[ad_1]

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

[ad_2]

[ad_1]

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

[ad_2]

[ad_1]

Opinions expressed by Entrepreneur contributors are their own.

For anybody who has ever questioned why the stock market appears to defy logic and common sense, Brian Feroldi’s latest book, Why Does The Stock Market Move Up? is a must-read. Feroldi provides readers with a unique perspective on the factors that drive stock market growth.

Brian is a financial educator with 350,000+ followers on Twitter, 50,000+ Youtube subscribers, 40,000+ newsletter readers and a run a hugely popular online course. If you want advice on frameworks and mental models to help you invest better, you can book a one-on-one video call with him today.

A fascinating aspect of Feroldi’s book is his emphasis on the role of psychology in stock market investing. He argues that human emotions such as fear and greed often play a larger role in stock market movements than economic fundamentals or company performance. For example, when investors become too optimistic and start buying stocks at inflated prices, a market bubble can form that eventually bursts and leads to a sharp drop in prices.

Feroldi also explores the power of storytelling in stock market investing. He notes that investors are often drawn to companies with compelling narratives, even if the company’s financials don’t justify the hype. For example, the rise of Tesla’s stock price in recent years can be attributed in part to the charismatic personality of CEO Elon Musk and the company’s vision of a sustainable future.

Another key theme in Feroldi’s book is the importance of innovation in driving stock market growth. He points out that the companies that have been the most successful in the stock market over the long term are those that have been able to adapt to changing markets and technologies. For example, Amazon’s dominance in e-commerce can be attributed to its ability to continually innovate and disrupt traditional retail markets.

But perhaps the most valuable aspect of Feroldi’s book is his ability to distill complex financial concepts into simple, easy-to-understand language. He explains concepts such as stock valuations, dividends, and earnings per share in a way that even novice investors can grasp. This makes the book accessible to a wide audience, from seasoned investors to those just starting out.

In the end, Why Does The Stock Market Go Up? is a compelling exploration of the many factors that drive stock market growth. Whether you’re a seasoned investor or just starting out, Feroldi’s insights and perspectives are sure to help you make more informed investment decisions and better understand the mysteries of the stock market. Book a one-on-one video call with him today.

[ad_2]

Brad Klune

Source link

[ad_1]

There were plenty of reasons to be bearish on the stock market (SPY) coming into 2023. This is especially true with inflation still too hot leading the Fed to increase their hawkish behavior. And then came along the specter of a potential banking crisis that only increases uncertainty…and that only increases odds of bear market. Read on below to discover Steve Reitmeister’s updated market outlook, trading plan and top picks to stay on the right side of market action.

The S&P 500 (SPY) has been downright bludgeoned of late giving back nearly all of the hard fought gains from the start of the year. That selloff ended Tuesday with a welcome relief rally.

However, if we are being honest…there is not much real relief in sight.

Let’s review where we stand now, what lies ahead for stocks along with our trading plan to outperform.

Market Commentary

We have to talk about the elephant in the room first. Of course, I am referring to the serious concerns over the recent bank closures that evoke “Ghosts of Financial Crisis Past”.

Now let me insert an important disclaimer.

I AM NOT A BANKING EXPERT!

And the sad fact is that 99% of the articles you have read this past week are not written by banking experts either. So please do appreciate that what I share comes from the perspective of an Economics major with 43 years of active investing experience.

This seems like more smoke than fire…but there likely will be small brush fires here and there.

Meaning that after the financial crisis of 2008 that there is much more bank oversight than the past. Combine that with the fact that there is not an equity bubble like last time in real estate…nor have we created new INSANE financial debt instruments that could implode the financial system.

Add that all up and it doesn’t sound like we are on the brink of systemic failure of the banking system. However, there are isolated incidents of balance sheet weakness and mismanagement that needs to be cleaned up. Especially true for banks with too much crypto exposure.

Will there be more bank failures?

Most likely yes. Unfortunately, there is great incentive on the part of hedge funds that short stocks to find any weakness and exploit it to their benefit.

Heck, even Cramer has openly joked about how easy it is for a hedge fund to short a stock then circulate rumors that crush the share price. Easy pickens.

This creates great headline risk in the mean time as each new bank failure will lead to more uncertainty. And that uncertainty is on top of all the previous concerns about inflation + Fed Hawkishness creating a recession and deeper bear market. So now is a good time to transition to that conversation.

Stocks were already selling off in February and early March as the road signs read: Caution Ahead!

Meaning that inflation was still too hot leading the Fed to heighten their hawkish rhetoric that rates would likely go higher and stay in place longer than previously stated. And what was previously stated was that rates would get to at least 5% and be on the books through end of 2023.

The previous notion was plenty ample enough to grind the economy down to recessionary levels. Thus, the odds of even more hawkishness is why we have spent the last six sessions under key psychological support at 4,000. And the last four sessions under the 200 day moving average at 3,940.

Now let’s ponder an interesting notion mentioned in this article:

Goldman Sachs no longer expects the Fed to hike rates in March

Rolling back a month ago it was assumed that the 3/22 Fed meeting would come hand in hand with a 25 basis point increase in rates as we saw in February. Next came more hawkish posturing by Fed officials and the odds started to move towards a 50 point hike to more aggressively get inflation under control.

So, what would happen if the Fed paused rate hikes because of the banking crisis?

I actually suspect that investors would take that as a negative. That is because it would be a signal to investors that the Fed is SERIOUSLY worried about the stability of the banking system that they have to deviate so significantly from their hawkish plans.

Meaning that investors SHOULD NOT consider such a move as a dreamed of “dovish pivot”. Rather this would be the Fed hitting the panic button that the stability of financial system is now more important than fighting inflation (which they have dubbed as Public Enemy #1 for over a year).

For as funny as it sounds…let’s all pray that the Fed continues to hike rates aggressively at the 3/22 meeting as pressing pause could be much worse for stocks.

Note that on Tuesday morning the Consumer Price Index report came out. Yes, it was a notch better than expected at JUST 6% year over year vs. 6.4% previously. Please don’t lose sight that the inflation target is still 2% and we are a long way off the mark.

For those that want to say that inflation was really a problem in the Spring of Summer of 2022 and not really that much of an issue today…unfortunately that notion is hogwash. The proof is the 0.4% increase month over month which still points to a 5% annual increase pace. (AGAIN remember that the target level is 2%).

Wednesday 3/15 brings the more forward looking Producer Price Index report along with Retail Sales. And then after that all eyes will be on the 3/22 Fed rate decision. than actually becoming dovish.

Adding it altogether, this is still a bearish environment. Even if the banking issues were not on the docket I would still be pounding the table on how the Fed’s actions open the door to a recession and natural deepening of the bear market.

However, when you sprinkle the uncertainty of the banking issues into the mix, and the serious headline risk that lies ahead…that is just a nail in the coffin for early 2023 bullish aspirations.

Meaning that the 2022 bear market took a mini-hibernation break to start the new year. Now it is awake and hungry to devour stock prices even lower.

Not lower every day, week or month. But as we look out over the next several months you should expect much more downside. And yes, I suspect we will go even lower than 3,491 level from October.

That is why the Reitmeister Total Return portfolio is built to profit as stocks descend further into bear market territory. Gladly it is not too late to apply that strategy if you have not already.

What To Do Next?

Discover my brand new “Stock Trading Plan for 2023” covering:

Wishing you a world of investment success!

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”)

CEO, StockNews.com and Editor, Reitmeister Total Return

SPY shares . Year-to-date, SPY has gained 2.43%, versus a % rise in the benchmark S&P 500 index during the same period.

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The post Bear Market Odds Skyrocket! appeared first on StockNews.com

[ad_2]

Steve Reitmeister

Source link

[ad_1]

FRP Holdings, Inc. (NASDAQ:FRPH – Get Rating) EVP John D. Milton, Jr. sold 5,912 shares of FRP stock in a transaction on Monday, March 13th. The shares were sold at an average price of $55.98, for a total value of $330,953.76. Following the completion of the transaction, the executive vice president now directly owns 2,158 shares of the company’s stock, valued at $120,804.84. The sale was disclosed in a legal filing with the SEC, which is available through this link.

