[ad_1]

S&P flash U.S. services index rises to 51.3 in December from 50.8

[ad_2]

Jeffry Bartash

Source link

[ad_1]

S&P flash U.S. services index rises to 51.3 in December from 50.8

[ad_2]

Jeffry Bartash

Source link

[ad_1]

The U.S. dollar has completed its first “golden cross” since July 2021, which could mean the greenback is going higher, creating more problems for stocks.

Heading into Friday’s settlement, the 50-day average on the ICE U.S. Dollar Index

DXY,

a gauge of the buck’s value against a basket of its biggest rivals that’s heavily weighted toward the euro, stands at 103.15, higher than the 200-day moving average, which was 103.11.

The index itself finished at 105.56 on Friday, trading at its highest level since March 10, 2023, the day that the Silicon Valley Bank collapsed, sparking a brief rally in safety plays like the dollar. It climbed 0.2% this week, booking its 10th straight weekly advance, its longest such streak since a 12-week sprint that ended in October 2014.

A golden cross occurs when the 50-day moving average closes above the 200-day moving average. It’s a popular signal among technical analysts and often — though definitely not always — signals that momentum is building in a given direction.

On the other hand, a “death cross” occurs when the 50-day moving average breaks below the 200-day. A “death cross” in the U.S. dollar occurred on Jan. 10. Afterward, the buck trended lower for the next six months, ultimately hitting its lowest level of 2023 on July 14. Since then, the buck has been in a sustained uptrend that some currency strategists think has grounds to continue, now that the Federal Reserve bolstered its forecast to keep interest rates above 5% through 2024.

According to an analysis by Dow Jones Market Data, the dollar typically continues to climb during the three months following a golden cross, gaining an average of 1.9%, while trading higher 79.2% of the time over. Performance is more mixed one year out, with the buck higher 58.3% of the time, with an average gain of 1.5%.

And if the previous golden cross is any guide, the dollar’s recent gains could be just the beginning of a larger advance. After a previous golden cross on July 29, 2021, the dollar index gained roughly 25%, advancing from about 91 to just shy of 115 in late September of 2022, when it touched its strongest level in two decades, according to FactSet data.

Some analysts have warned that the dollar’s advance, alongside rising Treasury yields, could create more problems for stocks. The S&P 500

SPX

fell more than 1.6% on Thursday, its biggest drop in a single day since March 22, according to Dow Jones Market Data.

“A new cycle high in yields and a golden-cross in the dollar are strong headwinds for the market,” said Jeffrey deGraaf, a technical strategist at Renaissance Macro Research, in a note to clients.

[ad_2]

[ad_1]

The U.S. dollar is proving its haters wrong.

Not only is the buck defying the expectations of Wall Street strategists who had anticipated that it would weaken this year, it’s also proving once again that talk of de-dollarization has been over-hyped.

In financial markets, a gauge of the dollar’s value against its biggest rivals is nearing its highest level in six months. The ICE U.S. Dollar Index

DXY,

a gauge of the dollar’s strength against the euro

EURUSD,

and other major currencies like the Japanese yen

USDJPY,

and British pound

GBPUSD,

traded at its highest level since early June on Friday after Federal Reserve Chairman Jerome Powell helped catapult it higher by talking up the possibility of more interest-rate hikes.

The index was adding to those gains on Monday, trading 0.1% higher at 104.13, according to FactSet data. A break above 104.70 would put it at its highest intraday level since March 16. The index is up 0.5% since the start of the year, having erased earlier year-to-date losses over the past six weeks.

Earlier this year, dollar weakness occurred against the backdrop of U.S. rivals like China and Russia making strides in their efforts to wean themselves off the buck.

But despite their efforts, data released last week by SWIFT, the nexus of international interbank financial transactions, showed that the dollar has never been more popular as a means of settling international trade and transactions.

SWIFT’s data showed that 46% of interbank payments conducted on the platform in July involved the U.S. dollar, a record high. The data also showed that the Chinese yuan’s share of international payments had ticked higher while the euro’s declined.

As if to underscore this point, the data from SWIFT arrived late last week just as a summit hosted by the BRICS nations in Johannesburg, South Africa, was breaking up.

Rather than being a watershed event for opponents of the U.S. dollar, as some had feared, statements from the group’s members revealed internal disagreement on the subject of a BRICS currency intended to offer an alternative to the greenback.

What’s more, while the economic alliance announced plans to admit a spate of new member nations in its first expansion in 13 years, one notable holdout seemed to spoil the party.

Indonesian President Joko Widodo opted to keep his country, one of the world’s most populous, with a fast-expanding economy, out of the economic alliance, at least for now.

To be sure, as MarketWatch reported back in April, talk of de-dollarization is hardly a new phenomenon, but it has received renewed attention as China, Russia and others have redoubled efforts to try and push for countries to conduct more trade in their own currencies as opposed to the dollar.

But Russia and China aren’t alone in their disappointment at the dollar’s resilience.

Read more: Opinion: China is nowhere near deflation, and global investors aren’t ready for what’s coming

A compilation of 2023 year-ahead outlooks produced by Bloomberg News back in December showed investment houses in Europe and the U.S. widely expected the buck to weaken this year, with some reasoning that the two-decade high reached by the dollar index in late September likely marked its peak for the cycle.

