Luxury athletic clothing retailer Lululemon Athletica Inc. (NASDAQ: LULU) was trading 12% lower mid-session Friday, after gapping down at the open. The move followed the company’s warning of higher-than-anticipated inventory levels.

MarketBeat.com – MarketBeat

Is Lululemon a harbinger of problems ahead for clothing retailers, in an era of inflation and remaining supply-chain issues?

At first glance, Lululemon’s quarterly numbers look pretty good.

After the bell Thursday, the Vancouver, British Columbia-based company said third-quarter revenue came in at $1.86 billion, a 28% year-over-year increase. Earnings were $2, up 23% over the year-earlier quarter.

Those results beat both top and bottom-line views. MarketBeat earnings data show that Lululemon has a solid history of beating, or at least meeting, analysts’ expectations.

But the holiday cheer was quickly soured by the company’s mention of higher inventory levels. That sent shares skidding in after-hours trading and plummeting in heavy volume at the open Friday.

While same-store sales, a common retail metric, increased in the quarter, they fell below Wall Street’s expectations.

Holding Above 200-Day Line

Even with Friday’s price drop, which sliced through the 50-day moving average, shares remained above the longer-term 200-day line. If that holds, it’s a signal that institutional investors still have conviction about the stock and aren’t bailing out en masse.

Certainly, the news was mixed. The company increased its revenue and earnings guidance. It now sees sales in a range of $7.944 billion to $7.994 billion for the full year, up from an earlier forecast of a $7.865 billion to $7.940 billion range.

It expects net income between $9.87 to $9.97 per share, better than a previous forecast of $9.82 to $9.90 per share.

Even so, investors weren’t ready to look at the bright side Friday. There’s a case to be made that Thursday’s report gave some investors a reason to take profits. Shares are up 4.01% in the past month and 8.31% in the past three months.

The stock has been trending near its 10-day moving average since rallying to a structure high of $370.46 on November 11. That represented the most recent technical buy point, but Friday’s action put the stock about 12% below that point.

Widespread Inventory Glut

The increase in inventories worried investors.

It’s not a problem that’s unique to Lululemon. For much of this year, retailers across various categories have reported higher inventories due to rapidly changing consumer buying habits throughout the various phases of the pandemic. Despite offering deep discounts, some items aren’t moving off the shelves as fast as companies had anticipated, based on earlier buying patterns.

Supply-chain and freight delays complicated the problem. High-demand items took a long time to arrive, and once they were available, consumers were no longer interested.

For their part, Lululemon’s management team maintains that ongoing demand will justify high inventory levels, rather than necessitating steep markdowns.

The company has a history of charging full price more than offering discounts. Some analysts appear to have confidence that the company can maintain its pricing power, as evidenced by MarketBeat analyst data for Lululemon, which show that four analysts boosted their price targets after the third-quarter report.

Analysts’ consensus price target for Lululemon is $413.12, a potential upside of 26.30%. That’s up from a price target of $400.74 a month ago.

Although clothing retailers as a group fell on Friday, one day does not make a trend. Holiday-season and fourth-quarter sales will reveal much more about changing buying habits, and the medium-term effects of inventory oversupply.

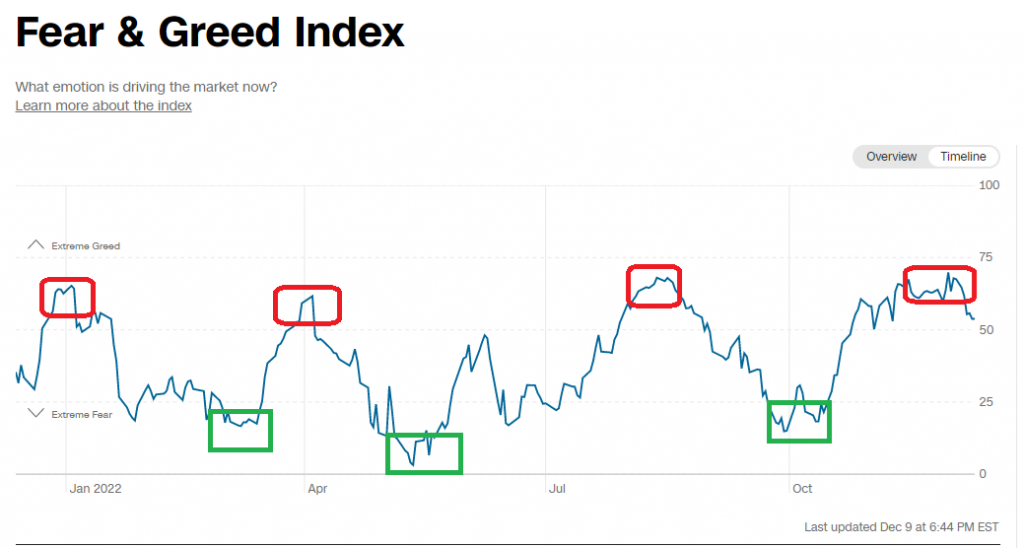

Bolster the Warren Buffet “Fear and Greed” mantra with three more reliable indicators to increase your odds of sucess in trading.

shutterstock.com – StockNews

“Be Fearful When Others Are Greedy And Greedy When Others Are Fearful” is a famous stock market adage of famed investor Warren Buffet. The CNN Fear and Greed Index certainly epitomizes that notion. The chart below shows how greed and fear tend to swing back and forth from one extreme to the other.

Following in the footsteps of Mr. Buffet is never a bad decision, in my opinion. Getting greedy when others are fearful and fearful when others are greedy has worked well in 2022. Adding in a few other tried and true methodologies to that philosophy can make it even more robust. Here are three more ways to increase the odds of success in trading.

Technicals

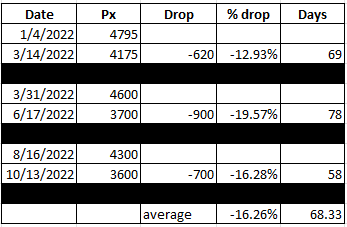

The chart below shows the one-year price action for the S&P 500 (SPX). It is evident that the SPX continues to be in a well-defined downtrend, with a series of lower highs and lower lows. Indeed, the recent strong rally we saw off the lows ended right at the trend line before beginning to reverse course.

How far the current pullback will go is anyone’s best guess. However, if previous history is any guide, then $3400 would be a good guess.

I pulled off the numbers from the prior three times the SPX fell from the downtrend line before bottoming out and heading back up, as seen in the table below.

The average of the three drops so far this year has been just over 16% and took roughly a little over two months. That would equate to a drop that ends up around $3400 in the S&P 500 by about February option expiration on 2/17/2023-if the averages hold.

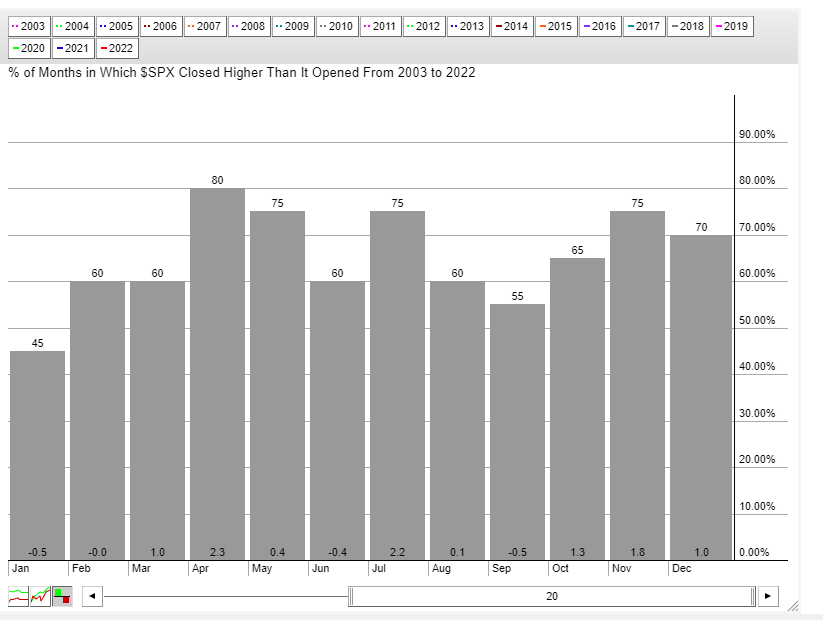

Seasonality

Certainly, many are still waiting for the so-called “Santa Claus Rally” to take stocks higher on a seasonal basis into Christmas. Given the red-hot rally since October, Santa may have already come early for the markets. But seasonality is a two-edged sword. Once Kris Kringle leaves town, stocks tend to suffer.

