Marie Osmond wants her seven kids to make their own fortunes, according to a new report.

The country singer believes individuals who are simply “handed money” often end up lacking drive and ambition, and she wants her children to discover their own interests on the road to forging meaningful careers. As a result, Osmond told Us Weekly she doesn’t plan to leave her kids an inheritance.

“Honestly, why would you enable your child to not try to be something? I don’t know anybody who becomes anything if they’re just handed money,” Osmond told the tabloid. “To me, the greatest gift you can give your child is a passion to search out who they are inside and to work. I mean, I’ve done so many things from designing dolls [and much more]. I love trying [and] I wanna try everything. I’m a finisher.”

By contrast, Inheritances “breed laziness and entitlement,” she added, noting that she plans to spend the money she’s made with husband Stephen Craig, whom she has married twice.

Osmond expressed similar views on leaving wealth to posterity in 2020 on “The Talk,” saying she believes inheriting large sums does children “a great disservice.” At the time she said she planned to donate her fortune to charity.

Warren Buffett’s advice

The late actor Kirk Douglas also donated most of his $61 million fortune to charity upon his death in 2020, according to Fox Business. The Douglas Foundation, the charity he co-founded, focuses on providing more equitable access to education, health care and the arts. The foundation has granted more than $118,000,000 to more than 200 organizations since its inception.

English musician Sting, whose wealth has been estimated at $300 million, has also spoken publicly about the downsides of kids inheriting their parents’ fortunes, saying his own children will inherit little of what he has earned.

“I told them there won’t be much money left because we are spending it. We have a lot of commitments. What comes in we spend, and there isn’t much left. I certainly don’t want to leave them trust funds that are albatrosses round their necks. They have to work. All my kids know that and they rarely ask me for anything, which I really respect and appreciate,” he told the Daily Mail in 2014.

English chef and food writer Nigella Lawson has also stated she will not leave her children with a financial cushion.

“I am determined that my children should have no financial security. It ruins people not having to earn money,” she said in 2014, according to the Washington Post.

Warren Buffett, who has long pledged to donate more than 99% of his wealth to charitable causes, has also said his children will inherit little of his fortune, which Bloomberg now pegs at $111 billion. As the noted investor wrote in 2021: “After much observation of super-wealthy families, here’s my recommendation: Leave the children enough so that they can do anything but not enough that they can do nothing.”

With many economists predicting a recession sometime soon, it’s wise to start preparing just in case. There are numerous ways to improve your financial situation regardless of your income level. Here’s how to get started, plus tips on what not to do during an economic slump.

Due – Due

The Predicted Recession

There’s growing talk of an economic downturn. With inflation gathering steam and the Fed predicted to push up interest rates in response, the first half of 2023 will likely bring a recession. Many factors are compounding the issue, including:

Rising food prices due to embargos on Russian wheat, wheat fields in Ukraine being burned and Ukrainian wheat harvests being stolen or destroyed.

Pandemic supply chain issues.

Billions of people spend more money than usual after quarantine, such as by going on vacation or getting married.

Increased energy prices due to Russian oil sanctions.

It’s essential to keep in mind that even if a recession happens, it may still be very mild or short-lived.

Tips for Preparing for a Recession

Whether or not the predicted recession materializes, it’s still a good idea to get your finances in order as soon as possible. That way, you’ll be even more prepared for the next economic downturn.

Create an Emergency Reserve

If you have car trouble, you need to visit the dentist, or your home has a water leak, can you pay for it without breaking the bank? Unexpected bills are a part of life, so it’s essential to prepare for them even during prosperous times. Having a solid emergency fund is critical during a recession.

Aim to start a fund that covers three to six months of minimal living expenses — that is, don’t budget for things like going out to eat or taking a vacation. If you’re retired, you’d do well to save for at least one to two years’ worth of expenses.

These emergency funds shouldn’t be tied up in real estate or an investment account. You should be able to draw from them immediately if you lose your job or face an unexpected rent hike. Other than paying off debts, prioritize building your emergency fund above all else.

You can start by putting just a few dollars a day into your account. Setting aside even $3 a day means that in one year, you’ll have saved $1,095, which can be immensely helpful if you get an unexpected bill. Consider what minor expenses you could eliminate — such as a streaming subscription or smoking habit — to save thousands of dollars in the long run.

Automate Your Savings

The easiest way to start saving money is to do it automatically. Set up an automatic transfer with your bank or employer to make regular deposits into a savings account. If you have any recurring bills, use autopay to cover them. This will reduce your financial stress, ensure your bills are paid on time and slowly build up your savings account.

Reduce Debt

Interest rates tend to increase during a recession. If your credit card has a variable rate — meaning the interest rate can change based on factors beyond your control — it’s vital to pay off the card as soon as possible. You could save hundreds or even thousands of dollars in potential interest by paying it off before the recession starts. This should be your number one priority during an economic downturn.

Put off Larger Purchases

Sometimes, making a large payment is unavoidable. If your car is beyond saving, but you live miles from any public transportation, you may have no choice but to buy another vehicle.

But don’t make large purchases unless absolutely necessary — now is the time to save as much as you can. If you lose your job, interest rates go up, or your cost of living increases substantially, you’ll want to have a large nest egg set aside.

Consider Sticking With Your Job

It’s true that many people are quitting their jobs right now. When polled, 45% of American employees said they would consider leaving their job if they got a better offer. This phenomenon even has a name — the Great Resignation.

It’s understandable if you’re tempted to look for better job opportunities, but recessions are a notoriously tricky time to be out of work. Many employers are forced to lay off workers and go on hiring freezes, meaning that if you put in your two weeks’ notice before a recession, it could be a while before you find another job.

Rather than looking for a higher-paying job, upskill yourself so you can earn more at your current place of employment. This also bolsters your chances of staying employed even if your company starts laying people off. If you do need to quit, have a solid backup plan in place. You should ideally have another job lined up before jumping ship.

Get a Side Gig

These days, it’s incredibly common to have a second job. Put in an hour or two per week mowing yards or selling art. If you can, get a side gig you can do alongside your main job, such as dog sitting or house sitting while you work on your laptop. That way, you can earn a little more without putting in too many extra hours.

Share Your Living Space

With rent prices soaring, it’s no wonder that as of 2021, over half of all Americans aged 18–24 lived with their parents. Others cut costs by sharing their home with roommates, a spouse, or an unmarried partner. Consider staying where you are if you already have a shared living situation. If you have an empty room in your house, you may even be able to rent it out to make some extra income.

Hold Onto Your Investments

If you have investments, you may feel rising anxiety as your portfolio shows falling prices. But remember — these losses are only theoretical until you withdraw your money, a principle called locking in your losses. Don’t let your emotions guide your financial decisions.

It’s common for the market to have some of its best days right after its worst days, so fight the urge to sell during a bear market. You want to invest for decades, holding steady even as your investments rise and fall in value over time. You’re statistically more likely to make a profit the longer you wait to sell.

Consider shifting your investments into sectors like energy, health care, and consumer goods, which people will always buy regardless of their financial situation. These are solid investments during a recession. Or, switch your assets from stocks to bonds.

Bonds are an excellent choice for people looking for a fixed income. Every year, you’re guaranteed to gain a small amount of interest on the bond, which adds up slowly over time. This offers a safe return on your investment, even if the return is much smaller than what you’d get by buying stocks. Bonds aren’t subject to plummeting in value during a recession like stocks are.

