The numbers: U.S. new-home sales fell 5.6% to a seasonally adjusted annual rate of 679,000 in October, from a revised 719,000 in September, the government reported Monday.

Analysts polled by the Wall Street Journal had forecast new-home sales to occur at a seasonally adjusted annual rate of 725,000 in October.

The numbers: U.S. pending home sales rebounded in September but remain near a record low as high mortgage rates and low inventory continue to hurt the real-estate sector.

Pending home sales rose 1.1% in September from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

But pending home sales were still depressed on an annual basis due to the dearth of home listings. The September figure was the second-lowest reading since the NAR began tracking the data in 2001.

Transactions were down 11% from last year.

Nonetheless, the sales pace exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 1.5% in September.

Pending home sales reflect transactions where the contract has been signed for the sale of an existing home, but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

The NAR also released an updated forecast for existing-home sales on Thursday. The group expects sales to fall 17.5% in 2023 to a pace of 4.15 million, which will be the slowest pace since 2008. Yet due to low inventory, the median home price will increase by 0.1% in 2023, the NAR said, to $386,700.

The group expects home sales to rebound in 2024, rising 13.5% to a rate of 4.71 million. Home prices are expected to rise 0.7% next year, to $389,500.

The NAR also expects the 30-year mortgage rate to fall to 6.9% in 2023 and 6.3% in 2024. The 30-year was averaging 7.98% as of Wednesday, according to Mortgage News Daily.

Big picture: The U.S. housing market is dealing with problems on both the demand and supply sides, but the NAR seems confident that the sector will recover in the new year.

At present, not only are rates high enough to discourage home buyers, the lack of inventory is also making homes more expensive, which further spooks buyers. The NAR expects the pace of existing-home sales to fall to the slowest in 15 years, when the U.S. was in the midst of a recession caused by the subprime-lending crisis.

What the realtors said: “Because of home builders’ ability to create more inventory, new-home sales could be higher this year despite increasing mortgage rates,” NAR Chief Economist Lawrence Yun said. “This underscores the importance of increased inventory in helping to get the overall housing market moving.”

The numbers: Home sales in September fell to the lowest level since 2010, as high mortgage rates continue to hammer the housing market.

Aside from low inventory, rising rates are eroding buyers’ purchasing power, and drying up demand. Sales of previously owned homes fell by 2% to an annual rate of 3.96 million in September, the National Association of Realtors said Thursday.

That’s the number of homes that would be sold over an entire year if sales took place at the same rate every month as they did in September. The numbers are seasonally adjusted.

The drop in sales was slightly better than what Wall Street was expecting. They forecasted existing-home sales to total 3.9 million in September.

Compared to September 2022, home sales are down by 15.4%.

Key details: The median price for an existing home in September rose for the third month in a row to $394,300. Prices are up 2.8% from a year ago. That was the highest price for the month of September since NAR began tracking the data.

Home prices peaked in June 2022, when the median price of a resale home hit $413,800.

Around 26% of properties are being sold above list price, the NAR noted.

The total number of homes for sale in September fell by 8.1% from last year, to 1.13 million units. Housing inventory for the month of September was the lowest since 1999, when the NAR began tracking the data.

Homes listed for sale remained on the market for 21 days on average, up from the previous month. Last September, homes were only on the market for 19 days.

Sales of existing homes rose only in the Northeast in September, as compared with the previous month, by 4.2%. The median price of a home in the region was $439,900.

All-cash buyers made up 29% of sales, highest since January 2023. The share of individual investors or second-home buyers was 18%. About 27% of homes were sold to first-time home buyers.

Big picture: The U.S. housing market is in the midst of a serious slowdown that is primarily driven by high mortgage rates. High rates spook home buyers, drying up demand, and high rates also deter homeowners from selling since they may have to purchase another home. For a homeowner with a 3% mortgage rate for the next few decades, there’s little incentive to move.

And the residential sector is likely to see sales fall further in October’s data, as the 30-year mortgage inches even higher. Demand for mortgages has collapsed, and some outlets like Mortgage News Daily are quoting a rate of 8% for the 30-year.

Existing-home sales in 2023 could fall to the slowest pace since the housing bubble burst in 2008, real-estate brokerage Redfin said on Thursday, at a 4.1 million pace.

