All eyes have been on shares of Tupperware Brands Corp. and Yellow Corp. in recent days as the stocks have soared despite a dearth of fresh news in the case of the former, and negative news in the case of the latter.

Over the weekend the Wall Street Journal reported that the less-than-truckload company has shut down operations as it prepares for bankruptcy. On Monday the International Brotherhood of Teamsters said it was served legal notice that Yellow was “ceasing operations and filing for bankruptcy.” MarketWatch has reached out to Yellow with a request for comment.

Related: How ‘left-for-dead’ Tupperware became a buzzy trading play

Set against this backdrop, the surging share prices for Tupperware

TUP,

-25.99%

and Yellow have sparked comparisons with the meme stock phenomenon, where discussions on social media can send share prices surging. This trend turned companies such as AMC Entertainment Holdings Inc.

AMC,

-3.45%

and GameStop Corp.

GME,

-4.42%

into meme stock “darlings” in recent years. But Samantha LaDuc, founder of LaDucTrading.com, says there’s a different explanation for what’s been happening to shares of Tupperware and Yellow.

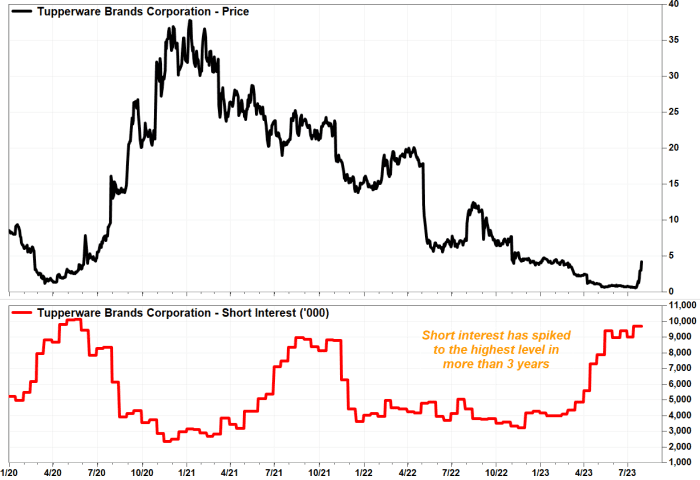

“Literally, it’s short covering, as the paired trade of long quality, short junk unwinds,” she told MarketWatch, via email. “And it typically always precedes volatility.”

Short selling of a stock occurs when an investor borrows shares and sells them immediately expecting the price to drop. The shares can then be repurchased and returned to the lender, with the investor pocketing the difference. Although sometimes vilified, short sellers are actually misunderstood, Robert Sloan, managing partner at financial analytics firm S3 Partners and author of “Don’t Blame the Shorts,” recently told MarketWatch.

Related: Short selling stocks — and trying to play short squeezes — can be very dangerous

In a letter to investors this week, Dan Loeb, the chief executive of the hedge-fund firm Third Point, explained that short selling is much more challenging today than it has been historically.

“Fundamental analysis is increasingly taking a back seat to monitoring daily option expiries and Reddit message boards, as evidenced by the numerous short squeezes and manipulations of heavily shorted stocks such as AMC and GameStop in 2021 and others this year,” he wrote. “While we have not abandoned short selling, we continue to reduce our single-name short exposure in favor of market hedges and short baskets.”

LaDuc explained that in June and July hedge funds aggressively covered shorts in global equities, and also noted the trend of FOMO, or fear of missing out.

“We have had the largest six-month increase in leverage on record (according to Goldman), with a clear case of FOMO-the-MOMO [momentum] chase in full view as concentration risk in megacap tech forced a NASDAQ “SPECIAL REBALANCE” to ‘down-weight’ AAPL, MSFT, GOOGL etc.”

Related: Short sellers are not evil, but they are misunderstood

Short covering occurs when a person with a short position buys back the shares, ending the short trade, and returns the shares to the seller. With this strategy, the short seller aims to cover after the share price falls and make a profit. They may also cover if the price goes up to limit their losses.

Last week LaDuc told MarketWatch how she was able to anticipate a Tupperware stock spike despite a dearth of traditional market-moving news around the name.

Tupperware’s stock has continued its upward trajectory, rocketing again on Tuesday. The stock eventually ended Tuesday’s session up 26% at $5.38, with LaDuc warning her clients of the risks involved in a parabolic rally. “I suggested to clients it was likely done and to be very cautious if still long because ‘Parabolas are trapped longs that can trigger volatility which can trigger a liquidation event’.”

Related: Yellow’s stock quadruples in 2 days even after reports that bankruptcy is coming

Shares of Tupperware are down 23.2% Wednesday. Yellow Corp.’s stock, which ended Tuesday’s session up 121.6%, is down 17.3% Wednesday.

With regard to Yellow Corp. LaDuc attributes its recent stock movements to insider and Wall Street manipulation. “Low priced, low-float stocks are VERY easy to push around,” she told MarketWatch.

Bankrupt companies such as Bed Bath & Beyond Inc.

BBBYQ,

+1.46%

have even proven attractive to some investors recently, sparking comparisons with the meme stock phenomenon.

“They are clearly retail investors, largely on the Robinhood

HOOD,

-4.16%

platform, that are readers of Reddit,” Howard Ehrenberg, a bankruptcy and reorganization practice partner at law firm Greenspoon Marder, told MarketWatch last month. “They are people buying on rumor and hoping that by participating in a mass purchase binge, they will make money.”

Related: Tupperware stock skyrockets to a record 434% gain in July

Hertz Global Holdings Inc.

HTZ,

-1.73%,

which filed for bankruptcy protection in 2020 and exited bankruptcy the following year, also fueled meme-stock comparisons, when mostly retail investors piled into the stock during the bankruptcy process.

Typically in a bankruptcy, shareholders are wiped out as creditors take control of the remaining assets. But those investors were rewarded when the company got a big capital injection and was able to resume trading on an exchange.

The investor behavior around these types of stocks has caught the attention of academics. Victor Ricciardi, visiting finance faculty at Tennessee Tech University and co-author of the new book “Advanced Introduction to Behavioral Finance,” recently described some of the behaviors that can prompt investors to purchase bankrupt stocks.

“Representativeness bias refers to when past performance influences how an individual perceives an investment,” Ricciardi told MarketWatch via email last month. “In particular, a person makes a general assumption about a small sample of information or experience.”

Related: Why investors gamble on shares of bankrupt companies — Bed Bath & Beyond, for example

So, for example, if a person made a substantial gain from a previous bankrupt stock they might conclude that all bankrupt stocks result in investment gains, according to Ricciardi. There are also parallels with gambling.

“The notion of the long shot bias is based on the tendency for people to overweight the probability of a long shot bet paying off, especially in horse racing and lotteries,” Ricciardi added. “This is driven by overconfident behavior and dreams of becoming a millionaire overnight.”

Tupperware’s stock has risen 250.6% in the last three months, while Yellow shares have climbed 84.3%.

Tomi Kilgore and Phil van Doorn contributed to this report.