Vision Hydrogen Corporation (OTCMKTS: VIHD) is a renewable energy company with a primary focus on developing clean hydrogen production facilities which supply clean hydrogen to manufacturers and gas and power traders. They also work with consumers in the industrial and heavy and marine transportation sectors.

MarketBeat.com – MarketBeat

Earlier this month, Vision Hydrogen Corp started a steady—and rapid—climb up the market, from $5 on Monday Oct 31 to a closing price of $10.00 by Friday, November 4. Although the stock is thinly traded, Friday’s dollar volume increased by 25% to $1.7 million. This is only the most recent action from the same stock that shot up from $2.50 in December 2020 to upwards of $50 within the next month.

Now known as Vision Energy Corporation (OTCMKTS: VIHDD), the stock is currently trading at $14.79 with a market valuation of $420M.

Strategic Stock Split Should Boost Shares

This recent—and dramatic—shift in momentum came after the energy company announced the approval of a 1 for 2 stock split on November 7, 2022. The declaration also included the intention to change its name from “Vision Hydrogen Corporation” to “Vision Energy Corporation.”

As of on November 8, then, Vision Energy Corporation common stock is now currently trading under the ticker symbol VIHDD, designating the forward split, for the first 20 days. Effectively, then, by the end of the month, they will receive a new ticker symbol.

For now, we know the company’s common stock new CUSIP number is 92837Y200. This Forward Split results in an increase in outstanding common shares, from 21,048,776 to 42,097, 552. It will also increase double the number of authorized shares, to 200,000,000.

Expanding Hydrogen Operations Shows Promise

At the same time, Vision Energy Corporation also offered an update on their pioneering Green Energy Hub project in the North Sea Port of Vlissingen, the Netherlands. Through Vision Energy’s wholly-owned subsidiary, Evolution Terminals BV, has now reached the advanced stages of planning for both construction and the delivery of Northwestern Europe’s first import, storage, and handling terminal designed exclusively for hydrogen carriers, renewable energy products and low-carbon fuels.

The substantial redevelopment will allow Evolution Terminals to adopt industry-leading sustainable operating practices to reduce emissions from terminal activities. It will also introduce a green and renewable energy business model to the Netherlands at an opportune time.

Why Split the Stock Now?

On April 1, 2017 VIHD hit a historical high of $32.50 only to IMMEDIATELY plummet back to a new low of $5.207 on November 01, 2018. The stock made a quick rebound and peaked, again, at $11.50 on January 1, 2018. It hit a bit of a plateau at $10 before another slide and bounce and then flattened out to around $2.05 through the second half of 2020. Fortunately, the stock shot up to $14.75 by the end of that year, only to begin another decline to reach its most recent low of $2.375 on September 1, 2022.

Net income has been negative for a majority of the company’s operations. This is particularly notable because net income went from -$478.4K in 2016 to +$8.9K in 2017 and then fell back down to -$554.0K in 2018. This translated to Earnings Per Share (EPS) of -$0.17, $0.00, and -$0.07, respectively.

At the same time, revenue has been increasing: from 20.9k in 2016 to 7.5M in 2018. Gross income from operating expenses also increased from 418K to 2.0M between 2016 and 2017, but then settled at 1.8M in 2018.

Observing all of this, it makes sense that Vision Hydrogen considered a split. With the decline, they’ve seen the last year this could give them a fresh start.

A Complicated Position in A Complex Industry

Moving forward, it is difficult to say how VIHDD will perform against its peers and competitors but its current state certainly implies the stock has a lot of room to grow. Yes, its current value is still around $15—basically, the historical high for the [new] stock—which is significantly better than the recorded historical low ($1.25); indeed, the year-to-date is up +224.32%.

However, these are probably the only positive values for VIHDD right now, especially when compared with companies like NextEra Energy (NYSE: NEE) and The Southern Corporation (NYSE: SO). NextEra ($81.61; +4.36%) is the largest electric utility holding company in the United States, including both fossil fuels as well as green energy like wind and solar. The Southern Company is a more traditional fossil-fuel-based electrical company (which Forbes has recently named the “2nd best Large Employer in America”)

Neither of these companies is having a stellar year, as NEE and SO are down -16.24% and -7.49%, respectively, on the year so far. That said, analysts have some positive expectations, suggesting upsides of around 19% for both energy companies. Furthermore, Southern has a Price-to-Earnings ratio (P/E) of 20.18; NextEra’s is roughly double that. These are also particularly excellent metrics, especially when compared against VIHDD’s current—and, let’s remember, limited—P/E of -45.42. Finally, both NEE and SO have favorable Return-on-Equity metrics—around 12.25% each—while VIHDD’s RoE is currently -391.22%.

By comparison, though, other hydrogen stocks are also down, despite the promise that hydrogen offers for the future of energy. Ballard Power Systems (Nasdaq: BLDP), Plug Power (Nasdaq: PLUG), and Bloom Energy Corp (NYSE: BE) are also all on an upswing from recent lows, hoping to recover their once-great heights.

At the end of the day, though, VIHDD gets a BUY rating, mostly because the split gives it more opportunity to grow; and the evidence suggests it will continue to do just that.

Opinions expressed by Entrepreneur contributors are their own.

So, you’ve done it. Your lifelong dream of being a business owner is now a reality. You’re running a successful company. But have you considered what happens when you’re ready to retire? Or even worse, what happens if there is a premature death or disability of an owner? While it may seem like a far-off reality, legacy planning for the business you’ve worked hard to build is an essential ingredient in running a successful business for the long haul. And that’s where a buy-sell agreement comes in.

A buy-sell agreement is, in its barest definition, a contract between business owners to provide for ownership succession. It is a foundational tool that helps ensure the business can keep thriving as the organization and its owners grow and change.

Below are some of the key questions to consider when creating your buy-sell agreement.

Often, we see that the exiting of an owner can cause the organization to produce a large amount of capital for the owner’s buyout, which has the potential to create financial stress on the company. This can often be mitigated through stipulations in the buy-sell agreement.

There are several ways to fund owner exits, including lump-sum payments, installment payments and gradual stock transfers. Transfer of this risk to an insurance company can also mitigate the capital needed from the business or other owners. Working with a wealth advisor and an attorney can be useful to figure out a good financing option for your organization.

2. How should you structure any insurance policies held to fund a buy-sell agreement?

While this may seem unlikely, protecting your business in the event of an owner’s death or disability is important. The two most common forms of funded buy-sell agreements are cross-purchase and entity purchase arrangements.

Usually implemented in businesses with fewer owners, in a cross-purchase arrangement, each owner purchases an insurance policy on the other. This allows the surviving owner to fund a buyout using the insurance proceeds and increases the tax basis of the survivor. This can also help reduce any subsequent taxes due on a future sale of the business. In an entity purchase arrangement, the business owns the insurance policies on all owners and uses the proceeds to repurchase the shares, which are then retired.

Typically, when owners start exiting, the business is still going. Therefore, it’s important that the buy-sell agreement lays out the terms of owner transition.

For example, who is replacing this owner? What guardrails are in place for the person replacing this exiting owner? How will knowledge transfer work? All of these items should be outlined in your buy-sell agreement to help ensure the business is not negatively impacted by an owner’s exit.

4. How do you prepare for the unthinkable?

Despite the efforts many business owners put into planning for the inevitable, you can’t predict the future. The unprecedented Covid-19 pandemic resulted in significant business slowdowns and caused many business owners to revisit their buy-sell agreements. Some took advantage of the temporarily decreased value of their businesses and moved them into trusts at a significantly lower valuation. Others temporarily adjusted valuation calculations and owner stipulations to keep the business safe while it “weathered the storm.”

Let’s say an employee wanted to buy into their business during the pandemic. Based on the existing valuation formula, the transaction would have occurred at a significantly undervalued price for the owner. A review of the business owner’s buy-sell provision in the operating agreement resulted in adding a section to allow for the normalization of earnings in times of temporary stress. We are seeing more and more agreements include these types of “failsafe” clauses to protect a business during unforeseen, usually temporary events.

