It hasn’t served a vital economic function since the government stopped treating it as money back in 1971. Actually, you could argue it stopped being necessary long before that.

Yes, some people prefer it in jewelry. It is used in some technological equipment, and sometimes, still, in dentistry. But so what? According to authoritative data from the World Gold Council, even all those uses only account for about half of the world’s supply each year. Logically, this should mean that there is a gigantic glut of gold and that its price would be in free fall.

But it isn’t. Gold is beating U.S. stocks and bonds this month. And this isn’t even a rarity. I’ve run some numbers and have found a couple of things that could be very important to retirees, and for all of us suckers saving for retirement.

Even though, according to traditional financial theory, they really make no sense at all.

The first thing is that over the past century including some gold in your portfolio alongside stocks and bonds has genuinely added value. It has produced higher average returns, less volatility and fewer of those disastrous “lost decades” where your portfolio ended up whistling Dixie.

The second thing is that this peculiarity has been showing no signs of letting up in recent years or decades — even though, if anything, gold makes even less sense today than it used to.

Let me explain.

As usual, I’ve tapped the excellent database maintained by the NYU Stern School of Business, which tracks asset values going back to 1928.

Over that period, a conventional so-called balanced portfolio invested 60% in the S&P 500 SPY, -0.06%

index of large-company stocks and 40% in U.S. 10-year Treasury bonds TMUBMUSD10Y, 3.832%

has generated an average return of 4.9% a year in “real” terms, meaning above inflation.

A portfolio that’s 60% invested in the S&P 500, 30% in the bonds and 10% in gold GC00, -0.26%

earned a slightly higher average, 5.1% a year in real terms. But the volatility was lower: The portfolio that included the gold had a lower standard deviation of returns, and a much higher “median” return, meaning the middlemost return if you ranked all the years from best to worst. The portfolio including gold beat the traditional one by five full percentage points in total over the typical 10-year period, and failed to keep up with inflation for 10 years on only five occasions — half as often as the portfolio consisting exclusively of stocks and bonds.

Nor is this just about olden times. The portfolio including 10% gold has beaten the traditional 60/40 by an average of 0.4 percentage point a year since President Richard Nixon finally killed the gold standard in 1971. And it has beaten the traditional portfolio by the same amount, an average of four-tenths of a percentage point, so far this millennium. (The 60/40 portfolio has done better if you start measuring only in 1980, as that ignores the golden 1970s but includes the long bear market for gold of the 1980s and 1990s.)

And gold has added value in five of the last seven years (while in the other two it was effectively a tie).

It’s not so much that gold is a great long-term investment on its own. It’s that gold has seemed to shine when others, specifically stocks and bonds, have failed. And it still does. It held up during the crash of 1929-32. But it also held up during the crash in 2002. And in 2008. And 2020.

A financial expert told me this was “hindsight bias.” But so is most financial analysis.

When your financial adviser tells you what you might reasonably expect from large stocks, small stocks, international stocks, real estate and so forth in the decades ahead, he or she is basing that on history. (In some cases this has been downright hilarious, as when advisers said you should still expect “average” historical returns of 5% a year from Treasurys, even when they had only a 2% yield.)

I’m danged if I know why. But so far this year, once again, you’ve been better off in a portfolio of 60% stocks, 30% bonds and 10% gold than in just 60% stocks and 40% bonds. Make of it what you will.

After a lifetime dedicated to service, Apostle Leina’ala Mars-Opoku earns the prestigious Presidential Lifetime Achievement Award

WASHINGTON D.C, USA, June 17, 2023/EINPresswire.com/ — On Friday, May 19, Apostle Leina’ala Mars-Opoku was distinguished with one of the highest honors given by the United States government, The Gold Lifetime Achievement Award.

The Biden’s Gold Lifetime Achievement Award is a prestigious honor that recognizes the efforts of individuals who have shown exemplary dedication to volunteer service. In order to achieve this award, individuals must meet a minimum of 4,000 volunteer hours, making this award incredibly difficult to achieve.

The President’s Volunteer Service Award acts as a symbol of American goodwill and is the embodiment of selfless leadership and community service. Through this award, the nation recognizes citizens who go above and beyond to effect change and improve lives, reinforcing the core values of altruism and public service.

Apostle Mars-Opoku is considered a spiritual powerhouse by her peers, and she has been a beacon of hope and faith from her early beginnings. Her steadfast dedication to serving God and humankind began at the young age of 8 when she first accepted Christ. There was no doubt that after receiving a prophetic word from God at 15, she was destined to become a great leader. Since that moment, Apostle Mars-Opoku has committed her life to spiritual service, overcoming…

Is America going into a recession or not? That depends on who you ask—and how old they are.

Consumer households from their 20s to their 50s are now spending sharply less on their credit and debit cards than they were a year ago reports Bank of America, after crunching the numbers on its customers.

A finance company boasting hundreds of apparently glowing online “customer reviews” and an A+ rating from the Better Business Bureau was this week civilly charged with cheating over 700 investors — many of them senior citizens — out of more than $30 million over 5 years.

El Segundo, Calif.–based Red Rock Secured and its controlling chief executive, Sean Kelly, were accused by the Securities and Exchange Commission of playing on the retirement and tax fears of older investors to sell them gold and silver coins at vastly inflated prices to hold in self-directed IRAs.

The markup on the coins “was almost always above 100 percent, and typically 120 percent or more,” the SEC said in its complaint.

Between 2017 and last year, Red Rock pocketed more than $30 million of the $50 million investors paid for the coins, said the SEC, which also sued two former Red Rock executives.

Attorney Michael Schafler of the Los Angeles law firm Cohen Williams, representing both Red Rock and its CEO, said the company had “nothing to hide” and has been “completely cooperative” with the SEC investigation.

“Red Rock has demonstrated that it is focused on compliance and providing clients with information necessary to make reasoned and informed decisions about purchasing precious metals,” he added. “Red Rock stands by that. It looks forward to the opportunity to defend itself against the government’s allegations in Court.”

According to the SEC, Red Rock used an aggressive marketing campaign to target investors, especially those who were “conservative” or “right wing” politically and “over 59½ [years old].”

Sales personnel played on customers’ fears about government policy, inflation, the stock market and retirement to persuade investors to move IRA funds to Red Rock and invest in gold and silver bullion, according to the SEC. But then, using what the commission calls a “bait and switch,” they persuaded investors instead to buy niche “premium” gold coins with huge, but hidden, markups, which included an 8% sales commission.

