Most investors have had a rough time in the turbulent 2022 stock market (SPY). Now more than ever they need a reliable way to identify winning stocks regardless of the current market conditions. The key to success is to take the guess work out of investing by having the computers do the heavy lifting for you. First, by narrowing down to the healthiest fundamental stocks using the POWR Ratings system. Next, applying leading edge technical analysis to find the timeliest of those stocks ready to break higher now. That’s what I discuss in more detail in the article below. Read on for more….

shutterstock.com – StockNews

So many traders and investors are always looking to get rich quick without any effort. Most never find it. They simply shuttle from one guaranteed get rich quick scheme to the next in the eternal quest for gold.

Ultimately, they always end up with fool’s gold…

Let me be the first to burst the bubble and tell you that the ‘Fountain of Youth’ doesn’t exist. You can’t lose weight without diet and exercise. Making money requires hard work.

Luckily, however, there are ways to have someone else do most of the heavy lifting for you. Two of the best ways I found are the StockNews POWR Ratings and Market Club’s Trade Triangles.

Using these two together pairs the fundamental strength of the POWR Ratings with the technical prowess of the Trade Triangles leading to serious outperformance.

Then I add in my 30 plus years of trading experience to uncover highly rated quality stocks that are on the brink of a breakout.

Combining all these into one trading program results in the POWR Breakouts Portfolio I manage.

A brief description of each of the components is shown below. I use each of these in my daily trading decisions for the POWR Breakouts Portfolio.

The Fundamentals – StockNews POWR Ratings

StockNews created the proprietary POWR Ratings model to put the odds of investing success firmly in your favor.

This is truly one of the most complete stock ratings systems available to investors today. In fact, we analyze 118 different factors for every stock, each of them contributing a little to the stock’s likelihood of outperformance.

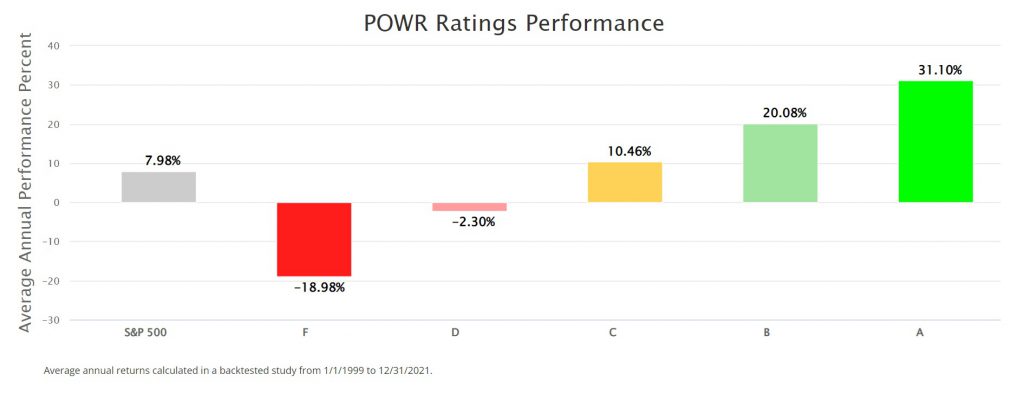

The combination of all these factors is what leads to the +31.10% annualized return for the “A” rated stocks, outperforming the S&P 500 by almost 4X since 1999.

Don’t worry…. you won’t need to analyze all 118 factors for each stock. We have simplified the process by narrowing it all down to an overall POWR Rating that clearly identifies whether the stock is likely to outperform (A & B rated).

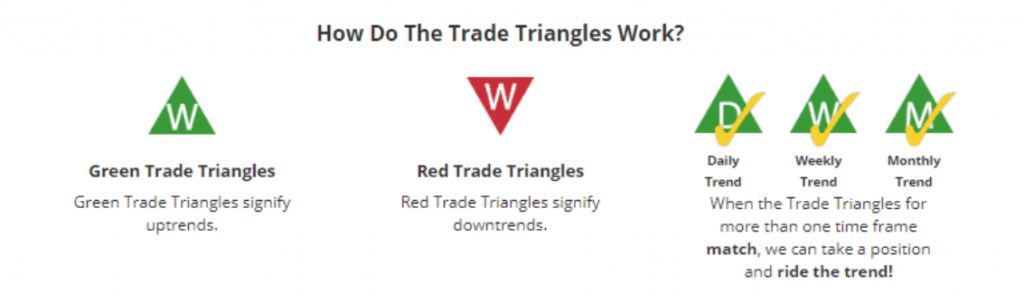

The Technicals – Market Club’s Trade Triangles

Know exactly when to get in and out of the market!

This complex analysis hides behind easy-to-use, easy-to-understand signals – giving you the answers to make confident investment decisions.

Instead of finding just one trend, they confirm trends for multiple time periods to put the mathematical odds in your favor that you will be on the winning side of that swing.

These signals are not intended to catch tops and bottoms. Instead, the signals help members find the majority of a swing trend.

Green Triangles suggest positive trends Red Triangles suggest negative trends

Monthly Triangles determine trend and possible entry points. Weekly Triangles determine timing exits, entries, and re-entries.

Interesting to note that both services (POWR Ratings and Trade Triangles) don’t claim to have a foolproof formula. Far from it. They do a lot of hard work to generate the results.

Instead of a magic bullet, they both state that they look to put the odds in your favor.

At the end of the day, trading is about probability, not certainty. There will be some losses, but the winners should more than outweigh the losers.

Trading is difficult and requires time, hard work, and discipline. There is no easy way to make money. The key is to have the computers do the heavy lifting.

For realistic traders and investors looking to realize above market type returns, using the combined efforts of the fundamental foundation of the POWR Ratings with the technical acumen of the Trade Triangles can help boost your odds.

Factor in the management by an industry veteran who isn’t afraid to take small losses and let winners run, and the probability of long-term success jumps even higher.

What To Do Next?

Discover my 7 hand picked stocks ready to burst higher even in the midst of the turbulent 2022 stock market. Plus 2 more picks are coming this Monday morning.

All you need to do is start a 30 day trial to POWR Breakouts to start enjoying more winning trades in the days and weeks ahead.

SPY shares fell $0.84 (-0.21%) in after-hours trading Friday. Year-to-date, SPY has declined -13.34%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

Approaching the final week of November CSL Ltd ADR (OTCMKTS: CSLLY) received some good news as the United States Food and Drug Administration approved CSL Behring’s new gene therapy drug, HEMEGENIX (etranacogene dezaparvovec-drib) for treating hemophilia B. The news helped continue the stock’s upward momentum, a trajectory that has been mostly consistent for at least the last four years.

MarketBeat.com – MarketBeat

Based in Australia, CSL Behring (AXS: CSL) is a segment of CSL Ltd, which trades under the ticker symbol OTCMKTS: CSLLY in the US market. Their other segments include CSL Plasma, CSL Seqirus, and CSL Vifor; all of which address various aspects of biotechnology and health services.

CSLLY stock’s current value is sitting in a good place: breaking the $100-theshold and resting just below the all-time high ($117.74 USD). Combined with a decent forward dividend yield of 1.11% and projected earnings growth of more than 21%, there could easily be more to come from this company (and its interconnected segments).

November 2022 Was Good to CSL Behring

This late November development is just the latest advance in what has been a busy month for CSL Behring. For example, earlier in the month the company announced its collaboration (and licensing agreement) with Arcturus Therapeutics Holdings, Inc (NASDAQ: ARCT). This partnership would develop and improve capabilities for large-scale clinical supply delivery; in particular enabling CSL to deliver mRNA vaccines to market more efficiently and effectively. These mRNA vacccines would eventually help treat common diseases like the flu and Covid-19.

The positive coverage of both the Arcturus collaboration and the HEMGENIX approval helped raise the price of CSL stock during November. Then, on November 23, CSL Limited share price broke through $300 (AUD) for the third time in all of 2022, closing out the month at $300.11 AUD. That is up 6.92% from the month prior. It has since settled back down a little, just south of that threshold.

The FDA approval comes amidst successful results in the ongoing HOPE-B trial, which happens to be the largest hemophilia-B gene therapy trial to date. So far, results show marked improvement over various study criteria that definitely qualify HEMGENIX as a more attractive treatment option. Effectively, the study found that roughly 94% of patients treated with HEMGENIX discontinued use of their traditional prophylactics.