January has been the worst performing month for stocks over the past two decades. The S&P 500 has shown an average loss of 0.5% in that time frame and has dropped 55% of the time. February has been a laggard as well.

Stocks may have trouble finding their footing until springtime if seasonality is any guide.

The VIX

The VIX is a measure of 30-day implied volatility in the S&P 500 options. It is also referred to as the fear gauge since it tends to rise when stocks drop and fall when stocks rally. I recently wrote an article that showed how you can use the VIX to time the market.

The chart below shows just how pops and drops in the VIX have corresponded almost precisely to similar drops and pops in the S&P 500. Also note how the VIX extremes correspond to the CNN Fear and Greed Index extremes noted at the start of this article.

The latest fall in the VIX from highs at 34 to the recent lows under 20, followed by a subsequent rally to nearly 23, generated another VIX-based sell signal for stocks. Each of the previous moves off the lows in the VIX ended up finally stalling at the 34 area. If history holds, the VIX has much further to head higher-and stocks have much further to fall.

As you can see in the chart, each new VIX-based Buy signal corresponded with a new low in the SPY, which is the S&P 500 ETF.

Everything being equal, stocks may not bottom out and be a buy until they make new lows on the year.

Trading is all about probability, not certainty. Using these three measures discussed in your decision making will help put probabilities-and therefore the odds- in your favor.

POWR Options

What To Do Next?

If you’re looking for the best options trades for today’s market, you should check out our latest presentation How to Trade Options with the POWR Ratings. Here we show you how to consistently find the top options trades, while minimizing risk.

If that appeals to you, and you want to learn more about this powerful new options strategy, then click below to get access to this timely investment presentation now:

SPY shares closed at $393.28 on Friday, down $-2.96 (-0.75%). Year-to-date, SPY has declined -16.24%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

Everyone wants to retire and spend the rest of their lives in comfort without worrying about their finances. That dream is definitely achievable, but, to do that, you must prepare for it as soon as possible. Whether you’re a bachelor or bachelorette, a widow or widower, there’s no better time to start preparing for retirement than now.

Due – Due

Truth be told, being single puts you at a significant advantage in preparing for retirement, as you have complete control of your life and are most likely not responsible for anyone else.

So, if you’re a single looking to get a head start on your retirement savings, keep reading because we’ll discuss how you can secure your retirement finances starting now.

How to prepare for retirement

Before we discuss the various ways to save for your retirement, we’ll first discuss the key steps to prepare for this important transition in life.

Step #1 Assess your current finances.

The first step in every journey is to figure out where you’re starting. The same is true in preparing for retirement; you must start by knowing where you are in terms of finances. To do that, start by assessing your sources of income.

Do you mostly rely on employment?

Do you have any sources of passive income?

Any side hustles?

Then, using that information, compute how much you earn and spend per year. This process will tell you how much money you have and, at the same time, determine how much you can afford to spend based on your financial goals for retirement.

For a more accurate assessment, including a detailed inventory of all your assets (savings, properties, investments, etc.) and liabilities (debt, mortgages, etc.).

You also need to track and clearly assess where your money is going every month. Keeping even small payments like your Spotify subscription or your credit card’s annual fee in check can go a long way in helping you understand your budget. While the latter won’t be the case if you choose a no-fee credit card, there will always be fixed and variable expenses that may add up significantly, potentially jeopardizing your financial goals. Comparing income and expenses is key to knowing how healthy your finances are.

Doing all these assessments help inform you of the appropriate steps you can take next.

You’ll know your current lifestyle is too expensive for your income if you lose money based on the previous assessment. If you’re not losing any money, congratulations, you could skip this step and proceed to the next. However, if you’re the opposite and losing money, maybe, it’s time to downsize here and there and start cutting your expenses.

This could mean anything from moving into a smaller house to cooking your own meals, paying back loans, or reducing unnecessary spending. Whatever you do, the goal is for you to be more profitable annually to build up your assets.

Step #3 Set your target.

Assessing your finances and right-sizing your lifestyle without a financial goal in mind would be useless (it’s not even possible to tell). So, based on your annual income and your right-sized annual expenses, set a realistic financial target you think you’ll need to achieve to live comfortably.

For example, if you currently earn $50k per year and roughly spend $45k annually, your goal should be to earn the same amount annually through passive income. So, ideally, your target could be about $450k in savings, which you can invest in some stocks with 10% APY.

Step #4 Save for emergencies.

Now you have a goal in mind, so you’re itching to start investing and earning those dividends. However, before doing that, you should first prepare your emergency fund.

An emergency fund is money you save in an easily accessible bank account, which you can use in case of a rainy day. Ideally, this fund should at least be 3 to 6 months’ worth of your monthly expenses to ensure that you won’t have to touch your retirement savings at all, no matter what happens.

Doing this step will safeguard you in case (knock on wood) you experience an emergency like losing your job.

Step #5 Invest in assets.

Now that you have your financial goals and an emergency fund, it’s time to invest your surplus in money-producing assets. Keep in mind the word assets. Assets are properties that appreciate, like stocks or real estate. Investing in them prevents your money from stagnating and losing its value because of inflation.

Unfortunately, buying a new car or a new boat is not considered an asset in the traditional use of the word. In some circumstances, these things are even considered liabilities, meaning you lose money just by owning them.

If you want to find recommendations for assets you can invest in, keep reading until the last section of this article, where we’ll discuss how you can secure your retirement finances by choosing the right investments.

Step #6 Estate planning.

The harsh reality of life is that all of us are mere mortals, and our stay in this world is temporary. So, if you pass away, you need to specifically tell your loved ones what you want to do with your assets. Generally, you need an attorney to write your last will. But, the process usually follows these steps:

Prepare a detailed inventory of all your assets. As we mentioned, an attorney and even an accountant can help you out with this.

Assign and review your beneficiaries. Once you have a detailed inventory of your assets, make a list of people you want to inherit your assets. If you want, you can even leave your assets to a charity.

Prepare a list of directives your attorney will implement through a legally binding document. This is just another way of saying, get your attorney to write a legal will.

Step #7 Join a community.

No man or woman is an island, and the same is true for you. So, the last step in preparing for retirement is finding and joining a community you will enjoy. Be sure to be thorough in searching and researching your prospect communities, as they can make or break your retired life.

Remember that whichever community you join, it should be one that will let you live peacefully and full of love and happiness.

Ten Ways to Secure Your Retirement Finances

Now, it’s time for the exciting part. We’ll discuss the different ways you can secure your retirement funds through smart investing.

This list contains different assets you can invest in, which appreciate in value over time through the magic of compound interest. Some of these will even allow you to live off of investment interest.

Having most of these assets will ensure you spend your retirement in the most comfortable way possible—a retirement where you’ll never have to worry about money again.

#1 Social Security

Social security is the safety net that societies put in place to cushion the financial blow of unexpected life events like unemployment, illness, disability, childbirth, or the death of a breadwinner.

Retirement is expensive—analysts believe you’ll need between 70 and 90 percent of your pre-retirement income to live comfortably. Getting a membership and investing in a social security fund as soon as possible benefits you in the long run.

This type of insurance allows you to maintain your standard of living once you start enjoying life after retirement.