Shares of NASDAQ FRPH opened at $56.00 on Wednesday. The stock has a market capitalization of $529.76 million, a PE ratio of 116.67 and a beta of 0.58. The business has a fifty day moving average price of $56.21 and a two-hundred day moving average price of $56.59. FRP Holdings, Inc. has a fifty-two week low of $53.08 and a fifty-two week high of $63.52.

Several hedge funds and other institutional investors have recently added to or reduced their stakes in FRPH. Swiss National Bank raised its holdings in FRP by 7.4% in the 1st quarter. Swiss National Bank now owns 14,500 shares of the financial services provider’s stock valued at $838,000 after acquiring an additional 1,000 shares in the last quarter. Dimensional Fund Advisors LP increased its stake in shares of FRP by 1.0% in the 1st quarter. Dimensional Fund Advisors LP now owns 469,931 shares of the financial services provider’s stock valued at $27,162,000 after purchasing an additional 4,782 shares during the last quarter. Guardian Wealth Management Inc. increased its stake in shares of FRP by 1.8% in the 1st quarter. Guardian Wealth Management Inc. now owns 18,981 shares of the financial services provider’s stock valued at $1,097,000 after purchasing an additional 330 shares during the last quarter. Charles Schwab Investment Management Inc. increased its stake in shares of FRP by 2.5% in the 1st quarter. Charles Schwab Investment Management Inc. now owns 47,247 shares of the financial services provider’s stock valued at $2,731,000 after purchasing an additional 1,150 shares during the last quarter. Finally, Ancora Advisors LLC bought a new position in shares of FRP in the 1st quarter valued at $151,000. 45.89% of the stock is owned by institutional investors and hedge funds.

FRP Holdings, Inc is a holding company, which engages in the provision of real estate business. It operates through the following segments: Asset Management, Development, Mining Royalty Lands and Stabilized Joint Venture. The Asset Management segment owns, leases and manages warehouse and office buildings primarily located in the Baltimore, Northern Virginia and Washington DC area.

Receive News & Ratings for FRP Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for FRP and related companies with MarketBeat.com’s FREE daily email newsletter.

[ad_2]

ABMN Staff

Source link

[ad_1]

The solid financials and the efforts of Salesforce (CRM) to support the digital transformation of its customers worldwide have positioned the company for substantial growth this year. Moreover, the company has launched a new AI product, joining the trend with other major tech firms. However, is it too late to buy the stock in 2023? Read more to find out.

Salesforce, Inc (CRM) is benefiting from increased corporate spending on digital transformation initiatives. In this piece, let’s discuss the stock’s potential that still makes it a solid buy.

Investors are showing strong interest in emerging technologies such as artificial intelligence, machine learning, and blockchain, which have the potential to revolutionize multiple industries. This has led to significant investment in these areas from both private and public sources.

The global business software and services market is expected to expand at a CAGR of 11.9% from 2023 to 2030.

CRM has gained 35.7% over the past three months to close the last trading session at $182.89. Moreover, it has gained 7.6% over the past month. Wall Street analysts expect the stock to hit $223.26 in the near term, indicating a potential upside of 22.1%.

CRM recently introduced “Einstein GPT,” the world’s first generative AI CRM technology that uses a range of AI models and real-time data to deliver AI-created content across various customer interactions at scale. The solution also integrates with OpenAI’s ChatGPT technology.

CRM also plans to integrate Einstein GPT with its Slack instant messaging program. This move is part of the company’s broader push into AI technology.

Moreover, CRM’S venture capital division is introducing its biggest fund to date, worth $250 million, which will be invested in startups specializing in generative artificial intelligence. The company has previously invested in companies like Zoom, Snowflake Inc. (SNOW), and DocuSign Inc. (DOCU).

In addition, CRM’s fourth-quarter earnings exceeded expectations. Also, its full-year revenue was $31.40 billion, representing an 18% year-over-year increase, or 22% in constant currency, making it one of the strongest performers for a software company of its size.

Marc Benioff, Chair and CEO of Salesforce. “We closed FY23 with operating cash flow reaching $7.1 billion, up 19% year-over-year, the highest cash flow in our company’s history, and one of the highest cash flows of any enterprise software company our size.”

Further, CRM’s revenue is projected to be $8.16-$8.18 billion for the first quarter and $34.5-$34.7 billion for the current fiscal year. The company also expects non-GAAP earnings per share to be $1.60-$1.61 for the first quarter and $7.12-$7.14 for the full year.

Here is what could shape CRM’s performance in the near term:

Solid Top-Line Growth

During the fiscal fourth quarter that ended January 31, 2023, CRM’s total revenues grew 14.4% year-over-year to $8.38 billion. Its subscription and support revenues rose 14% year-over-year to $7.79 billion. Its non-GAAP income from operations rose 123.3% from the year-ago value to $2.45 billion.

Also, the company’s non-GAAP net income and non-GAAP EPS stood at $1.66 billion and $1.68, up 96.4% and 100% from the prior year’s quarter, respectively.

Favorable Analyst Expectations

CRM’s revenue and EPS for the fiscal first quarter ending April 2023 are expected to increase 10.2% and 64.5% year-over-year to $8.17 billion and $1.61, respectively.

Analysts expect CRM’s revenue for the fiscal year 2024 to rise 10.4% year-over-year to $34.62 billion. Its EPS is expected to grow 36.2% year-over-year to $7.14 in the current year. The company also surpassed the consensus EPS and revenue estimates in each of the trailing four quarters, which is remarkable.

Robust Profitability

CRM’s trailing-12-month gross profit margin of 73.34% is 50% higher than the industry average of 48.89%, while its trailing-12-month levered FCF margin of 32.60% is 384.1% higher than the industry average of 6.73%.

The stock’s 2.55% trailing-12-month CAPEX/Sales is 5.8% higher than the 2.41% industry average. Its 17.34% trailing-12-month EBITDA margin is 54.6% higher than the industry average of 11.22%.

POWR Ratings Reflect Promising Outlook

CRM has an overall rating of B, which equates to a Buy in our proprietary POWR Ratings system. The POWR Ratings are calculated by considering 118 different factors, with each factor weighted to an optimal degree.

Our proprietary rating system also evaluates each stock based on eight distinct categories. CRM has an A grade for Growth, consistent with its steady growth in the last reported quarter. It also has an A for Sentiment, in sync with optimistic analyst expectations.

Moreover, its high profit margins justify the stock’s B grade for Quality.

Within the 134-stock Software – Application industry, CRM is ranked #19.

Click here to access the additional POWR Ratings for CRM (Value, Momentum, and Stability).

Bottom Line

The stock is currently trading above its 50-day and 200-day moving averages of $162.71 and $161.07, indicating an uptrend.

CRM’s strong performance in the last quarter was a result of the company’s unwavering attention to executing its strategies proactively. This success has positioned it for a significant transformation in the upcoming fiscal year 2024.

Moreover, the company is riding the wave of the AI boom and is focused on increasing investment. With the software industry showing strong growth prospects, I think CRM might be an excellent stock to buy in 2023.

How Does Salesforce, Inc. (CRM) Stack up Against Its Peers?

While CRM has an overall POWR Rating of B, one might consider looking at its industry peers, eGain Corporation (EGAN), Commvault Systems, Inc. (CVLT), and Progress Software Corporation (PRGS), which have an overall A (Strong Buy) rating.

Consider This Before Placing Your Next Trade…

We are still in the midst of a bear market.

Yes, some special stocks may go up. But most will tumble as the bear market claws ever lower.

That is why you need to discover the brand new “Stock Trading Plan for 2023” created by 40-year investment veteran Steve Reitmeister. There he explains:

You owe it to yourself to watch this timely presentation before placing your next trade.

CRM shares were unchanged in premarket trading Wednesday. Year-to-date, CRM has gained 37.94%, versus a 2.43% rise in the benchmark S&P 500 index during the same period.

Her interest in risky instruments and passion for writing made Kritika an analyst and financial journalist. She earned her bachelor’s degree in commerce and is currently pursuing the CFA program. With her fundamental approach, she aims to help investors identify untapped investment opportunities.

