Growth stocks may stage a recovery as interest rate hikes might slow, and the economy might achieve a soft landing. Moreover, a market rebound seems to be in the cards in 2023. Therefore, fundamentally strong growth stocks CVS Health (CVS) and General Motors (GM) could be solid buys now. Keep reading….

shutterstock.com – StockNews

At a recent policy meet, the Federal Reserve’s officials agreed that the central bank should slow the rate hikes. Officials also acknowledged that they had made significant progress in their fight against the multi-decade high inflation.

Fundstrat’s head of research, Tom Lee, said, “Stocks are 5X more likely to rise 20% than be flat, and more than half of the instances are over 20% gains.”

Given the backdrop, investors could consider buying fundamentally strong growth stocks CVS Health Corporation (CVS) and General Motors Company (GM), which look poised to deliver solid returns ahead.

CVS provides health services in the United States. The company operates through three segments: Health Care Benefits; Pharmacy Services; and Retail/LTC. It operates retail locations, online retail pharmacy websites, LTC pharmacies, and onsite pharmacies.

On December 1, CVS opened its first MinuteClinic locations in northern Delaware. MinuteClinic, the medical clinics inside select CVS Pharmacy stores, provides low-cost care for acute and chronic diseases to people 18 months and older. The company is continuing to expand its footprint, which should help strengthen its position in the industry.

CVS’ revenue has increased at a CAGR of 8.9% over the past three years, while its EBIT has increased at a 7.2% CAGR.

CVS has paid dividends for 14 consecutive years. Over the last three years, CVS’s dividend payouts have grown at a 3.2% CAGR. While CVS’s four-year average dividend yield is 2.77%, its current dividend translates to a 2.64% yield.

CVS’ total revenues increased 10% year-over-year to $81.16 billion for the fiscal third quarter that ended September 30, 2022. During the same period, the company’s product revenue increased 11.2% year-over-year to $57.64 billion.

Also, its current assets came in at $68.34 billion for the period ended September 30, 2022, compared to $60.01 billion for the period ended December 31, 2021.

Street expects CVS’ revenue to increase 3.4% year-over-year to $325.6 billion in 2023. Its EPS is expected to increase 2.7% year-over-year to $8.86 in 2023. It surpassed EPS estimates in each of the four trailing quarters. CVS’s stock has gained 3.7% over the past three months to close the last trading session at $91.49.

CVS’ Strong fundamentals are reflected in its POWR Ratings. The stock’s overall A rating represents a Strong Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

CVS has an A grade for Growth and a B grade for Value, Stability, and Sentiment. Within the Medical – Drug Stores industry, it is ranked first among the four stocks.

Beyond what is stated above, we’ve also rated CVS for Momentum and Quality. Get all CVS ratings here.

General Motors Company designs, builds, and sells trucks, crossovers, cars, and automobile parts and accessories worldwide. The company operates through GM North America; GM International; Cruise; and GM Financial segments.

On November 17, 2022, GM and Vale Canada Limited, a subsidiary of Vale S.A. (VALE), signed a long-term supply deal for battery-grade nickel sulfate to improve North American EV supply chains. This agreement is expected to assist GM in meeting its goal of producing one million electric vehicles annually in North America by 2025.

GM’s EBIT has increased at a 13.3% CAGR over the past three years. Also, its net income grew at a 2.6% CAGR over the past three years.

GM’s four-year average dividend yield is 2.10%, and its current dividend translates to a 1% yield.

GM’s total net sales came in at $41.89 billion for the third quarter that ended September 30, 2022, up 56.4% year-over-year. Its adjusted EBIT increased 46.7% year-over-year to $4.28 billion. In addition, its EPS increased 48℅ year-over-year to $2.25.

GM’s revenue is expected to increase by 3.7% year-over-year to $159.85 billion in 2023. Its EPS is expected to grow 15.7% per annum for the next five years. It surpassed EPS estimates in three of four trailing quarters. Over the past six months, the stock has gained 11.2% to close the last trading session at $35.92.

It’s no surprise that GM has an overall B rating, equating to a Buy in our POWR Ratings system. It also has an A grade for Growth and a B for Value and Sentiment.

The stock is ranked #19 out of 62 in the Auto & Vehicle Manufacturers industry. Click here to access the additional POWR Ratings for GM (Stability, Quality, and Momentum).

CVS shares fell $0.29 (-0.32%) in premarket trading Tuesday. Year-to-date, CVS has declined -1.82%, versus a 1.42% rise in the benchmark S&P 500 index during the same period.

About the Author: RashmiKumari

Rashmi is passionate about capital markets, wealth management, and financial regulatory issues, which led her to pursue a career as an investment analyst. With a master’s degree in commerce, she aspires to make complex financial matters understandable for individual investors and help them make appropriate investment decisions.

Saving money is a top priority for many people, and with good reason. It can be challenging to make ends meet, especially if you have a lot of financial obligations or are living on a tight budget. The good news is that there are many different ways to save money, and with a little bit of planning and effort, you can find ways to stretch your budget further and reach your financial goals.

Due – Due

Here are some of the best ways to save money in 2023:

1. Create a budget and stick to it

One of the most effective ways to save money is to create a budget and stick to it. A budget is a plan that outlines how you will allocate your income and expenses. By creating a budget, you can identify areas where you may be overspending and find ways to cut back.

To create a budget, start by listing your income and all of your expenses. This can include everything from your rent or mortgage payment to your groceries and entertainment expenses. Once you have a complete list, subtract your expenses from your income to see how much money you have left over.

If you find that you are spending more than you are earning, you will need to find ways to cut back on your expenses. This might involve cutting back on non-essential expenses, such as dining out or subscription services, or finding ways to save on your essential expenses, such as by negotiating lower rates for your bills or shopping around for better deals on groceries.

Here are 20 quick ways create a budget and stick to it:

Determine your income: To create a budget, you’ll need to know how much money you have coming in each month. This includes your salary, any side income, and any other sources of income.

Identify your expenses: Next, make a list of all your expenses, including your fixed expenses (such as rent or mortgage payments), variable expenses (such as groceries and gas), and discretionary expenses (such as entertainment and dining out).

Compare your income and expenses: Once you have a list of your income and expenses, compare them to see if your income is greater than your expenses. If it is, you’re in good shape. If not, you’ll need to find ways to cut back on your expenses or increase your income.

Set financial goals: Setting financial goals can help you stay motivated to stick to your budget. This might include paying off debt, saving for a down payment on a house, or building up your emergency fund.

Create a budget plan: Based on your income, expenses, and financial goals, create a budget plan that outlines how you’ll allocate your money each month.

Track your spending: To make sure you’re sticking to your budget, track your spending to see where your money is going. This can help you identify areas where you may be overspending and find ways to cut back.

Use cash or a debit card: Using cash or a debit card can help you stick to your budget by making it easier to track your spending and avoid overspending.

Use budgeting apps or tools: There are many budgeting apps and tools available that can help you track your spending and stay on track with your budget.

Automate your budget: Automating your budget can help you stay on track by automatically transferring money into savings or paying bills on time.

Avoid impulse purchases: Impulse purchases can be a major budget-buster, so try to avoid them as much as possible.

Shop around and compare prices: Don’t just go with the first offer you receive for a product or service. Take the time to shop around and compare prices to ensure you are getting the best deal.

Use coupons and discounts: Look for coupons and discounts to save money on your purchases.

Don’t be afraid to negotiate: Don’t be afraid to negotiate for a lower price on products or services.

Avoid high-interest credit cards: High-interest credit cards can make it harder to pay off debt and stick to your budget, so try to avoid them as much as possible.

