Hashrate Index has released its 2022 Bitcoin Mining Year In Review, an extensive report on the mining industry and markets surrounding it.

2022 was a difficult year for Bitcoin mining, with the bear market leading to a hashprice all-time low, bankruptcies and losses for miners. Despite this, hash rate still grew 41%, and Bitcoin mining still generated nearly double the rewards compared to the previous three years. The report covers all of these topics and more in detail.

One of the main focuses of the report is the growth of hash rate.

Bitcoin hash rate 2022 vs. 2021 — Source: Hashrate Index

Although the year involved many challenges to the mining industry, from an all-time low hashprice, to several public miner bankruptcies and even an arctic cyclone at the end of the year to top things off, hash rate still climbed, and at a much greater rate than 2021, which was stunted by China’s mining ban.

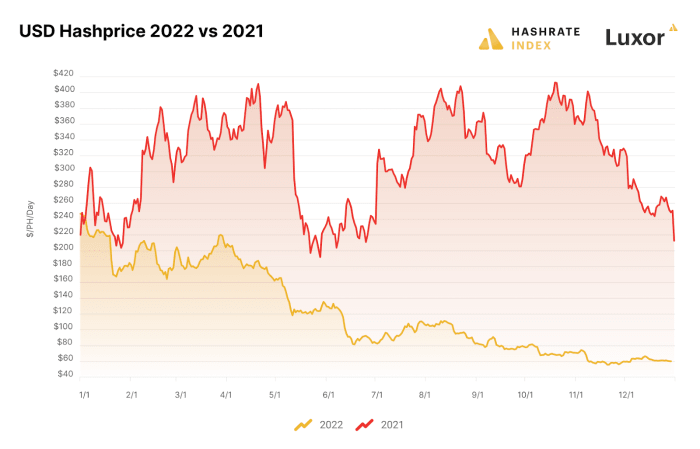

The report also describes a large decline in hashprice, with the high of the year being recorded on January 1 at $246.86/PH/day and only declining from there. Indeed, the year saw an all-time low in hashprice at $55.94/PH/day.

Bitcoin USD hashprice 2022 vs. 2021 — Source: Hashrate Index

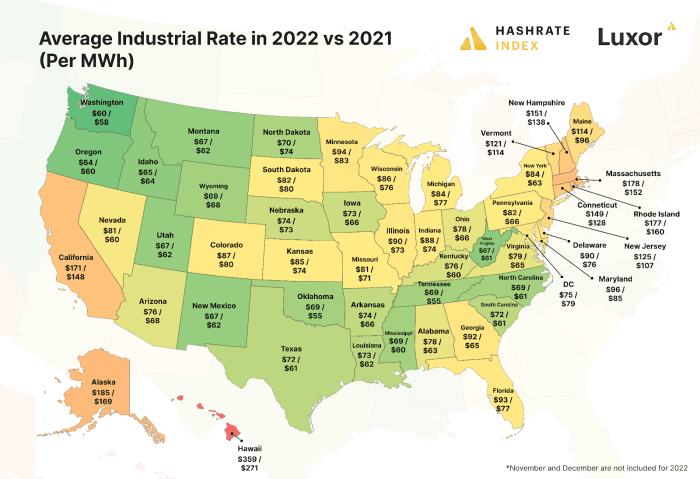

One factor that played into this, according to the report, is increasing industrial electricity rates across the country. But many states have been insulated from this rise in cost through abundant energy production sources like Washington’s hydropower, or other states’ access to natural gas, leading to certain states retaining viable mining operations. The report also notes that “power strategies can take many forms, but a common theme is that miners exploit the unique low-consequence-interruptibility of the bitcoin mining process by adjusting their electricity consumption based on market signals.” This was on display most recently when Texas miners turned off their operations in order to return energy supply to the grid, while getting paid nearly as much as they would have had they continued mining.

Average U.S. industrial power rate 2022 vs. 2021 — Source: EIA.gov

Hashrate Index also highlighted the increase in hosting costs, which prior to 2022, hovered around $0.05-$0.06/kWh. But now, “Anything below $0.075/kWh is considered “a steal” given market conditions.”

Suffering public miners were also a focal point in the analysis.