The post Is It Too Late to Get in Salesforce Stock in 2023? appeared first on StockNews.com

[ad_2]

Kritika Sarmah

Source link

[ad_1]

Opinions expressed by Entrepreneur contributors are their own.

Every trader’s goal is to achieve greater success. They want more consistency, more profits and more time to enjoy life. These goals are very worthy, but few traders achieve them. Do you relate to this?

Every day, week, month or year, you set profit goals (I’ll earn “x” amount of profits), you set rules (I’ll follow my trading strategy to a tee), and you set desires (I won’t let emotions cloud my judgment), yet somehow you never seem to achieve these objectives. Even with the best of intentions and the best trading strategy, somewhere down the line, you find a way to lose your stability of mind, and your plan goes out of the window. It’s like living in the movie Groundhog Day — you relive the same stuff over and over again.

Related: Grow Your Wealth by Mastering Trading Techniques

Well, the reason that happens is that “we can’t solve problems by using the same kind of thinking we used when we created them.” You’ve probably heard this quote before — it’s from the great Albert Einstein. Another variant of it is: “What got you here won’t get you there.” And that makes complete sense if you think about it. How can you possibly expect to be successful in trading if you remain the same person that’s generating the results you’re currently getting? I’m not suggesting that you need to become a completely different person, but at the very least, some things have got to change — your trading psychology!

The next level in your trading will come with the next level in your mindset. What do I mean by this? Well, you’ll need to introspect and search within yourself to investigate the beliefs, stories and patterns that make you the person you are today, but which don’t serve you well in trading.

I’m talking about things like:

The stubborn clinging to certainty: The reality of trading is that it doesn’t give you the kind of security that you get with a time-clock-punching job. The market doesn’t hand timely paychecks, it delivers rewards and bonuses to those who are proficient at strategic risk-taking.

The fear of failure: Failure is a critically important part of any successful life because it’s how you grow. And so, when you fear to fail, you fail to reach your full potential.

The inability to see one’s own biases: As a trader, you need a greater ability and readiness to see through your own illusions and delusions and self-correct immediately.

Related: How Mindfulness Can Help Traders Succeed

There are other systems of beliefs and behavioral inclinations to discover about yourself, but those are the main ones, I’d say. Here are some questions you can ask yourself to uncover what’s holding you back:

What are my biggest fears and doubts when it comes to trading and investing?

Am I being too conservative or too risky in my approach to trading? Why?

What are my strengths and weaknesses as a trader, but more broadly, as a human being?

What limiting beliefs do I have about myself, the market or trading in general that might be holding me back?

What external factors, such as market conditions or economic events, am I using as an excuse for not achieving my trading goals?

What is in my control to change? What isn’t?

What steps can I take to improve my trading psychology and technical skills?

Am I setting realistic and achievable trading goals?

What is it about losses that upset me so much? Why? What would happen if I wasn’t so afraid of losses?

Am I being consistent in my trading approach, or am I constantly changing strategies?

What personal or life factors are affecting my ability to focus on trading and make sound decisions?

Reflecting on these questions and being honest with yourself is key. Your answers will help you identify beliefs, excuses, patterns and stories that aren’t conducive to market success. And reflecting on those answers will kickstart real change in your trading psychology.

From there, I invite you to contemplate these next series of questions:

What do I want to achieve in trading starting right now?

What belief do I want to internalize as of today?

What will I no longer tolerate in my trading?

What are three objective and measurable action steps that I can take every day or week or month that will keep me moving in the direction of my trading goals?

How can I stick with those steps through thick and thin?

Related: Trading Psychology 101 — How Traders Can Manage Their Emotions and Achieve Success

As of today, reject mediocrity; reject the mindless path! Most traders are living on autopilot, acting out their pre-conditioned beliefs and patterns in the market. Once again, the next level in your trading will come with the next level of in your mindset. I’m asking you to reject what doesn’t work and focus all your attention, energy and time on developing the beliefs, habits and behaviors that do work. If you’re serious about trading, you must do that — you must look within yourself and take control of your own life because the status quo won’t cut it! It doesn’t work!

Now, I understand: Looking within can be a difficult process because not everything we discover about ourselves is beautiful, shiny and polished. There are a lot of unskillful aspects to our being; there is also a lot of pain that resides in our minds and hearts because life isn’t exactly fair. And facing all of that requires a lot of courage because it’s uncomfortable. However, it is ultimately a rewarding journey, as it allows us to overcome the internal obstacles that are hindering our success in trading and in life. “Face your fear and the death of fear is assured.” Ever heard this saying? That’s exactly what I’m trying to express here.

Let me give you a concrete example to make things more vivid. I’ve worked with a trader, a high net worth individual, who trades U.S. stocks, basically the first hour of the NY opening. He has a very rudimentary trading strategy — he identifies the long-term trend (weekly), zooms in on the 5-minute and places his trade in the direction of the long-term trend with a tight stop right under the first hour low.

As you can imagine, given how tight his stop is, he spends his time reaping losses, day after day after day. When he’s wrong, he’s wrong fast, but when he’s right, he can stay in that trade for months and ride that sucker to Valhalla.

But this trader was constantly plagued by the fear of giving back his open profits, which often led him to exit his positions prematurely. With such a low win percentage, small profits just don’t cut it — he needs those occasional monster profits to nullify those many small losses.

So, our work together consisted of identifying his limiting beliefs and emotional triggers. And through a series of coaching sessions, I helped him reframe his mindset, de-energize some unproductive beliefs he had about the market and develop a more positive and carefree approach to trade outcomes. I introduced specific techniques to help him manage his emotions and reduce stress, and now he’s much more confident and disciplined amidst the uncertainty.

If he had continued to trade with the same kind of behavior and mindset that were getting him the results he got, he would have still been stuck at the same level year after year. So, this isn’t platitude — the next level in your trading will come with the next level in your mindset!

What beliefs, stories, and patterns are you consciously or unconsciously holding onto? Ponder this question and the above ones. Take some time to reflect and write down your answers. Take charge today because so much more is possible, and so much more awaits you in terms of growth and trading success.

[ad_2]

Yvan Byeajee

Source link

[ad_1]

Following Fed Chair Jerome Powell’s testimony on monetary policy last week and February’s job report showing more job creation than expected, the probability of the Fed increasing interest rates have risen. However, given the rosy long-term prospects of the tech industry, fundamentally strong stocks Fortinet (FTNT), Teradata (TDC), and Box (BOX) look poised to deliver steady returns and could be ideal buys now. Keep reading.

February’s job report revealed an unexpectedly high number of new jobs created, increasing the likelihood of the Federal Reserve raising interest rates higher and for a more extended period.

Despite the market turmoil, I think Fortinet, Inc. (FTNT), Teradata Corporation (TDC), and Box, Inc. (BOX) are well-poised to deliver sustainable returns.

Although the Federal Reserve has been trying to curb the economy and reduce inflation, the most recent employment report shows that the labor market remains tight, and job growth is stronger than anticipated. In February, nonfarm payrolls rose by 311,000, above the 225,000 Dow Jones estimate.

Moreover, in remarks on Capitol Hill this week, Fed Chairman Jerome Powell called the jobs market “extremely tight” and cautioned that recent data showing resurgent inflation pressures could push interest rate hikes higher than expected.

Furthermore, the recent collapse of Silicon Valley Bank has caused concerns among investors. Markets then pushed back projections for eventual rate cuts, with many forecasters expecting the first one sometime in 2024.

However, despite the volatility, the tech industry’s long-term prospects look favorable. The software market is expected to generate revenues of $650.70 billion in 2023, driven by the growing demand for Software as a Service (SaaS) solutions due to the rise in remote and hybrid work cultures.

So, fundamentally solid stocks, FTNT, TDC, and BOX could be worth buying now.

Fortinet, Inc. (FTNT)

FTNT offers comprehensive, integrated, and automated cybersecurity solutions internationally. It sells FortiGate hardware and software licenses, which enable a range of networking and security features. It also provides security subscriptions, technical support, and training services.

