Home prices have climbed much faster than incomes over the last several years, up roughly 53% since 2019 compared with about a 24% increase in median household income.

First-time homebuyers make up a much smaller share of the market than in the past. In 2025, they represented just about 21% of buyers, down from 44% in 1981, and the median age for first‑timers has climbed to 40.

Social and household patterns are shifting too. More young adults ages 18–24 are living with their parents, fewer couples have children, and more people are choosing to live alone. These demographic trends are part of why builders are adjusting what they put into new homes.

“You can’t have housing prices rise that significantly for a sustained period of time and not experience housing affordability issues,” said Rose Quint, NAHB assistant vice president of survey research. “Clearly this will have implications on the size of homes we build and the types of amenities we include.”

In terms of house design, the median home size hasn’t changed much recently, but builders are adding features buyers care about. That includes flexible spaces like drop zones and multi‑purpose rooms and more homes with electric vehicle charging stations.

Builders are also trying different ways to address affordability. Sixty-seven percent are offering sales incentives, and roughly 41% have cut home prices compared with past years.

What buyers want varies by price point, according to the report. Entry‑level buyers tend to focus on value and practical layout needs, while higher‑end buyers often look for extra bedrooms and bathrooms, home offices, energy‑efficient features and community amenities.

Across income levels, outdoor space keeps coming up as something everyone values. Builders are finding creative ways to include patios, rooftop decks or other outdoor living areas, even in smaller homes.

There’s also movement toward offering a broader mix of housing types. Developers are looking at adaptive reuse projects and mixed‑density communities with townhomes or condos to give buyers more options.

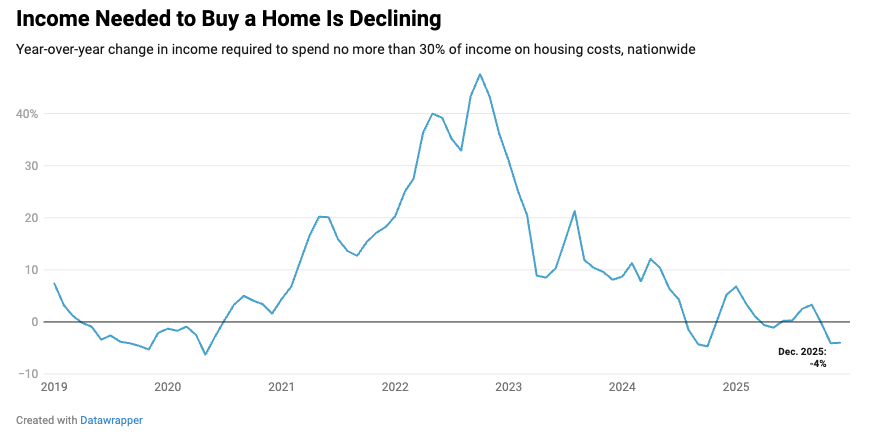

The amount Americans needed to earn declined 4% year over year in December, from $115,870 to $111,252, marking the second month in a row of declines after rising in nearly every month for five years in a row. Income needed to buy a home peaked at $122,000 in June.

Redfin attributed the improvement to lower mortgage rates and slowing home-price growth. The median home sale price in December was $426,747, up slightly from December 2024, but mortgage rates have fallen from 7% last year to about 6.1% now. Those factors brought the median monthly mortgage payment down from $2,800 to $2,675.

“The housing affordability crisis is showing signs of easing as costs come down slightly but meaningfully, opening the door for more Americans to make the jump to homeownership,” said Chen Zhao, Redfin’s head of economics research. “While housing remains historically expensive, the trajectory is finally starting to reverse, with the door to buying a home opening a bit wider rather than closing tighter. But while affordability is improving, Americans are contending with other obstacles on the road to buying a home, like nerves about layoffs and economic uncertainty.”

Redfin considers a home affordable if a buyer taking out a mortgage spends no more than 30% of their income on monthly housing payments. Redfin based its analysis on median home sale prices, prevailing mortgage rates and property tax payments.

Courtesy of Redfin.

While affordability is improving, the typical U.S. household does not earn enough to afford the median-priced home. The typical American household earns just $86,185, about $25,000 less than needed, according to the report.

On a local level, affordability is improving in 37 of the 50 largest U.S. cities, led by Dallas, where required earnings fell 7.4%, and followed by Sacramento, California, and Jacksonville, Florida, where the amount needed was down 6.8% and 5.9%, respectively.

On the flip side, the amount homebuyers needed to earn actually increased in some cities, led by Detroit (up 3.6%) and followed by Chicago (3.5%) and St. Louis (3%)

The typical household could actually afford to buy a median-priced home in only 12 metros, led by Pittsburgh, where buyers needed to earn $66,168, and the typical household earned $82,188, followed by St. Louis, where $73,984 is needed, and the typical household earned $87,471, and Cleveland, where $66,725 was needed, and the typical income was $76,912.

Long Island business confidence declined this year after a post-2024 election high.

Affordability and housing costs remain major concerns for local leaders.

Survey included 311 business leaders.

Last year there was a measurable uptick in confidence among Long Island business leaders. This year that confidence dipped. Some of that decline reflects ongoing challenges, including long-standing affordability issues and, more recently, broader uncertainty. Local leaders met Thursday morning at the Crest Hollow Country Club in Woodbury to better understand the factors that are shaping Long Island’s economy.

The gathering centered on the “Long Island Economic Survey Results Launch,” hosted by PKF O’Connor Davies in partnership with the Siena Research Institute (SRI). The results provided insights via 311 Long Island business leaders who participated in the survey, helping to identify emerging trends, challenges and opportunities.

The event included a panel moderated by PKF O’Connor Davies Partner Jeffrey Davoli. The survey’s results were delivered by Don Levy, director of SRI. Levy was also part of a panel discussion that included U.S. Reps. Nick LaLota (R-Amityville) and Tom Suozzi (D-Glen Cove), as well as Stacey Sikes, vice president of government affairs and communications at Long Island Association.

Business confidence slipped from a “post-2024 election high,” prompting leaders to take a more cautious approach, according to Levy.

“Fifty-four percent of the businesses we spoke to a year ago predicted that the year ahead was going to be better,” Levy said. “They were excited.”

Those business leaders had planned to invest in fixed assets, add employees and see increased revenue and profitability.

But, Levy said, “the year did not live up to their expectations.”

Expectations for both the Long Island and national economies, according to the survey, declined sharply, with pessimism about the Long Island economy more than doubling from the year prior.

Volatility, including tariffs and energy, may play a role in impacting business confidence, LaLota said.

“What government does or doesn’t do, I think, can help or hurt you, and just having stability in those areas” can be important to businesses as they look at revenues and the ability to hire, he said.

Uncertainty around tariffs are a big concern for owners, Suozzi said, adding that they are worried about upcoming changes to the current business environment.

“I’ve talked to so many businesses that ordered things from overseas. While it was on the boat, the tariffs went up,” Suozzi said. “They got hit when they got to the dock with a $500,000 bill that they didn’t plan for. People can’t function in that environment. That affects the confidence. That affects your desire to say yes, I’m going to invest in this.”

Also impacting confidence is affordability, something that’s now part of a national discussion, although Long Island has been grappling with the challenge, especially housing costs, for decades.

Affordability is even seeping into succession planning. Davoli pointed out that, according to the survey, “70 percent express concern, yet only 27 percent have a structure plan in place.”

Sikes said she wasn’t surprised that succession planning is an issue, especially at a time when the population is getting older.

“We already have a challenge keeping young people on Long Island,” she said. “A median home price is $800,000 on Long Island. How can any young person afford a down payment, a closing cost, the mortgage and the taxes?” The region’s high cost of living makes it difficult for businesses to bring in and retain the next generation of leaders.

When it comes to adding housing and navigating zoning, LaLota, said, “local control is always best. The state and the feds should not have a role in that.”