The price for this new drug is $3.5 million USD per dose, making it the most expensive drug in history. Of course, HEMGENIX is not alone in the upper ranges of drug cost. Take Novartis (NYSE: NVS), for example; their infant spinal muscular atrophy drug Zolgensma sold for $2.1 million USD a dose, upon its approval in 2019. And Bluebird Bio, Inc’s (NASDAQ: BLUE) beta thalassemia (blood disorder) treatment Zynteglo was listed at $2.8 million USD only a few months ago.

Of course, this news about HEMGENIX is typically the sort of thing that motivates investors. First of all, an independent nonprofit research organization, the Institute for Clinical and Economic Review (ICER), has determined that a fair price for HEMGENIX should be around $2.95 million USD. They determine this cost-effectiveness analysis by weighing the drug’s health benefits against offset costs. This gives the drug quite a premium, and that means more profit.

In addition, a treatment upgrade means the product will be more attractive to patients, even at a higher price point. Reducing much of the obstacles presented by other treatments can also make it more accessible to patients with particular sensitivities.

Stable Growth Could Make CSLLY Investment Worthy

All this in mind, CSLLY could be a moderate BUY, at least for now. While it is still stabilizing from the recent news, analysts expect at least 10% business growth in the future. And with a 52-week high of $312.92 AUD, CSL could be on its way to a record high in no time. CSLLY currently pays an annual dividend of $1.08 per share and has a dividend yield of around 1.1%, which greatly exceeds the 0.1% industry average. This industry category includes biotechnology, pharmaceuticals, and life sciences.

On the other hand, CSL has a Price-to-Earnings ratio (P/E) of 42.98, which is nearly double that of the industry average. This implies that the stock may not grow as quickly as analysts hope. Also, its 10.2 Price-to-Sale ratio (P/S) exceeds the industry average of 4.4. This could mean CSL is probably spending more than it would like to be.

Boeing (BA) – Get Free Report shares lurched higher Friday following a report that suggested United Airlines (UAL) – Get Free Report is close to making a deal for dozens of the planemaker’s trouble 787 Dreamliner.

The Wall Street Journal reported that United could confirm the purchase as early as this month, noting the multi-billion dollar deal would mark a major win for Boeing over its European rival Airbus just as it resumes deliveries of the flagship aircraft following a host of regulatory and production issues.

The Federal Aviation Administration gave Boeing the go-ahead in August to resume 787 Deliveries after halting them in May of 2021 over concerns linked to safety inspections.

Boeing booked orders for 10 of its 787-9 Dreamliner variant aircraft in October, the planemaker said last month, with overall bookings for all of its aircraft pegged at 122. October deliveries fell to 35 aircraft from the 51 reported in September.

Boeing shares were marked 3.3% higher immediately following news of the potential deal and changing hands at $181.65 each, a move that would extend the stock’s six month gain to around 29.3%.

Boeing posted an adjusted loss of $6.18 per share over the three months ending in October, a wider-than-expected tally that included a $2.8-billion charged linked to its Pentagon defense contracts.

Free cash flow, however, came in firmly ahead of Street forecasts at $2.9 billion, with the group holding to its full year forecast of positive free cash flow powered by stronger commercial deliveries.

FORT WORTH, Texas, December 2, 2022 (Newswire.com)

– Equify Financial continues to add to its equipment leasing and finance business by hiring National Sales Manager Greg Clemens to lead the Small-Ticket dealer and Vendor program sales team at Equify Financial, LLC.

Dan Krajewski, Executive Vice President of Equify Financial, states, “I’m very excited and grateful to add Greg Clemens to the team. His broad-based experience in building sales teams and dealer relationships will add significant value to Equify’s overall value proposition.”

Greg brings with him more than 30 years of successful experience in commercial vehicle and equipment financing alongside cumulative knowledge within sales/sales management, operations, syndication, and collections.

Greg Clemens added, “Equify’s strong customer and employee-driven culture attracted me to join the company. I’m looking forward to many years of success as we continue to build on our solid base.”

About Equify Financial, LLC

Equify Financial is a privately-owned, independent specialty finance company based in Fort Worth, Texas, serving the United States. Founded in 2011 on the principles of meeting our customers where they are and helping them get to where they want to go, Equify works with customers at any stage in their business. We tailor each service for our clients to build a strong relationship and future.

With over 180 years of combined experience in the equipment finance industry, we help our customers find the best financial path forward.

First American Financial (NYSE:FAF – Get Rating) and Argo Group International (NASDAQ:ARGO – Get Rating) are both finance companies, but which is the superior business? We will contrast the two businesses based on the strength of their risk, dividends, profitability, earnings, analyst recommendations, valuation and institutional ownership.

Analyst Ratings

This is a breakdown of current ratings and recommmendations for First American Financial and Argo Group International, as provided by MarketBeat.

Sell Ratings

Hold Ratings

Buy Ratings

Strong Buy Ratings

Rating Score

First American Financial

0

1

4

0

2.80

Argo Group International

0

0

0

0

N/A

First American Financial presently has a consensus price target of $58.88, suggesting a potential upside of 8.88%. Given First American Financial’s higher possible upside, equities analysts plainly believe First American Financial is more favorable than Argo Group International.

Valuation & Earnings

This table compares First American Financial and Argo Group International’s revenue, earnings per share (EPS) and valuation.

Gross Revenue

Price/Sales Ratio

Net Income

Earnings Per Share

Price/Earnings Ratio

First American Financial

$9.22 billion

0.61

$1.24 billion

$4.24

12.75

Argo Group International

$2.13 billion

0.44

$6.70 million

($5.53)

-4.87

First American Financial has higher revenue and earnings than Argo Group International. Argo Group International is trading at a lower price-to-earnings ratio than First American Financial, indicating that it is currently the more affordable of the two stocks.

Insider & Institutional Ownership

87.2% of First American Financial shares are owned by institutional investors. Comparatively, 90.5% of Argo Group International shares are owned by institutional investors. 3.2% of First American Financial shares are owned by insiders. Comparatively, 1.0% of Argo Group International shares are owned by insiders. Strong institutional ownership is an indication that hedge funds, large money managers and endowments believe a stock is poised for long-term growth.

Dividends

First American Financial pays an annual dividend of $2.08 per share and has a dividend yield of 3.8%. Argo Group International pays an annual dividend of $1.24 per share and has a dividend yield of 4.6%. First American Financial pays out 49.1% of its earnings in the form of a dividend. Argo Group International pays out -22.4% of its earnings in the form of a dividend. Both companies have healthy payout ratios and should be able to cover their dividend payments with earnings for the next several years. First American Financial has raised its dividend for 11 consecutive years. Argo Group International is clearly the better dividend stock, given its higher yield and lower payout ratio.

Volatility & Risk

First American Financial has a beta of 1.22, meaning that its share price is 22% more volatile than the S&P 500. Comparatively, Argo Group International has a beta of 0.97, meaning that its share price is 3% less volatile than the S&P 500.

Profitability

This table compares First American Financial and Argo Group International’s net margins, return on equity and return on assets.

Net Margins

Return on Equity

Return on Assets

First American Financial

5.66%

14.89%

4.67%

Argo Group International

-9.58%

2.59%

0.36%

Summary

First American Financial beats Argo Group International on 13 of the 16 factors compared between the two stocks.

First American Financial Corporation, through its subsidiaries, provides financial services. It operates through Title Insurance and Services, and Specialty Insurance segments. The Title Insurance and Services segment issues title insurance policies on residential and commercial property, as well as offers related products and services. This segment also provides closing and/or escrow services; products, services, and solutions to mitigate risk or otherwise facilitate real estate transactions; and appraisals and other valuation-related products and services, lien release and document custodial services, warehouse lending services, default-related products and services, mortgage subservicing, and related products and services, as well as banking, trust, and wealth management services. In addition, it accommodates tax-deferred exchanges of real estate; and maintains, manages, and provides access to title plant data and records. This segment offers its products through a network of direct operations and agents in 49 states and in the District of Columbia, as well as in Canada, the United Kingdom, Australia, South Korea, and internationally. The Specialty Insurance segment provides property and casualty insurance comprising coverage to residential homeowners and renters for liability losses and typical hazards, such as fire, theft, vandalism, and other types of property damage. It also offers residential service contracts that cover residential systems, such as heating and air conditioning systems, and appliances against failures that occur as the result of normal usage during the coverage period. First American Financial Corporation was founded in 1889 and is headquartered in Santa Ana, California.