On March 1, 2023, FTNT announced new and enhanced products and services for operational technology (OT) environments as an expansion of the Fortinet Security Fabric for OT. FTNT enables organizations to build a platform of integrated solutions to effectively mitigate cyber risk across OT and IT environments.

John Maddison, EVP of Products and CMO of the company, said, “The Fortinet Security Fabric for OT is specifically designed for operational technology, and we’re pleased to introduce additional cyber-physical security capabilities to protect these environments.”

In terms of the trailing-12-month EBIT margin, FTNT’s 21.85% is 271.5% higher than the 5.88% industry average. Its 19.41% trailing-12-month net income margin is 565.3% higher than the 2.92% industry average. Its 24.02% trailing-12-month levered FCF margin is 255.8% higher than the industry average of 6.75%.

During the fiscal fourth quarter that ended December 31, 2022, FTNT’s total revenue increased 33.1% year-over-year to $1.28 billion. Its non-GAAP operating income rose 52% from the prior-year quarter to $417.60 million.

Non-GAAP net income attributable to FTNT and non-GAAP net income per share attributable to FTNT came in at $349.70 million and $0.44, up 69.9% and 76% from the prior-year quarter, respectively.

Street expects FTNT’s revenue for the fiscal first quarter ending March 2023 to come in at $1.20 billion, representing a 25.9% rise year-over-year. Its EPS is expected to increase 52.9% year-over-year to $0.29. The company has an impressive earning history, as it has surpassed the consensus EPS estimates in each of the trailing four quarters.

The stock has gained 21.2% year-to-date to close the last trading session at $59.27.

FTNT’s POWR Ratings reflect its promising prospects. The stock has an overall rating of B, which equates to a Buy in our proprietary rating system. The POWR Ratings are calculated by considering 118 different factors, with each factor weighted to an optimal degree.

It has an A grade for Quality and a B for Growth and Sentiment. The stock is ranked #3 among 22 stocks in the Software – Security industry.

Click here to see the other ratings of FTNT for Value, Momentum, and Stability.

Teradata Corporation (TDC)

TDC provides a connected multi-cloud data platform for enterprise analytics to various industries, including automotive, energy and natural resources, financial services, government, healthcare, manufacturing, retail, and telco.

On March 8, TDC announced the integration and general availability of TDC VantageCloud, the complete cloud analytics and data platform, with Microsoft Azure Machine Learning (Azure ML).

VantageCloud offers scalability, openness, and industry-leading analytics through ClearScape Analytics™, while Azure ML simplifies and accelerates the ML lifecycle. The company is constantly enhancing its capabilities to serve customers better.

TDC’s 24.13% trailing-12-month levered FCF margin is 258.3% higher than the 6.73% industry average. In terms of the trailing-12-month ROTC, the stock’s 7.54% is 134.3% higher than the industry average of 3.22%. Its trailing-12-month gross profit margin of 60.67% is 24.1% higher than the 48.89% industry average.

During the fiscal fourth quarter that ended December 31, 2022, TDC’s public cloud annual recurring revenue rose 76.7% year-over-year to $357 million. Its cash provided by operating activities grew 35.8% year-over-year to $129 million, while free cash flow increased 41.2% from the prior-year quarter to $120 million. Moreover, the company reported a non-GAAP EPS of $0.35.

Analysts expect TDC’s revenue for the fiscal year 2023 to rise 1.5% year-over-year to $1.82 billion. Its EPS is expected to grow 20.4% year-over-year to $1.97 in the current year. The company also surpassed the consensus EPS estimates in each of the trailing four quarters, which is remarkable.

TDC’s shares have gained 14.3% over the past six months to close the last trading session at $37.01.

It is no surprise that TDC has an overall rating of B, equating to a Buy in our POWR Ratings system.

TDC has an A grade in Value and Quality. Within the 81-stock Technology – Services industry, TDC is ranked #10.

In addition to the POWR Rating grades just highlighted, you can see TDC’s growth, Momentum, Stability, and Sentiment ratings here.

Box, Inc. (BOX)

BOX provides a cloud content management platform that enables organizations of various sizes to manage and share their content from anywhere on any device.

The company’s Software-as-a-Service platform allows users to collaborate on content, automate content-driven business processes, develop custom applications, and implement data protection, security, and compliance features.

BOX’s 30.33% trailing-12-month levered FCF margin is 349.4% higher than the 6.75% industry average. In terms of the trailing-12-month gross profit margin, the stock’s 74.51% is 52.3% higher than the 48.94% industry average. Its 0.76x trailing-12-month asset turnover ratio is 25.4% higher than the industry average of 0.61x.

BOX’s revenue increased 9.9% year-over-year to $256.48 million in the fiscal fourth quarter that ended January 31, 2023. The company’s non-GAAP gross profit increased 14.9% year-over-year to $201.26 million, while non-GAAP operating income increased 37.3% year-over-year to $66.56 million.

The company’s non-GAAP net income attributable to common stockholders rose 52.7% year-over-year to $56.29 million, and non-GAAP net EPS attributable to common stockholders increased 54.2% year-over-year to $0.37.

BOX’s EPS and revenue for the fiscal first quarter ending April 2023 are expected to increase 18.4% and 4.6% year-over-year to $0.27 and $249.29 million, respectively. Also, it has surpassed the consensus EPS estimates in three of the trailing four quarters.

The stock has gained 5.6% over the past nine months to close the last trading session at $25.48.

BOX’s strong fundamentals are reflected in its POWR Ratings. The stock has an overall rating of A, equating to a Strong Buy in our proprietary rating system.

It has an A grade for Growth and Quality and a B for Value. It is ranked #5 in the Technology – Services industry.

To access the additional ratings of BOX for Momentum, Stability, and Sentiment, click here.

What To Do Next?

Get your hands on this special report:

What gives these stocks the right stuff to become big winners, even in this brutal stock market?

First, because they are all low-priced companies with the most upside potential in today’s volatile markets.

But even more important is that they are all top Buy rated stocks according to our coveted POWR Ratings system, and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks that could double or more in the year ahead.

FTNT shares were unchanged in premarket trading Tuesday. Year-to-date, FTNT has gained 21.23%, versus a 0.77% rise in the benchmark S&P 500 index during the same period.

Her interest in risky instruments and passion for writing made Kritika an analyst and financial journalist. She earned her bachelor’s degree in commerce and is currently pursuing the CFA program. With her fundamental approach, she aims to help investors identify untapped investment opportunities.

The post 3 Stocks That Could Take Your Portfolio to the Next Level in 2023 appeared first on StockNews.com

[ad_2]

Kritika Sarmah

Source link

[ad_1]

Silicon Valley Bank collapsed after a stunning 48 hours in which a bank run and a capital crisis led to the second-largest failure of a financial institution in U.S. history. What do you think?

“Let’s hurry up and bail it out so we can do this all over again.”

Ethan Dodds, Capsicum Specialist

“Just tell me if I have to jump out of my penthouse or not.”

Nora Khoury, Merkin Designer

“We deregulated our way into this mess, and we can deregulate our way out of it.”

Gary Dugan, Sleep Observer

[ad_2]

[ad_1]

Are you looking to take your business to the next level? As an entrepreneur, it’s easy to get caught up in the excitement of rapid growth and explosive revenue. However, if you want your business to thrive in the long run, it’s essential to take a measured approach that prioritizes financial stability and sustainability.

We’ll be exploring this concept and much more in our upcoming free webinar, Smart Money: How to Strategically Scale Your Business and Achieve Sustainability, brought to you by Oracle NetSuite and Entrepreneur. Moderator Terry Rice will sit down with Jay Jung, an experienced corporate finance consultant with expertise in M&A, capital raising and growth strategy. He has more than two decades-worth of strategic finance experience and has a passion for creating effective revenue models, identifying challenges and opportunities, and more.

In this webinar, Rice and Jung will explore practical strategies for growing your business without sacrificing financial sanity or long-term success. Join us to learn how to take a reasonable, grounded approach to business growth that sets you up for lasting success.

Attendees of this webinar will learn:

Join us for the Smart Money: How to Strategically Scale Your Business and Achieve Sustainability webinar, taking place live on Thursday, April 27 at 12 p.m. ET | 9 a.m. PT.