The ICE index traded as high as 114.78 on Sept. 28, its highest level since May 2002, according to FactSet data. The milestone marked the peak of a torrid rally that saw the buck emerge as one of the few havens from a punishing selloff in stocks and bonds that defined global markets in 2022. But the gauge has fallen 9.3% since then.

Now, with real yields in the U.S. pushing higher and Federal Reserve Chairman Jerome Powell hinting at the possibility of more interest-rate hikes later this year, strategists say the conditions are ideal for the U.S. dollar to climb even higher.

“Interest-rate differentials and relative economic strength are the foundation [of dollar strength],” Matt Miskin, co-chief investment strategist for John Hancock Investment Management, said during a phone interview with MarketWatch.

China’s struggles to revive its flagging economy have helped bolster the dollar while pushing the Chinese yuan

USDCNY,

toward its weakest level since late last year. The offshore yuan traded at 7.29 to the dollar on Monday, near its weakest level since November.

Read this next: Opinion: The debt supercycle that hit the U.S. and Europe has now come for China

A weakening eurozone economy has weighed on the euro and boosted the dollar. PMI survey data released earlier this month showed Europe’s services sector weakening alongside manufacturing. GDP data released by Eurostat, Europe’s official economic statistics agency, has been tepid compared to the U.S. The latest reading on second-quarter GDP put it at 0.3%.

Right now, the dollar will be tough to beat given the twin tailwinds created by rising real interest rates and still-robust economic growth.

The yield on the 10-year Treasury Inflation-Protected Security note

912828B253

was trading north of 2.2% Friday, according to data from the St. Louis Fed. The 10-year TIPS yield hit its highest level since 2009 earlier this month when it broke north of 2%. The inflation-protected security is often cited as a proxy for U.S. “real” yields, which refers to the return bond investors receive after adjusting for inflation.

On the growth side of the equation, the Atlanta Fed’s GDPNow forecast estimated the rate of growth for the third quarter at 5.9% according to its latest reading dated Thursday. A year ago, even the most optimistic economists on Wall Street were expecting growth of about 2%, and top Fed officials had a median projection of 1.2% growth for 2023, according to projections released in September.

“It’s hard to beat the dollar when it is a high yielder among safe havens in a risk-off environment,” Steve Englander, head of North America macro strategy at Standard Chartered, said in comments emailed to MarketWatch.

[ad_2]

[ad_1]

Federal Reserve Chair Jerome Powell set a high bar for additional interest-rate hikes, economists said Sunday in their commentary on all the talk at the U.S. central bank’s summer retreat in Jackson Hole, Wyo.

Michael Feroli, chief U.S. economist for JPMorgan Chase, said that the Fed chair certainly did not give a clear signal that more tightening was coming soon. He noted that Powell stressed the Fed would “proceed carefully” and balance the risks of tightening too much or too little.

“We remain comfortable in our view that the FOMC will stay on hold for the next several meetings,” Feroli said.

Read: Powell unsure of need to raise interest rates further

The caveat to this forecast is if inflation surprises to the upside or the labor market does not continue to soften.

Ian Shepherdson, chief economist at Pantheon, said that Powell’s speech seemed hawkish to some, particularly because the Fed chair made threats to hike again.

But Shepherdson said he thought the Fed “is likely done.”

“Behind the caveats, Mr. Powell’s speech fundamentally was optimistic, though cautious,” Shepherdson said.

Boston Fed President Susan Collins also emphasized patience in an interview with MarketWatch on the sidelines of the Jackson Hole summit.

Read: Fed has earned the right to take its time, Collins says

Other regional Fed officials who spoke “hinted that further action may be needed, but also observed that inflation is moving in the right direction and that the surge in yields would help cool down the economy,” said Krishna Guha, vice chairman of Evercore ISI, in a note to clients.

Traders in derivative markets expect a rate hike in November, but it is a close call, with the odds just above 50%.

The Monday following Jackson Hole has historically been an active one in the markets, across asset classes.

The 10-year Treasury yield

BX:TMUBMUSD10Y

ended last week just above 4.2%.

Read: Market Snapshot on Powell’s stance

The first test of the careful and patient Fed will come this coming Friday, when the government will release the August employment report.

Economists surveyed by the Wall Street Journal expect the U.S. economy added 165,000 jobs in the month. That would be the weakest job growth since December 2020.

In his speech on Friday, Powell emphasized that evidence that the labor market was not softening could “call for a monetary policy response.”

Economists at Deutsche Bank think an upside surprise in the employment data could provide enough discomfort for the Fed, and raise expectations for further tightening.

Other top global central bankers spoke at Jackson Hole, including European Central Bank President Christine Lagarde, Bank of Japan Gov. Kazuo Ueda and Bank of England Deputy Governor Ben Broadbent.

Guha of Evercore said he detected a careful effort by the officials not to surprise markets.

The exception to this rule might have been Bundesbank President Joachim Nagel, who said in a television interview that it was too early for the ECB to think about a rate-hike pause.

