Deutsche Boerse SE said Thursday it would make a voluntary takeover offer for Danish software company SimCorp AS for a total 3.9 billion euros ($4.31 billion).

The all-cash offer of DKK735 ($108.86) per share represents a 38.9% premium over the closing price of DKK529, and a 45.3% premium over the three-month volume-weighted…

Shares of PacWest Bancorp were shooting 15% higher in Tuesday’s aftermarket trading after the regional bank disclosed a rise in deposits in recent weeks.

PacWest PACW said alongside its first-quarter earnings report that total deposits rose to $28.2 billion as of March 31 from $27.1 billion when the company provided a March 20 investor update. The company saw deposit balances grow by an additional $700 million or so as of April 24.

UBS Group AG said Tuesday that earnings declined in the first quarter, hurt by litigation, but that the bank drew in billions in net new money at its global wealth-management business following the news of its acquisition of Credit Suisse Group AG.

The Swiss bank UBS CH:UBSG said its result was affected by $665 million in provisions related to U.S. residential mortgage-backed securities litigation.

Popular crypto exchange Coinbase COIN, -7.27%

late Monday asked a federal court to force the U.S. Securities and Exchange Commission to respond yes or no to its petition from July 2022 to make formal rules around digital-asset regulation.

Coinbase’s petition requested that the “Commission propose and adopt rules to govern the regulation of securities that are offered and traded via digitally native methods, including potential rules to identify which digital assets are securities.”

In March, Coinbase was hit with a Wells notice from the SEC, identifying potential violations of securities laws that might spur it to take legal action. The notice came after nine months of back-and-forth between the SEC and Coinbase, CEO Brian Armstrong said in March.

Coinbase was expected to respond to the notice by the end of April, but Monday’s filing reveals that Coinbase believes the SEC’s approach doesn’t provide enough regulatory guidance for crypto companies in the U.S. to operate.

“The SEC at a minimum must set forth how those inapt and inapposite requirements are to be adapted to digital assets. But the SEC has refused to do even that,” the filing says. “It has not conducted any rulemaking to provide the regulatory clarity and process that companies need to determine which digital asset products and services to register and how to make the registration that the SEC now demands.”

Coinbase shares slid more than 7% on Monday but are up 55% year to date. Still, the stock is down nearly 60% over the past 12 months. In comparison, the S&P 500 SPX, +0.09%

is up nearly 8% in 2023 and has declined almost 4% over the past year.

It was a two-week trading period like few had ever seen in the $24 trillion Treasury market.

In a span of roughly nine trading sessions between March 7 and 17, the yield on 2-year Treasury notes — a gauge of where U.S. central bankers are most likely to take interest rates over the next two years — sank a full percentage point to 3.85% from an almost 16-year closing high above 5%, with wide swings in both directions on the way down.

The 2-year yield’s yearlong upward trajectory made a sudden and dramatic descent, as investors swung from a view that interest rates would remain higher for longer to a scenario in which the Federal Reserve might need to cut borrowing costs to avert a deep recession and repeated bank failures. The wild swing in sentiment turned the 2-year Treasury rate TMUBMUSD02Y, 4.178%

into a roller-coaster ride and made it the most exciting space to watch in the traditionally staid government-debt market.

For traders like David Petrosinelli of InspereX in New York, a 25-year veteran of markets, March’s daily volatility was akin to “getting on an elevator with no buttons,” he said. He recalls telling people at his firm, who were worried about the positions they held at the time, that “a lot of this is a knee-jerk reaction to the unknown” — even if it felt both “eerily reminiscent” of rates volatility seen ahead of the 2007-2008 financial crisis, and “distinctly different’’ because it was driven by rapidly changing market expectations for the Fed and contained within the U.S. regional-banking system.

For more than a decade, there wasn’t much to say about the 2-year Treasury yield because the U.S. was mired in mostly low interest rates and “no one knew how to trade it,” according to Petrosinelli, 54, who began his career in the late 1990s as a as a portfolio manager focused on asset-backed and residential mortgage-backed securities. It was an overlooked rate in a sleepy corner of the market and nobody paid it much attention. That changed beginning in 2022, when monetary policy makers finally undertook the most aggressive rate-hike campaign in four decades to combat inflation — reinforcing the 2-year yield’s role as the best proxy for where the market thinks interest rates will end up. The 2-year yield rocketed to above 5% in early March from 0.15% in April 2021.

Suddenly, the 2-year Treasury became the most watched financial indicator on Wall Street, influencing the trajectories of stocks and the U.S. dollar throughout much of 2022. “This thing is relentless,” declared market commentator Jim Cramer on CNBC last year. He told viewers he was buying 2-year notes, not meme stocks. “The run to 4 is probably the most punishing one I can recall for the 2-year.” Other prominent names like Mohamed El-Erian, the former chief executive of PIMCO, and Jeffrey Gundlach, founder of DoubleLine Capital, wanted to talk about it. “If you want to know what’s going to happen in the year, follow the 2-year yield at this point,” El-Erian said on CNBC. “That’s the market indicator that has the most information.” More hedge funds and macro private-equity firms jumped on board and started trading it, said InspereX’s Petrosinelli. And head trader John Farawell of Roosevelt & Cross in New York, said family and friends who never showed much interest in fixed income before began regularly asking him if it was the right time to buy the 2-year Treasury note.