These so-called premium coins included an obscure silver Canadian coin for which Red Rock Secured controlled the entire market, allowing it to claim falsely that the “market value” of the coin was more than twice the value of its silver content, the SEC said.

Red Rock Secured salespeople were told to pitch the idea of a “worry-free retirement” to potential clients, while warning them that in the stock market “you could wake up and half your retirement could be gone,” the SEC said.

“The defendants used fear and lies to defraud investors out of millions of dollars from their hard-earned retirement savings,” said Antonia Apps, director of the SEC’s New York office.

There was no hint of any of this in the company’s glowing online “customer reviews.” At Google, Red Rock had an average rating of 4.8 stars out of 5 from 136 self-described customers. At Trustpilot, it got an average rating of 4.8 stars out of 5 from 167 alleged customers. Trustpilot said the rating was “excellent.” At the Better Business Bureau, Red Rock got an average rating of 4.75 stars out of 5 across 96 reviews. At Consumer Affairs it got an average rating of 4.9 stars out of 5.

The Better Business Bureau, contacted by MarketWatch, said it had added an alert to its site about the SEC probe into Red Rock. But, it added, “BBB ratings are not a guarantee of a business’s reliability or performance. BBB recommends that consumers consider a business’s BBB rating in addition to all other available information about the business.”

The organization, which provides information about businesses through a rating system and handles consumer complaints, said its standard policy is to check that all reviews are from legitimate customers by contacting the company being reviewed. The BBB does not possess legal or policing powers.

Business-review platform Trustpilot also told MarketWatch it had added an alert to the Red Rock Secured review page.

“Trustpilot is an open, independent review platform, meaning anyone who has had an experience with a business can leave a review — whether positive or negative — on the business’s Trustpilot profile page,” the company said in a statement “We are currently investigating Red Rock Secured to ensure that they are using our platform in line with our business guidelines, and should we find any evidence they are not, we will take the necessary steps to prevent it.”

When it comes to investing, some people don’t think in terms of thousands of dollars, tens of thousands, or even millions.

They think in hundreds of millions, or even billions. They have so much money they actually set up a private company, known as a “family office,” to manage all the loot.

David Rosenberg honestly doesn’t want to be bearish on stocks or bash the Federal Reserve. The veteran market strategist will get no satisfaction if he’s right about Americans having to slog through recession and consequently endure deflation, job losses and a wallop to the stock market.

“As I play the role of economic detective, I can see the smoking gun,” says Rosenberg, a former chief North American economist at Merrill Lynch and now president of Toronto-based Rosenberg Research.

David Rosenberg, the former chief North American economist at Merrill Lynch, has been saying for almost a year that the Fed means business and investors should take the U.S. central bank’s effort to fight inflation both seriously and literally.

Rosenberg, now president of Toronto-based Rosenberg Research & Associates Inc., expects investors will face more pain in financial markets in the months to come.

“The recession’s just starting,” Rosenberg said in an interview with MarketWatch. “The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle.” Investors can expect to endure more uncertainty leading up to the time — and it will come — when the Fed first pauses its current run of interest rate hikes and then begins to cut.

Fortunately for investors, the Fed’s pause and perhaps even cuts will come in 2023, Rosenberg predicts. Unfortunately, he added, the S&P 500 SPX, -0.61%

could drop 30% from its current level before that happens. Said Rosenberg: “You’re left with the S&P 500 bottoming out somewhere close to 2,900.”

At that point, Rosenberg added, stocks will look attractive again. But that’s a story for 2024.

In this recent interview, which has been edited for length and clarity, Rosenberg offered a playbook for investors to follow this year and to prepare for a more bullish 2024. Meanwhile, he said, as they wait for the much-anticipated Fed pivot, investors should make their own pivot to defensive sectors of the financial markets — including bonds, gold and dividend-paying stocks.

MarketWatch: So many people out there are expecting a recession. But stocks have performed well to start the year. Are investors and Wall Street out of touch?

Rosenberg: Investor sentiment is out of line; the household sector is still enormously overweight equities. There is a disconnect between how investors feel about the outlook and how they’re actually positioned. They feel bearish but they’re still positioned bullishly, and that is a classic case of cognitive dissonance. We also have a situation where there is a lot of talk about recession and about how this is the most widely expected recession of all time, and yet the analyst community is still expecting corporate earnings growth to be positive in 2023.

In a plain-vanilla recession, earnings go down 20%. We’ve never had a recession where earnings were up at all. The consensus is that we are going to see corporate earnings expand in 2023. So there’s another glaring anomaly. We are being told this is a widely expected recession, and yet it’s not reflected in earnings estimates – at least not yet.

There’s nothing right now in my collection of metrics telling me that we’re anywhere close to a bottom. 2022 was the year where the Fed tightened policy aggressively and that showed up in the marketplace in a compression in the price-earnings multiple from roughly 22 to around 17. The story in 2022 was about what the rate hikes did to the market multiple; 2023 will be about what those rate hikes do to corporate earnings.

“ You’re left with the S&P 500 bottoming out somewhere close to 2,900. ”

When you’re attempting to be reasonable and come up with a sensible multiple for this market, given where the risk-free interest rate is now, and we can generously assume a roughly 15 price-earnings multiple. Then you slap that on a recession earning environment, and you’re left with the S&P 500 bottoming out somewhere close to 2900.

This is just pure mathematics. All the stock market is at any point is earnings multiplied by the multiple you want to apply to that earnings stream. That multiple is sensitive to interest rates. All we’ve seen is Act I — multiple compression. We haven’t yet seen the market multiple dip below the long-run mean, which is closer to 16. You’ve never had a bear market bottom with the multiple above the long-run average. That just doesn’t happen.

David Rosenberg: ‘You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios.’

Rosenberg Research

MarketWatch: The market wants a “Powell put” to rescue stocks, but may have to settle for a “Powell pause.” When the Fed finally pauses its rate hikes, is that a signal to turn bullish?

Rosenberg: The stock market bottoms 70% of the way into a recession and 70% of the way into the easing cycle. What’s more important is that the Fed will pause, and then will pivot. That is going to be a 2023 story.

The Fed will shift its views as circumstances change. The S&P 500 low will be south of 3000 and then it’s a matter of time. The Fed will pause, the markets will have a knee-jerk positive reaction you can trade. Then the Fed will start to cut interest rates, and that usually takes place six months after the pause. Then there will be a lot of giddiness in the market for a short time. When the market bottoms, it’s the mirror image of when it peaks. The market peaks when it starts to see the recession coming. The next bull market will start once investors begin to see the recovery.