Suozzi said that 95 percent of housing should be single family homes, but recommended that 5 percent, or less, should include housing in downtowns. “We have to build places where young people can afford to live,” but still “preserve our suburban quality of life in the process,” he said.

Both Suozzi and LaLota spoke about bringing tax dollars back to New York State, adding that at the federal level, the state only gets back 85 cents for every dollar it sends to Washington, DC.

Suozzi pointed out that New York State is more expensive than Florida and Texas because New York has the lowest rate of uninsured adults and children, while the two other states have the highest. New York also pays teachers more than many other states.

New York, he said, has tremendous wealth, “but we have to get that wealth back to our state to try and reduce our costs. Or we’re going to lose this population fight because people are moving to these southwestern and southeastern lowest tax states, and we’re not keeping up with them.

“Federal tax policy can help with that,” he said. “But it’s going to be a tough fight.”

Gov. Hochul’s State of the State outlined the “Let Them Build Agenda” to reform SEQRA review requirements.

Proposals include exempting certain infrastructure and community projects from SEQRA review.

A mandatory two-year deadline would bring certainty to Environmental Impact Statement reviews.

New digital tools and permitting modernization aim to reduce delays and investor risk for development projects.

In her recent State of the State address, Gov. Kathy Hochul laid out a very aggressive agenda to help make New York more affordable for its residents. One area was for increased state investment in housing, and while there was no mention of any tax or other financial incentives for developers in New York, she did propose what she is calling her “Let Them Build Agenda.” This initiative seeks to provide common-sense reforms to the State Environmental Quality Review Act (“SEQRA”). If these changes come to fruition, it would help accelerate certain development projects here on Long Island by significantly reducing costs and time to check the state environmental box that all municipalities are required to manage.

Such proposals include:

The acceleration of critical infrastructure projects: The governor’s proposal will include eliminating SEQRA review for Type II projects. These include clean water infrastructure projects, green infrastructure, public parks, recreational bike paths, and new or renovated childcare centers.

Establishing clear deadlines for local communities: As every developer knows, the timing for SEQRA review is critical to obtain but is a “wild card” as to how long that process will take. The governor’s proposal is to make a two-year deadline mandatory for completion of the Environmental Impact Statement to the issuance of the final agency decision. Here on Long Island, many communities resist density increases, and municipal boards can use SEQRA’s flexibility to impose additional requirements or delay approvals, even for projects that would meet standard zoning. Clear state-mandated deadlines will bring more certainty to these projects.

Modernizing permitting processes: It has been decades since the state agencies have updated their processes and technologies used to review and approve environmental permits. Gov. Hochul is directing all agencies involved to give a full report no later than Sept. 1, 2026, as to how to best accelerate reviews. She also announced that the New York State Department of Environmental Conservation will launch “Smart Access,” which is a platform that enables applicants to track and monitor the progress of their application.

SEQRA has long been a thorn in the side of developers and a large risk for investors involved with the projects. Time and time again, projects with no negative impact on the environment have been delayed indefinitely because of administrative delays, costing valuable time and money. Those projects which do have an environmental impact are met with not only these administrative delays but also with endless hearings and Article 78 proceedings, causing developers to look elsewhere for their projects. While more incentives and reforms are needed to keep these projects moving on Long Island, streamlining and modernizing the SEQRA process will surely go a long way to helping critical projects move forward in the region.

Joe Campolo is the founder and CEO of Strata Alliance, and founder and chairman of the Strata Foundation. He also serves as managing partner of Campolo, Middleton & McCormick, LLP—all of which are based in Ronkonkoma.

President Trump’s pledge to ban large investment firms from buying single-family homes dinged the stock prices of some of the biggest institutional landlords, but the impact it would have on the housing affordability crisis is debatable.

Observers noted that major investors like Blackstone, Invitations Homes and American Homes 4 Rent own only about 1% of the single-family homes in the United States, and their holdings are concentrated in the South and Sunbelt, so the impact on overall U.S. home prices would vary widely by geography. Additionally, in the markets with relatively high concentrations of institutional ownership, home prices are already declining.

“The administration’s proposed ban on large institutional investors buying single-family homes aims to curb Wall Street’s role in housing, but evidence shows little connection between institutional ownership and affordability,” Jonathan Miller, president and CEO of property appraisal firm Miller Samuel, wrote in his HousingNotes blog.

“Their holdings are concentrated mostly in the South and Sunbelt, where inventory is relatively high and home prices have actually fallen, undermining claims that these investors drive housing costs higher. With most investor-owned homes held by small, local landlords, the proposed restriction is unlikely to meaningfully improve affordability or housing supply.”

Nevertheless, others expressed optimism that a ban would indeed have an impact in markets with high levels of institutional ownership.

“Because the Dallas–Fort Worth market has long been a hotspot for institutional ownership, any new restrictions from the Trump administration would likely be felt here sooner and more acutely than in markets with lower investor activity,” said Todd Luong of REMAX DFW Associates. “In many price ranges, especially entry-level and mid-priced homes, buyers have been competing against all-cash offers from large investment groups. Reducing that competition could give local buyers a better chance to secure a home with less pressure and more favorable pricing.”

Details about the ban have been scarce, and many questions remain. In a post on his Truth Social site announcing the proposed ban, Trump said, “I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it. People live in homes, not corporations.”

He added that he would provide more information on the proposal when he speaks at the upcoming World Economic Forum in Davos, Switzerland, in two weeks.

In a subsequent post, Trump said he would instruct Fannie Mae and Freddie Mac to use a purported $200 million in cash holdings to purchase mortgage bonds to bring mortgage rates down.

Timing of that proposal is everything, according to Victor Kuznetsov, managing director and co-founder of Imperial Fund Asset Management.

“In the short term, expect mortgage rates to level tighter than 2025 averages, but investment bank researchers tend to agree that most of these [mortgage-backed security] purchases have already been priced into rates, so the timing of the [government-sponsored enterprises’] MBS purchases will be important,” Kuznetsov said. “Will the GSEs purchase $200 [billion] over 2026’s calendar year, spreading out the tightening effects over a full year? Details on deployment timing have been sparse so far.”

According to the housing blog ResiClub, the most significant questions about the ban include:

What constitutes an “institutional investor”?

Would the investors be required to sell existing properties, or would they just be prohibited from purchasing additional ones?

Would the ban apply to existing properties scattered throughout a market, or also to build-to-rent development?

What would happen to existing tenants if the owners were forced to sell their homes?

In the end, industry observers agree that the ban would have a limited effect on overall housing affordability, and the key to bringing down costs is by increasing inventory.

“The first thing to do is build more housing starting now,” Miller said.

Gov. Gavin Newsom is set to deliver his final State of the State address as the state’s governor this Thursday.Newsom will host the address at the state Capitol in front of a joint session of the Legislature, the first time he has done so since 2020. In recent years, he has opted for writing letters to the Legislature, releasing pre-recorded messages or touring across the state to issue new policies and initiatives.Ahead of the address, the governor’s office offered brief outlines of themes Newsom is expected to touch upon. One topic includes homelessness and California’s efforts to resolve the state’s mental health crisis.Housing affordability, education and investment in public schools are other topics outlined. The governor also plans on addressing public safety, violent crime, and theft across the state, and the various levels of law enforcement working to handle those issues.Another major topic Newsom is expected to address is climate initiatives and how California’s policies have implications both nationally and globally.Newsom’s office also shared that Newsom will convey that California is a stable democracy, an economic engine with conscience, and a “functioning alternative to Donald Trump’s federal dysfunction.” The State of the State address begins at 10:30 a.m. Thursday.Because there is a two-term limit on holding the office of California governor, Newsom will not be able to run for a third term.See more coverage of top California stories here | Download our app | Subscribe to our morning newsletter | Find us on YouTube here and subscribe to our channel

SACRAMENTO, Calif. —

Gov. Gavin Newsom is set to deliver his final State of the State address as the state’s governor this Thursday.

