The Senate has unanimously approved legislation that would ban the use of TikTok on government phones and devices as part of the push to combat security concerns related to the Chinese-owned social media company. What do you think?

“God help the staffer who has to explain to Biden what he’s signing.”

Samantha Graham, Textiles Coordinator

“Good. I prefer our congress people’s data to be stolen by an American company.”

James Gomez, Medical Librarian

“Now the only hurdle is teaching senile legislators how to delete an app from their phone.”

FORT WORTH, Texas, December 16, 2022 (Newswire.com)

– Equify Financial, LLC is excited to announce the appointment of Christian Torresluna, Toby Newhouse and Naszier Colburn as Regional Sales Managers for its Small-Ticket Dealer and Vendor Program Equipment Finance Business.

Greg Clemens, National Sales Manager for Equify Financials’ Dealer and Vendor finance platform, states, “We are fortunate to add these three experienced Regional Sales Managers to the team. I look forward to working with them as we expand our footprint across the entire U.S. market.”

With his vast experience, Christian Torresluna can make an invaluable contribution to Equify’s Small-Ticket Dealer and Vendor program. He specializes in recognizing opportunities for development, honing business operations, and constructing customer financing solutions that always prioritize client fulfillment first and foremost.

With his strong background in technology and equipment, Naszier Colburn is a specialist at executing sales strategies and initiatives to promote business growth. He has an impressive record in providing solutions for the needs of clients looking to acquire equipment.

Toby brings two decades of sales experience from both mortgage lending and private lending realms. In his tenure as a private lender alone, he’s managed to secure over $1 billion dollars for customers while delivering stellar customer service at every step along with portfolio management.

Dan Krajewski, EVP of Equify Financial, added, “Equify’s unique employee and customer-first culture allows us to attract the best talent in the equipment finance market. As we continue our expansion plans, we will continue to hire best-in-class employees.”

About Equify Financial, LLC

Equify Financial is a privately-owned, independent specialty finance company based in Fort Worth, Texas, serving the United States. Founded in 2011 on the principles of meeting our customers where they are and helping them get to where they want to go, Equify works with customers at any stage in their business. We tailor each service for our clients to build a strong relationship and future.

With over 180 years of combined experience in the equipment finance industry, we help our customers find the best financial path forward.

Yesterday’s retail sales report showed that consumers pulled back on spending last month, raising fears of a recession. Moreover, the Fed signaled to keep raising rates more through the following year. Given an uncertain market backdrop, investors should buy fundamentally sound and dividend-paying stocks Johnson (JNJ), Coca-Cola (KO), and Cardinal Health (CAH), which could keep gaining and generate significant long-term returns. Read on….

shutterstock.com – StockNews

With inflation cooling considerably in the last two months, the Federal Reserve slightly eased its monetary policy tightening by raising its benchmark interest rate by 50 basis points this week.

“Inflation data received so far for October and November show a welcome reduction in the monthly pace of price increases. But it will take substantially more evidence to have confidence that inflation is on a sustained downward path,” said the Fed Chair, Jerome Powell.

The Fed officials indicated plans to keep raising rates through next year, with no reductions until 2024, and expect the “terminal rate” at 5.1%. Furthermore, the weaker-than-expected retail sales data suggests that inflation is taking a toll on consumers. Retail sales dropped 0.6% in November, worse than the Dow Jones estimate of a 0.3% decline.

The disappointing retail sales report and the Fed’s indication of extending rate hikes sparked recessionary fears. Wall Street tumbled yesterday, with the Dow Jones closing out its worst day in three months. The Dow Jones declined 2.3%, while the S&P 500 and Nasdaq Composite fell 2.5% and 4.5%, respectively.

Amid the ongoing market uncertainties, investing in fundamentally strong and dividend-paying stocks Johnson & Johnson (JNJ), The Coca-Cola Company (KO), and Cardinal Health, Inc. (CAH) could be wise for investors looking to generate massive long-term returns.

JNJ, the world’s largest and most diverse healthcare conglomerate, develops, manufactures, and sells various healthcare goods. Its business operates through three segments, Consumer Health Products; Pharmaceutical Products; and MedTech. Its core focus is items relating to human health and well-being.

On November 1, JNJ and Abiomed Inc. (ABMD), a world leader in breakthrough heart, lung, and kidney support technologies, announced that they have entered into a definitive agreement under which JNJ will acquire through a tender offer all outstanding shares of Abiomed, for an upfront payment of $380.00 per share in cash.

ABMD’s skilled workforce, strong ties with clinicians, unique cardiovascular portfolio, and extensive pipeline will complement JNJ’s MedTech portfolio. It will also enable JNJ to implement its strategic priorities, and vision for the new JNJ focused on Pharmaceutical and MedTech.

For the fiscal 2022 third quarter ended September 30, 2022, JNJ’s sales in the United States grew 4.1% year-over-year to $12.45 billion, while its overall reported sales increased 1.9% year-over-year to $23.79 billion, with adjusted operational growth of 8.2%. Its net earnings rose 21.6% year-over-year to $4.46 billion, while its EPS increased 22.6% from the year-ago value to $1.68.

JNJ paid a quarterly dividend of $1.13 per share on December 6, 2022. It pays a $4.52 per share dividend annually, which translates to a 2.51% yield on the current price. Its four-year average dividend yield is 2.60%. JNJ’s dividend payout has grown at a 5.9% CAGR over the past three years and a 6% CAGR over the past five years. The company has raised its dividend for 60 consecutive years.

For the fiscal year ending December 2022, analysts expect JNJ’s revenue to increase 1.4% year-over-year to $95.04 billion. The company’s EPS for the current year is expected to increase by 2.5% year-over-year to $10.05. JNJ has surpassed the consensus EPS estimates in each of the four trailing quarters, which is impressive.

In addition, analysts expect the company’s revenue and EPS for the next fiscal year to grow 2.6% and 3.2% year-over-year to $97.54 billion and $10.37, respectively. Over the past month, JNJ has gained 3% and 4.4% over the past six months to close the last trading session at $177.49.

JNJ’s strong fundamentals are reflected in its POWR Ratings. The stock has an overall rating of A, which equates to a Strong Buy in our proprietary rating system. The POWR Ratings are calculated by considering 118 different factors, each weighted to an optimal degree.

The stock has an A grade for Stability and a B for Value and Quality. Within the Medical-Pharmaceuticals industry, it is ranked #7 of 160 stocks.

Beyond what we stated above, we also have JNJ’s ratings for Growth, Sentiment, and Momentum. Get all JNJ ratings here.

KO is a famous beverage company that manufactures, markets, and sells various nonalcoholic beverages worldwide. The company offers sparkling soft drinks, flavored and enhanced water, sports drinks, juice, dairy, plant-based beverages, and energy drinks. It operates through a network of independent bottling partners, distributors, wholesalers, and retailers.

On September 29, KO and Molson Coors Beverage Company (TAP) entered an exclusive agreement to develop and commercialize Topo Chico Spirited, a line of spirit-based, ready-to-drink cocktails inspired by the bright and refreshing taste of tequila and vodka-based beverages. It will be launched in more than 20 markets across the country in 2023 and might boost the company’s revenue stream.

For the fiscal 2022 third quarter ended September 30, 2022, KO’s net operating revenues increased 10.2% year-over-year to $11.05 billion. The company’s gross profit grew 7.1% year-over-year to $6.50 billion. Its operating income came in at $3.09 billion, up 6.6% year-over-year.

Furthermore, the net income attributable to shareholders of KO was $2.83 billion, up 14.3% year-over-year. Its non-GAAP net income per share grew 6.2% from the year-ago value to $0.69.

On December 15, KO paid its shareholders a regular quarterly dividend of $0.44 per common share. The company pays $1.76 per share annually, which translates to a 2.75% yield at the current price. Its four-year average dividend yield is 3.07%.

KO has a record of 60 years of consecutive dividend growth. The company’s dividend payouts have grown at a CAGR of 3.2% over the past three years and a CAGR of 3.5% over the past five years.

Analysts expect KO’s EPS to increase 7.4% year-over-year to $2.49 for the fiscal year ending December 2022. Likewise, the revenue estimate of $42.70 billion indicates a 10.5% growth from the previous year. Also, the company has surpassed the consensus EPS and revenue estimates in all four trailing quarters.