But the recession’s just starting. The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle when the central bank has cut interest rates enough to push the yield curve back to a positive slope. That is many months away. We have to wait for the pause, the pivot, and for rate cuts to steepen the yield curve. That will be a late 2023, early 2024 story.

MarketWatch: How concerned are you about corporate and household debt? Are there echoes of the 2008-09 Great Recession?

Rosenberg: There’s not going to be a replay of 2008-09. It doesn’t mean there won’t be a major financial spasm. That always happens after a Fed tightening cycle. The excesses are exposed, and expunged. I look at it more as it could be a replay of what happened with nonbank financials in the 1980s, early 1990s, that engulfed the savings and loan industry. I am concerned about the banks in the sense that they have a tremendous amount of commercial real estate exposure on their balance sheets. I do think the banks will be compelled to bolster their loan-loss reserves, and that will come out of their earnings performance. That’s not the same as incurring capitalization problems, so I don’t see any major banks defaulting or being at risk of default.

But I’m concerned about other pockets of the financial sector. The banks are actually less important to the overall credit market than they’ve been in the past. This is not a repeat of 2008-09 but we do have to focus on where the extreme leverage is centered.

It’s not necessarily in the banks this time; it is in other sources such as private equity, private debt, and they have yet to fully mark-to-market their assets. That’s an area of concern. The parts of the market that cater directly to the consumer, like credit cards, we’re already starting to see signs of stress in terms of the rise in 30-day late-payment rates. Early stage arrears are surfacing in credit cards, auto loans and even some elements of the mortgage market. The big risk to me is not so much the banks, but the nonbank financials that cater to credit cards, auto loans, and private equity and private debt.

MarketWatch: Why should individuals care about trouble in private equity and private debt? That’s for the wealthy and the big institutions.

Rosenberg: Unless private investment firms gate their assets, you’re going to end up getting a flood of redemptions and asset sales, and that affects all markets. Markets are intertwined. Redemptions and forced asset sales will affect market valuations in general. We’re seeing deflation in the equity market and now in a much more important market for individuals, which is residential real estate. One of the reasons why so many people have delayed their return to the labor market is they looked at their wealth, principally equities and real estate, and thought they could retire early based on this massive wealth creation that took place through 2020 and 2021.

Now people are having to recalculate their ability to retire early and fund a comfortable retirement lifestyle. They will be forced back into the labor market. And the problem with a recession of course is that there are going to be fewer job openings, which means the unemployment rate is going to rise. The Fed is already telling us we’re going to 4.6%, which itself is a recession call; we’re going to blow through that number. All this plays out in the labor market not necessarily through job loss, but it’s going to force people to go back and look for a job. The unemployment rate goes up — that has a lag impact on nominal wages and that is going to be another factor that will curtail consumer spending, which is 70% of the economy.

“ My strongest conviction is the 30-year Treasury bond. ”

At some point, we’re going to have to have some sort of positive shock that will arrest the decline. The cycle is the cycle and what dominates the cycle are interest rates. At some point we get the recessionary pressures, inflation melts, the Fed will have successfully reset asset values to more normal levels, and we will be in a different monetary policy cycle by the second half of 2024 that will breathe life into the economy and we’ll be off to a recovery phase, which the market will start to discount later in 2023. Nothing here is permanent. It’s about interest rates, liquidity and the yield curve that has played out before.

MarketWatch: Where do you advise investors to put their money now, and why?

Rosenberg: My strongest conviction is the 30-year Treasury bond TMUBMUSD30Y, 3.674%.

The Fed will cut rates and you’ll get the biggest decline in yields at the short end. But in terms of bond prices and the total return potential, it’s at the long end of the curve. Bond yields always go down in a recession. Inflation is going to fall more quickly than is generally anticipated. Recession and disinflation are powerful forces for the long end of the Treasury curve.

As the Fed pauses and then pivots — and this Volcker-like tightening is not permanent — other central banks around the world are going to play catch up, and that is going to undercut the U.S. dollar DXY, +0.70%.

There are few better hedges against a U.S. dollar reversal than gold. On top of that, cryptocurrency has been exposed as being far too volatile to be part of any asset mix. It’s fun to trade, but crypto is not an investment. The crypto craze — fund flows directed to bitcoin BTCUSD, +0.35%

and the like — drained the gold price by more than $200 an ounce.

“ Buy companies that provide the goods and services that people need – not what they want. ”

I’m bullish on gold GC00, +0.22%

– physical gold — bullish on bonds, and within the stock market, under the proviso that we have a recession, you want to ensure you are invested in sectors with the lowest possible correlation to GDP growth.

Invest in 2023 the same way you’re going to be living life — in a period of frugality. Buy companies that provide the goods and services that people need – not what they want. Consumer staples, not consumer cyclicals. Utilities. Health care. I look at Apple as a cyclical consumer products company, but Microsoft is a defensive growth technology company.

You want to be buying essentials, staples, things you need. When I look at Microsoft MSFT, -0.61%,

Alphabet GOOGL, -1.79%,

Amazon AMZN, -1.17%,

they are what I would consider to be defensive growth stocks and at some point this year, they will deserve to be garnering a very strong look for the next cycle.

You also want to invest in areas with a secular growth tailwind. For example, military budgets are rising in every part of the world and that plays right into defense/aerospace stocks. Food security, whether it’s food producers, anything related to agriculture, is an area you ought to be invested in.

You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios. If you follow that you’ll do just fine. I just think you’ll do far better if you have a healthy allocation to long-term bonds and gold. Gold finished 2022 unchanged, in a year when flat was the new up.

In terms of the relative weighting, that’s a personal choice but I would say to focus on defensive sectors with zero or low correlation to GDP, a laddered bond portfolio if you want to play it safe, or just the long bond, and physical gold. Also, the Dogs of the Dow fits the screening for strong balance sheets, strong dividend payout ratios and a nice starting yield. The Dogs outperformed in 2022, and 2023 will be much the same. That’s the strategy for 2023.

This is an opinion editorial by Q Ghaemi, a stocks and bitcoin analyst and author of the Qweekly Update newsletter.

Earlier this month, reports surfaced that the Central Bank of Iran is working with the Russian Association Of The Crypto Industry And Blockchain to create a stablecoin that will be backed by gold to settle trade. This is not the first foray into the crypto universe for either country, nor will it be the last. But this venture will come to nothing, ultimately bringing both countries one step closer to adopting Bitcoin.