[ad_2]

Entrepreneur Events

Source link

[ad_1]

How to power up the POWR Pairs Trades to lower risk and increase return in a big range, no change market environment.

After a rip-roaring start to 2023, stocks have come crashing back to pretty much unchanged on the year.

The NASDAQ 100 (QQQ) still is up nicely so far in 2023 at a little over 8%, but that is more than a 50% drop from the highs in early February. The S&P 500 (SPY) and Russell 2000 (IWM) have fallen further and are clinging to slight gains for the year. The Dow Jones Industrials (DIA) are now firmly in negative territory in 2023.

The roles were reversed in 2022 with the DIA being by far the best performer (down just under 14%) of the four indices while QQQ (down over 25%) was the worst.

This type of big range, no change market environment makes buying stocks more difficult and puts a definite premium on stock picking. Using the POWR Ratings to uncover the best stocks to buy and the worst stocks to sell will be an even decided edge in 2023.

That’s exactly the approach we have used with great success in POWR Options. A POWR Pairs Trade to coin the term.

We start by looking at bullish calls on the highest rated stocks and bearish puts on the lowest rated stocks. This eliminates much of the overall market exposure and distills the relative performance down to the power of the POWR ratings. Higher rated stocks outperform lower rated stocks to a large degree as shown in the chart below.

Then we identify situations where the lower rated stock has out-performed the higher stock in a big way and is in a position to profit from the expected convergence of the two back to a more historically traditional relationship. In the past, we invariably used this pairs philosophy with two stocks in the same industry to further dampen risk.

We also always consider implied volatility (IV) in every trading decision. POWR Options buys comparatively cheap options to further put the overall odds in our favor.

In our latest POWR Pairs Trade, however, we decided to forego the same industry requirement and just look at buying good stocks doing lousy and shorting bad stocks doing too good.

It ended up being a very viable additional approach to our pairs trading philosophy. A quick walk-through our latest POWR Pairs Trade will help shed some light.

While not a “traditional” pairs trade, since the two stocks are in different industries, it still is a POWR Ratings performance pairs trade.

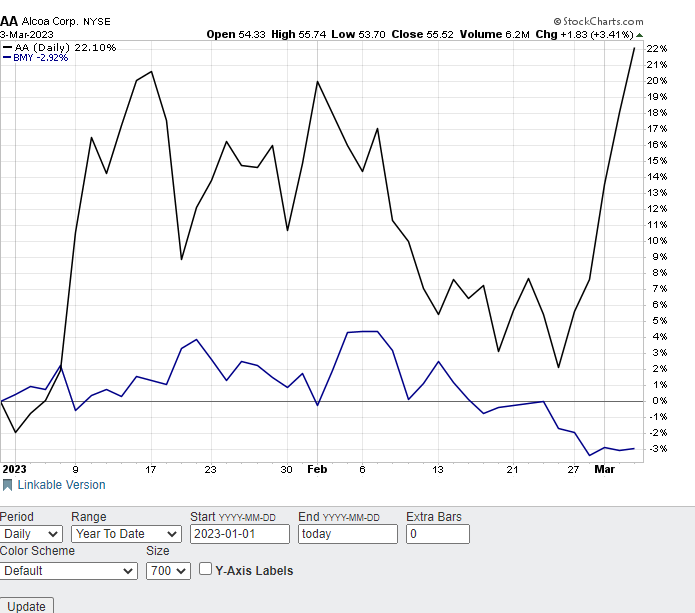

Buying bearish puts on the much lower-rated but much better performing Alcoa (AA) and buying bullish calls on the much higher-rated but much lower performing Bristol-Myers Squibb (BMY).

D rated -Sell- Alcoa (AA) is trading at yearly highs for 2023, up 22%.

A rated -Strong Buy-Bristol Myers (BMY) is just off the yearly lows, down about 3% year-to-date.

The chart below shows the comparative performance so far in 2023. Note how AA did drop sharply in February while BMY hugged the flatline. Since the end of February, however, AA has exploded higher once again while BMY has drifted lower. Performance differential got to 25%.

Look for AA to be a relative underperformer to BMY over the coming weeks as the price performance between the two stocks converges as it has in the past.

On March 3, The POWR Options portfolio bought the AA June $50 puts for $3.90 ($390 per option) and at the same time bought the BMY June $67.50 calls for $4.20 ($4.20) per option. Total combined outlay was $810.

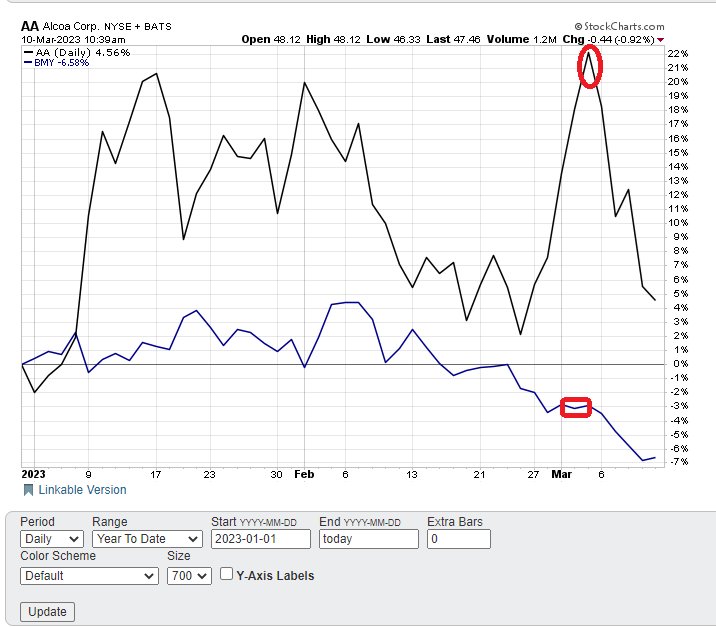

Fast forward to Friday March 10. You can see how AA has dropped over 17% since the pairs trade was initiated (highlighted in red). BMY has fallen as well, but only a little over 3.5%.

This led to closing out the pairs trade since the spread had converged dramatically. The original performance differential of over 25% on March 3 shrank, or converged, by more than half to just over 11% on March 10.

Just as importantly, implied volatility rose in that time frame. This gave a lift to both our long puts on AA and long calls on BMY. The AA puts went from a 53.81 IV to a 56.30 IV. The BMY Calls rose from a 21.14 IV to a 22.28 IV.

Exited the bullish BMY calls for a loss of $120. Got out of the bearish AA puts for a gain of $290. Net overall gain was $170 ($290 -$120). Actual trade data seen below.

Net percentage gain on the trade was just over 20% ($170 net gain/ $810 initial combined outlay). The holding period was just a week. In on Monday, out on Friday.

Investors and traders looking to generate similar low-risk but solid short-term returns may want to consider using the POWR Pairs Trade approach to significantly reduce the downside but still leave plenty of upside open for grabbing gains.

What To Do Next?

While the concepts behind options trading are simpler than most people realize, applying those concepts to consistently make winning options trades is no easy task.

The solution is to let me do the hard work for you, by starting a 30 day to my POWR Options newsletter.

I’ve been uncovering the best options trades for over 30 years and with the quantitative muscle of the POWR Ratings as my starting point I’ve achieved an 82% win rate over my last 17 closed trades!

During your trial you’ll get full access to the current portfolio, weekly market commentary and every trade alert by text & email.

I’ll be adding the next 2 exciting options trades (1 call and 1 put) when the market opens this Monday morning, so start your trial today so you don’t miss out.

There’s no obligation beyond the 30 day trial, so there is absolutely no risk in getting started today.

About POWR Options & 30 Day Trial >>

Here’s to good trading!

Tim Biggam

Editor, POWR Options Newsletter

shares closed at $385.91 on Friday, down $-5.65 (-1.44%). Year-to-date, has gained 0.91%, versus a % rise in the benchmark S&P 500 index during the same period.

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader. Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

The post Better To Be Bullish Or Bearish? Being Both Is The Best Approach appeared first on StockNews.com

[ad_2]

Tim Biggam

Source link

[ad_1]

How to power up the POWR Pairs Trades to lower risk and increase return in a big range, no change market environment.