#2 IRA

To help you save for retirement, the government offers tax breaks for contributions made to Individual Retirement Accounts or IRAs. IRAs are among the best vehicles for long-term financial planning.

You can establish an IRA with little effort. The majority of the population can open one and make deposits. What’s great is that there is no minimum age requirement—however, you must have taxable income. Opening an IRA is quick and easy at most financial institutions.

The primary advantage of a traditional IRA is the ability to delay paying taxes on earnings and contributions until distributions are due. It’s possible that the more money you put away now (and over the years), the more you’ll have to withdraw when you’re ready to retire.

The choice to handle your finances on your own or with the assistance of a financial advisor is yours. You can also use the automated route and have your investments tracked and regularly rebalanced if you want.

#3 401(k)s

You should already have a 401(k) if you currently work in a company, especially since many companies provide employees with access to 401(k) plans, which allow them to save for retirement while enjoying favorable tax treatment.

When you, as an employee, enroll in a 401(k), you consent to have a set amount of your income automatically deducted and deposited into a savings or investing account. So, it’s usually a set-it-and-forget-it type of deal.

As an added benefit, you’ll also reduce your taxes using this plan since your company deducts it from your paycheck before applying federal taxes.

#4 Long-term care

If you qualify for long-term care (LTC) insurance, it’s something you should definitely consider, especially if you’re single and planning for retirement. LTC pays for all or a significant portion of care received at an assisted living facility or home once you reach a certain age, so you won’t have to worry about being left old, sick, and broke.

#5 Stocks

Stocks are popular assets to invest your money in. You may have already heard about this from people around you or even on the media you consume. Stocks are individual shares that make up a company’s ownership. Thus, buying and owning a stock means owning a single share of the company.

The stock market is an excellent way to diversify your portfolio, grow your wealth, and shield your assets from the effects of inflation and taxes. You’ll likely see solid gains if you’re willing to invest in stocks for the long haul.

#6 Bonds

Bonds are a relatively safe investment because these are usually issued by a government, municipality, or corporation (usually to raise money).

Typically, people invest in bonds because this guarantees a steady flow of cash in the future. A bond’s interest is usually paid semi-annually. It is the type of investment that can help you keep more of your money, thanks to the fact that you earn your original investment back if you patiently wait for the bond to reach maturity.

#7 Dividends

In addition to our earlier discussion of stock investment, where you earn money as a consequence of the stock’s value going up, there are other ways to profit from investing in a company—dividends!

Even when capital gains are difficult for the corporation, investors can still get paid with dividend stocks. So basically, there are two ways to profit from these investments: the steady income from dividend payments and growth in the stock price.

#8 Treasury bills

Like bonds, Treasury Bills (or T-Bills) are among the most secure and risk-free investment options available as the government guarantees them. The country’s treasury issues short-term debt instruments, the T-bills, with maturities ranging from a few days to a year.

Additionally, T-bills have low initial investment requirements, and the interest is not subject to income tax at the state or local level. However, it is still taxed at the federal level. There’s a trade-off, though, since less risk also means less potential yield.

If you want to invest in treasury bills, you can easily buy them from the secondary bond market.

#9 Annuities

Annuities are another investment option that is helpful post-retirement. Retirees commonly purchase annuities as a means of securing their income. They are contracts that guarantee payments at regular intervals for a set length of time or even for the rest of your life.

If you pass away before your benefits kick in, any money you have invested will go to your designated beneficiary, depending on the particular type of annuity you purchased.

#10 Invest in real estate

One of the most important assets one may have is real estate. A safe and secure home is necessary for everyone at all times. Unlike paper assets, real estate can be sold quickly and rarely loses value (unless there’s a bursting bubble or something). Residential housing has the potential to generate the most steady revenue.

Most importantly, the land is an immutable investment that never loses value. As time passes, this will continue to appreciate, so selling it later down the line will almost surely turn a profit.

The bottom line

Planning will get you places — including a secure and happy future free of worries (at least financially). Minor adjustments in your current lifestyle and proper management of your assets and income all add up and paint the circumstance of your future self.

You will thank yourself someday for the mindful decisions you make today, so don’t stall anymore and start saving for your financial future.

Consumers are taking the plunge into solo traveling, despite the cost of traveling surging in recent months due to higher inflation and interest rates.

Due – Due

Traveling alone during retirement is nothing new, and millions of retirees and more mature adults are enjoying the excitement of experiencing a new country or culture by themselves.

Most recent statistics indicate that 16% of people in the United States have taken a vacation by themselves, that’s more than 53 million Americans embarking on a solo adventure. More surprisingly an additional 83 million of them are planning a solo trip in the coming months and years even as the cost burden weighs on their budgets.

Though it tends to be harder, and more expensive to travel alone, many consumers are finding it easier to do so, as it allows them better freedom and flexibility to visit destinations and experiences they’ve always dreamt of.

With droves of Americans taking to the skies again amid the travel rebound, older and more mature adults are also now tapping into the idea of solo travel, even if it requires some meticulous planning.

The most recent data from 2016 suggest that out of the 32 million Americans older than 65 years that live alone, more than 10% of them tend to travel alone or embark on a solo adventure at least once during their retirement.

Going back even further to 2014 we see that travelers aged 45 years and up were highly satisfied with their solo experience, and a majority – 81% – said they were already planning on taking another single-person adventure in the 12 months that followed after the survey was conducted by The American Association of Retired Persons (AARP).

David Stewart, CEO of travel aggregator Guide to Europe tells that, “consumers shouldn’t feel restricted to travel because of their age, we see all sorts of people taking advantage of solo travel these days, regardless of their age and that shows to us as a team how we can make a difference in other people’s lives through the services we provide them.”

Age is indeed just a number, but that number does come with a lot of challenges and risks if you end up booking the wrong holiday or not doing proper research. To make matters easier, here’s a look at some of the mistakes many retirees come face-to-face with when they plan for a solo trip.

Mistakes To Avoid As A Solo Retired Traveler

1. Not knowing your physical limitations

At any given age or period in your life, you have encountered an activity that has pushed you to your limits. Whether you’re a young 20-something, or recently stepped out of the workforce and into retirement – we all have our limits.

As a retiree that looks to embark on a solo trip during your golden years, it’s important to understand what your physical limitations are, and how you can plan a trip that accommodates your needs.

Before you start planning, make sure to visit your doctor to get a professional opinion on the state of your health. You might feel as if you’re in the best shape you’ve ever been, but it’s best to be prepared and know what you can and cannot do while you’re on holiday.

2. Not effectively planning

Traveling comes with a lot of planning, from choosing a destination, booking tickets, deciding on accommodation options, and looking for fun, yet applicable activities to do within your means.

If you ask any travel expert or even someone who often travels alone, they will tell of the benefits that come with planning well ahead, and there’s good reasoning behind it as well.

For starters, last-minute travel deals are also not so readily available, and for someone at your age, you want to make sure you have everything sorted before arriving. Once you know where you want to go, you can consider how you will be getting around, or if the area is safe enough to travel alone as a foreigner.

Additionally, you need to think of things such as clinics and hospitals in case of a medical emergency, or if you need a prescription refilled while abroad. You may need to renew your passport or apply for one if you’re a first-time traveler. This all takes time and requires some upfront money to cover the costs so it’s best to start planning early.

3. Ignoring budget-friendly group options

While you may be thinking of taking a solo trip, often due to financial or personal limitations, you will be required to make some adjustments. Before you completely cancel your trip or postpone it until a later time, do a bit of research if there are any budget-friendly group travel options available in your area.

Group travel packages are often specifically designed and planned around senior citizens, to ensure they can get the most out of their experience and the best bang for their buck. On top of this, depending on where travel groups may go, you will be able to meet similar like-minded people who share the same wanderlust excitement as you do.

Travel agents and several travel aggregators have travel groups that visit some exciting and interesting places, both abroad and back home as well.