The stock has gained 3.2% over the past month and 8.7% over the past year to close its last trading session at $63.11.

KO’s POWR Ratings reflect this promising outlook. The stock has an overall B rating, equating to a Buy in our proprietary rating system.

KO has a grade of A for Sentiment and B for Stability and Quality. Within the A–rated Beverages industry, it is ranked #16 out of 33 stocks.

Beyond what we’ve stated above, we have also given KO grades for Value, Momentum, and Growth. Get all KO ratings here.

CAH provides various healthcare services and products in the United States, Canada, Europe, and Asia. The company operates through two segments: Pharmaceutical and Medical. It offers customized solutions for hospitals, healthcare systems, pharmacies, clinical laboratories, and at-home patients.

Last month, CAH launched Velocare™, a supply chain network and last-mile fulfillment solution that will reach patients in one to two hours with critical products and services required for hospital-level care at home. Through a collaboration with Medically Home, Cardinal Health at-Home Solutions supports Medically Home health system customers with Velocare™ to enable scaled, high-acuity care in the home.

On September 15, CAH and PayrHealth announced a collaboration to help specialty physician practices simplify payor contracting and maximize financial performance. “We are very excited to partner with PayrHealth to bring meaningful efficiencies and cost savings to practices, so they can focus on patient care,” said Amy Valley, vice president of Clinical Strategy & Technology Solutions at Cardinal Health.

In the fiscal 2023 first quarter ended September 30, 2022, CAH’s revenue increased 12.8% year-over-year to $48.60 billion. Its revenue from the Pharmaceutical segment rose 15.1% from the year-ago value to $46.83 billion, while its segment profit came in at $431 million, up 6.2% year-over-year. The company’s adjusted free cash flow for the quarter stood at $342 million.

On November 8, CAH’s Board of Directors approved a quarterly dividend of $0.4957 per share, payable on January 15, 2023. Its annual dividend of $1.98 yields 2.91%. Moreover, the company’s dividend payouts have grown at a 1% CAGR over the last three years and a 1.6% CAGR over the past five years. The company has a record of 27 years of consecutive dividend growth.

The consensus revenue estimate of $199.25 billion for the fiscal year ending June 2023 represents a 9.9% improvement year-over-year. The consensus EPS estimate of $5.29 for the ongoing year indicates a 4.6% year-over-year growth. Furthermore, the company’s revenue and EPS for the next fiscal year are expected to grow 6.3% and 18% year-over-year to $211.81 billion and $6.25, respectively.

Shares of CAH have gained 51.1% year-to-date and 59.7% over the past year to close the last trading session at $78.57.

CAH’s financial strength and solid growth prospects are reflected in its POWR Ratings. The stock’s overall A rating translates to a Strong Buy in our proprietary rating system.

CAH has a grade of B for Growth and Value. Within the Medical – Services industry, it is ranked #4 of 77 stocks. To see additional POWR Ratings (Sentiment, Quality, Momentum, and Stability) for CAH, click here.

JNJ shares were unchanged in premarket trading Friday. Year-to-date, JNJ has gained 6.48%, versus a -17.02% rise in the benchmark S&P 500 index during the same period.

About the Author: Mangeet Kaur Bouns

Mangeet’s keen interest in the stock market led her to become an investment researcher and financial journalist. Using her fundamental approach to analyzing stocks, Mangeet’s looks to help retail investors understand the underlying factors before making investment decisions.

A classic cup-with-handle base is often a precursor to a stock’s run-up, and retailer Tractor Supply Company (NASDAQ: TSCO) is forming exactly that type of consolidation.

The Tennessee-based company specializes in items for rural lifestyles, including hardware, supplies for livestock and domestic animals, lawn and garden items, fencing, mowers, and clothing.

It’s the nation’s largest consumer farm retailer. As of September, it operates 2,027 Tractor Supply stores in 49 states and an e-commerce platform. In October, it acquired 81 stores from Orscheln Farm and Home. These will be rebranded to Tractor Supply by the end of next year.

Tractor Supply also owns Petsense by Tractor Supply, a small-box pet specialty supply chain primarily in small and mid-size communities. It runs 180 Petsense stores in 23 states.

MarketBeat analyst data for the company show a “moderate-buy” rating with a price target of $235.94 and a potential upside of 10.88%.

Analysts Expect More Store Openings

Morningstar analyst Jaime Katz writes that she expects Tractor Supply to grow to around 3,000 stores by 2031, including Petsense. Over time, the company seems poised for growth, but what about the more immediate future?

Shares are up 14.41% in the past three months as the stock began etching the right side of a cup pattern in September. It rallied to an interim high of $229.81 on December 1 and has been forming a handle since then. The cup-with-handle formation offers an early entry point before a stock regains the high price of the cup base.

As the handle formed, the stock declined 1.63% in the past month. You don’t want to see a handle decline of more than 10% or possibly 15% at the outset; that would mean the setup has broken down.

Another good sign in the current handle is: Trading volume has been below normal in the past two weeks as the price declined. That’s ideal, as a heavy-volume selloff could indicate a lack of conviction among institutional buyers. Instead, this handle appears (so far) to be the result of some mild profit-taking. That can serve to shake out investors who lack conviction, setting the stage for more interested buyers to nab shares at a lower price.

But does the current setup suggest more significant potential for gains than even the analysts see?

Shares were trading around $213.27 mid-session Thursday. That’s roughly 7% below a potential buy point near $230. If the stock clears that buy point without the handle sinking much further, then the stock may have the juice to rise more than 10.88%, primarily if a broad market rally also provides a lift.

The three-year revenue growth rate is 20%, and its three-year earnings growth rate is 29%. Revenue grew between 43% and 8% in the past eight quarters. One possible caveat: Revenue growth has been slowing from mid-double-digit rates to single-digit rates over the past six quarters. Make no mistake: Sales are still increasing at healthy year-over-year clips, but less frenetically than before.

Earnings have been growing each year, as well. For the full year, Wall Street is eyeing a net income of $9.62 per share, an increase of 12%. Next year, that’s expected to grow another 9% to $10.47 per share.

As with many stocks, Tractor Supply’s price action has tended to track the broader market. For example, shares advanced in five of the subsequent six sessions after the company’s most recent earnings report on October 20. However, as a nascent rally in the S&P 500 sputtered in early November, Tractor Supply also fell. Even its current handle formation is occurring in tandem with a moderate selloff in the S&P.

The cup-with-handle base, solid earnings and revenue growth, and future projections make the stock an attractive watchlist candidate. Investors should resist the temptation to jump into a promising stock too early, as their money may languish while other stocks rally sooner.

Despite the aggressive rate hikes that plagued tech stocks since the start of the year, the software industry’s prospects look strong, thanks to rapid digitalization and demand for cloud-based solutions. While fundamentally strong software stocks Salesforce (CRM) and Mitek Systems (MITK) could be worth buying to capitalize on the industry’s long-term growth prospects, it would be wise to steer clear of fundamentally weak stocks Robinhood Markets (HOOD) and Fastly (FSLY). Keep reading….

shutterstock.com – StockNews

2022 has been a challenging year for tech stocks due to various macroeconomic concerns. The Fed’s aggressive rate hikes have made the high-growth tech stocks look unattractive to investors, leading to the tech-heavy Nasdaq Composite shedding 28.6% year-to-date.

However, inflation is now showing signs of cooling down, with November’s CPI rising 0.1% from the previous month and 7.1% from a year ago, below analyst estimates. The easing of inflation has prompted the Fed to stick to the word of slowing down the pace of rate hikes, as it announced a 50-basis-point rate increase yesterday.

With the Fed starting to slow down the pace of rate increases, software stocks could again turn into attractive investment options for investors. According to Gartner, enterprise software spending isprojected to grow 8.6% in 2023.

Although the industry’s prospects look bright, not all software stocks will likely turn out to be profitable investments. In order to capitalize on the industry’s recovery prospects, it could be wise to buy fundamentally strong software stocks Salesforce, Inc. (CRM) and Mitek Systems, Inc. (MITK). On the other hand, Robinhood Markets, Inc. (HOOD) and Fastly, Inc. (FSLY) could be best avoided now due to their weak fundamentals and poor growth prospects.