What the realtors said: “Mortgage rates and limited inventory has been the story throughout this year — no different this month, other than the fact that interest rates are moving higher,” said Lawrence Yun, chief economist at the National Association of Realtors.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” he added. “We don’t want the Fed to overdo it and cause great harm to real estate.”

Yun also questioned whether there will be a “fundamental change” or a temporary one to the “American way of life” due to the slowdown in sales.

Market reaction: Stocks were down in early trading on Thursday. The yield on the 10-year note BX:TMUBMUSD10Y

rose above 4.9%.

Chinese regulators eased the nation’s mortgage requirements to let more home buyers enjoy favorable mortgage conditions that were previously limited to first-time home purchasers, the state-run Xinhua News Agency said on Friday.

China’s central bank, the Ministry of Housing and Urban-Rural Development and the National Financial Regulatory Administration jointly eased the requirements for home buyers who have already purchased homes to boost property sales as the real-estate slump continued, according to Xinhua.

Home buyers who don’t have family members with houses registered under their names can enjoy favorable terms that were previously limited to people buying their first homes, according to Xinhua.

First-home buyers are normally given cheaper mortgage rates than other buyers who have at least one apartment. First-home buyers are also required to make smaller down payments, as low as 20% of the total property value.

Write to Singapore editors at singaporeeditors@dowjones.com

The majority of second-quarter earnings season is over, with a handful of major technology and retail names left to report this week. Economists will be focused on any news from an annual gathering of monetary policy thinkers and practitioners in Jackson Hole, Wyoming.

The numbers: Home sales inched up for the first time in four months, even as the U.S. housing market continues to deal with a dearth of listings.

Pending home sales rose by 0.3% in June from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

The figure exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 0.5% in June.

Transactions were still down 15.6% from last year.

Pending home sales reflect transactions where a contract has been signed for the sale of an existing home but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

Big picture: Home sales rose as the housing market contends with excess buyer demand and a shortfall in the supply of homes for sale.

What the real-estate experts said: “The recovery has not taken place, but the housing recession is over,” NAR chief economist Lawrence Yun said. “The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply.”

The NAR also said it expects rates for 30-year mortgages to average 6.4% this year and to fall to 6% in 2024.

The NAR also expects existing-home sales to fall 12.9% in 2023 from the previous year, to 4.38 million, before recovering in 2024 to a rate of 5.06 million.

The group also expects home prices to hold steady this year, falling only slightly by 0.4% to $384,900, before rising 2.6% next year to $395,000.

“The West — the country’s most expensive region — will see reduced prices, while the more affordable Midwest region is likely to see a small positive increase,” Yun added.

The housing market may feel out of whack to home buyers coping with fast-rising home prices and 7% mortgage rates. But like it or not, the housing market is in the pink of health.

Several economic indicators that measure housing activity — from home prices to sentiment surveys — show that home builders and sellers (the few that are out there) are finding strong demand from home buyers.

News of the housing market’s relative health may be welcome to some — like real-estate agents and investors — but it’s becoming a concern for economists. The more buoyant the housing market, economists say, the more likely the U.S. Federal Reserve will unveil another interest-rate hike, which further heightens the risk of a recession.

“‘The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents.’”

— Torsten Slok, chief economist at Apollo

“The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents,” Torsten Slok, chief economist at Apollo, wrote in a note in May. And housing is a big part of how the government measures inflation, he added. This will make it more difficult to reduce inflation from 5% to the Fed’s 2% inflation target, he said.

If the Fed launches another rate hike, it would push mortgage rates, which are already in the 7% range, to go even higher.

“The housing market is in a very — if fragile — recovery,” Mike Simonsen, founder and president of real-estate analytics firm Altos Research, told MarketWatch.

“There appears to be more demand than available supply for homes, especially in the real-estate market,” he explained, which is keeping home prices high, but that doesn’t mean demand could evaporate if the current situation changes. Recall when rates doubled from pandemic-era lows in 2021 to 7% last year, which zapped home-buying momentum.

House hunters have adjusted their expectations. But if rates were to jump from 7% today to even higher levels, “I would not be at all surprised if homebuyers stopped abruptly again,” Simonsen said, stating his thesis for the fragility of the sector. Americans broadly expect rates to go over 8%, according to a March survey by the New York Federal Reserve.