Newsom will host the address at the state Capitol in front of a joint session of the Legislature, the first time he has done so since 2020. In recent years, he has opted for writing letters to the Legislature, releasing pre-recorded messages or touring across the state to issue new policies and initiatives.

Ahead of the address, the governor’s office offered brief outlines of themes Newsom is expected to touch upon. One topic includes homelessness and California’s efforts to resolve the state’s mental health crisis.

Housing affordability, education and investment in public schools are other topics outlined. The governor also plans on addressing public safety, violent crime, and theft across the state, and the various levels of law enforcement working to handle those issues.

Another major topic Newsom is expected to address is climate initiatives and how California’s policies have implications both nationally and globally.

Newsom’s office also shared that Newsom will convey that California is a stable democracy, an economic engine with conscience, and a “functioning alternative to Donald Trump’s federal dysfunction.”

The State of the State address begins at 10:30 a.m. Thursday.

Because there is a two-term limit on holding the office of California governor, Newsom will not be able to run for a third term.

An empty lot at 3901 Elati Street in Fox Island, Dec. 24, 2025.

Kyle Harris / Denverite

The developer Fox Street Investments spent millions of dollars buying 3901 North Elati Street and designing a 20-story building with 400 apartments in Globeville.

A few years later, the dusty lot sits empty in that slice of Globeville known as Fox Island. The promise of housing has yet to be fulfilled. And the company is suing the city of Denver.

A complaint the company filed in U.S. District Court on Tuesday argues the city is preventing the developer from building much-needed housing on the three-quarters of an acre lot with “arbitrary” rules and mandates.

“For decades, the City has failed to invest in sufficient public traffic infrastructure in the Globeville neighborhood, one of Denver’s most economically disadvantaged neighborhoods,” the complaint states. “Instead, the City adopted development rules within Fox Island … that attempt to completely and unlawfully shift this burden to the last-in-time developers trying to build housing in the neighborhood.”

Denver Community Planning and Development and the City Attorney’s Office declined to answer Denverite’s questions about the complaint since it’s pending litigation.

The requirements for the developer to improve traffic infrastructure are beyond the scope of the project and address needs far beyond what the new development will create, the complaint argues.

“The Rules are unconstitutionally vague and provide unidentified City bureaucrats with apparently unlimited discretion to condition development of the Property on FSI’s agreement to construct public traffic infrastructure improvements that are not directly linked to any resulting impacts from the development of the Property and that are completely disproportionate to such impacts,” the complaint states.

The company estimates that without the rules, the land would be worth $20 million. As is, with current rules, it’s “essentially worthless.”

The city has long negotiated with developers to add amenities that will benefit the public good to their projects: affordable housing, landscaping and more.

But the developer argues the city has gone too far and is interfering with the city’s own goals of increasing housing stock.

The company is asking the court to declare the rules unlawful and for the city to financially compensate the company so it can build the project it has set out to complete.

Some might say the new Aurora Regional Navigation Campus that opened recently in a former 255-room hotel is undergirded by one of humanity’s seven deadly sins — envy.

The intent is to turn that feeling into a motivational force. For his part, Mayor Mike Coffman prefers to refer to the three-tiered residential system at the homeless navigation center as an “incentive-based program” — one that awards increasingly comfortable living quarters to those showing progress on their journey to self-sufficiency.

“The notion here is (that) different standards of living act as an incentive,” Coffman said in early November during a ribbon-cutting ceremony for the campus, which occupies a former Crowne Plaza Hotel at East 40th Avenue and Chambers Road. “The idea is to move up the tiers into much better living situations.”

Clients in the new facility, which opened its doors on Nov. 17, start at the bottom with a cot and a locker. They can eventually migrate to a hotel room, with a locking door and a private bathroom.

But that upgrade comes with a price.

“To get a room here, you have to be working full time,” Coffman said.

It’s an approach that the mayor says threads the needle between housing-first and work-first, the two prevailing strategies for addressing homelessness today. The housing-first approach emphasizes getting someone into a stable home before requiring employment, sobriety or treatment. A work-first setup conditions housing on a person finding work and seeking help with underlying mental health and addiction problems.

“We’re providing a continuum of services that starts with an emergency shelter,” said Jim Goebelbecker, the executive director of Advance Pathways.

Advance Pathways, the nonprofit group that ran the Aurora Resource Day Center before its recent closure, was chosen through a competitive bidding process to operate the new navigation campus in Aurora — with $2 million in annual help from the city. Goebelbecker said the tiered approach at the new facility “taps into a person’s motivation for change.”

The Aurora Regional Navigation Campus’ debut nearly completes a mission that has been in the works for more than three years. It is the fourth — and penultimate — metro Denver homeless navigation center to go online since the Colorado General Assembly passed House Bill 1378 in 2022.

The bill allocated American Rescue Plan Act dollars to stand up one central homeless navigation center. The plan has since shifted to five smaller centers, with locations in Aurora, Lakewood, Boulder, Denver and Englewood. The Colorado Department of Local Affairs in late 2023 approved $52 million for the centers. The final center, the Jefferson County Regional Navigation Campus in Lakewood, is undergoing renovations and will open next year.

Aurora’s center, with 640 beds across its three tiered spaces, is by far the largest of the five facilities.

Cathy Alderman, a spokeswoman for the Colorado Coalition for the Homeless, said the opening of Aurora’s navigation campus is “a really big deal.” Aside from serving its own clientele, she expects the center to send referrals to the coalition’s newly opened Sage Ridge Supportive Residential Community near Watkins, where people without stable housing go to address their substance-use disorders.

“A person can go to one place and get multiple needs met,” Alderman said, referring to the array of job, medical and addiction treatment services that give homeless navigation centers their name. “We are excited that the new campus is now up and running.”

The new Aurora Regional Navigation Campus, operated by Advance Pathways, photographed in Aurora on Thursday, Nov. 6, 2025. (Photo by Andy Cross/The Denver Post)

‘How do I move up?’

Walking into the Aurora Regional Navigation Campus feels like walking into, well, a hotel.

The swimming pool was removed during renovation, as was a water fountain in the lobby. Everything else stayed, including beds, bedding, furniture — even a stash of bottled cocktail delights. But not the alcohol to go with it.

“They left everything, down to the forks and knives and a wall of maraschino cherries,” said Jessica Prosser, Aurora’s director of housing and community services, as she walked through the hotel’s industrial kitchen.

The kitchen, which was part of the $26.5 million sale of the Crowne Plaza Hotel to Aurora last year, was a godsend to an operation tasked with serving three meals a day to hundreds of people. The city spent another $13.5 million to renovate the building.

“To build a new commercial kitchen is a half-million dollars, easy,” Prosser said.

The layout of the navigation center was deliberate, she said. The hotel’s convention center space is now occupied by Tier I and Tier II housing. The first tier is made up of nearly 300 cots, divided by sex. There are lockers for personal belongings and shared bathrooms. Anyone is welcome.

On the other side of a nondescript wall is Tier II, which is composed of a grid of 114 compartmentalized, open-air cubicles with proper beds and lockable storage. The center assigns residents in this tier case managers to help them treat personal challenges and get on the path toward landing a job.

The Tier II “Courage” space, which offers overnight accommodation for people who are working on recovery, employment and housing pathways at the new Aurora Regional Navigation Campus in Aurora, on Thursday, Nov. 6, 2025. (Photo by Andy Cross/The Denver Post)

Tier III residents live in the 255 hotel rooms. They must have a full-time job and are required to pay a third of their income to the program. Residents in this tier will typically remain at Advance Pathways for up to two years before they have the skills and stability to find housing on the outside, Goebelbecker said.

People living in the congregate tiers can house their dogs in a pet room, which can accommodate 40 canines. (No cats, gerbils or fish). The center also doesn’t accept children. Around 60 staff members, plus 10 contracted security personnel, will work at the facility 24/7.

Shining a bright light on the path forward and upward inside the facility — the windows of some of the coveted private rooms are fully visible from the lobby — is an “intentional design feature,” Prosser said.

