact on domestic natural-gas supplies or prices, said Energy Outlook Advisors’ Alhajji.

LNG prices and the rate at which new LNG export terminals can be constructed help determine LNG export volumes, the EIA said, and higher LNG exports can result in upward pressure on U.S. natural-gas prices, while lower U.S. LNG exports can pressure prices.

On Friday, natural gas for February delivery NG00, +0.23%

NGG24, +0.26%

settled at $2.71 per million British thermal units, up 7.7% for the week.

Meanwhile, the U.S. is likely to keep its position as the world’s top LNG exporter, according to Tortoise’s Thummel.

The U.S. is the currently the largest LNG exporter at almost 12 bcf per day, with Qatar coming in second, he said.

Qatar is expanding its LNG export capacity and is expected to have the ability to export almost 20 bcf per day by 2028, he said. The EIA reported recently that Qatar has averaged 10.3 bcf per day in exports during the last 10 years.

That would mark sizable growth. But the EIA reported in November that LNG export capacity from North America is likely to more than double from around 11.4 bcf per day to 24.3 bcf per day by the end of 2027.

The EIA said North America’s LNG export capacity is likely to more than double by 2027.

EIA

Given expected growth in U.S. LNG export capacity, the U.S. is likely to “remain the largest exporter of LNG in the world” despite the U.S. announcement, said Thummel.