5. How will you valuate your business?

Your buy-sell agreement should outline how you value the business. There are a few ways one can value their business for legacy ownership or sale. Earnings Before Interest, Taxes, Depreciation and Amortization (EBIDTA) multiples are one way but are not the only way.

From book value to enterprise value, it’s vital to use the right formula for your industry and organization. It is also fairly common to include a failsafe provision that allows an independent valuation expert to appraise the business. And even more importantly, as the company grows, it’s essential to reassess your valuation formula. Of course, it’s not wise to constantly change your valuation formula. However, if your company grows from 20 employees to 200, it may be time to revisit your valuation method.

6. How will you create a business prepared for your exit?

Once you’re ready to retire and fully enjoy the fruits of your labor, it’s important that the transition set you — and the organization you’ve worked hard to build up for success. Will you remain on the board? Will you be passing the organization to family or key employees? Will you be selling the business? These are key questions to consider as you build the legacy terms in your buy-sell agreement.

Whether you’re a business owner who hopes to sell soon or one who wants to build the company for many more years, an effective succession begins before the exit happens. Developing a high-quality buy-sell agreement is an important part of legacy planning. Answering these questions can help protect the integrity of the business you’ve worked hard to establish.

Revenue is growing and losses are narrowing, but that wasn’t enough to stop shares of luxury electric vehicle maker Lucid Group (NASDAQ: LCID)from gapping down Wednesday.

MarketBeat.com – MarketBeat

The company reported third-quarter results late Tuesday, with shares plummeting more than 18% on news of declining reservations, or advance orders, for the Lucid Air electric sedan.

Lucid was already trending lower ahead of the release. The stock is down 27.88% in the past three months and 64.52% year-to-date.

The company specializes in luxury EVs. It is vertically integrated, meaning it engineers, designs, and manufactures vehicles, battery systems, and powertrains.

It went public in 2021 via a SPAC merger, although the company was founded in 2007 to produce battery technologies.

California-based Lucid said it received reservations for around sedans in the quarter, down from 37,000 previously. The company said it was on track to deliver between 6,000 and 7,000 for the full year.

Lucid reported a loss of $0.32 per share, greater than the consensus estimate of $0.31 per share. That was still an improvement over a loss of $0.43 per share in the year-ago quarter, but Wall Street was looking for more.

Missing Analyst Views

Revenue came in at $195.5 million, a huge year-over-year improvement, but also falling short of analyst expectations.

Those misses, combined with a slower rate of advance orders, resulted in Wednesday’s selloff.

Other highlights from the report include:

Record quarterly production of 2,282 vehicles, more than triple the number in the previous quarter

Third-quarter revenue driven by customer deliveries of 1,398 vehicles in the quarter

More than 34,000 reservations, representing potential sales of over $3.2 billion

Announced plans to open Project Gravity SUV reservations in early 2023

Capital expenditure was $290,064 in the quarter, more than triple the year-ago quarter’s $92,780. Investors can see the results in the company’s greater production recently.

For the full year, analysts expect Lucid to post a loss of $1.05 per share, narrowed from 2021’s loss of $3.48 per share.

The stock’s chart shows a decline that began in November of last year, punctuated by failed rally attempts in July and August, and again in October. In fact, Lucid notched a gain of 2.29% in October, but the stock quickly rolled over.

It’s not the only EV startup suffering. Rivian Automotive (NASDAQ: RIVN), which reported earnings after the bell on Wednesday, is down 16.38% in the past three months and 69.28% year-to-date.

Wall Street had expected the maker of electric trucks to post a loss of $1.82 per share on revenue of $550 million. The company reported per-share earnings of $1.57 on revenue of $536.

Supply Chain Still An Issue

The company cited supply-chain constraints as a factor that limited production in the quarter.

In the earnings release, the company said, “Based on our latest understanding of the supply chain environment, we are reaffirming our 2022 production guidance of 25,000 total units produced. We are also reaffirming the annual guidance provided during our second-quarter earnings call of $(5,450) million in Adjusted EBITDA.”

Rivian said it was slashing its capital expenditure guidance to $1.75 billion, shifting some of that to next year.

The company expects its R2 platform, with production based in Georgia, to launch in 2026.

Rivian is also a newly public company, having made its debut exactly one year ago, just as broader markets were weakening and pulling into a downtrend. That was unfortunate timing, to be sure. The stock has had small tradeable rallies when it was possible to pocket some fast profits, but for investors, it hasn’t offered much of an opportunity yet. Shares were up in after-hours trading Wednesday.

Opinions expressed by Entrepreneur contributors are their own.

In July, world leaders agreed to impose extra import tariffs on Russia during the G7 Summit, but the impact has been felt in other countries, including the U.S., with trade reduced by an estimated 62%, according to an analysis of the economic consequences of war. Russia’s war with Ukraine, and the subsequent trade sanctions placed on Russia, have impacted many businesses that rely on overseas trade. Now, businesses with overseas suppliers need to prepare for the uncertainty of trade tensions, tariffs and even the potential for embargos as the war escalates.

Just look at Shell. When they ceased operation and use of any Russian properties or partnerships for their oil production, they certainly felt the impact. Shell, like many other energy companies, had to fill the void left after they their relationship ended with Russian energy. Ultimately, this led to a rise in oil and gas prices across the world. This isn’t something felt only by big business, though, as everyone deals with the impact of tariffs either directly or indirectly.

If your business is facing tariffs, trade sanctions or the effects of war, here are some strategies to plan against the potential threat it could pose to your business internationally.

Up until June of this year, the U.S.’s whiskey industry experienced lean times while exporting to the U.K. and EU, as Trump-era disputes over steel and aluminum trade resulted in steep tariffs on American whiskey. The whiskey companies had to monitor their profit margins and the number of tariffs their profits could take.

For international businesses experiencing periods of higher tariffs, it requires analyzing what costs can be absorbed and covered, and what sorts of belt-tightening and cost-cutting could help mitigate the impact of tariffs and to offset their cost on your business. While cutting costs can help improve profit margins, the negative effects of the tariff still exist, but at least consumers won’t see a drastic increase in price of your product. It’s all a matter of how much your business can stand to lose in profit margin and remain profitable domestically and abroad or if it can at all.

Pass the cost onto the consumer

On the other hand, a business always has the option to raise its prices to offset the tariffs’ impact on its bottom line. With that, however, comes the risk that customers may no longer want to buy your product.

Harvard Business Review emphasized that risk can be offset, though, if your business has an honest approach to explaining why it’s raising its prices. Communication is key. Leveling with your customers and being honest regarding the realistic implications of a trade war go a long way.

Transferring the risk by insuring against it is another option. Risks from tariffs can, in many cases, be included in Business Interruption Due to Legislative insurance. However, the trade-related risk is ever-evolving and complex, which can make it difficult and costly to insure in the third-party commercial insurance market. This is where captive insurance can be an option.

Captive policies often have fewer policy exclusions than commercial insurance policies. Captive insurance also negates the perceived sunk cost of paying insurance for a risk that doesn’t materialize.

For example, insuring against tariff risk for 10 years without any losses to tariffs occurring over the course of those 10 years would equate to money out the door. Outside of the comfort of knowing you’re insured, the business really has nothing to show for the premiums paid over that decade.

With captive insurance, however, your business can retain profits when claims aren’t paid. Thus, allowing for a build-up of cash reserves and benefiting the balance sheet of your business. This makes captive insurance a very effective tool especially in times like now where many businesses have been left scrambling after the sweeping sanctions against Russia and high inflation.

Decide whether to exit a market or category completely or find a supplier not subject to tariffs

Tariffs cut both ways, even though they exist to operate as barriers to prevent competing foreign products and businesses from damaging domestic industries. Just look to the specific industry of washing machines as tariffs introduced by the U.S. during the Trump presidency resulted in washer prices rising by almost 12%, according to economists at the University of Chicago and Federal Reserve.