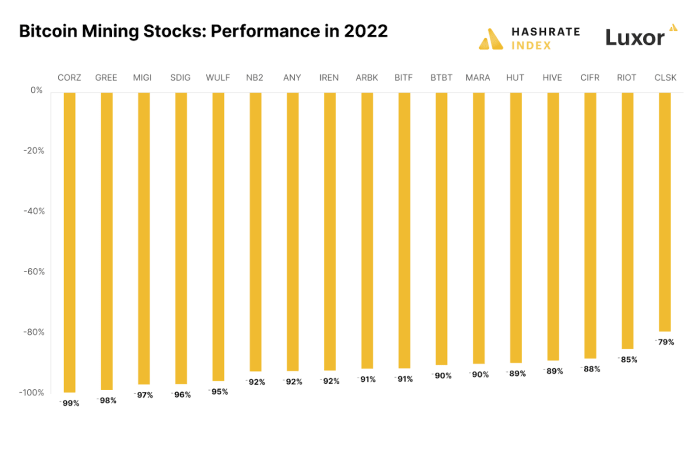

Bitcoin mining stock performances in 2022 — Source: TradingView

With the bull market in full swing, public bitcoin miners made big bets with their equipment purchases and expansionary moves. But the bear market hit some larger performers particularly hard, with behemoths like Core Scientific taking losses of nearly 100% — the company is currently undergoing Chapter 11 bankruptcy procedures. These were difficult-to-swallow pills for the market, but public miners did expand in terms of their hash rate dominance, ending the year at 19%.

Overall, the report signified Bitcoin’s resilience in the face of various major headwinds. Macroeconomic pressures, environmental anomalies and major public mining stocks tumbling more than 90% still couldn’t hamper major growth in network hash rate. Apparently, even such horrendous extraneous conditions as those on display in 2022 cannot temper the growth of the Bitcoin mining industry.

This is an opinion editorial by Alex, a bitcoin miner with Kaboomracks.

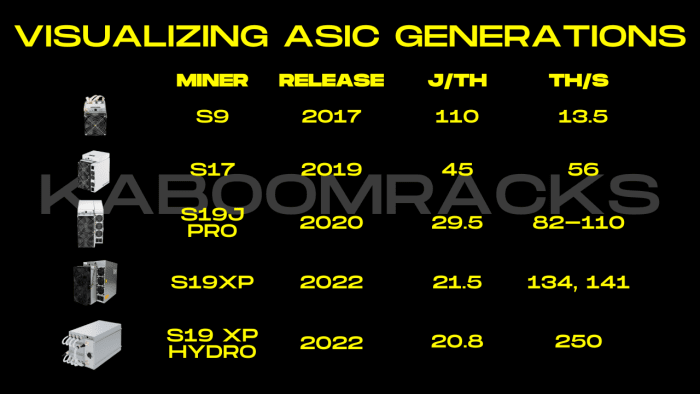

It is important for individuals looking at bitcoin mining for the first time to understand the importance of Bitcoin’s difficulty adjustment as well the impact this has on mining profitability. Many newcomers to bitcoin mining will consult the profitability of an ASIC on a mining calculator, expecting that that profitability will stay relatively the same going forwards in the future. This is a misunderstanding as the profitability of any given machine, trends downwards over time. Increases in difficulty should be understood before purchasing an ASIC.

A simple way of understanding this is comparing an ASIC to any other electronic device. The longer the device is in use, the less relevant it is as new software requires more computing power. If you were to use an iPhone from 6 years ago, its performance would be incredibly frustrating. The older the phone gets, the less utility it has.

A very similar process happens in mining. When you are mining, you are competing with all the other miners around the world. As more miners turn on machines, it gets more difficult to compete. Having newer and more efficient hardware makes you more competitive, but that hardware is quickly moving towards being less competitive.

Picture courtesy of coinwarz.com

Bitcoin Difficulty Adjustment

Bitcoin’s difficulty adjustment is something built into the Bitcoin protocol in order to ensure Bitcoin has a stable and predictable supply schedule. If there was no difficulty adjustment, all of the bitcoin likely would’ve already been mined and there would be little to no incentive for miners to secure the network. When more miners join the network, blocks are minted at a faster rate as a result of a hash rate increase. The network responds by adjusting the difficulty higher to ensure that blocks come in around 10 minutes. For miners, increased difficulty adjustments mean less profits. For the average Bitcoin user, it means more security for the monetary network they are using.