“Once we started to hit 4% on the 2-year yield last September for the first time since 2007, everyone got interested,” said Farawell, 66, a trader for the past 41 years. He estimates that interest in the 2-year yield among his firm’s clients has gone up about 30% in the past 12 months. “We have seen retail customers suddenly saying they want to put their money to work in the 2-year note because of an interest rate that we have not seen in years.”

From his office in Midtown Manhattan, Nicholas Colas noticed an abrupt and unexpected shift over the past year and it had to do with the 2-year Treasury. As the co-founder of DataTrek Research, a Wall Street research firm, Colas realized that the 2-year Treasury yield was influencing trading in the stock market. When the 2-year Treasury yield shot higher in 2022, the equity market would become volatile and often drop. In fact, the 2-year Treasury seemed to influence equity-market volatility in both directions. Whenever the 2-year yield briefly stabilized, Colas said, stocks tended to rally since equity investors took the stabilization in the 2-year rate to mean that Fed policy was “no longer as much of a wild card.”

To Colas, equity markets appeared to be taking any selloff in the 2-year note, and thus a rise in its corresponding yield, as a sign that the Fed would have to increase interest rates by more than expected and keep them higher for longer. With stocks and U.S. government debt both getting trounced regularly in last year’s selloffs, Colas said his first thought was that “all of a sudden, Treasurys were no longer a safe haven — something that has rarely happened since I started my career in 1983.”

Trading in government debt, like elsewhere in financial markets, is a two-way street of buyers and sellers. When yields are moving higher, that means the price of the corresponding Treasury security is dropping — and vice versa. The 2-year Treasury note pays out a fixed interest rate every six months until it matures. The trick to trading it, as opposed to buying and holding, is to either sell it before its underlying value gets destroyed by higher interest rates, or to buy it before the Fed starts cutting rates — which would, theoretically, produce a lower yield and make the government note more expensive.

Throughout the yield’s march higher, investors sold off the underlying 2-year note — a move which diminished the note’s value for existing holders like banks, pension funds, credit unions, foreign central banks, and U.S. corporations. Two-year Treasury notes also constitute about 1% to 2% of the total holdings at the 10 largest actively managed money-market funds, according to Ben Emons, senior portfolio manager and head of fixed income at NewEdge Wealth in New York.

“Policy expectations are what really drive the 2-year yield,” said Thomas Simons, a U.S. economist at Jefferies, one of the two dozen primary dealers that serve as trading counterparties of the Fed’s New York branch and help to implement monetary policy. “We had a major paradigm shift in terms of what investors’ expectations were for the sustainability of higher inflation and what the Fed would do in response. The impact on markets has been far less appetite for risk than there otherwise would be,” with stocks putting in a dismal performance in 2022, though generating somewhat better 2023 returns. Tucked into the note’s selloff, though, was plenty of interest from prospective government-debt buyers, which helped temper the magnitude of the 2-year yield’s rise once the rate got to 4%. Many looking to buy were individual investors hoping to benefit from higher yields and to diversify away from stocks, said traders like Tom di Galoma, a managing director for financial services firm BTIG.

Historically, banks, mutual funds, hedge funds, foreign investors and even the Fed have been the biggest buyers of Treasurys across the board; some of those players, particularly foreign central banks and money-market mutual funds, are mandated to buy and hold government debt. All two dozen primary dealers are involved as market makers for the 2-year security, stepping in to buy it in the absence of either direct or indirect buyers.

The 2-year note remains a reliable source of funding for the U.S. government, given the consistent demand for the maturity, which enables the U.S. Treasury Department to “raise a lot of cash quickly, if needed,” said Simons of Jefferies. In 2020, for example, when the government authorized $2.4 trillion in Covid-related spending and relief programs, the amount of 2-year notes sold at auction was one of the biggest of any maturity — far exceeding the 10- and 30-year counterparts — “because it had the capacity to handle that.’’

Sources: Treasury Department, Bureau of Public Debt, Federal Reserve Bank of Dallas.

Currently, the Treasury has $1.421 trillion in total outstanding 2-year notes, representing about 13% of all the debt issued out to 10 years, according to Treasurydirect.gov. The most recent 2-year note auction in March was for $42 billion — more than the 10-year note sale.

Fallout from the banking sector and worries about a potential recession altered the trajectory of the 2-year starting in March, triggering concerns that the Fed’s rate-hike cycle had gone too far. Fresh buyers poured into the 2-year space and pushed the yield below 4% — driven by the view that rates weren’t likely to go much higher from here and that policy makers might cut them by year-end.