Keep Investing if You Can

Taking on additional debt or making big purchases during a recession is not advisable. However, keep investing if you’re financially privileged enough to do so. Whether you have a Roth IRA, brokerage account, or 401k, stick to your plan and keep depositing money into your account. You’re more likely to avoid losses the longer you stay in the market.

Don’t Co-Sign on a Loan

A recession isn’t the best time to co-sign on a loan, meaning you’re signing up to be someone’s backup in case they fall through on their payments. Although co-signing can help a friend or family member with a poor credit history, you’re ultimately responsible for the debt if they can’t pay it off. That’s a risky move during an economic downturn. Instead, give someone cash or a personal loan if you want to help them financially.

Stay Calm

Remember that recessions are a regular, temporary part of the economic cycle and the economy always bounces back even stronger afterward. You’ve already been through multiple recessions in your lifetime. In the US, the average post-war recession only lasts 10 months, while expansion periods last almost five years.

So, don’t fall prey to fear, uncertainty, and doubt. You don’t need to constantly watch the news or read every doomsday article predicting another Great Depression. It’s possible to stay informed without fixating on the worst outcomes, and it’s possible to be prepared without being anxious. Protect your mental health during a recession by reminding yourself economic slumps are usually short-lived.

Weathering Any Storm

Recessions are a part of life. The good news is experts know how they work, so there are reliable ways to prepare for and get through them unscathed. Your best bet is to create an emergency savings account, hold on tight to your investments, reduce your debt and wait to make large purchases until after the recession ends.

Above all, keep a clear head and do your best not to make any irrational financial decisions. Things will be back to normal before you know it.

Inflation moved the S&P 500 (SPY) this week as the December Consumer Price Index (CPI) report was released on Thursday. Let’s break it down in today’s issue. I think the results may surprise you.

shutterstock.com – StockNews

(Please enjoy this updated version of my weekly commentary originally published January 12th, 2023 in the POWR Stocks Under $10 newsletter).

Reflecting on the Consumer Price Index (CPI) report this past week, here are the two most interesting data points I saw:

Home prices increased just 0.8% compared to last month. Shelter accounts for about a third of CPI. Gains in this line have levelled off and are no longer driving large jumps in inflation.

Used car prices were down 2.5% last month and down 8.8% over the past year. While used car prices account for a much smaller portion of CPI — just 3.6% — Fed officials blamed the spike in used car prices for inflation when it began rising in 2020. I’d bet Fed economists are still watching the data and are pleased with this drop.

This month’s report also marked the third consecutive downtrend in consumer inflation.

I’m not going to come out and declare that we’ve won the war—if you’ve been reading these issues for the past few months, you know I think there is still more room for downside than upside—but I will go on record saying things are trending in the right direction.

The fact that we now have three consecutive months of reports all pointing in the same direction is very positive.

Additionally, the fact that the labor market has somehow remained healthy gives me a spark of hope that the elusive “soft landing” may actually come to pass.

I found the details to be encouraging. And based on the rally that took place afterward, it looked like other traders agreed.

About an hour after the report was released, the stock market (SPY) opened. Shares were down a little on the open but rallied and ended the day higher.

This may actually be bullish…

There’s so much more that could be said about the Fed and inflation and what all of this means going forward.

A number of analysts are concerned about what things look like later in the year if inflation plateaus, potentially forcing the Fed to to keep rates high.

I do believe Powell when he says there won’t be rate cuts in 2023, but I also know that the Fed members make their decisions based on data.

It really all just depends on whether the trend stays in place.

Conclusion

Stocks are still up for the year, and the latest inflation data points are marking out a bullish trend. Is it too good to be true? We’ll find out at the beginning of February when the Fed meets again.

What To Do Next?

If you’d like to see more top stocks under $10, then you should check out our free special report:

What gives these stocks the right stuff to become big winners, even in this brutal stock market?

First, because they are all low priced companies with the most upside potential in today’s volatile markets.

But even more important, is that they are all top Buy rated stocks according to our coveted POWR Ratings system and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks which could double or more in the year ahead.

SPY shares closed at $398.50 on Friday, up $1.54 (+0.39%). Year-to-date, SPY has gained 4.20%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Meredith Margrave

Meredith Margrave has been a noted financial expert and market commentator for the past two decades. She is currently the Editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Meredith’s background, along with links to her most recent articles.

The recent short covering rally in Tesla stock provides a better price point to position to profit on a further pullback in TSLA.

shutterstock.com – StockNews

Tesla(NASDAQ:TSLA) is in trouble. It is down $80 a share (40%) in the past month and a half and $260 a share (67%) since making a high last April. And it’s becoming increasingly clear that China — the very market that the company once appeared dependent on for survival — may ultimately spell even more trouble for Elon Musk in the weeks and months to come.

In October, Morgan Stanley analysts said that Tesla Motors is so dependent on the Chinese market that it is essentially a Chinese tech stock. “We estimate Tesla generates as much as one-half of its profitability from the Chinese market,” they remarked, “arguably making the stock a derivative of a Chinese tech stock.” That’s a problem when considering Musk’s sales in China continue to plummet, and Musk’s business ties to China continue to incite congressional movement.

Following China’s slashing of a pro-Tesla subsidy program, deliveries of its China-made cars hit its lowest point in five months in December, causing TSLA to cut prices in the country for the second time in three months. As of today, prices are now down between 12% to 24% from September.

Is this a minor stock blip? History indicates that it may not be. In fact, in 2017 when the country scaled its tax subsidies back significantly, car registrations plummeted over 95%, so Tesla’s travails just might be getting started. Even China has conceded that Tesla may need to take drastic actions to stay afloat, with the China Merchants Bank International (CMBI) saying that, “Tesla needs to further cut prices and expand its sales network in China’s lower-tier cities amid ageing models.”

Worse news for TSLA is that, even if Musk does right this ship with China, the new Congress is highly expected to crack down on companies that they perceive to be tied too closely to the communist regime this year. And Musk’s companies appear to be at the top of this list.

Last year, The Wall Street Journal published a news story that expressed legislators’ “concerns…on the potential for China to gain access to the classified information possessed by Mr. Musk’s closely held Space Exploration Technologies Corp., including through SpaceX’s foreign suppliers that might have ties to Beijing.” The piece went onto state that some lawmakers are troubled “by the lack of clear lines between SpaceX and auto maker Tesla Inc.” These concerns caused Rep. Chris Stewart (R-UT), who sits on the House Permanent Select Committee on Intelligence, to call for classified briefings and Sen. Marco Rubio (R-FL) to introduce a bill that would seemingly restrict the government from utilizing contractors like Musk who retain their ties to the Chinese Communist Party.

Now that the House and Senate is split between Republican and Democratic control, expect regulating companies like Musk’s to become an even bigger congressional priority as it represents one of the only ways they can govern in a bipartisan fashion 2023. As a senior fellow with the Chongyang Institute for Financial Studies put it, “only through the topic of containing China is it possible for both parties to form a united front. This is not because China has really become the enemy that will destroy the U.S. tomorrow morning, but because they can’t reach a consensus on many US domestic problems, they can only use China to shift the subject.”

The election of Kevin McCarthy as Speaker of the House has only compounded the concerns for TSLA’s future. He said this summer that he will lead a congressional delegation to Taiwan and co-authored an op-ed with Rep. Mike Gallagher (R-Iowa), chairman of the Select Committee on China, titled, “China and the US are locked in a cold war. We must win it. Here’s how we will win it.” Expect him to partner with Sen. Majority Leader Chuck Schumer (D-NY) to address the perceived China threat in some capacity.