4. Skipping the travel insurance

The chances of you ever using your travel insurance are somewhat unlikely, but you can never be too safe, especially when you’re traveling by yourself. Travel insurance is a simple and secure way to protect your belongings, and help cover unforeseen costs such as a canceled flight.

In some more severe instances, travel insurance will also help assist in case of a medical emergency, or if you end up in a hospital in a foreign country. You may also need insurance to help you in case you lose your passport, or you require a repatriation flight back home.

There are a lot of reasons why travel insurance is important, and it’s best to follow up with your health insurance provider, or credit card company about the type of coverage they may already be offering in your current policy, or if you will be required to take out a temporary policy while overseas.

5. Choosing the wrong destination

Once you have some idea of where you want to go, you will need to start researching whether they cater to your needs and meet all your requirements.

Most destinations these days cater to a wide range of travelers from all age groups, and while this has given travelers the chance to freely roam, there’s always that one thing that could potentially become an inconvenience.

If you’re planning to visit a remote destination, consider how you will be getting there, either by plane, train, or boat, and how long it will take you to get there. Once you’re there, how will you be getting around to seeing the sites? Do the locals speak English, and will they understand you if you need assistance?

Make sure to choose a destination that’s closely related to where you’re from, as this will not only help you get around easier but also make the trip more enjoyable.

6. Going all out from the start

Now that you’re retired, you might be looking to squeeze in as much traveling as possible. While this is not completely impossible, it’s easy to overdo yourself on the first trip a bit too much, which can often leave a bad taste in your mouth.

As you start to plan your solo trip, see how you can find a balance between travel and relaxation, without overindulging in the entire experience. Although you want to see as much as possible and visit as many places as possible, make a list of the most important things, and narrow it down to a few options.

Take enough time to make sure you are in the right shape to travel alone, not only for your safety, but also for things such as carrying your luggage, standing in long queues at the airport, or having to walk long distances.

7. Breaking the bank

With travel costs up across the board, from airline tickets to lodging and even car rental, you will need to have a travel budget at hand to make sure you don’t spend all of your savings on a single trip.

Once you know where you want to go, you can set up a budget that includes transportation, accommodation, car rental, and food, among others. Additionally, you will need to budget for activities and excursions as well, such as entry to parks and museums.

Luckily for retirees, there are plenty of senior travel package deals and promotions available year-round. More so, if you have a travel rewards card, you can make use of the senior citizen benefits, or look for deals that are specifically tailored to your age group.

8. Not properly making use of technology

Nowadays it’s possible to book an entire trip in one single click. What’s even more impressive is the fact that you can plan, book, and pay for a holiday using one simple mobile application.

Digital tools and technology have brought the world closer to us, and with it, it’s also made it a lot easier for us to travel more conveniently.

Before you leave, read up about the latest travel apps you can use while abroad, or ask a younger family member to assist you with the app. Additionally, you can play around with the app a bit, to make sure you are comfortable enough to use it without the assistance of others.

Technology has done incredible things for us, and not properly utilizing it will result in costly and inconvenient mistakes.

9. Assuming things are still like they used to be

Often we have a certain level of expectation before we embark on an exotic holiday. And while things may have been a certain way back when you were younger, it’s unlikely that things are still the same today.

There is a lot that can change through the years, and you will be able to notice it within your retirement community as well. When you travel abroad, it’s best to manage your expectations, do a bit of reading, or ask around in your circles if anyone has recently visited the place you want to go.

If you have an idea of what you might encounter, it’s best to consider that through the years things may have changed a bit, regardless of the current state of affairs.

10. Not doing it sooner

A lot of mature adults will often leave traveling until retirement, simply because they will have more time and money to do so once they leave the workforce. More so, single retirees will often not travel solo because they feel restricted by their health, or not having someone to do it with.

Although these may be valid reasons to travel later, rather than sooner, it’s best to start planning and ensure you get to experience as much as you possibly can.

Retirement allows you more freedom and flexibility to travel as frequently as you want, and for as long as you please. This is the best time to enjoy the simpler luxuries of life and make the most of your golden years.

The bottom line

Traveling solo has its perks, but it does come with some considerations at the same time. For retirees who are willing to plunge into solo travel, making sure they are up to date with all the latest insights and trends in terms of traveling will help them plan a memorable vacation.

For solo travelers, it’s best to make sure you have an idea of where you want to go, how much it will cost you, and how you will be exploring the area once you’re there. Additionally, you want to make sure you have accommodation sorted before you leave and that you have communicated with friends and family back home about your travel plans.

If you make time to properly plan, your holiday will be more relaxing, and enjoyable, while you indulge in the simple pleasures life has to offer you at the age of retirement.

40 year investment veteran Steve Reitmeister shares his most complete and up to the minute analysis of what lies ahead in 2023. First a return of the bear market with the S&P 500 (SPY) making news lows. Yet just at the darkest hour the new bull market will emerge ushering in tremendous gains to investors who time it right. Steve shares his trading plan along with top 8 picks to profit on the way to bear market bottom. Next he shares a plan to buy the market bottom with 2 top picks set to rally 100%+. Get the full story below.

shutterstock.com – StockNews

It’s that time of year again for investors.

To put the past behind us in order to focus on the year that lies ahead.

This led me to record a timely presentation and trading plan that you should watch now:

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.43 (-0.11%) in after-hours trading Friday. Year-to-date, SPY has declined -16.24%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The S&P 500 (SPY) has been shedding weight all week long because inflation is looking too “sticky”. What does that mean? And why does it matter? 40 year investment veteran Steve Reitmeister spells it all out in this timely commentary that includes market outlook, trading plan and top picks. Read on below for the full story.

shutterstock.com – StockNews

Inflation and the Fed once again are taking center stage for investors. First, were signs of wages inflation being hotter than expected last Friday. Next comes an unwelcome increase in the Producer Price Index this Friday.

These are signs of “sticky inflation”. The kind that doesn’t fade so easy. The kind the Fed warned us about.

Oddly traders tried to shrug off the early losses this Friday…but came to their senses by selling with gusto into the close.

Let’s ponder why that is the case, along with the broader investment outlook, in this week’s commentary below…

Market Commentary

In my last commentary I discussed the catalysts at play for investors. Both the factors that cause bullish rallies as well as bearish drops.

The nutshell version of the article is to appreciate that the key ingredient for stock prices is the state of inflation and therefore how long the Fed will have to remain hawkish. The longer inflation stays around…the longer the Fed has high rates…the more likely to have recession and lower stock prices.

Most investors talk about the Consumer Price Index (CPI) when discussing inflation. However, the leading indicator of where that will be in the future is the related, Produce Price Index (PPI).

That’s because this report reviews the costs being taken in by companies now, that will show up as higher prices for their products and services down the road. Now you appreciate why the higher than expected reading for PPI Friday morning was not a welcome sign leading S&P 500 (SPY) futures to immediately drop from +0.5% to -0.5%…and then closing at -0.73% on the session.

What should really jump off the page for investors is to appreciate that the +0.3% month over month increase in PPI came at the same time that gasoline prices were down a full 6%. This is exactly what the Fed fears…that inflation is becoming “sticky” in other places.

Meaning more permanent. Meaning higher rates from the Fed on the way. Meaning still a long term battle to fight inflation which increases odds of hard landing (recession). And yes, meaning lower corporate earnings which begets lower stock prices.

Now let’s remember that on Friday 12/5 we learned in the Government Employment report that wage inflation was higher than expected. And wage inflation is about the stickiest category.

The release of that information had stock futures down about -1.5% at the time of the open. Oddly bulls kept bidding up stocks into the finish to a nearly breakeven result.

Over the weekend investors sobered up to the realization that this news was indeed quite bearish. That is why stocks trimmed over 3% in the first 3 sessions of the week.

This action is somewhat similar to the reaction to PPI this Friday morning. Stock futures dropped like a rock on the news. But somehow fought their way back until the final hour when the bears took the wheel.