Substantial downside volatility in the 2-year Treasury yield has actually helped to stabilize stock prices this year, in Colas’ estimation, because it’s been interpreted as the bond market’s sign that the Fed is approaching the end of its rate-hiking cycle.Like InspereX’s Petrosinelli, Colas says he had visions of the 2007-2008 financial crisis during March’s flight-to-quality trade, which occurred amid regional bank failures and “significantly more stress than the market was expecting.”

As of Thursday morning, the 2-year rate was at 4.17%, below the Fed’s benchmark interest-rate target range — implying that traders still believe policy makers will follow through with rate cuts. That’s a turnabout from the thinking that prevailed over most of 2022 through early last month, when the 2-year rate had been on an aggressive march toward 5% as the Fed continued to hike rates to combat inflation.

Meanwhile, poor liquidity continues to plague the Treasury market broadly, based on Bloomberg’s U.S. Government Securities Liquidity Index, which measures prevailing conditions. According to the New York Fed, the Treasury market was relatively illiquid throughout last year — making it more difficult to trade. As a result, there was a widening in the bid-ask spread — or difference between the highest price a buyer is willing to pay versus the lowest price a seller is willing to accept — of the 2-year note relative to its average.

“The volatility we’re seeing in the 2-year, we think, is largely a function of uncertain Fed rate hiking expectations coupled with poor liquidity,” said Lawrence Gillum, the Charlotte, N.C.-based chief fixed income strategist at LPL Financial.

“The 2-year is the most sensitive to changing policy expectations and since this Fed is ‘data dependent,’ any and all new data that could potentially change the inflation/economic growth narrative has increased volatility substantially,” Gillum said in an email. “As the Fed’s rate hiking campaign comes to an end (we think there is one more hike and then they’ll be done), we would expect the volatility to decline. Moreover, the Treasury and Fed are looking at ways to improve liquidity, but so far nothing has happened. Hopefully, they will do something, though, since the Treasury market is arguably the most important market in the world.”

At InspereX, Petrosinelli regards the 2-year note as an “anchor” to any short-term portfolio, and says that “it’s not a bad place for investors to hide out for at least a year.’’ That’s because even if the yield does come down, “investors wouldn’t be getting too hurt price-wise,” he said. “We think the Fed will leave rates elevated for some time.”

However, the 2-year could continue to dip below the fed-funds rate on soft economic data, especially related to consumption, later this year, Petrosinelli said. In order for the 2-year rate to go above the Fed’s main interest-rate target — now between 4.75% and 5% — “people would have to think the Fed is behind the curve again on inflation.”

For Farawell of Roosevelt & Cross, which was founded in 1946 and is one of Wall Street’s oldest independently owned municipal-bond underwriters, the 2-year note “has become such an attractive asset class for us’’ that “you almost can’t go wrong with putting money in it.” Friends and family “ask me about this 2-year and say, ‘It sounds good.’ I say, ‘It’s a great rate, you should buy it — until the Fed starts to change course.’”

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

If you invest in dividend stocks, you are probably looking for long-term growth to go with the income. Otherwise you might be content to hold one-month U.S. Treasury bills, which yield 4.5% or park your money in an online savings account for a yield close to 4%.

Below is screen of stocks with current dividend yields ranging from 4.14% to 8.46%. What sets these apart from other stocks with high dividend yields is that their payout increases are expected to accelerate in 2023 and 2024 from those in 2022.

On Tuesday, S&P Dow Jones Indices said in a press release that it expected dividend payments by publicly traded U.S. companies to continue to hit record levels in 2023. But Howard Silverblatt, a senior index analyst with the firm, said that the pace of dividend increases in the first quarter had slowed and that he expected this year’s increases to be “at half the pace of the double-digit 2022 growth.”

Silverblatt also said current events in the banking industry were “expected to negatively impact future spending from both consumers and companies, which in turn may curtail corporate dividend growth.”

For many banks, there’s another big item on the table. A focus on share buybacks in recent years is very likely to end — this is a use of cash that can raise earnings per share if the share count is reduced, but there can be consequences, especially after a year of rising interest rates that pushed down the market value of banks’ investments in bonds.

In a note to clients on March 16, Dick Bove, a senior research analyst with Odeon Capital, predicted that stock repurchases in the banking industry would be “meaningfully cut back if not flat out eliminated.” He made three general points about buybacks in the banking industry:

Buybacks remove working capital that would otherwise provide returns to a bank.

Buybacks mean a bank’s board of directors is “in favor of flat-out giving capital away to investors that want nothing to do with the bank — they are selling its stock.”

Buybacks do “nothing to increase bank stock prices – many bank stocks are selling at below their prices of five years ago.”

A company might find it much easier to curtail or stop buying back shares to preserve cash than it is to cut regular dividends. Preserving and increasing the dividend over time has been correlated with good performance for stocks over time. These articles provide examples of how dividend compounding is correlated with long-term growth as income streams build up:

The S&P Dow Jones Indices report raises the question of which stocks might buck the trend.