“How do I move up?” she mused, stepping into the shoes of a resident eyeing the facility’s layout. “How do I get in there?”

The Tier III “Commitment” space, which provides private rooms that will serve people who are in the workforce and are building towards financial independence, seen at the new Aurora Regional Navigation Campus in Aurora on Thursday, Nov. 6, 2025. (Photo by Andy Cross/The Denver Post)

It’s a system that demands something of the people using it, Coffman said, while at the same time providing the guidance and help that clients will need.

“This is not just maintaining people where they are — this is about moving people forward,” the mayor said.

The approach is familiar to Shantell Anderson, Advance Pathways’ program director. She told her life story during the ribbon-cutting ceremony, bringing tears to the eyes of some in the audience.

A native of Denver’s Park Hill neighborhood, Anderson fell in with the wrong crowd. She became pregnant at 15 and got hooked on cocaine. She spiraled into a life on the streets that resulted in her children being sent to an aunt for caretaking.

But through treatment and by intersecting with the right people, she recovered. She earned a nursing degree and worked at RecoveryWorks, a nonprofit organization that operated a day shelter in Lakewood, before taking the job at Advance Pathways.

The Tier I “Compassion” emergency shelter, which provides immediate short-term shelter for those in need at the new Aurora Regional Navigation Campus in Aurora on Thursday, Nov. 6, 2025. (Photo by Andy Cross/The Denver Post)

“This is a system that honors people’s dignity,” Anderson said, her voice heavy with emotion.

In an interview, she said assuming the burden to improve her situation was critical to her transformation.

“I actually did that — no one gave me anything,” said Anderson, 48. “If it was handed to me, I didn’t appreciate it.”

How much responsibility to place on the people being helped by such programs is still a matter of intense debate by policymakers and advocates for homeless people. The housing-first approach favored by Denver and many big cities across the country is anchored in the idea that work or treatment requirements will result in many people falling through the cracks and staying outside, particularly those who face mental-health challenges.

The Bridge House in Englewood, one of the five metro area navigation centers, follows a “Ready to Work” model that is similar to that of the upper tiers of the Aurora Regional Navigation Campus.

Opened in May, the Bridge House has 69 beds. CEO Melissa Arguello-Green said the organization asks its clients (called trainees) to put skin in the game by landing a job with Bridge House’s help and then contributing a third of their paycheck as rent.

“We help them find employment through our agency so they can leave our agency,” she said. “We’re looking for self-sufficiency that will get people off system support.”

Arguello-Green said she would like to see more coordination between the metro’s five navigation centers, though she acknowledged it’s still in the early going.

“We’re missing that come-to-the-table collaboration,” she said.

Advance Pathways volunteer outreach coordinator Evan Brown organizes the clothing bank before the Aurora Regional Navigation Campus’ grand opening ceremony in Aurora on Thursday, Nov. 6, 2025. (Photo by Andy Cross/The Denver Post)

Homeless numbers still rising

Shannon Gray, a spokeswoman for the Colorado Department of Local Affairs, said her department had started convening quarterly in-person meetings across the locations.

“While each navigation campus is unique and reflects community-specific strategies, they are all a part of a regional effort to bring external partners together onsite to provide needed services and referrals,” Gray said. Together, they are “building towards a larger regional system to connect homeless households to a larger network of opportunities.”

The centers are permitted to “tailor their approach to their unique needs and vision,” she said. While Englewood and Aurora use a tiered system, Gray said, the other three centers don’t.

“It is important to understand that DOLA serves as a funder for these regional navigation campuses — we do not oversee their operation or maintenance,” she said.

Denver’s navigation center, which opened in December 2023 in a former DoubleTree Hotel on Quebec Street, offers 289 rooms to those in need, said Julia Marvin, a spokeswoman for the city’s Department of Housing Stability.

She called the facility an “integral component of Denver’s All in Mile High homelessness initiative,” Mayor Mike Johnston’s ambitious effort to appreciably reduce homelessness in the city. The center is just one of several former hotels and other shelter sites in the system.

Earlier this year, his administration cited annual count numbers showing a 45% decrease in the number of people sleeping on the streets since 2023 — dropping from 1,423 to 785 people, despite overall homelessness continuing to increase in that time.

In fact, homelessness numbers are still going in the wrong direction across the seven-county metro, per the latest Point-in-Time survey from the Metro Denver Homeless Initiative, which captures a one-night snapshot. The January count revealed that 10,774 people were homeless on the night of the survey, up from 9,977 in the count the year before.

Anderson, the Advance Pathways program director, said the new Aurora facility was opening at just the right time. Despite a recent calming in runaway home values in metro Denver, the $650,000 median price of a detached home in October still demarcated a housing market that was out of reach for many.

“I am excited,” Anderson said of the Aurora navigation campus’ debut. “I’m waiting for people to walk through the door and start the next chapter of their journey.”

A cash-strapped school district that’s looking to unload a shuttered elementary school.

A nonprofit human services agency that’s in need of a bigger home as it serves more than 60,000 households a year.

And a judge who’s telling Colorado’s fifth-largest city not to make any moves on the whole situation — a complex deal that would allow the agency to move into the school — until she can determine whether everything is on the up and up.

That’s the strange nexus at which Lakewood, Jeffco Public Schools and The Action Center have found themselves after their proposed real estate deal was challenged in court by a former Lakewood city councilwoman who thinks the whole arrangement is “taking place in secret.”

“Government should have to do this in a way that’s transparent and above board — and includes the public in this kind of decision-making,” said Anita Springsteen, who’s also an attorney. “I think it’s unethical. I think it’s wrong.”

The deal on the table calls for Lakewood to purchase Emory Elementary — which closed three years ago because of declining enrollment — from Jeffco Public Schools for $4 million. At the same time, the city would buy The Action Center’s existing facility on West 14th Avenue for $4 million.

The Action Center, in turn, would buy Emory from the city for $1 million when the organization, which for more than a half-century has provided free clothing and food, family services and financial assistance to those in need, moves to its new home in the former school on South Teller Street.

The core problem, Springsteen says, is that Lakewood did not properly announce two September 2024 executive sessions during which officials discussed details of the deal in private. In a lawsuit, she accused the city of violating Colorado’s open meetings law, which requires governments to state, in advance and “in as much detail as possible,” what will be discussed behind closed doors “without compromising the purpose for the executive session.”

Jefferson County District Judge Meegan Miloud had enough questions last week about how Lakewood gave public notice of its executive sessions that she imposed a temporary restraining order on the City Council — forbidding it from voting on three ordinances that would authorize the deal to move forward.

The council had been scheduled to consider the measures Monday night.

Miloud said the city’s executive session notices on the council’s September 2024 agendas were “so vague that the public has no way of identifying or discerning what is being negotiated or what property is being assessed.”

On Tuesday morning, the judge conducted a hearing on the matter but did not make a ruling. She called another hearing for next Monday and said in a new order that her injunction remains in effect.

The fast-moving situation has Lakewood playing defense. A special council meeting that had been set for Wednesday night — to once again put the ordinances up for a council vote — will now have to be rescheduled, city spokeswoman Stacie Oulton said.

Lakewood, she contended, has been open throughout the process.

“The public process has included updates from the city manager during public City Council meetings, and the city has followed the public notification process for these agenda items,” she told The Denver Post in an email this week. “Additionally, the proposed end user of the property, the Action Center, has had several public community meetings about its proposal.”

Anita Springsteen, a lawyer and former Lakewood city councilwoman, is leading a challenge to a complex land deal between the City of Lakewood, Jeffco Public Schools and The Action Center that would bring the humans services nonprofit to the former Emory Elementary School in Lakewood on Oct. 28, 2025. She posed for a portrait outside the former school. (Photo by RJ Sangosti/The Denver Post)

Questions about meetings, market value

Jeff Roberts, the executive director of the Colorado Freedom of Information Coalition, said it was “unusual” for a judge, via a temporary restraining order, to preempt a city council from casting a vote.