[ad_2]

[ad_1]

Worries about a possible policy tweak by the Bank of Japan threw a wet blanket on a stretched U.S. stock-market rally Thursday, with the Dow Jones Industrial Average snapping its longest winning streak since 1987 after the 10-year Treasury yield surged back above the 4% level.

The Japanese yen also strengthened after a news report said policy makers on Friday would discuss a possible tweak to the Bank of Japan’s so-called yield-curve control policy that would loosen the cap on long-dated government bond yields.

Nikkei, without citing sources, reported that BOJ officials would talk about the matter at Friday’s policy meeting and that the potential change would allow the yield on the 10-year Japanese government bond

TMBMKJP-10Y,

to trade above its cap of 0.5% “to some degree.”

Why is that a negative for U.S. Treasurys and, in turn, U.S. stocks?

The “ultimate fear” is that Japanese investors, who have vast holdings of U.S. fixed income, including Treasury notes and other securities, “begin to see a higher level of yields in their own backyard,” Torsten Slok, chief economist at Apollo Global Management, told MarketWatch in a phone interview. That could prompt heavy liquidation of those U.S. positions as investors repatriate holdings to reinvest the proceeds at home.

That dynamic explains the knee-jerk reaction that saw the 10-year U.S. Treasury yield

TMUBMUSD10Y,

surge more than 16 basis points to end above 4%, he said. Yields rise as debt prices fall.

The surge in yields, in turn, saw stocks give up early gains, with U.S. indexes ending lower across the board.

The Bank of Japan began implementing yield curve control, or YCC, in 2016, a policy that aims to keep government bond yields low while ensuring an upward-sloping yield curve. Under YCC, the BOJ buys whatever amount of JGBs is necessary to ensure the 10-year yield remains below 0.5%.

Nikkei said a possible tweak would allow gradual increases in the yield above 0.5%, but would clamp down on any sudden spikes, allowing the BOJ to rein in fluctuations driven by speculators.

Global market participants are sensitive to changes in YCC. The BOJ sent shock waves through markets in December when it lifted the cap from 0.25% to 0.5%. Investors were rattled by the prospect of the Bank of Japan giving up its role as the remaining low-rate anchor among major central banks.

BOJ Gov. Kazuo Ueda in May said the bank would start shrinking its balance sheet and end its yield-curve control policy if a 2% inflation looks achievable and sustainable after many years of undershooting.

The yield on the 10-year JGB has traded above 0.4%, but remained below the 0.5% cap. Continued interest rate rises by the Federal Reserve and other major central banks in the past year have raised worries that the 10-year JGB yield could test the limit, Nikkei reported. Those rate hikes, meanwhile, have added pressure to the yen, whose weakness is seen contributing to inflation pressures.

The yen

USDJPY,

strengthened following the report. The U.S. dollar was off 0.5% versus the currency, fetching 139.48 yen.

The Dow Jones Industrial Average

DJIA,

ended the day down nearly 240 points, or 0.7%, snapping a 13-day winning streak, while the S&P 500

SPX,

declined 0.6% and the Nasdaq Composite

COMP,

lost 0.5%.

Japanese stocks have solidly outpaced strong gains for U.S. equities in 2023, with the Nikkei 225

NIK,

up 26% so far this year versus an 18.7% rise for the S&P 500.

See: Japan’s stock market is roaring 25% higher. These 4 things could keep the rally going.

Investors are waiting to see what the Bank of Japan actually has to say.

While the Nikkei report helped “exaggerate” a selloff in Treasurys, the market may be inoculated against bigger swings after the BOJ’s December adjustment to the rate band, said Ian Lyngen and Benjamin Jeffery, rates strategists at BMO Capital Markets, in a note.

The analysts said they expect that “the magnitude of the follow through repricing in U.S. rates will be comparatively more contained than would otherwise be expected.”

More recently, the weak yen has raised the cost of hedging long Treasury positions for Japanese investors. So a stronger yen resulting from a shift toward tighter policy would help make hedging costs for owning Treasurys less onerous for Japanese investors as well, Lyngen and Jeffery wrote, “which over the longer term may begin to make Treasurys more attractive to Japanese buyers and add to the list of sources for duration demand.”

That could make U.S. debt more attractive to new Japanese buyers, Slok agreed.

But that’s oveshadowed by the near-term worry, Slok said, that existing Japanese investors will be inclined to sell Treasurys. Flow data will be very much in focus if the Bank of Japan follows through on the apparent trial balloon floated in the Nikkei report.

Investors will be watching, he said, to see “if the train is leaving the station.”

[ad_2]

[ad_1]

The slide in the U.S. dollar in the last eight months could mean that mean all of its gains in the wake of the coronavirus pandemic will soon be lost, according to Kit Juckes, a macro strategist at Société Générale who has been a long-time currency analyst.

Juckes said in a note shared with SocGen clients and the media on Tuesday that he expects the greenback could return to its lows from December 2020, the level it fell to during the pandemic given the market is pricing in an end to interest rate rises by the Federal Reserve this year.