Starting with the S&P 500 SPX, -0.50%,

there are 71 companies stocks with current dividend yields of at least 4.00% indicated by annual payout rates. Among these companies, 68 increased dividends during 2022, according to data provided by FactSet.

Then we looked at the pace of dividend increases in 2022 and the consensus estimates for dividends paid during 2023 and 2024, among analysts polled by FactSet. Among the remaining 68 companies, there are 29 for which the estimated 2023 dividend increase is higher than the 2022 dividend increase. Narrowing further, there are 14 for which the estimated 2024 dividend increases are higher than the estimated 2023 dividend increases.

Here are the 14 stocks that passed the screen, sorted by current dividend yield:

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Any stock screen is limited, but can be useful as a starting point or supplement to your own research. If you see any companies of interest, do some research to form your own opinion of how likely they are to remain competitive over the next decade, at least.

Be careful what you wish for. U.S. job openings dropped below 10 million, a symbolic sign that the Federal Reserve’s efforts to combat inflation by sapping labor-market demand was working — and U.S. stocks promptly fell. Perhaps the bigger issue is that investors were not willing to push stocks out of the 3,800 to 4,200 range the S&P 500 SPX, -0.48%

has been trading in for months.

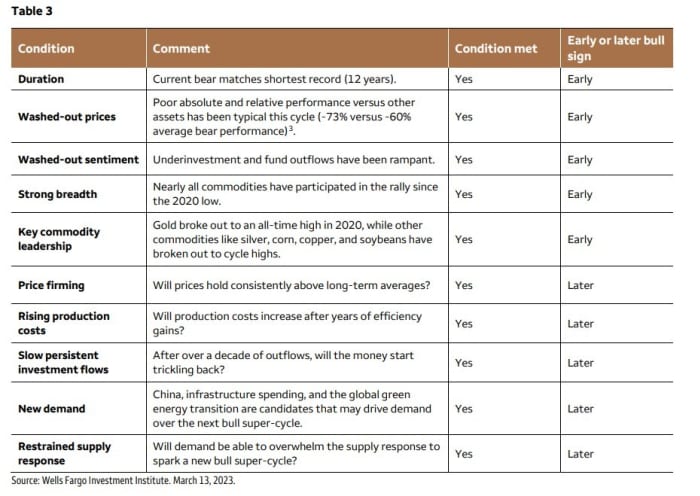

It might not be the most obvious time to be discussing a commodity supercycle, with recession talk growing, but then that’s what makes this call more interesting. Strategists at Wells Fargo investment Institute argue it’s year three of a commodity supercycle, which they say has plenty more room to run.

John LaForge, head of real asset strategy, and Mason Mendez, investment strategy analyst, say commodities are like black holes, in that escaping the gravity of a supercycle is difficult for any individual commodity. They point to this chart, looking at commodity momentum since 1800, plotted in 10-year moving averages, which shows that food, energy and the commodity complex as a whole tend to follow each other around.

Right now nearly all the signs, both technical and fundamental, point to a commodity bull market, they say. The early signs are mostly shifting prices and technical indicators, and the latter signs are more fundamental in nature, like restrained supplies. “The bottom line is that the key early technical indicators are confirming to us that a new supercycle likely began in 2020.”

The analysts went further into depth on what they call washed-out sentiment. They say the process goes something like this: near the end of a commodity bull supercycle, prices go so high that oversupplies become rampant and need to be worked off, which results in investment stopping to flow into production. They say that in both corn C00, +0.80%

and gold GC00, -0.17%

— not commodities with much in common — supply growth rates have turned negative in recent years. Both showed similar conditions at the start of the last supercycle, in 1999.

They advise using commodities as portfolio diversifiers, which certainly would have helped last year, when both stocks and bonds fell but the Bloomberg commodity index rose nearly 16%. They highlight commodity prices typically move differently than stocks or bonds over the long run. And they say that supercycles have historically lasted a decade or longer, and the shortest commodity bull market on record was nine years.

One caveat: the speed of technology advances. Sometimes technology can help fuel demand, but conversely, to the extent technology can make commodities easier to extract, it can also buoy supplies. The obvious example here, not pointed out in the note, is the shale-oil revolution. There’s an interesting article in The Economist (subscription required), how copper has yet to be the beneficiary of a technology boost.

NQ00, -1.08%

edged lower. Oil prices CL.1, -0.62%

fell but held over $80 per barrel. The yield on the 10-year Treasury TMUBMUSD10Y, 3.295%

turned lower after the latest jobs data.

Overseas, New Zealand’s central bank made a larger-than-expected 50 basis point rate hike, while a joint forecast of Germany’s leading institutes upgraded its view on the eurozone’s largest economy, now expecting a 0.3% advance.

Alphabet’s GOOGL, -0.63%

Google says its chips are faster and more power efficient than comparable chips from Nvidia NVDA, -3.41%.

Western Alliance Bancorp WAL, -16.47%

shares fell in premarket trade after the regional lender detailed the latest losses in its portfolio of loans and securities.