MarketWatch looked at three housing-market indicators — and the picture looks rosier than ever:

Active listings are down — blame interest rates

Redfin’s deputy chief economist, Taylor Marr, said his go-to indicator was active listings.

Active listings are down this spring, compared to the previous year, according to the company’s data. At the end of June, the number of homes listed for sale on the market was down 8.1% over the prior year.

“It really captures that supply is pulling back significantly relative to demand,” Marr said.

Redfin data says that active listings of homes are down.

As a result, the housing market is seeing an excess of demand and not enough supply, which has led to a resurgence of bidding wars in some parts of the U.S.

While this metric is showing signs of the housing market returning to life and heating up amid a shortage of houses for sale, Marr said he’s not yet ready to call it a recovery. “It’s hard to declare completely the bottom of the housing market,” he said.

Still battle-scarred by the housing crash of the Great Recession, Marr said economists “might be hesitant” to say that the housing market is in recovery mode. “We still have a lot of uncertainty with the economy ahead,” he added. “If the economy really takes a turn three or four months from now for whatever reason, it could certainly bring the housing market back lower than it was even last November,” he added.

The price gap between new and existing homes

With a major shortage of resale homes, new-home sales have been taking off.

Home builders, understandably, are thrilled about the inventory shortage.

The National Association of Home Builders measures builders’ sentiment in a monthly index, and that indicator has been very cheery of late. In June, the index turned positive for the first time in nearly a year. Builders were scaling back price reductions; they were happy about current sales conditions as well as sales over the next six months, the NAHB said.

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” said Rob Dietz, chief economist of the NAHB.

One of the major U.S. home builders, Lennar, also offered some commentary on its second-quarter earnings call last month. The company’s executive chairman, Stuart Miller, said that “the market and the economy will remain constructive for home builders as pent-up demand continues to come to market and consume affordable offerings.”

Miller also doesn’t expect the supply issue to be fixed anytime soon: “We believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance,” he said on the call. “The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.”

Home-builder confidence, as a result, is signaling high optimism about the future of the housing market, and a return to normalcy.

Builders have ramped up building new single-family and multi-family homes.

Ali Wolf, chief economist at Zonda, looks at how prices of new homes trend relative to resale homes as a key indicator of the health of the housing market. Her conclusion? Housing industry professionals involved in the construction and sale of new homes are out of a recession, given the robust demand.

In fact, demand has been so strong that new homes — generally considered to be more expensive than resales — have become more affordable in home buyers’ eyes given the competition in the existing home space.

Typically, new homes are 20% more expensive than resales, Wolf said. And today? That spread has fallen to 4%.

So what’s going on? Builders are not necessarily slashing prices. Instead, existing home prices have risen as homeowners are reluctant to sell.

That’s a good deal for buyers. New homes, Wolf said, are traditionally considered a “luxury good.” They’re brand new, and buyers can often customize them. They also require less maintenance than older homes.

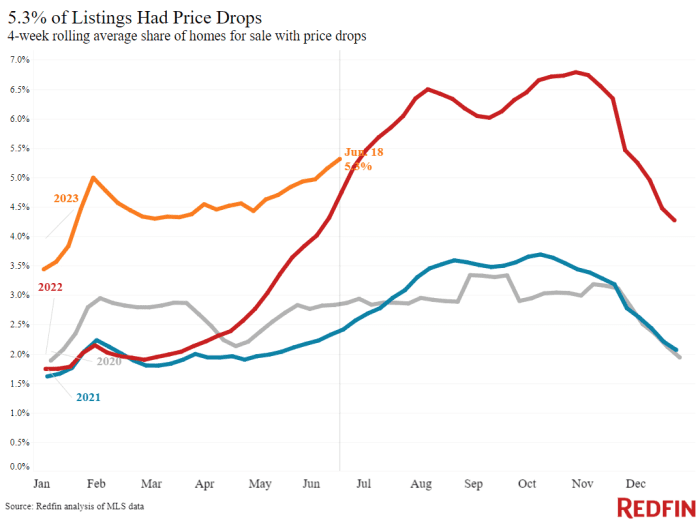

Sellers are holding out on cutting prices

Simonsen, who leads Altos Research, said price cuts were his go-to indicator to gauge the health of the real-estate market. Specifically, price cuts formed a proxy for demand, he explained.