Argo Group International Holdings, Ltd. underwrites specialty insurance and reinsurance products in the property and casualty markets. The company operates in two segments, U.S. Operations and International Operations. It offers primary and excess specialty casualty, general liability, commercial multi-peril, and workers compensation, as well as product, environmental, and auto liability insurance products; management liability, transaction liability, and errors and omissions liability insurance; primary and excess property, inland marine, and auto physical damage insurance; and surety, animal mortality, and ocean marine insurance products. The company also provides directors and officers liability, errors and omissions liability, and employment practices liability insurance; international casualty and motor treaties insurance; professional indemnity and medical malpractice insurance; direct and facultative excess insurance, North American and international binders, and residential collateral protection for lending institutions; and personal accident, aviation, cargo, yachts, and onshore and offshore marine insurance products. It markets its products through wholesale and retail agents, managing general agents, brokers, and third-party intermediaries. The company was founded in 1948 and is headquartered in Pembroke, Bermuda.

Receive News & Ratings for First American Financial Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for First American Financial and related companies with MarketBeat.com’s FREE daily email newsletter.

Put simply, dividends are the primary method by which a publicly traded company returns profits to shareholders.

MarketBeat.com – MarketBeat

Are you ready to understand “What is a good dividend yield?” in simple terms? You may also want to simplify your knowledge of what a dividend is and why you might want to buy one.

In this article, we go into deep detail on what makes a good dividend yield, how to calculate dividend yield, what “high” and “low” dividend yield is and what it means. Let’s dive in.

What is Dividend Yield?

The dividend yield refers to the amount of money a stock pays when you own it. Dividends are money a company pays to investors, usually from earnings (but not always). They are a foundational reason to own stocks and one of the reasons why the stock market exists. Investments pay you to own them, either through capital gains or profits. Dividends show how a company in today’s stock market pays profits to shareholders.

What is a good dividend yield for a portfolio? Naturally, it’s a tougher question to answer.

What is a Good Dividend Yield?

What is a good dividend yield? It’s a loaded question.

What is good for one company may not be good for another and neither may be good for your portfolio. A good yield is one that a company can sustain as they pay it. A regularly paid dividend is the foundation of a buy-and-hold mentality and something most companies hope for and strive to achieve.

For easy reference, a good yield should be high relative to the broad market S&P 500 and the company’s peers. Ironically, you don’t even have to own stock for more than a day to get the dividend. To find out how, you need to know about the ex-date versus the day of record.

How is Dividend Yield Calculated?

The dividend yield is an easy calculation. You determine yield by dividing the dividend payout amount by the stock price. There are two ways to calculate yield: You can use the dividend payments over the trailing twelve-month (TTM) period and you can also use the expected dividend payments over the coming twelve-month period.

Why is Dividend Yield Useful?

The dividend yield is useful because it is one of only two reasons to own a stock — growth and dividends:

Growth: The company is growing and the stock will be worth more in the future.

Dividends: The company shares its profits in the form of dividends. Dividends are also useful as a means of generating income, leveraging your portfolio by dividend reinvestment and they can help offset inflation decay.

What is a good annual dividend yield? One that makes you smile when you think about it. One way to find those is to use the best dividend stocks tool.

When is a Dividend Yield too Low?

When is a dividend yield too low? You have to answer that question for yourself.

Some of the reasons why it might be too low may be due to your portfolio strategy, the yield relative to peers, the yield relative to the S&P 500 and the risk relative to owning bonds. If the goal of the portfolio is low risk and you want to achieve income with no need for capital gains, your threshold may be lower than if the portfolio was more risk tolerant and if you were looking for growth.

At face value, no dividend yield is too high because higher is better as long as it is sustainable. In reality, dividends have to be sustainable in order to be attractive to investors. Unfortunately, high yields are not always sustainable.

A dividend is too high when the company cannot sustain the payment. If there is risk of a dividend cut or suspension, that could weigh on the share price and worse, it could cause the loss of capital if the cut or suspension comes to pass.

What is good dividend yield? In this case, it’s a dividend you can rely on.

What Causes a High Dividend Yield?

There are many reasons that could affect the yield dividend stocks, including the payout amount and the price action. Let’s take a look at a few reasons more in depth:

A stock’s dividend yield is a function of its payment. Assuming the stock’s price remains static, the higher the payment, the higher the yield. The problem (or opportunity) for investors and traders, depending on how you look at it, is that a stock’s price is rarely static.

A stock’s dividend yield is also a function of its price action. Assuming the dividend distribution amount remains static, which so often is the case, an upward movement in the stock price will reduce yield. The inverse of this is true if the stock’s price moves lower. In that case, the yield would move higher and open up a potentially high-yield opportunity for investors.

A stock’s dividend yield is also a function of data. Sometimes the data used to determine the yield that is displayed is based on past results and not relevant to the future. One example is an MLP, REIT or shipping stock that pays its monthly payment based on income. In some cases, traditional corporations are governed by managed distribution plans that dictate how much, how often and when a dividend payment can get paid out. For example, the company Cal-Maine Foods (NASDAQ: CALM) cannot make a distribution for any quarter with negative earnings and the company cannot make a distribution until those lost earnings are made up.

News can have a big impact on the yield. For example, news displayed on websites and in stock searches may send a stock price into the trash bin and spark a massive spike in yield. The trouble with this type of “high yield” is that the news may have already included a dividend cut or suspension or may lead to one in the future.

Evaluating High Dividends for Risk

High dividends are attractive to investors because more is better, right? In the case of dividends, high payouts can be a red flag or, in some cases, an indication of trouble that has already happened. Check out a list of things to review to know whether a stock’s high yield is worth buying or not.

Compare the Yield with Peers

Dividend-paying stocks in the same sector tend to pay out similar yields relative to their values. The first thing to check when evaluating a high yield is to see if it is abnormally high for the group. A higher-than-average yield is one thing — it could signal an opportunity. However, a significantly higher yield is reason enough to dig deeper into the details.

You get what you pay for. What you don’t want to pay for is a distribution cut or suspension that will leave share prices in the dust.

Check Out Dividend Statistics

Most stock websites will publish a list of commonly followed dividend statistics that you can use to weed out risky high-yield stocks. Among these metrics is the payout ratio, the compound annual growth rate (CAGR) and the years of consecutive increase.

The payout ratio tells you how much of a company’s earnings are paid out in dividends. In this case, lower is better and higher is worse. The higher the payout ratio, the less room in the cash flow for dividend increases or paying for other things like growth.

The next statistic is the CAGR, which tells you the pace of distribution increase which can be more important than yield. The higher the CAGR, the better, because it means the yield on investment continues to grow and should grow at a similar pace in the future.

The final statistic is the number of years of increases. This figure can tell you a lot because a history of sustained dividend increases can be a powerful reason to buy and hold a stock. The top dividend stocks have a decades-long track record of dividend increases.

Check the Balance Sheet

It doesn’t take an accountant to see red flags on a balance sheet. The easy numbers to look for include cash and equivalents (known as liquidity) and the company’s debts, both short and long term. If the company has a healthy cash balance and little to no debt, the cash flow is unimpeded by debt payments and free for use.

If not, the company may have a hard time paying out dividends or sustaining its record of consecutive annual increases. You can check the leverage ratio, a measure of how much debt the company carries relative to its assets. In this case, low is good. A leverage ratio under three is very good; under 10 is okay depending on the reason why the debt exists.

Learn What Others Say About the Stock

Finally, what do others say about the stock? Check the analyst’s ratings and the trend in analyst sentiment. If the analysts are getting warmer and this matches the fundamental outlook, the high yield dividend stock is likely a good buy. If the analyst’s sentiment cools, you may want to avoid it. After that, check the headlines and find out whether the company struggles in any way or faces hurdles that may impact its results.

A Good Dividend Yield is Where You Find it

So, what’s a good dividend yield? Put simply, it’s one the company can sustain and which fits the needs of the portfolio.

You’ll treasure a good dividend yield, but good is relative. A good yield for a tech stock may be a horrible yield for a consumer staple stock — not all types of companies can sustain a “high yield.” To find a good yield, make sure the company can pay it and compare it to others in the sector. If it looks attractive relative to its peers, then it is a good yield.

FAQs

Still have some questions about what makes a good dividend yield? There’s no one single answer to rule them all. However, we’ll dive into some frequently asked questions to help you understand which dividend yields are good and which ones to avoid.