After a rip-roaring start to 2023, stocks have come crashing back to pretty much unchanged on the year.

The NASDAQ 100 (QQQ) still is up nicely so far in 2023 at a little over 8%, but that is more than a 50% drop from the highs in early February. The S&P 500 (SPY) and Russell 2000 (IWM) have fallen further and are clinging to slight gains for the year. The Dow Jones Industrials (DIA) are now firmly in negative territory in 2023.

The roles were reversed in 2022 with the DIA being by far the best performer (down just under 14%) of the four indices while QQQ (down over 25%) was the worst.

This type of big range, no change market environment makes buying stocks more difficult and puts a definite premium on stock picking. Using the POWR Ratings to uncover the best stocks to buy and the worst stocks to sell will be an even decided edge in 2023.

That’s exactly the approach we have used with great success in POWR Options. A POWR Pairs Trade to coin the term.

We start by looking at bullish calls on the highest rated stocks and bearish puts on the lowest rated stocks. This eliminates much of the overall market exposure and distills the relative performance down to the power of the POWR ratings. Higher rated stocks outperform lower rated stocks to a large degree as shown in the chart below.

Then we identify situations where the lower rated stock has out-performed the higher stock in a big way and is in a position to profit from the expected convergence of the two back to a more historically traditional relationship. In the past, we invariably used this pairs philosophy with two stocks in the same industry to further dampen risk.

We also always consider implied volatility (IV) in every trading decision. POWR Options buys comparatively cheap options to further put the overall odds in our favor.

In our latest POWR Pairs Trade, however, we decided to forego the same industry requirement and just look at buying good stocks doing lousy and shorting bad stocks doing too good.

It ended up being a very viable additional approach to our pairs trading philosophy. A quick walk-through our latest POWR Pairs Trade will help shed some light.

While not a “traditional” pairs trade, since the two stocks are in different industries, it still is a POWR Ratings performance pairs trade.

Buying bearish puts on the much lower-rated but much better performing Alcoa (AA) and buying bullish calls on the much higher-rated but much lower performing Bristol-Myers Squibb (BMY).

D rated -Sell- Alcoa (AA) is trading at yearly highs for 2023, up 22%.

A rated -Strong Buy-Bristol Myers (BMY) is just off the yearly lows, down about 3% year-to-date.

The chart below shows the comparative performance so far in 2023. Note how AA did drop sharply in February while BMY hugged the flatline. Since the end of February, however, AA has exploded higher once again while BMY has drifted lower. Performance differential got to 25%.

Look for AA to be a relative underperformer to BMY over the coming weeks as the price performance between the two stocks converges as it has in the past.

On March 3, The POWR Options portfolio bought the AA June $50 puts for $3.90 ($390 per option) and at the same time bought the BMY June $67.50 calls for $4.20 ($4.20) per option. Total combined outlay was $810.

Fast forward to Friday March 10. You can see how AA has dropped over 17% since the pairs trade was initiated (highlighted in red). BMY has fallen as well, but only a little over 3.5%.

This led to closing out the pairs trade since the spread had converged dramatically. The original performance differential of over 25% on March 3 shrank, or converged, by more than half to just over 11% on March 10.

Just as importantly, implied volatility rose in that time frame. This gave a lift to both our long puts on AA and long calls on BMY. The AA puts went from a 53.81 IV to a 56.30 IV. The BMY Calls rose from a 21.14 IV to a 22.28 IV.

Exited the bullish BMY calls for a loss of $120. Got out of the bearish AA puts for a gain of $290. Net overall gain was $170 ($290 -$120). Actual trade data seen below.

Net percentage gain on the trade was just over 20% ($170 net gain/ $810 initial combined outlay). The holding period was just a week. In on Monday, out on Friday.

Investors and traders looking to generate similar low-risk but solid short-term returns may want to consider using the POWR Pairs Trade approach to significantly reduce the downside but still leave plenty of upside open for grabbing gains.

What To Do Next?

While the concepts behind options trading are simpler than most people realize, applying those concepts to consistently make winning options trades is no easy task.

The solution is to let me do the hard work for you, by starting a 30 day to my POWR Options newsletter.

I’ve been uncovering the best options trades for over 30 years and with the quantitative muscle of the POWR Ratings as my starting point I’ve achieved an 82% win rate over my last 17 closed trades!

During your trial you’ll get full access to the current portfolio, weekly market commentary and every trade alert by text & email.

I’ll be adding the next 2 exciting options trades (1 call and 1 put) when the market opens this Monday morning, so start your trial today so you don’t miss out.

There’s no obligation beyond the 30 day trial, so there is absolutely no risk in getting started today.

About POWR Options & 30 Day Trial >>

Here’s to good trading!

Tim Biggam

Editor, POWR Options Newsletter

shares closed at $385.91 on Friday, down $-5.65 (-1.44%). Year-to-date, has gained 0.91%, versus a % rise in the benchmark S&P 500 index during the same period.

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader. Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

The post Better To Be Bullish Or Bearish? Being Both Is The Best Approach appeared first on StockNews.com

[ad_2]

Tim Biggam

Source link

[ad_1]

How to power up the POWR Pairs Trades to lower risk and increase return in a big range, no change market environment.

After a rip-roaring start to 2023, stocks have come crashing back to pretty much unchanged on the year.

The NASDAQ 100 (QQQ) still is up nicely so far in 2023 at a little over 8%, but that is more than a 50% drop from the highs in early February. The S&P 500 (SPY) and Russell 2000 (IWM) have fallen further and are clinging to slight gains for the year. The Dow Jones Industrials (DIA) are now firmly in negative territory in 2023.

The roles were reversed in 2022 with the DIA being by far the best performer (down just under 14%) of the four indices while QQQ (down over 25%) was the worst.

This type of big range, no change market environment makes buying stocks more difficult and puts a definite premium on stock picking. Using the POWR Ratings to uncover the best stocks to buy and the worst stocks to sell will be an even decided edge in 2023.

That’s exactly the approach we have used with great success in POWR Options. A POWR Pairs Trade to coin the term.

We start by looking at bullish calls on the highest rated stocks and bearish puts on the lowest rated stocks. This eliminates much of the overall market exposure and distills the relative performance down to the power of the POWR ratings. Higher rated stocks outperform lower rated stocks to a large degree as shown in the chart below.

Then we identify situations where the lower rated stock has out-performed the higher stock in a big way and is in a position to profit from the expected convergence of the two back to a more historically traditional relationship. In the past, we invariably used this pairs philosophy with two stocks in the same industry to further dampen risk.

We also always consider implied volatility (IV) in every trading decision. POWR Options buys comparatively cheap options to further put the overall odds in our favor.

In our latest POWR Pairs Trade, however, we decided to forego the same industry requirement and just look at buying good stocks doing lousy and shorting bad stocks doing too good.

It ended up being a very viable additional approach to our pairs trading philosophy. A quick walk-through our latest POWR Pairs Trade will help shed some light.

While not a “traditional” pairs trade, since the two stocks are in different industries, it still is a POWR Ratings performance pairs trade.

Buying bearish puts on the much lower-rated but much better performing Alcoa (AA) and buying bullish calls on the much higher-rated but much lower performing Bristol-Myers Squibb (BMY).

D rated -Sell- Alcoa (AA) is trading at yearly highs for 2023, up 22%.

A rated -Strong Buy-Bristol Myers (BMY) is just off the yearly lows, down about 3% year-to-date.

The chart below shows the comparative performance so far in 2023. Note how AA did drop sharply in February while BMY hugged the flatline. Since the end of February, however, AA has exploded higher once again while BMY has drifted lower. Performance differential got to 25%.

Look for AA to be a relative underperformer to BMY over the coming weeks as the price performance between the two stocks converges as it has in the past.

On March 3, The POWR Options portfolio bought the AA June $50 puts for $3.90 ($390 per option) and at the same time bought the BMY June $67.50 calls for $4.20 ($4.20) per option. Total combined outlay was $810.

Fast forward to Friday March 10. You can see how AA has dropped over 17% since the pairs trade was initiated (highlighted in red). BMY has fallen as well, but only a little over 3.5%.