This resulted in domestic business owners being left having to pay their own domestic government tariffs for buying the products instead of the country they imported them from. As you can imagine, this has implications for international business owners as well, especially in industries like agriculture where the World Trade Organization cites 100% of products as having a tariff.

For the businesses and consumers that needed those washers, they were left paying the increased price for them instead of China or other countries targeted by U.S. tariffs. According to UCLA Anderson Review, additional studies have also concluded that the trade war hurt U.S. consumers and companies more than it did China.

The example illustrates why having an international supplier that isn’t affected by the sanctions or tariffs faced by your company or products from your country is very important. This option is, however, mostly reserved for businesses that can afford to move major portions of their supply chain to other countries — making this option limited to few businesses. Partnering with a business in a country without the same tariffs or sanctions is also an option, but again, has many logistical complexities few businesses are prepared for.

Although there are immediate implications concerning the sanctions against Russia that can potentially decimate a supply chain, it’s crucial for businesses to keep in mind that the impact will also be felt long-term. Trade wars typically slow economic growth. Thus, it behooves businesses to start now and conduct a risk assessment in relation to both the sanctions and the potential for an economic slowdown. Even if your business isn’t impacted now, it could be in the future.

On the surface stocks just seem to be trading calmly in a trading range. Under the surface things are setting up for continuation of the bear market which is why UBS now predicts market bottom around 3,200 for the S&P 500 (SPY). Get 40 year investment veteran, Steve Reitmeister’s, updated market outlook, trading plan and top picks to profit even as stocks head lower.

shutterstock.com – StockNews

The S&P 500 (SPY) is virtually frozen week over week. But don’t let that calm exterior fool ya’. There has been a serious spike in volatility since the Fed meeting.

What does it mean?

In a word…NOTHING!

If you are interested in a deeper explanation, with a trading plan for what comes next, then keep on reading this week’s edition of Reitmeister Total Return commentary.

Market Commentary

In last week’s commentary I was preparing folks for the Fed’s Wednesday announcement. Here were the key points that proved to be quite true:

“Let’s start with the Fed’s game plan as clearly spelled out in Chairman Powell’s Jackson Hole speech in August:

This is a long-term battle to get inflation back to 2% target

Do NOT expect lower Fed rates through 2023

Expect “economic pain” which was further described as below trend growth and a weakening of employment.

Now let’s remember that this speech quickly sobered up investors who were enjoying a 18% summer rally up to 4,300. A month later we were making new lows below 3,600.

The Fed cherishes clarity and consistency in their communication. And thus, I say that any investor who thinks there will be a meaningful change in policy announced Wednesday, only a couple months after the Jackson Hole speech, is smoking something that is still quite illegal.

Now we get down to the tricky part. That being to determine which is the more likely scenario going forward.

Scenario 1: Inflation moderates sooner than expected leading to less total Fed intervention and creation of soft landing for economy. In this case, it is not unreasonable to say that we have reached market bottom and new bull market emerging.

Scenario 2: We have already opened up Pandoras box with the economy. Once the wheels are in motion to move towards recession, then the economy can go through a vicious cycle that grinds lower and lower. In this case the bear market is still in play with likely bottom closer to 3,000.

Which scenario is right?

I believe Scenario 2 is much more likely and why I remain bearish. However, Scenario 1 is a possible outcome that needs to be monitored closely.”

(End of 10/28/22 Commentary)

Now let’s remember the key point made by Chairman Powell on Wednesday. That being the window to create a soft landing has narrowed. That statement was the nail in the coffin for stocks as the S&P 500 (SPY) went screaming lower by -2.50% on the session.

Therefore Scenario 1 of a soft landing is even less likely than I stated last week and therefore the bearish Scenario 2 is that much more likely.

None of the news since then has been a positive for stocks including:

Slew of large layoffs from leading tech companies like Twitters, Meta, Peleton, Ford, Snap, Wayfair, Robinhood. The list is much longer. Read more here if you can stomach it.

PMI Composite Index for October ends at 48.2 down from 49.5. Even worse is the Services component at 47.8. (Under 50 = contraction).

NFIB Small Business Optimism Index drops to 3 month low of 91.3 (below 100 is bad news). Here is the key line from NFIB Chief Economist, Bill Dunkelberg: “Owners continue to show a dismal view about future sales growth and business conditions, but are still looking to hire new workers.”

Commodity prices, especially energy, have spiked once again not helping the inflation picture. See that here.

Reity, if all of this is true…then why are stocks not falling farther, faster?

Because that is not how the market works.

Even during the most raging bull market there are countless pullbacks and corrections before stocks make their next leap forward. That is no different with a bear market. Just everything is 180 degrees in the opposite direction.

Meaning that during bear markets we have tremendous drops followed by rip roaring rallies followed by the next drop to new lows. The sooner you are comfortable with this pattern, the easier it will be to ride out the highs and lows.

So at this stage the price movements are just noise and nonsense. Quite likely investors are awaiting the next obvious catalyst. I suspect that will come on the employment front that has been a bit too robust for investors to fully fret a looming recession.

Simply these newly announced layoffs are just the tip of the iceberg that starts the souring of the employment picture. Once that negative trend gets a foothold, investors know it will only get worse.

That is when we likely start the next leg lower for stock prices. First retesting the recent lows just under 3,600. And after that quite a bit lower.

Unknown and unknowable at this time. Yet, I am confident predicting much lower than we are now…and probably another 3-6 months until that final capitulation before the next bull market begins.

As such, keep your bearish bias in place with trading strategies to generate profits as stocks head lower.

What To Do Next?

Discover my special portfolio with 9 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a robust gain for investors as the market tanked.

And now is great time to load back up as we make even lower lows in the weeks and months ahead.

If you have been successful navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 9 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.10 (-0.03%) in after-hours trading Tuesday. Year-to-date, SPY has declined -18.64%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Restaurant operator The Cheesecake Factory (NASDAQ: CAKE) stock remains buoyant despite reporting a surprise loss in its Q3 2022 earnings. It operates over 310 restaurants under the Cheesecake Factory banner also including North Italia and Flower Child restaurants. The Company continues to be impacted by the economic headwinds of cost and wage inflation in a potential recessionary backdrop as consumers tighten their discretionary spending. The Cheesecake Factory missed on nearly every metric in its recent earnings report and expects commodity inflation of 15% for its fourth quarter, and yet shares were not only able to snap back from lows, but also breakout through its year-long weekly downtrend channel. When stocks remain resilient after a grim earnings report, it usually means Mr. Market thinks the worst is behind them. Cheesecake Factory shares are down (-13%) for the year, which still outperforms the S&P 500 (NYSEARCA: SPY) down (-21%).

MarketBeat.com – MarketBeat

Word of Mouth Marketing

To its credit, Cheesecake Factory has been a success story that’s grown a multi-generational customer base solely through word of mouth. Casual dining restaurant brands like Darden Restaurants (NYSE: DRI) with Olive Garden, Brinker International (NYSE: EAT) with Chilli’s or Bloomin Brands (NASDAQ: BLMN) with Outback Steakhouse spend a considerable amount on marketing and advertisements through television, newspaper and digital channels. Although it does keep an active presence on social media, The Cheesecake Factory is unique because it hardly spends any money on advertising.

Sugar Crash

On Nov. 1, 2022, Cheesecake Factory released its third-quarter fiscal 2022 results for the quarter ending September 2022. The Company reported a non-GAAP diluted earnings-per-share (EPS) loss of ($0.03), missing analyst estimates for a profit of $0.30 by (-$0.33). Revenues rose 3.9% year-over-year (YoY) to $784 million, missing analyst estimates for $799.2 million. Same store sales rose 1.1% YoY (missing expectations for 2.8%) and 9.5% compared to 2019. Inflationary pressures took its toll on margins. The Company bought back 889,000 shares for $26.7 million in the quarter and increased their stock buyback authorization by 5 million shares, raising total authorization to 61 million shares. The Company plans to open 13 new restaurants in fiscal 2022. The Company ended the quarter with $372 million in liquidity comprised of $133 million in cash and $239 million in available credit.