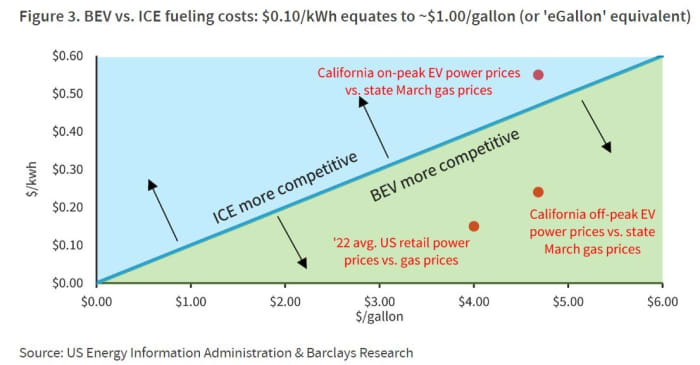

Sure, higher gasoline prices naturally drive demand for electric vehicles. But at what point do high electricity prices make it more cost-effective to buy old gas guzzlers? This chart from Barclays breaks it down — roughly, 10 cents per kilowatt hour equates to $1 per gallon. Right now it’s cheaper to fill a car at the pump than recharge at peak hours.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Wall Street bonuses fell 26% in 2022, the largest drop since the collapse of Lehman Brothers in 2008, as New York state and city officials dial back their expectations for the economic impact of the securities industry.

While many people bemoan the salaries commanded by the Big Apple’s white-shoe bankers, the financial sector provides an economic boost to city and state budgets, helping to find public services that touch the lives of residents.

Now, with the banking sector absorbing the impact of the collapse of Silicon Valley Bank and Signature Bank in recent weeks and of a lack of investment bank deal-making, 2023 isn’t looking particularly strong. The current malaise may signal what’s in store for bonuses and employment in the coming year.

Rahul Jain, state deputy comptroller, said state and city official are baking in conservative projections for a decline in Wall Street profits and bonuses in 2023 partly because much remains unknown such as when the Fed will pause its interest rate hikes or possibly cut them.

“What we can’t tell is what the Fed will do with interest rates,” Jain told MarketWatch. “It doesn’t seem like we’ll return to the levels of 2020 and 2021, but there’s hope that 2023 will level off near 2022.”

While Wall Street and the banking sector is challenged, the overall economy remains relatively healthy, as other sectors such as travel make up for weakness in the securities industry in the New York area.

“The broad economy still matters and it’s still resilient,” he said. “People still want to do things.”

Like the FDIC and other regulators, the comptroller’s office is keeping an eye on the commercial real estate market, which will hinge on how much credit is available for loan refinancings.

“Any kind of credit crunch would make the situation worse,” Jain said.

Even with the cut, the bonus alone eclipses average U.S. wages. Full-time employees in management, professional and related occupations have the highest median weekly earnings reported by the Bureau of Labor Statistics, and the median income for this group across the U.S. was $1,729 a week, or $89,908 a year, in the fourth quarter of 2022 for men, and $1,316 per week, or $68,432 per year, for women.

Wall Street banker bonuses jumped by 28% in 2020 and grew by another 12% in 2021, only to fall 26% in 2022. That is the largest drop since the 43% fall in 2008, the year Lehman Brothers collapsed and triggered a global financial crisis.

At the same time, employment in the securities industry climbed to 190,800 by the end of 2022, the highest level in at least 20 years and surpassing the previous 20-year high of 188,900 in 2007.

Collectively, Wall Street firms generated $25.8 billion in profits in 2022, less than half the $58.4 billion produced in 2021 as the impact of inflation, the war in Ukraine and supply constraints bit into deal-making.

The securities industry accounted for about $22.9 billion in state tax revenue, or 22% of the state’s tax collections in fiscal 2021-’22, and $5.4 billion in city tax revenue, or 8% of total tax collections over the same period.

New York State Comptroller Thomas P. DiNapoli estimated a drop of $457 million in 2022 tax income for the state and of $208 million for New York City, when measured against the lucrative year of 2021.

With recession in the headlines and markets selling off in 2022, however, policy makers have already adjusted their expectations for tax income.

New York Gov. Kathy Hochul’s proposed budget assumes that bonuses in the broader finance and insurance sector will drop by 25.2% in 2022-’23, while the city’s 2023 financial plan assumes a decrease of 35.6% for the securities industry.

“While lower bonuses affect income tax revenues for the state and city, our economic recovery does not depend solely on Wall Street,” DiNapoli said in a statement. “Employment in leisure and hospitality, retail, restaurants and construction must continue to improve for the city and state to fully recover.”

The fate of Wall Street’s bonuses in 2023 remains tied up in what markets and interest rates do for the balance of the year. Based on the storm clouds over the banking sector now, it’s possible bonuses could fall again.