Iran’s Foray Into Cryptocurrencies Favor Bitcoin

In August 2022, a headline came and went and most did not hear about it, and those who did gave it little thought: “Iran Approves Use Of Cryptocurrency For Imports To Bust Sanctions.” Ignoring the fact that the source for this headline was a Saudi-funded media outlet with the likely goal of destabilizing and delegitimizing Iran, it is important to recognize that Iran successfully completed a trade in August with an estimated value of $10 million, which can be assumed to have been conducted in bitcoin.

Based on daily volume, there are about 20 possible cryptocurrencies that could have been used to complete this transaction, however, if we take these cryptocurrencies by daily volume and agree that none with a daily volume less than $1 billion could have possibly been used (anything greater than 1% of daily volume would move the price too significantly: 1% of $1 billion is $10 million) we are left with seven possible cryptocurrencies: Ripple (XRP), Solana (SOL), USDC, Ethereum (ETH), Binance (BNB), Tether (USDT) and Bitcoin (BTC).

We can quickly eliminate USDC, Solana and Ripple because they are all run by U.S. corporations and, due to sanction laws (see: Tornado Cash), they would be forced to prevent Iran from using their platform (also it is safe to assume that the Iranian government chose to avoid U.S. companies for simplicity’s sake). Tether can also be thrown out given its link to the U.S. dollar. I will also throw out Ethereum because Iranians are too cheap to pay those gas fees. This leaves us with two options: BNB and Bitcoin. Personal bias aside, no one is settling international trade with BNB without Binance CEO Changpeng Zhao (CZ) taking some sort of a victory lap. Bitcoin wins.

Iran also previously banned Bitcoin mining operations due to stress on Tehran’s power grid. It has since returned all of the mining equipment and, as noted above, made the claim that $10 million in international trade was completed using cryptocurrency. Suffice to say, Iran has begun to see the potential of Bitcoin.

Russian Foray Into Cryptocurrencies Demonstrates Need For Unsanctioned Exchange

Russia has also begun to dip its toes in the broader cryptocurrency space. After the U.S. government responded to the invasion of Ukraine with sanctions, Russia was forced to explore alternatives to completing international trade. President Vladimir Putin’s response was to forgo the over $500 billion in its reserves and mandate that every buyer of Russian natural gas pay in Russian rubles. The ruble responded very positively to this news (see the chart below with a red arrow pointing to when U.S. sanctions began and a green arrow pointing to when the ruble became the only payment for Russian natural gas).

Russia then slowly began to reverse its 2020 position on cryptocurrencies. Late last year, Russia announced that it will allow international settlement in cryptocurrencies without any restrictions, a huge reversal from its previous stance. These moves prove that Russia sees the potential for cryptocurrencies as a medium of exchange.

Sanctions Make The Bond Stronger

Both countries have been on the receiving end of U.S./Western sanctions but have found ways to navigate around them to remain in power. The lesson that both of these countries have learned is to trust no one, especially in the world of finances. Putin profusely announced that by freezing Russia’s dollar holdings, it “practically defaulted,” signaling that even the mighty dollar may not be as mighty as the U.S. wants you to believe.

Iran is also no stranger to the empty promises of the West: after negotiating and agreeing to a nuclear deal in 2015, President Donald Trump came in and tore up the old agreement. While this may be common practice in some (shady) business ventures, this is an insult in Persian culture. Every indication that a new nuclear deal will be signed by Iran was laughable: why would Iran assume the next deal would be upheld after this president left office? Needless to say, the Iranian government has very little trust of foreign governments.

“The enemy of my enemy is my friend” plus “keep your friends close but your enemies closer” equals Iran/Russia relations.

In 2023, it almost makes sense to Westerners that Russia and Iran would work together. Both countries are deemed villains by many Western countries, and strict sanctions prevent them both from selling their resources to the world. Both have stockpiles of oil and gas that the world desperately needs. And yet, their history is far from harmonious.

Until the 1920s, both the U.K. and Russia fought over control of the resources of Iran. The Qajar dynasty would bend the knee and give anything foreign powers requested in exchange for wealth and riches for its family. This all changed after the 1921 coup brought an end to the Qajar dynasty and brought to power Reza Shah.

Reza Shah refused to give concessions to foreign powers and focused on growing Iran. The Soviet Union came to be one year later, which caused the USSR to focus on domestic growth as well. As Iran began to grow in importance to the West (chiefly to the U.K. and the U.S.), Reza Shah and his son (the last Shah of Iran, Mohammad Reza Shah), would use the West’s fear of communism to their advantage. If Iran would not get what it wanted from its Western trade partners, it would go make a small deal with the USSR to remind them who was in charge.

Despite the once contentious history between these two nations, it seems like they have found a common ground: perception as an enemy of the West.

Why The New Stablecoin Will Fail

I made a lofty claim that the stablecoin experiment between Iran and Russia will fail and cause them to adopt Bitcoin. How will it fail? There is no trust: there never was and there never will be.

Trust can be eroded while the network is being formed. While many Russian and Iranian leaders may believe that their countries’ top engineers can craft a product that is able to circumvent any adversarial attacks, what is to stop the other country from giving themselves backdoor access? What is stopping someone from creating a way to double spend tokens? Now, this is all conjecture: I am presenting just a handful of potential flaws in this system — how many more can you think of?

The largest question is regarding the gold reserves backing the stablecoin: Where will the gold be stored and who will verify that the amount of gold listed is still there? Given the lack of trust, neither country can be expected to blindly accept that the other is holding the amount of gold it claims to be (see “The Bitcoin Standard” for more on this topic), and sanctions prevent a reputable third party from getting involved (although China could fit into the puzzle in some way here).

As this very large and very important hurdle is met, another question will continue to loom: Why? Why do we need to do any of this when there is a cryptocurrency out there with enough liquidity to suffice their needs and that requires no trust in either party?

Both countries are still in the information-gathering stage and, if by some miracle, a researcher stumbles across this article, let me spell it out plain and simple: History has proven that when given the opportunity to control money, the people in charge will manipulate the money for their benefit.

There is a reason the Roman Empire fell and that we don’t use guilders or pounds as global currencies. Instead of bringing this temptation into the equation, adopting a trustless form of money that cannot be manipulated or inflated is the only solution. Bitcoin is the inevitable money you are looking for. Whether you get there before your enemies is up to you.

This is a guest post by Q Ghaemi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Ansel Lindner, a bitcoin and financial markets researcher and the host of the “Bitcoin & Markets” and “Fed Watch” podcasts.