“As was the case in January/February before the SVB mini crisis, the market is anticipating the peak in US rates and a further narrowing relative rates. If nothing happens to scupper those expectations (another upside surprise in US growth, or further European growth disappointment) I would expect the Dollar Index to move closer but not all the way to, the lows at the end of 2020,” he said.

“That won’t happen in a straight line and will require further interest rate convergence between the U.S. and other major economies, however.”

Over the past week, investors’ expectations about the outlook for where U.S. interest rates are headed have shifted. Following lower-than-expected readings last week on U.S. June inflation, as measured by the consumer price index and the producer price index, many investors expect the Fed will raise its benchmark interest rate only once more when the central bank holds its policy meeting next week.

Read this next: U.S. stocks benefiting from ‘sense of urgency’ as investors rush into equity mutual funds

Fed-funds futures, which are used to bet on the expected path of interest rates, are pricing in nearly a 100% probability of a hike in July, but analysts also think rate cuts could come by the Fed’s January policy meeting, where futures markets already see a nearly 40% probability of a cut, according to CME’s FedWatch tool.

This shift in expectations has triggered a wave of dollar-bearishness across Wall Street, with many top currency analysts opining that the path of least resistance for the U.S. dollar is likely lower.

The ICE U.S. Dollar Index

DXY,

a gauge of the dollar’s strength against a basket of major currencies, was trading modestly higher on Tuesday, up 0.1% at 99.96, but on Monday, the index touched its lowest level since mid-April 2022.

Back in December 2020, it briefly broke below 90 to what was at the time its weakest level in more than two years.

Read more: Why stocks could get a boost from a falling U.S. dollar

Another important question for markets will be whether the dollar’s peak in late September 2022, when the dollar index traded just shy of 115, its highest level in more than two decades, will mark a long-term cyclical peak. As Juckes notes, the dollar has traded at a succession of higher lows since 2007.

Another issue on Juckes’ radar: the prospect that the U.S. dollar and Chinese yuan

USDCNY,

could weaken in tandem. Juckes said he expects the yuan to climb to 7.40 against the dollar by the end of the year, a level it hasn’t seen in roughly 15 years.

The onshore renminbi, which incorporates the yuan’s more tightly controlled exchange rate within China, was trading at 7.18, with the dollar climbing 0.1%.

While American consumers could see the price of imported goods rise and international travel become more expensive, a weaker dollar could also help boost U.S. equity prices, as earnings of exporters get a boost from the currency’s slide, and the chances of a global recession eases, as MarketWatch reported on Monday.

[ad_2]

[ad_1]

Stocks rose for a fourth day in a row on Thursday, a day ahead of second-quarter earnings from America’s biggest lenders. The Dow Jones Industrial Average

DJIA,

rose about 46 points, or 0.1%, ending near 34,394, according to preliminary data from FactSet. But the S&P 500 index

SPX,

gained 0.9% to end at 4,509, clearing the 4,500 mark for the first time since April 5, 2022 when it ended at 4,545.86, according to Dow Jones Market Data. The Nasdaq Composite Index

COMP,

scored another blockbuster day, up 1.6%. Investors have been optimistic as inflation pressures ease and as perhaps the best-telegraphed U.S. economic recession in recent history has yet to materialize. The S&P 500 and Nasdaq have been charging higher on buzz about AI technology, with much of this year’s stock-market gains fueled by a small group of stocks. The risk-on tone ahead of earnings from JPMorgan Chase and Co.,

JPM,

Wells Fargo

WFC,

and Citigroup

C,

had the U.S. dollar

DXY,

earlier on pace to end at its lowest level since early April 2022. Treasury yields also continued to fall, with the 10-year

TMUBMUSD10Y,

rate back down to 3.759%, after topping 4% in recent weeks. The six biggest banks are expected to issue a deluge of fresh debt after earnings, despite the Federal Reserve having sharply increased rates and borrowing costs for businesses and households to tame inflation.

[ad_2]

[ad_1]

U.S. stocks just touched their highest levels in two months. Yet, signs of a looming selloff are piling up, according to Jonathan Krinsky, chief technical strategist at BTIG.

The S&P 500

SPX,

and Russell 3000

RUA,

are both trading just shy of their highs from mid-February, but market breadth hasn’t recovered, as index gains over the past month have largely relied on megacap names like Microsoft Corp.

MSFT,

and Apple Inc.

AAPL,

helping to offset weakness in other areas of the market.

As of Friday, only 45% of Russell 3000 stocks were trading above their 200-day moving averages, according to data cited by Krinsky. By comparison, when the broad-market gauge was trading at its highest level of 2023 back in February, 70% of the individual stocks included in the index were trading above their 200-day moving average. Technical analysts use moving averages as a gauge of a stock or index’s momentum.

Lackluster breath is looking like more of an issue analysts say, especially now that the Nasdaq’s outperformance appears to be fading after leading markets higher since the start of the year.

Over the last two weeks, the Dow Jones Industrial Average

DJIA,

has outperformed the Nasdaq Composite

COMP,

by the widest margin since the two-week period ending Dec 30, according to FactSet data.