Keep Your Chin Up

Cheesecake Factory CEO David Overton commented, “While our operational performance has been solid and core cost inputs have become more stable and predictable, we continue to face a dynamic and challenging inflationary environment in some areas. As a result, our profit margins in the quarter reflected higher than anticipated operating expenses particularly in utilities and building maintenance.” He continued, “However, we remain highly focused on returning restaurant margins to pre-pandemic levels in the near-term supported by appropriate pricing actions to offset the higher costs while also managing the business for the long-term including increasing market share.” In an attempt to return margins back to pre-pandemic levels, the Company will be raising menu prices by another 2.8% starting in December 2022. This is in addition to the 4.2% price hikes its already administered.

Impressive Unit Volumes

It’s worth noting that average unit volumes at flagship The Cheesecake Factory brand restaurants track $12 million for the year. This underscores the strong affinity for the brand, even more impressive due to lack of any spend on advertising. Labor productivity and food efficiency exceeded internal expectations but building and maintenance costs were higher than anticipated. The Company opened three new restaurants in the quarter including The Cheesecake Factory in Katy, TX, North Italia in Dunwoody, GA, and its first Fly Bye restaurant in Phoenix, AZ. Fly Bye is its latest fast casual dining concept incorporating Detroit enhanced stretch style pizza and crispy chicken.

Reversing a Year-Long Downtrend Channel

The weekly chart for CAKE stock illustrates the year-long falling downtrend channel that’s been in place since peaking at $51.19 in September 2021 and hitting a low of $26.12 in July 2022. Shares bounced and gained momentum on the breakout through the weekly market structure low (MSL) trigger above $27.92 on July 18, 2022. This propelled shares to breakout through the upper falling trendline at $32.50 on October 17, 2022. The 20-period exponential moving average (EMA) resistance is now sloping up as support at $32.25 followed by the 50-period MA at $34.42. The recent bounce peaked at $36.46 before pulling back through the weekly 50-period MA to form a weekly market structure high (MSH) sell trigger on a breakdown below $31.81. The weekly 20-period EMA is trying to hold support at $32.25. Selling volume spiked in the last week of October but was absorbed by the weekly 20-period EMA. Pullback support levels to watch sit at the $31.81 weekly MSH trigger, $29.96, $27.92 weekly MSL trigger, $26.12 swing low, and $24.86.

The stock market continues to be a challenging environment with rising rates a potent headwind. So far, the economy has been stable enough so that earnings growth has not contracted, but this is unlikely to persist the longer the Fed stays hawkish. This article discusses characteristics of stocks that are likely to outperform and 3 stocks with these characteristics – Lockheed Martin (LMT), Vertex Pharmaceuticals (VRTX), and Elevance Health (ELV).

shutterstock.com – StockNews

The stock market dove lower following the FOMC press conference where Chair Powell made it clear that even if the Fed were to slow its pace of hikes, the job is nowhere close to completion. This led to estimates of the ‘terminal rate’ of this hiking cycle to increase following the meeting with 5.5% now the consensus.

Of course, the higher the terminal rate, the more pain that will be inflicted on the economy especially in areas like finance, housing, and real estate. Bonds are likely to suffer, and there are increased chances of a liquidation event if borrowers are unable to meet their obligations which becomes more likely in a high-rate world. Stocks will also suffer which could intensify if earnings materially decline.

These environments mean that investors have to be extremely judicious in terms of making their selections. They should look for stocks whose prospects are disconnected to near-term economic or monetary factors.

LMT is a security and aerospace company that has four segments: Aeronautics; Missiles and Fire Control; Rotary and Mission Systems; and Space. The company produces high-tech weapons and defense systems but is best known for its F-35 fighter jets. In addition to these services, LMT provides a wide variety of services for governments all over the world.

In terms of the current environment, LMT is an ideal selection to ‘beat’ the bear market. For one, government budgets and defense spending are much less volatile than other parts of the economy. In fact, defense spending, on a global level, has grown at about an average, annual rate of 5% over the last couple of decades with the only dip being during the dissolution of the Soviet Union in the early 90s.

Second, companies like LMT often receive long-term contracts and only have a few competitors given that these projects are quite sophisticated and require security clearance. They also tend to have large balance sheets and a long history of paying and raising dividends which also leads to outperformance during periods of economic turbulence.

LMT has an overall B rating, which translates to a Buy in our POWR Rating system. B-rated stocks have posted an average annual performance of 20.1% which compares favorably to the S&P 500’s annual performance of 8.0%.

In terms of component grades, LMT has a B for Value due to its forward P/E of 14 which is cheaper than the S&P 500 (and less prone to negative revisions). It also has a B for Quality due to being one of the leading aerospace & defense companies. Click here to see more of LMT’s POWR Ratings.

Vertex Pharmaceuticals (VRTX)

VRTX discovers and develops small-molecule drugs for the treatment of serious diseases. Its key drugs are Kalydeco, Orkambi, Symdeko, and Trikafta for cystic fibrosis, where Vertex therapies remain the standard of care globally. The company also focuses on developing treatments for pain, type 1 diabetes, inflammatory diseases, influenza, and other rare diseases.

The company’s cystic fibrosis drugs are poised to continue dominating the market for the foreseeable future due to the disease-modifying potential of the drugs, consistent use by patients, and very little competition. VRTX combination therapies also have lengthy patents, which protect its cystic fibrosis portfolio from generics. There is also potential for its non-cystic fibrosis pipeline, which has exposure to promising areas, such as AAT deficiency, sickle cell disease, and beta-thalassemia.

VRTX has an overall grade of A which equates to a strong Buy rating in the POWR Ratings service. A-rated stocks have posted an average annual performance of 31.1% which compares favorably to the S&P 500’s average annual gain of 8.0%.

VRTX also has strong component grades including an A for Quality due to 11 out of 19 analysts covering the stock having a Strong Buy rating with only 2 having a Sell rating. It’s also regarded as one of the top companies in the space due to its dominance of the CF market and strong pipeline of potential, blockbuster treatments. Click here to see more of VRTX’s POWR Ratings.

ELV is a managed care company, providing medical benefits to roughly 44 million members. The company offers employer, individual, and government-sponsored coverage plans. It is also the largest single provider of Blue Cross Blue Shield branded coverage. This sector has also been particularly strong due to a very low unemployment rate which means that the company has seen strong growth in enrollees.

Further, the pandemic was a boost to its bottom-line as less people were going to the doctor and undergoing procedures. Therefore, the company’s payout ratio declined. Many analysts had been expecting an above-average reading as the economy normalized, but so far this has simply returned to pre-pandemic levels.

Another reason to like managed care stocks is their pricing power as healthcare spending tends to rise at a faster pace than inflation. And, they tend to be less affected by economic slowdowns. Currently, the company is seeing growth from its Medicare Advantage plans and virtual care services.

With these attributes, it’s not surprising that ELV has an overall grade of A, which translates into a Strong Buy rating in our POWR Ratings system.

LMT shares . Year-to-date, LMT has gained 38.22%, versus a -19.84% rise in the benchmark S&P 500 index during the same period.

About the Author: Jaimini Desai

Jaimini Desai has been a financial writer and reporter for nearly a decade. His goal is to help readers identify risks and opportunities in the markets. He is the Chief Growth Strategist for StockNews.com and the editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Jaimini’s background, along with links to his most recent articles.

Disclosure: Our goal is to feature products and services that we think you’ll find interesting and useful. If you purchase them, Entrepreneur may get a small share of the revenue from the sale from our commerce partners.

Companies love robots working alongside humans. They don’t take days off and are incredibly reliable. That’s why, in a restaurant industry plagued by labor shortages, kitchen automation solutions from Miso Robotics have been gaining a ton of traction.

MisoMiso Robotics

After successfully automating kitchen operations for major U.S. fast food brands, Miso is sending its robotic assistants to the international market and allowing investors a chance to join them.

Here’s why Miso may truly hold the key to the future of fast food.

Miso helps make restaurants more efficient.

