The November U.S. jobs report on Friday showed the U.S. economy gained 261,000 jobs last month, with the unemployment rate holding steady at 3.7%.

Economists polled by the Wall Street Journal had expected an addition of 200,000 jobs.

Wages jumped 0.6% in November, double the expected pace.

Below are some initial reactions from economists and other analysts as U.S. stocks DJIA, -0.20%

SPX, -0.37%

traded lower and the yield on the 10-year Treasury note TMUBMUSD10Y, 3.569%

jumped following the data on nonfarm payrolls.

“You probably want to revise your view on inflation and it’s overall dynamic more based on today’s job report than any other data report this entire year. And not in a favorable direction,” The report dashes hopes wage growth was cooling, said Jason Furman, economics professor at Harvard and former Obama White House economist, in a tweet.

“A stronger than expected 263,000 monthly payroll print plus the spike in wages…will reinforce the Fed’s assessment that the labor market remains very overheated, and rates will need to go higher for longer in order to bring it back into balance,” said Krishna Guha, vice chairman of Evercore ISI.

“The Fed will not like the renewed strength in wages,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

“The U.S. labor market has lost some momentum this year, but it’s still speeding ahead as we approach the new year. Continue to underestimate the momentum in the U.S. labor market at your own peril. Job gains continue to be added at a pace that would have drawn cheers in 2019. The labor market might encounter some bumps in the road next year, but it’s heading into 2023 cruising,” said Nick Bunker, head of economic research at the Indeed Hiring Lab.

Federal Reserve Gov. Christopher Waller said Sunday that financial markets seem to have overreacted to the softer-than-expected October consumer price inflation data last week.

“It was just one data point,” Waller said, in a conversation in Sydney, Australia, sponsored by UBS.

“The market seems to have gotten way out in front over this one CPI report. Everybody should just take a deep breath, calm down. We’ve got a ways to go ” Waller said.

Investors cheered the soft CPI print, released Thursday, driving stocks up to their best week since June. The S&P 500 index SPX, +0.92%

closed 5.9% higher for the week.

The data showed that the yearly rate of consumer inflation fell to 7.7% from 8.2%, marking the lowest level since January. Inflation had peaked at a nearly 41-year high of 9.1% in June.

Waller said it was good there was some evidence that inflation was coming down, but noted that there were other times over the past year where it looked like inflation was turning lower.

“We’re going to see a continued run of this kind of behavior and inflation slowly starting to come down, before we really start thinking about taking our foot off the brakes here,” Waller said.

“We’ve got a long, long way to go to get inflation down. Rates are going keep going up and they are going to stay high for awhile until we see this inflation get down closer to our target,” he added.

The Fed is focused on how high rates need to get to bring inflation down, and that will depend solely on inflation, he said.

Waller said “the worst thing” the Fed could do was stop raising rates only to have inflation explode.

The 7.7% inflation rate seen in October “is enormous,” he added.

The Fed signaled at its last meeting earlier this month that it might slow down the pace of its rate hikes in coming meetings.

The central bank has boosted rates by almost 400 basis points since March, including four straight 0.75-percentage-point hikes that had been almost unheard of prior to this year.

“We’re looking at moving in paces of potentially 50 [basis points] at the next meeting or the next meeting after that,” Waller said.

The Fed will hold its next meeting on Dec. 13-14, and then again on Jan. 31-Feb. 1.

At the same time, Powell said the Fed was likely to raise rates above the 4.5%-4.75% terminal rate that they had previously expected.

“The signal was ‘quit paying attention to the pace and start paying attention to where the endpoint is going to be,’” Waller said.

In the wake of the CPI report, investors who trade fed funds futures contracts see the Fed’s terminal rate at 5%-5.25% next spring and then quickly falling back to 4.25%-4.5% by November. That’s well below the levels prior to the CPI data.

Investors feeling giddy about last week’s sharp rally for stocks might want to give a listen to Tom Waits’ song, “Whistlin’ Past the Graveyard” from 1978, to sober up for the dangers that still lurk ahead.

The surge in stocks catapulted the S&P 500 index SPX, +0.92%

almost back to the 4,000 mark on Friday, also lifting it to the biggest weekly gain in roughly five months, according to Dow Jones Market Data.

“We are not convinced this is the beginning of a new bull market,” said Sam Stovall, chief investment strategist at CRFA Research. “We believe that we are headed for recession. That has not been factored into earnings estimates and, therefore, share prices.”

Stovall also said the stock market has yet to see the “traditional shakeout of confidence capitulation that we typically see that marks the end of the bear markets.”

Yet, information technology stocks in the S&P 500 jumped 10% for the week, while financials, which stand to benefit from higher interest rates, rose 5.7%, according to FactSet.