“When the houses are on the market, if there are no buyers for the current houses that are listed, people start taking price cuts,” Simonsen said.

And to be clear, price cuts jumped last year, when rates jumped, he added.

But that dynamic has since changed, as seen in the chart below. “There are currently fewer price reductions now than in 2018 or 2019,” Simonsen said.

Data from Redfin says that homeowners aren’t cutting prices on their homes when selling, possibly due to strong interest from buyers.

And for those of you holding out for home prices to crash? Keep waiting, Simonsen said.

“There’s nothing in the data that shows prices crash,” he said. Even if a recession hits at the end of the year, which results in more job layoffs, demand for home-buying falling, and an increase in foreclosures and distress, that’s still a few years from now, he added.

“There’s no signal of home prices crashing anywhere,” Simonsen added.

Data on the U.S. consumer and housing market, plus several notable earnings reports, will be this week’s highlights. Barring any surprises, federal financial regulators’ Congressional testimony will be the main event on the banking front.

On Wednesday, Fed Vice Chair for Supervision Michael Barr and Federal Deposit Insurance Corp. Chairman Martin Gruenberg are scheduled to testify before the House Financial Services Committee. They’ll discuss the collapses of Silicon Valley Bank and Signature Bank and efforts to maintain confidence in the U.S. banking system.

The numbers: U.S. pending-home sales rose 2.5% in December, reversing a six-month losing streak, according to the monthly index released Friday by the National Association of Realtors (NAR).

Pending home sales were down for six months in a row, as the U.S. Federal Reserve increased interest rates and mortgage rates took off.

Pending-home sales beat analyst expectations. Analysts polled by the Wall Street Journal had forecast the pending home sales index to drop by 1%.

Contract signings rose in the South and the West.

Pending home sales reflect transactions where the contract has been signed for an existing-home sale, but the sale has not yet closed.

Economists view it as an indicator for the direction of existing-home sales in subsequent months.

Mortgage application activity hints at the housing market’s further recovery. Mortgage demand rose in the latest week.

Key details: Compared with a year earlier, transactions were down by 33.8%.

On a monthly basis, pending sales rose in the South and the West. Sales dropped in the Northeast and Midwest.

Pending home sales fell the most since last December in the West, by 37.5%.

Big picture: A dip in rates has boosted demand for mortgages. Buyers are coming back to the market, and the housing market is slowly recovering. But inventory remains low, as sellers hold out. Many are looking to the spring to see if sellers are motivated to list their homes.

What the realtors said: “This recent low point in home sales activity is likely over,” NAR Chief Economist Lawrence Yun said. “Mortgage rates are the dominant factor driving home sales, and recent declines in rates are clearly helping to stabilize the market.”

Yun expects mortgage rates to hover between the 5.5% and 6.5% range.

He also expects the South to outperform in terms of sales, since the job market is stronger in the region.

What they’re saying: “Home sales have now largely adjusted to the collapse in demand since late 2021. … [but] a sustained recovery likely remains a long way off,” Kieran Clancy, senior U.S. economist at Pantheon Macroeconomics, wrote in a note.

“The downturn in sales is coming to an end, but the decline in home prices is only just getting underway,” he added. He expects home prices to fall 15% over the next year.

Market reaction: The Dow Jones Industrial Average DJIA, +0.08%

and the S&P 500 SPX, +0.25%

were mixed in early trading on Friday. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.511%

rose above 3.5%.

The numbers: U.S. existing-home sales fell 1.5% to a seasonally adjusted annual rate of 4.02 million in December, the National Association of Realtors said Friday.

This is the 11th straight monthly decline in existing-home sales. The losing streak is the longest since NAR began tracking sales in 1999.

Economists polled by the Wall Street Journal were expecting existing-home sales to drop to 3.95 million.

The level of sales activity was lowest since November 2010, in the midst of the foreclosure crisis in America.

Compared with December 2021, home sales were down 34%.

Total sales of existing homes in 2022 were down 17.8% from the previous year. Last year, 5.03 million existing homes were sold, which is the lowest level since 2014.

The last time existing home sales dropped by this magnitude was in 2008.

Key details: The median price for an existing home fell to $366,900 in December, from $370,700 in November.