Krinsky cited exchange-traded funds that feature megacap technology names, including the iShares Expanded Tech-Software ETF

IGV,

the Communications Services Select Sector SPDR Fund ETF

XLC,

and Consumer Discretionary Select Sector SPDR Fund ETF

XLY,

as examples of emerging weakness in this critical sector of the market. Meanwhile, regional bank stocks, small-cap stocks and shares of retailers, all of which have lagged behind the market this year, look weak.

See: Are tech stocks becoming a haven again? ‘It is a mistake,’ say market analysts.

Krinsky summed up this dynamic thus: “The weak parts of the market remain weak, while the strong parts now appear vulnerable,” the BTIG analyst said in a Sunday note to clients.

Furthermore, “[i]n absolute and relative terms, the tech sector looks like a poor risk/reward to us here,” Krinsky added.

Low implied volatility is another issue for markets, Krinsky said. That can mean investors have gotten too complacent and markets may be heading for a selloff, analysts say.

The Cboe Volatility Index

VIX,

otherwise known as Wall Street’s “fear gauge,” finished Friday at its lowest end-of-day level since Jan. 4, according to Dow Jones Market Data. The Cboe S&P 500 9-Day Volatility Index, which tracks implied volatility over a shorter time horizon, has also fallen to January lows, FactSet data show.

Such low levels mean volatility could be poised to “mean revert,” Krinsky said, which may portend a selloff in the months ahead for the S&P 500, the most liquid and most closely watched gauge of U.S. stock-market performance.

Implied volatility gauges measure activity in option contracts linked to the S&P 500 to gauge how volatile traders expect markets to be over the coming days and weeks. Typically, implied volatility advances when U.S. stocks are falling.

The greenback has shown some signs of life in recent sessions, although the U.S. dollar remains well below the multi decade highs it reached back in September. That the buck bounced off its February lows late last week suggests that momentum could be skewed toward the upside for the dollar, Krinsky said, which could create more problems for stocks given the dollar’s tendency to weigh on markets during 2022.

The ICE U.S. Dollar Index

DXY,

a gauge of the dollar’s strength measured against a basket of rivals, was up 0.7% in recent trade at 102.22.

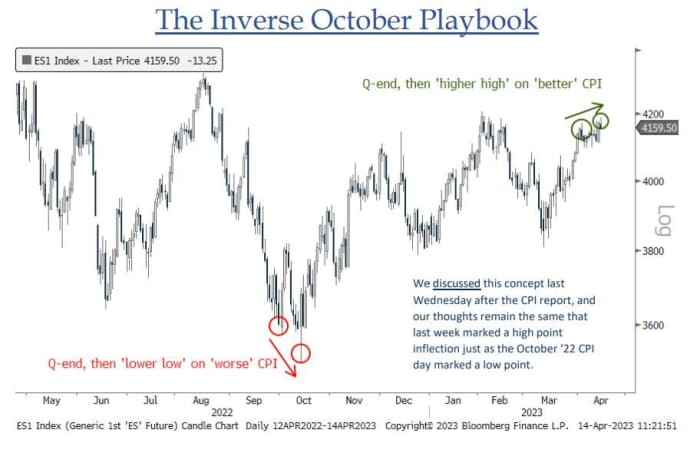

All of these factors support the notion that stocks could be headed for what Krinsky called the “reverse October playbook.”

Just as the S&P 500 bottomed following the hotter-than-expected September report on consumer-price inflation, the market’s monthslong rebound rally may have peaked following last week’s CPI report for March, which showed consumer prices rose a scant 0.1% last month, less than the 0.2% increase that had been forecast by economists polled by MarketWatch.

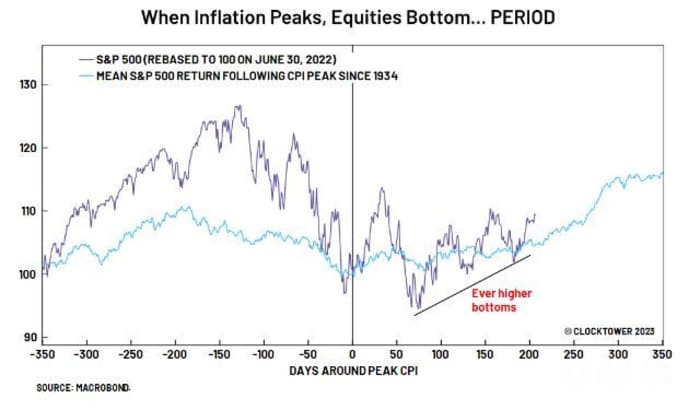

Not everybody agrees with this assessment. Marko Papic, chief strategist at Clocktower Group, cited market data going back to 1934 to show that U.S. stocks tend to rally after inflation peaks. Consumer-price inflation reached its highest level in more than four decades when the CPI headline number showed prices up 9.1% year-over-year in June.

U.S. stocks look set to decline for a second day in a row on Monday, with the S&P 500 off 0.3% at 4,126, while the Nasdaq Composite was down by 0.4% at 12,070, and the Dow Jones Industrial Average traded marginally lower at 33,881.

[ad_2]

[ad_1]

Thousands of miles away from U.S. shores last Wednesday, a headline began working its way across Europe, then Wall Street, sparking fresh panic as it dawned on investors that they may be facing yet another banking crisis.

