[ad_1]

The Magnificent Seven group, which was crafted by Mad Money host Jim Cramer, is renowned for its impressive growth potential and its ability to roll with the economic punches. With shares of Tesla (NASDAQ:TSLA) now on the outside looking in (Cramer removed it from the Magnificent Seven) following its brutal quarterly flop, questions linger as to which other growth companies are more deserving of a spot in the group.

Therefore, in this piece, we’ll check in with TipRanks’ Comparison Tool to stack up two candidates that I believe are deserving of consideration now that Tesla is no longer magnificent enough to stay in the Magnificent Seven.

Netflix (NASDAQ:NFLX)

Remember the days when the FAANG (also a term and cohort created by Jim Cramer) group was dominating the financial headlines, powering broader markets higher? If you’re a new investor who jumped into the market waters within the past two years, you’re probably more familiar with the Magnificent Seven group. Either way, I do think the “N” — Netflix — in the original FAANG is starting to prove its potential once again, and this has me incredibly bullish about its future.

The stock took a massive beating back in late 2021 and early 2022, crashing by around 75% from peak to trough. The implosion caused Netflix stock to be scratched out of the conversation, ultimately marking the beginning of the end of FAANG and the beginning of the Magnificent Seven group.

Today, Netflix is making an epic comeback, proving its doubters wrong, with a handful of impressive quarters that have helped fuel a more than 220% gain off its 2022 lows. Indeed, competition in the streaming space was getting intense, and as the pandemic lockdown winners reversed course in violent fashion, it was natural to think that Netflix was on its way out of the conversation.

After the latest impressive number, though, Netflix has proven to us all that it is still magnificent and that the 2021-22 crash was a blunder made by Mr. Market. The original streaming kingpin remains king, with its impressive content that’s kept users coming back, even following substantial price hikes. Additionally, the ad-based tier and gaming expansion have made the firm more of a growth stock again.

Only time will tell if Netflix is headed for new heights as it continues adding to its strength in the new year. Unbelievably, shares are down around 18% from their peak in 2021. With co-founder Reed Hastings slashing his stake by $1.1 billion, gains will be harder to come by in the new year. The stock’s already endured quite a bit of multiple expansion in recent quarters. So much so that some analysts have been downgrading it due to valuation concerns.

At 46.8 times trailing price-to-earnings (P/E), the stock is pricier than its historical average and that of its peer group. While Netflix stock deserves a premium, I believe the company will need to keep releasing high-quality content and experience more success with its gaming push if it’s to keep growth at the level that warrants inclusion into the “Magnificent Seven.”

Can it be done? I think it can. Management has really executed, and the stock reflects a massive rebound in investor confidence.

What Is the Price Target for NFLX Stock?

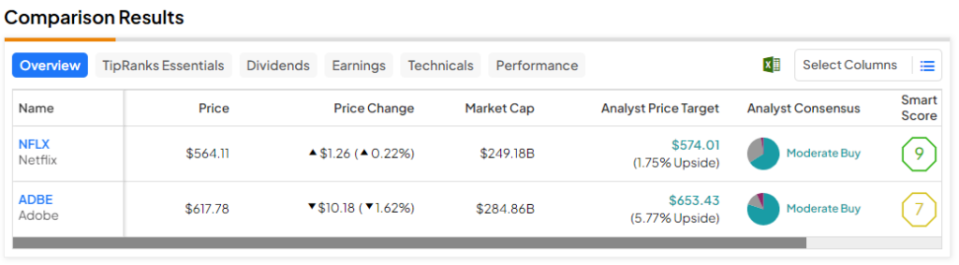

Netflix stock is a Moderate Buy, according to analysts, with 27 Buys, 13 Holds, and one Sell assigned in the past three months. The average NFLX stock price target of $574.01 implies 1.8% upside potential.

Adobe (NASDAQ:ADBE)

Adobe stock is another tech titan that’s been scorching hot in 2023, blasting off nearly 70% in the past year. Generative artificial intelligence (AI) is a huge reason why Adobe stock has been able to turn the tide so fast. With impressive AI technologies (think Firefly and Sensei) ingrained into the company’s already impressive creative suite, the firm may have the means of charging its users even more.

If it’s adding more value, users should be more than willing to pay the higher price. As Adobe continues embracing the AI age, I can’t help but stay bullish on the stock.

In fact, I view AI as the catalyst that could propel ADBE stock right back to all-time highs. Recently, BakerAvenue’s King Lip stated that the company’s AI business is “extremely compelling.” With such a sizeable and loyal installed user base, upselling AI offerings is likely to be no issue for the firm.

It’s not just about putting profound AI power into creative hands that has me most intrigued. Given the horrific headlines surrounding AI-generated deep fakes of Taylor Swift that went viral, I believe more attention ought to be placed on AI guardrails to ensure the responsible use of AI products.

In that regard, I believe Adobe is a firm that can put the appropriate guardrails in place to prevent (or minimize) misuse of AI tools. As the company moves on from its abandoned Figma acquisition, look for the firm to become as much of an AI innovator as it is a major player in AI safety and ethics.

All things considered, Adobe stock stands out as a magnificent tech firm worthy of more investor (and Cramer) praise.

What Is the Price Target for ADBE Stock?

Adobe stock is a Moderate Buy, according to analysts, with 24 Buys, four Holds, and two Sells assigned in the past three months. The average ADBE stock price target of $653.43 implies 5.8% upside potential.

The Takeaway

Undoubtedly, there are a slew of high-growth companies that are doing incredibly well, with drivers that could help keep growth elevated for some time. That alone doesn’t guarantee a spot with the now six magnificent companies (the so-called Super Six, if you will).

However, I do think Netflix and Adobe are companies worthy of the most exclusive and enviable high-growth cohort out there. Between the two, analysts expect more upside from Adobe (5.8%) for the year ahead.

[ad_2]

Source link