Certainly, some big players are looking for the recent rebound in Tesla shares to reverse. Almost 10,000 of the February $100 puts traded Friday at around $3.00. This equates to roughly a 3 million dollar wager that the sell-off in Tesla has further to go.

The big-time buyer of these put options is positioning more pain in Tesla stock and a meaningful break of the $100 support level. Using bearish put options in place of shorting the stock allows the trader to participate in the downside in a defined risk manner.

Add this all up, and it appears that TSLA is in a classic “damned if you do, damned if you don’t” scenario. Fixing its profitability problems in China may help it in the immediate short term — but doing so may only fuel its looming congressional regulatory crackdown in ways that could significantly affect sales in its largest market, the United States. Investors would be wise to stay away until this dust settles.

POWR Options

What To Do Next?

If you’re looking for the best options trades for today’s market, you should check out our latest presentation How to Trade Options with the POWR Ratings. Here we show you how to consistently find the top options trades, while minimizing risk.

If that appeals to you, and you want to learn more about this powerful new options strategy, then click below to get access to this timely investment presentation now:

TSLA shares closed at $122.40 on Friday, down $-1.16 (-0.94%). Year-to-date, TSLA has declined -0.63%, versus a 4.20% rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

Opinions expressed by Entrepreneur contributors are their own.

Some projections state that a new startup could take as long as four years to start earning a profit. Your business may be growing, but waiting four years may not be an option. If you want to start earning passive income that you can use to grow your business, then the stock market may be a viable option. If this is your first foray into stock investing, then the 2023 Stock Candlestick and Options Profit Trading Bundle could help you learn to be a wise investor.

StackCommerce

This course can help you mitigate your risks and maximize potential payouts. It contains 25 hours of instruction, starting from the basics. Get your first look at investing strategies in Options Trading 101 and Learn to Trade Options from Some of the Industry Greats. Both of these courses are led by professionals from MoneyShow, an investment advising organization with 40 years of experience.

Once you’re confident in your investment strategy, you can automate it using Python and a style of coding you could learn in the course Automatic Stock Trading with Python. It even comes with its own automatic trading bot that can make investments for you based on parameters you input.

The bear market has been downright brutal for growth stocks. Thus making it clear that now is the time for value. That is why you need to discover the attractiveness of Bristol-Myers Squibb (BMY) shares. Read on below for the full story.

shutterstock.com – StockNews

Bristol-Myers Squibb (BMY) is the poster child for a stock to own during a bear market. First, because it’s in the defensive healthcare industry which doesn’t buckle when the economy is under pressure. Second, the north of 3% dividend yield is a welcome sight when you bank account pays nothing on cash.

Add it all up and you understand why shares were in positive territory in 2022 when most other stocks were painted red. Gladly with the market outlook still dark because of looming recession, BMY continues to be a terrific choice for the year ahead.

As noted above, healthcare is always a safe haven for investors in the midst of recession and growth concerns as most people will sacrifice spending in other places to stay on a healthy track. This notion shows up quite clearly in their long term earning track record with only 1 miss in the past 20 quarters. And that includes 4 straight beats in 2022.

On the POWR Ratings front it is chock full of high ratings that point to strong price action ahead. That party starts with A overall + A for Value. After that you have a string of B’s for Stability, Sentiment and Quality.

Stability points to lower beta and better nights sleep during rough times. Whereas Quality says it’s extremely well run company likely to continue to produce positive earnings results in the future.

Just for good measure BMY offers healthy income to go along with the growth and value story. When cash is paying virtually nothing, then it certainly helps the ROI story when you add a nearly 3% dividend yield into the mix.

This really is an all-weather value stock. But especially beneficial to consider when the bearish storm clouds are still in the air.

Want to Discover More Value Stocks?

BMY is just 1 of 7 attractive value stocks found in a new special report we just put together. Click the link below to claim your free copy now:

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

BMY shares were trading at $71.65 per share on Thursday afternoon, down $0.29 (-0.40%). Year-to-date, BMY has gained 0.37%, versus a 4.02% rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

In the face of the current adverse economic conditions, many would-be retirees are worried about their financial capacity. Inflation remains elevated, matched with skyrocketing interest rates on borrowing. Financial advisers and personal loan management experts may recommend adding more sources of income to cover their living expenses and loan repayments upon retirement.

Due – Due

It’s no surprise that many people postpone any retirement plan and get back to the hustle and bustle of the office. A recent survey indicates that retirement delays in the private sector have doubled in the last year.

However, amidst rampant financial insecurity, more opportunities are being offered in the market. It may not be too late to compare various financial products and get one for retirement.

Retirement savings accounts and investments are the most common sources of retirement income. But there are more ways to improve your finances while building asset protection.

Life insurance may be the first thing you consider, but are you familiar with annuities? Research shows that 39% of investors aged 55 and above are not. Although that sounds like a lot, it’s still a notable improvement from 47% in 2014. Of those who do understand these financial plans, over 80% appreciate their value, which is an increase from pre-pandemic levels.

People are learning powerful lessons from the events of the last two years. This article considers annuities and how they work to provide you with a retirement income.

What Is a Non-Qualified Annuity?

Annuities are insurance contracts issued by financial institutions like banks and insurance companies, which guarantee a fixed investment fund payout in the future. You can invest in them or purchase them with premiums or lump-sum payments.

After accumulating funds, you can start receiving payments at a fixed schedule for a specific period or as long as you are alive. Even better, you can structure an annuity into different financial instruments, giving you more flexibility. So, annuities provide an effective retirement income stream if your savings are insufficient.

Annuities provide a consistent cash flow for annuitants upon retirement in addition to other ordinary income. It assures you of a steady income stream even if you outlive your assets. In the event that more than savings and dividends from investments are needed, it’s a good idea to consider purchasing an annuity contract.

But before we focus on non-qualified annuities, we must first differentiate annuity products from life insurance. The table below shows the fundamental difference between the two financial products.

Life Insurance vs. Annuity

Life Insurance

Annuity

A death benefit, so not a retirement plan.

Payout is distributed as long as the recipient is alive.

Dependents receive the income.

Policyholders receive fixed payouts like an income stream.

Life insurance is not subject to income tax.

Subject to tax, but the extent varies according to type.

Put simply, annuities are the opposite of life insurance. They can be qualified or non-qualified, which determines how taxes may apply to them. A non-qualified annuity is an investment vehicle bought with after-tax dollars. It can help reduce taxes upon retirement while providing tax-deferred income.

But that doesn’t mean you can use them to avoid taxes completely. You don’t have to pay taxes as your money accumulates; instead, you will pay taxes when you receive a payout. Withdrawals and lump-sum payments are taxed as ordinary income, not capital gains. The good thing is that it only applies to gains or earnings of non-qualified annuities since taxes are already deducted upon purchase and contribution.

For example, let’s say you purchase a retirement plan. Once you reach retirement age, you can either take withdrawals or annuitize them. If you choose the former, taxes apply as last-in-first-out (LIFO). The withdrawal amount is taxed first as the growth element of a non-qualified annuity. However, the extent of taxation is only up to the amount of gains. Once the withdrawn amount exceeds gains, subsequent withdrawals will become tax-free. Let’s say your $100,000 deposit becomes worth $250,000; you’ve gained $150,000. So, every dollar you withdraw up to $150,000 is taxable. Gains are treated as the last in and are therefore taxed first.