Avoid unnecessary fees: Fees, such as ATM fees or overdraft fees, can add up quickly and make it harder to stick to your budget. Try to avoid unnecessary fees as much as possible.

Cut back on non-essential expenses: To create a budget that works for you, you’ll need to cut back on non-essential expenses. This might involve canceling subscription services or cutting back on dining out.

Find ways to save on essential expenses: Look for ways to save on your essential expenses, such as shopping around for the best deals on utilities or car insurance.

Use cash-back or rewards credit cards wisely: If you do use a credit card, consider using one that offers cash-back or rewards for your purchases. Just be sure to pay off your balance in full each month to avoid interest charges.

Enlist the help of a financial advisor: If you’re having trouble creating a budget that works for you, consider seeking the help of a financial advisor.

Write down everything you spend: You’ll find that the more you write down, the less you’ll want to spend.

2. Pay off Debt

Another effective way to save money is to pay off your debt. High-interest debt, such as credit card debt, can be especially costly, as the interest charges can add up quickly. By paying off your debt, you can save a significant amount of money in the long run.

To pay off your debt, you can consider a few different strategies. One option is to focus on paying off your highest-interest debt first, as this will save you the most money in the long run. Alternatively, you could try the debt snowball method, which involves paying off your smallest debts first and working your way up to your larger debts. This can be a good strategy if you need to see some quick wins to stay motivated.

You may also want to consider consolidating your debt, which involves taking out a single loan to pay off multiple debts. This can help simplify your payments and potentially reduce your interest charges. Just be sure to compare the terms and fees of different consolidation options before you decide on one.

Here are 20 quick ways to pay off debt fast:

Make a budget: To pay off debt quickly, you’ll need to have a clear plan for how you’ll allocate your income and expenses. Creating a budget can help you identify areas where you may be overspending and find ways to cut back.

Make more than the minimum payment: To pay off debt faster, make more than the minimum payment each month. The more you pay, the faster you’ll be able to pay off your debt.

Pay off your highest-interest debt first: To save the most money in the long run, focus on paying off your highest-interest debt first.

Use the debt snowball method: The debt snowball method involves paying off your smallest debts first and working your way up to your larger debts. This can be a good strategy if you need to see some quick wins to stay motivated.

Consolidate your debt: Consider consolidating your debt by taking out a single loan to pay off multiple debts. This can help simplify your payments and potentially reduce your interest charges.

Transfer your balance to a lower-interest credit card: If you have a high-interest credit card, consider transferring your balance to a card with a lower interest rate to save money on interest charges.

Cut back on expenses: To pay off debt faster, you’ll need to find ways to free up more money in your budget. This might involve cutting back on non-essential expenses or finding ways to save on your essential expenses.

Increase your income: Another way to pay off debt faster is to increase your income. This might involve taking on additional work, starting a side hustle, or negotiating for a raise at your current job.

Sell items you no longer need: Consider selling items you no longer need or use to generate additional income to put towards your debt.

Use windfalls wisely: If you receive a windfall, such as a tax refund or bonus, consider using it to pay off debt instead of spending it on non-essential items.

Consider a debt management plan: A debt management plan can help you pay off your debt faster by consolidating your payments and negotiating lower interest rates with your creditors.

Use the debt avalanche method: The debt avalanche method involves paying off your debts in order of highest interest rate to lowest. This can save you the most money in the long run, but may be less motivating than the debt snowball method.

Seek professional help: If you are having trouble managing your debt on your own, consider seeking professional help from a financial advisor or credit counselor.

Get a part-time job: Taking on a part-time job can provide additional income to put towards your debt.

Rent out a room in your home: If you have an extra room in your home, consider renting it out to generate additional income to put towards your debt.

Use a cash-back or rewards credit card: If you do choose to use a credit card, consider using one that offers cash-back or rewards for your purchases. You can then use the cash back or rewards to help pay off your debt.

Cut back on non-essential expenses: Consider cutting back on non-essential expenses, such as dining out or subscription services, to free up more money in your budget to put towards your debt.

Refinance your loans: If you have high-interest loans, consider refinancing them to a lower interest rate to save money on interest charges.

Get a personal loan: If you have high-interest credit card debt, consider taking out a personal loan at a bank vs loan shark.

Sell blood and Plasma Factoids: Every 56 days, up to 6 times a year you can sell your plasma. It’s not the easiest thing to do but pays well. You will earn between $30 and $60 per donation session.

3. Save on your monthly bills

Another way to save money is to look for ways to lower your monthly bills. This might involve negotiating lower rates for your bills, such as your rent or mortgage payment, or shopping around for better deals on things like your cell phone or internet service.

You can also look for ways to save on your utilities. This might include turning off lights and appliances when they are not in use, using energy-efficient products, and sealing any drafts in your home to reduce your heating and cooling costs.

Here are 20 quick ways to save money on monthly bills:

Shop around and compare prices: Don’t just go with the first offer you receive for a service or product. Take the time to shop around and compare prices from multiple providers to ensure you are getting the best deal.

Negotiate lower rates: Don’t be afraid to negotiate lower rates for your bills. Contact your service providers and ask if they can offer you a better deal.

Switch to a cheaper cell phone plan: If you’re paying a high price for your cell phone plan, consider switching to a cheaper provider or a plan with fewer features.

Shop for a lower rate on your home or car insurance: Insurance rates can vary significantly between different providers, so it’s worth shopping around to find the best deal.

Cut back on your cable or satellite TV service: Do you really need all those channels? Consider canceling your cable or satellite TV service and switching to a streaming service instead.

Use energy-efficient products: Using energy-efficient products can help you save on your monthly utility bills. Look for Energy Star certified products, which are designed to be more energy-efficient.

Use LED light bulbs: LED light bulbs are more energy-efficient and can help you save on your monthly electricity bill.

Unplug appliances and electronics when not in use: Appliances and electronics can still use energy when they are turned off but still plugged in. Unplugging them can help you save on your energy bill.

Lower the temperature on your water heater: Setting your water heater to a lower temperature can help you save on your monthly energy bills.

Install a programmable thermostat: A programmable thermostat can help you save on your monthly energy bills by allowing you to set the temperature to automatically adjust when you are away or asleep.

Check for leaks: Leaks in your home can increase your water bill. Check for leaks and repair them promptly to save money.

Install low-flow showerheads: Low-flow showerheads can help you save on your monthly water bill by using less water.

Don’t leave the water running: Turn off the water when you are not using it, such as while you are brushing your teeth or washing dishes.

Use the dishwasher and washing machine only when full: Running these appliances with a full load can help you save on your monthly water and energy bills.

Shop for a cheaper internet service provider: If you’re paying a high price for your internet service, consider switching to a cheaper provider or a plan with fewer features.

Use public transportation or carpool: If you have a long commute to work, using public transportation or carpooling can help you save on your monthly gas bill.

Walk or bike instead of driving: If you have a short distance to travel, consider walking or biking instead of driving to save on gas.

Buy a fuel-efficient car: If you are in the market for a new car, consider a fuel-efficient model to save on gas costs.

Shop around for a lower rate on your credit card: Credit card rates can vary significantly between different providers, so it’s worth shopping around to find the best deal.

Use cash or a debit card instead of credit cards: Credit cards can be tempting, but they often come with high interest rates. Using cash or a debit card can help you save on interest charges and avoid overspending.

4. Cut back on non-essential expenses

Another way to save money is to cut back on non-essential expenses. This might include things like dining out, subscription services, or expensive hobbies. By cutting back on these types of expenses, you can free up more money in your budget to put towards your financial goals.