CRM provides customer relationship management technology that brings companies and customers together worldwide. Its Customer 360 platform empowers its customers to work together to deliver connected experiences for their customers. The company’s service offerings include Sales, Service, Marketing, and Commerce.

On September 21, 2022, Insurtech leader, Zywave, announced a dedicated partnership and increased collaboration with CRM. This partnership is believed to bring together the worlds of insurance agency sales and client service, creating more efficient, strategic workflows powered by data and content to deliver a seamless client experience.

Raja Singh, Senior VP and General Manager at CRM, said, “Together, Salesforce and Zywave enable users to efficiently do their jobs and unlock their critical business data, so it can be leveraged for real-time intelligence going forward.”

For the fiscal third quarter ended October 31, 2022, CRM’s total revenues increased 14.2% year-over-year to $7.84 billion. The company’s gross profit increased 14.5% year-over-year to $5.75 billion. Moreover, its income from operations increased significantly year-over-year to $460 million.

Analysts expect CRM’s EPS and revenue for the quarter ending December 31, 2022, to increase 61.6% and 9.2% year-over-year to $1.36 and $8 billion, respectively. CRM has an impressive earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters. The stock has fallen 15.1% over the past month to close the last trading session at $134.75.

CRM’s strong fundamentals are reflected in itsPOWR Ratings. The stock has an overall rating of B, equating to a Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

Within the Software – Application industry, it is ranked #15 out of 139 stocks. It has an A grade for Growth and a B for Sentiment.

We have also given CRM grades for Value, Momentum, Stability, and Quality.Get all CRM ratings here.

MITK develops, markets, and sells mobile image capture and digital identity verification solutions worldwide. The company’s solutions are embedded in native mobile apps and web browsers to facilitate digital consumer experiences. It offers products such as Mobile Deposit, Mobile Verify, Mobile Fill, CheckReader, among others.

For the fiscal third quarter ended June 30, 2022, MITK’s total revenue increased 23.8% year-over-year to $39.33 million. Its non-GAAP net income came in at $10.18 million. The company’s non-GAAP EPS came in at $0.23, representing no change from the year-ago period.

Analysts expect MITK’s revenue for the quarter ended September 30, 2022, to increase 16.1% year-over-year to $38.61 million. For fiscal 2022, its EPS is expected to increase 17.1% year-over-year to $0.89.

It has a commendable earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters. The stock has gained 24.7% over the past six months to close the last trading session at $10.90.

It is no surprise that MITK has an overall rating of B, translating to a Buy in our proprietary rating system. Within the Software – Application industry, it is ranked #8. In addition, it has a B grade for Growth, Value, and Quality.

Click here to see the additional ratings of MITK for Momentum, Stability, and Sentiment.

HOOD operates a financial services platform that allows users to invest in stocks, exchange-traded funds, options, gold, and cryptocurrencies. The company also offers various learning and education solutions comprising Snacks, Learn, Newsfeed, and cash management services.

HOOD’s total net revenues for the fiscal third quarter ended September 30, 2022, declined 1.1% year-over-year to $361 million. Its net loss narrowed 87% year-over-year to $175 million. Additionally, its loss per share narrowed 90.3% year-over-year to $0.20.

HOOD’s EPS for the quarter ending December 31, 2022, is expected to remain negative. Its revenue for fiscal 2022 is expected to decline 24.6% year-over-year to $1.37 billion. The stock has fallen 48.8% year-to-date to close the last trading session at $9.09.

HOOD’s grim outlook is reflected in its POWR Ratings. The company has an overall rating of D, which translates to a Sell in our proprietary rating system. Within the same industry, it is ranked #120. The company has an F grade for Stability and a D for Value and Quality.

Click here to see the additional POWR Ratings of HOOD for Growth, Momentum, and Sentiment.

FSLY operates an edge cloud platform for processing, serving, and securing its customer’s applications worldwide. The edge cloud is a category of Infrastructure as a Service that enables developers to build, secure, and deliver digital experiences at the edge of the internet. It is a programmable platform designed for web and application delivery.

For the fiscal third quarter ended September 30, 2022, FSLY’s non-GAAP gross margin came in at 53.6%, compared to 57.5% in the year-ago period. The company’s non-GAAP operating loss widened 53.4% year-over-year to $19.84 million. Additionally, its non-GAAP net loss per common share widened 27.3% from the prior-year quarter to $0.14.

FSLY’s EPS for the quarter ending December 31, 2022, is expected to remain negative. The stock has fallen 73.2% year-to-date to close the last trading session at $9.50.

FSLY’s bleak prospects are reflected in its POWR Ratings. The company has an overall rating of D, translating to a Sell in our proprietary rating system. It is ranked #130 in the Software – Application industry. In addition, it has a D grade for Momentum, Stability, and Sentiment.

To see the additional ratings of FSLY for Growth, Value, and Quality,click here.

CRM shares were trading at $130.55 per share on Thursday afternoon, down $4.20 (-3.12%). Year-to-date, CRM has declined -48.63%, versus a -16.86% rise in the benchmark S&P 500 index during the same period.

About the Author: Malaika Alphonsus

Malaika’s passion for writing and interest in financial markets led her to pursue a career in investment research.

With a degree in Economics and Psychology, she intends to assist investors in making informed investment decisions.

As a result of the financial crisis of 2008, Warren Buffett lost about $23 billion personally, and his company, Berkshire Hathaway, lost its AAA credit rating. So how can he tell us not to lose money, then?

His point is that a sensible investor has a certain mindset that includes:

Avoid frivolous spending.

Make sure you don’t gamble.

Don’t make investments with a cocky attitude that you can lose money.

Educate yourself.

He invests only in companies that he understands and thoroughly researches. You shouldn’t enter into an investment expecting to lose money, just as he doesn’t. For Buffett, temperament is more important than intellect when it comes to investing. To become a successful investor, you should not worry about what the crowd thinks.

It is natural for the stock market to fluctuate. Buffett stays focused on his goals no matter how good or bad the economy is, and all investors should do the same. It does not matter what the market does; this esteemed investor rarely tweaks his long-term investment strategy.

But I’d also add that sometimes you have to learn by making mistakes. Sure, I’m just as guilty of sharing hacks on how to make millions. But I want to flip the script and share with you the six mistakes that collectively cost me $4.2 million. Hopefully, you won’t repeat the same blunders that I did.

1. Penny Stock Mishap

Penny stocks should only cost pennies, right? It’s not quite that simple. To qualify as a penny stock, the stock price must be less than $5.00. Penny stocks also have the following characteristics:

The Nasdaq or any exchange does not trade them

The price is less than $5.00

The company does not meet the financial standards of listed equity companies.

Penny stocks are popular among investors because of their low cost and “potential” payoff. Ideally, “potential” could be translated as “highly unlikely.”

There’s no liquidity in penny stocks, which makes them risky. In addition, the penny stock market is not listed on the major exchanges (NYSE or Nasdaq) but on the Over the Counter Bulletin Board (OTCBB) or the Pink Sheets.

Many of these companies don’t have to provide as detailed a report as their publicly traded counterparts because the listing requirements are far less stringent.

Another risk involved with penny stocks is that they’re prone to scams. Typically, penny stock fraud involves a “pump and dump.” First, small groups of speculators will accumulate large shares of penny stocks. Then, as soon as they secure their positions, they will release positive financial propaganda, news so unexpected and titillating it can drastically change people’s perceptions.

It aims to entice small-time investors to begin trading irrationally. Most of the time, the news is false, but before it is discovered, the stock price skyrockets, and the original speculators profit greatly.

My penny stock blunder.

If we go back in time a little bit, I used to be a financial advisor. And that’s when this debacle took place. To be honest, it still makes me sick to my stomach.

So, what exactly happened?

A client told me about their daughter’s boyfriend, whose dad worked for a mining company. In hindsight, this should have been a red flag. But I was caught up in the moment.

Since this was a penny stock, also known as a thinly traded over-the-counter security, there wasn’t much news about it since it had just signed some new deals. But, according to his theory, this penny stock would soar pretty quickly.

I had some cash in my investment account and decided to roll with it. So, I placed a trade to buy some shares of this stock that would make me millions.

As far as trading is concerned, the OTC market is like the Wild West. Just because the stock is trading at $0.90 doesn’t mean it will be bought or sold at $0.90.