It is possible to contribute to an annuity without paying taxes on payouts after retirement. You can accomplish this by funding it in a Roth account like a Roth IRA or Roth 401k. However, there are contribution limits to this type of retirement account.

What Is the Purpose of a Non-Qualified Annuity?

A non-qualified annuity is one of the best tax-deferred investment options for people who have already used up retirement plans offered by their employers. It’s another way to save while generating gains and receiving fixed payouts or a lump-sum value in the long run.

Often, annuities have two phases, namely, the accumulation and the distribution phase. The accumulation phase refers to the part where you pay premiums while your money grows. You may withdraw funds but face tax or early withdrawal penalties during this phase. Typically, the penalty amount is a specific percentage of the withdrawn amount.

The distribution phase happens when you receive payouts through self-directed withdrawals or scheduled payments. You have the option to either withdraw the lump-sum value or annuitize it. If you withdraw it, you will receive taxable earnings on top of the principal amount. That way, the principal amount remains intact while generating new earnings. If you choose annuitization, it will provide you with a fixed income stream after retirement, but you cannot get the lump-sum value of the annuity. Either way, earnings are subject to taxes, but you have more control over your funds.

When the annuitant dies, the payout schedule and terms may vary. Some plans may allow you to have a beneficiary receive scheduled payments. Some do not have this option, so payouts end upon death. If you choose not to annuitize your fund, your beneficiary will receive a death benefit to the value of your annuity.

Qualified vs. Non-Qualified Annuity: How Are They Different?

As we discussed above, annuities can be qualified or non-qualified. As with the non-qualified type, individuals can contribute to their qualified annuities while their money increases. Accumulation and distribution phases are present in this type, too. Additionally, they can get the lump-sum value or annuitize contributions for scheduled payments. But these annuity products have notable differences regarding contribution, distribution, and withdrawal mechanisms.

First, qualified annuities are purchased and funded with pre-tax dollars, unlike non-qualified ones. Contributions are deducted from the person’s gross income and increase tax-free. Upon retirement, payouts are subject to taxes. But potential income may be smaller than non-qualified annuities due to contribution limits. Qualified annuities are capped according to the person’s income and whether they have other qualified pension plans.

With regard to early withdrawals, both types are subject to a penalty, typically 10%, but the extent may vary. Both types set a minimum withdrawal age of 59½, so withdrawals before that age have corresponding penalties. For non-qualified annuities, only the earnings and interest are typically subject to the penalty. For qualified plans, the entire amount is subject to a tax penalty.

Once you reach the mandatory withdrawal age of 72, you can withdraw funds or receive a guaranteed income. That applies to qualified annuities, whereas non-qualified annuities do not set a mandatory withdrawal age. Once you withdraw or start receiving payouts, qualified annuities have a different tax treatment.

Except for a Roth IRA, these are subject to required minimum distribution (RMD) guidelines. The whole distribution amount is taxable for the payouts since the contribution is made using before-tax dollars. Also, if you purchase one to fund a retirement plan or an IRA, you will not have additional tax deferral benefits for that plan. But for a non-qualified annuity, only the earnings are taxable.

What Are the Different Types of Non-Qualified Annuity?

Before deciding what non-qualified annuity products are best for you, you must first investigate the different options. You may want to get one to cover your living expenses after retirement. Knowing how much you need and how much return you want to generate is essential. That’s why proper financial planning is so important; the earlier, the better. Talking with a financial advisor may help you become familiar with your options.

Immediate and Deferred

Some annuities may start immediately upon the deposit of a lump sum of money. This is referred to as an immediate annuity. It’s the opposite of the typical annuity that has to season for a period of time and accumulate before funds can be withdrawn or annuitized. Put simply, an immediate annuity is purchased with a single lump-sum payment. It then starts distributing payouts right after you buy it.

For example, you sell your car and use the proceeds to purchase an immediate annuity. It will provide you with an agreed-upon income scheduled for a specific number of years or as long as you live. However, you cannot invest or spend your purchased annuity in any other way. Remember that you ensure a specific outcome when you buy immediate annuities, not investing. To be precise, the outcome you will get is income in your retirement years or for the specified period you prefer.

Annuities can also be structured as deferred benefits. A deferred annuity or deferred income annuity will take time to pay out after the initial payment. Instead, holders choose an age at which they will start receiving payouts.

This type is more suitable for a retirement account. Since it is a tax-deferred growth annuity, you only pay tax when you withdraw. This is the typical sort as opposed to an immediate annuity.

Also, a deferred non-qualified annuity has no contribution limits. You can even invest it with an insurance firm and choose among fixed, variable, equity-indexed, and longevity contracts. You will pay income tax on gains once you withdraw.

Depending on which type you choose, you may or may not recover some portion of the principal invested. It’s more typical in a straight or lifetime payout for there to be no refund. The payments continue as long as the annuitant lives, and there is no death benefit. There are some options in which annuitants can declare beneficiaries and continue receiving payments once they die. But if the annuity is only for a specific period of time, payouts will last until the period ends. Annuitants or their beneficiaries can withdraw or refund the remaining principal.

Fixed, Variable and Indexed

Annuities can be structured according to varying levels of risk tolerance. Financial advisors will consider market volatility and your financial position before taking risks. You may prefer to play it safe, but you stand to benefit from higher potential returns if you agree to face more risk.

A typical example of a safe investment is a fixed annuity. This type has a guaranteed and conservative interest rate set by the insurance company. The fixed option is a perfect fit for low-risk investments.

On the other hand, a variable annuity is invested in securities like stocks, bonds, and mutual funds, which tend to yield more. The earnings are based on the performance of the securities you select. You may choose either type or a combination of the two.

Variable annuities are riskier, especially now that market volatility remains high, leading to a bearish trend in the stock and bond market. Therefore, they are more suitable for those with higher risk tolerance.

If you want better returns than a fixed annuity but wish to avert risks in a variable annuity, consider choosing an equity-indexed annuity. With this type, you may enjoy the best of both worlds. You can realize upside growth based on market performance without negative yields. This annuity generates credited interest varying with the performance of an equity market benchmark. It includes the S&P 500 and NASDAQ composite indexes. But since it has a 0% floor, some EIA cap gains and fees can eat away a huge chunk of the account value during downtrends in the market benchmark.

Protect Yourself, Learn More About Non-Qualified Annuity

Having a foolproof retirement plan has become more crucial than ever. You have to ensure adequate financial capacity, especially during economic downturns. Fortunately, a non-qualified annuity promises financial safety. You can generate an income stream to fund your living expenses after retirement while adding an extra layer of protection.

Growth stocks are back! And, they are poised to lead the S&P 500 (SPY) higher after the brutal bear market investors experienced in 2022. Read on to find out the best strategy to profit from the next big bull market in growth stocks.

shutterstock.com – StockNews

Earlier in 2022, we unveiled an important article titled…

The crux of this popular article is that it was a precarious time for growth stocks. And, we gave readers specific advice on avoiding particular stocks that were egregiously overpriced. This included:

Using the POWR Ratings to eliminate the worst growth stocks

And, it’s a major reason why the service has so greatly outperformed all the most popular growth ETFs and even the Nasdaq.

BUT, it’s NOW time for an IMPORTANT update.