Is a 6% dividend yield good?

A 6% dividend yield is good. That is more than three times what the average S&P 500 company pays and well above the threshold to be considered a “high yield.”

What is a too-high dividend yield?

A too-high dividend yield refers to one that isn’t sustainable. A 10% yield coming from a highly leveraged growth stock isn’t the same as if it were paid by a REIT. To get an understanding of a too-high dividend yield, compare yields within sectors and check out the earnings, free cash flow and balance sheet to see if the company has the money.

What is a good average dividend yield?

A good average dividend yield depends on the sector and stock. Each sector tends to trade at a different valuation and those vary over time. To find “average” dividend yields, compare yields within a sector and with the broad market S&P 500.

Ford said Thursday that it would invest $180 million to increase production of EV power units by 70% at a plant in the U.K. It’s part of the company’s push to bring more EVs to market and transition its products away from internal combustion engines.

Ford’s move is part of the company’s European electrification plan, which is focused on zero-emission cars by 2030, followed by all vehicles five years later. The power units manufactured at the plant, in Halewood, England, will be installed in 70% of Ford EVs sold in Europe by 2026.

The plant currently makes transmissions for internal combustion vehicles but is transitioning to EV parts manufacturing. The power unit is made there replaces conventional engines and transmissions.

Slashing AI Spending

That’s a clear sign that the auto industry is changing at a rapid pace. In October, Ford said it had slashed capital spending on its artificial intelligence-powered Level 4 driver assistance systems.

In its third-quarter earnings release, the company noted that “large-scale profitable commercialization of Level 4 advanced driver assistance systems will be further out than originally anticipated.

However, it added that “Development and customer enthusiasm for benefits of L2+ and L3 ADAS warrant dialing up the company’s near-term aspirations and commitment in those areas.”

The Level 2 and Level 3 driver assist technologies typically include features such as rear-end accident avoidance and lane-centering. Cars currently on the market, even those a few years old, now utilize these technologies.

In contrast, Level 4 technologies deliver something closer to a fully self-driving experience. The AI in this case calculates when a crash may be about to occur, and corrects accordingly. It also allows hands-free driving.

Although Ford said its partner in the L4 systems, Argo AI, which also had investment from Volkswagen (OTCMKTS: VWAGY), “had been unable to attract new investors.” Ford took an impairment charge in the quarter related to Argo AI’s closure and said it would hire some of Argo AI’s engineers.

In the third-quarter earnings conference call, Ford chief financial John Lawson emphasized that the company is very bullish on the potential for driver-assisted technologies, despite not seeing “a profitable, scalable business in the L4, L5 space for at least five years. We also see that to get there, it’s going to take billions of dollars.”

Ford is deploying existing capital and human resources toward the L2+ and our L3 systems. “We believe that addressable market expands our entire product portfolio from our retail customers to our commercial customers,” Lawson said.

Flat Sales Expected

Ford is slated to release its November sales figures on Friday. Industry analyst J.D. Power-LMC Automotive forecast industry-wide sales to be flat for the month, as higher vehicle prices and higher interest rates mute demand.

Ford’s earnings and revenue track records have been erratic. Earnings growth declined in four of the past eight quarters, but there have also been quarters where increases looked good, due to easy comparisons over sluggish sales in 2020, due to pandemic restrictions.

For the full year, Wall Street sees Ford earning $1.98 per share, an increase of 25% over 2021. That’s seen declining by 11 next year, to $1.76 per share.

Ford Motor is a part of the Entrepreneur Index, which tracks some of the largest publicly traded companies founded and run by entrepreneurs.

House Democrats chose caucus chair Hakeem Jeffries of New York to succeed Nancy Pelosi as leader of the Democrats in the chamber next year, a historic move that will make him the first Black person to lead one of the two major parties in either chamber of Congress. What do you think?

“Isn’t 52 a little young to be leading the Democrats?”

James Clark, Unemployed

“He probably had to kill twice as many progressive bills as his white colleagues to get to where he is today.”

Vivian Kirk, I.D. Designer

“Hopefully this paves the way for future corporate attorneys to seek leadership positions.”

China-based electric vehicle maker NIO (NYSE: NIO)powered more than 19% higher Wednesday. Shares were trading at $12.51 with an hour left in the session.

MarketBeat.com – MarketBeat

NIO, along with other Chinese EV manufacturers, rose in tandem with XPeng (NYSE: XPEV), which reported a third-quarter loss of $0.36, meeting views. Revenue $959.2 million came in below analysts’ expectations.

As always, investors look to the future, and there’s now optimism about these companies’ ability to increase production and introduce new models. XPeng’s forecast for deliveries in the current quarter was better than expected.

In addition, the Chinese government may be softening its stance on Covid lockdowns amid protests. That could bode well for increased factory production.

A government official said this week that the nation has “been studying and adjusting our pandemic containment measures to protect the people’s interest to the largest extent and limit the impact on people as much as possible.”

Although markets rose Wednesday primarily on news that the U.S. Federal Reserve may soon begin slowing interest rate hikes, the China-specific news was likely a factor in the uptick in stocks hailing from that nation.

These pieces of potentially good news occurred as the broader market surged in the first day of upside trade since November 23.

Revenue Growth Slowing

NIO, which went public in 2018, is not yet profitable. The company’s three-year revenue growth rate is a very healthy 103%, but that strong number masks a problem: The pace of growth has been declining sharply.

In late 2020 and in the first three quarters of 2021, NIO was growing revenue at triple-digit rates. In the quarter that ended in March 2021, revenue grew by an almost astounding 529%.

However, growth rates in the past four quarters ranged from 53% to 20% most recently. That’s still very good, but well below the torrid levels in 2020 and 2021.

NIO is not the only China-based EV maker that’s seen revenue growth slow dramatically. XPengposted triple-digit sales increases in 2020 and throughout 2021. In the past four quarters, growth decelerated from 208% to 8% most recently.

NIO acknowledged the slowdowns in its most recent earnings report. The loss in the most recent quarter was $0.30 per share, the largest in the past two years, and equal to the loss for the entire year of 2021.

For the full year, analysts expect NIO to lose $0.89 per share. For next year, Wall Street sees a loss of $0.56 per share.

There have clearly been problems brewing for several quarters, ahead of the latest round of Covid lockdowns in China. But while the rest of the world has found ways to essentially live with Covid, China retains more strict policies that have potential to slow production at factories on a moment’s notice.

That’s where concerns about NIO’s future value become relevant.

Increased Spending On R&D, Sales

In its most recent report, NIO said it had boosted research and development spending and was looking to add new products to the pipeline. The company also said selling, general and administrative spending was up, mostly due to building out the sales team.

Both of those increased line items point to expansion plans, which could be impacted if fewer cars are rolling off assembly lines.

BYD has been profitable in recent years, with the exception of 2020. However, unlike startups created to produce EVs, BYD is an established firm that makes buses, trucks, bicycles, forklifts, batteries, and other cars.

NIO, on the other hand, has some glamor appeal as a company formed to produce EVs and related products, such as battery-charging stations. NIO has maintained its position as a luxury brand, which may help its revenue as the more mainstream brands cut prices.

Despite a year-to-date decline of 66.86%, NIO still qualifies as a large cap, with a market cap north of $20 billion. If the company can show that it has the potential to increase deliveries at a pace that satisfies investors, the November rally may have some staying power.

Opinions expressed by Entrepreneur contributors are their own.

When you’re establishing your startup, it can be a challenge to choose the right bank and the right business checking account, particularly if you have limited business experience. You need a bank account that not only meets your current needs but will grow as your requirements evolve with your expanding business.

You might be wondering if you need a business checking account. While a personal checking account will perhaps meet your needs for your basic day-to-day business activities, you need to consider whether you need a business loan in the future or want to hold profits in a savings account.

Your new checking account can be the start of your banking relationship, so you can start to establish goodwill and trust. However, while the bank is important, the characteristics of the checking account are also vital. So, here we’ll explore how to choose a business checking account for your startup.

Think about what you need from your bank

The first thing you need to consider is what you need from your bank. Are you just looking for a checking account or do you also need a small business loan? There are lots of banks that not only offer a variety of business checking accounts but also have great business product lines such as business loans and lines of credit, business credit cards and tax counseling.

While you may be looking for a checking account to handle your checks and manage client payments, you may need a line of credit or other products in the immediate future. So, take some time to think about your immediate and potential future needs to see which banks can meet your requirements.