When I place a buy order “at the market,” the price could shoot up to $1.90 or $3.00, depending on whatever their price might be. So essentially, that’s what happened in my case.

I ordered 2,500 shares (I can’t remember exactly), and a few 100 shares were executed at what I thought was the market price. Unfortunately, my mistake was that many of them were double the price I wanted to buy them for.

Even worse, after the trade settled, the prices reflected what I had originally paid.

So, to summarize:

Despite believing I was buying a penny stock for $.90 per share, I submitted a buy order for 2500 shares at market.

Although I bought a few hundred shares at $.90, most executed at least twice or three times that price. As a result, I invested $5,000 instead of the expected $2,250.

Upon settlement, the price reverted back to $.90. I would have taken a massive loss if I had sold it that day.

Where did it all go wrong?

I have to swallow my pride here. But here’s how I screwed this one up.

The advice I received came from someone I had no business listening to. My client knew nothing about the stock besides what his daughter’s boyfriend had told him about the company. So make sure you consider the source of any investment advice you receive.

Over-the-counter markets were foreign to me. The system is not like logging into my TD Ameritrade account and purchasing a stock on the NY stock exchange.

The experience was more like going to Spain, going to a flea market, and trying to bargain with a vendor.

Greed isn’t always a good thing. My boring mutual funds were making a decent return, but the chance of quadrupling my money in a short time got the better of me.

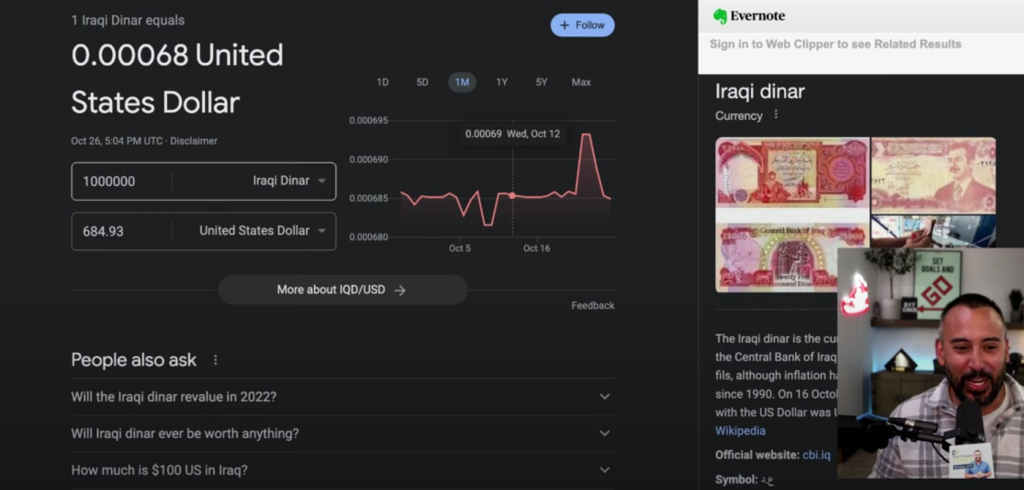

2. Iraqi Dinar

Iraqi Dinar

The Iraqi Dinar was all the rage while we were deployed. It’s basically their currency. I don’t remember all the details. But I remember the Kuwaiti dollar back then, whenever the US went in and got their government in order. So, as a result, the Kuwaiti skyrocketed.

So, the Kuwaiti currency might have taken only $1,000 in US currency to buy a million-dollar bill. I don’t know if you would have had that much extra money, But if you did, that’s a huge, huge return.

Well, many speculated that the exact same thing could happen in Irag. Some claimed that if you invested in Iraqi Dinar, you could make a 100 return. In the end, I bought a million dollars worth of Iraqi dinars.

Since this was 2005, I can’t recall the exact ratio. But the exchange rate was somewhere around 750 or 800. And there were also fees thrown as well.

What is the current state of the Dinar?

Here’s the thing. After all these years, it’s still sitting in our safe. If I put in 750-800 bucks back in 2005, that’s worth $684.93 US dollars. So think about what would have happened if I’d bought $800 of the S&P 500 instead. I lost an opportunity because I didn’t invest in something that would have definitely turned a profit.

3. Solo 401k Business

Solo 401(k)s and individual 401(k)s can help you save considerably more for retirement than just IRAs if you’re self-employed or own a small business.

Both the employee and employer contribution limits are astronomical ($58,000 in 2022), and you don’t need a traditional employer or “boss” to open this account.

Solo 401(k)s work precisely as they sound. If you decide to open your own account with an online brokerage firm, you take the initiative to do so. In terms of Solo 401(k) brokerage firms, there are many to choose from online.

So far, so good. What was the financial blunder?

Well, I came across a solo 401(k) when I co-founded my own investment firm. I had a SEP IRA at the time, But I wanted to save more. So, a Solo 401(k) was appealing to me — especially as a business retirement plan.

Along my journey, I eventually ended up on a sales call. And, to be honest, the pitch was incredible. They told me that if I invested $8,000, they would give me all the proper training so that I could sell this plan to other entrepreneurs. If I sold a couple, I would easily get my money back.

How many did I sell? Zero.

I’m blaming this company completely. I was just in way over my head because I didn’t know how much work would be involved. And I should have that question from the get-go.

4. Investing in Sports Cards

Sports Cards

This next one is more recent and a little more personal since my kid’s here into this. And that’s sports cards.

We used to call these baseball cards in the day regardless of the sport. However, today, they’re known as sports cards. And they blew up during the pandemic.

For example, after the tragic passing of Kobe Bryant, the price of his cards spiked. Then, a documentary came out that was similar to the “Last Dance.” So, people were speculating that just like Micheal Jordan, the value of Kobe Bryant cards would soar.

Guess what? I bought into the speculation and dropped a grand on a Kobe rookie card. Today, I can buy that same card for $250 or $300.

Where it gets really bad is that I purchased a lot of rookies for players like Keven Durant and Zion Williamson. And the prices have all plummeted. I might even go as far as to say that I spent more on sports cards than the Solo 401(k).

Buying and holding. This is the traditional way to make money with all types of investments. In this case, you can buy Bitcoin on a site like Coinbase and park it.

Earning interest. Cryptocurrency savings accounts, or stable coins, allow you to earn interest. BlockFi offers attractive yields.

Trading. Unless you’re a trader who monitors this constantly, it’s all based on a hunch. So instead, I would use bots. For example, Grid trading involves placing a bunch of buys and sell orders around a fixed price at predefined intervals.

One of my close friends, who I respect, also joined the podcast and talked a lot about Celsius Network. I am not blaming him in any way for what happened. I’m a grown man, after all. However, I didn’t have to go to Celsius Network. Despite that, I appreciated what he had to say.

I ended up transferring a large amount of my cryptocurrency after conducting my own research. When I transferred it, I think there was some Bitcoin and Ethereum, and perhaps Cardano. In any case, Bitcoin was trading between $40 and $60 dollars at the time. It is currently trading at around $20 as of the date of this article.

Look, the crypto market is volatile. That’s the risk you take. But, it’s what specifically happened to Celsius Network where I suffered the most amount of losses.

In case you weren’t aware, Celsius Network filed for bankruptcy. This means that any money I had at Celsius Network is now worthless.

The case is currently in claims court. I may be able to get some of it back from the bankruptcy proceeding. But I’m not holding my breath.

Considering its peak, I should probably have looked this up. The price, however, was over $200. Everything has gone downhill since then, as you all know. Let’s say Bitcoin was $60, and then it went to $220, but now it’s down to 20. If you take a third of that, I have only lost about seventy thousand dollars. I only say that because many others invested much more than I did. Or they invested a more significant portion of their net worth in Celsius Network.

The lesson? Beware of the new shiny object, like investing in Celsius Network.

6. Bad Business Partnership

There’s always risk involved when starting your own business. The most common examples include financial hurdles, ineffective business planning, inadequate management, and marketing disasters.

But, if you start a business with someone else, this is another risk you should be aware of. Unfortunately, I learned this the hard way.

Initially, the partnership was fruitful. It propelled growth and generated more income than I ever imagined I could earn from my blog and online business. And I’ll always be grateful for that.

However, after a stretch of self-discovery, I realized that this partnership contributed to my stress and anxiety. And, even though it took a while, I needed to sever ties with this partner.