Conditions have been improving for growth stocks. Ironically, this is just as fund managers and retail traders have capitulated on their holdings.

Valuations have become incredibly enticing as the bear market has created a bounty of GARP (growth at a reasonable price) opportunities for savvy investors.

In the POWR Growth service, we have responded by snapping up the healthiest of these stocks with the most enticing upside potential.

The job is not done as we continue to identify enticing opportunities in the alternative energy space, biotechs, genomics, and cloud computing.

These are companies that will grow earnings at a double-digit pace over the next decade and have all the characteristics of becoming leading stocks in the next bull market.

As Warren Buffett said, “A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at good prices.”

Life-changing returns can be unlocked by investors who are able to put aside their emotions during challenging economic times and act in a logical and intelligent manner.

It’s not unusual for leading stocks in a bull market to deliver returns in the 3-digit, 4-digit, or even 5-digit range. The key is to buy them early and patiently hold as long as fundamentals continue improving.

In the POWR Growth service, we have done the hard work of sifting through the rubble to find the companies that are still growing, expanding margins, and generating free cash flow (or on the path to).

In order to take advantage of this opportunity, professional investors spend countless hours investigating, learning, and identifying the growth stocks that have been unfairly punished during the selloff.

For those of you who don’t have that kind of time, the POWR Growth service will allow you to confidently invest in high-quality, undervalued growth stocks with significant potential.

This active trading service achieves consistent outperformance by going way beyond the outdated buy and hold (or buy and hope!) approach that many newsletters offer.

That’s because it takes a systematic approach to zero in on the market’s best stocks, by utilizing the computer driven Top 10 Growth Stocks strategy with average annual returns of +46.85%.

I then carefully examine what is going on in the markets and tell you exactly what to buy, when to buy AND what to avoid.

I’ll also let you know when it’s time to get more defensive to preserve capital (as we did for most of 2022) and when it’s time to get more aggressive again to maximize your gains.

This exclusive portfolio gets most of its fresh picks from our proven “Top 10 Growth Stocks” strategy which has produced stellar average annual returns of +46.85%.

And yes, it continues to outperform by a wide margin even during these rough and tumble markets.

If you would like to see the current portfolio of growth stocks, and be alerted to our next timely trades, then consider starting a 30 day trial by clicking the link below.

SPY shares were unchanged in after-hours trading Friday. Year-to-date, SPY has gained 4.20%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Meredith Margrave

Meredith Margrave has been a noted financial expert and market commentator for the past two decades. She is currently the Editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Meredith’s background, along with links to her most recent articles.

Hey are you enjoying the early gains for the 2023 stock market? Me too. Unfortunately this appears to be a mirage with the S&P 500 (SPY) ready to head lower…and probably make new lows in the months ahead. Why is that? Read on below for the answer.

shutterstock.com – StockNews

The market has been hot out of the gate to start the new year. Perhaps too hot as the applause for softer inflation blocked out the noise that these lower prices happened because of serious recessionary red flags.

I sense this may be the last gas for bulls and the bears are about to take the steering wheel again.

Why?

That will be the focus of today’s commentary…

Market Commentary

The new year always brings with it fresh optimism. That alone could explain the +4.2% showing for the S&P 500 (SPY) to kick off the year.

On the surface, bulls can point to exciting news that inflation continues to decline. That was the headline read for sure, especially after the 1/12 CPI report. Let’s dig in deeper on that one…

At this stage month over month is more important than year over year. That’s because most of the inflation pain happened many months ago, especially in the spring of 2022. That makes inflation look high year over year…but the month over month tells you the true current pace.

On that front we see Core Inflation up +0.3% month over month which points to annualized +3.6% which is nicely lower than the past…but still well above the Feds desired 2% target.

More specifically “sticky inflation” is still a problem. This report shows an +0.8% increase in shelter prices (housing) which translates to nearly 10% a year. Far too hot.

Further wage inflation was report last week at +4.6% year over year with a slight slowing of trend to +0.3% month over month (+3.6%) per year.

The sum total of this information says that the Fed will not change there tune. So given what the Fed has said in the past about keeping rates higher for a long time…and then repeating that mantra over and over again including this past week…then it points to the February 1st Fed announcement as another cold shower for bulls.

Now let’s get to what is causing lower inflation. That being 9 straight months of restrictive Fed policy that is finally doing its job. However, that is the view over the left shoulder. If you look over the right shoulder you will see it has come at the cost of an economy on the brink of recession.

48.4 ISM Manufacturing on 1/4 with 45.2 New Orders (reads recession)

49.6 ISM Services on 1/6 with 45.2 New Orders (reads recession)

89.8 NFIB Business Optimism Index on 1/10 (lower reading than during Covid…reads recession)

1/13 Earnings season begins with 2 of the 4 major banks soiling the bed. JPM warning that they are braced for recession.

Note that the US has not had an inflation induced recession since the 1980’s, so investors are a bit out of tune on how to handle this rare environment. Meaning they are far too interested in watching inflation data and predicting the likely Fed response as opposed to what they should be doing. That being to monitor the health of the economy as their guide of whether to be bullish or bearish.

If recession is on the way, that begets lower corporate earnings (typically 20% drop in EPS) and this begets lower stock prices given what investors are willing to pay for that weakened earnings profile. This is why it’s very hard to be bullish at this time.

Let’s press forward with a discussion of earnings season. The previous quarter was likely one of the worst in years as earnings estimates got slashed precipitously for coming quarters. Another round of that would be harmful to stock prices.

This means we have to watch earnings trends closely. Specifically speaking, the change in estimates going forward and if the current expectations for a 7% decline in earnings in Q1 darkens or brightens from here. That will have market moving consequences.

Here again, the average recession leads to a 20% reduction in EPS expectations. That is certainly not factored into stock prices at this time. All the more reason to watch earnings estimates more carefully. The early bank results foreshadow more pain on the way.

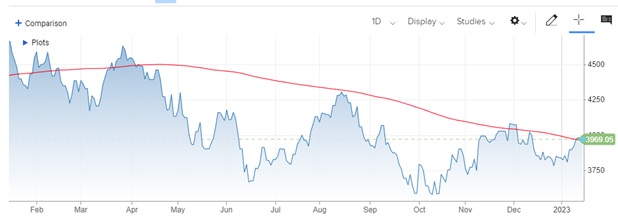

Now let’s rotate to price action. Bulls have already had some pretty impressive runs in the midst of the past years bear market only to get thwarted at the moment of truth. See S&P 500 one year chart below.

Be sure to focus on the 200 day moving average (red line) which keeps ending bullish advances. Both in mid-August and late-November and perhaps once again here in January.

Note that as of the Friday close the S&P stands at 3,999 while the 200 day moving average is at 3,981. Sounds scare that we are above that mark at this time. But before joining the bull party, please hear me out.

This is VERY typical behavior at the end of a bull run. Especially one that ends on a Friday.

Here we had premarket futures down 1% after some really bad bank earnings reports. Yet even then I knew that stocks would end the day higher pressing up against 4,000.

Why?

Just call it pattern recognition as I have seen it many times before. That being where the bulls have just enough energy to punch back one more time setting up a cliff hanger type moment: Will we break higher?…Are will the bear be back on the prowl? Tune in next week for the exciting conclusion.

Unfortunately, the Friday action is kind of like sprinting into the tape at the end of a marathon…just not a lot of energy to run again any time soon. This sets up for high likelihood of downside action on the way. However, I admit that anything is possible and indeed the bulls could have a couple more laughs in store.