This led to closing out the pairs trade since the spread had converged dramatically. The original performance differential of over 25% on March 3 shrank, or converged, by more than half to just over 11% on March 10.

Just as importantly, implied volatility rose in that time frame. This gave a lift to both our long puts on AA and long calls on BMY. The AA puts went from a 53.81 IV to a 56.30 IV. The BMY Calls rose from a 21.14 IV to a 22.28 IV.

Exited the bullish BMY calls for a loss of $120. Got out of the bearish AA puts for a gain of $290. Net overall gain was $170 ($290 -$120). Actual trade data seen below.

Net percentage gain on the trade was just over 20% ($170 net gain/ $810 initial combined outlay). The holding period was just a week. In on Monday, out on Friday.

Investors and traders looking to generate similar low-risk but solid short-term returns may want to consider using the POWR Pairs Trade approach to significantly reduce the downside but still leave plenty of upside open for grabbing gains.

What To Do Next?

While the concepts behind options trading are simpler than most people realize, applying those concepts to consistently make winning options trades is no easy task.

The solution is to let me do the hard work for you, by starting a 30 day to my POWR Options newsletter.

I’ve been uncovering the best options trades for over 30 years and with the quantitative muscle of the POWR Ratings as my starting point I’ve achieved an 82% win rate over my last 17 closed trades!

During your trial you’ll get full access to the current portfolio, weekly market commentary and every trade alert by text & email.

I’ll be adding the next 2 exciting options trades (1 call and 1 put) when the market opens this Monday morning, so start your trial today so you don’t miss out.

There’s no obligation beyond the 30 day trial, so there is absolutely no risk in getting started today.

About POWR Options & 30 Day Trial >>

Here’s to good trading!

Tim Biggam

Editor, POWR Options Newsletter

shares closed at $385.91 on Friday, down $-5.65 (-1.44%). Year-to-date, has gained 0.91%, versus a % rise in the benchmark S&P 500 index during the same period.

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader. Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

The post Better To Be Bullish Or Bearish? Being Both Is The Best Approach appeared first on StockNews.com

[ad_2]

Tim Biggam

Source link

[ad_1]

The real estate market is in an interesting state right now. Home sales are slowing because of higher interest rates, but prices in some areas have yet to drop. Overall, the median existing home sales price in January 2023 was up 1.3% from the same time last year, but home prices in expensive areas have gone down, while prices in less expensive areas have gone up.

Considering that home prices were reaching record highs in 2021, one would expect them to have normalized with the slowing market, but that has yet to happen. However, if interest rates continue to rise, prices should continue to drop.

But what does that mean to you and your finances? This article will explore how the current real estate market can impact you financially.

There are several situations that you may find yourself in where the real estate market may affect your finances.

If you’re in the market to buy a home, you’re going to pay a higher interest rate than you would have in 2021. However, the inventory of homes is high and the number of buyers is down. That means that you may have more negotiating power with sellers. Prices may be higher, but chances are, most sellers are very motivated which could put you in the driver’s seat.

But you’ll end up paying a higher rate, but with a lower price point for the home, so it may even out for you financially. You can also refinance later if interest rates go down and get ahead of the game.

Be sure to do your research into what is happening in your area in terms of prices and the number of sales that are occurring. Every local market is different. Make sure that your real estate agent talks to you about current comparable sales, and use your negotiating power.

If you’re planning to sell your home in the near future, you may be under a bit of pressure. Buyers are fewer in many areas due to the higher interest rates, so the people that are buying have the negotiating power. If you can, you may be better off waiting to sell until rates go back down. However, what will happen with interest rates and when is a great unknown.

If you need to sell and you want to get a specific profit on what you paid for the home or on what you owe on your mortgage, you can calculate here what price you need to stick to.

Often the best strategy in this kind of market is to price your home higher than what you actually need. That way the buyer can negotiate and feel like they’re getting a deal. It cannot be stressed enough, however, that the best strategy depends on your local market.

Do your homework and talk to your real estate agent about what is happening in your market and what comparable homes are selling for. And if you need to make a certain profit on your home, you can stick to your guns and wait for that buyer that “must have” your home.

Work with your agent to make your home as appealing to buyers as possible by making repairs or upgrades and staging the home well. In a tough market, you need to make your home stand out from the competition.

Also, work with your tax advisor when considering the price that you need to get. Selling at lower price means less in capital gains tax, so that will have an impact on your finances overall.

Special note: there was $400mm in sales in January 2023.

Investing in real estate right now is an interesting proposition. Warren Buffet said “be greedy when others are fearful”. Real estate investors right now are fearful of economic and market instability; however, having that kind of outlook depends on your goals and your risk tolerance.

If you’re looking to flip houses as an investment, it’s likely that you can find deals, particularly on distressed properties. But with the number of home buyers decreasing, you may find yourself having trouble finding a buyer and thus incur carrying costs. You can still make a profit, though, if you can put minimal money into the property and price it competitively based on local real estate conditions.

Your best bet if you want to flip homes now, is to carefully analyze each potential deal, including what is happening in the specific area the property is in, and cherry pick only the deals that make the most sense and have the least risk. With so many “fearful” investors, you’ll have less competition, so you can afford to be choosy.

If you’re considering buying rental properties, it’s still a matter of looking at each deal. The higher interest rates mean that fewer buyers are buying and are renting instead, which can drive rents up. That’s great if you can find a great deal and pay cash for the property. If you need to finance the property, however, you’ll be paying a higher interest rate which will reduce your cash flow.

The bottom line is, if you’re considering investing, you have to really understand your local market. Do considerable research before making a decision.

Clearly, if your current interest rate is lower than current mortgage rates, refinancing your mortgage may not be a good idea, and vice versa. You also have to consider your closing costs when deciding if refinancing is financially beneficial.

If you are refinancing to a lower rate and getting cash out from your equity, you may find that when the bank assesses your home’s market value, it may be lower than you think. Again, it depends on what’s happening to prices in your local market.

If you want to refinance to a shorter loan term, you may still be able to benefit. Rates on 10 or 15 year mortgages are generally lower than 30 year mortgages, but your payment may still be higher because of the shorter term.

Another thing to consider is that lenders tend to be more conservative in a slow real estate market, so it may be more difficult to qualify for the refinance. Credit score and income requirements will be tighter, so be prepared to go through a more rigorous application process.

Your best bet is to shop around for the best rates and terms, analyze your options, and decide which option, if any, is right for you.

Here is a nifty refinance mortgage calculator to help you.

If you’re considering getting a home equity loan, whether the real estate market will impact you depends on your goals.

If you want a home equity loan to consolidate other debt, current mortgage rates are still likely lower than the rates on other debt such as credit cards. However, similar to a cash-out refinance, your equity may not be as high as you expect based on market values.

If you want a home equity loan to remodel your home, if you’re doing it just because you want your house to be nice and you can afford the payments, go for it. You might want to consider a home equity line of credit with a variable rate so that the rate goes down when rates go down in general. However, rates may also go up.

If you want a home equity loan for remodeling, but with the goal of selling your home for a higher price in the near future, you’ll need to give it careful consideration. If rates continue to rise and home prices fall, you may not get your money back from the remodeling you do and the interest you pay on the loan. Be sure not to overdo your improvements.

Fewer people buying homes means more people renting, which is creating a rental shortage due to high demand. As a result, in 2023 many predict that rental price growth is likely to remain high, which is bad news for renters.

Other economic factors are also decreasing the amount of income that renters can spend on rent. What this means is that rentals in higher-priced areas will be less in demand, which should start to force prices on those rentals down a bit.

In the longer term, rental prices are likely to start to come back down, so if you’re finding it difficult to afford current rents, you may only be struggling temporarily.

As with all the other effects of the real estate market, how the current conditions will affect renters is location dependent. If you’re in the market for a new rental, do your homework and shop around, and don’t be afraid to negotiate with landlords to try to get a better rate.

The real estate market is interesting right now, and it’s difficult even for experts to predict exactly what will happen in 2023 and beyond. Many factors will have an impact on the market’s direction, so you should stay informed about what’s happening in the market, particularly in your area.