Perhaps that is because some traders don’t fully appreciate that PPI is the leading indicator for the more widely followed CPI report which comes out Tuesday 12/13. Perhaps they want to roll the dice and see what happens there.

Or perhaps they want to wait for the next Fed rate decision on Wednesday 12/14. Let me remind investors that what happened at the last meeting. They foolishly rallied 2% within minutes of the announcement that future rate hikes would be lower.

However, when Powell took to the podium thirty minutes later, he reminded folks of the long term battle ahead. And the odds of creating a soft landing for the economy had greatly diminished. That speech turned that 2% rally all the way down to a -2.5% finish on session.

Long story short, investors can stay bullish if they want rolling the dice on what is in the 12/13 CPI report or 12/14 Fed announcement. However, when you pull back and look at the entirety of what is going on, which is what I did in my “2023 Stock Market Outlook”, then you will appreciate that odds still point firmly to recession forming early next year with lower lows on the way for stock prices.

What To Do Next?

Watch my brand new presentation: “2023 Stock Market Outlook” covering:

Why 2023 is a “Jekyll & Hyde” year for stocks

5 Warnings Signs the Bear Returns in Early 2023

8 Trades to Profit on the Way Down

Plan to Bottom Fish @ Market Bottom

2 Trades with 100%+ Upside Potential as New Bull Emerges

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.43 (-0.11%) in after-hours trading Friday. Year-to-date, SPY has declined -16.24%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Opinions expressed by Entrepreneur contributors are their own.

Come January 3, a new Congress will convene in Washington, DC, setting the stage for potential tax changes that could impact small and medium-sized businesses. With that in mind, it’s important for businesses to engage in certain tax planning strategies and to take advantage of tax credits that will soon expire or be phased out.

The Employee Retention Credit (ERC) is one such credit. Created in 2020 to provide economic relief during the Covid-19 pandemic, the ERC lets businesses claim thousands of dollars in refundable tax credits to compensate for losses experienced in 2020 and 2021 while they continued to pay employees. Businesses subject to a full or partial shutdown or significant decline in gross receipts can qualify.

Many small and midsize businesses I know are eligible for two quarters or more of credits, which can range as high as $7,000 per quarter per employee in 2020, with higher per-employee limits in 2021. But the time frame for claiming this credit is shrinking. Start planning now.

Businesses have just three years from the time they filed their 2020 and 2021 quarterly tax returns to claim the credit. Even if you received funds from the Paycheck Protection Program (PPP) previously you can qualify for the ERC credit, but you’ll need time to gather all the necessary documentation before filing the required amended return.

Beware of companies advertising huge ERC payouts that are “too good to be true,” as the IRS noted in a special warning. The agency further cautioned that “improperly claiming the ERC could result in taxpayers being required to repay the credit along with penalties and interest.”

Know how to find someone who can help you if a problem arises. I had a client who signed a contract with a firm that promised an ERC credit twice as large as what we projected along with lifetime audit protection, but the firm was cagey about how to handle a prospective audit and did not list addresses and phone numbers. A red flag for sure, and a reminder that taxpayers should never get too greedy.

The importance of tax planning

How many business owners can honestly say their accountants are advising them on tax planning, like the ERC benefit, rather than merely doing their taxes? Is yours building a tax-strategy foundation that generates recurring savings year after year?

Take the initiative and ask your accountant what plans they have in place to generate savings year in and year out, plus what strategies they’re using to accomplish that.

Don’t make the mistake of merely asking your accountant how you can save on taxes just before the year’s end. If you do, you may be advised to buy a vehicle for your business because the cost can be fully written off using a bonus depreciation. This is not an example of a great, forward-thinking tax strategy. And that particular deduction, by the way, will lose 20% of its value in each of the next four years, starting in 2023. It’ll be completely phased out by 2027.

Accountants should have a plethora of strategies to help small and midsize businesses and their owners save on taxes. For example, ask yours about research and development credits, or credits for hiring veterans and disabled individuals and members of other groups that the government has identified as facing employment barriers.

How to avoid an audit

It’s more important than ever to use only legal ways to limit your tax liability. Here’s a list of some dos and don’ts:

Don’t put your family vacation on your company’s books. If there is a business purpose for a partial business/family trip and that purpose constitutes more than 50% of the trip, document it and proportionally deduct your costs. Include notes about the purpose of the travel, your itinerary, the agendas of meetings and conferences, whom you met with, etc. The IRS has heightened record-keeping requirements for travel deductions.

Keep original receipts, not just credit card statements. Taxpayers often assume a credit card statement constitutes a receipt. It does not. Your expense items on a credit card receipt only will likely be denied.

Get in a habit of documenting all relevant expenses while you’re incurring them; and consider assigning an employee for that purpose or use technology. You’ve got to document the business reasons for the deductions claimed because there are heightened documentation requirements for business travel and for meals. You probably won’t remember all these necessary details if the IRS audits you two or three years after an event has taken place. If you fail to document actual expenses, you should deduct IRS-published travel per diems by city.

Don’t pay personal expenses through your company. Write a check to yourself from the company for a legitimate reason like a salary, wages or distribution. Then pay personal bills for your mortgage and electric bill out of your checkbook, not the company’s.

The messages are slowly sinking in. Four clients so far have told me they’ve completely revamped their internal processes to take better records. They’re spending the time to do this now because they understand it could be riskier in the future.

Nobody knows what tax changes, if any, are in store, but there are changes already on the books that business owners should be aware of, including benefits that are slated to disappear. Act now before it’s too late.

Large-cap pharmaceuticals Pfizer Inc. (NYSE: PFE) and Johnson & Johnson (NYSE: JNJ)are among stocks outperforming the broader market in the past year, particularly in the past three months. Both stocks are S&P 500 components, so a comparison with that index offers an appropriate benchmark for pharmaceutical stocks.

MarketBeat.com – MarketBeat

While the pharma industry has languished, these companies offer examples of company-specific news that can boost prices even amid wider malaise.

Pfizer is up 6.69% in the past month and 9.78% in the past three months. Shares closed Wednesday at $50.24, a gain of $0.53 or 1.07%. That’s compared to the S&P’s return of 3.34% in the past month and decline of 1.15% over the past three months.

On Wednesday, a U.S. district judge dismissed tens of thousands of claims that Pfizer, along with GSK PLC (NYSE: GLC) and Sanofi SA (NASDAQ: SNY), pertaining to heartburn treatment Zantac, caused cancer. The judge ruled that the claims failed to show legitimate links between Zantac and several types of cancer, including bladder, gastrointestinal, esophageal, pancreatic and liver cancers.

There are still more cases pending around the country, but Wednesday’s ruling means remaining litigation will occur in various state courts; the number of cases has dropped significantly.

Pfizer had more good news Wednesday. According to the company, the U.S. Food & Drug Administration accepted for priority review a Biologics License Application (BLA) for a respiratory syncytial virus (RSV) vaccine candidate submitted by Pfizer. The treatment should prevent respiratory tract disease caused by that particular virus in people ages 60 and older.

Priority review designation by the FDA cuts the standard BLA review time period by four months.

In a statement issued by Pfizer, Annaliesa Anderson, senior vice president and chief scientific officer of vaccine research and development, said, “With no RSV vaccines currently available, older adults remain at risk for RSV disease and potential severe outcomes, including serious respiratory symptoms, hospitalization, and in some cases, even death.”

She noted that the FDA’s acceptance of the BLA for the company’s vaccine candidate is an important regulatory milestone.

Pfizer has consolidated for the past year after peaking at $61.70 in December 2021.

Johnson & Johnson also Outpaces Broader Market

Johnson & Johnson, in addition to its pharmaceutical business, also diversifies into various health care pursuits.

That stock is up 3.08% in the past month, 8.67% in the past three months and 6.17% year-to-date. Shares closed $0.61 higher Wednesday, at $177.17.