Here are 20 quick ways to cut back on non-essential expenses:

Cancel subscription services you don’t use: If you have subscriptions to services you don’t use or need, consider canceling them to save money.

Eat out less: Dining out can be a major expense, so try to eat out less and cook at home instead.

Cut back on non-essential shopping: Avoid making unnecessary purchases and stick to a shopping list when you do shop to avoid overspending.

Cut back on entertainment expenses: Consider free or low-cost entertainment options, such as watching a movie at home instead of going to the theater.

Cancel gym memberships you don’t use: If you have a gym membership but rarely go, consider canceling it and finding alternative ways to stay active.

Shop around for a cheaper cell phone plan: If you’re paying a high price for your cell phone plan, consider switching to a cheaper provider or a plan with fewer features.

Cut back on expensive hobbies: Consider cutting back on expensive hobbies or finding more affordable alternatives.

Cancel unnecessary memberships: If you have memberships to organizations or clubs that you don’t use or need, consider canceling them to save money.

Cut back on non-essential travel: While travel can be a fun and enjoyable experience, it can also be a major expense. Consider cutting back on non-essential travel or finding more affordable options.

Cut back on non-essential entertainment expenses: Consider cutting back on non-essential entertainment expenses, such as going to concerts or sporting events.

Use a cash-back or rewards credit card: If you do choose to use a credit card, consider using one that offers cash-back or rewards for your purchases.

Cut back on luxury items: Consider cutting back on luxury items, such as designer clothing or expensive jewelry, to save money.

Cut back on unnecessary insurance: If you have insurance coverage that you don’t need or use, consider canceling it to save money.

Use apps or websites to find deals: There are many apps and websites that can help you find deals on non-essential expenses and other items. Check out sites like Groupon or Coupons.com to find discounts on your purchases.

Cut back on expensive haircuts or salon treatments: Consider cutting back on expensive haircuts or salon treatments and opt for more affordable options.

Cut back on expensive beauty products: Consider cutting back on expensive beauty products and opt for more affordable alternatives.

Cut back on non-essential car expenses: Consider cutting back on non-essential car expenses, such as car washes or unnecessary car repairs.

Cut back on non-essential home improvement projects: While home improvement projects can be enjoyable, they can also be a major expense. Consider cutting back on non-essential projects to save money.

Cut back on expensive gifts: Consider cutting back on expensive gifts and opt for more affordable options.

Use cash or a debit card instead of a credit card: Credit cards can be tempting, but they often come with high interest rates. Using cash or a debit card can help you save on interest charges and avoid overspending.

5. Cut back on non-essential expenses

Groceries can be a major expense, and finding ways to save on them can make a big difference in your budget. One way to save on groceries is to make a shopping list and stick to it. This can help you avoid impulse purchases and stay focused on the items you actually need.

Here are 20 quick ways to save money on groceries:

Make a shopping list and stick to it: This can help you avoid impulse purchases and stay focused on the items you actually need.

Buy in bulk: Buying in bulk can often save you money, especially if you purchase items that have a long shelf life. Just be sure to consider whether you will actually use the larger quantities before you buy.

Shop at discount stores: Discount stores, such as Aldi or Lidl, often have lower prices on their products compared to traditional grocery stores.

Shop the sales and use coupons: Keep an eye out for sales and use coupons to save on your groceries.

Buy generic or store-brand products: Generic or store-brand products are often just as good as their name-brand counterparts, but at a lower price.

Buy produce in season: Produce is often cheaper when it is in season, so consider buying in-season produce to save money.

Buy frozen or canned produce: Frozen or canned produce can be a more affordable option, especially if fresh produce is not in season.

Buy meat in bulk and freeze it: Buying meat in bulk and freezing it can save you money, as long as you have the freezer space and will use it before it spoils.

Grow your own produce: If you have the space, consider growing your own produce to save on your grocery bill.

Shop at farmers markets: Farmers markets often have fresh produce at lower prices than traditional grocery stores.

Don’t shop when you’re hungry: It’s easy to make impulse purchases when you’re hungry, so try to shop on a full stomach to avoid overspending.

Plan your meals: Planning your meals in advance can help you avoid wasting food and save money on your groceries.

Use leftovers: Don’t let leftovers go to waste. Use them to create new meals or freeze them for future use.

Use a meal delivery service: Meal delivery services, such as Blue Apron or Hello Fresh, can be a convenient way to save on groceries, as they provide all the ingredients you need for a meal in one package. Just be sure to compare the cost to your local grocery store to ensure you are getting a good deal.

Shop at a warehouse store: Warehouse stores, such as Costco or Sam’s Club, often have lower prices on their products due to their bulk sizes. Just be sure to consider whether you will actually use the larger quantities before you buy.

Use cash or a debit card instead of a credit card: Credit cards can be tempting, but they often come with high interest rates. Using cash or a debit card can help you save on interest charges and avoid overspending.

Avoid pre-packaged or convenience items: Pre-packaged or convenience items are often more expensive than buying the ingredients separately and making the item yourself.

Don’t shop when you’re in a rush: When you’re in a rush, you may be more likely to make impulsive purchases or choose more expensive options. Take your time while shopping to make more mindful decisions.

Use a cash-back or rewards credit card: If you do choose to use a credit card, consider using one that offers cash-back or rewards for your purchases.

Use apps or websites to find deals: There are many apps and websites that can help you find deals on groceries and other items. Check out sites like Groupon or Coupons.com to find discounts on your purchases.

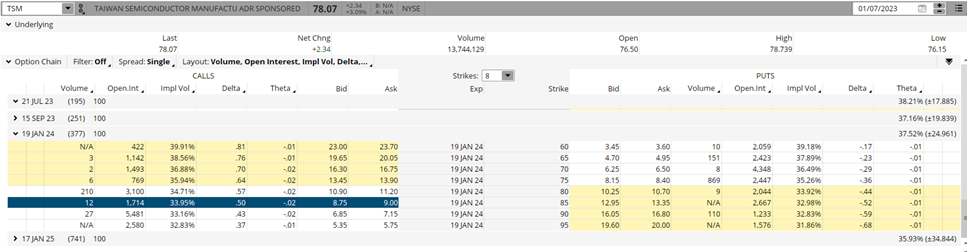

How to use a covered call strategey to buy the dip and sell the rip on the latest Warren Buffett buy in Taiwan Semiconductor (TSM).

shutterstock.com – StockNews

Berkshire Hathaway (BRK.B) disclosed last quarter that it bought a sizable stake in Taiwan Semiconductor (TSM) stock. How sizeable? How about just over 60 million shares at just under $69 per share. This equates to roughly a $4.1 billion dollar outlay for Berkshire and famed chairman and CEO Warren Buffett.

The news of the acquisition on November 15 sent TSM stock soaring over 10% on the day. Shares moved from under $73 pre-announcement to close above $80 post-announcement. Taiwan Semiconductor has since pulled back somewhat to the $78 area.

Buying Taiwan Semi stock at current levels means paying close to the highest price TSM has been in several months. It also is well above the price Mr. Buffett paid for his large stake in the company.

Luckily, a covered call options strategy provides a way to get into TSM stock at a discount close to the Buffett Buy price while pre-positioning to be a seller of the shares on a big move higher.

A covered call trade involves buying 100 shares of the underlying stock and simultaneously selling 1 call option against those shares. It is sometimes referred to as a buy-write since it entails buying the stock and writing the call options.

Effectively, you receive the premium of the call option sold to help reduce the net cost of the trade and provide a downside cushion. That’s the good part.