Picture taken from insights.braiins.com

Downwards difficulty adjustments mean that miners will be earning more profits as these are a result of hash rate coming offline. The famous example of this happening is when China banned Bitcoin mining and a large portion of the network hash rate went offline for a period of time. Downwards difficulty adjustments are not the norm as mining hardware is always getting more powerful and efficient. Even if there was a stagnation of machine efficiency and hash rate increases, more machines would be produced and plugged in. The Bitcoin mining industry is incredibly immature and there is a tremendous amount of room for growth going forward which means that hash rate is almost certainly going to increase at rapid rates going forward over the long run.

We are currently seeing a bull market in energy prices with a suppressed bitcoin price which means that miners are experiencing quite a bit of pain. There is a possibility that there could be a series of downward difficulty adjustments as hash rate comes offline, but this is not something that miners should put in their models. It is important to prepare for the worst case scenario which is what we have seen the last few months.

New Machines Coming To Market

Every couple years, ASIC manufacturers release a new machine with significant improvements in regards to hash rate and efficiency. Recent network hash rate increases are largely due to seeing Bitmain’s S19 XP and S19 Hydro being deployed. Another factor is that a large amount of older generation machines are finally being turned on as a result of infrastructure being built out.

This chart is an oversimplification just for visual purposes.

When you buy an ASIC, its value will be constantly depreciating as both network hash rate increases and new machines come onto the market. The value will fluctuate depending on the Bitcoin price, but it’s safe to say the machine loses value over time. That is why it is incredibly important to have the machine running when you have it. Buying it to plug in later means you are throwing money away unnecessarily.

Bitcoin Purchasing Power

Bitcoin mining is like taking a long position on Bitcoin, but with a lot of headaches and execution risk. If done correctly, it can be incredibly lucrative. If done incorrectly, it is a fantastic way to get poor quickly. The income the machine makes is fairly consistent, but the purchasing power of that income varies tremendously. Power prices may be stable priced in dollars, but are very volatile when priced in the income you are making from that machine. A S19j Pro may make 38,000-40,000 sats a day in income, but if you are mining on $0.10 a kWh, your power costs will be 41,263 sats with bitcoin trading at $17,461.

This is why it is incredibly important to try and get the lowest possible electricity prices in order to be profitable and ROI on your equipment. Finding cheap electricity is neither straightforward nor easy. Oftentimes there are hidden fees or complications that cause miners to fail. All miners regardless of how big or small are subjected to these economics of variable purchasing power, network hash rate increases, and machine devaluation/obsoletion.

ASIC Pricing

There is a base cost for the manufacturers to produce new equipment. We are currently at or reaching that floor for new equipment coming from the manufacturer. As a result, they are either slowing down or halting production of certain models. Individuals choose to pay a premium for new equipment because they come with warranties. Used equipment on the other hand generally does not come with a warranty, and also uncertainty of conditions that it was run in. For this reason, used equipment is often sold at a substantial discount.

ASIC pricing is variable just like every other industry. Supply and demand are the major factors that determine price. Individuals buying ASICs have a million different reasons why they may want to purchase at a certain time, but Bitcoin price and difficulty are major influences. If the purchasing power of the income being earned by an ASIC is low, there will be less demand and the ASIC price will fall. Bear markets are generally good times to buy because the demand drops significantly.

Moore’s Law And The Future Of ASICs

“Moore’s Law: an axiom of microprocessor development usually holding that processing power doubles about every 18 months especially relative to cost or size.” — Merriam Webster

We are coming to the end of the computer chip revolution as chip makers are pushing the boundaries of physics. In no way is this the end of massive increases in Bitcoin’s network hash rate. The mining industry is very rough around the edges in regards to very basic principles such as heat dissipation, software implementations, and relationships with energy producers. Computer chips may have slower leaps as far as increases in computing power, but we have barely scratched the surface in regards to other technological leaps forward that will ultimately lead to more power being consumed and more computing power expended in order to secure the Bitcoin Network.

As bitcoin becomes more widely adopted, and its value understood, the demand for mining is bound to increase globally. The result will naturally be an increase in Network hash rate. As a miner, this is a painful reality as it means the profitability of my hardware will decrease over time. As a Bitcoiner, it gives me confidence in the monetary network that I use daily.