Johnson & Johnson has had some recent news that helped boost the stock price. Last month, the company said it would acquire cardiovascular device maker Abiomed Inc. (NASDAQ: ABMD)for nearly $17 billion. The deal will likely accelerate J&J’s presence in a growing area, but J&J’s existing growth in the device space has lagged behind other areas.

The device area has attracted investor interest now, with Ra Medical Systems Inc. (NYSE: RMED) rising an almost astonishing 97.55% in the past week and 43.20% in the past month.

In September, privately held Catheter Precision announced a definitive merger agreement with Ra, which makes lasers for use in the treatment of vascular and dermatological ailments. If completed, the deal would result in a combined publicly traded company focusing on cardiac electrophysiology, or the diagnosis and treatment of conditions affecting the electrical activity of the heart muscle.

Lower Price Targets

Despite recent stock price increases, analysts are somewhat mixed when it comes to the near-to-medium-term outlook for J&J. Since the company’s last earnings report in mid-October, five analysts lowered their price targets on the company.

Johnson & Johnson’s chart reveals a cup-shaped pattern that began forming in late April. Currently, a possible buy point is above $188.69. So far, the correction has declined 15% and hasn’t undercut prior structure lows.

Since the 2020 COVID-19-driven market meltdown, J&J has formed a series of bases with higher highs as well as higher lows. Each time, it has failed to rally more than 20% before pulling back again.

One has to laugh at the macho stock rally the bulls pulled off last week as they ONCE AGAIN misunderstand the statements of the Fed. As clearer heads prevail the stock market (SPY) have erased all of last weeks gains and then some. That is the past. What matters is how to invest going forward. 40 year veteran Steve Reitmeister shares his timely market outlook, trading plan and 8 top picks to generate gains in the weeks ahead.

shutterstock.com – StockNews

Hey, do you remember that awesome rally after Powell’s speech last week…and how the bulls were claiming victory as stocks went soaring above the 200 day moving average?

Yes, that bout of irrational exuberance is over as foretold in my last commentary: Is the Bear Market Over??? (spoiler alert…NO IT AINT OVER!).

The more updated, educated, and elucidated version of that story is shared with you below…

Market Commentary

Indeed, it looks like Mike Wilson of Morgan Stanley called it right when he previously predicted stocks would rally to a range of 4,000 to 4,150 before the bear market resumes in earnest. Thus, after reaching those temporary heights last week he is now reminding everybody to prepare for bottom somewhere between 3,000 to 3,300 by April 2023.

This outlook is not a surprise to Reitmeister Total Return members as I have been beating the drum about this being a long term bear market where we have not yet seen bottom. And not to be suckered in by any of these seemingly impressive bear market rallies as they are all just mirages.

This explains why I still have a hedged portfolio in place to profit as the serpentine pattern of this market eventually winds lower. Just like the +1.86% gain the past 3 brutal sessions for the overall market.

The oddity of recent action is what has become bullish vs. bearish catalysts. I thought it would be useful to summarize that for you folks today to appreciate the events that lead to rallies…and those that get us back in bear market mode.

NOTE OF CAUTION: What I am about to share is the current triggers for price action. However, there is a bizarro world inverse logic being used by bulls that wont last over the long haul. More on that in the next section.

What Are the Bullish Catalysts for Today’s Market?

Anything that points to softening inflation.

This can come in many forms. First, is actual inflation reports like the early November CPI/PPI reports that came in lower than expected. This potential signaling that inflation has peaked was like drinking 5 Red Bulls for traders to bid up prices.

Yes, 7.7% inflation is better than the previous 8% rate. But a long, long, long way from the 2% Fed target which is why Powell has been clear that they will stay hawkish for a long, long, long time.

Also in this category of disinflationary news is weak economic reports. This is the bizarro world concept I referred to early. That’s because normally the chain reaction works like this:

Weak economic data > greater likelihood of recession > lower corporate earnings > lower share prices

Yet at this stage, when investors are myopically focused on only inflation, then they see the equation as follows:

Weak economic data > greater likelihood of recession > tamps down inflation > less hawkish Fed involvement > the sooner the Fed will lower rates in the future > the more bullish long term for stocks > let’s buy stocks NOW!

This latter equation may seem logical on the surface, yet completely misses the superior, and more historically accurate aforementioned version of the bearish chain reaction to this news. And thus it explains why the market too easily sloughed off the truly weak ISM Manufacturing report last Thursday.

Typically the first reading under 50 would have investors rushing to hit the sell button. Yet investors were more than happy to be drunk with bullishness last week as this report came in at 47.7.

This “bad news is good news” mantra is the same flawed logic that had investors buying up stocks in November and December of 2008 as they saw it leading to more favorable Fed actions. However, as we can clearly see in the chart below that rally gave way to a much nastier drop in early 2009 given how decimated the economy was demanding lower stock prices.

That final leg down in Q1 of 2009 became the true and lasting bottom before the next bull market emerged. And yes, I sense that same kind of formation may be taking hold now with lower lows in early 2023 before it is truly time to be bullish once again. (Thus mirroring the view shared by Mike Wilson of Morgan Stanley).

Now let’s consider the flips side of the coin…

What Are the Bearish Catalysts for Today’s Market?

The inverse of above. That being anything that points to inflation remaining too high for too long.

The perfect example is what happened Friday when the Government employment report showed robust job gains of 263,000. Well above expectations.

But what really got investors choked up was the sticky wage inflation that Powell discussed in his most recent speech. Year over year it came in at 5.1% when only 4.6% was expected. That is because the month over month increase was 2X expectations.

The initial reaction to this news was a -1.5% sell off premarket. Yet bit by bit the bullish momentum from earlier in the week returned to eat away at those losses leading to a nearly breakeven close.

Over the weekend investors were clearly stewing on this information as they came out of the gate this week in a selling mood.

-1.79% on Monday

-1.44% on Tuesday

-0.19% on Wednesday

Added altogether we have wiped off the board the entirety of last week’s illogical and ill-fated rally.

To me there is little doubt that the odds of recession and deepening of the bear market have increased given recent economic data. Heck, even just the Chicago PMI coming in at 37.2 last week should have been enough for most investors. That’s because 8 out of the last 8 recessions have been signaled by this report coming in under 40.

And don’t forget the deepening of the inverted yield curve which is as tried and true in calling a recession as any indicator. That got kicked into high gear the past couple weeks as the 10 year Treasury rate has tumbled.

Interesting to note that even the 2 year rate is down of late because it is widely believed the recession is in the works for 2023 which has disinflationary properties (like wiping out many jobs > lower income > lower demand (spending) > lower prices).

For as obvious as these bearish catalysts appear to be, it would also not surprise me to see a repeat of 2008/2009 cycle as noted earlier. That being a market staying aloft on the “bad news is good news mantra” coupled with a dose of Santa Claus rally.

The point being that this week’s decline may be nothing more than taking some froth out of the recent rally…but not necessarily a sign that investors are ready to retest the October lows. In fact, I would bet on us settling into a temporary range between the bear market designation line of 3,855 on the low side and the 200 day moving average on the high side (4,040).

In the meantime, the following reports will be closely watched given their focus on inflation and likely Fed actions:

12/9 Producer Price Index (PPI)

12/12 Consumer Price Index (CPI)

12/13 Fed Interest Rate Decision

The long term trend is still bearish. Very little doubt about that. The only real question is when that comes back into play and we retest the October lows.

That could start in December if the above reports point to sticky inflation that keeps the Fed raising rates much further, which only exacerbates already declining economic activity. However, if bulls continue to read the signals wrong, then they may have one more burst of activity in December to close at near term highs before the rug gets pulled out in early 2023.

All the above explains why I remain decidedly bearish with a portfolio built to not just weather the storm…but actually accumulate gains as the overall market heads lower. That includes our 3 day gain of +1.86% as the market tanked.

With the market closing today at 3,933 and a likely bottom 20% lower in the coming year, explains why it is not too late to employ the strategies advocated in Reitmeister Total Return if you have not already.

What To Do Next?

Discover my special portfolio with 8 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a robust gain for investors as the market tanked.