For having a much lower initial cost on the trade, however, your upside is capped off at the strike price of the call sold.

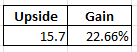

An example of a covered call strategy in TSM stock would be to buy shares at current prices ($78.10) and sell the January $85 calls at $8.80 to reduce the cost of the stock purchase by the amount of the call sale.

The table below shows that selling the TSM Jan $85 call reduces the net purchase price by the premium received for the call sale of $8.80. This puts the net cost for the trade at $69.30 ($78.10 minus $8.80), providing an 11.27% downside cushion until break-even on the stock.

Of course, there is no free lunch in trading. The upside is limited to the strike price of the covered call sold of $85. That, however, still leaves potential upside gain of $15.70 points ($85 short strike price less $69.30 initial cost). This amounts to a 22.66% potential gain on the trade if the stock closes higher than $85 on January 19, 2024 expiration.

This trade certainly fits into the Warren Buffett philosophy of being fearful when others are greedy and greedy when others are fearful. You are willing to be a buyer of TSM stock on a 11.27% drop when others would likely be getting fearful. You are also willing to sell TSM on a 22.66% rally when others would probably be getting greedy.

Plus, TSM sports a solid dividend yield of 1.83% and a low payout ratio of about 25% which would further boost the overall return or lower the risk for the covered call trade.

Investors could use different call strikes or expiration months to sell to fit their risk/return profile. Selling lower strike calls would bring in more premium to lower the risk on the trade but it also lowers the return as well.

2022 was a tough year for stocks. The S&P 500 was down 19% while the NASDAQ 100 did even worse. Luckily, my POWR Options program returned well over 50%.

Many experts expect a difficult market environment in 2023. Investors and traders looking to hedge the downside while still allowing for realistic upside would be wise to consider an option-based covered call strategy.

POWR Options

What To Do Next?

If you’re looking for the best options trades for today’s market, you should check out our latest presentation How to Trade Options with the POWR Ratings. Here we show you how to consistently find the top options trades, while minimizing risk.

If that appeals to you, and you want to learn more about this powerful new options strategy, then click below to get access to this timely investment presentation now:

TSM shares closed at $78.07 on Friday, up $2.34 (+3.09%). Year-to-date, TSM has gained 4.81%, versus a 1.48% rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

Now is the time for value stocks and thus now is the time to discover the attractiveness of AutoNation (AN) shares. Read on below for the full story.

shutterstock.com – StockNews

Many investors have the wrong idea about a bear market. That’s because they see that the average stock is down 20% or more…even worse, high profile growth stocks like Tesla or Roku are down 60-80%. This makes them think there is no way to generate gains in the negative environment.

The real lesson is to seek value. That is the path that leads to outperformance even in the face of a bear market. And that is why I want you to train your attention on AutoNation (AN).

AutoNation is the largest automotive dealer in the United States, has benefited greatly from the increase in used car sales and their rising value. The company also launched its AutoNation USA used vehicle store concept, which is expected to drive massive profits in the years to come. This gives investors a nice combination of steady organic growth along with an exciting new growth driver.

Even as interest rates have risen, US consumers continue to show their clear love and devotion to cars as buying demand remains high. This shows up loud and clear with the Auto Dealers Group still being in the top 1/3rd of our Industry Rank proudly sporting a healthy B rating.

On the value front it is quite shocking to notice that the current PE stands just a notch below 5. Even in the midst of the 2022 sell off that is an eye-popping cheap level for any stock let alone an industry leader like AutoNation.

The value story continues with an overall A rating. Meaning that across the 31 different factors in the POWR Ratings model, AN stands in the top 5% in value. This likely explains why the analyst at Bank of America still has a $238 price target on shares which is more than 100% above current level. That alone could make AN the poster child for this report of severely undervalued stocks.

Want to Discover More Value Stocks?

AutoNation is just 1 of 7 attractive value stocks found in a new special report we just put together. Click the link below to claim your free copy now:

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

AN shares closed at $111.00 on Friday, up $1.89 (+1.73%). Year-to-date, AN has gained 3.45%, versus a 1.48% rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

It’s finally 2023! Hello new year and good riddance to the year that was. Last year was a rough one for the S&P 500 (SPY) by anyone’s measurement… So let’s put that behind us and move on with 2023 to see what that has in store for us. There’s a lot coming up in the next few weeks, so let’s jump right in. Read on below.

shutterstock.com – StockNews

(Please enjoy this updated version of my weekly commentary originally published January 5th, 2023 in the POWR Stocks Under $10 newsletter).

Market Commentary

You know what I’m most excited about? Not having to talk about the Federal Reserve every single week over and over again and…

For better or for worse, the Federal Reserve is still a big market driver. And we’re still going to be talking about it in this newsletter. A lot.

But to Chair Jerome Powell’s credit, the minutes from December’s meeting make their 2023 outlook extremely clear.

“Read my lips: NO NEW RATE CUTS.”

Okay, that’s not a direct quote from anyone, but it might as well be.

Even though many many many investors have already been talking about a potential 2023 policy pivot, the minutes showed not a single Fed official expects a rate cut at any point during the year.

They even included a line warning investors to keep the market rallies to a minimum.

“Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.”

…..?

“Said differently, if equities continue to rally on bad economic news, the Fed will need to push forward to an even higher terminal rate and unofficially add ‘weaker stocks’ to the mandate,” wrote BMO Capital Markets strategists Ian Lyngen and Benjamin in a note Wednesday.

Ah.

Now, I know that may seem extremely dour — it kind of reads as if the Fed has its foot on the neck of the entire stock market (SPY).

And yet, St. Louis Federal Reserve Bank President James Bullard gave a speech earlier today saying the prospects of a soft landing are rising due to the continued strength in the labor market.

So, a little bad and a little good.

We’ll know more by mid-month. There are a number of important economic reports scheduled to be released in the next two weeks. Then, we have the next FOMC meeting, scheduled for the last day of January and the first day of February.

Each of these events will give us one more piece of information we can use to form our 2023 market outlook. Right now, mine is cautious…

I’ll be watching the data and the markets. As much as I wish otherwise, I am concerned that we’re in for another year like the one we just bid “good riddance” to.

But as you can see from a few of the positions in the current portfolio, we can still rake in solid profits even if the Fed keeps the broader market under their thumb.

What To Do Next?

If you’d like to see more top stocks under $10, then you should check out our free special report:

What gives these stocks the right stuff to become big winners, even in this brutal stock market?

First, because they are all low priced companies with the most upside potential in today’s volatile markets.

But even more important, is that they are all top Buy rated stocks according to our coveted POWR Ratings system and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks which could double or more in the year ahead.

SPY shares closed at $388.08 on Friday, up $8.70 (+2.29%). Year-to-date, SPY has gained 1.48%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Meredith Margrave

Meredith Margrave has been a noted financial expert and market commentator for the past two decades. She is currently the Editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Meredith’s background, along with links to her most recent articles.

The #1 problem for investors is underperforming the stock market (SPY). The #2 problem is how much time they spend (aka waste) to achieve these poor outcomes. The above problems explain why 40 year investment veteran Steve Reitmeister is now sharing insights on a proven method to beat the market in as little as 10 minutes a month. Note Steve has employed this method himself to enjoy a real world $104,390 gain since February 2021. Read on below for full details.

shutterstock.com – StockNews

This was the right way to start off the new year for investors.

That’s because I just shared with a live audience how to stop wasting time with their stock selection process. And how they could handily beat the market with the minimum of effort.

The title of the webinar kind of says it all. And gladly you can watch the replay now:

No doubt a lot of the attendees were skeptical at first. Kind of sounded like “8 Minute Abs” for stock investing.