Yet with the recessionary clouds darkening and earnings season off to a rocky start and the Fed likely to repeat their hawkish “a long time” mantra at the February 1st meeting…then I suspect we are soon at the end of this bullish run with more downside on the way.

Even if stocks do break above the 200 day moving average at this time, I would be hard pressed to join that party til the Fed announcement on 2/1 where they are likely to pour cold water on bulls once again.

What To Do Next?

Watch my brand new presentation: “2023 Stock Market Outlook” covering:

Why 2023 is a “Jekyll & Hyde” year for stocks

5 Warnings Signs the Bear Returns in Early 2023

8 Trades to Profit on the Way Down

Plan to Bottom Fish @ Market Bottom

2 Trades with 100%+ Upside Potential as New Bull Emerges

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares rose $0.08 (+0.02%) in after-hours trading Friday. Year-to-date, SPY has gained 4.20%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Opinions expressed by Entrepreneur contributors are their own.

Your employee is asking for a raise. And you can’t blame them. Inflation is running between 7-8%, and people need to, at the very least, keep up with the cost of living. This is now the norm in 2023. It’s happening everywhere. Payroll company ADP recently reported that employees received 7.3% more pay over the past months — with employees changing jobs seeing more than double that amount. And many experts say that trend will continue through this year.

But giving raises is certainly easier said than done. Big companies may be able to absorb the additional costs. But if you’re running a small or even mid-sized business doing so isn’t so simple. The good news is that there are options. So before handing out that raise and shouldering that extra expense, here are seven things you can do that may lessen the impact.

Consider a profit a sharing plan for your employees or a bonus tied to achieving agreed-upon goals. When someone asks for a compensation increase, this can be viewed as a mutual opportunity. You can be the one to happily agree to pay that increase — perhaps even more than what’s being requested — as long as you receive something in return. People don’t have to be in sales to earn a commission. You can set specific job-related goals that either increase revenues and productivity or decrease expenses so that a specific return on investment can be achieved, with added profits shared.

2. Offer more PTO and flexibility

Instead of increasing pay, consider increasing paid time off. Or provide more flexible work hours. Or maybe this is the time to implement a four-day workweek program or expanded work-from-home benefits.

Compensation does not always have to be in cash. People value their time just as much. Flexibility is important, and one of the biggest benefits of working for a small business is the ability to have that flexibility without the bureaucratic oversight experienced by employees at larger companies. Yes, paying someone not to work is still an added cost to you. But if you both agree on job deliverables, you and your employee can together make sure the work gets done on a schedule that suits you both.

Many business owners forget that, in most cases, health insurance payments are both non-taxable to the employee while still being deductible for the employer. If you just give a salary increase, the employee gets taxed, and you have to pay employer payroll taxes. But if instead, you offer to pay more for health insurance, you both save money on taxes, and the employee gets more in their net paycheck. It’s a win-win. Of course, talk to your tax accountant to make sure there are no other factors that would impose on this benefit.

4. Pass through the cost to customers

If you increase your employee’s pay, you may consider passing that cost increase to your customers in the form of higher prices or fees. But be careful. You don’t have to pass on the full amount of a pay increase if you can find savings elsewhere. And if you spread the cost across your entire overhead so that it’s fully absorbed, you may find it easier to spread the price increase across many customers and products and therefore cushioning the impact.

5. Offer a long-term employment contract

When an employee asks for more compensation, you can also ask for something in return: a longer-term commitment. Although most employer/employee relationships are “at-will” which means that both can end things whenever they want, by entering into a longer-term contract you can not only set goals and include future benefits that can be earned, but also agree on a fixed compensation increase over the term of that contract that will enable you to better budget your future costs.

6. Do a 401(k) match

Instead of a salary increase, you can offer to increase your 401(k) retirement plan match for that employee. Not only does that employee receive that money on a pre-tax basis (which means that you can pay a lower amount to the employee). It also means more money in your employee’s 401(k) account, which they can put away for retirement. You also don’t fail any of the required “discrimination tests,” which limits your contributions as a higher-paid employee or owner. Also, thanks to the recently passed Secure 2.0 retirement legislation, some businesses will soon receive a tax credit of up to $1,000 per employee every year for five years when they contribute to a 401(k) plan. This means you can give your employee added compensation and the government will pay for it!

7. Finally, consider an ESOP

Thanks to an aging population, there has been a significant increase in interest in employee stock ownership plans or ESOPS. So rather than dolling out increased compensation to your existing workers, you can create an ESOP where you get paid for a portion of your equity that you sell to an entity owned by your employees, and then you receive significant future tax benefits on both your payback to the bank for financing the transaction and for the income allocated to that ESOP. A great resource to figure out whether an ESOP is right for your business is here.

You’re going to have to pay your employees more this year. That’s a given. But just because your employees request (and need) a raise doesn’t mean you have to bear the entire cost burden. There are options.

Opinions expressed by Entrepreneur contributors are their own.

Cryptocurrency is nothing new. While many people discuss the digital asset as an enigma, it is a medium of exchange worth significant value. True, digital coins do not have the same tangible backing as cash, but the security of design, and the blockchain setup, create (or should create) a level of confidence.

If your business has yet to embrace crypto as a form of payment, it is falling behind and missing valuable opportunities to thrive. While not all companies yet embrace crypto, those that do experience unparalleled access to otherwise distant consumer pools.

The number of companies embracing crypto is rising, including such names as Gucci, Paypal and Visa. Permitting crypto payment options can expand your market share and improve your position in the marketplace; it can also demystify this legitimate form of payment.

The reasons crypto is right for your business model

It is easy to look at the failings of FTX and lose confidence in the system, but investors and businesses need to review the market’s otherwise successful history. Bitcoin is only one asset out of thousands that continues to outperform investor expectations. The folly of one digital coin should not deter innovative businesses from embracing a payment option that proves time and time again its ability to persevere.

If your company wants to look toward the future, it must embrace crypto because it isn’t going anywhere. The financial “new normal” demands that businesses adapt and embrace changing structures. Besides the need to adjust, there are many reasons businesses benefit from accepting crypto payments.

Many companies are victims of friendly fraud or mistaken consumers. In the digital subscription age, many consumers don’t remember all their purchases and may report an issue of credit card fraud where there is none. Unfortunately, whether friendly mistakes or criminal, chargebacks cost businesses billions yearly.

Embracing bitcoin payments can reduce fraudulent chargeback risks. Crypto payments report to an immutable public ledger. The payment method does not allow for alteration, meaning once a transaction is complete, nothing can reverse it, eliminating the false claims of fraud on the purchase end.

Cryptocurrencies exist within the blockchain — a decentralized, distributed digital ledger. All transactions are permanent, unmodifiable, and impossible to delete. The entire crypto concept is a vision for secure monetary assets.

A business can improve the security and usability of crypto by partnering with blockchain monitoring services. Some payment processors will offer additional security measures; however, even bare-bones, cryptocurrency is more secure than credit cards and other payment methods.

Accepting crypto shows your consumers that you care about their security and yours. The additional security and finality of digital coins also provide assurances for businesses providing subscriptions or other services in a techno-focused era.

Credit card fees present a significant thorn in the side of many merchants. Fees represent a profit loss on individual transactions. Besides the on-top percentage taken from the sale, many credit card processors also charge a nominal fee per incoming transaction.