And now is great time to load back as we deal with yet another bear market rally before stocks hit even lower lows in the weeks and months ahead.

If you have been successful navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 8 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.14 (-0.04%) in after-hours trading Wednesday. Year-to-date, SPY has declined -16.26%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The stock’s price has held above its November 4 low of $69.29. Does that mean we’ve heard the last of its downtrend?

Spotify attempted a rally in the summer, roughly in tandem with the broader market, but it fizzled and the stock has been trending generally lower, although it’s notched a 5.78% one-month gain.

The streaming audio service is grabbing headlines this week because it rolled out its annual year-end feature called Spotify Wrapped, which compiles user a user’s listenership data for the previous year, categorized by music categories, most listened to, and other designations. The feature was launched in 2016.

Struggled During The Pandemic

Spotify, which went public in April 2018, is based in Sweden. After its IPO, it struggled to regain its 2019 highs, and fell with the rest of the market in early 2020. But Spotify failed to rally along with other streaming stocks, such as Netflix Inc. (NASDAQ: NFLX), which staged a big as subscribers craved at-home entertainment in the early days of the pandemic.

The difference, of course, is that people tend to listen to music and podcasts on their commutes to work, which were eliminated while stay-at-home orders were in place. Usage on most Spotify platforms and devices declined in 2020.

However, Usage on TVs and game consoles increased that year as people listened to music in familiar ways at home: while cooking, doing household chores or spending time with the family.

That undoubtedly helped, but it wasn’t enough to narrow the company’s losses, as there was a net decline in daily active users.

Fast forwarding to 2022, the stock is down 67.60% in the past year and 20.23% on a three-year basis.

Netflix, of course, had its own struggles retaining subscribers and maintaining growth rates as pandemic restrictions faded. Nonetheless, it managed to rally in August, September, and October of 2021, sending it to new highs, while Spotify had a shorter rally and rolled over dramatically after a short-lived rally attempt in November of last year.

Since then, Spotify has trended significantly lower, as the one-year return indicates.

Underperforming Broader Market

Even as the broader market rallied in October and November of this year, Spotify investors continued hearing the sound of a downtrend.

If the chart wasn’t enough to convince you that Spotify is underperforming relative to the broader market, then it’s worth taking a look at analysts’ views.

Since the company reported its third quarter on October 25, 11 analysts lowered their price targets on Spotify. Nonetheless, MarketBeat data show that analysts have a “moderate buy” rating on the stock with a consensus price target of $151.72, a potential upside of 101.19%.

In the quarter, Spotify had a total of 456 million monthly active users, a gain of 20% from the year-earlier quarter. It reported 195 million paid subscribers, a 13% increase over the same quarter in 2021.

The company lost $0.84 per share on revenue of $2.975 billion. Earnings were below analysts’ estimates, but revenue came in higher than expected.

Advertising Revenue Is Up

Revenue from advertising, an area the company has targeted for growth, increased 19% from the year-ago quarter and constituted 13% of total sales.

Spotify said most of the advertising growth came on the podcasting side of the business. year over year and made up 13% of total revenue. Spotify rolled out podcasts in 2015. More recently, it added audiobooks and has ramped up those offerings quickly.

It’s pretty clear that digital streaming platforms of various kinds represent the future of audio content consumption. However, Spotify isn’t the only show in town. Despite seeing room for upside, analysts’ reduced price targets for the next 12 to 18 months show a degree of dampened enthusiasm that the company has what it takes to generate excess returns.

Whenever you see that, ask yourself whether you are willing to incur the opportunity cost of owning a particular stock, or are you more likely to get a higher return elsewhere. That question is certainly relevant where Spotify is concerned.

The question of a Fed pivot isn’t if, it’s when because the FOMC can’t continue to hike rates indefinitely. In that scenario, economic activity would grind to a halt and recede, GDP would shrink and the global world order would collapse. No, the FOMC’s mission is to maintain economic stability through price stability and its dual mandate of labor market support. In this light, the FOMC needs to contain inflation not destroy it and that means a careful balance of policy. The question of when the Fed will pivot is a different story and it may be sooner rather than later.

MarketBeat.com – MarketBeat

Economic Activity Lags FOMC Policy By 1 to 2 Years

It is a generally accepted phenomenon that central bank policy takes 1 to 2 years to take effect. This is because the big spending budgets that are impacted by central bank policies are usually set well before the policies are put in place and those policies are changed ever so slowly (usually). Because the first post-pandemic interest rate hike was put in place in March 2022 it’s likely the true impact of the first interest rate hike is yet to be felt. Now, 8 months and 350 basis points of increase later, it won’t be until late in 2024 that the impacts of what the Fed has done to date will be fully integrated into the economy. And they are still raising rates.

The latest indications from the Fed are that 1) they will (or could) slow the pace of interest rates as soon as next week and 2) the peak of interest rates could be higher than the market is forecasting and may stay at that level for longer than anticipated. In the first scenario, the FOMC is already pivoting or trying to pivot in case they’ve already gone too far. We’ll call this the first pivot. In the second scenario, they leave the door open for an even more aggressive policy that may not fully impact the US and the global economy until well into 2025 and that’s where the 2nd pivot will come into play.

Expect A 2nd Fed Pivot Sometime Late In 2023.

The FOMC likes to cling to its data and that is a good thing. If they’d done that in early 2021 when inflation started to increase maybe we would be where we are now. The point is that inflation is so hot and has been running so high for so long that the FOMC needs to be sure it’s tamped down. The talk from that quarter is rates will need to come down to at least 2% to make them happy and, by that time, they may well be behind the curve once again. The target rate indicated by the CME’s Fedwatch Tool is 475 to 500 basis points by July 2023. That will have sent the US economy into a recession that is being led by the housing sector. When this data shows up in the broader economy the Fed will have to start cutting rates because, guess what, it could take up to 2 years for economic activity to catch up with the new, easier policy.

The question now is how bad will the downturn be. The word from the C-suite is that it could be very bad and the housing data backs that up. While strength was shown in the current quarter and current year, Toll Brothers (NYSE: TOL) F23 guidance is indicating a 15% to 23% decline in volume sales compounded by an 11% decline in home prices. This is bad news for home builders, home sellers and every industry affected by the home building industry which is virtually all of them.

When Will The FOMC Pivot?

The FOMC is trying to pivot now, but the data may not let them. If consumer-level inflation doesn’t stay down or if it lingers at new lower but still high levels the Fed will be forced back onto the track of interest rate hikes. The risk for the market is that economic activity will contract so quickly and/or so sharply the FOMC will be forced to pivot again and start cutting rates. So much for them being in charge of the money.

In 1857, John Henry Hopkins Jr. wrote “Three Kings of Orient,” the popular Christmas carol more commonly known today as “We Three Kings.” Based on the Biblical Magi who bore gold, frankincense, and myrrh, the song is about the importance of sacrifice — and believe it or not, it has investing connotations.

MarketBeat.com – MarketBeat

In stock investing, there are always choices to be made. At the core, picking prospective winners is a tradeoff between risk and reward. Then there are other decisions — U.S. versus international companies, growth versus value, and high or low volatility. Not to mention an array of industry groups.

Of course, the total return of a stock is ultimately what we’re after as investors. This includes both price growth and dividend payments. Opting for growth typically requires sacrificing stable income, and vice versa.

Investors that prefer stability should consider the Dividend Kings, the “perfect light” of perpetually increased dividends. These are companies that have raised their dividend in each of the last 50 years or more.

This elite group of 37 stocks comes from all sorts of sectors and has a range of yields, but have one thing in common — they are great long-term wealth builders. Yes, the tradeoff is usually lower price appreciation. However, given this year’s market selloff, for some, the near-term upside is better than usual.

Here are “Three Kings” that the wise men and women on Wall Street feel have a particularly good upside.

What is National Fuel Gas Company’s Annual Dividend Payout?