However, over the course of the webinar I clearly laid out the sound fundamental logic behind the process.

And how it consistently helps find the best stocks.

And how it only takes 10 minutes a month to enjoy market topping results.

Better yet…I showed how I have been using this very same process in my Roth IRA account since February 2021 leading to a real life $104,390 gain far surpassing the meager S&P 500 (SPY) return.

Gladly we have many strategies to choose from so you can dial into the perfect stocks for who you are as an investor.

That’s because every investor is different. Some more aggressive…some more conservative.

Then you have growth, value, income and momentum factors to weigh for each stock.

And then you have current market conditions to consider which is why we have built separate strategies for bullish times as well as bearish.

So whatever type of strategy you are looking for it will be easy to find it…and apply it successfully in just 10 minutes a month.

And yes, these strategies have performed incredibly well even during the rough and tumble 2022 bear market. The full proof of this is shared in this timely webinar below.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, StockNews.com

SPY shares closed at $388.08 on Friday, up $8.70 (+2.29%). Year-to-date, SPY has gained 1.48%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Preparing for retirement may take more time, money, and effort than you think. It is especially harder to transition this year as inflationary pressures intensify. Although it may benefit savers and lenders, its impact is less desirable than we think. It erodes the value of dollars and, in turn, hurts the purchasing power of consumers. Not even the financial market can’t dodge or at least cushion the blow.

Due – Due

Older Americans are more vulnerable to risks associated with economic volatility. Over the past decade, they have composed the majority of bankruptcy filings in the US. The figures may increase further as uncertainties persist. Hence, it is no surprise that many would-be retirees have decided to continue working. This year, 25% would postpone their retirement, a massive drop from the previous year.

Fortunately, their awareness of investments has improved in the last two years. The capital market sees more inflows despite the bearish trend. Dividend-paying stocks, ETFs, and mutual funds have become a favorite for many, as they offer a sense of security, especially for newcomers, knowing they will receive constant returns. With that, we will discuss everything about dividends and how they can support your retirement.

What is a dividend?

Before investing in the equity market, you must first determine your goals. Investments can become an excellent passive income if you know what you want. However, you must remember that not all investments pay dividends.

You can become a short-term trader, which appears risky but can generate instant returns. Buying a stock or an ETF at a low price and selling when it goes up can be promising. Also, dividends may not be your priority, and it’s fine. But, it can also be challenging, especially when the price moves sideways or downwards. You have to identify the patterns and volumes. Doing so will help you find a good entry point before taking a buy or sell position. Other short-term investments do not require trading skills like technical analysis. These include treasury bonds, money-market accounts, and certificates of deposits.

For many retirees, dividend-paying stocks and ETFs provide income without a job. Often, they are for those who do not have time to monitor the market every second. They are suitable long-term investments since payouts are constant. In essence, dividends are a portion of company earnings distributed to eligible shareholders. They can be paid out every quarter, half-year, and year. Note that both public and private companies can distribute dividends, but not all companies do since dividends are not part of their legal requirements. The following are the typical types of dividends.

Cash Dividend

Cash dividends are the most common type of dividends. Ordinary dividends have periodic payments, while special dividends are non-recurring payouts. Often, companies distribute them during periods of boom or when they have excess income.

It is also essential to know the type of shares before investing. Preferred dividends are deducted from the net income for preferred shares. Because they have a higher priority, they are paid before common shareholders. Meanwhile, common shares receive common dividends. They are the last in the hierarchy when it comes to company payments. Shareholders and traders in the equity market are also common shareholders. They learn about dividend payments through company press releases.

Stock Dividend

Cash dividends can have an impact on a company’s liquidity. Sometimes their cash flows are insufficient to cover dividends after capital expenditures (CapEx) and borrowings. Dividends can be paid in the form of stocks rather than cash. They appear similar to an automatic dividend reinvestment plan (DRIP). Stock dividends, like cash dividends, can be ordinary or special. However, they provide instant gains since you can sell these extra stocks at their trading price.

A stock dividend differs from a stock split because stock dividends increase shareholder value, while stock splits happen when companies increase or decrease the number of stocks. These regulate stock liquidity. However, they have no effect on shareholder value because the income per share remains constant

Scrip Dividend

Scrip dividends are issued in the form of promissory notes. It happens when the company does not have enough cash to pay cash dividends.

Property Dividend

Another non-monetary dividend payment is a property dividend. The recording of the distributed property is based on its market value.

Liquidating Dividend

The company may distribute liquidating dividends to return the capital of shareholders. It often precedes company dissolution or shutdown.

How To Live Off Dividends

Despite improved financial literacy, 30% of Americans retire without savings. This group believes that the meager retirement funds and social security benefits can suffice their needs. Sadly, many retirees are yet to secure a constant fund source for their retirement. That is why soon-to-be retirees must catch up with their retirement savings.

It is advisable to invest if you want to expand your money or have a passive income. The best option for a reliable income source is dividend-paying stocks. However, they must prepare to live off of dividends. Any investment is good, but remember that you have to stay liquid.

Determine your retirement living expenses

One of the biggest mistakes you may commit is downgrading expenses in your retirement years. It is not enough that your funds can suffice your basic needs. Retirement can last longer than you think. And as you grow older, you may incur more expenses, such as long-term care and hospitalization. Statistics show that retirees are more than twice as likely to require hospitalization than younger adults. You may also run into debts, as statistics show that 75% of retirees carry debt through their retirement.

You must determine your retirement expenses, including long-term healthcare. Note that Medicare will not last you a lifetime. Your social security benefits may not be enough for your cost of living. You also have to anticipate taxes on your retirement funds. Once you get the figures, you can estimate the dividend income you need on top of your savings and pension funds.

Abide by the 4 Percent Rule

The four-percent rule is a more practical rule of thumb for estimating your retirement living expenses. Retirees may rely on it to decide on the amount to withdraw from their retirement savings every year. This rule helps avoid overspending by keeping a constant retirement income stream. This rule is based on the historical stock and bond returns from 1926 to 1976. Typically, withdrawals consist of dividends on savings and compounding interests on bonds. That way, you can keep adequate funds in the following years.

But of course, it may vary with different scenarios. You may adjust it to 5% in worst-case scenarios. Others suggest lowering it to 3% since it fits the current trends in interest rates. You must consider life expectancy and emergency expenses for a more precise estimation.

Nevertheless, it is still better to have passive income streams than withdraw investments for your retirement expenses. It makes it possible to live off dividends for a long time. You will have an opportunity to maximize the potential value of your investments. Also, you can maintain your assets by keeping expenses lower than what you generate in dividends.

Invest in Stocks That Focus on Dividends

Investment portfolio diversification is an excellent choice to boost your retirement funds. When investing in stocks, you may choose between actual trading for instant capital gains. For long-term investments, you may opt for stocks that pay dividends. Dividend investing promises returns even without watching the stock price every minute.

For better security, you wish to buy blue-chip stocks. They have already stood the test of time and can operate amidst economic volatility. For higher dividends, you may choose the Dividend Aristocrats instead. Either way, you must check the fundamental health of the company. Check its cash levels in the Balance Sheet. You may also look into the Free Cash Flow to determine if it can sustain its operations and pay dividends. You can also combine it with Net Debt/EBITDA to know if the company earns enough to cover financial leverage. These accounts and financial ratios are more important measures for capital-intensive companies.