But case law, he said, makes it clear that governing bodies in Colorado must provide as much detail as possible when they announce closed-door sessions — short of disclosing or jeopardizing strategies and positions that are crucial in real estate negotiations.

“In general, an announcement that doesn’t give any indication of the topic is not enough information for the public,” Roberts said. “In most cases — and that’s why it’s in the law — you must tell the public what the executive session is about.”

That standard, he said, was upheld by the Colorado Court of Appeals in 2020, when it ruled that the Basalt Town Council violated the state’s open meetings law several times in 2016 by not properly announcing the topic of private deliberations it would be having regarding a former town manager.

In the Lakewood school matter, the alleged open meetings violations are not the only thing that bothers Springsteen. She objects to the structure of the proposed real estate transaction, saying it would be a sweetheart deal for The Action Center and a waste of money for taxpayers.

“They are stealing money out of our pockets,” said Springsteen, who served on City Council from 2019 to 2023.

Lakewood, she said, would be underpaying for the 17-acre Emory Elementary School parcel, overpaying for The Action Center’s current facility and basically giving the school property away to the nonprofit.

“For the city to not intend to own the property, but to buy it on behalf of a nongovernmental organization — when did we become an agent for other agencies?” Springsteen said.

According to the Jefferson County assessor’s site, The Action Center’s buildings on West 14th Avenue have a total value of about $2 million, while the city has proposed purchasing them for double that. The assessor’s office lists Emory Elementary as having a total value of up to $12 million.

Springsteen said she is flummoxed by the Jeffco school district’s willingness to sell the elementary school to Lakewood for a third of that valuation.

“What bothers me most is the way Jeffco schools is handling this,” she said. “The district didn’t even have a school resource officer at Evergreen High School because of budgetary issues.”

A spokesperson for Jeffco schools said a decision on whether to sell Emory Elementary to Lakewood hadn’t been made yet. That vote, by the district’s school board, is expected Nov. 13.

Raven Price picks out food at The Action Center’s food bank in Lakewood on Oct. 28, 2025. (Photo by RJ Sangosti/The Denver Post)

‘We need to bring this into our community’

Pam Brier, the CEO of The Action Center, said property values don’t tell the full story.

“There are many instances locally and nationally of municipalities helping to support the affordable acquisition of properties for organizations like The Action Center — who are serving such a critical need in our community,” she said, “and ultimately saving taxpayer money by helping to meet people’s basic needs.”

On Wednesday, she provided The Denver Post a May 2024 appraisal done by Centennial-based Masters Valuation Services that valued the organization’s current facility — made up of a 14,960-square-foot building and a 15,540-square-foot building — at $4 million.

Her organization, Brier said, serves 300 households a day. It provides a free grocery and clothing market, financial assistance, free meals, family coaching, skills classes and workforce support to people who are down on their luck.

“As public dollars dwindle, our work is more important than ever,” she said. “Without organizations like The Action Center to provide food, clothing and other critical support, individuals and families fall into crisis, needing assistance that will cost taxpayers and cities so much more.”

Oulton, the Lakewood city spokeswoman, said it was not unusual for cities and counties across metro Denver to “provide financial support in a variety of ways to nonprofits that serve their communities.”

“Additionally, Jeffco Public Schools has clearly communicated to the city that the district views the value of this project in more than the dollars involved, because the district’s priority has been to see former schools used in a way that will continue providing services and support to Jeffco Public Schools students and their families,” Oulton said.

Diana Losacco, a 48-year resident of Lakewood who lives about a mile from the Emory site, was one of more than three dozen people who urged the city to pursue the purchase and sale of the school to The Action Center on the Lakewood Speaks website.

Raven Price and her 4-year-old son, Gabriel Luna, head home with a wagon full of food they selected from The Action Center’s food bank in Lakewood on Oct. 28, 2025. (Photo by RJ Sangosti/The Denver Post)

“This will provide opportunities to people to become self-sufficient, which will provide significant financial savings for our community,” Losacco told The Post in an interview. “We need to bring this into our community. It needs to be in a neighborhood.”

But not her neighborhood, said Katherine Byrne. Byrne has owned Stockton Pet Hospital on South Wadsworth Boulevard for six years. The business, which was founded in 1964, sits just a few hundred feet west of Emory Elementary.

There are enough challenges with assaults, shots fired and drug dealing in the vicinity, especially along the nearby bike path, Byrne said. Because The Action Center won’t be providing overnight shelter space at its new location for people who are homeless, she worries about where people using the organization’s services might go once the doors close.

And she wonders why the city didn’t look at wealthier areas of Lakewood for potential sites to relocate The Action Center.

“It’s just a ridiculous, unsavory plan to put this center in the middle of a neighborhood that didn’t know it was coming,” Byrne said.

Building boom left a lot of space to fill, and landlords are looking to make deals.

An “Apartment for Rent” sign in the window of a building in Denver’s Speer neighborhood. April 27, 2023.

Kevin J. Beaty/Denverite

Denver landlords are making deals to entice renters to move into empty apartments.

Incentives, such as free rent, are at a 15-year high, according to a new report from the Apartment Association of Metro Denver. Landlords are trying to fill units after a building boom in recent years left a glut of space to fill.

“It’s good news for (soon-to-be renters) to see so many opportunities. Several communities are offering great discounts, including a few weeks of free rent on top of falling rates,” Mark Williams, executive vice president of Denver’s apartment association, said in a statement accompanying the report. “It’s truly the best time for new renters to move into an apartment.”

The effective rent, which is the rate people are paying after concessions are baked in, averaged $1,709 per month during the third quarter, according to the report. That compares to $1,874 per month two years ago. Average rents started falling at the end of last year, the association’s data show. They are now the lowest they’ve been in more than three years.

Boulder and Broomfield counties have the lowest vacancy rate in the region at 5.1 percent. Arapahoe County, with a 7.4 percent vacancy rate, has the highest.

Construction of new apartment buildings has slowed way down from the peak in mid-2023. That should lead to fewer empty apartments becoming available, which will eventually lead to rents stabilizing, according to the report.

The metro area vacancy rate is already down a little bit from earlier this year.

“As vacancy continues to fall, it appears the peak has been reached,” Scott Rathbun, a researcher with Apartment Insights who authored the report, said in the statement.

Ball Arena seen from the Auraria Campus. Sept. 21, 2024.

Kevin J. Beaty/Denverite

After 15 months and thousands of hours of work, a coalition of groups from downtown and central Denver has struck a deal with Kroenke Sports and Entertainment over a massive development on 64 acres of parking lots around Ball Arena.

The signing of the new community benefits agreement could be crucial for billionaire Stan Kroenke’s ambitious plan to expand downtown Denver. The project goes before Denver City Council for approvals on Monday, and several council members have said they’ll only support the project if Kroenke gets the neighbors on board.

In exchange for signing the agreement, Kroenke will have the full-throated support of the Ball Arena Community Benefit Agreement Committee (BACBAC), the coalition of registered neighborhood groups and institutions in and near central Denver. It includes groups from the Auraria Campus, the La Alma/Lincoln Park neighborhood and beyond.

Susan Powers — a LoDo resident and a member of the BACBAC coalition — says the negotiations between the community groups and the developer were sometimes tense, but ultimately productive.

“They really stepped up,” said Powers, who is also the head of the redevelopment firm Urban Ventures. “They worked with the community from the very beginning.”

However, the project still faces concerns from some council members, especially because its towers could block some downtown residents’ legally protected views of the mountains.

Ball Arena and Speer Boulevard downtown. Sept. 17, 2024.Kevin J. Beaty/Denverite

Here’s what the Community Benefits Agreement will do:

The project could include a total of more than 6,000 housing units. The deal requires that Kroenke build 18 percent of those units as affordable housing for sale and for rent, and a portion of those must be two bedrooms or more.

Of the businesses that lease on-site, 20 percent will be small businesses or women- or minority-owned. Residents of low-income parts of the city will have first dibs on construction jobs. And 20 percent of the permanent jobs on site will be prioritized for people in those communities, too.