Cryptocurrency transactions eliminate any additional fee structures when handled on the business end. If you decide to use a payment processor (recommended), you will need to pay a service fee, typically less than traditional processors will charge.

4. Improve transaction speed, regardless of country of origin

Besides transaction fees, credit card transactions take time to process. As a business owner, you do not have time to waste. Most cryptocurrency transactions occur in real-time — one of the many perks of a decentralized system.

Traditional credit card or debit card payments can take several days, depending on a consumer’s location. Crypto is borderless, so location does not affect or inhibit transaction speed. Also, because the digital asset does not involve cross-country settlements or obstacles, there are no costly currency conversions.

The growth potential of crypto is twofold for business owners: financial and market share. Any crypto investor can tell you about the exponential growth of digital assets in recent years. For a business owner, the potential valuation increases for some cryptocurrencies are enough to embrace the payment method. Permitting crypto payments means you can potentially earn greater profits from the same volume of purchases.

Besides the monetary gains, permitting crypto also opens your business to a wealthier consumer pool and buyers who may not have considered your company before. Crypto allows for a level of anonymity and privacy that other payment forms do not. Newer, more private consumers will appreciate your business’s steps to secure their privacy.

6. Taking crypto means getting cash

You get cash, not crypto, for your payment by dealing with a reputable payment platform. Trusted platforms will convert crypto payments into cash. And by taking crypto, you’re making it easy for crypto holders to buy products and services, all while receiving cash in your bank account. It’s a win-win and a great cost-effective opportunity to increase your revenue.

Crypto is the future and the future is now

Whether a high-end, established retailer or a small, young business, it is time to use cryptocurrency, permitting it as a payment option. Digital currency is more secure than other transaction methods and allows for growth opportunities while maintaining consumer privacy. Embrace crypto and embrace the future of your business.

Your credit score impacts everything from getting a favorable interest rate on a credit card to buying a home, paying for insurance, and more.

Due – Due

If your current credit score is less than ideal, here are ten hacks to increase your credit score fast.

1. Dispute Errors on Your Credit Report

Because of your credit report’s far-reaching impact and the countless ways it affects your everyday life, it must be accurate.

If there’s an error on your credit report, you’ll want to dispute it immediately to clear the issue up to avoid bad credit.

So how do you do this?

First, get a copy of your credit report, which can be found in the Annual Credit Report.

Everyone is entitled to a free copy of their credit report every 12 months.

If you find an error on your credit file, you’ll need to dispute it with the credit bureau that made a mistake.

After filing a dispute, the credit bureau has 30 days to investigate the issue. If the information is found to be inaccurate, your credit report should be updated within those 30 days.

This resource from the Federal Trade Commission will walk you through the process of disputing credit report errors step-by-step.

2. Pay Your Bills on Time

This may sound like a no-brainer, but it’s hard to stress the importance of being prompt with paying your bills enough.

To quantify, debt payment history accounts for 35% of your credit score, making it the most critical credit scoring factor overall.

And research has found that a single late payment can lower your credit score by as much as 180 points.

Not only will always paying your bills on time help quickly build credit, but it can also save you money, as you’re less likely to encounter late fees with your credit accounts.

If you struggle with this, we recommend signing up for automatic payments or setting up reminders through email or on your phone.

Once you get in the habit, it should serve as positive momentum for credit repair and can go a long way in improving your credit score.

3. Reduce Your Credit Utilization Ratio

Your credit utilization ratio, simply put, is the percentage of your available credit that you’re currently using.

If, for example, you have $10,000 of available credit and you have $2,000 of debt on your credit card bill, your credit utilization ratio would be 20%.

This accounts for about 30% of your credit score, making it the second most significant factor after payment history.

And that’s precisely why you should strive to reduce your credit utilization ratio.

According to Experian, “your credit utilization ratio should be 30% or less, and the lower you can get it, the better it is for your credit score.”

If you’re currently sitting at 31% or higher, you’ll want to make every effort to get that number down to a max of 30%.

Once you do so, be sure to keep credit utilization in mind when deciding what percentage of your available credit to use in the future.

4. Request Credit Limit Increases

This ties into our previous credit score hack.

A simple way to reduce your credit utilization ratio is to get a credit limit increase.

Say, for example, you had $2,000 of debt with $5,000 in available credit.

You would have a credit utilization ratio of 40%, which is higher than it should be.

But let’s say you requested a credit limit increase of $3,000 for a new total of $8,000.

In that case, having $2,000 of debt would only mean a credit utilization ratio of 25%.

Just like that, you would use a smaller percentage of available credit, which should help improve your credit score.

Just be sure not to go overboard and request credit limit increases on several accounts simultaneously because it can signal to lenders that you may be a borrowing risk.

The longer your credit history, the better your credit score should generally be, and vice versa.

Following this logic, you should avoid opening new credit lines because, by default, it reduces the length of your credit history.

As a result, it’s likely to affect your credit score adversely.

This isn’t to say you should never do so, as it’s often unavoidable, and opening a new credit line is necessary for establishing yourself long-term.

But you should always be cognizant of it, and especially avoid opening multiple new lines of credit at once.

6. Pay Off Your Balance

Let’s go back to the credit utilization rate, where the less percentage of available credit you use, the better.

If keeping your credit utilization ratio no higher than 30% is good, paying off your credit card debt is even better.

And it’s a win-win because not only does paying off your debt help build credit, but it also prevents you from paying interest.

With the average person paying $855 in interest each year, this can help put you in better financial health.

So having a zero credit card balance goal is a massive two-pronged attack for improving your credit rating and keeping you out of unnecessary debt.

Plus, it makes you far more attractive to a credit card company.

7. Become an Authorized User on a Credit Card

Becoming an authorized user on another person’s credit card (the primary cardholder) means you can make purchases with the card as if it was your own.

Also, it means you’re responsible for repaying any debt that accumulates with the credit card.

This is another relatively simple but effective way to lift your credit score, especially if it’s on a card with a high credit limit, low credit utilization ratio, and good payment history.

Some experts even say this can help you achieve a credit score of 700 or higher after a few years.

And this is a popular way to help teenagers start to build credit.

As long as you and the primary cardholder pay off your debt quickly, this can help boost both of your credit scores at once.

In terms of who’s eligible to become an authorized user, it can be anyone who meets the age requirements of the credit card issuer, with examples being a spouse, partner, child, or close friend.

Ideally, the primary cardholder will have a good credit history, plenty of mutual trust, and someone who wants to improve both of your credit scores actively.

8. Have a Variety of Credit Accounts

Your credit mix contributes to 10% of your credit score, which means it’s helpful to use a variety of credit accounts.

Note that there are three main types of credit accounts.

Revolving credit – Accounts where you can repeatedly borrow and repay up to a specific limit (unsecured credit card, secured credit card, and credit lines)

Installment credit – Accounts where you borrow money in one lump sum and repay it, typically with interest, in installments (mortgage loan, auto loan, student loan, or any type of installment loan)

Open credit – Accounts where the debt balance has to be paid in full each month

If, up until now, you’ve only used a few types of credit accounts or less, adding diversity should contribute to achieving good credit and make you more attractive to lenders.

Note that you can also turn everyday expenses like paying rent into credit accounts of sorts.

Rent reporting services like BoomPay and PaymentReport will report you making your payments on time, which can further assist in credit repair.