Two forces have dominated the globe economically and politically for the last 75 years: globalization and trust-based money. However, the time for both of these forces has passed, and their waning will bring about a great reset of the global order.

But this is not the global, Marxist kind of Great Reset promoted by Klaus Schwab and those who attend Davos. This is an emergent, market-driven reset characterized by a multipolar world and a new monetary system.

Globalization Is Ending

The first reaction I usually get to my claim that the age of hyper-globalization is ending is flippant disbelief. People have so completely integrated the environment of the dying global order into their economic understanding that they cannot fathom a world where the cost-to-benefit analysis of globalization is different. Even after COVID-19 exposed the fragility of complex supply chains, like when the U.S. very nearly ran out of surgical masks and basic medications or when the world struggled to source semiconductors, people have yet to realize the shift that is happening.

Is it that hard to imagine that the businessmen who designed such fragile, overcomplicated production processes didn’t properly weigh the risks?

All that is needed to break globalization is for risk-adjusted costs to change a few percentage points and outweigh the benefits. The pennies saved by outsourcing numerous tasks to numerous jurisdictions will no longer outweigh the possibility of complete collapse of supply chains.

Gone is the time when complex supply chains were robust against typical risks. The risks today are much more systemic. Sure, there were skirmishes around the world and disagreements among parliaments, but great powers did not openly threaten one another’s spheres of influence. Risk-adjusted costs and benefits to globalization have radically changed.

Credit Doesn’t Like Conflict

Very closely related to deglobalization of supply chains is deglobalization of credit markets. The same factors that affect business peoples’ physical, risk-adjusted costs and benefits are also felt by bankers.

Banks don’t want to be exposed to the risk of war or sanctions wrecking their borrowers. In the current environment of deglobalization and rising risks to international trade, banks will naturally pull back on lending to those associated activities. Instead, banks will fund safer projects, likely fully-domestic or friend-shoring opportunities. The natural reaction by banks to this risky global environment will be credit contraction.

The deglobalization of supply chains and credit will be as closely linked on the way down as they were on the way up. It will start slowly, but pick up speed. A feedback loop of rising risk leading to shorter supply chains and less credit creation.

The Credit-Based U.S. Dollar

The prevailing form of money in the world is the credit-based U.S. dollar. Every dollar is created through debt, making every dollar someone else’s debt. Money is printed out of thin air in the process of making a loan.

This is different from pure fiat money. When fiat money is printed, the balance sheet of the printer adds assets alone. However, in a credit-based system, when money is printed in a loan, the printer creates an asset and a liability. The borrower’s balance sheet then has an offsetting liability and asset, respectively. Every dollar (or euro or yen, for that matter) is therefore an asset and a liability, and the loan that created that dollar is both an asset and a liability.

This system works extremely well if two factors are present. One, highly-productive uses of new credit are available, and two, a relative lack of exogenous shocks to the global economy. Change either of these things and a breakdown is bound to occur.

This dual nature of credit-based money is at the root of both the dollar’s spectacular rise in the 20th century, and the coming monetary reset. As global trust and supply chains break down, the comingling of assets in banks becomes more risky. Russia found this out the hard way when the West confiscated its reserves of dollars held in banks abroad. How is trust possible in that sort of environment? When credit-based money’s creation is based on trust… Houston, we have a problem.

Bitcoin’s Role In The Future

Luckily, we have experience with a world that doesn’t trust itself — i.e., the entire history of man prior to 1945. Back then, we were on a gold standard for reasons which included all those that bitcoiners are very familiar with (gold scores highly in the characteristics that make good money), but also because it minimized trust between great powers.

Gold lost its mantle for one reason — and you’ve probably never heard this anywhere before: because the global economic, political and innovation environment post-WWII created an extremely fertile soil for credit. Trust was easy, the major powers were humbled and all joined the new international institutions under the security umbrella of the U.S. The Iron Curtain provided a stark separation between zones of trust economically, but after it fell, there was a period of roughly 20 years where the world sang “kumbaya” because new credit was still extremely productive in the old Soviet block and China.

Today, we are facing the opposite sort of scenario: Global trust is eroding and credit has exploited all productive low-hanging fruit, forcing us into a period that demands neutral money.

The world will soon find itself split between regions/alliances of influence. A British bank will trust a U.S. bank, where a Chinese bank will not. To bridge this gap, we need money that everyone can hold and respect.

Gold Vs. Bitcoin

Gold would be the first choice here, if not for bitcoin. This is because gold has several drawbacks. First, gold is owned mainly by those groups who are losing trust in one another, namely the governments of the world. Much of the gold is held in the United States. Therefore, gold is unevenly distributed.

Second, gold’s physical nature, once a positive holding profligate governments in check, is now a weakness because it cannot be transported or assayed nearly as efficiently as bitcoin.

Lastly, gold is not programmable. Bitcoin is a neutral, decentralized protocol that can be tapped for any number of innovations. The Lightning Network and sidechains are just two examples of how Bitcoin can be programmed to increase its utility.

As globalization of both trade and credit is breaking down, the economic environment favors a return to a form of money that doesn’t depend on trust between major powers. Bitcoin is the modern answer.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Mike Ermolaev, head of public relations and content at Kikimora Labs.

Setting The Context: Global Economy Fundamentals

The economy is still recovering from the COVID-19 outbreak as new problems arise. We are now in a time of rampant inflation with central banks trying to remedy that by raising interest rates.

The U.S. CPI data (consumer price index), released on October 13, came in higher than expected (8.2% year-over-year), negatively impacting the bitcoin price. But inflation is not the only issue, the global economy is also struggling with the energy crisis, affecting Europe more than the U.S., due to its strong dependency on Russian natural gas and raw material.

On the eastern side, the war in Ukraine with ensuing sanctions on Russia, add further geopolitical instability and economic uncertainty. Also, China’s zero-COVID policy is disrupting the supply chain worldwide, and the Evergrande default undermines one of the world’s biggest economies.

If we look at the main currencies, the dollar index looks strong, compared to others. The Federal Reserve raised interest rates by 75 basis points in November, and the Bank of England raised interest rates by the same amount. This policy of quantitative tightening aims to reduce the money supply and mitigate price pressure. It is likely to continue into next year and beyond. However, a global recession and risk of stagflation is still very strong, so no country may feel safe from central bank monetary policy.

Bitcoin Correlation With The Economy

Bitcoin has shown not to be immune from this global turmoil. Although the price in its early stage was independent of traditional finance, correlation began to show in 2016.