From low wages to hot grease, people have found plenty of reasons not to work in fast-food kitchens. As a result, 500,000 new fast-food jobs go unfilled each month, leaving many brands in desperate need of automation solutions.

That’s why Miso designed robots to cook food, pour drinks, and perform other repetitive tasks that humans prefer to avoid. For example, Miso’s Flippy 2 robot can fry, its Sippy robot pours drinks, and its Flippy Lite robot can fry and season items, most recently used by partners to make tortilla chips.

All of these robots improve efficiency over time thanks to machine learning. And as a result, restaurant staff have more time to focus on customer-oriented service, knowing Miso’s bots deliver consistent quality.

What’s more, Miso’s tech also addresses the fast-food industry’s longstanding tradition of low profit (average 5% margin) and rapid labor turnover, which have contributed to many restaurants’ lack of consistency and quality.

With Miso, these are problems of the past. Its robots provide restaurants with a low-cost, user-friendly way to boost efficiency and have shown the potential to increase restaurant profit margins threefold.

And thanks to the Robot-as-a-Service (RaaS) model, restaurants only pay a monthly fee for Miso’s tech, allowing them to see a positive return on the first day of operations.

It’s no surprise that so many restaurants have already partnered with Miso, but this is just the beginning.

Miso’s world tour.

Many of fast food’s top brands have already adopted Miso’s AI-powered automation solutions. White Castle, Jack in the Box, Buffalo Wild Wings, and Caliburger are among many beloved restaurants that already have Flippys and Sippys lowering costs and boosting efficiency.

But the opportunity for Miso to expand its footprint is even bigger abroad. Take Europe, for example, where brands spend up to 50 percent more trying to fill the labor gaps.

That’s exactly why Miso’s landed a new international partnership that they expect will play a huge role in the company’s expansion to the 20-million-restaurant global marketplace — a 17 times larger opportunity than in the U.S. alone.

With several top fast-food restaurants stateside and a global house of brands on the horizon, Miso’s believes it has proven that there’s a universal need for its automation solutions.

Get in on Miso’s as it plans a global expansion.

More than 20,000 investors have already realized Miso’s status as an early mover, giving Miso the chance to build a solid foundation and partner with America’s most formidable fast-food brands. Now, they are going global and raising additional funds to further innovation in a market where demand is even stronger than when they started.

Miso Robotics is offering securities through the use of an Offering Statement that has been qualified by the Securities and Exchange Commission under Tier II of Regulation A. A copy of the Final Offering Circular that forms a part of the Offering Statement may be obtained from: Miso Robotics

Entrepreneur may receive monetary compensation by the issuer, or its agency, for publicizing the offering of the issuer’s securities. Entrepreneur and the issuer of this offering make no promises, representations, warranties, or guarantees that any of the services will result in a profit or will not result in a loss.

Opinions expressed by Entrepreneur contributors are their own.

Once an entrepreneur, always an entrepreneur, right? It’s in the DNA of a founder to re-create their original success over and over by starting new businesses. After all, it’s why the term “serial entrepreneur” is so popular. Richard Branson, Elon Musk and many more continually reinvest their profits in new ventures. While that is certainly one tactic, using a portion of your profits to create an investment fund can be infinitely more valuable.

tdub303 | Getty Images

There are many forms of investment companies that manage pooled assets of multiple private investors, such as venture capital, private equity and hedge funds. While most startup founders don’t think of themselves as finance experts or professional investors, their experience building and exiting successful companies may very well equip them to succeed in making investments on behalf of others.

The seeds of my journey to creating a hedge fund started when I was an engineer focused on research and education computing (far from a finance background!). Eventually, that led to my role as a CTO at a startup, and I co-founded a firm that grew to $30 million in revenue in just under two years. Several liquidity events from that business became the foundation for building my family office, a private wealth management firm that runs like a hedge fund.

Today, that is the foundation from which I build my wealth rather than embarking on new business ventures. But why should other entrepreneurs consider following this path? Here are three reasons:

If you’ve started one successful company, it’s easy to think that you can do that repeatedly. But doing so can be more challenging than expected. The conditions that created outsized achievements the first time are hard to replicate as the world around us constantly changes. The best use of your proven business acumen may be to invest on behalf of others rather than diving headlong into developing another company.

That said, starting an investment fund isn’t unlike establishing another company. Your first step — even before you line up initial investors — should be to hire a good lawyer and contact your state’s Secretary of State for guidance about investment fund business structures. In the case of hedge funds, most are formed as limited partnerships, in which the founder acts as the general partner and an incorporated group of investors act as the limited partners. This means you would likely need to set up two entities: one for the fund itself and one to incorporate its various investors.

Bigger potential upside

A fund structure is attractive because it allows a successful entrepreneur to use their expertise to help others navigate investments. In addition, the financial rewards can be substantial. Successful fund managers, whether in venture capital, private equity, hedge funds or real estate, are highly compensated and only limited by their performance and how many investors they can attract.

For successful entrepreneurs such as myself, launching or participating in funds can amplify their expertise with capital and create a new kind of business that also brings about material financial contributions. In the course of founding your startup, you likely got to know some wealthy individuals who contributed to your success. Founding a fund can enable you to deliver value to these individuals in a new way. Because time is our most scarce resource, it doesn’t make sense for individuals with $20MM to invest their time into a $1-2MM opportunity, when instead they could invest that capital into your fund, go to the beach and call it a day.

Once entrepreneurs have participated in major liquidity events, they realize a great deal can be gained by exploring new investment opportunities, managing taxation, and utilizing estate planning. After all, the point of founding a startup for many entrepreneurs is to compress the working years of one’s life, sell the company and have more years of freedom. Founding an investment fund can allow you to do that.

For me, the idea of a fund seemed an appropriate encore to a successful business career. Fast forward to today — the strategies I spun off from my family office have become the heart of the TrueCode Capital Crypto Momentum Fund I founded. It allows me to spend my time sharing the lessons that made me a successful investor in digital assets and helping individual investors and family offices achieve growth, all while sleeping through the night.

Of course, founding an investment fund — like any venture — isn’t for everyone. But for those with confidence in their ability to read the market, with contacts among high net-worth individuals, and with a proven track record of business success, starting your own hedge fund may be the next career step you’ve been looking for.

Last week, we talked about how it felt like deja vu as the S&P 500 (SPY) embarked on its 3rd bear market rally of the year. Well, today it feels even more that way, as the market is rapidly giving back these hard-fought gains. The market is down 4% from yesterday’s brief spurt higher when it seemed like the FOMC was endorsing a slowdown in the pace of hikes. But, these hopes were dashed during the press conference when FOMC Chair Powell pushed back against this notion and stuck to his hawkish leanings. In fact, he said that the terminal rate could go much higher which was the catalyst behind the selloff. In today’s commentary, I want to break down the Fed meeting and then discuss why it’s a bearish development for the market and confirmation of our bear market thesis. Read on below to find out more….

shutterstock.com – StockNews

(Please enjoy this updated version of my weekly commentary originally published November 3rd, 2022 in the POWR Stocks Under $10 newsletter).

Over the last week, the S&P 500 (SPY) is down by 2%. And, it’s a brutal end to the bear market rally. In fact, it is better evident if we look at the Nasdaq 100, where 2 of the market’s generals have been slaughtered and laid to waste – GOOGL and META.

The index has already given back about 75% of its gains from the bear market rally. In contrast, the losses for the Russell 2000 and S&P 500 are much more muted.

This is a continuation of a theme that we discussed last week – the ‘market of stocks’ is holding up much better than the stock market.

And, it shouldn’t be too surprising given the rise in long-term rates which is more of a headwind for large and mega-cap stocks.

The rise in rates could relent if the market (or the Fed) saw some weakness in inflation data or the economy. That doesn’t seem to be the case although we will learn more about the state of the employment market tomorrow.

But so far, there is no indication of truly broad-based weakness for employment (based on unemployment claims) which means that rates are going to be ‘higher for longer’.