This is a guest post by Kaboomracks Alex. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

Bitcoin mining companies continue struggling to survive the ongoing bear market. Dreams of outperforming bitcoin as a public mining company are long gone. Bankruptcies and lawsuits make routine headlines. And even Wall Street analysts that were once bullish on bitcoin mining investment opportunities now say they’re “pulling the plug” until the market improves. But exactly how bad is the current bear market?

It’s always darkest before dawn, as the adage says. And compared to previous bear markets, the mining industry looks much closer to the end of a turbulent market phase than the beginning of it. This article explores a bunch of data sets from the current and previous bear markets to contextualize the state of the industry and how the mining sector is faring. From hardware lifecycles and miner balances, to hash rate growth and hash price declines, all of these data tell a unique story about one of Bitcoin’s most important economic sectors.

Mining Revenue Is Evaporating

When bitcoin’s price drops, it’s not surprising that dollar-denominated mining revenue also drops. But it has – a lot. Roughly 900 BTC are still mined every day and will be until the next halving in 2024. But the fiat price for those bitcoin has plummeted this year, meaning miners have far fewer dollars for expenses like electricity, maintenance and the servicing of loans.

As the chart below demonstrates, in November, the entire bitcoin mining industry earned less than $500 million from processing transactions and issuing new coins. The bar chart below shows this monthly revenue compared to the past five years. November mining revenue marks a two-year low for monthly earnings.

This past month marked a two-year low for Bitcoin mining company revenue.

Potential Hash Rate Uptrend Reversal

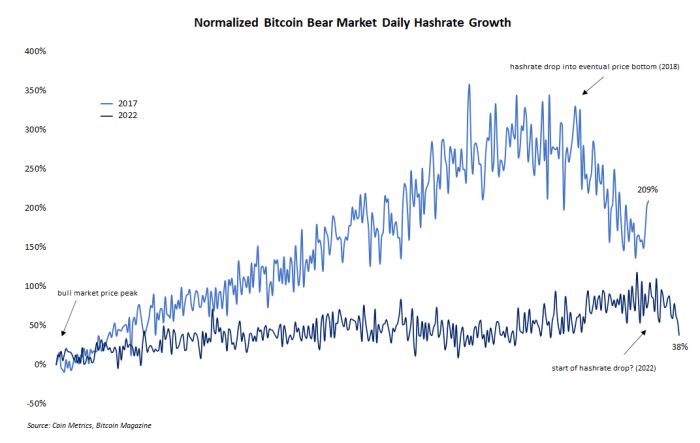

Comparing the current bear market to the previous one in 2018 offers some interesting insights into how the mining industry has changed and how it has remained the same. One such comparison is hash rate growth during downward price trends. It’s not uncommon to see hash rate grow during bear markets. The annotated line chart below shows normalized hash rate growth during the 2018 and 2022 bear markets from bitcoin’s price peak to the drawdowns’ history (or current) lows.

So far in this bear market, Bitcoin hash rate has only grown.

But one thing that is obviously missing from the above chart is a correction in hash rate growth during the later period of the bearish phase. In 2018, for example, the growth trend clearly changed course and dropped as the market eventually found a low for bitcoin’s price. But in the current market, hash rate has only grown. Perhaps a slight drop in hash rate through late November signals a trend change, but the question is still open.

Collapse Of Public Mining Companies

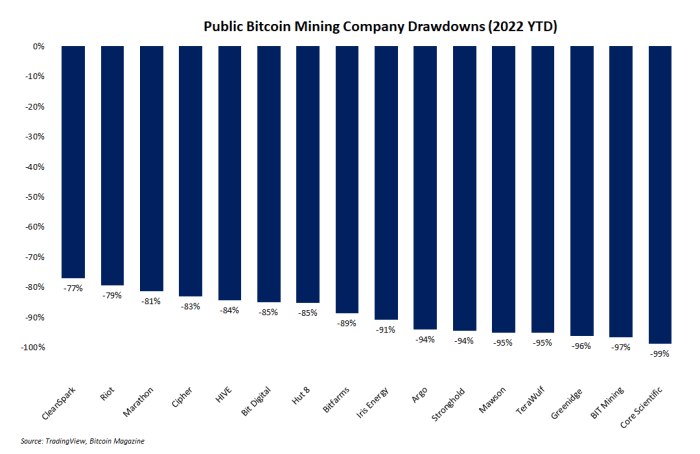

Perhaps the most brutal bitcoin mining chart of all shows the drawdowns of publicly-traded mining companies this year. It’s no secret that the past year has been brutal for bitcoin, other cryptocurrencies, and the global economy in general. But mining companies in particular have been clobbered. Over half of these companies have seen their share prices fall over 90% since January. Only two — CleanSpark and Riot Blockchain — have not dropped more than 80%.