The idea of bitcoin as a “digital gold” became popular because both shared the scarcity and difficulty of extraction (mining), as well as fulfilled the role of being a store of value. Since many view bitcoin as a risk asset, its correlation with the S&P 500 and Nasdaq-100 became visible — no different than traditional stocks.

At the time of writing, bitcoin’s 40-day price correlation with gold reached 0.50 (after being around zero in August). According to Alkesh Shah and Andrew Moss, strategists from Bank of America:

“A decelerating positive correlation with SPX/QQQ and a rapidly rising correlation with XAU indicate that investors may view bitcoin as a relative safe haven as macro uncertainty continues and a market bottom remains to be seen.”

Negative Events

There are some macroeconomic factors in the larger cryptocurrency ecosystem that contributed to a bearish market: the Terra/LUNA collapse, forced liquidation of Three Arrows Capital and the bankruptcy of Celsius being the main ones.

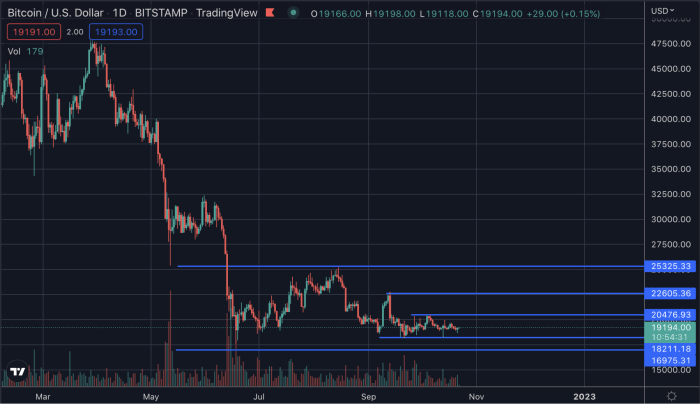

Despite all the above adverse events, bitcoin was able to somehow keep its price in the $19,000-$20,000 range, with record-low volatility. Currently, we are observing unusual stability in the bitcoin price, recently even matching volatility of the British pound.

On the contrary, stocks have experienced high volatility and whipsaw price action, also following speculations about the Fed’s future decisions. According to Bloomberg’s Chief Commodity Strategist Mike McGlone, that’s why bitcoin may rise after a steep discount and eventually beat the S&P 500. He believes that bitcoin’s finite supply and deflationary approach may help it recover its previous price levels.

Since the last flash crash in mid-June, the price has been quite steady, but we know it rarely sits still for too long. This means that the probability of a sudden (bullish or bearish) breakout increases over time. The longer the price remains idle, the stronger the breakout is going to be.

Bitcoin price consolidation

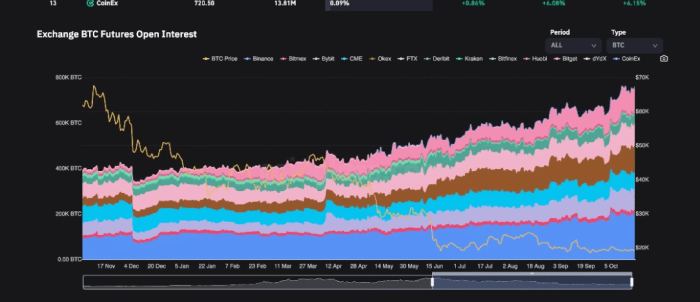

Additionally, the BTC futures open interest is higher than ever, with liquidations reaching all-time low. A lot of liquidity is accumulating here, meaning that there will be an even stronger impulse when the price starts to move again.

According to the strategist Benjamin Cowen, bitcoin is expected to rise to “fair value,” after falling an additional 15%. “Right now, the data would suggest that we’re about 50% undervalued compared to where the fair value is.” Cowen thinks we may need to wait until early 2024 to see this rise happen.

Goldman Sachs strategist Kamakshya Trivedi has a different view, claiming that the U.S. dollar index, showing record values since 2002, may be bad news for the currently bearish bitcoin.

A Bearish Scenario: Could The 2018 Drop Happen Again?

Some analysts have been wondering if the 2018 scenario (low volatility, then big price drop) may happen again today because the market conditions look quite similar. We have the same 10% trading range and we know something is going to happen soon.

Comparison between 2022 BTC price (top) versus 2018 (bottom) using eight-hour candles. (Source)

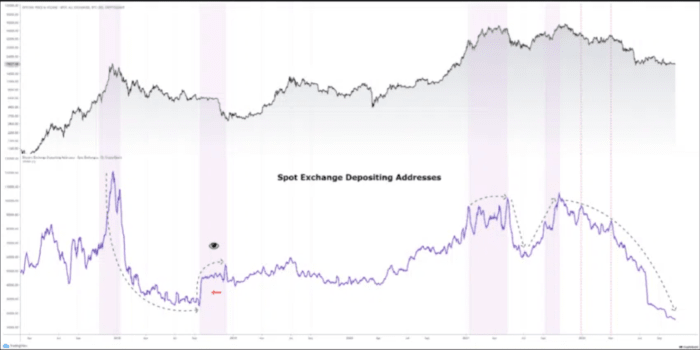

A remarkable difference between the two cycles is that in 2018 there was an increase in addresses sent to spot exchanges, while in our current cycle we are observing liquidity moving away from exchanges and not many new addresses being created. According to a CryptoQuant analyst, this should mean that we won’t witness a similar scenario to 2018.

A 2018/2022 comparison of spot exchange depositing addresses. (Source)

What About Uptober and Moonvember?

Historically, Q4 is a great time for bitcoin, with bullish trends starting in October and increasing in November. So the months of October and November were colloquially renamed “Uptober” and “Moonvember” — at least, this is what happened back in 2021.

Can we still expect such a bullish Q4 in 2022? It’s hard to say, but the adverse macroeconomic situation and geopolitical issues make it harder to imagine the same rally we saw last year. After all, the bitcoin market has been down for 10 consecutive months and we don’t see any particular sign of recovery at the moment.

We must also keep in mind that, despite the negative global scenario, the “safe haven” role of bitcoin may contribute to giving the price some additional strength, especially in these troubled times.