Shares of Credit Suisse

CS,

CSGN,

would eventually sink 25% last week to a fresh record low, unable to find footing days after the head of top shareholder Saudi National Bank said they won’t invest any more in the bank. By Sunday, the struggling Swiss bank had a new owner, leaving investors to wonder if at least one chapter in a current roller coaster of global banking stress can be closed.

Swiss authorities steered rival UBS AG

UBS,

to an all-stock deal worth 3 billion francs ($3.25 billion), or 0.76 francs per share, a not-so-slight discount to the 1.86 franc close on Friday of Credit Suisse. So important was the agreement, it was announced by Switzerland’s President Alain Berset, with both banks and the chairman of the Swiss National Bank on either side of him.

“With the takeover of Credit Suisse by UBS, a solution has been found to secure financial stability and protect the Swiss economy in this exceptional situation,” the SNB said in a statement.

The Swiss National Bank said either Swiss bank can borrow up to 100 billion francs in a liquidity assistance loan, and Credit Suisse will get a liquidity assistance loan of up to 100 billion francs, backed by a federal default guarantee. The U.S. Federal Reserve had worked with its Swiss counterpart on the deal as well.

“We welcome the announcements by the Swiss authorities today to support financial stability. The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient,” said a statement Sunday by Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell.

European Central Bank President Christine Lagarde also praised Swiss authorities for “restoring orderly market conditions and ensuring financial stability,” while reiterating the “resilience” of the euro-area banking sector. She said the ECB stands ready to provide liquidity if needed.

Her comment comes days after the the ECB pulled the trigger Thursday on a 50-basis-point rate hike, as it warned “inflation is projected to remain too high for too long.”

The deal for Credit Suisse comes in the wake of stress on the U.S. banking sector, triggered by the collapse of Silvergate Bank, Silicon Valley Bank and Signature Bank, all within the space of a week.

“Virtually everyone at this high-level Swiss press conference — government officials, regulator, central bank governor, and executives of the two banks — blamed the US banking sector turmoil for being the catalyst for the financial turmoil in #Switzerland,” tweeted Mohamed A. El-Erian, chief economic adviser at Allianz, of the press conference Sunday with Swiss authorities to announce the deal.

And for U.S. investors who have had quite enough anxiety lately, a logical question would be to ask if the deal that brings together the two Swiss banking giants will now remove one layer of stress from global markets, and hence Wall Street.

For that reason, many will be watching how Asian and U.S. equity futures trade later on Sunday, as well as Europe’s opening reaction on Monday.

The Credit Suisse news may only go so far to assuage investors, with some raising an eyebrow over Powell and Yellen’s Sunday statement about the Swiss deal. “Seriously, if everyone truly believed the ‘The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient’ … Would they have to tell us? Are these words enough?” said Jim Bianco, president of Bianco Research, on Twitter. “Or do investors want to see Warren Buffett writing checks to regional banks in the next two hours (before Asia opens)?”

Fox News and other media outlets reported over the weekend that the Berkshire Hathaway

BRK.A,

BRK.B,

chairman and CEO had been talking to President Joe Biden’s administration in recent days over possible investments in the battered regional bank sector, and offering his advice.

The billionaire investor was responsible for a capital injection to Bank of America

BAC,

in 2011 as its shares tumbled due to subprime mortgages, as well as $5 billion to Goldman Sachs

GS,

amid the 2008 financial crisis.

Some had said ahead of the deal last week that global-market stability depended on the Swiss first getting their house in order.

“I don’t think there are any direct consequences for U.S. investors, but it’s extremely negative for sentiment if a major Swiss bank fails, hot on the heels of SVB/SBNY,” Simon Ree, the founder of Tao of Trading options academy school and author of the book by the same name, told MarketWatch last week.

“The market will be (temporarily) wondering who’s next. It could start to have the optics of a global banking crisis, rather than an idiosyncratic failure of a niche U.S. regional bank,” said Ree.

Credit Suisse’s troubles came amid a revamp and five straight money-losing quarters, following a painful legacy that included billions worth of exposure to the collapsed Archegos family office and $10 billion worth of funds tied to Greensil Capital it had to freeze.

Read: In its delayed annual report, Credit Suisse admitted to financial control weaknesses

“The SNB and the Swiss government are fully aware that the failure of Credit Suisse or even any losses by deposit holders would destroy Switzerland’s reputation as a financial center,” said Otavio Marenzi, CEO of Opimas, a management consulting firm focused on global capital markets, in a note to clients last week.

The bank’s plummeting stock price and soaring bond yields was “mimicking Silicon Valley Bank’s recent collapse in a frightening way. In terms of the outflow of deposits, Credit Suisse’s position looks even worse,” said Marenzi.

As far as some are concerned, the market may have more stress ahead of it.

“The SVB failure highlights the potential for other skeletons to be hidden in closets and the market will spend the next few weeks/months hunting them out. Even just the extreme volatility we’ve seen on bond markets the last five days renders any attempt to ascribe a value to other asset classes redundant,” said Ree.