Mining companies in general are often considered to be a high-beta investment in bitcoin, meaning when bitcoin goes up, mining stock prices go up more. But this market dynamic cuts both ways, and when bitcoin falls, the downside for mining stocks is even more brutal. The bar chart below shows the massacre these stocks have endured.

Bitcoin mining stocks have been massacred.

The Rise And Fall Of Bitcoin Mining’s ‘AK-47’

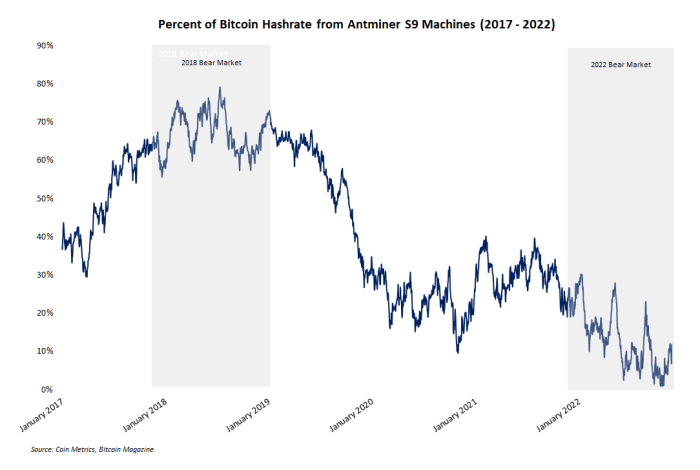

An underappreciated hallmark of the current bitcoin bear market is the precipitous decline in hash rate contributed by Bitmain’s Antminer S9 machines. This model of mining machine is occasionally referred to as the “AK-47” of mining because of its durability and reliable performance. And at one point in the 2018 bear market, the S9 was king. Nearly 80% of Bitcoin’s total hash rate came from this Bitmain model during the depths of the previous bear market.

But the current bear market tells a completely different story. Thanks to new, more efficient hardware and a vice-grip squeeze on mining profit margins, the percentage of hash rate from S9s dropped below 2% in early November. The annotated line chart below shows the rise and fall of this machine.

The Antminer S9 has seen a remarkable fall.

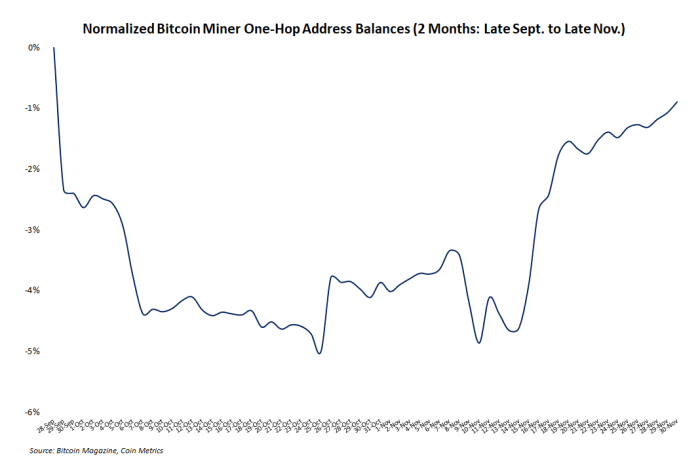

Miner Balance Retraces Its Sell Off

The past few months have been disastrous for the “crypto” industry as exchange wars, insolvent custodians and other forms of financial contagion swept the market. Many bitcoin investors like to assume their segment of the industry is mostly insulated from the chaos of the rest of “crypto,” but this is usually false. In the case of miners, who are notoriously bad at timing the market, some panic was evident as address balances and miner outflows appeared to drop and spike, respectively.

But this activity was short lived. The line chart below shows that miner address balances have almost fully retraced their drop from late September through October. In short, miners appear to be back in HODL mode, impervious to exogenous market events. Whether the bear market is over or not is unknown. But miners seem to be accumulating more than selling.

Miners appear to be back in HODL mode.