Once you have a short list of things you need from your bank, you can start comparing the offerings from different banks both in your area and nationally. If you are considering a couple of banks, you can speak to their customer support team and obtain product information or even schedule a meeting to discuss your requirements.

However, if your startup will only require basic account services, you could consider online banks. These tend to offer various products with minimal fees. The downside to this is that you don’t have face-to-face interaction, and depositing cash can be tricky.

Considerations for choosing a business checking account

1. Location restrictions

Even if you’re not looking at an online bank, some traditional banks put location restrictions on certain accounts. If you’re considering a business checking account that has very low fees, it is worth checking if it is online only.

Depending on your operation, you may need to speak to a bank representative in person, pay in cash or send certified checks. In these scenarios, having a business checking account that does not have branch access could be a problem.

2. Digital tools

Most modern startups benefit from digital tools such as mobile deposits, and digital bill payments. So, it is well worth assessing what digital tools are offered with the checking account.

Many banks and financial institutions have an app that allows you to manage your account on your mobile device. Make sure that you check the reviews for the accompanying app to see if there are any potential issues.

3. Fees

As with a personal checking account, the fees for your business checking account can quickly add up. For most startups and small businesses, every cent counts, so it is crucial to check the fee structure for your new checking account before you sign up. If your bank offers fee waivers for monthly maintenance charges, be sure to check the criteria to ensure that you can meet the minimum balance needed to waive it.

4. Relationship perks

Many banks offer some great perks, such as fee waivers and preferential rates if you link multiple accounts. So, it is worth checking if the bank holding your personal checking account offers relationship perks if you open a business account.

You may find that your existing bank will provide some excellent account options and since you already know and enjoy the bank, you can feel confident with your new business checking account. On the other hand, if there are no benefits to having the same bank for your personal and business accounts, don’t feel obliged to stick with them.

When you have a startup, you’ll have plenty of administration tasks that will keep you busy every day. So, it can be very handy if you can provide your trusted team members with a company debit card.

This means that you won’t need to micromanage essential purchases or deal with annoying reimbursement requests.

6. Business savings accounts

Another important consideration is whether the business checking account has an accompanying or compatible savings account. While some business checking accounts are interest-bearing, you may still have startup capital that would be better in a savings account.

A compatible savings account would allow you to keep your funds on hand for when they are needed. Some banks even facilitate automatic transfers. This will transfer funds from your savings account if the checking account balance reaches a certain threshold. This is a great feature, as you don’t need to worry about going overdrawn or having payments refused, yet you can still be earning a higher rate of interest.

7. Additional resources

Finally, it is worth checking whether your new business checking account provides access to additional resources. Many banks appreciate the challenges of operating a startup and offer help and guidance. This could be something as simple as a learning center that offers live webinars, informative guides, or access to a business banking manager.

8. Business vs. personal checking account

There are several good reasons to keep a separate checking account for your business if you own one. According to the SBA, business banking offers some personal liability protection by keeping your personal and corporate funds apart. Check writing and debit cards are features that both personal and business checking accounts can provide.

A company checking account, however, could provide benefits that a personal checking account does not. While some personal checking accounts can be opened for as little as $1, depending on the bank or credit union, a business checking account may cost $500, $1,000, or more to open. Combining your personal and commercial operations in one checking account, if you plan to do both, can make bookkeeping difficult and tax season a nightmare.

Bottom line

Once you have begun your startup, you are likely to be excited to get working on your core business, but the right checking account can be an ally or a hindrance. The right checking account will provide you with the tools and services your startup needs.

In our previous article, we made the case for Finance to take stewardship of enterprise data. The benefits are compelling. Data is the raw material of Finance. Quality assured enterprise datasets managed under the proven stewardship of Finance can be used to generate insights to inform and energise business decision making.

So how does Finance build and operate such a capability? Here we define four pillars that a Finance data strategy should consider, and define the steps needed to realise the benefits across the bank.

Trends and innovations in banking

In Switzerland and throughout Europe, banks are going through the most innovative times anyone can remember. Increasingly, consumers are embracing the convenience of digital channels. Digital innovation generates opportunity − customers leave an electronic trace of all their interactions with their bank. The immense volumes of available data are a never-before-seen resource with which to build fresh insights into customers’ financial behaviour and tailor new personalised products and offerings.

The economic winds are changing. After a decade of benign inflation and low or negative interest rates both are now rising. Customers are responding by adapting their financial behaviour, and for bank Finance teams forecasting has become harder. Experience and instinct continue to play their part, but for smart banks the data trails of their customers reveal tell-tale signs of where they are heading and inform the bank’s response.

The traditional skills of Finance in data stewardship mean that it is in the best position to capture the benefits for their organisation of the advances in data analytics. And the opportunity extends beyond existing business lines into new markets in data. We see five main areas of opportunity:

Figure 1: Finance data leveraging opportunities

Realising this opportunity requires a structured approach. A Finance data strategy is the roadmap to becoming an insightful bank.

The four pillars of Finance data strategy

We believe there are four key pillars for the design of a successful Finance data strategy:

The scope of products and services for which insights can add most value

The stakeholders operating along the data value chain

The data architecture

The enabling technologies

Figure 2: Four pillars of a Finance data strategy

Don’t drive blind. Decide from the outset the decision-support insights that Finance needs to generate. Collaborate across the business to identify where fresh data-driven insights could yield the highest return.

The list of insights can be extensive. For example:

Is there an untapped revenue stream in our product offering?

Can we learn more about our clients?

Can we monetise our data by collaborating with fintechs?

What insights can further inform our AML capabilities?

We have identified multiple use cases which, taken together, could form the scope of a Finance data strategy:

Figure 3: Finance data strategy use cases

Determining which insights are needed shapes the design of the remaining three pillars of the strategy.

Three key factors are needed to support data stakeholders in delivering the outcomes of a winning Finance data strategy:

a well-defined process framework along the data value chain

data-centric governance

a strong data culture

Well-defined process framework

Acquire, integrate, analyse. Each step in this process requires a distinct skillset. The acquire-and-integrate phase depends on the attention to detail which is a hallmark of financial stewardship and underpins accuracy. Analysis requires a mindset of questioning and curiosity to hunt for fresh insights and apply a storytelling skill to convey them to decision-makers. Technology has a role − interactive, connected planning dashboards are an example of how Finance is able to rapidly adjust its projections of the bank’s performance. However the real step forward is in the new skill of the Finance team to bring the numbers to life for the business and to provide insights for taking action, for client reach-out or more precise planning.

Data-centric governance

People along the entire data value chain should be given clear responsibilities. From identification to publication, actors must understand the processes within data management, communicate their importance to executing teams, and close gaps that could lead to inaccurate or incomplete data.

Strong data culture

In an insightful Finance team, data management skills are at a premium. Prowess in data management will be a hallmark of the successful finance teams of tomorrow. A sustained focus on data management as a key Finance capability is needed to nurture these skills.

Appropriate data architecture is a foundation for capturing and integrating data from multiple sources. The challenge often lies in the sheer scale of the architecture required to manage enterprise-wide volumes of information. Whilst different design options are available, rigorous analysis is needed to avoid potentially costly mistakes in selecting the wrong architecture, tool decommissioning, process redefinition and governance redesign.

We identify three distinct architectural models which would enable banks to consolidate enterprise-wide data into usable resources and to scale their analytical capability.

Figure 4: Finance data architecture models

Technology is a key enabler of insightful Finance, and the pace of innovation accelerates, the focus must shift from finding any technology to finding the right technology. Banks which invest resources into finding the right tools to analyse, identify and deliver insights will build a competitive edge over their peers.

A list of all the available technology would be too long to include here. We can narrow the scope to key areas relevant to data analytics which fit in with the mission of insightful Finance. Powerful tools can be found along the entire data value chain, with advanced innovation particularly in the areas of predictive planning and AI-enabled data visualisation.

Figure 5: Examples of Finance data technology

The four pillars of a winning Finance data strategy are interconnected parts of the same strategy. A decision in one area will impact the others, and a comprehensive approach is needed to maximise the chances of success.

We can help you assess your data needs and define a solution that best fits your vision for Finance. We can assist you in implementing a data strategy which transforms your Finance function into an insights-driven partner for the business.

In a one-day Data Strategy Lab, we can help you define the insights that you would like to build, and in a four-week Data Strategy Assessment, we can assess your current state and define your transformation path to an insightful finance function.