Exchange Data Analysis

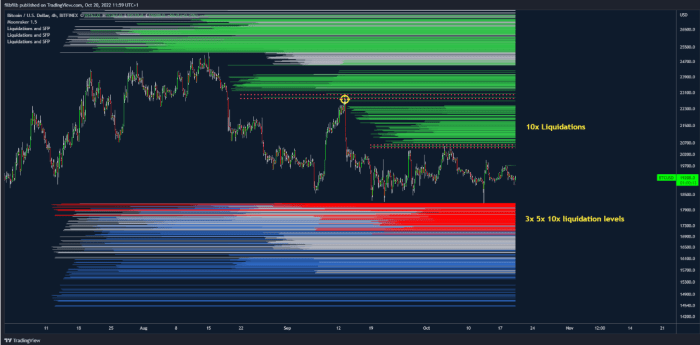

Liquidation data on the Bitfinex exchange was analyzed by filbfilb. He concluded that an upward breakout would have less momentum than a downward one. In fact, liquidity above $20,500 is mostly 10x, while liquidity below $18,000 is predominantly 10x, 5x and 3x, which means that a bullish breakout would be “less brutal” than a bearish one.

We are currently witnessing a period of stasis in the bitcoin market. The bitcoin price needs to start moving again after two months of consolidation. The overall economic scenario doesn’t look bright at all, and bitcoin is correlated to events in the real world, but investors can still recognize the digital gold, safe-haven role of the most popular cryptocurrency. A strong bitcoin price breakout is expected, with new volatility incoming.

The possible scenarios may be: a quick dump and then a bullish recovery (V-shaped bounce) or a longer and deeper price collapse, after the break of the $19,000 resistance level.

Whatever happens, bitcoin will keep being the most innovative technology of the last decade, allowing financial freedom and direct control over one’s own wealth. Bitcoin has historically witnessed numerous strong bearish times and has always recovered from them.

This is a guest post by Mike Ermolaev. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

Opinions expressed by Entrepreneur contributors are their own.

Gold has long been regarded as one of the most effective investments for protecting one’s wealth from various possible adverse financial effects. A plummeting stock market and an increase in inflation are two examples of these hazards. Currently, inflation is at extremely high levels, yet gold prices have not been doing particularly well. In terms of the U.S. dollar, it has decreased by over 10% so far this year, which contradicts the overarching perception of gold as an inflation hedge.

Uncovering the appeal of gold as a traditional inflation hedge

To reduce their risk exposure, traders and investors in the financial markets often use a strategy known as hedging. In most cases, this is accomplished by creating an opposite position in the market to compensate for any loss that may have been made in their primary position. Hedging may be thought of in a straightforward manner by comparing it to purchasing an insurance policy. When we speak about hedging against inflation, we are referring to the process of preserving your capital from the depreciating effects of inflation. Therefore, to hedge against inflation, investors want assets that are unaffected by growing inflation.

Gold has always been seen as a hedge against inflation throughout time. As a result, it is the asset of choice for investors who want to ensure that their money will continue to have the same buying power in the future while minimizing the amount of risk they are exposed to. When there is an uptick in inflation that is being kept under control, central banks will not necessarily vote to raise their key interest rates automatically. This indicates that the real interest rates, calculated by subtracting the nominal interest rate from the inflation rate, will be negative for assets such as government bonds.

When interest rates are at historically low levels, gold’s ability to shift in the opposite way of real interest rates makes it an efficient hedge against inflation. Because of this, investors can protect the value of their funds from experiencing a significant decline.

In March 2022, as a direct consequence of the conflict between Ukraine and Russia, the price of gold reached an all-time high of more than $2,000 per ounce. Although inflation has reached record highs, gold prices have been falling for the last few months.

As interest rates continue to climb, some investors are considering selling gold, which does not pay interest, to purchase assets that do pay interest. Temptations come in the form of greater returns, which are now accessible in bonds, property or even shares of stock. Other temptations come in the form of higher interest rates on cash.

Gold’s position in comparison to other asset classes — such as stocks, currencies and bonds — has recently seen significant shifts due to these developments. All asset classes function independently of one another for various reasons, including changes in how the economy operates, modifications to monetary and fiscal policy and many other factors. Because each of these asset classes experiences a different price action dependent on a variety of factors, including supply and demand, the prevailing interest rate regime, inflation, gross domestic product and other factors, investors should view each of these asset classes as having equal importance.

Nowadays, the reputation of gold as a trustworthy hedge against inflation is in jeopardy as investors go to other parts of the market in which they might seek refuge from increasing costs.

Some analysts consider that gold is a good method to protect oneself against inflation before it occurs. However, the situation changes drastically whenever there is significant price inflation — assuming that the Fed successfully brings inflation under control. Once inflation has reached a high level, it is essentially too late to “hedge” against the inflation that has already occurred, and the gold prices often suffer when the dollar is stronger as well. The price of bullion is expressed in terms of the U.S. dollar, and a strong dollar has the effect of dampening excitement.

“Gold seems to protect purchasing power over a long period — say, 100-plus years — but provides very little protection against inflation in the short term,” according to Kevin Lum, a CFP and founder of Foundry Financial.

While buying gold coins or bars for investment purposes we often only compare prices without paying heed to the purity of the yellow metal. This could be a mistake as purity plays an important role and could be the one of the main reasons for variation in prices.

“The buyer should only invest in the purest quality gold available to them, as the additives such as copper or silver corrode over time, which harms your investment. For jewellery, in any case, the purity is 18K or 22K as lower-purity gold is harder and more durable. However, in coins and bars the highest level of gold purity is 99.99% while the market standard is 99.5% or 99.9%,” says Gaurav Mathur, Founder & MD, SafeGold, a homegrown digital currency platform.

Millesimal Fineness, a system denoting the purity of gold, measures the purity by parts per thousand or the percentage of gold, instead of karats. Under this, 999 means that your 24K gold is 99.90% pure and other metal constitutes only 0.1%. Similarly, 999.9 means your gold is 99.99% pure, which means only 0.01% is other metal. Before buying, it is always better to ask your jeweller, bank, or digital platform about the purity of gold. For example, in the case of MMTC-PAMP and SafeGold gold products the purity is 99.99%. Usually, jewelleries come in different purity levels ranging from 14K, 18K, 22 K which indicate a fractional measure of purity for gold alloys.

“Our entire communication with the customer is that not only are you getting the purest goal, but also the only ones with a four-nine purity, which basically means 99.99 per cent,” says Vikas Singh, MD and CEO of MMTC-PAMP, a joint venture between Switzerland-based bullion brand, PAMP SA, and MMTC Ltd, a Government of India undertaking.

However, purity does not hold much relevance while purchasing digital gold online. It only matters when you ask for delivery of your gold. “What matters more is the reliability of the digital gold provider and if they have a robust structure of independent checks and balances to ensure the safety of your gold,” says Mathur.