The site will include an early learning center for at least 150 kids. The agreement sets aside $1 million in internships for career pathways in sports and entertainment. A $1 million investment in internships in sports and entertainment will be marketed to Indigenous youth and descendants of residents displaced by the arrival of the Auraria Campus.

At least $5 million will be spent on public art. Of that, 25 percent will go to Denver artists and another 25 percent will go to Colorado artists. Additionally, there will be 5,000 square feet of community art space.

There will be funding for youth programming in collaboration with local nonprofits like Youth on Record. Kroenke will provide financing for tenant eviction assistance, downpayment assistance and other renter support services.

Bike and pedestrian paths will connect the new development to the rest of the city, including a the planned 5280 Trail around downtown.

Rothman’s Children’s Park, one of the few kid-friendly public spaces in downtown, will be preserved.

The area will host regular free events for the broader community.

Additionally, there will be a $16 million community investment fund. The money for that will come from a 1 percent public improvement fee on retail sales and hotel bills in the new development.

The first phase of the project is expected to include a hotel, a 5,000-seat music venue that could rival Mission Ballroom, and new residential buildings. But future phases could be more complex, as the property is in a flood plain that will need to be addressed, Powers said.

The agreement between the developer and the community will be enforced by a yet-to-form nonprofit.

“I hope that this serves as a model for future efforts,” said Simon Tafoya, a La Alma/Lincoln Park resident on the BACBAC.

“It also shows that developers and community don’t always have to be at odds, that members of the community want to see investment, but it also means that we want to have a voice, and we also want to give voice to those who don’t always have a seat at the table.”

Ball Arena. Aug. 11, 2022.Kevin J. Beaty/Denverite

The plan for tall towers is still drawing concerns.

The project would require changes to the Old City Hall view plane, which limits the height of buildings in order to preserve views of the mountains. Some high-rise residents of Lower Downtown worry that will cut off their long-protected vistas.

View planes, as these residents see it, are preserved in city law for a reason and should not be modified. That’s become a point of concern for several council members.

District 2 Councilmember Kevin Flynn told his fellow councilmembers that he was having “heartburn” over amending the view plane.

And he wasn’t alone.

“It is very concerning, the kind of precedent that we might set in getting rid of view-plane restrictions, simply for a large development that we all want to happen in a place that is right now nothing but parking lots and a terrible use of land,” said District 5 City Councilmember Amanda Sawyer, when the development came before city council for a first reading.

Council President and District 1 Councilmember Amanda Sandoval and District 10 Councilmember Chris Hinds also expressed concerns about the view plane when the issue came before city council earlier this week.

Nonetheless, all voted recently to move the issue forward to Monday’s meeting, when the public will have a chance to comment and the council will take its final vote.

The work of the BACBAC has included a slew of organizations: the Auraria/Central Platte Valley RNO, the Auraria Higher Education Campus, the Community College of Denver, the CU Denver Community Collaborative Research Center, the Denver American Indian Commission, the Denver Housing Authority, the Denver Streets Partnership, the Downtown Denver Partnership, Fresh Start, Inc., the La Alma/Lincoln Park Neighborhood, the Lower Downtown Neighborhood Association, Sun Valley Community Coalition and WORKNOW.

John Fabbricatore enforced federal immigration laws in his position as an ICE field office director until two years ago, and now he hopes to help secure America’s borders as a congressman.

The Republican candidate in Colorado’s 6th Congressional District is drawing on his career with U.S. Immigration and Customs Enforcement as he runs against U.S. Rep. Jason Crow in the Nov. 5 election. Crow, a Democrat, just finished his third term in Congress as the representative of the district, which includes Aurora, Littleton, Englewood, Greenwood Village and Centennial.

The odds weigh heavily in Crow’s favor. The nonpartisan Cook Political Report doesn’t consider the fight for the 6th District to be competitive. It’s ranked as solidly Democratic, in part because Crow, 45, won all three of his elections by double-digit percentages and redistricting in 2020 resulted in boundaries more favorable to Democrats.

That’s a change from 2018 when the district was seen as a battleground and Crow won his first race by unseating then-U.S. Rep. Mike Coffman, now Aurora’s mayor.

But this time, Fabbricatore, 52, says voters are looking for a candidate who will prioritize the economy and lower taxes — and he contends that he’s the person for the job.

“They want someone that wants to fight,” Fabbricatore said.

He and Crow share certain traits. They’re both veterans: Fabbricatore served in the U.S. Air Force, and Crow was an Army Ranger. They’re hunters, each having longstanding experience with firearms. Neither hails from Colorado originally, with Fabbricatore raised in New York City and Crow in Madison, Wisconsin.

And the candidates, both fathers of two children, reside in Aurora.

Beyond that, their stances on major issues diverge — including on immigration, which Fabbricatore refers to as his “subject matter expertise.”

He argues jobs are going to immigrants compensated with lower wages, taking positions that could be filled by Americans for higher pay. Fabbricatore says he supports “legal, vetted” immigration and more stringent enforcement of existing laws.

“If we actually just enforce those laws, we will be doing much better than we are doing today with immigration,” he said.

In recent weeks, Fabbricatore has raised the alarm alongside former President Donald Trump and other conservatives about the presence of Venezuelan gangs in Aurora — while Crow has called out exaggerations and criticized Trump for distorting the problems in certain apartment complexes.

Crow notes that he represents “one of the most diverse districts in the nation,” with nearly 20% of his constituents born outside of the U.S. He wants to use federal grants and other programs to help immigrants and defend them against racist rhetoric.

He said he backed a bipartisan immigration deal that ran aground earlier this year after failing to earn enough Republican support. It would have boosted the number of border patrol agents, immigration judges and officers that oversee asylum cases, as well as established more legal pathways for migrants and others without documentation.

Fabbricatore said in a Denver Post candidate questionnaire that he would not have supported the bipartisan bill, instead preferring another bill with a greater focus on border security.

Gun violence is what motivated Crow to run for office. He backs a ban on assault weapons and supports universal background checks. He’s also working to pass a bill that would apply the same restrictions to out-of-state residents when they purchase long guns and shotguns as they face when buying handguns — requiring that the gun be shipped to a federally licensed seller in their home state, with a background check performed there.

Gun violence is “just an unacceptable, avoidable, ongoing national tragedy,” Crow said. “We don’t have to live with mass shootings.”

Fabbricatore says he believes in gun rights and is instead pushing for investments in mental health.

The candidates differ on abortion. Crow favors abortion rights, saying he aligns with the majority of Coloradans who back legal access to abortion — and he would support a federal law establishing that as a right. Fabbricatore says Congress should leave abortion’s legal status to the states. He opposes abortion, but he says he recognizes a need for exceptions, including in cases of rape.

“Having been someone who worked in sex trafficking and saw what many women went through, I could never tell a woman that she couldn’t have a medical procedure to end what happened to her,” he said.

Fabbricatore points to the economy as his No. 1 issue, saying it’s impacted by energy policy and immigration. He sees Colorado’s potential to participate in the energy sector through solar, wind, fracking and coal.

He says he wants to leave the younger generations with a prosperous economy, reliable job market and reasonable housing prices.

Crow says the nation’s inflation and interest rates are dropping, but he contends that prices are still “way too high for many Coloradans.”

He points to corporate price gouging as a contributing factor. Crow argues that the labor shortage, which drives up prices, could be addressed through immigration reform.

“There’s more work to do, but we’re on a good path — and certainly need to keep on the path that we are to make sure things are affordable,” Crow said.

More than half of California tenants strain to pay their rent, while more than a third of homeowners are burdened by housing costs.

Last year, 56 percent of statewide renters spent 30 percent or more of their income on housing, the fifth-highest share among the states, the Orange County Register reported, citing figures from the U.S. Census Bureau. At the same time, 35 percent of homeowners spent a similar proportion, the second highest in the U.S.