Suppose the company has solid fundamentals, allowing it to cover dividends, you still have to find out how long and how much it can sustain dividends. Using the Dividend Payout Ratio, you can check the allocation of net income to dividends. You can choose to use Free Cash Flow in place of net income, as some people find it more realistic since it accounts for cash transactions. Deducting the CapEx tells you how much cash is left. Once you are sure the company is capable, you must check how enticing the dividends are.

Dividend Growth

Let’s face it; stock dividends usually increase over time, unlike bond interest. The stock market may be riskier, but growth prospects are promising. Dividend growth should be one of the considerations for an excellent long-term investment. In the last two years, many companies halted dividend growth, while some did not pay dividends at all. That is why it is essential to note those who withstand the blow of pandemic disruptions. Now that the global economy faces inflationary pressures, pessimism is taking over again.

Dividend investors must keep an eye on companies with increasing dividends despite market volatility. Dividend Aristocrats are excellent choices. These are a lot of S&P 500 companies that have increased dividends for 25 consecutive years. But, companies other than the S&P 500 may pay the same or better dividends.

Indeed, there are a lot of companies you can add to your portfolio. You may check the five-year, ten-year, or twenty-five-year average dividend growth. Doing so will help you check how much their dividends have grown.

Dividend Yield

You already have a long list of excellent dividend stocks. So, it’s time to trim down your choices. Before buying stocks, you must determine if the dividend is worth the price. The dividend yield shows how much the company pays relative to the stock price.

There is no definite percentage of excellent dividend yield, but analysts recommend a yield of at least 2%. It is advisable to check if the company is part of the S&P 500, 400, or 600. You can also check whether it is on the NYSE and NASDAQ. Once you derive the dividend yield, you can compare it to the average of these stock indices.

Moreover, the dividend yield helps find a reasonable stock price relative to the dividends. The Dividend Discount Model is one of the many stock valuation techniques. It uses the average dividend growth, dividend yield, estimated annual dividend, and cost of capital equity.

What types of investments pay dividends?

Economic volatility and financial capacity influence the risk tolerance of investors. It is not too late to start investing and growing your retirement account. Yet, you must study and observe before putting your eggs into different baskets. Doing so promises more security and potential returns. These are the best dividend investment choices.

Stocks

The stock market is the most popular and preferred choice of dividend investors. Typically, these are publicly-traded companies with a history of dividend payments and growth. Investing has also become more convenient with the advent of electronic trading.

Many S&P 500 companies are considered Dividend Aristocrats. This distinction refers to companies raising dividends for at least 25 years.

Companies other than the S&P 500 have maintained dividend growth for more than 25 years. They are referred to as the Dividend Champions. As of 3Q 2022, there are 147 dividend champions on the NYSE and NASDAQ. Meanwhile, companies that raised dividends for 10-24 consecutive years are called Dividend Contenders. The Dividend Challengers are companies that increased dividends for 5-9 years.

Mutual Funds

Mutual funds are also a favorite among many investors. Mutual funds may also offer dividend payouts. These mutual funds are those used to buy dividend-paying stocks. In turn, dividends are passed on to the investors after deducting the management fees. They appear to be an indirect stock investment and dividend reinvestment.

ETFs – Exchange-Traded Funds

Like mutual funds, ETFs operate as a pool of investment security. Their difference is that ETFs can be traded on the stock market like individual stocks. Dividends are also distributed to investors.

Real Estate Investment Trusts

REITs are companies owning and financing real estate companies that generate income. They are also similar to mutual funds since they act as a pool of capital. In other words, the amount is invested directly in real estate companies. Hence, you can earn dividends without buying, operating, or financing properties. The downside, however, is that REITs offer little capital appreciation.

Consult a Financial Advisor for Your Retirement Plan

Living off dividends amidst volatility is challenging but achievable. With preparation, knowledge, and wise portfolio diversification, returns may offset risks. It is important to be familiar with dividend-paying stocks and other investments. That way, you can assess the level of risk you can tolerate and the returns you can generate.

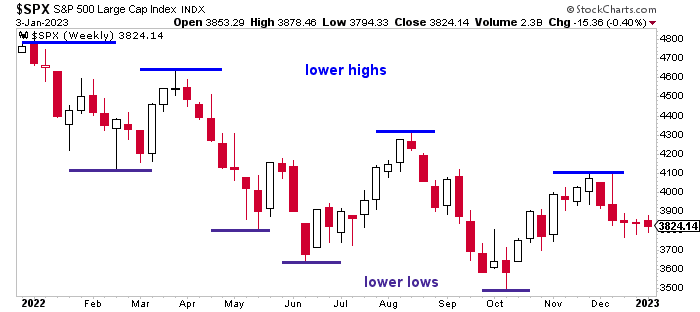

The new year has begun with a roller coaster ride for investors. Some excited…some losing their lunch. That is the past. The key is what it all means for the future especially as we close in on the all important 200 day moving average for the S&P 500 (SPY). Check out what 40 year investment veteran Steve Reitmeister has to say about it all in his new commentary including a trading plan to stay one step ahead of the market.

shutterstock.com – StockNews

The first trading week of the new year ended on a strong note. However, it wasn’t all “lollipops and ice cream” as stocks sank one day then surged the next…then sank…then surged again.

The reason for this extreme volatility is some mixed signals on the economic front. Some quite bullish. Some quite bearish. All quite confusing.

So I will do my level best to make sense of it all in this week’s commentary.

Market Commentary

The best place to start this conversation is by sharing with you the contents of a trade alert this morning to take profits on a 3X inverse ETFs in my Reitmeister Total Return service:

“Today we got a goldilocks set of reports for bulls. Employment strong + wage inflation moderating + weak ISM report = odds of less hawkish Fed are higher and thus bulls will have some fun for a little while…and thus best to sell HIBS.

Reity, are you becoming bullish?

No. I am becoming slightly less bearish with today’s information. And thus taking our most aggressive bearish bet off the table.

Right now investors are most focused on inflation and that is moderating nicely while employment remains strong. This improves the soft landing narrative.

Unfortunately, they are taking their eye off the collapsing economy such as ISM Services dropping from 56.5 last month to a contractionary 49.6 this month. And yes, the forward looking New Orders component is even worse at 45.2.

I think the S&P 500 (SPY) may try and make a move back towards 200 day moving average (3,999) and then reassess if inflation is the only story worth noting…or should the deteriorating economy weigh into decision making???

If truly break above 200 day moving average in meaningful way…then yes, we will get less and less bearish…and more and more bullish.”

(end of Friday morning note)

There really is a “Catch 22” scenario in rooting for lower inflation. That’s because the #1 way to reduce inflation is by lowering demand. Yes, that is the explicitly stated goal of the Fed with their rate hiking regime.

But let me do a little language translation for you:

“Lower Demand” is Fed speak for “Let’s Create a Recession”

So yes, we are taming inflation by greatly harming the economy. This shows up loud and clear in the key economic reports this week starting with ISM Manufacturing on Wednesday ebbing ever lower to 48.4. This goes hand in hand with the 45.2 showing for New Orders pointing to even lower readings ahead.

And as already shared ISM Services, the larger part of the economy, is also in a state of decline. Let me correct that…in a state of falling of a cliff.

Yes, this is disinflationary. Hooray!

But it is also opening up the Pandoras Box known as recession. Boo, Hiss!

And if that really does pick up speed then employment will finally falter with lower spending as a result which only exacerbates the recessionary pressures.

So…is it time to get bullish because lower inflation may have the Fed less hawkish down the road. Or time to get more bearish because there are greater signs of a recession forming now???

That indeed is the key question for investors. But with the Fed likely mum until their next decision date on February 1st, then I could see the bulls having a little more fun up to the serious resistance at 4,000.