In one positive sign, the equities market has managed to post gains so far in 2023 after bruising losses in 2022. At last check, the S&P 500 SPX, +0.57%

is up 5.6% in 2023, while the Nasdaq COMP, +0.73%

has risen 14.9%. The Financial Select Sector SPDR exchange-traded fund XLF, -0.22%

is down 6.6% so far in 2023.

After Wall Street bonuses fell 43% in 2008, they rebounded by 39% in 2009. Such a rapid recovery may not be in the cards for the coming year, however.

Member firms at the New York Stock Exchange generated profits of $13.5 billion in the first half of 2022, down by more than half from year-ago levels, according to an October report on the securities industry in New York by the comptroller’s office.

Revenue on trading, underwriting and securities offerings dropped about 48% over the same time period, while global debt offerings dropped by 17%.

At the same time, interest-rate expenses tripled as the U.S. Federal Reserve boosted interest rates.

“Despite this uncertainty, the city’s latest forecast predicts annual profits to average $21 billion over the next five years, comparable to the 10-year pre-pandemic average of $20.3 billion,” the study said.

The bonus pool of $33.7 billion in 2022 fell 21% from 2021’s record of $42.7 billion, the largest drop since the Great Recession.

stock rose Thursday after the payments group responded to some of a short seller’s allegations.

Last week, Hindenburg Research disclosed a short position in the company, alleging that Block (ticker: SQ) had inflated user metrics and didn’t rein in illicit activity by users on its Cash App platform.A short position is a bet that a stock will fall: Traders who try it borrow shares of a company and then sell them, hoping to buy them back later at a lower price.

Sam Bankman-Fried, the founder and former chief executive of bankrupt crypto exchange FTX, is facing new charges for bribery, according to an indictment on March 28.

It claims Bankman-Fried in 2021 transferred over $40 million worth of cryptocurrency to Chinese government officials. The founder allegedly made the transfer to “influence and induce them to unfreeze the accounts” of Alameda Research, which contained over $1 billion in cryptocurrency that Beijing had frozen, according to the document.

The indictment contains 12 charges that Bankman-Fried previously was facing, plus the additional one for conspiracy to violate the Foreign Corrupt Practices Act, bringing the new tally to a 13-count indictment.

Bankman-Fried’s lawyer didn’t immediately respond to a MarketWatch request for comment.

Bankman-Fried has been restricted from using messaging apps, but prosecutors and Bankman-Fried’s attorneys have asked U.S. District Judge Lewis Kaplan to approve a new set of proposed restrictions that would limit his access to electronic devices and the internet.

He has pleaded not guilty to eight counts over the collapse of FTX and is currently under house arrest with his parents in Palo Alto, Calif.

U.S. District Judge Lewis Kaplan set a new hearing for Thursday.

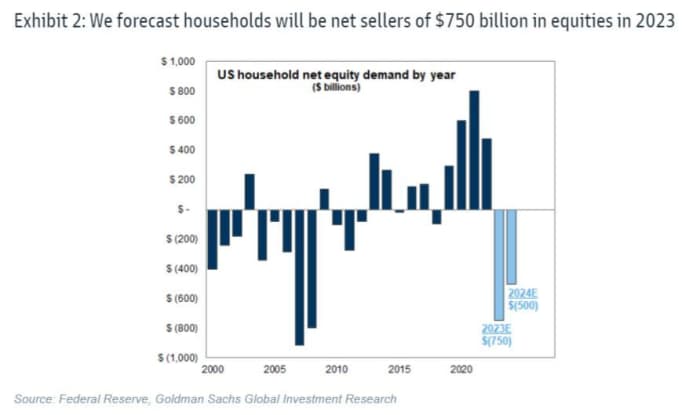

This year could mark the end of the affair — between Americans and their stockholdings.

That’s according to Goldman Sachs analysts who say due to the rise in bond yields since the start of 2022, and increased flows to bond and money-market funds, U.S. households could end up dumping up to $1.1 trillion of equity holdings this year.

“The current level of market yields clearly shows that the era of TINA (There is No Alternative) has ended and that now there are reasonable alternatives (TARA) to equities,” said a team of strategists led by Cormac Conners and David Kostin.

“Although equity demand remained resilient amid sharply rising rates in 2022, we believe the YTD [year-to-date] flows into money market and bond funds signal an escalating household shift away from equities and toward the alternatives.”

Their model of household equity demand is based on the 10-year U.S. Treasury yield and personal savings rate. The analysts say that higher yields and lower savings tend to be associated with a decrease in demand for equity among households.

In their base case, they estimate net selling of $750 billion this year, alongside their forecast for the yield on the 10-year Treasury note TMUBMUSD10Y, 3.435%

to rise from around 3.6% currently to 4.2% by the end of this year, and the personal savings rate will rise to 5.3% from 4.5%. Conners and the team said such stock selling would reverse six previous quarters of household equity demand.

Uncredited

Should bond yields tilt lower, and the savings rate move higher, Goldman sees that estimate nearly halved to $400 billion in equity sales. In a worst-case scenario, where yields push even higher and the savings rate lower, household selling would reach $1.1 trillion, they cautioned.