National Fuel Gas Company (NYSE: NFG) is a relatively new member of the Dividend Kings club having reached the 50-year mark in 2020. Yet the company carries a more distinguished trait. It is the only energy sector name to appear on the list.

Yes, it operates similarly to a utility, of which there are several among the Dividend Kings — but it is the only one classified as energy by virtue of its oil and natural gas production arm and pipelines.

The stock combines the steady nature of a regulated gas company with the growth potential of an E&P business. National Fuel has paid a dividend for 120 years with strong cash flow generation enabling it to raise its payout for 52 straight years. The $1.90 per share annual payout equates to a 3% forward yield.

Sell-side research firms are mostly bullish on National Fuel because of the rare combination of growth and shareholder value. It ended fiscal 2022 on a high note with 80% adjusted earnings growth, but management lowered its fiscal 2023 outlook on moderating natural gas prices. The Street sees this as a long-term opportunity. The consensus price target of $81.50 implies 29% upside.

What is ABM Industries’ Dividend Growth Streak?

ABM Industries Incorporated (NYSE: ABM) is a mid-cap company that provides building maintenance services. The steady nature of its service contracts generates consistent profits, a portion of which are passed on to shareholders in the form of dividends. ABM Industries is riding a 54-year dividend hike streak after boosting its quarterly dividend to $0.195 per share.

While the 1.7% dividend yield is roughly on par with the broader S&P 400, ABM Industries has above-market upside according to analysts that actively cover the stock. Current price targets range from $52 to $65 and the $58.50 average points to 29% upside.

ABM Industries is a late earnings season reporter scheduled to announce fiscal Q4 results on December 13th. The Street is forecasting 4% year-over-year EPS growth on 16% revenue growth. Not overwhelming figures but considering the company has topped EPS estimates in 7 straight quarters, it could be a good earnings play.

More importantly, ABM Industries screams stability and low risk. Its facilities management solutions — including engineering, electrical, lighting, HVAC, janitorial, and even landscaping and parking — are employed by a wide range of customers from hospitals and schools to airports and data centers. A track record of profitable growth, dividend increases and buybacks make this one to own for at least the next 12 months.

Does Nordson Corporation Have Good Upside?

Nordson Corporation (NASDAQ: NDSN) is another lesser-known industrials Dividend King. The diversified coatings and adhesives conglomerate is a poor man’s 3M — which is a fellow Dividend King along with sector peers Dover, Emerson Electric, Parker-Hannifan and Stanley Black & Decker.

Up nicely from its 2022 low but still, 12% below its 2021 record high, analysts see more room to run for Nordson. The consensus price target of $272 implies a 15% upside from here. Not too shabby for a low-volatility dividend grower.

Big things are expected for Norsdon’s upcoming fiscal Q4 earnings release. On December 14th, the Street will look for 24% year-over-year earnings growth reflecting strong end-market demand and effective cost-cutting measures. The company has surpassed EPS expectations in nine of the last 10 quarters.

Aside from the dividend prowess, another reason to like Nordson long-term is the recent acquisition of CyberOptics, a leading global manufacturer of 3D sensing technologies. The addition is slated to boost Nordson’s semiconductor testing capabilities and may turn out to be well-timed given an anticipated rebound for chipmakers.

CBS News business analyst Jill Schlesinger joins “CBS Mornings” to talk about how to budget for raising a child. She also discusses the benefits you need to consider as a parent, like life insurance.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

For many investors, investing during a bear market means staying away from small-cap stocks. That could be a mistake as these stocks are the ones that often lead the way when the market reverses. And…spoiler alert…the market always does turnaround.

MarketBeat.com – MarketBeat

Nevertheless, quality still matters, and it matters even more when investing in companies with a small market cap. With that in mind, The Bancorp (NASDAQ: TBBK) is a small-cap regional bank that appears to be well-positioned for whatever happens in 2023.

This article will introduce you to The Bancorp and explain why it may deserve a place on your 2023 watchlist.

An Emerging Name Among Regional Banks

The Bancorp may not be a household name when it comes to regional banks, but that could be changing. The company operates as the financial holding company for The Bancorp Bank. That bank provides a portfolio of banking products and services made up of fintech solutions, institutional banking, commercial lending, and real estate bridge lending.

Although you may not have a credit or debit card with The Bancorp name, chances are that it may underwrite one of the many private label companies you’ve heard about and may get offers from. The company is the number one issuer of prepaid cards in the United States.

In August 2022, the Bank Director 2022 Ranking Banking study, ranked The Bancorp Bank as the number one bank among those with assets between $5 billion to $50 billion. The bank’s ranking was measured by its return on equity and assets, asset quality, capital adequacy and total shareholder return.

A Profitable Bank That is Showing Growth

In its most recent quarter, The Bancorp missed analyst expectations for revenue and earnings. But some context is important. The company has delivered revenue and earnings in the first three quarters that are higher on a year-over-year (YOY) basis. For the first three quarters, the company is ahead of 2021’s revenue pace by 5% and is ahead in terms of earnings per share (EPS) by 10%.

TBBK Stock is One for the Watchlist

As we get into the home stretch of 2022, it’s a good time to take a critical look at your portfolio. Weeding out underperforming stocks is often the easy part. Replacing them is a different matter altogether.

The consensus in the financial media is that there will be a recession of unknown length and severity in 2023. Of course, there are also those that believe we’re already in one. Either way, investors are likely to be dealing with higher interest rates in 2023. This makes financial stocks attractive.

But the risk of financial stocks comes from the lending side of the business. That’s another reason to look at The Bancorp. The company has a history of having a loan portfolio with low credit losses

TBBK stock is not heavily covered by analysts. However, the two analysts that are tracked by MarketBeat give the stock a buy rating with a price target that gives investors the potential for a 26% upside. That kind of gain, along with a P/E ratio of just around 13x earnings and a forward P/E ratio of around 12x makes up for the lack of a dividend and makes The Bancorp one to have on your 2023 watchlist.

Worst to first. It can happen fast when it comes to U.S. stocks.

MarketBeat.com – MarketBeat

One of the hottest groups in the recent market rally is consumer cyclicals. Long a distant underperformer in 2022, the sector has come to life in recent weeks thanks to some improved economic data, signs that inflation may have peaked and a more dovish Fed.

Economically sensitive companies are finding favor again because investors are seeking out oversold names in hopes of a lengthy rebound. From home improvement stores and apparel retailers to hotels and restaurants, some big gains are emerging from the S&P 500’s October 13th bottom.

With many consumer discretionary stocks arguably way oversold, the gains may just be getting started. More positive economic releases and a less aggressive Fed rate hike campaign could turn the sector from a laggard to a leader in 2023.

These three stocks already have the wind at their back heading into the new year.

Will Peloton Stock Be a 2023 Winner?

Peloton Interactive, Inc. (NASDAQ: PTON) has doubled off its 2022 low and seems to be finding favor as a turnaround story. The indoor cycling company rode a seven-day win streak into December despite a rather lackluster third-quarter earnings report. A wider-than-expected net loss reflected supply chain disruptions, higher material, and freight costs, and a shift from at-home exercise to gym memberships.

Regardless, sentiment around Pelton has turned bullish with the market sensing the worst may be over for the former pandemic winner. A healthier economy next year could mean increased consumer confidence and spending on connected fitness equipment and subscriptions. Combined with an improvement in logistics constraints and cost inflation, Peloton’s bottom line would theoretically be in better shape.

Whether demand for interactive fitness strengthens in a healthier economy remains to be seen. Absent the pandemic boost, Peloton does still have two powerful tailwinds: 1) global interest in health and wellness and 2) work-from-home trends. Both are supportive of purchasing digital fitness experiences.

Still, the biggest key to a 2023 Peloton comeback may lie in the effectiveness of recently formed partnerships with UnitedHealthCare, Dick’s Sporting Goods, Hilton, and Amazon which could significantly expand Peloton’s audience.

Has Alibaba Stock Finally Found a Bottom?