That could reflect optimism about the odds of a slower pace of Federal Reserve rate hikes in the months ahead, after sharp rate rises helped to undermine valuations and pull tech stocks dramatically lower in the past year. However, Loretta Mester, president of the Cleveland Fed, and other Fed officials since the October inflation reading on Thursday have reiterated the need to keep rates high, until 7.7% annual rate finds a clearer path to the central bank’s 2% target.

The stock-market rally also might suggest that investors view continued mayhem in the crypto sector as contained, despite bitcoin BTCUSD, +0.42%

trading near its lowest level in two years and the shocking collapse in recent days of FTX, once the world’s third-largest cryptocurrency exchange.

Blows to the American economy rarely have been good for stocks. A look at seven past recessions, starting in 1969, shows declines for the S&P 500 as more typical than gains, with its most violent drop occurring in the 2007-2009 recession.

The more than 37% drop of the S&P 500 from 2007 to 2009 was the worst of its kind in a recession since the late 1960s.

Refinitiv data, London Stock Exchange Group

While a looming U.S. recession isn’t a foregone conclusion, CEOs of America’s biggest banks have been warning about the risks for months. JP Morgan Chase’s Jamie Dimon said in October that a “tough recession” could drag the S&P 500 down another 20%, even though he also said consumers were doing fine, for now.

Still, the steady stream of warnings about the recession odds have left many Americans confused and wondering if one can even happen without an increase in job losses.

Big moves lately in stocks also have been hard to decode, given the economy was shocked back to life in the pandemic by trillions of dollars in fiscal stimulus and easy-money policies from the Fed that are now being reversed.

“What I think goes unnoticed, certainly by the average person, is that these moves are not normal,” said Thomas Martin, senior portfolio manager at Globalt Investments, about stock swings this week.

“It’s all about who is positioned how — and for what — and how much leverage they’re employing,” Martin told MarketWatch. “You get these outsized moves when people are offside.”

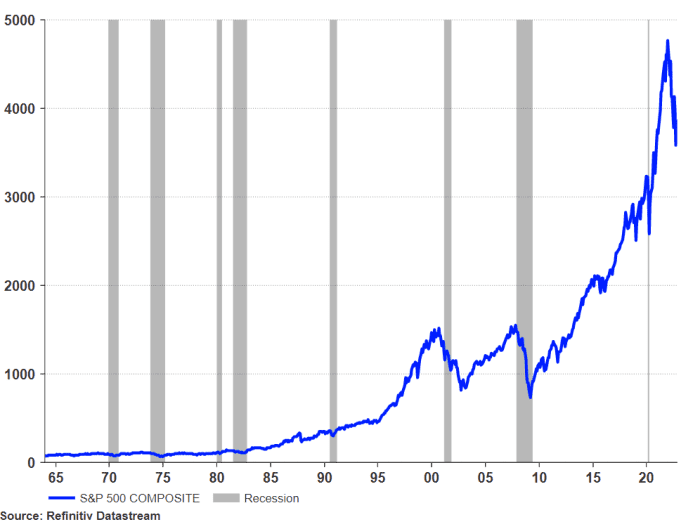

Here’s a view of the sharp trajectory upward of the S&P 500 since 2010, but also its dramatic drop this year.

Sharp rise of S&P 500 since 2010, but recent fall

Refinitiv Datastream

While Martin isn’t ruling out the potential for a seasonal “Santa Claus” rally heading into year-end, he worries about a potential leg lower for stocks next year, particularly with the Fed likely to keep interest rates high.

“Certainly what’s being priced in now is either no recession or a very, very mild recession,” he said .

However, Kristina Hooper, Invesco’s chief global market strategist, said the overarching story might be one of stocks sniffing out the first steps in a path to economic recovery, and the Fed potentially stopping its rate hikes at a lower “terminal” rate than expected.

The Fed increased its benchmark interest rate to a 3.75% to 4% range in November, the highest in 15 years, but also has signaled it could top out near 4.5% to 4.75%.

“If often happens that you can see stocks do well, in a less-than-good economic environment,” she said.

The S&P 500 rose 4.2% for the week, while the Dow Jones Industrial Average DJIA, +0.10%

gained 5.9%, posting its best weekly gain since late June, according to Dow Jones Market Data. The Nasdaq Composite Index shot up 8.1% for the week, its best weekly stretch in seven months.

In U.S. economic data, investors will get an update on household debt on Tuesday, retail sales and homebuilder data on Wednesday, followed by jobless claims and housing starts data Thursday. Friday brings existing home sales.

As expected, the US central bank – Federal Reserve – on Wednesday hiked interest rates by another 75 basis points in a bid to cool down persistent inflation. The move was on expected lines as inflation continues to be high despite previous rate hikes. On September 21, the Fed increased the rate by similar percentage points.

