[ad_1]

U.S. stocks ended sharply higher Friday, with the technology-heavy Nasdaq Composite leading the way up, as hopes rose for a debt-ceiling deal in Congress.

The Nasdaq and S&P 500 also closed at their highest levels since August 2022.

How stock indexes traded

-

The Dow Jones Industrial Average

DJIA,

+1.00%

rose 328.69 points, or 1%, to close at 33,093.34, snapping a five-day losing streak. -

The S&P 500

SPX,

+1.30%

gained 54.17 points, or 1.3%, to finish at 4,205.45. -

The Nasdaq Composite

COMP,

+2.19%

jumped 277.59 points, or 2.2%, to end at 12,975.69.

For the week, the Dow fell 1%, while the S&P 500 edged up 0.3% and the Nasdaq advanced 2.5%. The tech-heavy Nasdaq booked a fifth straight week of gains for its longest win streak since the stretch ending in early February, according to Dow Jones Market Data.

What drove markets

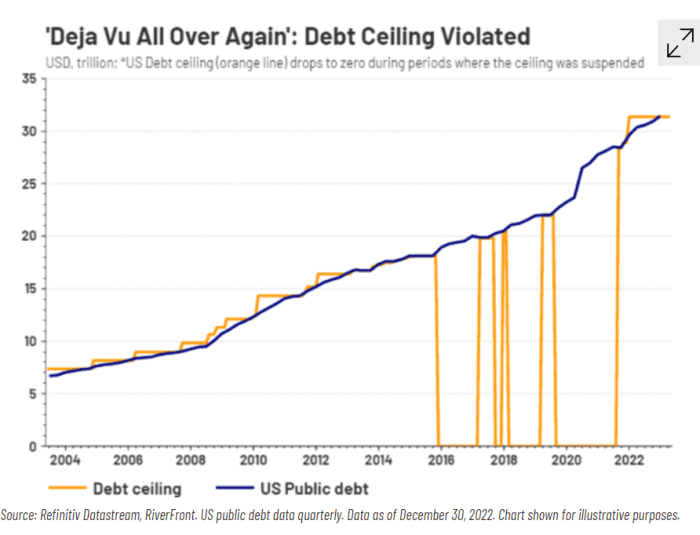

Stocks rose ahead of Memorial-Day weekend as investors were encouraged by reports suggesting that Congress was close to a deal to raise the U.S. debt ceiling.

“It’s a little bit of a relief rally on the debt ceiling,” said Ryan Belanger, founder and managing principal at Claro Advisors, in a phone interview Friday.

While Treasury Secretary Janet Yellen says the U.S. could run out of money as soon as June 1 if the debt ceiling is not raised, other projections estimate the federal government may have until the middle of the month.

“I think we’ll all be able to exhale by mid-June, although it will likely be an increasingly volatile market environment between now and then,” said Kristina Hooper, chief global market strategist at Invesco. “Once that drama recedes, I think all eyes will be back on central banks.”

Belanger said that he’s expecting the Federal Reserve may raise its benchmark interest rate by another quarter percentage point in June to battle high inflation.

The Bureau of Economic Analysis said Friday that the personal-consumption-expenditures-price index showed core inflation, which excludes food and energy, rose 0.4% in April. That’s more than the 0.3% increase that economists had expected, as core inflation rose 4.7% year over year from a rate of 4.6% in March.

Rubeela Farooqi, chief U.S. economist at High Frequency Economics, said inflation appeared to be moving “in the wrong direction” at the start of the second quarter.

Fed-funds-futures traders now see a 65.9% chance of the Fed hiking its rate by a quarter percentage point in June, and a 34.1% probability of a pause, according to the CME’s FedWatch Tool, at last check. In the bond market, two-year Treasury yields

TMUBMUSD02Y,

rose 7.9 basis points Friday to 4.587%, according to Dow Jones Market Data.

PCE data also showed consumer spending sprang back to life in April, rising 0.8%, the largest gain in three months to surpass expectations, as Americans bought more cars and spent more on services.

“The consumer is hanging in there,” said Victoria Fernandez, chief market strategist at Crossmark Global Investments, in a phone interview Friday. “I don’t think we want to underestimate the ability of the consumer to continue spending, even if they’re spending a little bit less.”

Meanwhile, the U.S. Census Bureau said Friday that orders for manufactured durable goods in the U.S. jumped 1.1% in April. The gain was largely driven by military spending, but business investment rose sharply as well.

Updated GDP data released earlier this week showed the U.S. economy grew at annual pace of 1.3% during the first quarter, above previous estimates.

For now, debt-ceiling optimism and enthusiasm surrounding artificial intelligence are outweighing concerns about the potential for another Fed rate hike, according to Fernandez. “I just don’t think there is the demand destruction that the Fed is looking for at this point in time,” she said, as the unemployment rate remains low.

Fernandez said she anticipates the Fed could pause its interest-rate hikes in June to asses the economy before potentially raising its policy rate again in July.

Technology stocks have helped propel gains this week in the U.S. equities markets, with Nvidia’s stock

NVDA,

surging Thursday on optimism surrounding its AI-fueled outlook for sales in the second quarter.

The tech-heavy Nasdaq Composite has soared 24% this year through Friday. “I would be taking profits on the Nasdaq,” said Belanger, suggesting some stocks in the index have become frothy amid the AI buzz.

Companies in focus

-

Marvell Technology Inc.’s stock

MRVL,

+32.42%

surged 32.4% after the chip company said it expected revenue from artificial intelligence to at least double this fiscal year. -

Gap Inc. shares

GPS,

+12.40%

rallied 12.4% after the retailer took Wall Street by surprise and posted an adjusted profit of a penny a share. -

Ford Motor Co. shares

F,

+6.24%

rose 6.2% after announcing that its electric-vehicle owners soon will have access to the more than 12,000 Tesla Inc.

TSLA,

+4.72%

Superchargers in the U.S. and Canada starting next year. -

Workday Inc. shares

WDAY,

+10.01%

jumped 10% after the software company easily topped earnings expectations and brought on a new chief financial officer.

—Steve Goldstein contributed to this report.

[ad_2]