Why the FOMC Was so Bearish for the Markets

One of the reasons behind the ‘bear market rally’ was the belief that the Fed could be on the verge of ‘pivoting’ in terms of slowing its pace of hikes and eventually stopping sometime in early 2023.

Well, this is now in doubt as the stubbornness of inflation and specifically, core inflation makes it clear that hikes are going to continue for some meaningful period of time.

Now, we are back to the initial conditions which made January 2022 so bearish. Rates are rising, while growth is slowing. But growth isn’t slowing fast enough to cause the Fed to pivot.

Thus, rates will keep rising until the economy breaks or inflation breaks.

Rising rates are a potent headwind for the stock market. As we learned this year, the most bullish scenario is a choppy sideways market that gets some nice rallies out of oversold conditions.

While the most bearish scenario is that the S&P 500 (SPY) plunges lower when we get the combination of rising rates and negative news on the earnings or economic front.

Now that this bout of bullishness is over, I expect reality to set in over the next couple of weeks and the market to visit lower levels.

Portfolio Strategy

We are back to a neutral setting and prepared to take more action if the market breaks key levels on the downside which includes the October lows of around 3,600.

I would expect that cyclical stocks would lead on the downside, while defensive stocks and sectors would outperform.

What To Do Next?

If you’d like to see more top stocks under $10, then you should check out our free special report:

What gives these stocks the right stuff to become big winners, even in the brutal 2022 stock market?

First, because they are all low priced companies with the most upside potential in today’s volatile markets.

But even more important, is that they are all top Buy rated stocks according to our coveted POWR Ratings system and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks which could double or more in the year ahead.

SPY shares were trading at $373.35 per share on Friday morning, up $2.34 (+0.63%). Year-to-date, SPY has declined -20.48%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Jaimini Desai

Jaimini Desai has been a financial writer and reporter for nearly a decade. His goal is to help readers identify risks and opportunities in the markets. He is the Chief Growth Strategist for StockNews.com and the editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Jaimini’s background, along with links to his most recent articles.

The S&P 500 (SPY) may be in bear market territory, but that doesn’t mean that every stock is down. In fact, there are 3 really good reasons why Casey’s General Stores (CASY) has been in the plus column this year…and likely to stay there. Read on below for why you should be filling up your portfolio with CASY shares at this time.

shutterstock.com – StockNews

Let there be no doubt we are in the midst of a bear market. And most stocks will continue to head south.

Gladly some stocks will go up. Casey’s General Stores (CASY) is the perfect example. Not only is it up 10% in the past month. More impressively is it up over 15% year to date while the stock market sank brutally into bear market territory.

Why is CASY rising above the pack?

First, because investors cling to more defensive names that are at less risk when a recession is on the horizon. Indeed, CASY fits nicely into the consumer staples camp which is in fashion at times like these.

Second, and more importantly, the profit picture for CASY keeps on improving. The higher EPS picture compels investors to bid up shares given the increased valued found there.

Third, our POWR Ratings model analyzes 5,300 stocks across 118 unique factors to find those built to outperform. Not only is CASY sporting a rating of A (Strong Buy) rating. But even more impressive it is in the top 1% of all stocks across these 118 factors.

All this explains why Wall Street is a big fan of this stock with the analyst at Deutsche Bank pounding the table the loudest with $276 price target. That may not seem that much higher in the grand scheme of things. However, with the bear market far from over, and most stocks likely to fall another 100-20% from here…then that $276 target makes CASY quite compelling at this time.

What to Do Next?

You may be curious to see some of my other top pick articles. In fact, I recently shared my top 2 picks for the year ahead. Check those out below:

CASY shares closed at $224.94 on Friday, down $-2.27 (-1.00%). Year-to-date, CASY has gained 14.79%, versus a -19.84% rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

How funny it was to see traders get it wrong once again. They misread the Fed announcement at 2pm ET leading to a big 1% rally for the S&P 500 (SPY). Within minutes of Chairman Powell speaking it dawned on every body that things have not gotten better…only worse. And thus the odds of future recession and greater stock downside have greatly increased. This article spells out why. Even better it highlights a game plan and top picks to profit as the market heads lower from here.

shutterstock.com – StockNews

After the famed Chairman Powell speech from Jackson Hole in August investors got the memo that the recent rally was unfounded and time to start selling stocks once again. This prompted me to write this article, Investors: Wake Up and Smell the Pain.

Wednesday’s Fed announcement and press conference feels very much the same. That being investors getting ahead of themselves with a 9% rally in October before Chairman Powell lowered the hammer once again.

They say “fool me once, shame on you…fool me twice, shame on me”.

If true, then let’s highlight the key elements from the recent Fed announcement so you understand why we are likely headed towards a recession. And why stock prices will head much lower before this bear market ends.

Market Commentary

There are so many threads to pull on from the Fed statements on Wednesday. However, at the end of the day the key point came out 45 minutes into Chairman Powell’s press conference when he had to admit that the window to create a soft landing had narrowed.

Meaning it is possible to create a soft landing for the economy. But HIGHLY UNLIKELY.

Let’s remember that Fed has a slightly optimistic bias as they don’t want to unnecessarily scare people. And indeed, a soft landing is their preferred outcome. That being to bring down inflation with as little damage to the economy as possible before resuming growth and prosperity.

You could tell that Powell was trying to be as honest as possible with his answer for which he had to begrudgingly admit that the window for creating a soft landing had narrowed. That is because they have raised rates this much with little real effect on taming inflation. Thus, how much harder they will have to push on rates to bring down demand that will most likely lead to recession.

The S&P 500 (SPY) was up about +1% when his speech began. Within minutes investors could finally see that there may have been an improvement in clarity in their statements…but not a real change in policy. From there stocks started heading lower. But once Powell declared the window for soft landing had narrowed…it became a downright bloodbath for stocks ending in a -2.5% session.

The above is my morning after thoughts that would not allow me to get back to sleep before I got typed it out. Meaning above is what is most important for investors to understand. Yet indeed there is more to share.

Let’s roll back to the 2pm ET when the announcement came out.

I was watching CNBC intently and could not take my eyes off the movement of stocks with every new comment made on screen. It was truly amazing how every positive comment was followed by an uptick just seconds later. And every negative comment with a decrease in stock prices.

Most of the commentators were saying how amazing it was that this pivot was taking place to discuss the idea of slowing the pace of rate hikes and then pausing to see how the “lagged effects”. I was screaming at the TV “you guys don’t get it!!!” My wife joked that I was having a mental break.

Gladly CNBC economic commentator Steve Liesman echoed my view that indeed there is an improvement in the clarity of policy steps…but not a real change in the long term Hawkishness of the Fed. This became all the more apparent within minutes of Powell’s prepared speech that echoed many of the points from Jackson Hole just a couple months back. That being…

This is a LONG TERM battle to create price stability (closer to 2% target inflation)

Will not ease off too soon as it may reignite inflation before the job is done. “It is premature to discuss pausing”.

The economy will slow and labor markets will weaken. That is because the Fed intends to weaken demand to get in line with supply. This is how they expect to achieve lower inflation.

All in all, it seems the Fed is still on a path to a restrictive 5% rates with smaller rate hikes in the future. Followed by a pause to see the “lagged effects” of policy. Some are giving this idea of a pause far too much significance.

Just remember there is a 1-2 quarter delayed effect of Fed policy on the economy. So this is just the Fed being logical about reviewing conditions before making their next move as they fear going too far which would be even more detrimental to the economy.

As stated at the top, the most beneficial Fed statement came a full 45 minutes in when many folks may have checked out. He was asked if the window to create a soft landing has narrowed. He unfortunately had to admit that was the case and odds of soft landing are greatly diminished.

Also consider that as of now the Fed sees no real improvement in inflation. Especially true in the labor markets generating wage inflation. And thus, will keep raising rates. And thus, the full measure of those policies is not yet seen in the economy.

In my book there is NO WAY to bet on start of next long term bull market til investors appreciate how bad the economy will get. That is a first half of 2023 event and thus far too early to get bullish.