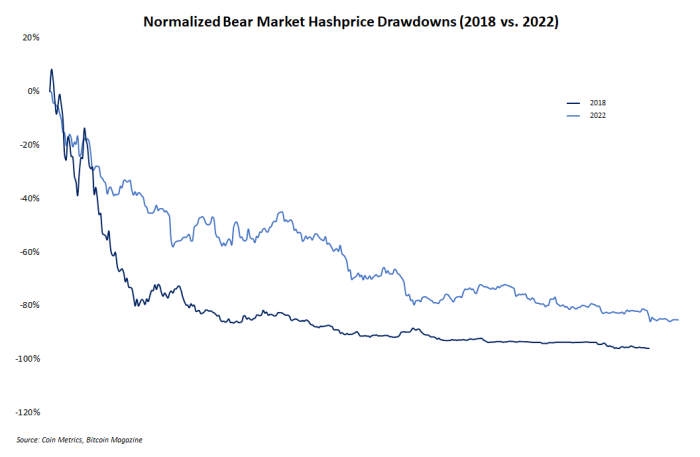

Hash Price Drop Today Vs. 2018

Hash price is one of the most popular economic metrics for miners to track, even though few people outside of the mining sector understand it. In short, this metric represents the dollar-denominated revenue expected to be earned per marginal unit of hash rate. And like everything else in the bear market, hash price has fallen significantly. But its decline is not unusual, especially when it’s compared to the hash price decline in 2018.

Shown in the chart below are normalized hash price drawdowns from 2018 and 2022. Readers will notice the fairly similar slope and size of the drawdowns. 2018 was slightly steeper. 2022 to date has been shallower but longer. But both were and are brutal for fledgling mining operations.

This 2022 hash price drawdown has been shallower but longer than its 2018 equivalent.

The Next Phase Of Mining

Boom and bust cycles are a natural series of events for any properly functioning market. The bitcoin mining sector is no exception. For the past year, mining has seen its weaker, unprepared operators weeded out as the excesses from the bull market are brought to account. Now, in the depths of a bearish period, the real builders can continue to expand their operations and build a solid foundation for the next phase of euphoric bullishness.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Riot Blockchain has released its unaudited production and operations updates for November 2022. According to the release, the company produced 521 BTC, a 12% increase on its November 2021 production of 466 BTC. It sold 450 BTC, generating net proceeds of $8.1 million, and had a deployed fleet of 72,428 miners with a hash rate capacity of 7.7 exahashes per second (EH/s) on 30 November.

Jason Les, CEO of Riot stated, “Riot again achieved a new record for total hash rate capacity during the month of November, resulting in our highest monthly bitcoin production figure to date.” He did caveat this positivity, saying, “Despite this new level of production, expected production was approximately 660 bitcoin given our operating hash rate over the month, assuming normalized performance of the mining pool we participate in. Variance in a mining pool can impact results and while this variance should balance out over time, can be volatile in the short term. This variance led to lower bitcoin production than expected in the month of November, relative to our hash rate.”

To better formulate an outlook on their production, Les stated in the release, “In order to ensure more predictable results going forward, Riot will be transitioning to another mining pool which offers a more consistent reward mechanism, so that Riot will fully benefit from our rapidly growing hash rate capacity as we work towards our goal of reaching 12.5 EH/s in the first quarter of 2023.”

The report did not specify which mining pool Riot will now point its miners towards.

Looking ahead, Riot seeks to achieve a total self-mining hash rate capacity of 12.5 EH/s during Q1 2023, assuming full deployment of approximately 115,450 Antminer ASICs.

However, this does not include any potential incremental productivity gains from the company’s utilization of 200 MW of immersion-cooling infrastructure. The majority of Riot’s self-mining fleet will consist of the latest S19-series miners. In addition to its self-mining operations, the company hosts approximately 200 MW of institutional Bitcoin mining clients.

The pain in the mining world continues as hash rate skyrockets, the difficulty adjusting upwards as a result and hash price craters as the price of bitcoin has remained in a tight range between approximately $18,000 and $20,000 for more than six weeks. After yesterday’s upward difficulty adjustment of 3.4%, hash price fell to $0.055, according to Braiins Insights. This is the lowest it has been in the ASIC era.