Does the highest purity come with an additional cost? The expert says that there is no additional cost for higher purity. Just check the provider’s delivery options to ensure that 99.99% of gold coins are available for delivery. “To clarify, the rate per gram of pure gold is the same for 995 or 999.9 purity. The headline rate of gold will be higher in cases of higher purities. This is because the rate has a direct relation with the additional grams of pure gold. For example, if the rate for 995 is Rs 5000/gm, the rate for 999.9 will be 5000 x 999.9/995 = Rs. 5024.62/ gm,” says Mathur.

Burton Mills – The World Gold Council suggests that annual global gold production may not be capable of exceeding current levels.

Press Release –

updated: Sep 28, 2017

TAIPEI, Taiwan, September 28, 2017 (Newswire.com)

– Burton Mills: The World Gold Council has announced that global gold production may have reached what it is calling “peak gold”. The term was traditionally been applied to oil production at a time when producers were unable to increase production beyond a certain point but the term “peak oil” has recently fallen into disuse as a glut of oil suppresses global oil prices.

According to Taipei, Taiwan-based investment boutique, Burton Mills, production of gold will likely plateau before slowly decreasing as demand for the precious metal grows, particularly in light of geopolitical risks and vigorous purchases by traditional consumers in India and China.

The firm’s comments echo those of WGC Chairman, Randall Oliphant who opined that uncertainty over how the US political landscape would unfold may drive more investors into the perceived safety of gold. Mr. Oliphant has served as an executive on several of the world’s largest gold producers.

Speaking at the Denver old Forum, the Chairman suggested that gold prices could rise to as high as $1400.00 an ounce within the next year. Burton Mills has a bullish outlook on gold prices despite the metal’s lackluster performance this year. The firm believes that US interest rates are highly unlikely to return to historical norms and, consequently, the US will slowly lose the safe-haven attributes some investors apparently have confidence in.

However, since reaching a record $1,923.70 in 2011, gold prices have retraced as much as 50% leading some to speculate that, with inflation running low in many developed economies, the precious metal may not see a return to glory for a decade or more.

Mr. Oliphant told gathered delegates that he found it difficult to envision a gold mining industry that was capable of meeting future demand.

Contact: Biz City News – Lane 167, Section 8, Minquan East Road, Neihu District, Taipei City, Taiwan 114. info@bizcitynews.com

Introducing the Winter Wonderland and One Country Christmas collections – Creative accessories to make your planner sparkle!

Press Release –

Oct 17, 2016

Eatonville,Washinton, October 17, 2016 (Newswire.com)

– Amber Mace, designer and owner of One Crafty Country Girl, is proud to announce the unveiling of two new winter collections for the upcoming holiday season. These two collections feature exclusively designed accessories to decorate the inside and outside of an organized individual’s favorite tool, a planner. Designed to fit the most popular brands of ring-binder and disk planners, these two stunning collections include uniquely designed and handcrafted planner charms, tassels, planner stickers, and resin-topped paperclips.

The Winter Wonderland collection invites us to sparkle into the season with colors inspired by ice crystals and the winter night sky. Sparkly crystal snowflakes and pearlescent beads hang from a gold or silver chain in the planner charms, designed to clip to the upper ring or disk of a planner. The charm can dangle outside the planner as decorative bling or hang inside the planner as a place-marker. Planner stickers in the Winter Wonderland collection include scenes of snowy landscapes, clouds and stars, and other winter themes. A limited edition of angel and snowflake pendant necklaces lovingly handmade from crystal beads will be available as part of the collection.

The One Country Christmas collection is an invitation to recapture the moments with a nostalgic, country feel of warm memories and firelight, cocoa and marshmallows, warm mittens and stockings hung by the fire. Warm reds, greens and creamy ivory are the colors associated with this collection. The planner charms in the One Country Christmas collection feature golden deer and silver Christmas trees, while the planner stickers include charming images of foxes, owls and pine cones. Paperclips are topped with resin shapes of snowmen, wrapped gifts and roses embellished with glitter. Both collections will be launched on October 20, 2016, just in time for the holiday shopping season.

About One Crafty Country Girl: Amber Mace lives in Eatonville, Washington with her husband and 13-year-old son, whom she home schools. Due to health issues, Amber was inspired to begin her home-based business to help provide for her family. She makes awareness boxes each month and donates half of the proceeds of those sales to different charities, benefiting breast cancer awareness, narcolepsy, etc. Her hobbies include designing planner accessories, spending time with her family, watching football and supporting her favorite team, the Seattle Seahawks. Her new website is scheduled to launch in January 2017.

The new brand launches this week with The Essential Home Collection featuring metallic gold art prints.

Press Release –

Oct 3, 2016

Seattle, WA, October 3, 2016 (Newswire.com)

– Emma + August is proud to announce The Essential Home Collection, set to premiere on October 7th, 2016. This 10-piece collection features radiant gold foil art prints with real shine. Each print is meticulously handcrafted by life-long artist and shop creator, Em Marshall. Em uses high quality matte paper made with renewable energy from responsibly managed forests. When asked about her creation process Em said, “I use unique mixed media techniques, lots of love, and my own two hands. My inspiration for this collection comes from the desire to help others create a positive and blissful home. I love to work with gold because it’s both modern and timeless.” Em’s much anticipated limited edition original, “Her,” a self-portrait in rose gold, is expected to sell out.

Shoppers will enjoy the new Emma + August golden maps, now introducing yellow gold and rose gold world map prints, ideal for any room or office. Emma + August is also releasing detailed city map prints from around the world. It’s starting now with The Pacific Northwest, featuring Seattle, WA; Portland, OR; and Vancouver, BC, as well as a European limited edition set of Rome, Paris, and Prague. Em explains, “These golden city maps were designed with the idea in mind that now, you can take your favorite cities home with you.”

“I use unique mixed media techniques, lots of love, and my own two hands. My inspiration for this collection comes from the desire to help others create a positive and blissful home. I love to work with gold because it’s both modern and timeless.”

Em Marshall, Owner of Emma + August

Other pieces in The Essential Home Collection include a four-piece Botanical Set featuring the rose, iris, orchid, and poppy; a three-piece Sea Creatures Set with vintage sketches of the turtle, lobster, and crab, a Hops Sketch for beer lovers, an American Bison print, a Good Vibes Only sign, and a Record Player print, all in alluring metallic gold foil. Shoppers have the choice of a clean and chic white and gold print, or a bold and powerful black and gold print.