As for the idea that there are now reasonable alternatives to equities (TARA), Goldman said households tend to buy fixed income products during years in which they sell stocks. They pointed to data showing $51 billion has flowed out of U.S. equity mutual funds and exchange-traded funds, year to date, while $282 billion has poured into U.S. money-market funds and $137 billion into U.S. bond funds.

Picking up some of the slack left by U.S. investors, the Goldman team predict foreign investors and corporations will be net stock buyers of $550 billion and $350 billion, respectively.

“We expect buyback and cash M&A activity will slow but remain relatively robust this year, driving corporations to be net buyers of U.S. stocks – though a potential [second-half] recovery in equity issuance presents one risk to this forecast. A weaker dollar should drive foreign investors to be net buyers of U.S. stocks in 2023. Pension funds will also be net buyers of $200 billion in equities in 2023,” said the strategists.

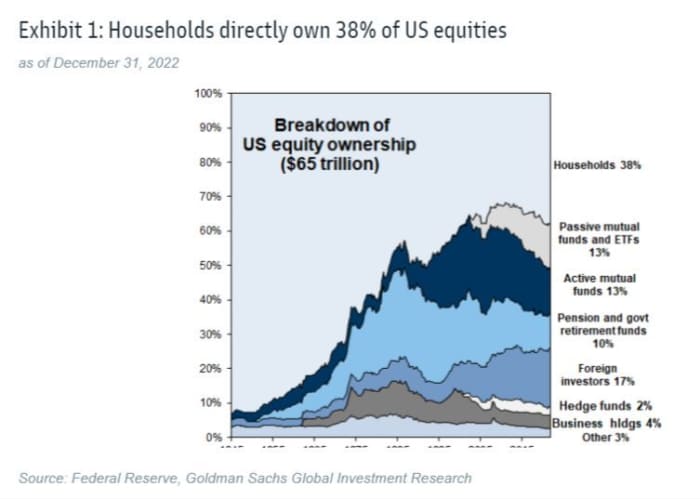

The pace of household buying has been slowing, they noted. Citing the Federal Reserve’s Financial Accounts data, Goldman said households are estimated to own 38% of the total equity market. From the start of 2020 through mid-2022, they bought $1.7 trillion in equities, but in 2022 demand for those assets fell 40% to $480 billion.

“Adjusting the Fed’s household demand series for our estimate of hedge fund net equity demand (which is included in the household category by default), implies households were net buyers of just $209 billion in equities in 2022, a 78% decline from 2021,” they said.

Up 2% so far this year, the S&P 500 SPX, +0.25%

lost 19% in 2022, the worst year for the index since the global financial crisis of 2008, as a war in Europe added to inflationary pressures across the globe, driving central banks such as the Federal Reserve to raise interest rates sharply. Wednesday’s 25-basis point Fed rate hike marked the ninth rise since March 2022.

From under 1.5% at the start of 2022, the yield on the 10-year Treasury note TY00, +0.60%

has climbed to around 3.468%, levels not seen since the 2008 crisis.

Shares of Coinbase Global Inc. dropped 15.8% in the extended session Wednesday after the crypto exchange disclosed a warning from regulators that it may have broken securities laws.

Coinbase COIN, -8.16%

said it received a Wells notice from the Securities and Exchange Commission, which could lead to formal charges.

“We asked the SEC for reasonable crypto rules for Americans. We got legal threats instead,” Coinbase said in a blog post detailing the action. “Rest assured, Coinbase products and services continue to operate as usual — today’s news does not require any changes to our current products or services.”

Based on discussions with the SEC, Coinbase said that the potential charges relate to the company’s spot market, its staking service Coinbase Earn, Coinbase Prime and Coinbase Wallet.

The crypto exchange said it asked the regulators to detail which assets in its platforms the SEC believes may be securities, but the SEC declined to do so. Coinbase called it a “cursory investigation.”

SEC representatives declined to comment Wednesday.

The company said that the investigation is “still at a very early stage,” and that it has turned in documents and provided two witnesses for testimony, “one on the basic aspects of our staking services and one on the basic operation of our trading platform.”

Shortly after Silicon Valley Bank disclosed on March 8 that it was running short of cash and needed to raise capital, First Republic Bank’s epic stock slide began.

The stock FRC, -15.47%

has lost 90% of its value in less than two weeks, hitting an all-time low of $12.18 a share on Monday.

Supportive comments from Treasury Secretary Janet Yellen helped it snap back on Tuesday, but it’s hovering between positive and negative territory on Wednesday as investors await a key Federal Reserve decision on interest rates.

The bank’s troubles stem from its overlap both in clientele and parts of its balance sheet with doomed Silicon Valley Bank, which is being sold off this week by the Federal Deposit Insurance Corp. after it officially failed on Friday, March 10. Silicon Valley Bank suffered a classic run on a bank, when depositors, nervous that it needed to raise capital, yanked their deposits.