The goal of an insight-generating Finance capability is nearer than you might think.

Markus Zorn, Partner, Consulting

Markus leads the Swiss Finance & Performance practice of Deloitte Switzerland. He has been advising CFOs for over 20 years on their most challenging Finance transformation and digitalization endeavours.

Tobias has an extensive experience focusing on large and complex Finance transformation programs leveraging ERP, mainly SAP. Tobias leads the banking offering of the Swiss Finance & Performance team

Daniele is a passionate consultant with extensive track record for development and execution of Finance transformation programs in Europe. Daniele leads the Insightful Finance offering within the Swiss Finance & Performance team

Lorenzo is a consultant in the Swiss Finance & Performance team with a strong focus on the banking sector. He helps our clients understand the true power of data in creating business value.

Zoom Video (NASDAQ: ZM)has gone from an obscure but easy-to-use video communications platform to becoming a verb synonymous with video conferencing and remote engagement driven by the COVID-19 pandemic. Zoom Video was one of the major benefactors of the pandemic that helped usher in the “new normal” of hybrid work in a post-pandemic world. While other video calling tools were available, Zoom’s incredibly easy interface brought video conferencing to the mainstream masses. The Company’s growth has since peaked as normalization continues to set in. The question is where the baseline is for Zoom and what catalysts can help it speed growth back up. The Company compete with many teleconferencing and business collaboration software companies like Adobe (NASDAQ: ADBE), Microsoft Teams (NASDAQ: MSFT), Salesforce (NASDAQ: CRM), Google Workspace (NASDAQ: GOOG), Cisco Webex Meetings (NASDAQ: CSCO) and even Verizon (NYSE: VZ) with its BlueJeans Meetings app. The Company wants to become a unified communication platform with the addition of email and calendar functions. It has also partnered with AMC Entertainment (NYSE: AMC) to turn some locations into Zoom meeting rooms

MarketBeat.com – MarketBeat

Growth Continues to Slow

On Nov. 21, 2022, Zoom Video released its third-quarter fiscal 2023 results for the quarter ending October 2022. The Company reported earnings-per-share (EPS) profit of $1.07 beating consensus analyst estimates for a profit of $0.84 by $0.23. Revenues rose 4.9% year-over-year (YoY) to $1.1 billion, matching consensus analyst estimates for $1.1 billion. $100,000 annual run rate (ARR) customers rose 31% to 3,286. Enterprise customers rose 14% YoY to 209,300. Enterprise revenue rose 20% YoY to $614 million. Online average monthly churn was 3.1% down 60 basis points from same period last year. Zoom Video ended the quarter with $5.2 billion in cash and cash equivalents and marketable securities. Zoom Video CEO Eric Yuan commented, “Our customers are increasingly looking to Zoom to help them enable flexible work environments and empower authentic connections and collaboration. Proactively addressing these needs with Zoom’s expanding platform continues to be our focus in this dynamic environment.”

Lump of Coal Guidance

Zoom Video issued downside guidance for fiscal Q4 2023 with EPS between $0.75 to $0.78 versus $0.82 consensus analyst estimates. Fiscal Q4 2023 revenues are expected to come in between $1.095 billion and $1.105 billion versus $1.12 billion. Incidentally, constant currency revenues are expected between $1.12 billion to $1.13 billion. Total fiscal 2023 revenues are expected between $4.370 billion to $4.380 billion and $4.42 billion to $4.452 billion in constant currency. Non-GAAP EPS for full-year fiscal 2023 is expected between $3.91 to $3.94 with 304 million weight average shares outstanding.

Analysts Cut Price Targets

Piper Sandler lefts its Neutral rating unchanged but cut its target price to $77 from $84 per share. Analyst James Fish was underwhelmed by its Q4 lump of coal outlook and concerned for the declining total customer base as the rate of new business continues to decelerate. Baird kept its Outperform rating but slashed the price target for Zoom shares to $95 from $100 per share. Analyst William Power felt the Q3 2022 results were solid, but its outlook remained mixed due to currency headwinds are weaker deferred revenues. Zoom remains a top holding at 8.31% in the Ark Innovation ETF (NYSEARCA: ARKK) operated by famed fund manager Cathie Wood.

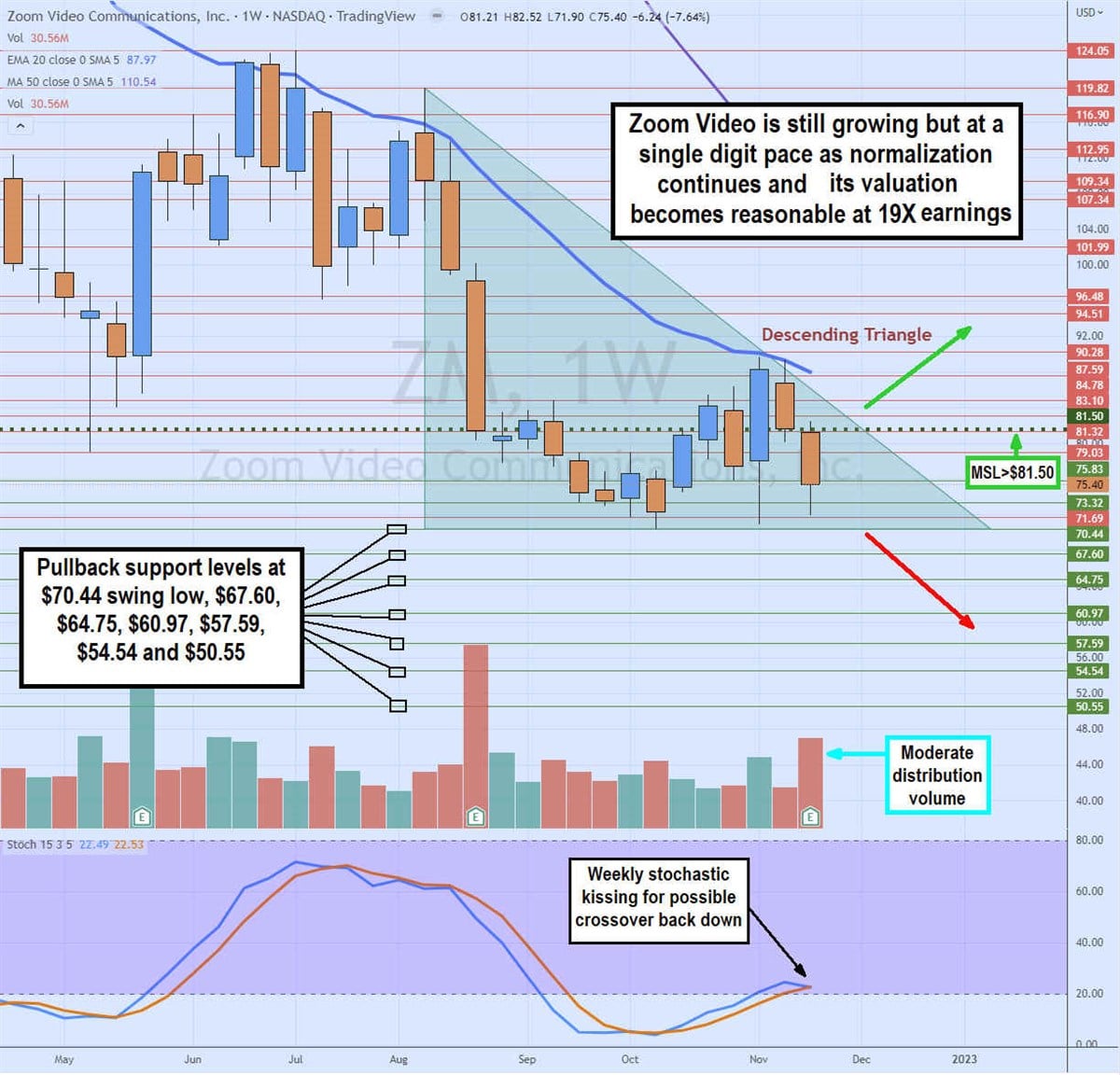

Weekly Descending Triangle Risk

The weekly candlestick chart illustrates the potential for a descending triangle breakdown as it makes lower highs against a flat low at $70.44. Shares continue to reject off the falling weekly 20-period exponential moving average (EMA) now at $87.97. The Q3 2022 earnings reaction further accelerated the selling towards the $70.44 low area before a coil attempt failed to trigger the weekly market structure low (MSL) buy trigger above $81.50. Distribution volume rose upon the earnings release but was moderate compared to nearly double the volume on its Q2 2022 earnings sell-off. The weekly stochastic bounce through the 20-band stalled on the selling pressure setting it up for a potential crossover back down as shares near the flat lower trendline of the weekly triangle. As the channel between the falling upper trendline and flat trendline gets tighter towards the apex, shares will either breakout by triggering the weekly MSL or finally breakdown through the swing lows. This should resolve by the end of the year. Pullback support levels to watch sit at the $70.44 swing low, $67.60, $64.75, $60.97, %57.59, $54.54, and the $50.55.