That area is now doubly reinforced. Not only is it a psychologically important hurdle…but it also is connected to the 200 day average which now stands close by at 3,999.

We have seen quite a few momentary breakouts above the 200 day moving average since the bear market began. And then quickly the coffin was shut with more downside on the way.

To sum it up, I am still bearish as I think the catalyst of recession is more important than ebbing inflation. However, other investors may not agree. Thus, if we see a meaningful break above the 200 day moving average I would be compelled to get a bit more bullish too.

If investing were easy…then everyone would do it with a high degree of success.

Clearly not the case. Which is why we weigh all the key factors to create a market outlook along with a portfolio constructed to outperform in that environment. Then we go into each new day with an open mind to objectively review each next bit of information. This gives us the best chance to adjust our strategies to stay on the right side of the action.

I will continue to do my level best to share you timely updates as things evolve with appropriate trade recommendations.

What To Do Next?

Watch my brand new presentation: “2023 Stock Market Outlook” covering:

Why 2023 is a “Jekyll & Hyde” year for stocks

5 Warnings Signs the Bear Returns in Early 2023

8 Trades to Profit on the Way Down

Plan to Bottom Fish @ Market Bottom

2 Trades with 100%+ Upside Potential as New Bull Emerges

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.20 (-0.05%) in after-hours trading Friday. Year-to-date, SPY has gained 1.48%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

A 1099 form is a document that businesses use to report various types of government payments to both the IRS and payees.

LPETTET | Getty Images

This includes payments for services, dividends, interest, rents, royalties, and other types of income. There are various 1099 forms, each with specific instructions for filling them out.

If you’re an entrepreneur or small business owner who wants to stay compliant with the IRS, it’s critical to understand what a 1099 form is and how it applies to your business. Read on for an overview of the different types of 1099 forms and how to navigate the filing process.

What is a 1099 form, and what is it used for?

A 1099 form is an information return that reports taxable income other than wages, salary, and tips.

For example, if you’re self-employed or earn rental income, you’ll likely receive a 1099 form.

The 1099 form reports what’s referred to as miscellaneous income, and there are many different types of 1099s.

Here’s a quick run-through of some of the other common 1099 forms and what they report:

Form 1099-B: Proceeds from broker transactions

Form 1099-C:Cancellation of debt

Form 1099-DIV: Dividends and distributions from investments

Form 1099-H: Health insurance premiums that the taxpayer pays

Form 1099-INT:Interest income earned throughout the year

Form 1099-K: Merchant card and third-party payment transactions

Form 1099-NEC:Nonemployee compensation

Form 1099-Q: Distributions from qualified education programs

Form 1099-R: Distributions from pensions or annuities

Form 1099-S: Proceeds from real estate transactions

Form 1099-SA:Distributions from health savings accounts (HSA)

All that said, the most common type is the 1099-MISC, used to report income earned from rental property, providing services as an independent contractor, or earning royalties. If you receive a Form 1099-MISC, you’re considered self-employed (an important fact to remember).

While this may seem like a lot of extra work, being self-employed has some benefits, such as the possibility of deducting business expenses on your tax return.

Be sure to speak with a qualified tax professional if you have questions about filing your taxes after receiving a 1099 form.

A 1099 form is not the same as an income tax return. It’s an informational form that reports specific types of income and other financial activities. Essentially, you use the information from the 1099 forms to complete your taxes.

The Internal Revenue Service (IRS) requires businesses to file 1099 forms for almost any payment over $600 made throughout the year. That includes payments for services, mortgage interest, royalties, and other miscellaneous income.

The payee doesn’t need to issue a 1099 form for any payments under $600; nonetheless, both the issuer and recipient must report this income on their tax returns.

A 1099 is an IRS form that shows an individual’s income from specific types of payments.

A Form W-2 is a tax form that reports the wages an individual has received.

The primary difference is that 1099 forms are issued to non-employees, whereas W-2 forms are issued to employees. Businesses are responsible for reporting employee wages on W-2 forms, while self-employed individuals (think freelancers and independent contractors) must report payments outlined on their 1099s.

Additionally, self-employed individuals may receive 1099s and W-2s, depending on the work they perform.

Generally, W-2 forms report wages from full-time employment or an employer/employee relationship, whereas 1099 forms report income from freelance work, contract labor, royalties, or rent payments.

Unlike 1099s, W-2 forms withhold federal income taxes (and state taxes) from employees’ wages. Therefore, individuals need to note whether their income was reported as a W-2 or 1099 to know what taxes they must pay.

A 1099 form reports income from freelance work, rentals, investments, and other alternative sources. In most instances, if you earned more than $600 from any of these sources during the year, the person who paid you must send you a 1099 form by January 31st. You will then use this form to complete your taxes.

When reporting your income on your taxes, use the correct 1099 form.

For example, if you received payment from freelancing, you should generally fill out a 1099-MISC.

Note that you’re responsible for paying taxes on all of your income, regardless of whether or not you receive a 1099 form.

Speak to a tax professional if you have any questions about whether or not you need to file a 1099 form. They can guide you through all the reporting requirements and help keep you above board.

For businesses, 1099 forms are due by January 31st of the year following the calendar year when payments were made. This applies both to copies to be sent to contractors and the IRS.

For individuals, 1099 forms must be received by January 31st, following the calendar year during which payments were made. All relevant 1099 forms should be reported on individuals’ tax returns by April 15th of the same year.

If an individual does not receive a 1099 form from a business or other payer, they should still report the income on their tax return. Individuals should keep track of their income throughout the year in case 1099 forms are not provided.

Failure to meet these deadlines can result in expensive penalties. Businesses that fail to file 1099 forms on time face a minimum penalty of $50 per form, with a maximum of $290 per year. The specific penalty depends on the form type and the time passed after the deadline.

The IRS can also impose additional penalties for what it finds as intentional or negligent filing errors.

How do I file a 1099 form with the IRS?

If you’re an independent contractor or self-employed individual, you’ll need to file a 1099 form with the IRS come tax time.

Here are three things to know about 1099 forms and how to file them with the IRS:

1. A 1099 form reports income not subject to withholding tax.

This includes interest, dividends, royalties, and payments made in exchange for services (including rent, commissions, fees, and tips). The payer of this income should send a 1099 form to both the payee and the IRS.

2. There are many types of 1099 forms (more than 15), each for a different type of income.

The most common is the 1099-MISC, used to inform the IRS of miscellaneous income. You would file a 1099-MISC if you received income such as rental income or freelancing income during the year. Other common 1099 forms include the 1099-INT (for interest income) and the 1099-DIV (for dividend income).

3. When it comes time to file your taxes, you’ll need to include your 1099 forms with your return.

You’ll also need to send a copy of each form to the IRS, so be proactive about keeping the informational report handy.

Here are some tips for filing your 1099 forms correctly:

Review each form you receive and make sure the information is accurate.

Choose the correct filing method, whether direct entry, paper filing, or digital e-filing.

Double-check your work to ensure all your forms are filled out completely and accurately.

File your forms with the IRS and report them on your tax return by the deadline.

Correctly filing your 1099 form is essential for ensuring that you comply with the IRS and local tax agencies. It also helps to protect you from any potential penalties and audits.

Common mistakes people make when filing 1099 forms

Perhaps the most common mistake is failing to report all the income they receive. While this can be fraudulently intentional, unintentional misreporting can happen if you forget to include income from a side gig, lottery winning, or receive cash payments instead of a check or money order.

If you don’t know whether to report a specific type of income, it’s generally best to err on the side of caution and include it. Otherwise, you could face IRS penalties or miss out on potential tax credits.