Once again, given that the Fed was late to the party to raise rates means they are highly unlikely to create a soft landing. They even admitted as much which was truly the nail in coffin for stocks on Wednesday.

So a hard landing means recession with commensurate reduction in stock prices. Thus the bearish thesis is unchanged. Just a matter of when the rest of the market wakes up to the message with correlated lowering of stock prices.

Not just a retest of recent lows. I mean the full measure of pain associated with a bear market.

Remember 34% decline is the average drop for a bear market. That equates to 3,180. However, the valuations for stocks started near record highs…yes even worse than the tech bubble of 1999. Thus, may have to fall a bit further than 3,180 to find bottom.

In the end the investment story is as simple as “Don’t Fight the Fed”.

They are telling you with a straight face that the odds of recession are very high.

BELIEVE THEM!

And trade accordingly with full expectation of lower lows on the way for stocks prices.

What To Do Next?

Discover my special portfolio with 9 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a robust gain for investors as the S&P 500 (SPY) tanked.

And now is great time to load back up as we make even lower lows in the weeks and months ahead.

If you have been successful navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 9 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares were trading at $370.94 per share on Thursday afternoon, down $3.93 (-1.05%). Year-to-date, SPY has declined -21.00%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Oil stocks have been one of the few bright spots in the S&P 500 (SPY), during the doom and gloom of the 2022 bear market. However, that party could soon be coming to an end. Below I lay out 3 reasons why oil stocks are no longer a buy, plus reveal how you can still profit from oil stocks as they retreat from their recent highs. Read on for more….

shutterstock.com – StockNews

Oil stocks have been the one place to make some serious upside over the past year. But even the energy names are looking tired and toppy following a frenzied rally at current levels.

Looks like it is finally time to take some profits and position for a pullback in big oil…

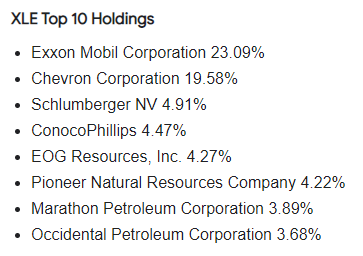

For our discussion, we are going to be using XLE, the Energy Select SPDR ETF, as the proxy for oil stocks. The top two holdings of XLE are the major oil companies ExxonMobil (XOM) and Chevron (CVX). Together these two comprise over 42% of the weighting for the ETF.

Oil Stocks Got Overbought But Are Weakening

The one-year price chart below shows the price action for the XLE. As you can see, XLE got to overbought levels on Wednesday before dropping sharply. 9-day RSI hit 80 then pivoted. MACD neared an extreme before softening. Bollinger Percent B approached 100 then fell.

Shares were trading at a big premium to the 20-day moving average. Previous times these indicators aligned in a similar fashion marked significant intermediate term tops in oil stocks.

I also highlighted the magnitude and length of the prior two rallies (purple lines). Note how they coincide almost identically with the current price action in XLE.

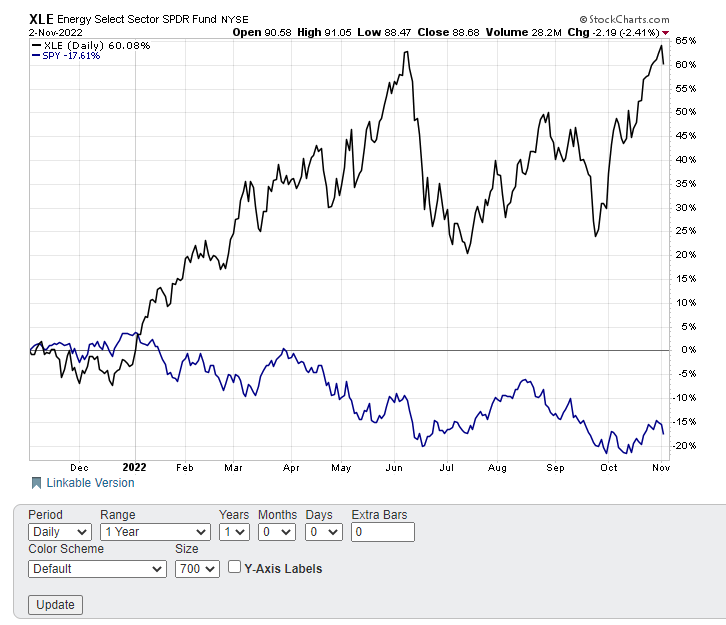

Oil Stocks Getting Extended Versus Stocks Generally

The yearly chart below of oil stocks (XLE) versus the S&P 500 (SPY) shows just how great the outperformance of XLE has gotten to stocks overall. The XLE shows a robust gain of just over 60% in the past 12 months compared to a nearly 17.5% loss for the SPY.

Remember that the major oil stocks such as ExxonMobil and Chevron are in the SPY as well, making the comparative performance even greater once the oil names are stripped out.

Interesting to note that the last time oil stocks hit such heights back in early June led to a significant drop, or mean reversion, in XLE. Look for a similar scenario to unfold with XLE being a relative underperformer to SPY over the coming months.

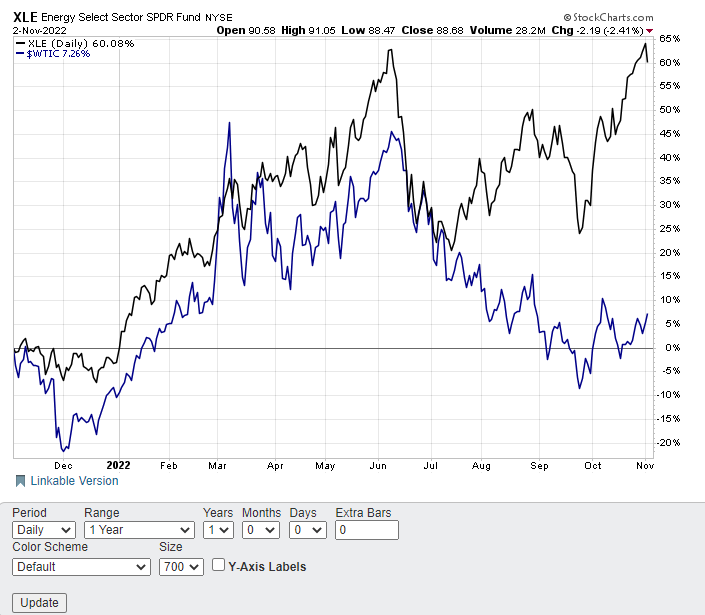

Oil Stocks Getting Way Ahead of Oil Itself

Oil and oil stocks tend to be well-correlated. This certainly makes intuitive sense. If crude climbs, oil stocks should follow and vice-versa.

That certainly was the case for the first half of the year, as seen in the chart below. Both oil and oil stocks made highs in early June as West Texas Intermediate Crude prices ($WTIC) traded well over $120 barrel.

Since then, however, we have seen $WTIC retreat sharply back under $90 barrel while XLE made a fresh new high. This divergence has now gotten to an extreme. XLE is now out-performing $WTIC by over 50% in the past 12 months.

I expect oil stocks to start to drop in sympathy with lower oil prices into year-end.

Traders and investors looking to position to profit from the anticipated convergence in XLE to lower levels can buy puts and put spreads on oil stocks or sell out-of-the money bear call spreads. We have done just that recently with a put diagonal on ExxonMobil (XOM).

What To Do Next?

While the concepts behind options trading are simpler than most people realize, applying those concepts at the right time to consistently make winning trades is no easy task.

With the quantitative muscle of the POWR Ratings as my starting point, I’ve uncovered some of the best options trades in the tough markets we’ve experienced this year.

That’s because I take advantage of both call and put options trades to generate big gains in ALL market conditions.

In fact, since launching the service in November 2021 I have delivered a market beating +65.44% return for my subscribers.

The good news is that you can become a subscriber today for just $1.

During your $1 trial you’ll get full access to the current portfolio, my weekly market insights and every trade alert by text & email.

Plus, I’ll be adding the next 2 exciting options trades (1 call and 1 put) when the market opens this Monday morning, so start your trial today so you don’t miss out!