Across the nation, 52 percent of renters faced such budget stresses, compared to 25 percent of owners.

Anyone paying 30 percent or more of their income on housing bears a housing-cost burden, according to the Register.

When it comes to renters, Florida was the No. 1 state for burdened tenants, at 62 percent, followed by Nevada and Hawaii at 57 percent, and Louisiana at 56 percent. Texas ranked No. 12 at 53 percent.

Renters in the Thirty Percent Club fared best in North Dakota at 37 percent, South Dakota and Wyoming at 41 percent and Kansas and Nebraska at 44 percent.

California ranked No. 1 with 3.2 million renters in the 30 percent affordability bracket, making up 15 percent of the nation’s 22 million, according to the Register.

As for homeownership, only Hawaii’s 36 percent share of stressed owners topped the Golden State. Florida was No. 3 at 31 percent, followed by New York at 30 percent and New Jersey at 29 percent. Texas was No. 14 at 26 percent.

Owners overall faced the lowest financial pressure in West Virginia at 16 percent, North Dakota at 17 percent, followed by Indiana, Ohio and Iowa at 19 percent.

The rest of the nation is catching up to the Golden State’s housing-cost challenges.

Read more

Median price for a California home soars past $900K, a record

Residential

San Francisco

New homes don’t cure affordability in California, study finds

Residential

San Francisco

Number of affordable homes plunges across California

In 2019, the growth of California renters spending 30 percent or more on housing grew 7 percent. California now ranks No. 35 among the states and was below the nation’s 11 percent expansion.

When it comes to high-payment homeowners, California’s grew 12 percent from 2019, compared with a 19 percent increase nationally. The largest jump in cost-challenged ownership was in Florida, up 35 percent, followed by Kansas, Texas, North Dakota, and Oklahoma at 34 percent.

Aurora’s Edge at Lowry apartment complex. Sept. 4, 2024.

Kevin J. Beaty/Denverite

Last week, Aurora Mayor Mike Coffman urged the city to shut down the apartment buildings that have made national headlines over an alleged “Venezuelan gang takeover.”

“I strongly believe that the best course of action is to shut these [buildings] down and make sure that this never happens again,” he posted on Facebook.

He was responding to reports of activity by the Venezuelan gang Tren de Aragua at several apartment buildings, which has become the focus of national media coverage.

He added that the Aurora City Attorney’s Office was preparing to, “request an emergency court order to clear the apartment buildings where Venezuelan gang activity has been occurring by declaring the properties a ‘Criminal Nuisance.’”

But those plans are not moving forward, for now.

Aurora is working with the property owners on other options, local officials said. A spokesperson for Coffman said that closing the buildings is no longer the mayor’s goal.

The proposed closures would have affected hundreds of people living in two buildings owned by CBZ Management: The Edge at Lowry and Whispering Pines Apartments.

Residents of Aurora’s Edge at Lowry apartment complex, and their supporters, hold signs during a press conference to “set the record straight” on an alleged “gang takeover” of the property. Sept. 4, 2024.Kevin J. Beaty/Denverite

The apparent change of plans comes as Coffman is reportedly negotiating with the landlords at CBZ Management. They’re working on a plan, according to a city spokesperson.

“Due to new communications with the property owners and their attorneys since [last] Friday, there are no immediate plans to go forward with such a request at this time,” wrote Aurora spokesperson Michael Brannen, in a statement this week. “But it remains one of the City’s legal options moving forward, if needed.”

What we know and what we don’t about these apartment complexes and Tren de Aragua

The city and the landlord have a strained relationship. Coffman has called the owners “slumlords,” while the landlords have accused the city of letting Tren de Aragua “take over” the buildings.

The city and the landlord have been in a multi-year battle with the city over zoning code and habitability issues — complaints residents have been making for years. That dispute led to the previous shutdown of Fitzsimons Place, forcing families out of nearly 100 units.

There’s another complicating factor: Coffman doesn’t have the power to unilaterally shut down apartments, according to Councilmember Crystal Murillo. She’s the representative of the district in western Aurora that is home to the apartment buildings.

Aurora Police officers march into the recently closed Fitzsimons Place apartments in Aurora to make sure people move out. Aug. 13, 2024.Kevin J. Beaty/Denverite

A shutdown would require support from Council and also work from the City Manager, she said.

Murillo is uncertain how her fellow council members would vote, but she opposes a shutdown. She told Denverite she’s concerned that the apartments are unlivable and that the landlord has abandoned the building — but if the building is closed, residents will have nowhere to go, and many could be left homeless.

“I am concerned that people are still at risk,” Murillo said. “We already know there’s a shortage of affordable units that are livable. And you know, I’m concerned that this false narrative is making that even harder.”

Inside an apartment at Aurora’s Edge at Lowry complex, where residents are protesting their landlords alleged negligence of the property. Sept. 4, 2024.Kevin J. Beaty/Denverite

Community activists rallied on Tuesday to decry the idea of shutting down the apartments, as well as to protest CBZ Management’s alleged poor upkeep of the buildings, as well as to push back on what they described as racist and biased media coverage of their community.

Several Venezuelan immigrants said they can’t find new apartments because landlords don’t want to rent to them — a problem that’s only grown worse with sometimes hyperbolic claims of a gang takeover in Aurora.

The City of Aurora is already embroiled in legal action against Zev Baumgarten, an owner of CBZ. The company has not responded to multiple Denverite requests for comment. Coffman also has not responded to requests for interviews about those negotiations or his desire to shutter the buildings.

Aurora previously shuttered a separate CBZ Management property, displacing hundreds of people

The closure of Fitzsimons Place, at 1568 Nome Street, forced 300 tenants out of 99 units.

The City of Aurora provided those tenants with a few weeks of rent and the possibility of downpayment assistance, but no city workers were on the ground to help tenants on the day of the shutdown. Only nonprofit workers were present.

Weeks after the shutdown, Nate Kassa, an organizer with the East Colfax Community Collective, said organizers are overwhelmed as they try to find new housing for so many people.

Emily Goodman, with the East Colfax Community Collaborative, helps Yubusay Fonseca find a place to go after she and her neighbors were forced to move out of the recently closed Fitzsimons Place apartments in Aurora. Aug. 13, 2024.Kevin J. Beaty/Denverite

Many families from the Nome Street apartments fell through the cracks, and he worries they may be living on the streets, he said. Murillo fears the same would happen to the residents of the other CBZ Management apartments the city has considered shuttering.

Murillo has heard from housing advocates that some landlords are reluctant to rent to people coming from the CBZ buildings, “because now they’re all being labeled incorrectly and falsely as gang members,” she said.

“And so really, the collateral damage are still the residents. They were the victims in the first place. They’re still the victims now. And they’re suffering the consequences and being caught in the crossfire of this political grandstanding that’s happening.”

A home for sale in Washington Park West. Jan. 4, 2024.

Kevin J. Beaty/Denverite

Denver’s housing market is languishing this summer.

The number of homes for sale keeps rising as high borrowing costs slow down deals. In July, inventory shot up 68 percent compared to the same time last year, according to a report from the Denver Metro Association of Realtors.

Inventory has been rising for months. Spring and summer are typically the busiest times for house hunters, but activity has been relatively slow throughout the summer.

The glut of available homes is a result of buyers sitting on the sidelines with mortgage rates the highest they’ve been in decades. But for those that are willing – and able – to stomach higher interest rates, there’s more to choose from in and around Denver than there has been in years.

“Buying now allows for a thoughtful search with room for negotiation and a refinance at a later date,” the association wrote in the report. “Some price ranges, and areas of town, have become a buyer’s market due to the number of available options.”

Borrowing costs could start falling soon. U.S. central bankers are signaling that they’ll be ready to cut interest rates when they meet again in September now that inflation appears to be largely under control. That could make it a home more affordable, but it’s also likely to increase competition from other buyers.

Prices have declined slightly while people wait for mortgage rates to come down. The median price dipped to $600,000 last month, down about $1000 from the month before. That’s still roughly $10,000 more than the same house would have cost at this time last year.