If I had to guess, ending this partnership, cost me between $2-$4 million in recurring income. That far exceeds the other ways that I’ve lost money.

Thankfully, I have more than enough income to support my family. And I do have multiple sources of income. But, still, that’s a serious hit.

Enterprise Products Partners (NYSE: EPD) has recently been on a wild ride. It has gone thru some stunning peaks and troughs and ended up 7.82% year to date. As a result, investors might wonder if its current stock price represents a good entry for buying shares.

So let’s examine the bull and bear case for investing in EPD to see if we can piece together its valuation.

The Bull Case

Wall Street’s opinion on a given stock is a good starting point when investigating if it’s potentially undervalued. According to the MarketBeatconsensus price target of $30.50, EPD has a 24.95% potential upside. In addition, eleven analysts rated the stock and came to the consensus that it was a moderate buy.

Other aspects of EPD’s fundamentals are also substantial, including the fact that some of its insiders have been buying shares and its low short-interest ratio. Insiders bought $248,000 worth of shares last quarter, and it has a short-interest ratio of 1.63%.

Then there’s EPD’s macro backdrop, which has improved substantially since the war in Ukraine began and crucially due to Russia’s termination of its Nord Stream 1 output to Europe. In July, the International Monetary Fund (IMF) wrote that Russia’s stoppage of natural gas to this region means that Europe’s economic output could fall by as much as 6 percent.

This means that alternative hydrocarbon suppliers such as EPD are poised to see an increase in demand in the region to help make up for the shortfall. And as geopolitical tensions between Russia, China, and NATO countries continue to escalate, western-aligned energy companies are likely to benefit from favoritism as a strong tailwind.

The Bear Case

Some weaknesses in EPD’s fundamentals and backdrop should be explored.

The first is its dividend, often cited as one of its main draw cards for buying the stock. EPD has increased its dividend for 24 consecutive years and is on track to become a dividend aristocrat.

However, the problem lies in its dividend coverage ratio, which currently stands at 81.90%. This means the company is paying out a considerable sum and proportion of its net income in dividends to shareholders, which is likely unsustainable under normal business conditions.

EPD may reduce its dividend within the next few years, thus ending its dividend growth streak. However, a plausible thesis is that the company will redirect some of its earnings on dividends into scaling its capital expenditure, which could lead to greater returns to shareholders later. This would mean EPD could further tap into a couple of opportunities, including the gas shortage in Europe.

Another catalyst is the world’s energy transition to renewables, which will be facilitated first through a rise in demand for hydrocarbon products. These are solid reasons for EPD to consider diverting its spending to infrastructure due to a quickly rising total addressable market for its output.

The final reason is that natural gas does not fit into the renewable energy paradigm and will eventually be replaced by cleaner and more efficient energy sources, such as green hydrogen and nuclear fusion. This means that while natural gas stocks like EPD may rise over the next decade, they provide only a transitory solution to reducing carbon emissions. Their preference may quickly wear off as better energy technologies are developed further.

The question then is one potential upside over the long-term and opportunity cost. In other words, are investors better off paying a premium for natural gas stocks to possibly receive a faster return, or do they invest where the energy market is ultimately heading at a lower price?

Uranium stocks, for instance, have lower valuation ratios on the whole than natural gas stocks, and hydrogen stocks can also be scooped up at a relative bargain. Investors waiting on these decades-long timeframes for hydrogen and uranium stocks to take off also take on more risk, which always is a factor to consider.

The Bottom Line

EPD has the momentum to continue its rally over the short term, and over the medium time frame, it will benefit from a couple of solid catalysts in its macro backdrop. However, investors should also consider their investment horizons and risk tolerance, as natural gas is not the intended solution for the world’s energy needs. There are less expensive stocks to buy that fit this solution which may have a more significant (as well as more speculative) upside potential than gas stocks like EPD.

Latin American e-commerce specialist MercadoLibre Inc. (NASDAQ: MELI) has only trended lower in 2022, and a new partnership could boost the stock.

Earlier this month, the chief financial officer of the Argentina-based company told Reuters that MercadoLibre would begin processing business payments for WhatsApp users.

WhatsApp, owned by Meta Platforms Inc. (NASDAQ: META), offers free multiplatform messaging capabilities. Not well known in the U.S., but it’s popular worldwide among family members, friends, and business associates who live in different countries.

While users have long had access to functionality, including making text messaging and voice and video calls, payment processing would be a new feature.

MercadoLibre CFO Pedro Arnt told Reuters that the two companies are testing payment processing in Brazil. “This could be an opportunity for us to leverage WhatsApp efficiently to generate more sales and better customer contacts,” Arnt said.

“Seamless Checkout Experience”

In a company blog post, WhatsApp addressed the Brazil initiative, saying, “Ultimately, we want people to be able to make a secure payment right from a chat with their credit or debit card. We recently launched this experience in India, and we’re excited to test this in Brazil with multiple payment partners. This seamless checkout experience will be a game-changer for people and businesses looking to buy and sell on WhatsApp without having to go to a website, open another app or pay in person.”

WhatsApp has been offering in-app payments in India since 2020. The Brazil test began in November.

The company has expanded its operational capabilities in the years since and now includes a lending unit and in-house shipping operations. It also runs an advertising platform that provides classifieds, which allows users to list users to vehicles, vessels, aircraft, real estate, and services outside the Marketplace platform.

MercadoLibre reported having more than 88 million unique users in the most recent quarter, with operations in 18 countries.

Strong Earnings And Revenue Growth

Despite this year’s poor stock price performance, sales and earnings growth have been vital in recent quarters. MarketBeat analyst data for MercadoLibre show a “moderate-buy” rating on the stock, with a price target of $1,317, representing a potential upside of 51.27%. A trend line connecting a series of recent price lows illustrates how that price may be reachable by mid-2023.

Since the company’s most recent earnings report on November 3, Citigroup lowered its price target from $1,150 to $1,050. Nonetheless, that still reflects optimism about a potential upside of 23.34%.

MercadoLibre’s three-year revenue growth rate is 74%. Sales increased between 45% and 111% in the past eight quarters.

The bottom line has been more erratic, with losses in 2018, 2019, and 2020. Last year, the company returned to profitability, earning $1.67 per share. This year, analysts expect the company to earn $8.47 per share, an increase of 407%, and projected to rise another 63% next year to $13.78 per share.

That figure has been revised higher recently, but not necessarily because analysts have weighed in on the potential of the WhatsApp partnership.

Missed Earnings Views

Earnings data compiled by MarketBeat show MercadoLibre missing bottom-line views in the past three quarters. In addition, it missed top-line views in one of those quarters.

MercadoLibre’s chart shows a first-stage base that began in mid-August. It’s corrected 31% thus far, although it’s working on its fifth week in a row of declines. The stock is down 10.69% in the past month and 7.76% in the past three months.

So far, the stock is holding above its previous low of $600.68 in mid-June. However, as of mid-session Wednesday, shares were trading below short- and longer-term moving averages. That means the stock still needs to stage a rally that could make it a less risky investment candidate.

Generally, it’s better to focus on stocks beginning a rally rather than being mired in a correction.

U.S. mid-cap stocks are on pace to outperform their large-cap peers for the second straight year. The S&P 400 is down 13% year-to-date, a roughly 400 basis points edge over the S&P 500.

Mid-cap land has long been regarded as the ‘sweet spot’ for equity investors. Companies are fairly well-established in their respective markets but often have more room for growth than mature large caps. With mega caps out of favor in 2022, investors are discovering winners a bit further down the capitalization spectrum.

Another explanation for the return disparity is relative sector weightings. Technology dominates the S&P 500 with a 26% weight, double that of the S&P 400. The Industrial sector makes up the biggest portion of the mid-cap index at 19% but is just 8% of the large cap index. Tech is this year’s worst-performing group. Industrials have held up well and trail only the vastly outperforming Energy sector.

At the individual stock level, only one S&P 500 component has doubled year-to-date, that being Warren Buffet pick Occidental Petroleum. Ditto for the S&P 400 where oil & gas refiner PBF Energy quadrupled before a sharp pullback.

Whether or not mid-caps outperform again in 2023 is anyone’s guess. What’s more certain is the classic risk-reward tradeoff — smaller-sized companies generally have greater return potential. Devoting more resources to mid-caps comes with increased risk but could help a portfolio recover faster.