The U.S. apparel market is forecast to contract 2% this year. Not bad considering the myriad of challenges facing clothing manufacturers and retailers. Ongoing supply chain disruption, higher materials costs and inventory build-ups have weighed on the industry in 2022.

MarketBeat.com – MarketBeat

Thankfully, apparel investors may not lose their shirts for much longer.

Fewer logistics issues and moderating inflation are part of a more comfortable outlook for clothing companies. According to Statista, apparel industry volume will increase 9.7% next year as product availability and demand improve. Over the next five years, apparel market sales are forecast to grow 3.6% annually.

The bullish outlook and recent quarterly earnings releases have several apparel stocks trending higher in recent weeks. And since many were hemmed in half from their 2021 peaks, the road to recovery remains a long one. Here are a few of the names worth trying on for sizable gains.

Why is The Gap Stock Going Up?

The Gap, Inc. (NYSE: GPS) has almost doubled from its September 2022 low and has finished higher in 10 of the last 11 trading days. The momentum kicked into high gear after the retailer posted better-than-expected Q3 sales and profits. The double beat was driven by demand for more formal attire as Americans returned to the office and in-person social engagements. Dresses, woven tops and pants are flying off the shelves again.

Banana Republic is again a strength for the company after notching 8% sales growth last quarter. The relaunch of work clothing drew more people to the stores. Old Navy and fitness-apparel arm Athleta also delivered growth while the flagship Gap business had flat sales due to soft kids clothing demand.

The biggest reason for investors to get excited about The Gap is e-commerce. Digital sales were up 55% from pre-pandemic levels and 5% over last year. At a time when online shopping is slowing, The Gap’s e-commerce growth shows that consumers are finding value in the products. Digital sales now account for almost 40% of overall revenue.

Despite management anticipating a ho-hum holiday shopping season, Gap shares gapped up on the report. This tepid outlook has undoubtedly contributed to Wall Street’s skepticism around the stock’s surge — but makes the retailer an intriguing contrarian play heading into 2023.

What is Abercrombie & Fitch’s Growth Strategy?

Abercrombie & Fitch Co. (NYSE: ANF) gapped up in heavy volume last week on the heels of an impressive top and bottom line beat. Although both sales and earnings declined year-over-year, encouraging demand trends and ample inventory for holiday shoppers have investors lining up for a comeback.

Six months removed from a major plunge, the casual clothing company is re-establishing credibility due to strength in its core Abercrombie brand and progress with its ‘2025 Always Forward’ initiative. While omnichannel growth is a popular buzz phrase, the real reasons to invest are prospects for improved profitability.

By the end of fiscal 2025, management is targeting an 8% operating margin compared to the 2% to 3% expected this year. Longer term, it sees operating margin expansion beyond 10% as cost savings kick in and global recognition of Abercrombie and Hollister broadens.

Abercrombie & Fitch has been one of the best clothing retailers when it comes to building out its online presence. Higher margin digital sales account for roughly half of all sales and are poised to be an even bigger part of the business going forward. Digital marketing and social selling hold the key to attracting Millennial and Gen Z customers.

Burlington Stores Had a Bad Q3…Why Did the Stock Go Up?

Burlington Stores, Inc. (NYSE: BURL) is on the move despite a disappointing Q3 performance that included a 17% decline in same-store sales. The off-price retailer has yet to capitalize on the macro environment but believes it will attract bargain shoppers in 2023. Burlington touts prices on coats and other apparel that are as much as 60% below the competition.

The upbeat outlook combined with positive peer earnings reports has pushed the stock back to the $200 level for the first time in six months. However, given the weak sales and margin pressures, the stock is now a ‘show me’ story with little room for error.

To build off the fortunate momentum, Burlington Stores must demonstrate that its ‘2.0 Off-Price strategy’ is working. The key component here is communicating a better message to consumers about the value the stores offer. Keeping the merchandise assortment fresh and inventory management will also be important but at the end of the day, effective marketing campaigns and word of mouth must drive stronger customer traffic.

Unlike The Gap and Abercrombie & Fitch, Wall Street loves Burlington Stores. Twelve of thirteen analysts called the stock a buy after the Q3 update. Proof of execution is needed here but this discount clothing retailer could be a good fit for the current economy.

GAP is a part of the Entrepreneur Index, which tracks some of the largest publicly traded companies founded and run by entrepreneurs.

Opinions expressed by Entrepreneur contributors are their own.

None of us is immune to what’s currently happening in the economy, forcing many business owners and executives to consider ways to cut costs. I recently asked my leadership team to take a good, hard look at their expenses to determine what can and should be cut and gauge the effects those specific savings would have on the business.

Finding ways to save money in your business is not always as obvious as you think and can come from a few places that are not typically looked at. Here I outline ten money-saving ideas all business owners should consider.

Take a look at how technology can play a role in improving efficiencies. How can you utilize technology to minimize time, effort and money spent where it doesn’t need to be? Whether it’s analytical data that helps you be quicker to market or process improvements that make your supply chain run more efficiently — plus having good processes around where you spend money.

For larger projects, obtain three quotes from separate vendors before placing an order. Make sure you negotiate the best possible cost on a meaningful purchase. Be assured that what you are buying is right for your business.

I think that the mentality of being scrappy is essential. What I mean by scrappy is being pugnacious and determined not to be wasteful. Think local and establish relationships with local businesses. In our industry, for example, we buy, manufacture and print labels for our customers and brands. Fortunately, our label vendor is literally down the street, so we’re saving money on transit costs. Utilizing your local network ensures you’re getting the best price, not just in direct costs but also in time and effort.

3. Make sure you have the right employees for the right roles

This boils down to “right people, right seats.” When you look at the world today and how the labor pool has, for various reasons, contracted, having the right person in a role who’s passionately engaged is vital. They get it, they want it and they can do it. Over the long haul, that spells increased efficiency and savings. Running a business where you don’t have the right people in the right seats makes everything cumbersome and challenging.

In most businesses, marketing tends to be something companies can overspend on. That’s why it’s essential to have the right marketing person in the right seat. This person has relationships and expertise and knows when a consultant can do something and when something should be handled in-house.

Employee retention helps, too. Teams have chemistry, they understand how people operate and they play off each other’s strengths and weaknesses. When you’re constantly replacing people on the team, that’s all learning that must be done over again instead of doing the job.

4. Expand on social media and community engagement

I’ve seen brands effectively connect the organization to the consumer through social media. One thing to understand is that your content should be organic and user-generated, not scripted or overly polished. Recording content on your own versus paying an influencer or agency thousands of dollars has a cost-benefit. But there’s an even bigger reason why you want to choose this path.

Today’s consumers see right through content that’s heavily produced and edited. Instead, they follow, work with, purchase from and remain loyal to easily relatable brands that don’t take themselves too seriously and have no problem being transparent about every aspect of their business.

Sit with your marketing and finance teams to determine what percentage of the annual budget needs to be allocated toward purchasing equipment and boosting posts. Use data and analytics to determine what posts help you meet your goals (e.g., engagements, views, conversions, etc.) and place your bets accordingly.

5. Refine, then automate

When you’re talking about logistics and shipping and the operational piece of the business, the more automated you get your orders in and out the door, the more efficient you’ll be. This hopefully means you’ll have more bandwidth to spend time doing other things, right?

I also believe in minimizing clicks and pain points within your sales process. Have information readily available, so employees don’t have to click five different screens to get to what they need to get through. You want to free up the time to sell and reduce the time spent on administrative tasks. For example, you could automate invoicing or utilize a service that consolidates your accounts payable, so you don’t have to pay somebody for that.

If you can operate all aspects of your business under one roof, that’s ideal. For example, if you complete the shipping or manufacturing of your products in-house, you don’t want to be in three different buildings — you want to be in one building so you can organize things, get the best use of your staff, maximum use of the space and highest possible output.