The number of homes on the market fell 13.4% to 970,000 units in December.

Expressed in terms of the months-supply metric, there was a 2.9-month supply of homes for sale in December, down from the previous month. Before the pandemic, a four- or five-month supply was more the norm.

Homes remained on the market for 26 days on average, up from 24 days in November. Pre-pandemic, the average time for homes to remain on the market was a month.

Sales of existing homes mostly fell across the country, led by the South, which saw a 2.2% drop. Sales were unchanged in the West.

All-cash transactions made up 28% of all transactions. About 31% of homes were sold to first-time home buyers, up from the previous month.

Big picture: Mortgage rates have moved lower, and many buyers are coming back to the real-estate market.

So with rates continuing to move downwards, sales may likely rebound in the next few months, breaking an 11-month losing streak.

But the market still has to figure out inventory, since there are so few homes for sale on the market.

What the realtors said: “We really need to begin to address this supply issue,” Lawrence Yun, chief economist at the National Association of Realtors said.

Yun said that overall, homeowners have enjoyed more in home price appreciation versus their 401k performance in the stock market.

What are they saying? Even though sales dropped considerably, “this result was somewhat better than expected,” Stephen Stanley, chief economist at Amherst Pierpont, wrote in a note.

And as rates move lower, that will “help to boost demand for homes generally,” Stanley added, “but it will also lessen the impact of homeowners being ‘trapped’ in their current locations.”

Market reaction: Stocks were up in early trading on Friday. The yield on the 10-year note TMUBMUSD10Y, 3.479%

rose above 3.45%.

The numbers: U.S. pending-home sales fell 4% in November, which is the sixth straight monthly drop, according to the index released Wednesday by the National Association of Realtors (NAR).

The index was last at this level in the midst of the pandemic lockdown, in April 2020.

Analysts polled by the Wall Street Journal had forecast the pending home sales index to drop by 1.8%.

Contract signings fell in all regions across the country.

Pending home sales reflect transactions where the contract has been signed for an existing-home sale, but the sale has not yet closed.

Economists view it as an indicator for the direction of existing-home sales in subsequent months.

Key details: Compared with a year earlier, transactions were down by 37.8%.

On a monthly basis, pending sales fell in all four major U.S. regions, led by the Northeast, where the index fell by 7.9%, followed by the Midwest, the South and the West.

But pending home sales fell the most since last November in the West, by 45.7%.

Pending home sales have fallen in all but one month in 2022.

Big picture: The housing market continues to stumble through 2022, as elevated mortgage rates keep buyers out of the market.

Buyers are finding it hard to find an existing home for sale, as sellers hold on to their homes tied to ultra-low mortgage rates.

November’s data is also tied to the period of time when mortgage rates were above 7%.

What the realtors said: “With mortgage rates falling throughout December, home-buying activity should inevitably rebound in the coming months and help economic growth,” NAR Chief Economist Lawrence Yun said.

What they’re saying: “Housing markets have entered a winter freeze,” George Ratiu, senior economist at Realtor.com, said in a statement.

“With prices for existing homes still elevated … and mortgage rates above 6%, homebuyers are finding much of today’s real estate landscape inaccessible,” he added.

Ratiu estimated that monthly mortgage payment for a median-priced home has gone up by $780 since last year.

Market reaction: The Dow Jones Industrial Average DJIA, -1.10%

and the S&P 500 SPX, -1.20%

were mixed in early trading on Wednesday. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.872%

rose above 3.8%.

(Realtor.com is operated by News Corp subsidiary Move Inc., and MarketWatch is a unit of Dow Jones, also a subsidiary of News Corp.)

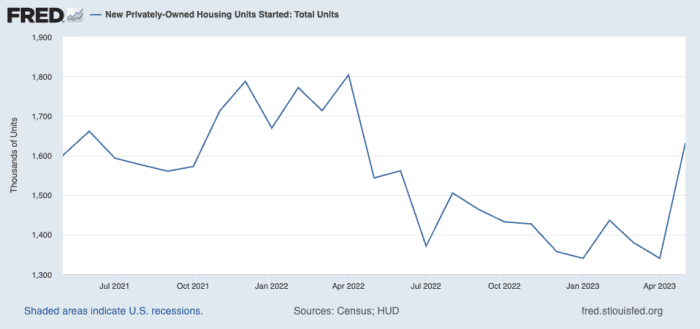

The numbers: U.S. new home sales rose 5.8% to a seasonally-adjusted rate of 640,000 in November, from a revised 605,000 in the prior month, the Commerce Department reported Friday.