Here are three mid-caps Wall Street sees as two-baggers over the next 12 months.

What is the Outlook for Intellia Therapeutics?

Intellia Therapeutics, Inc. (NASDAQ: NTLA) develops therapies based on the widely followed CRISPR-Cas9 genome editing technology. It has several in vivo and ex vivo programs for the treatment of lung disease, liver disease, cancer, and other indications. Intellia’s most promising candidate is NTLA-2001, which is being co-developed with Regeneron Pharmaceuticals as a therapeutic for ATTR amyloidosis.

Absent any commercialized products, Intellia’s revenue is limited and its losses are steep — but Wall Street sees an inflection point ahead. The pipeline is progressing well and an investigational new drug (IND) application is expected to be filed next year to launch clinical studies on a lung disease candidate. The potential for marketed products is at least a few years away but clinical success could be a major catalyst.

Analysts remain wildly bullish on Intellia as it slips to a new 52-week low. A $100 average price target equates to over 150% upside.

Will Traders Lift Lyft in 2023?

Lyft, Inc. (NASDAQ: LYFT) continues to find support from the Street, and it makes sense. The ridesharing company has generated 30% higher revenue year-to-date and recovered from steep pandemic losses to book six straight profitable quarters. And yet the stock is down more than 70% this year.

Despite the financial recovery, Lyft faces plenty of challenges. Ridership remains below pre-Covid levels and an impending economic downturn points to fewer nights out on the town and demand for a lift. The company laid off another 700 employees last month as it braces for a challenging 2023.

Still, the long-term outlook is positive and that’s why sell-side analysts see Lyft trading near an all-time low as an opportunity. Price targets are all over the map but the average of $22 would be a 100% return from here.

The prevailing thesis is that current challenges will subside and lend way to an early-stage secular trend towards on-demand, cash-free transportation via car, scooter, or bike. Volatile gas prices and expensive repairs along with a craving for convenience are expected to shift consumers away from car ownership to transportation-as-a-service (TaaS). In turn, a lot of money could shift from car dealers to ride-hailing apps. It is a long road ahead for Lyft, but growth investors may want to come along for the ride.

Does Samsara Stock Have Good Upside?

Samsara Inc. (NYSE: IOT) is an Internet-of-Things (IoT) company that picked the wrong time to go public. It is the creator of the Connected Operations Cloud which helps businesses gain actionable insights and improve operations based on IoT data. The Street is mostly bullish on the $13 stock in thinking it can return to its December 2021 IPO levels in the mid-$20.

Samsara is focused on video-based safety solutions for the transportation industry that detect things like driver cell phone usage and lack of seatbelt usage. Together with telematics and AI-powered video search, its subscription-based products generate strong recurring revenue.

On account of its 2,828% three-year revenue growth, Deloitte recently named Samsara one of the fastest-growing technology companies in North America. It is coming off a beat and raise quarter that showed end market demand is sturdy despite the macro weakness.

Not all enterprise SaaS companies are holding up this well, nor are they moving closer to profitability as Samsara is. Management is projecting 49% top-line growth this year and a narrower net loss. If this under-the-radar IoT play can deliver these kinds of results in a weakened economy, the future is surely bright.

Opinions expressed by Entrepreneur contributors are their own.

A nonqualified deferred compensation (NQDC) plan is a great way for employers to attract and retain key talent. It also represents a potentially massive tax savings opportunity for highly compensated employees. There is a lot that you need to know about these plans before deciding to participate in one, however. So, let’s get into the basics.

A nonqualified deferred compensation (NQDC) plan allows employees to earn their pay, potential bonuses and other forms of compensation in one year but receive those earnings in a future year. This also defers the income tax on the compensation. It helps provide income for the future, and there’s a possibility for a reduced amount of income tax payable if the employee is in a lower tax bracket at the time of the deferred payment.

It’s worth noting that tax law requires these NQDC plans to be in writing. There needs to be documentation about the amount being paid, the payment schedule and what the future triggering event will be for compensation to be paid out. There also needs to be an assertion from the employee of their intent to defer the compensation beyond the year.

A NQDC plan is a contractual fringe benefit often included as part of an overall compensation package for key executives. It can serve as an important supplement to traditional retirement savings tools, such as individual retirement accounts — IRA and 401(k) plans.

Like a 401(k), you can defer compensation into the plan, defer taxes on any earnings until you make withdrawals in the future and designate beneficiaries. Unlike a 401(k) plan or traditional IRA, there are no contribution limits for an NQDC — although your employer can set its own limits. Therefore, you can potentially defer up to all your annual bonuses to supplement your retirement. We have seen companies allow you to defer as much as 25-50% of your base salary as well.

Employers: Take note

NQDC plans carry some benefits for employers as well. The plans are a low-cost endeavor. After initial legal and accounting fees, there are no annual payments required. There are no unnecessary filings with government agencies like the Internal Revenue Service.

Since the plans are not qualified, they are not covered under the Employee Retirement Income Security Act (ERISA). This provides a greater amount of flexibility for both employers and employees. Employers can offer NQDC plans to select executives and employees who would benefit the most from them.

Companies can customize plans toward valued members of their workforce, creating incentives for these employees to remain with the company. For example, an employee’s deferred benefits could be rendered forfeit if said employee decides to leave the company before retirement. We call this strategy a “golden handcuffs” approach.

For highly compensated employees, social security and 401(k) can only replace so much of your income in retirement. You could potentially build up the bulk of your retirement savings with your NQDC plan. There’s also the bonus of reducing your annual taxable income by deferring your compensation. This brings into play the idea of being in a lower tax bracket, decreasing the amount of taxes you would need to pay. Many employers even incentivize this, offering a match of some kind.

Timing of payment

The timing of when you take NQDC distributions is important since you’ll need to project your potential cash flow needs and tax liabilities far into the future.

Deferred compensation plans require you to make an upfront election of when you will receive the funds. For example, you might time the payments to come at retirement or when a child is entering college. In addition, the funds could come all at once or in a series of payments. There is tremendous flexibility often in these plans.

Taking a lump-sum payment gives you immediate access to your money upon the distributable event (often retirement or separation of service). While you will be free to invest or spend the money as you wish, you will owe regular income taxes on the entire lump sum and lose the benefit of tax-deferred compounding. If you elect to take the money in installments, the remainder can continue to grow tax-deferred, and you’ll spread out your tax bill over several years.

An NQDC plan does come with some risks. When you participate in a qualified plan, your assets are segregated from company assets, and 100% of your contributions belong to you. Because a Section 409A plan is nonqualified, your assets are tied to your employer’s general assets. In case of bankruptcy, employees with deferrals become unsecured creditors of the company and must line up behind secured creditors in the hopes of getting paid.

Thus, you should consider how much of your wealth — including salary, bonus, stock options and restricted stock — is already tied to the future health and success of one company. Adding deferred compensation exposure may cause you to take on more risk than is appropriate for your personal situation.

Before you choose to participate in an NQDC plan, you should speak with both your financial advisor and your tax professional. You really want to model out how and when you will receive these disbursements. Ideally, you are planning with enough foresight that you will offset this income tax event in retirement with withdrawals from a brokerage account or a Roth IRA or 401(k). You will also want to pay attention to the impact of high income with the taxation of Medicare Part B — if you think there are a lot of moving parts here, you are right! When executed properly, you can truly develop a unique plan that is customized to your exact living situation and future goals.

Any discussion of taxes is for general informational purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax or accounting advice. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

Inflation eased again in November, which could allow the Fed to slow interest-rate hikes into the following year. Overall, the odds of the economy avoiding an anticipated recession are increasing. Given this backdrop, quality stocks CVS Health (CVS), ADT (ADT), ODP Corporation (ODP), and Universal Logistics (ULH) will likely see further upside next year. Read on….

shutterstock.com – StockNews

This year, the stock market has seen significant volatility due to record-high inflation, the Russia-Ukraine war, and the Fed hiking interest rates at a pace not seen in decades. However, inflation cooled notably last month and is at its lowest since December 2021.

The Labor Department yesterday reported that the Consumer Price Index (CPI) increased 7.1% from a year ago in November, lower than economists’ expectations of 7.3%. The moderation in inflation made investors optimistic about the central bank’s future course of action on the policy front.