You don’t want to sit on tons of office space because that is bleeding money. Whatever you can do to get out of those situations as soon as possible, the better off you’ll be. Looking into co-working spaces might be worthwhile in certain cases, too.

7. Look at insurance and cash flow

You need to have somebody who has the experience, knows the right questions to ask, understands your business needs, and is bound to save you money regarding insurance. For employee health benefits, make sure people have a choice and have an option that makes sense for both the business and the employee. Over and above making sure you’re not under-insured or over-insured, it’s more important that you’re insured correctly.

Avoid short-term loans, cash advances and borrowing on high interest. If you’re buying things on credit, pay it off. And don’t get smashed with interest. Make sure you’re only buying what you need. All of those things factor into good cash flow.

One of the things my CEO mentor always used to say is that there always needs to be a certain number in the bank. So, if we even got close to that number, he would send out fire alarms. It was all hands on deck evaluating things, cutting things we didn’t need and making sure that the company’s cash position was one we felt comfortable with. This way, we could sleep at night and know we were in good shape. That’s just one of those old-school mentalities that have always stuck with me.

8. Staff up or hire out?

If you don’t have the expertise, you need to be ultra-selective in ensuring you’re not just being penny-wise and pound-foolish. I always say you don’t want to step over the dollar bills to pick up pennies. If you can save money on wages and other things, that’s great, but you must set KPIs.

You have to understand (and communicate) what your expectations are from these independent contractors; otherwise, you’re just going to be spending good money without seeing any benefit from it. And that’s throwing money out the window. So, there’s a little bit of a catch-22 there. You’ll save money on the fringe but must have measurables to ensure they’re performing.

If you don’t have to travel, don’t. But when you do need to travel, travel effectively. Make sure that there’s a good travel policy about meals, hotels, flights, etc. These expenses can go through the roof if you don’t have some control. Use Zoom, Teams and other messaging applications when possible, but also be cost-effective in managing travel.

So, you’re a sales and marketing operation, and you’re struggling. Then you, all of a sudden, decide you’re going to start doing packaging, but you have no clue how to do it. This is probably a recipe for failure because you’re not focusing on the areas you’re good at, and you’re taking time and effort away to try and learn something you don’t need to. But the nice thing about the way the world is that somebody out there can do it; you need to find the right partner.

Being careful with money doesn’t mean being cheap — quite the opposite. It means honoring the value of the money entrusted to your company by customers for goods and services they care about.

Hardware and infrastructure solutions provider Dell Technologies (NASDAQ: DELL) is a diversified technology company comprised of two main segments, Infrastructure, and Client Solutions. The segment that manufactures and sells PCs, monitors, accessories and gaming hardware is the Client Solutions segment. The acquisition of storage solutions provider EMC over a decade ago helped shape the storage and networking solutions segment known as the Infrastructure Solutions Group. While the Client Solutions Group (CSG) saw revenues fall due to normalization from the pandemic driven 2021 comps, its Infrastructure Solutions Group (ISG) continues to set record revenues. The Company also Alienware gaming systems, SecureWorks cybersecurity, and cloud computing management software company Virtustream. Dell also divested its 81% stake in virtualization company VMWare (NASDAQ: VMW). The Company has continued to gain commercial PC market share in 35 of the past 39 quarters and has been able to reduce quarterly operating expenses by more than $300 million since Q1 2022. Despite the strong U.S. dollar having a 500-basis point impact, Dell handily beat its Q3 2022 EPS estimates and like rival HP Inc. (NYSE: HPQ) may be indicating that the bottom of the normalization process for PC sales may have been made.

MarketBeat.com – MarketBeat

Pandemic Bolsters APEX As-a-Service Solutions Model

The pandemic was also a boon to Dell’s infrastructure business as companies pulled back on heavy capex spending for infrastructure due to the unpredictability of the COVID pandemic and the budgetary constraints from lockdowns. This caused more companies to consider as-a-service subscription plans (IE: Software-as-a-Service, Storage-as-a-Service, Hardware-as-a-Service, etc.) that allowed for lower costs in the face of uncertainty while gaining more flexibility, value and capacity. For Dell and other as-a-service (aaS) providers, it meant steady, predictable, and consistent cash flows. Dell’s APEX allowed for companies to procure hardware, storage, software, security and cloud in a single offering with complete end-to-end maintenance and management making it scalable and affordable with no overage charges under its hybrid subscription and consumption billing plans. This was especially accommodating to companies employing a growing remote workforce and suited for the “new normal” of hybrid work and the elastic office.

Strong Beat But Still…

On Nov. 21, 2022, Dell released its third-quarter fiscal 2022 results for the quarter ending October 2022. The Company reported earnings-per-share (EPS) of $2.30 excluding non-recurring items versus consensus analyst estimates for a profit of $1.61, a $0.69 per share beat. Revenues fell (-6.4%) year-over-year (YoY) to $24.72 billion, beating consensus analyst estimates for $24.61 billion. The comparisons to 2021 were tough since it was a banner year for the Client Services segment as consumer PC and hardware sales hit record levels driven by the pandemic. Dell COO Jeff Clarke commented, “Stepping back, the near-term market remains challenged and uncertain. On one hand, we are seeing some customers delay IT purchases. Other customers continue to move ahead with Dell given the criticality of technology to their long-term competitiveness and a growing need to drive near-term productivity through IT. The world continues to digitally transform, data continues to grow exponentially, and customers continue to look to technology to drive their business forward, no matter the economic climate.” On Nov. 16, 2022, Dell also announced a $1 billion settlement in a class action lawsuit regarding its return as a public company. It’s insurers may pay part of the settlement but still needs final approval from a Delaware Chancery Court judge.

DELL Weekly Cup and Handle Pattern

The weekly candlestick charts illustrate the triangle breakdown occurring in August 2022 setting the stage for the collapse under the $45 level taking shares down to the swing low at $32.90. Shares managed to stage a rally upon forming a rounded bottom leading to the weekly market structure low (MSL) breakout through $36.98 trigger driven by the weekly stochastic bounce through the 20-band. Shares broke higher through the weekly 20-period exponential moving average (EMA) resistance which has now become support at $41.22 as shares head towards the weekly 50-period MA resistance at $47.01. The rally is causing shares to form a potential weekly cup and handle formation upon peaking at the lip area between $45.40 and $46.73, which was also the earlier triangle apex and breakdown level. A shallow pullback towards low $40s and a breakout through the weekly 50-period MA would trigger the pattern. Since the weekly stochastic is only at the 50-band, there is potential for a higher move. Pullback support levels sit at the $41.18, $39.90, $38.32, $36.98 weekly MSL trigger, $34.80, and the $32.90 weekly swing low.

The two-pronged axis of employee-sponsored pension plans and individual retirement accounts is the stage where, for most Americans, the majority of retirement planning happens. Within that framework, Roth IRAs are renowned for their unparalleled ability to secure tax-free growth.

Due – Due

But there is a catch – contribution limits and restrictions on high-income individuals severely curtail these benefits. The rollover is one of the best-kept Roth IRA secrets – it allows investors to both sidestep Roth IRA income limitations and contribution limits, as well as rake in the benefits of tax-free growth.

A move like this might seem highly technical and complex — after all, with the benefits that we’ve mentioned, it would only make sense. But thankfully, it isn’t so — rollovers are simple to execute and require very little time and effort.

However, there are a fair number of points that should be kept in mind when deciding on a move like this. We’ll cover all of those considerations today – so that you can have a clear overview of the situation before deciding if a rollover is something that would interest you.

When Converting a 401(k) to a Roth IRA Makes Sense

First things first – by far, the most common scenario in which rolling over a 401(k) into a Roth IRA is considered involves an employment transition. While there are numerous choices available when leaving your job (we’ll get into those shortly), this particular method offers unique benefits – so let’s cover the situations when such a move makes sense.

For starters, for investors who expect to be in a higher tax bracket after retiring – whether due to RMDs or other sources of income, footing the tax bill now and enjoying tax-free growth and withdrawals later has some obvious benefits which are quite difficult to find elsewhere. One should also keep in mind the possibility that taxes as a whole will increase in the future – something that seems quite likely when looking at future budget proposals.

Speaking of RMDs or required minimum distributions – the mandatory payments that start at age 72 associated with traditional IRAs – well, Roth IRAs don’t have them. This helps keep down taxable income in retirement and allows for a much greater degree of control.