Plus: Here’s what’s really protecting your bank deposits

His view is shared by many analysts, who in part point to increasing uncertainty around how the Federal Reserve will react going forward as it tries to balance market and economic risks. Some now see full percentage rate cuts by year-end, amid banking stress.

Samantha LaDuc, the founder of LaDucTrading.com who specializes in timing major market inflections, said she stands by her advice (that she shared with MarketWatch in February) that investors are being “paid to wait,” by staying in cash.

Read: Looking for a place for your cash? Grab these 5% CDs while you still can.

“I have been literally recommending and tweeting to clients that we are PAID TO WAIT in T-bills at 5% until [the] bond market can figure out if we have recession or not. All that happened last week pulled forward recession risk,” she told MarketWatch.

Prior to the SVB crisis, she had been recommending clients short reflation trades, such as banks

XLF,

KRE,

energy

XLE,

and metals and mining

XME,

SLX,

and has been saying she sees “unattractive risk-reward for either stocks or bonds.”

Opimas’ Marenzi said the threat to Wall Street from Credit Suisse was simple:

“You mean what do American investors who do not own any non-American stocks and do not own a passport and could not find Switzerland on a map and who think that anyone who speaks any language other than English is a bit weird have to worry about? Not a lot, other than the contagion spreading back into the US banking system and causing a meltdown,” he told MarketWatch.

[ad_2]

[ad_1]

Twitter voters favor Elon Musk stepping down, as Tesla shares rise

Nearly 58% or about 17.5 million Twitters votes were cast in favor of Elon Musk stepping down from the company, Musk’s Twitter account said Monday. Meanwhile shares of Tesla Inc. , the electric car company that Musk also runs, saw its stock rise by 4.7% in premarket trades. Musk has been running Twitter for 53 days, during which time he’s laid off a large percentage of the company’s work force and drawn criticism recently for suspending accounts of four journalists. The latest controversy revolved around whether Twitter would ban accounts that post links or usernames for certain “prohibited” third-party social media platforms. The social media platform announced the ban and then seemingly rescinded the rule about 12 hours later. During that issue, Musk then asked Twitter users to vote on whether he should continue to run the company.

[ad_2]

[ad_1]

Golden Dragon China ETF pulls back after record monthly rally in November

The Invesco Golden Dragon China ETF started December with a pullback, after enjoying a record monthly rally in November amid increasing signs that China was starting to back off from the zero-COVID policy. The ETF, which tracks American depositary shares (ADS) of China-based companies that only list in the U.S., slipped 0.9% in premarket trading Thursday, after running up 9.6% on Wednesday and 41.8% in November. The pullback comes as futures for the S&P 500 tacked on 0.4%, after the index jumped 3.1% on Wednesday. The Golden Dragon ETF’s biggest decliner ahead of Thursday’s open was electric vehicle maker XPeng Inc.’s stock, which dropped 6.0% after rocketing a daily record 47.3% on Wednesday. Elsewhere, shares of Nio Inc. fell 2.0%, Alibaba Group Holding Ltd. shed 2.5%, Li Auto Inc. gave up 3.6%, Tencent Music Entertainment Inc. declined 0.9% and Pinduoduo Inc. was down 2.3%.

[ad_2]

[ad_1]

U.S. stock-index futures sank Sunday night, as Asian markets fell following widespread public demonstrations in China and as oil prices hit a 2022 low.

Dow Jones Industrial Average futures

YM00,

fell more than 150 points, or 0.5%, as of 10 p.m. Eastern, while S&P 500 futures

ES00,

and Nasdaq-100 futures

NQ00,

dropped even more sharply.

Wall Street finished mixed on Friday with the Dow notching its highest close since April 21. The S&P 500

SPX,

finished down 1.1 points, or less than 0.1%, at 4,026.12; the Dow Jones Industrial Average

DJIA,

closed 152.97 points, or 0.5%, higher at 34,347.03; and the Nasdaq Composite

COMP,

shed 58.96 points, or 0.5%, to 11,226.36.

Stocks in Asia declined Monday, led by a 2% fall by Hong Kong’s Hang Seng Index

HSI,

The Shanghai Composite

SHCOMP,

slid as well, as thousands of protesters in major Chinese cities, including Shanghai, called for President Xi Jinping to resign. The unprecedented protests were spurred by frustration with China’s strict lockdowns as part of its “zero-COVID” policy.

“Sentiment has turned sour as unrest across China grows,” Stephen Innes, managing partner at SPI Asset Management, said in a note Sunday night. “The risk of the situation escalating from here and short-term volatility remains high.”

Oil prices fell sharply Sunday as well, as investors worried about slipping demand in China. West Texas Intermediate crude futures

CL.1,

were last down more than 2%, at $74.27 a barrel, its lowest price year to date. Prices for Brent crude

BRNF23,

the international standard, sank as well.

[ad_2]

[ad_1]

Federal Reserve Gov. Christopher Waller said Sunday that financial markets seem to have overreacted to the softer-than-expected October consumer price inflation data last week.

“It was just one data point,” Waller said, in a conversation in Sydney, Australia, sponsored by UBS.

“The market seems to have gotten way out in front over this one CPI report. Everybody should just take a deep breath, calm down. We’ve got a ways to go ” Waller said.