If you’re in any of the situations discussed, be sure to do your market research and look to professionals, whether it be a real estate agent or a financial advisor, for advice. By doing so, you can find ways to successfully navigate this unpredictable market and protect your finances.

The post How the Current Real Estate Market Can Affect Your Finances appeared first on Due.

[ad_2]

Carolyn Young

Source link

[ad_1]

It’s been another doozy of a week for the S&P 500 (SPY). We had Fed Chair Jerome Powell giving his semiannual testimony before the Senate Banking Committee. We had the latest job openings summary from January. We had a surprise run on a bank in Silicon Valley push the entire financial indicator under the microscope. And we had the February employment report. That’s a lot to cover, so let’s get to it!.

(Please enjoy this updated version of my weekly commentary originally published March 10th, 2023 in the POWR Stocks Under $10 newsletter).

Market Commentary

So much happened this week, that I’m taking it day by day. Feel free to imagine the ticking clock from “24” when you read the name of each day.

Monday

All quiet on the Western Front.

Tuesday

Things finally kick off with the first day of Powell’s testimony before the Senate Banking Committee. The biggest takeaway from the day?

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.”

Powell says that inflation remains high and the labor market is strong and that, even though inflation has been moderating in recent months, it still has a long way to go before it reaches 2%.

His comments trigger a 1.5% selloff across the market, with every sector finishing lower for the day.

Wednesday

On his second day at the podium, Powell repeats his message that the U.S. central bank is likely to take rates higher than previously anticipated, but following Tuesday’s selloff, he goes off-script to stress that policymakers had not yet made up their minds on the size of their interest-rate increase later this month.

“If — and I stress that no decision has been made on this — but if the totality of the data were to indicate that faster tightening is warranted, we’d be prepared to increase the pace of rate hikes.”

“The data” Powell is referring to the handful of important economic reports on deck, including the January reading on U.S. job openings, February’s employment report, and next week’s consumer price data.

On Wednesday, we also get the first of those reports — the latest Job Openings and Labor Turnover Summary (JOLTS) from January, which show the number of job openings fell to 10.82 million, down from the upwardly revised 11.2 million openings in the prior month.

The Bureau of Labor Statistics reports that construction, leisure, hospitality, and finance industries showed the major pullbacks in job openings.

Stocks fare slightly better, with the S&P 500 (SPY) and Nasdaq closing slightly up and the Dow closing only slightly lower.

Thursday

This was supposed to be a relatively quiet day in the market, with Powell’s testimony over and no major reports scheduled to be released.

But instead, we see Silicon Valley Bank (SIVB), the preferred bank of many startups, shoot itself in the foot after announcing it was liquidating its entire short-term securities book and raising $2.25 billion fresh capital.

That in itself wasn’t a problem; it was when the CEO tried to assure its investors that the bank had plenty of liquidity and stated to the group, “the last thing we need you to do is panic.”

No better way to start a run on a bank!

The entire banking sector gets shoved under the microscope, with many stocks dropping double digits. The S&P 500 closes below the important 200-day moving average.

Friday

Another jobs release, another hotter-than-expected report. The economy added 311,000 jobs in February (more than the 215,000 expected) and the unemployment rate rose to 3.6% as inflation forces more people to look for jobs.

The bright spot in the report was that wage growth came in at 4.6%, slightly lower than the anticipated 4.7%. However, that’s still significantly above the pre-pandemic level… and that’s going to be a concern for the Fed.

Oh, and that bank I mentioned earlier… the FDIC shut it down Friday morning. It’s the biggest bank to fall since Washington Mutual collapsed in 2008. Not great!

Whew! What a week. Here’s a chart to show you where things stand.

You know, through it all, I think my biggest takeaway from everything is still the potential that the Federal Reserve may go back up to a 50-bps hike after slowing to 25 basis points in the latest meeting.

Why did that catch my attention? Because the Fed hasn’t stutter-stepped at the end of a rate hiking cycle since 1990.

What would it mean for the economy if we got a 50-bps hike on March 22?

Would it be an automatic “everyone panic, the recession is coming” siren? Absolutely not.

Would it be an “Oh good, we’re definitely going to get a soft landing” all clear? Also definitely not.

In fact, we don’t know what it would mean because we haven’t seen it happen in recent history. And because we don’t know what it means, we have to tread cautiously.

We will still keep trading, and we will still keep using our edge to find stocks under $10 that are ready to explode to new heights.

Can all that happen in a market that feels like it’s on shaky ground? Absolutely.

Conclusion

If you thought this week was volatile, then buckle up for the boom!

We’ve got CPI and PPI scheduled for Tuesday and Wednesday, quadruple witching on Friday (an options event that usually comes with a wave of volatility), and then the next Federal Reserve meeting the week after.

With everyone on edge, another bank going under or a higher-than-expected inflation report could send stocks sinking. As I said, we’re going to be treading carefully and while still keeping an eye out for our next big winner.

What To Do Next?

If you’d like to see more top stocks under $10, then you should check out our free special report:

What gives these stocks the right stuff to become big winners, even in this brutal stock market?

First, because they are all low priced companies with the most upside potential in today’s volatile markets.

But even more important, is that they are all top Buy rated stocks according to our coveted POWR Ratings system and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks which could double or more in the year ahead.

All the Best!

Meredith Margrave

Chief Growth Strategist, StockNews

Editor, POWR Stocks Under $10 Newsletter

SPY shares closed at $385.91 on Friday, down $-5.65 (-1.44%). Year-to-date, SPY has gained 0.91%, versus a % rise in the benchmark S&P 500 index during the same period.

Meredith Margrave has been a noted financial expert and market commentator for the past two decades. She is currently the Editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Meredith’s background, along with links to her most recent articles.

The post Making Sense of a Wild Week in the Markets appeared first on StockNews.com

[ad_2]

Meredith Margrave

Source link

[ad_1]

Did you ever really buy the bullish argument touted by some to start the new year? Yes, it was an amusing fable that has now lost its luster as the bears are firmly back in charge as proven by the break below the 200 day moving average for the S&P 500 (SPY). What happens from here? Steve Reitmeister shares his views in the new commentary below.

It is not unusual for the new year to start bullish. Just a fresh dose of optimism comes with flipping the calendar.

Those good vibes are over!

Now more investors are coming back around to the bearish premise that never really went away. Add in a dose of concerns about the health of the financial industry and we finally broke below the 200 day moving average with odds of much more downside on the way.

I am here to make sense of it all in this week’s market commentary below…

Market Commentary

As they say a picture is worth a thousand words. So, let’s start with the picture of the S&P 500 (SPY) this past year including the long term trend line better known as the 200 day moving average (in red).

You can see how vital the 200 day moving average has been in framing the action this past year. First being the bearish break below in April 2022 with many subsequent suckers’ rallies that failed as they approached this key level.

However, the bulls really tried to make a convincing run of things by finally breaking above in January and staying above for nearly two months. That party ended yesterday with the first close below the 200 day (3,941). And today was a convincing follow through session to the downside.

Now the bears are firmly in charge once again. Let’s discuss why…

On Tuesday of this week Fed Chairman Powell reminded everybody why they should reconsider their bullish ways. In essence he stated that given the facts in hand that rates will likely need to go higher than previously stated…and stay in place for longer.

This led to a -1.5% sell off on Tuesday. Just for clarity, here is the key quote from Powell so you appreciate that there is little room for misinterpretation.

“The process of getting inflation back down to 2% has a long way to go and is likely to be bumpy. As I mentioned, the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

This reminds folks of the Feds intent to lower demand…which is a fancy way of saying likely to create a recession as a necessary evil to tamp down the flames of inflation. Hard to be bullish when the Sheriff of the economy is putting up a roadblock to economic advance.

When you have this clear message already in hand, then it becomes unnecessary to wait all the way for the Fed meeting on 3/22 to start selling. This notion was taken to the next level on Thursday with the first break below the 200 day moving average in quite some time.

Most of the investment media outlets stated that the reason for this downward pressure is that more people were getting spooked about the likelihood of employment report being too strong on Friday which would be a cherry on top for further Fed hawkishness.