9. Get a Credit Builder Loan

To put your foot on the gas pedal, you can get a credit builder loan that strategically aims to increase your credit score.

Unlike a traditional loan, where you get the money upfront and gradually pay it back over time, a credit builder loan is different.

With it, a lender holds the amount borrowed in an account, and you make fixed payments.

As you make payments, you gain more access to the funds — all the while, everything is made known to a credit reporting agency.

This makes it a great way to show you’re capable of making payments on time, which can catapult your credit score quickly, even without a credit card.

10. Avoid Closing Old Credit Cards

Let’s say you just got a new credit card, and you’re no longer using an old one.

You should close it out, right? Actually, no.

There are two main reasons why having multiple credit card options is wise.

Keeping old credit cards means having more available credit and extended credit history.

A lower credit utilization ratio often comes with a higher amount of available credit.

And with a longer credit history, you’re more established — something lenders prefer over borrowers with little to no credit.

While there might be exceptions, such as paying high annual fees, you’ll generally want to keep it around, as it should help you achieve better credit.

As you increase the length of your credit history and use a lower percentage of available credit, you can transform a low credit score into a fair, good, or even excellent one.

Wrapping Up

Many people’s credit scores aren’t nearly as high as they’d like them to be.

Fortunately, there are several ways to raise yours and achieve a good credit score quickly.

From disputing errors on your credit report to paying your bills on time to having a healthy credit mix, these are all integral to credit repair and should put you on your way to good credit.

Opinions expressed by Entrepreneur contributors are their own.

If you need funds for your enterprise, it can be very tempting to go for the first business loan on offer. However, there are a number of things you should look for before you sign on the dotted line.

1. The right loan type

As with personal finance, there are several different forms of business loans, so you need to choose the one that best suits the needs of your enterprise.

Traditional loans: These are the business equivalent of a personal loan, which can be secured or unsecured. You’ll borrow a set amount and have a set repayment schedule with a fixed interest rate.

Line of credit: A line of credit provides you with a set funding amount but you don’t need to receive and pay interest on the full amount. You can call down funds as you need them and you’ll only pay interest on the amounts you borrow.

Equipment financing: If you need funds to purchase equipment, this type of business lending is designed to suit your needs. The piece of equipment you purchase will act as collateral for the loan, so you can usually access more flexible terms.

SBA loans: SBA or Small Business Administration loans are an option if you would struggle to qualify for a bank business loan. The lending criteria is more flexible, which could be a more agreeable choice for new enterprises.

Before you agree to a business loan offer, it is well worth assessing the other types of business lending to confirm the loan is the best fit for your enterprise.

2. Manageable loan repayments

Before you sign the loan contract, you should have an opportunity to check the details of the loan repayment requirements. You will need to think carefully about whether you can comfortably accommodate the monthly payment in your budget, not only now but throughout the lifetime of the loan.

If you have concerns that the payments may be difficult, or you may struggle to meet the payment deadlines, it is best to look for another loan product. Missed or late payments can not only create additional financial stress but can have a massive impact on your credit.

This follows on from the previous point, but you should also be fully aware of what fees you will incur with your new business loan. In addition to paying interest, you may incur origination fees, and processing fees. These will be added to your loan principal or you’ll need to pay them upfront. Ideally, your new business loan will have little or no such fees.

You also need to watch for the fees you may incur during the lifetime of the loan. For example, you don’t want to get stung with a massive late fee if there is a mix-up at the bank. It is also a good idea to look out for early repayment fees. If your business finances change and you want to clear the loan, you won’t want a loan that imposes a hefty early repayment fee.

4. A good lender reputation

Unfortunately, not every lender in the market offers the same level of service, in fact, some can be downright risky. The adage of “too good to be true” certainly applies here. So, it is vital to investigate the lender’s reputation and be on the lookout for some red flags. These include:

No verifiable credentials: If the lender does not have a professional website and does not provide details of a physical address.

Lack of fee transparency: Lenders should be very clear about their loan fee structure, so you are completely aware of how much the financing options will cost.

Pressure selling: If the sales rep is trying to pressure you to immediately accept a business loan offer without presenting you with information and the time to study it.

5. The correct loan amount

While it may be tempting to get the biggest business loan you can get approved for, this is not likely to be a good idea. Likewise, if the loan offer won’t cover your immediate funding needs, it is not the right choice.

Think carefully about what funds you need and how you’ll use them, so you can be sure to obtain a loan for the correct amount.

6. An attractive interest rate

As with any form of finance, your interest rate will determine the cost of your business loan. Lenders will use a variety of criteria to determine your risk profile and therefore your rate. However, these criteria vary from lender to lender, with some lenders being more rigid and some lenders being more flexible.

If you have a brand new enterprise, you’re not likely to get the best rates, unless you have excellent credit yourself. But, it is still important to compare rates to ensure that you’re getting the lowest possible rate for your enterprise.

However, you may be prepared to pay a slightly higher interest rate if there are minimal fees or other benefits to the loan. So, don’t look at the interest rate comparisons without some context.

While you may not need the funds urgently, you are still likely to want to implement your plans as soon as possible. So, check the funding times each lender offers for their business loans. After you submit your application and receive approval, when can you expect to receive the funds in your bank account?

Some lenders can release funds in 24 hours or only a few days, but other lenders are slower. If you will have to wait weeks or months for your funds, it is a good idea to look at alternative options.

8. Solid customer support

Finally, it is worth checking the levels of customer support offered by your potential lenders. If you have queries or questions about your loan, can you speak to the support team quickly? Some lenders have phone helplines, while others rely solely on email or chat. So, you need to be comfortable with the customer support options.

It is well worth reading some reviews of the lender to see if there are any red flags about long call wait times, slow responses to emails or other customer support issues before you become a customer.

Bottom line

Getting the right business loan for your needs requires some time to compare the different aspects and lenders. When you follow the factors above and make sure to maximize each of them, you can save money, time and financial stress.

With inflation moderating for the sixth consecutive month, the Fed halting interest-rate hikes may not be too distant a possibility. Hence, shares of fundamentally strong and growing businesses Salesforce (CRM), ADT (ADT), and Rambus (RMBS) could be worth investing in. Continue reading….

shutterstock.com – StockNews

In line with consensus estimates, the consumer price index (CPI) for December 2022 fell for the sixth consecutive month to register an increase of 6.5% from a year ago. The 0.1% decline from the prior month marked the largest month-over-month decrease since April 2020. The core CPI increased 5.7% year-over-year, compared to 6% in November.

With aggressive interest-rate hikes by the Federal Reserve during the previous year starting to bring the current inflation cycle down from its peak of 9.1%, hopes of a sooner-than-expected moderation in the monetary stance of the Fed have been rekindled.

Given the expectations of buoyancy returning to markets in the not-too-distant future, it could be wise to load up on shares of fundamentally strong businesses Salesforce, Inc. (CRM), ADT Inc. (ADT), and Rambus, Inc. (RMBS), which are well-positioned to keep meeting their growth expectations.

CRM is a customer relationship management platform provider. The company’s Customer 360 platform connects customer data across systems, applications, and devices to help companies conduct commerce from anywhere.

On December 15, CRM announced its contribution towards helping Casey’s General Stores, Inc. (CASY) to achieve increased revenue and engagement with its customer base. By consolidating fragmented technologies and transitioning to CRM’s platform, CASY has been able to use automation effectively to conduct more marketing while incurring a lesser expenditure.