Another common mistake made on the business end is incorrectly reporting the taxpayer identification number (TIN) of the person or business you paid. The TIN can be either a Social Security number (SSN) or an employer identification number (EIN).

If you report an incorrect TIN, the IRS might flag the return as inaccurate and send you a notice asking for clarification. As such, you always want to double-check the TIN before filing your return.

Lastly, some taxpayers fail to file their 1099 forms (and other information returns) by the established deadline. The deadline for paper filings is February 28th, and the deadline for electronic filings is March 31st.

If you miss the deadline, you may be subject to late fees and interest charges from the IRS. By avoiding these mistakes, you can ensure that your 1099 filing process goes smoothly (or at least increase the chances of a smooth process).

Are there penalties for not filing a 1099 form on time or incorrectly filing one?

The IRS imposes various penalties for businesses that fail to file 1099 forms on time or file them incorrectly. Perhaps the most significant penalty is the failure-to-file penalty, assessed at a rate of 0.5 percent of unpaid taxes per month; a business will be subject to this penalty if it fails to file a 1099 form within 30 days of the due date.

Moreover, if a business files a 1099 form more than 60 days after the due date, the penalty can increase to $435 per form.

In addition to the failure-to-file penalty, businesses may also be subject to a failure-to-pay penalty if they don’t pay the amounts shown on the 1099 forms by the due date. This penalty is equal to two percent of the unpaid tax liability and accrues monthly until the total amount gets paid.

Finally, businesses may be subject to interest charges on any unpaid taxes.

How can I get help if I’m having trouble filing my 1099 form correctly?

If you struggle to fill out or file your 1099 form correctly, there are a few places to turn for help.

IRS website

The IRS website has a wealth of helpful resources to answer most tax filing questions.

You can call them if you can’t find what you’re looking for on the website. They have customer service representatives who can help answer your questions and get you on the right track.

Remember that IRS employees and those who work for other financial institutions are often overwhelmed with calls, especially during tax season, so you may need to plan for long wait times.

Tax professionals

Another great resource is your tax preparer or accountant. They can guide you through each step of the process and ensure everything is filed correctly.

Your tax professional can also help you get the maximum amount on your tax refund. If you don’t have a tax preparer or accountant to rely on, make it a priority to find one as soon as possible.

Tax filing software

Finally, there are many software programs available that can help you file your taxes. These programs can walk you through the process in an easy-to-use interface.

If you’re overwhelmed by the different options on the market, read online reviews highlighting each product’s features and costs. Then, choose the best tax software for your needs and budget.

Getting help with your 1099 form can be easy, whichever route you choose. Research the plethora of resources available to help you get everything filed correctly and on time.

Ready to file a 1099 form?

1099 forms are important documents for both the IRS and taxpayers. Businesses and individuals should understand who needs to file them, when they are due, and how to get help filing them correctly.

Filing deadlines are strict, so it’s best to start gathering your information early and contact a tax professional if you have any questions.

Opinions expressed by Entrepreneur contributors are their own.

As I write this, commercial interest rates — the rate businesses pay for working capital, equipment and property loans — have more than doubled over this past year. My clients are now seeing commercial rates exceed 10% — that’s going to be a big challenge for those that rely on debt to fund their operations and expansion, let alone those entrepreneurs looking to startup and grow their businesses.

The financing environment will be tough in 2023. Less businesses will get approved for loans as the financial services industry contracts in response to continued high interest, inflation and a slowing economy. But it’s not a catastrophe. There will be money out there if you’re willing to pay for it. Here are your best choices to consider.

For starters, if you don’t need a loan, then you should definitely go to a traditional bank. I’m kidding, of course. But traditional banks — and you know the names — are the most risk-averse of all lenders. They are going to lend money to businesses that have collateral, history, solid credit and the ability to pay the loans back almost without question. Interest rates and terms, assuming you meet those requirements, will always be the most favorable compared to other financing options.

Small bank loans

Besides the big banks, there are independent and community banks and credit unions all of which offer different types of loan arrangements and may be more amenable to dealing with a smaller company that isn’t as qualified to get a loan from a big bank. But still, these banks, though a little more entrepreneurial, tend to also be very risk averse and will require significant due diligence.

SBA Loans

The best option in 2023 is to seek out a loan from a lender certified by the Small Business Administration. Those loans (called Section 7a or 504) can be offered at market or slightly above market interest rates. Because most of the amounts are guaranteed by the federal government, the banks offering these loans can do so to smaller companies with less of a financial history or collateral available and are less at risk. But it’s still not a slam dunk and you’ll have plenty of hoops to jump through.

If you’re looking for a very short-term loan to satisfy an immediate financing need (a big inventory purchase, a down payment on a lease, a deposit on a new piece of equipment) you can try an online banker like Kabbage, Fundbox and OnDeck. These companies charge extremely high annual interest rates, but no sane business person would borrow from them for the long term. The upside is that these services provide funds very quickly — in some cases within 24 to 48 hours — and (as opposed to many banks) are more technology-oriented to gather data, monitor their loans and communicate issues.

Merchant advances

If you’re in the retail world then you might want to consider a merchant advance, which are short-term loans provided by popular payment services like Square, PayPal and QuickBooks Merchant Services. Your loan qualifications are determined by your actual sales volume to which these payment services are privy because, well, they’re already handling your cash. Like online lenders, interest rates are much higher than what traditional banks offer but the funds are quickly deposited in your account and payback is done automatically through the sales transactions you record with the service.

SSBCI

If you’re a very small business or a minority business owner or someone located in a lower-income part of the world then you should definitely look into the State Small Business Credit Imitative. Thanks to prior pandemic-related legislation, $10 billion is being distributed this year and next by the Treasury Department to states (based on a number of factors) that will then be allocated to local nonprofits and other organizations that support small and minority-owned businesses. You can Google your state and the State Small Business Credit initiative to find out what organizations are getting this funding and then apply directly to those organizations. Grants and equity investments are also available through this program.

Micro loans

For startups and very small businesses, you can also look for microloans offered by nonprofit organizations like Kiva, for example. These amounts are — by definition — very small but organizations like this one also provide good consulting services and can connect you to other places that offer finances for companies at your early stage.

Private lenders

Although these companies don’t charge as much interest as some of the short-term online lenders mentioned previously, interest rates are still higher but so are approval rates. Collateral — oftentimes receivables (for companies that “factor these amounts) and inventory — will be required. The best place to find these lenders (and other more traditional forms of financing) are platforms like Lendio and Fundera which offer a “marketplace” of different vehicles provided by their partners and an easy way to apply for them all.

Credit cards

What about credit card financing? You know you’ll pay a hefty interest rate but don’t knock it entirely — it may be a bad choice unless it’s for very short-term needs. Just make sure you’re not building your business around credit card debt because as interest rates continue to rise, so will credit card rates.

Family and friends

Finally, there are friends and family. A lot’s been written on this so I don’t have to tell you of the potential perils. You already know them. But getting a loan from a reasonable friend or family member can provide you with a reasonable rate of interest and flexibility. It all depends on the people involved.

The takeaway is that 2023 will be a tough year for financing. But not impossible. Just make sure you can afford it. And give yourself the flexibility to renegotiate in the future when rates do eventually come down.

Retirement is a time to enjoy and relax. But the question is where?

Due – Due

Some people look for a place close to their family and friends, while others want good weather year-round. And still, others want to live in an area with plenty of activities and entertainment.

If you’re looking for a place to retire and need help figuring out what to look for, keep reading this article. We’ll discuss the different essential factors you should consider and give our recommendations on where you can find them.