“Cooling inflation will boost the markets and take pressure off the Fed for raising rates, but most importantly this spells real relief starting for Americans whose finances have been punished by higher prices,” said Robert Frick, corporate economist with Navy Federal Credit Union.

A weaker-than-expected CPI report combined with favorable data on jobs and income is increasing hopes that the economy could avoid an anticipated recession next year or suffer a mild downturn. Moody’s Analytics chief economist Mark Zandi is confident that the U.S. economy will narrowly avoid a recession, citing the recent favorable economic and market indicators.

According to Gagnon of the Peterson Institute of International Economics, the chances of a soft landing are between 50% and 60%, including the possibility of a “very, very mild recession.”

Given the backdrop, we think it could be wise to invest in fundamentally sound stocks CVS Health Corporation (CVS), ADT Inc. (ADT), The ODP Corporation (ODP), and Universal Logistics Holdings, Inc. (ULH) that have more room to run next year.

CVS provides health services in the United States. The company operates through three segments: Health Care Benefits; Pharmacy Services; and Retail/LTC. It operates more than 9,900 retail locations and 1,200 MinuteClinic locations, online retail pharmacy websites, LTC pharmacies, and onsite pharmacies.

On December 1, CVS opened its first MinuteClinic locations in northern Delaware. MinuteClinic, the medical clinics inside select CVS Pharmacy stores, offers high-quality, affordable, and convenient care for various acute and chronic conditions for patients ages 18 months and older.

On September 5, CVS entered a definitive agreement with Signify Health (SGFY) to acquire Signify Health.

CVS Health President and CEO Karen S. Lynch said, “This acquisition will enhance our connection to consumers in the home and enables providers to address patient needs better as we execute our vision to redefine the healthcare experience. In addition, this combination will strengthen our ability to expand and develop new product offerings in a multi-payor approach.”

For the fiscal 2022 third quarter ended September 30, 2022, CVS’ total revenues increased 10% year-over-year to $81.16 billion. Its adjusted operating income increased by 3.9% from the prior-year period to $4.23 billion. In addition, the company’s adjusted earnings per share came in at $2.09, up 6.1% year-over-year.

Over the past three years, CVS’ revenue and EBIT have grown at CAGRs of 8.9% and 7.2%, respectively.

Analysts expect CVS’ revenue and EPS for the current fiscal year (ending December 2022) to increase 7.7% and 2.6% from the prior year to $314.49 billion and $8.62, respectively. The company’s revenue and EPS for the next year are expected to grow 3.4% and 2.7% year-over-year to $325.26 billion and $8.86, respectively.

Furthermore, the company has surpassed the consensus revenue and EPS estimates in each of the trailing four quarters. Over the past month, the stock has gained 2.7% and 11.3% over the past six months to close the last trading session at $101.19.

CVS’ strong fundamentals are reflected in its POWR Ratings. The stock has an overall rating of A, which translates to a Strong Buy in our proprietary rating system. The POWR ratings assess stocks by 118 different factors, each with its own weighting.

CVS has an A grade for Growth and a B for Stability and Sentiment. It is ranked first out of 4 stocks in the B-rated Medical – Drug Stores industry.

We have also given CVS grades for Value, Momentum, and Quality. Get all the CVS ratings here.

ADT provides security, interactive, and innovative home solutions to serve residential, small business, and commercial customers in the United States. Its segments include Consumer and Small Business (CSB); Commercial; and ADT Solar business (Solar). The company operates through a network of nearly 250 sales and service offices and three regional distribution centers.

On September 6, ADT announced its partnership with State Farm. State Farm will make a $1.2 billion equity investment in ADT, resulting in State Farm owning approximately 15% of ADT. Additionally, ADT plans to partner with State Farm and build upon its existing relationship with Alphabet (GOOG) (GOOGL), with the latter agreeing to commit an additional $150 million to support this opportunity.

In August, ADT announced its partnership with Uber Technologies, Inc. (UBER) to integrate ADT mobile safety solutions into the Uber app for riders and drivers in the United States to get live help, via phone or text, from ADT professional monitoring agents. This marks yet another addition to ADT’s growing Clientele that utilizes Safe by ADT to power their app-based mobile safety features.

For the third quarter of the fiscal year 2022 ended September 30, ADT’s total revenue increased 21.8% year-over-year to $1.60 billion, while the company’s adjusted EBITDA grew 11.9% year-over-year to $620 million. The company reported an adjusted net income of $83 million or $0.10 per share, compared to an adjusted net loss of $54 million or $0.07 per share in the previous-year quarter.

ADT’s revenue and EBIT have grown at CAGRs of 6.9% and 18%, respectively, over the past three years.

Analysts expect ADT’s revenue for the fiscal year ending December 2022 to increase 20% year-over-year to $6.37 billion. The company’s EPS for the current year is expected to come in at $0.51, compared to a loss of $0.25 per share during the previous year. Moreover, ADT’s EPS is expected to grow by 3.9% per annum over the next five years.

Shares of ADT have gained 7.1% over the past month and 20.5% over the past year to close the last trading session at $9.83.

ADT’s POWR Ratings reflect its bright prospects. The stock has an overall rating of B, translating to a Buy in our proprietary rating system. It has an A grade for Growth and Sentiment and a B for Stability.

ADT is ranked #5 of 60 stocks in the Home Improvement & Goods industry. Click here to see the additional ratings of ADT for Value, Momentum, and Quality.

ODP is an office supply holding company that offers business services, products, and digital workplace technology solutions through an integrated business-to-business distribution platform and omnichannel presence. It serves small, medium, and enterprise businesses. The company operates through two segments: Business Solutions and Retail.

In August, Office Depot, a wholly owned subsidiary of ODP and Uber Technologies, Inc., teamed up to bring business, office, and school essentials to customers nationwide. Office Depot is the first business solutions and office supply retailer to be available on Uber Eats. This partnership might boost the company’s revenue streams and extend its market reach.

For the fiscal 2022 third quarter ended September 24, 2022, ODP’s reported sales from ODP Business Solutions Division increased 9% year-over-year to $1 billion as more business customers returned to the workplace. Its earnings per share from continuing operations came in at $1.36, up 2.3% year-over-year. Operating cash inflows from continuing operations grew 34.7% year-over-year to $163 million.

Furthermore, the company’s adjusted free cash flow came in at $160 million, up 30.1% year-over-year.

ODP’s EPS has grown at an 85.4% CAGR over the past three years. Moreover, its total assets have increased at a CAGR of 7.6% over the same period.

The consensus revenue estimate of $2.14 billion for the fourth quarter of fiscal 2022 (ending December 31, 2022) indicates a 4.6% year-over-year improvement. Also, analysts expect the company’s EPS to grow 10.7% year-over-year to $0.79. The company has topped the consensus EPS estimates in three of the trailing four quarters.

The stock has gained 26% over the past six months and 22.1% over the past year to close its last trading session at $46.11.

ODP’s solid fundamentals and promising outlook is reflected in its POWR Ratings. The stock has an overall rating of A, equating to a Strong Buy in our proprietary rating system.

ODP has a grade of A for Growth and Quality and a B for Value. In the 47-stock Specialty Retailers industry, it is ranked #1.

Click here to access the additional POWR Ratings for ODP (Stability, Momentum, and Sentiment).

ULH provides transportation and logistics solutions in the United States, Mexico, Canada, and Colombia. It offers truckload services; domestic and international freight forwarding, customs brokerage services; and final mile and ground expedite services.

For the fiscal third quarter ended October 1, 2022, ULH’s total operating revenues increased 13.5% year-over-year to $505.69 million. The company’s income from operations came in at $69.77 million, up 317.4% year-over-year. Its non-GAAP EBITDA was $84.40 million, compared to $33.10 million in the prior year’s quarter.

In addition, the company’s net income increased 371.9% year-over-year to $48.48 million, while its EPS came in at $1.84, representing a 384.2% increase from the prior-year quarter.

ULH’s revenue and EBIT have grown at CAGRs of 4.9% and 8.1%, respectively, over the past three years. Its EPS has improved at a 6.5% CAGR over the same period.

Analysts expect ULH’s EPS for the fiscal year (ending December 2022) to come in at $6.40, indicating a 90.3% year-over-year increase. The consensus revenue estimate of $2.02 billion for the ongoing year represents a 15.4% year-over-year rise. The company has an impressive earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters.