The US has been reeling under decades-high inflation caused by a combination of factors. The inflation number for September came in at 8.2 per cent, over four times the target set by the Fed. In September, Fed chairman Jerome Powell had said that he was strongly committed to bringing inflation back down to 2 per cent.

The Fed’s rate-setting committee – Federal Open Market Committee – said that recent indicators pointed to modest growth in spending and production. It said job gains had been robust in recent months, and the unemployment rate had remained low.

“Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures,” the Fed said, adding that Russia’s war against Ukraine is causing tremendous economic hardship and the war and related events are creating additional upward pressure on inflation and are weighing on global economic activity.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.046%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.030%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

These kinds of headlines are great for grabbing people’s attention, but otherwise they are not very helpful. As I (and others) have pointed out repeatedly, the year-to-year inflation rates will remain elevated for many more months even if the price level stays perfectly flat. That’s simply the math that we’re stuck with because the initial spike in prices was so high.

But those year-to-year rates say little about whether the Fed is currently failing to tame inflation or if the current rate of inflation is alarming.

To get a handle on these questions, one must look at the month-to-month inflation trends. The year-to-year changes reveal more about how the price level behaved earlier in the year. So, let’s check out those month-to-month changes that were released on October 13th.

From August to September, the Consumer Price Index rose 0.4 percent.

Is that figure alarming? Is inflation out of control? Those terms are rather subjective, but the monthly rate is well shy of the 8.2 percent annual rate reported for September.

As for the monthly trend, starting with July, the previous three rate increases were zero, 0.1, and 0.4 percent. So, the September rate is a bit higher than August when the monthly change was just 0.1 percent. Still, the last three months look better than the previous four, when the CPI increased by 1.2 percent (March), 0.3 percent (April), 1.0 percent (May), and 1.3 percent (June).

For the last three months, the rate of inflation averaged 0.17 percent. It averaged almost one percent for the previous four months.

Then, there’s the bigger question of what should the Fed do? To answer that question, let’s take a closer look at the details underlying the last two monthly CPI releases.

Many of the individual categories driving the overall inflation rate (i.e., driving the full CPI) were essentially unchanged from September to August. Changes in both major food categories and shelter, for example, were identical. New vehicle prices were only 0.1 percentage point different.

One of the main reasons the overall CPI rate was up a bit is that transportation services increased 1.9 percent in September, while it had only increased 0.5 percent in August. Moreover, energy prices fell just 2.1 percent in September after declining five percent in August. (Gasoline prices fell 4.9 percent in September after falling 10.6 percent in August, and fuel oil fell 2.7 percent in September versus 5.9 percent in August.)

A deeper look at those transportation numbers reveals what caused the 1.9 percent spike in September. The transportation services category includes the following three smaller items: (1) Motor vehicle maintenance and repair; (2) Motor vehicle insurance; and (3) Airline fares. From August to September, the first two items changed very little. However, airline fires increased 0.8 percent in September after having declined 4.6 percent in August.

Given that so many of the other CPI categories were essentially unchanged from August, if airline fares had declined at the same rate as the previous month, the overall CPI would have been flat. In that case, the average rate for the last three months would have been very close to zero.

Either way, there’s not much cause for alarm in the September numbers compared to the last few months. When the overall CPI barely moves for two consecutive months, and only increases by 0.3 percentage points because airline ticket prices rose (after having declined in the previous month), it’s hard to say the United States is experiencing runaway inflation.

This finer level of detail also has broader implications for the Fed and the way that it conducts monetary policy. The Fed adjusts its rate targets based on the overall rate of inflation to either slow down the overall flow of credit or boost it. For the last year or so, the Fed has been tightening, trying to slow down the overall flow of credit to slow down the economy and, therefore, the rate of inflation.

Whatever the Fed does right now with rates, it will likely have very little effect on airline fares. The Fed has poor price setting powers regarding specific categories of goods. Monetary policy is a very blunt instrument, and the past year has been a textbook case for why a central bank should not target prices at all.

So, while it makes sense for the Fed to stay its current course–talking tough on inflation and raising its targets if market rates continue to rise–it must avoid the clickbait.

Put differently, the Fed can ignore the dire headlines and avoid tightening so much that it causes a recession. If inflation expectations stay anchored–and there are indications that the Fed has succeeded on this front–the Fed won’t have to go crazy.

As I’ve argued before, journalists can help the Fed manage these inflation expectations. Just give more weight to the recent direction of the price level and stop fixating on the “record” annual rates. Those are going to stay high for many more months unless the Fed engineers a massive, rapid price deflation. And nobody, least of all the Fed, wants that outcome.