SPY shares rose $4.99 (+1.34%) in premarket trading Friday. Year-to-date, SPY has declined -20.33%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

This is a transcribed excerpt of the “Bitcoin Magazine Podcast,” hosted by P and Q. In this episode, they are joined by John Carvalho to talk about building on top of Bitcoin, Bitcoin philosophy and what is happening with the Lightning Network.

Listen To The Episode Here:

Q: Is credit not “fiat” in nature or is there a way to create a healthy credit system through sound money? I feel like this is often debated and discussed and I don’t act or claim to know the right answer to this, I’m just genuinely curious if you feel as though there are components of credit that just make it inherently fiat.

John Carvalho: No, I mean, I think that’s kind of — I’m not trying to be rude or anything, but that’s just a word salad. They have definitions; these things had definitions. To you guys and everybody in the audience, if you want to try to have a tighter grasp of both the dynamics of Bitcoin and the economics that are relevant to it, read “Cryptoeconomics” by Eric Voskuil. There’s no Bitcoiner that understands these things on that level better. My interactions with him and reading with him helped me understand these things a lot more deeply as well.

He would describe Bitcoin as a market fiat. It’s almost like how some people would joke and say it’s a headless Ponzi. There’s no promise that you will get a trade value of bitcoin in the future for any specific amount.

Like bitcoin could be gone and nobody would be accountable. Bitcoin could be the most popular thing on Earth and you could buy a house with something that you only paid $5 for, but there’s no enforcement of the price by anything in the Bitcoin system. The only enforcement in bitcoin is just the quantity of them that you have in the system.

So you don’t know what you’re gonna get for your bitcoin until you try to sell it and it’s all relative to the person you’re selling it to. There’s no enforcement of the price. In a way, bitcoin itself is like a market fiat, a new type of fiat because there’s no controller, there’s no central issuer.

It’s something the market created to be able to have this concept of, and use this abstracted resource as a money. Credit and fiat are just two totally separate concepts. Credit is just simply saying [that] you have people that trust each other. So you have bitcoin for trustlessness. The market fiat, the trustless system, is simply saying, “If I want to have a unit of account where I don’t have to trust anybody to be able to use that, the ultimate store of value in the abstract, you have bitcoin. Everything else is credit.

You can say that fiat is a type of credit where they promise nothing. Fiat is just fiat by decree. You’re saying, “This is money.” You have no promise that the issuer will give you something for that money. Unless you wanna get philosophical and say, “Oh, they’re gonna give you an army for that money if you agree to have that money inflated or taken from you at will.” I don’t wanna get philosophical, so we’ll just say there’s no actual promise behind fiat, but credit is a trusted system. It’s acknowledging the fact that two people that trust each other can accomplish more than one person alone.

You can have a kind of singular nature. There’s kind of this dichotomy with humans, you have competition and cooperation. You wouldn’t have society if everybody was competing on everything all the time. When you have cooperation, you have society. Society is trust.

If you want to now cooperate with people over abstractions of economic concepts, you need credit systems. You need to be able to say, “I have one coffee shop. I have proven to my friends P over here that I can run a pretty great coffee shop and I want to have two coffee shops, but my profit margin to open two coffee shops would take me 10 years to open my second coffee shop and I want to open one next year.” And so if he says, “I think John can handle that, I’ll trust John with my money.” Now this is just a form of financing. Credit is like the minimum form of finance. It’s just saying, “I trust you for something in the future.”

I could say, “Ok. I am Starbucks. And I don’t wanna involve P,” I want to say to my customers, “Hey, I’m to sell coffees and I want you to buy them for the future at say a 20% discount.” And now you say, “Well I plan on buying coffees from John or Starbucks for the next five years. That’s a great deal and I’m gonna pre-buy them.” I can now take that and I can leverage that trust and I can use that extra money to open the second coffee shop as long as I can meet my commitments to the redemptions of the coffee.

So you can see how credit is not that much different than finance because you can kind of independently finance things if you take risks on leveraging your credit obligations.

While the Fed hinted at slowing the pace of interest rate hikes after increasing rates by another 75 basis points today, the market is expected to remain under pressure as a soft landing still looks impossible. However, this bear market also presents the perfect opportunity for bargain hunters to increase stakes in resilient businesses Walmart (WMT) and Gartner (IT) available at attractive valuations before Wall Street realizes their rebound potential. Read on….

shutterstock.com – StockNews

As widely expected, the Fed has raised interest rates by 75 basis points for the fourth consecutive time today. While the central bank intends to reduce the pace in the future, the market volatility is not expected to ease anytime soon, with recession worries remaining intense.

While institutional fund managers on Wall Street sell their stocks and run for the hills to protect their market gains, bargain hunters may consider this golden opportunity to scoop up quality stocks available at discounted valuations.

Therefore, attractively valued stocks of fundamentally strong companies, Walmart Inc. (WMT) and Gartner, Inc. (IT),could be suitable investments before they are in vogue on Wall Street.

As a world-renowned big box retailer, WMT offers opportunities to shop an assortment of merchandise and services at everyday low prices (EDLP) in retail stores and through e-commerce platforms. The company operates through three segments: Walmart U.S.; Walmart International; and Sam’s Club.

On October 27, 2022, WMT and Netflix (NFLX) announced an in-store expansion of the popular Netflix Hub in more than 2,400 stores. It would offer customers a brand-new streaming gift card, fan-favorite exclusives, and more.

On October 26, WMT announced the completion of the renovations made to the retrofitted regional distribution center in Texas, transforming it into a high-tech automation center. This investment is set to modernize Walmart’s vast supply chain network.

Also, on October 26, WMT and ANGI HomeServices Inc. (ANGI) announced the launch of a new product integration where customers who purchase nearly any Christmas lighting from Walmart can easily add installation by a pro on Angi. Since this bundling would provide additional value to customers, it is expected to impact the topline for both companies positively.

For the second quarter of the fiscal year 2023 ended July 2022, WMT’s total revenues increased 8.4% year-over-year to $152.86 billion. The company’s consolidated net income attributable to WMT increased 20.4% from the prior-year period to $5.15 billion, up 23.7% year-over-year. WMT’s total assets stood at $247.20 billion as of July 31, 2022, compared to $238.55 billion a year ago.

In terms of forward EV/Sales, WMT is currently trading at 0.75x, 57.3% lower than the industry average of 1.75x. Also, its forward Price/Sales multiple of 0.65 compares to the industry average of 1.24.

WMT’s revenue and EPS for the fiscal year ending January 2024 are expected to increase 3.1% and 12.8% year-over-year to $613.68 billion and $6.60, respectively. The company has an impressive earnings surprise history since it surpassed consensus EPS estimates in three of the trailing four quarters.

The stock has gained 8.7% over the past month to close the last trading session at $141.69.

WMT’s POWR Ratings reflect solid prospects. The stock has an overall rating of A, equating to a Strong Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

WMT has grade B for Growth, Stability, Sentiment, and Quality. It is ranked #5 of 38 stocks within the A-rated Grocery/Big Box Retailers industry

Click here to see the additional POWR Ratings of WMT for Value and Momentum.

IT operates as a global research and advisory company. The company operates through three segments: Research; Conferences; and Consulting. It also provides solutions for various IT-related priorities, including IT cost optimization, digital transformation, and IT sourcing optimization.

For the third quarter of the fiscal year 2022 ended September 30, IT’s revenues increased 15.2% year-over-year to $1.33 billion. During the same period, the company’s adjusted EBITDA increased 8.9% year-over-year to $332 million, while the adjusted net income increased 12.2% year-over-year to $193 million. The company’s adjusted EPS came in at $2.41, up 18.7% year-over-year.

In terms of forward P/E, IT is currently trading at 33.07x, 11.6% lower than its 5-year average of 37.40x. The stock’s forward EV/EBITDA multiple of 21.29 is 1.6% below its 5-year average of 21.64. Also, its forward Price/Sales multiple of 4.44 compares with its 5-year average of 3.59.