The stock has gained 92.3% year-to-date and 103.3% over the past year to close the last trading session at $35.98.

ULH’s POWR Ratings reflect this positive outlook. The stock has an overall rating of A, translating to a Strong Buy in our proprietary rating system.

ULH has a grade A for Growth. The stock has a grade B for Value, Momentum, Stability, and Sentiment.

CVS shares were unchanged in premarket trading Wednesday. Year-to-date, CVS has gained 0.30%, versus a -14.39% rise in the benchmark S&P 500 index during the same period.

About the Author: Mangeet Kaur Bouns

Mangeet’s keen interest in the stock market led her to become an investment researcher and financial journalist. Using her fundamental approach to analyzing stocks, Mangeet’s looks to help retail investors understand the underlying factors before making investment decisions.

Bulls had to slow their roll on Tuesday as the immediate +3.5% rally was shaved by 80% into the close. Why did the rally fritter away? And what does it mean next for the stock market (SPY) going forward? 40 year veteran Steve Reitmeister shares his timely market outlook, trading plan and 8 top picks to generate gains in the weeks ahead.

shutterstock.com – StockNews

It felt like every trader on earth hit the buy button at 8:30am ET Tuesday morning as the softer than expected CPI report came out. This led to a shocking +3.5% surge in stock futures. If that held up it would have put the S&P 500 all the way up at 4,130.

But that didn’t hold up…neither did the recent high of 4,100…neither did the 200 day moving average at 4033…instead stocks only closed up modestly higher at 4,019.

Why did the rally fritter away? And what does it mean next for the bull/bear battle going forward?

That will be the focus of this week’s Reitmeister Total Return commentary.

Market Commentary

First, and foremost a reminder to watch my “2023 Stock Market Outlook” if you have not already. That’s because it covers the following vital topics:

Why 2023 is a “Jekyll & Hyde” year for stocks

5 Warnings Signs the Bear Returns in Early 2023

8 Trades to Profit on the Way Down

Plan to Bottom Fish @ Market Bottom

2 Trades with 100%+ Upside Potential as New Bull Emerges

The above outlook provides an important backdrop in which to discuss all new information including the CPI report from Tuesday morning. Assuming you have watched it already…then let’s pick up the story from there.

Yes, the Consumer Price Index (CPI) came in softer than expected this morning (7.1% yearly increase vs. 7.3% expected). And yes, this softer than expected trend is happening more and more often.

Now the wakeup call.

7.1% is not the same as 2% target (for those with who did poorly in math class).

Also the Producer Price Index last week was higher than expected. And that is the leading indicator of where CPI will be in the future. That’s because these are the input prices for manufactures and service providers which shows up in their offerings down the road. Meaning this softer than expected read may give way to higher readings in the future given the foreshadowing in PPI.

On top of that many of the forms of “sticky” inflation remain, well…STICKY.

Things like wages and rents are still too hot. The former issue of high wage inflation was on display in the 2X higher than expected monthly increase for wages found in the Government Employment Situation report back on 12/5…and helped spark a 4% selloff the following week.

Think of it this way…CPI looks backwards and PPI looks forward. So which is more important? (he asks rhetorically).

Yes, PPI. And that is telling you quite clearly that problem of high inflation is far from solved.

I sense that as the early morning excitement wore off, and investors sobered up, they began to realize that it was a bit too early to celebrate the death of inflation. And perhaps they need to wait to see what the Fed says Wednesday afternoon.

That’s because inflation is like a horror movie monster. You can’t just shoot it once and assume it’s dead. It will keep getting up each time you think the job is done and the death defying chase resumes.

In fact, Powell has discussed this many times over that the worst thing they can do is take their foot of the brakes too soon and inflation comes back with a vengeance. Inflation needs to be “dead and buried” before the Fed reverses course with lower rates.

As great proof of that notice how every time that we have one of these big stock rallies on news of softening inflation that commodity prices soar…which yes, speaks to inflation rising once again. The exact problem we are trying to solve.

Here was the early morning read for energy and key commodities as stock futures soared:

Long story short, the Fed has splashed cold water on exuberant traders several times this year. Thus, it pays to see what happens with the rate hike and announcement on Wednesday afternoon.

50 basis points is the expectation. The real key is the “dot plot” of where rates likely go in the future (how high…for how long) along with any statements they make that foreshadows future plans.

There we will find out if the Fed agrees with traders that inflation is moderating nicely and they do not have to be as hawkish for as long as previously expected. On the other hand, they may state quite clearly that they continue to see inflation as being more sticky and persistent than they would like, keeping them on the job much longer…with more pain to the economy…and likely lower stock prices.

The answer to that tells you whether stocks are truly ready to break out above the all important 200 day moving average (4,033). Or if it is time to head lower once again?

However, we are getting foolishly sucked into the investing worlds myopic fixation on inflation and the Fed. There is much more going on…like the health of the overall economy that is moving closer and closer still to recession. That was the central theme of my 2023 Stock Market Outlook presentation from last week with several leading indicators pointing in that darkening direction.

A prime example of this recessionary concern was on full display Tuesday morning from another low reading for the NFIB Small Business Outlook. Here is the key statement from their report:

“…most of the readings were still consistent with a recession and weak economic activity.”

So as the recessionary storm clouds keep circling…and inflation is far from dead…with the Fed still to keep their foot firmly on the brakes with higher rates on the way …then I see no wisdom in chasing this rally as stocks going down over the next 3-6 months makes a lot more sense then new bull market emerging now.

The only thing at this moment to change my mind is a clear Fed pivot on Wednesday to say indeed inflation is coming under control and they do not need to be as Hawkish as previously advertised.

This is possible…but highly improbable given the slew of statements that have made in the recent past. And that we have already seen the data they are looking at which includes too hot readings for PPI and wage inflation. And the nature they are slow and deliberate. Added altogether and it would be the shock of shocks for them to say “Mission Accomplished” on Wednesday.

Worst case scenario is another 2-3% upside into year end thanks to current momentum plus bullish bias of Santa Claus rally.

On the other hand, if still a bear market…which is the base case…then retreating to the previous lows of 3,491 in the New Years is still in the cards. And likely much lower.

What To Do Next?

Watch my brand new presentation: “2023 Stock Market Outlook” covering:

Why 2023 is a “Jekyll & Hyde” year for stocks

5 Warnings Signs the Bear Returns in Early 2023

8 Trades to Profit on the Way Down

Plan to Bottom Fish @ Market Bottom

2 Trades with 100%+ Upside Potential as New Bull Emerges

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.22 (-0.05%) in after-hours trading Tuesday. Year-to-date, SPY has declined -14.39%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The stock rocketed to an eight-month high Monday, advancing as much as 191% intraday before settling down to a gain of 22.61%. Shares closed at $1.41 Monday, up $0.26. Tuesday, the stock closed lower after gapping down at the open.

Monday’s huge upside action followed the company’s release of updated interim results for its myeloma drug that’s in Phase 1 clinical trials. The treatment is currently known as HPN217.

According to Harpoon’s news release, “The interim results, as of the data cut-off date of October 17, 2022, showed that HPN217 demonstrated continued evidence of clinical activity and a tolerable safety profile in heavily pre-treated patients” with relapsed/refractory multiple myeloma.

Relapsed/refractory multiple myeloma occurs when a patient has received treatment for a cancer called multiple myeloma, a rare cancer that affects bone marrow. It’s currently incurable, with the most common path being remission interspersed with periods when the disease becomes active. It’s termed relapsed/refractory multiple myeloma when the patient’s condition is especially difficult to treat.

Meaningful Clinical Benefits

“The encouraging initial clinical activity with deepening and durable responses observed in patients who have received multiple prior lines of therapy, combined with a generally well-tolerated safety profile, suggest the investigational T cell engager HPN217 may offer meaningful clinical benefits for patients with relapsed/refractory multiple myeloma,” said Al-Ola A. Abdallah, a doctor at the University of Kansas Medical Center, a principal investigator in the study.

“I look forward to continuing to study this promising drug candidate in these patients with advanced disease for whom there remains a significant unmet need for new treatment options,” Abdallah added.

Remarks like those gave investors hope.

San Francisco-based Harpoon went public in February 2019 at $14. The stock essentially meandered sideways until June of last year, when shares began declining.