First Republic has suffered the same deposit flight.

As a San Francisco bank with a focus on serving high-end clients, First Republic has acted as wealth manager for the greater Silicon Valley region of executives, managing directors and startup CEOs, as well as their counterparts on the East Coast.

The list incudes Facebook META, -1.16%

Founder Mark Zuckerberg, who has a large mortgage courtesy of First Republic, as the Wall Street Journal has reported. Few of its loans ever sour — it had $213 billion in assets at the end of 2022 and $176 billion in deposits.

With its sophisticated lending products and access to the technology startup world, Silicon Valley Bank was also known for its a customer base from the venture capital and private equity world.

Those well-heeled clients of both banks started running into problems as interest rates rose last year, pundits warned of an economic slowdown and investors switched to a risk-off strategy of conserving cash and containing costs.

The collapse of FTX and strain in the crypto world also fed the need for cold, hard government-backed currency. Rising interest rates made it more expensive to borrow and put a chill on the deal-making environment.

All of this and other factors led to a drain on deposits at Silicon Valley Bank and others as it faced “elevated client cash burn” at a rate that was double pre-2021 levels, even as venture capital and private equity funds were slowing down their capital raising activities, the company said in an ill-fated mid-quarter report.

On March 8 after the market close, Silicon Valley Bank said it planned to sell $2.25 billion in common stock and a type of preferred stock, with one of its major clients, private equity firm General Atlantic, in line to buy $500 million worth. Goldman Sachs Group Inc. GS, -1.14%

was handling the deal.

The company also disclosed that it had lost $1.8 billion on the sale of $21 billion in available-for-sale securities on its balance sheet to cover deposit withdrawals.

It was this last part that caused big trouble for First Republic. Not only did its clientele overlap with Silicon Valley Bank, its holdings included some of the same securities that Silicon Valley Bank sold at a loss.

Wall Street investors quickly started bidding down shares of First Republic and other regional banks and the credit rating agencies moved in, cutting the bank’s rating from investment grade deep into junk in just a few days.

None of this helped First Republic hold on to its deposits.

As one longtime banking official said recently, money from Silicon Valley types typically comes in the form of uninsured deposits, which means they’re in excess of the $250,000 that the FDIC will guarantee if a bank goes out of business. This so called hot-money is great for banks when times are good, but can move away quickly if the environment changes.

“When hot money gets nervous, it runs,” former FDIC chairman Bill Isaac told MarketWatch recently.

While an unprecedented effort on March 16 by 11 banks to inject $30 billion into First Republic’s deposits temporarily provided a lift to its stock, the move apparently wasn’t enough.

First Republic said last Thursday that it had borrowed between $20 billion and $109 billion from the Federal Reserve during that week. It also increased short-term borrowing from the Federal Home Loan Bank by $10 billion at a rate of 5.09%.

Jefferies analyst Ken Usdin said the numbers revealed that First Republic’s total deposits had dropped by up to $89 billion in the week ended March 17 past week—or about three times more than the $30 billion injection from the bank.

“With [First Republic’s] earnings profile clearly impaired, the new deposits effectively bridge the estimated $30.5 billion of uninsured deposits still on [the bank’s] balance sheet, providing time for [it] to likely explore a sale,” Usdin said.

Janney Montgomery Scott analyst Tim Coffey said First Republic’s stock drop in recent days reflects uncertainty around what a potential second bailout would look like, or how the bank’s balance sheet is faring after a steep run in deposits and the falling value of its long-dated securities.

Another unknown is the company’s latest Tier 1 capital Ratio, a key measure of a bank’s balance sheet strength.

Like Silicon Valley Bank, First Republic’s balance sheet has had more than the usual exposure to long-dated securities, which have been falling in value as interest rates rise.

A typical mix for a bank of comparable size is to hold about 72% of securities as available for sale. The remaining 28% are held to maturity. First Republic’s mix is reversed with 12% available for sale and 88% held to maturity.

The bank’s mix of longer-dated assets now commands a lower market value, given where interest rates are. The bank’s emphasis on long-dated securities provided a better return when interest rates were near zero, but they have been a liability in the current environment.

“They’ve had duration risk where the value of their securities started going down as interest rates rose,” Coffey told MarketWatch.

Another problem for First Republic is that many of those long-dated securities are in the mortgage business, which has been ailing as interest rates rise.

Plenty of questions remain about First Republic’s situation and whether it could have been avoided. The challenges facing First Republic as well as the demise of Silicon Valley Bank and Signature Bank will be the focus of hearings on Capitol Hill next week.

Wall Street is also awaiting comments from the U.S. Federal Reserve when it updates its interest rate policy later on Wednesday.

And JPMorgan Chase continues to work with First Republic on a potential bailout, even as the bank has reportedly hired Lazard LAZ, -2.17%

to weigh strategic alternatives.

All of these factors add to the uncertainty swirling around First Republic, giving investors little reason to go long on the stock for now.