The days of needing to save two to three months’ worth of rent for a security deposit are largely over in California.

Legislation took effect Monday that limits a security deposit on a rental property to no more than one month’s rent for all but the smallest landlords. The law, passed as Assembly Bill 12, was authored by Assemblymember Matt Haney (D-San Francisco).

“Massive security deposits can create insurmountable barriers to housing affordability and accessibility for millions of Californians,” said Haney, who chairs the California Legislature’s Renters Caucus, in a statement.

Previously, owners could charge two months of rent for unfurnished property and three months for furnished.

Supervisor Lindsey Horvath noted in May 2023 that she was unable to move into a rental a couple of years earlier because she was asked to pay “nearly a half a year’s rent upfront.”

“As someone with a well-paying job, making more than the median income of the county, it was difficult for me to rent a new apartment because of the substantial deposits that were required,” she said.

But the legislation raises concerns among some in the real estate industry.

Sharon Oh-Kubisch, a partner at Irvine-based Kahana Feld, which practices real estate law, noted two potential drawbacks to the legislation.

While she supports the bill’s aim of alleviating high costs of renting, financial burdens are being flipped to landlords, she said.

She noted that security deposits are intended to cover damages when a tenant moves out. Lower deposits mean landlords are more likely to have to sue clients who cause considerable damage.

“A landlord can demand damages at the back end, but then they’re more than likely going to have to sue and hire counsel to get that money,” Oh-Kubisch said.

Additionally, she said that reducing security deposits may work against tenants who have less than perfect credit or lack a strong history of renting.

Higher security deposits allowed landlords to be more flexible, Oh-Kubisch said. With those “safeguards” gone, she expects landlords to be “more precise and heighten scrutiny for tenants.”

Still, others say the legislation will benefit those who have the most trouble finding housing.

Masih Fouladi, executive director of the California Immigrant Policy Center, said in a statement that the law will help vulnerable communities.

“In California’s high-cost rental market, expensive security deposits are often imposed on immigrants and people of color, effectively limiting access to safe and affordable housing,” he said. “By capping high security deposits, AB-12 advances a measure of equity.”

Catherine A. Rodman, director and supervising attorney of San Diego-based Affordable Housing Advocates, a tenants rights legal group, said the news received mixed reviews among her mainly working-class clients.

“I know that it’s been a big relief to many throughout the state, but at least here in the San Diego area, it’s not a big issue,” Rodman said.

Zillow lists the median rent in San Diego at $3,095.

She said “soaring rents” have already led most area landlords to require no more than one month’s rent as a security deposit.

“I’ve been here for 40 years, and I’ve only encountered security deposit gouging on a few occasions,” Rodman said. “Our issue is rent.”

Rodman said she didn’t want to “pooh-pooh” the legislation but hoped it was part of a broader vision to make housing affordable for larger swaths of the state.

“I’m sure it helps, but we need to address the cost to rent, because that’s really the big roadblock,” she said.

Coloradans looking to buy homes or simply hold onto their property face a barrage of challenges: a white-hot real estate market, high interest rates and soaring property taxes. You can add surging home insurance rates to the pile of problems eroding the landscape of affordable housing options.

Colorado homeowners are reporting premium increases ranging from roughly 30% to more than 130% in just the past few years. People are getting the bad news that their policies won’t be renewed. Some insurance companies are deciding not to write new policies to cut their risks.

And condo owners are getting hit with special assessments and higher dues because premiums are skyrocketing for homeowners associations. The groups must often resort to non-standard carriers, which typically charge sky-high rates for lesser coverage.

“We truly have the hardest market that we’ve seen in a generation for property insurance,” said Carole Walker, executive director of the trade organization Rocky Mountain Insurance Information Association.

Colorado’s not alone. Inflation, higher home costs and the rising number and severity of natural disasters and wildfires are pushing up insurance costs. The average premium rate increase nationwide in 2023 was 11.3%, according to S&P Global Market Intelligence.

But Colorado’s recent increases stand out. The state was one of three with the biggest cumulative change in rates 2018-2023. Colorado logged a 57.9% jump, just behind Texas at 59.9%. Arizona saw a 52.9% increase.

A convergence of factors is driving the run-up in costs, Walker said. Higher inflation is one of those. “You have everything that insurance pays for going up in cost.”

Building materials are more expensive. Labor costs are up and labor shortages create delays and add to the expense. Walker said insurance-related lawsuits also help push up premiums.

An even larger force is the fallout from increasingly costly wildfires, hail storms and other disasters. Insurance companies doing business in Colorado reported the fourth-highest losses in the country for five years, according to data compiled for a 2023 report by the Colorado Division of Insurance.

“I hate to say it, but we all likely need to adjust to higher premiums over the long term,” Walker said.

The effects of the mounting risks are being felt by a lesser known, but crucial link in the chain that connects to homeowners: the reinsurance market. Reinsurers are typically large, global companies that provide insurance to insurance companies to help spread the risk.

“The international impact of climate change, of increasing climate disasters, the severity of those disasters is causing reinsurers to consider their risk, reduce their exposure or increase their premiums,” said Vince Plymell, spokesman for the insurance division.

As a result, the effects of hurricanes and earthquakes in other parts of the country or world can eventually show up in a Colorado homeowner’s insurance bill, said Jason Lapham, the state’s deputy commissioner for property and casualty insurance.

Closer to home are the growing risks of wildfire and hail storms. Colorado is second in the nation for hail-damage claims and second only to California for the number of homes at risk from wildfires. Colorado hasn’t seen the kind of wide scale refusal of companies to write new policies that California has, but Lapham said there is a trend of some companies not re-upping policies in areas prone to wildfires or other disasters or taking “a pause” on new clients.

“It doesn’t mean they’re leaving the state entirely, but for those people who are affected, the effect is the same,” Lapham said.

State officials don’t have a lot of insight into the modeling used by companies to decide which areas are too risky to insure, Lapham said. “We’re focused on getting a better understanding and creating transparency, not just for us but also for policy holders.”

Levi Ware, project manager from Red Hawk Roofing company from Denver, takes pictures of a roof damaged by large hail and a tornado along Chesapeake Street in Highlands Ranch on June 23, 2023. A rare tornado hit the Highlands Ranch area Thursday afternoon causing damage to roofs and uprooting large trees. (Photo by Andy Cross/The Denver Post)

What’s worse than rising premiums?

There were plenty of insurance options for Bryan Watts and his wife when they bought a house in Guffey in Park County, west of Cripple Creek. The premium was about $2,000 in 2019 and rose gradually to $2,522 for the 2023-2024 policy year.

“Things changed dramatically in August 2023 when we received a notice of non-renewal at the policy maturity of June 2024,” Watts said. “I called them and was told it was simply due to wildfire risk.”

Watts tried to reason with the company, saying he had done a lot of work to reduce threats from wildfire. He offered to send pictures of his home or show an inspector around his property. But the insurer told him that it wasn’t going to cover homes in his zip code.

“I thought, ‘Well, no big deal. I’ll just move to another carrier,’” Watts said. “I had no idea how bad it had gotten just in the last year or two.”

A broker Watts worked with found only nonstandard insurers willing to cover his home. The insurers might take on customers that more traditional companies consider too risky, but the coverage comes at a high price. In Watts’ case, the quote was for nearly $35,000.

After making calls on his own, Watts found one of the big-name companies willing to write a policy for $4,800. A hang-up for companies that turned him down was that the nearest fire station is about 16 miles from his home. “They’re looking for substations that are 10 miles or closer,” Watts said.

Like a lot of people, Watts has a mortgage on his house, which means he needs to carry insurance. “There are going to be very few people who are able to live out here without a mortgage,” he said.

Escalating home insurance premiums and companies scaling back coverage are creating angst in the real estate industry. Brian Tanner, vice president of public policy for the Colorado Association of Realtors, said agents are seeing properties lose coverage or unable to find insurance.