The November sales figure beat analyst estimates. Analysts polled by the Wall Street Journal had forecast new home sales to come in at 600,000 in November.

The sales of new homes are below a peak of 1.04 million in August 2020.

Year-over-year, new home sales are still down by 15.3%.

New home sales rose a revised 8.2% to 605,000 in October, compared with the initial estimate of a 7.5% increase to 632,000.

The new home sales data are volatile month-on-month and are often revised.

Key details: The median sales price of a new home sold in November was $471,200, down from $484,700 in October.

The supply of new homes for sale fell by 7.5% between October and November, equating to an 8.6-month supply.

Regionally, the West led the U.S. in the number of new homes sold, with new homes sold surging by 27.6%, followed by the Midwest.

Sales of new homes dropped in the Northeast and the South this November.

Big picture: 7% mortgage rates didn’t put a damper on new home sales, as seen in today’s report.

New home sales jumped in November, likely as buyers wanted to take advantage of incentives that builders are offering, from mortgage rate buydowns to price cuts.

But with rates coming back down since, expect housing data to improve further.

What are they saying? “I suspect that builders are much more motivated sellers (especially given the surge in financing costs) than current homeowners, who do not want to part with their 3% or lower mortgages,” Stephen Stanley, chief economist at Amherst Pierpont, wrote in a note. “This may explain why new home sales are rising while existing home sales plunge. ”

But overall, sales are still weaker than usual: Stanley noted that combined existing and new home sales in November fell to the lowest level since 2011.

Market reaction: The Dow Jones Industrial Average DJIA, +0.53%

and the S&P 500 SPX, +0.59%

were down in early trading on Friday. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.749%

rose above 3.7%.

Shares of builders, including D.R. Horton, Inc. DHI, -1.29%,

Lennar Corp LEN, -0.46%,

PulteGroup Inc. PHM, -0.52%,

and Toll Brothers Inc. TOL, -0.33%

traded lower during morning trading.

The numbers: U.S. pending home sales fell 4.6% in October, the fifth straight monthly decline, the National Association of Realtors said Wednesday.

Economists polled by the Wall Street Journal expected pending home sales to fall 5.5%.

The index captures transactions where a contract has been signed, but the home sale has not yet closed.

Key details: On a year-on-year basis, pending home sales were down a sharp 37%.

Sales fell in three of the four regions, with the Midwest registering an increase.

Big picture: Sales have stalled as mortgage rates have jumped, making houses less affordable. Pending home sales are a leading indicator for the sector. Some economists think that buyers might return to the market as mortgage rates have plateaued.

The numbers: Existing-home sales fell 5.9% to a seasonally adjusted annual rate of 4.43 million in October, the National Association of Realtors said Friday. Compared with October 2021, home sales were down 28.4%.

Economists polled by the Wall Street Journal had expected an decrease to 4.37 million units.

The level of sales is the lowest since December 2011 excluding the 2020 pandemic.

This is also the ninth straight monthly decline in sales, the longest streak on record.

Key details: The median price for an existing home was $379,100 up 6.6% from October 2021.

But price gains are decelerating. Prices were up over 20% on a year-on-year basis earlier this year.

Housing inventory fell 0.8% to 1.22 million units in October. Unsold inventory sits at a 3.3-month supply at the current sales pace, up from 3.1 months in September and 2.4 months a year ago.

A 6-month supply of homes is generally viewed as indicative of a balanced market.

Sales declined in all regions of the country.

Big picture: Home sales have dropped as mortgage rates have risen sharply and affordability has dropped.

Softer inflation data in October have led to a drop in mortgage rates, which could lead for a floor on sales.

At the same time, Federal Reserve officials may pencil in a “peak” interest rate above 5% at the policy meeting next month.

Economists see home prices have further to fall in this market.

What the NAR is saying: Home sales have been very low and the softness could continue for a few months. But sales could pick up early next year if the mortgage rate has peaked, said Lawrence Yun, chief economist at the NAR.