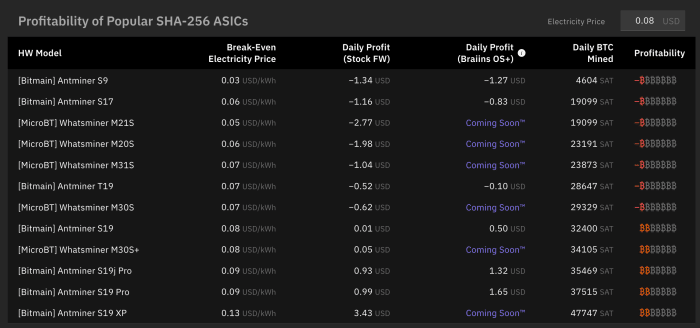

Let’s put this into perspective by highlighting the profitability of different ASIC models mining at an all-in electricity cost of $0.06, $0.08 and $0.10 per kWh.

As you can see, at an all-in cost of $0.06/kWh, most ASIC models are profitable, though not very. If you’re running S9s, M21s or M20s, you are currently mining at a loss. Now let’s check out how this looks when we bump up the cost of electricity by $0.02/kWh.

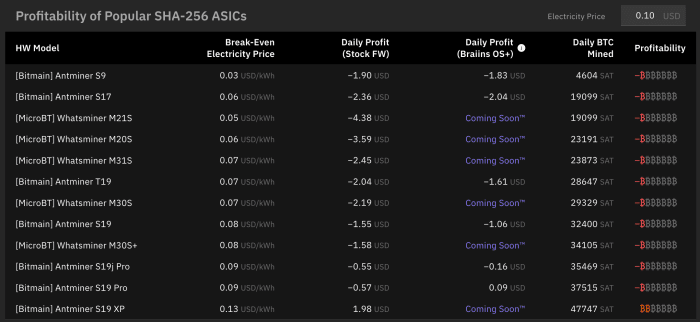

Four more ASIC models get driven into unprofitable territory with the S19 and M30s+ scraping by with $0.01 and $0.05 of daily profit, respectively — unless you’re running Braiins OS+ firmware on the S19, in which case you’d be netting $0.50 per day in profit. The pain is starting to get nauseating. Now let’s bump it up to the all-in cost of $0.10/kWh.

This is what we in the business refer to as an “absolute bloodbath.” The only miner that is profitable outside of an S19 Pro running Braiins OS+ is the S19 XP — the newest, most efficient and highest-hashing model on the market. If you are running any other model, you are currently in the process of bleeding money. Not a situation anyone wants to be in.

If I had to guess based on my knowledge of the mining industry and the electricity rates I have come across while interacting with other miners in the space over the course of this year, I would wager that there is a significant amount of hash rate plugged into power sources that are charging $0.07 to $0.10/kWh. Miners are either barely getting by or hemorrhaging money at the moment. The pain is real.

Every single miner hosting with Core Scientific who isn’t running an S19 XP or an S19 Pro with Braiins OS+ firmware is currently mining at a loss. According to its most recent monthly update, the company self-mines 13 EH/s produced by roughly 130,000 ASICs and hosts 102,000 ASICs producing 9.5 EH/s. I think it’s safe to say that most of these machines aren’t S19 XPs considering they just started deploying that model in July 2022. With that being said, Core Scientific’s self-hosted miners are probably mining at lower than $0.10/kWh considering they own the power purchase agreement and are likely mining at cost while charging hosting customers a higher rate to produce a margin for their business. Still, this is not an ideal environment for Core Scientific or any other miner with an all-in electricity cost above $0.06/kWh.

This all begs the question, “Why the hell is the hash rate still screaming?”

From what I have heard, a lot of projects that have been in development for well over a year in Texas just got electrified at the beginning of the month. These teams spent tens of millions of dollars in infrastructure costs and went through the administrative troubles that come with connecting to ERCOT. They weren’t going to reach the finish line and not turn on their ASICs. As it stands today, the mining industry seems to be caught in a game of “who can hold their breath the longest.” How long can these market conditions continue without countless miners having to turn off their machines so they stop losing money, or worse file for bankruptcy?

Compute North was the first domino to fall almost a month ago when they filed for bankruptcy. Your Uncle Marty expects them to be the first of many unless the price rips or some on-grid mega mine has a critical error that turns their machines off. Neither situation is what you want to be banking your business on if you’re a bitcoin miner.