Investors cheered the soft CPI print, released Thursday, driving stocks up to their best week since June. The S&P 500 index

SPX,

closed 5.9% higher for the week.

The data showed that the yearly rate of consumer inflation fell to 7.7% from 8.2%, marking the lowest level since January. Inflation had peaked at a nearly 41-year high of 9.1% in June.

Waller said it was good there was some evidence that inflation was coming down, but noted that there were other times over the past year where it looked like inflation was turning lower.

“We’re going to see a continued run of this kind of behavior and inflation slowly starting to come down, before we really start thinking about taking our foot off the brakes here,” Waller said.

“We’ve got a long, long way to go to get inflation down. Rates are going keep going up and they are going to stay high for awhile until we see this inflation get down closer to our target,” he added.

The Fed is focused on how high rates need to get to bring inflation down, and that will depend solely on inflation, he said.

Waller said “the worst thing” the Fed could do was stop raising rates only to have inflation explode.

The 7.7% inflation rate seen in October “is enormous,” he added.

The Fed signaled at its last meeting earlier this month that it might slow down the pace of its rate hikes in coming meetings.

The central bank has boosted rates by almost 400 basis points since March, including four straight 0.75-percentage-point hikes that had been almost unheard of prior to this year.

“We’re looking at moving in paces of potentially 50 [basis points] at the next meeting or the next meeting after that,” Waller said.

The Fed will hold its next meeting on Dec. 13-14, and then again on Jan. 31-Feb. 1.

At the same time, Powell said the Fed was likely to raise rates above the 4.5%-4.75% terminal rate that they had previously expected.

“The signal was ‘quit paying attention to the pace and start paying attention to where the endpoint is going to be,’” Waller said.

In the wake of the CPI report, investors who trade fed funds futures contracts see the Fed’s terminal rate at 5%-5.25% next spring and then quickly falling back to 4.25%-4.5% by November. That’s well below the levels prior to the CPI data.

[ad_2]

[ad_1]

The numbers: A closely-watched index that measures U.S. manufacturing activity fell 0.7 percentage points to 50.2 in October, according to the Institute for Supply Management on Tuesday.

Economists surveyed by the Wall Street Journal had forecast the index to inch down to 50. Any number below 50% reflects a shrinking economy.

It is the lowest level since May 2020.

Key details: The index for new orders remained in contraction territory, rising 2.1 points to 47.1. The production index rose 1.7 points to 52.3.

The employment index rose 1.3 points to 50 in October.

Supplier deliveries fell 5.6 points to 46.8 in October. This is the first time that deliveries were in a “faster” territory since February 2016.

The price index dropped 5.1 points to 46.6., also the lowest reading since the pandemic. Pricing power is shifting back to the buyer, the ISM said.

Only 8 of the 18 manufacturing industries reported growth in October.

Big picture: Manufacturing has been slowing recently led by softening business spending and fading demand for consumer goods. Economists think it is inevitable the index slips below the 50 threshold.

In a separate data, the S&P global U.S. manufacturing PMI inched up to 50.4 in its “final” reading in October from the “flash” reading of 49.9. This is down from a reading of 52 in September.

What ISM said: Manufacturing is slowing down and could soon enter contraction territory, but that doesn’t mean there will be a recession in the U.S., said Timothy Fiore, chair of the ISM factory business survey.

“I don’t see a collapse of new orders. I don’t see a collapse of the PMI,” Fiore said.

Looking ahead: “Recession jitters among manufacturers won’t disappear any time soon…manufacturing will endure more pain as demand weakens at home and abroad while prices stay high and interest rates remain fairly elevated,” said Oren Klachkin, economist at Oxford Economics.

Market reaction: Stocks

DJIA,

SPX,

were lower after the economic data. The yield on the 10-year Treasury note

TMUBMUSD10Y,

moved back above 4%.

[ad_2]

[ad_1]

The Chicago Business Barometer, also known as the Chicago PMI, dropped to 45.2 in October from 45.7 in the prior month, according to data released Monday.

Economists polled by the Wall Street Journal forecast a 47 reading.

Readings below 50 indicate contraction territory.

The index is produced by the ISM-Chicago with MNI. It is released to subscribers three minutes before its release to the public at 9:45 am Eastern.

The Chicago PMI is the last of the regional manufacturing indices before the national factory data for October is released on Tuesday.

Economist polled by the Wall Street Journal expect the closely-watched Institute for Supply Management’s factory index to barely remain above the 50 breakeven level in October.

[ad_2]

[ad_1]

First the easy part.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

See: U.S. third-quarter wage pressures cool a little from elevated levels

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

See: U.S. inflation still running hot, key PCE price gauge shows

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note

TMUBMUSD10Y,

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

[ad_2]

[ad_1]

First the easy part.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

See: U.S. third-quarter wage pressures cool a little from elevated levels

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

See: U.S. inflation still running hot, key PCE price gauge shows

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note

TMUBMUSD10Y,

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

[ad_2]

[ad_1]

This is a Real-time headline. These are breaking news, delivered the minute it happens, delivered ticker-tape style. Visit www.marketwatch.com or the quote page for more information about this breaking news.

[ad_2]