U.S. stocks and bonds are both falling again, with the S&P 500 just wrapping up its worst quarterly performance in a year after another surge in Treasury yields.

“That creates a lot of anxiety,” as there’s still a fair amount of “investor PTSD” from last year, when markets were rocked by losses in both equities and bonds, said Phil Camporeale, a portfolio manager for J.P. Morgan Asset Management’s global allocation strategy, by phone.

But it’s not the same environment.

Last year was about the Federal Reserve rushing to tame runaway inflation with rapid interest-rate hikes after being “behind the curve,” he said. Now investors are grappling with a surge in Treasury yields after the Fed in September doubled its U.S. growth forecast this year to 2.1%, according to Camporeale, pointing to the central bank’s latest summary of economic projections.

“This is your kiss-your-recession-goodbye trade,” he said, with sharp market moves in September reflecting the notion that “the Fed is not easing anytime soon.”

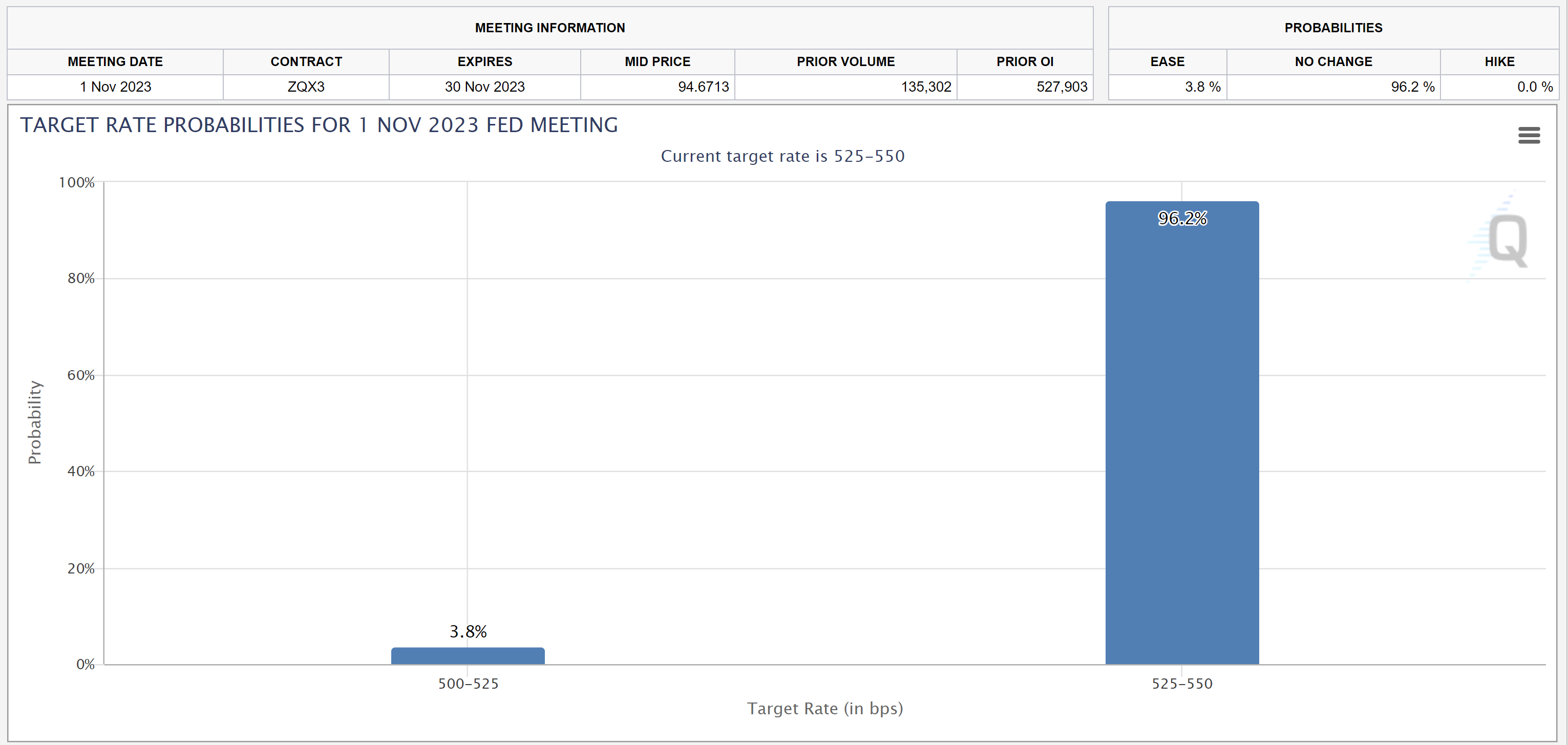

The U.S. labor market has been strong despite the central bank’s aggressive tightening of monetary policy, with the unemployment rate at a historically low 3.8% in August. In September, the Fed projected the jobless rate could move up to 4.1% by the end of next year, below its previous forecast from June.

“Inflation is falling,” Camporeale said. “The most important metric right now is the labor market.”

As he sees it, investors are worried that the Fed will hold interest rates higher for longer should the unemployment rate remain low and the labor market “tight.” The Fed projected in September that it could raise rates once more this year before reaching the end of its hiking cycle, with fewer potential rate cuts penciled in for 2024 than previously forecast.

Investors expect to get a look at the U.S. employment report for September this coming week, with nonfarm payrolls data scheduled to be released on Oct. 6.

See: Government shutdown averted for now as Congress approves 45-day funding bridge

Meanwhile, the U.S. stock market ended mostly lower Friday, with the Dow Jones Industrial Average

DJIA,

S&P 500

SPX

and Nasdaq Composite

COMP

all closing out September with monthly losses as investors weighed fresh data on inflation.

A reading Friday of the Fed’s preferred inflation gauge showed that core prices, which exclude volatile food and energy categories, edged up 0.1% in August. That was slightly less than expected. Meanwhile, the core inflation rate slowed to 3.9% over the 12 months through August.

But headline inflation measured by the personal-consumption-expenditures price index rose more than the core reading on a month-over-month basis, as higher gas prices fueled its increase.

S&P 500’s worst month of 2023

Investors have been anxious that the Fed may keep rates high for longer to bring inflation down to its 2% target.

Friday’s close left the S&P 500 logging its worst month since December, dropping 4.9% in September for back-to-back monthly losses. The S&P 500 sank 3.6% in the third quarter, suffering its biggest quarterly loss since the three months through September in 2022, according to Dow Jones Market Data.

The U.S. stock market has been startled by surging bond yields following the Fed’s policy meeting in September, after being jolted by the rise in Treasury rates in August.

“The price to pay for a resilient economy is higher yields,” said Steven Wieting, chief economist and chief investment strategist at Citi Global Wealth, in an interview. “We’re probably near the peak in yields.”

The yield on the 10-year Treasury note

BX:TMUBMUSD10Y

ended September at 4.572%, after rising just days earlier to its highest level since October 2007, according to Dow Jones Market Data. Yields and debt prices move opposite each other.

But for Camporeale, it’s still too early to venture out to the back end of the U.S. Treasury market’s yield curve to add duration to bondholdings. That’s because the yield curve is not yet “re-steepened” and he views the U.S. economy as currently on course for a soft landing with rates staying higher for longer.

“If you avoid recession, why should you have a lower yield as you go out in time?” said Camporeale. “You should be compensated for having more yield as you go out in time if you avoid recession, not less.”

The 2-year Treasury rate

BX:TMUBMUSD02Y

finished September at 5.046%, continuing to yield more than 10-year Treasury notes.

The yield curve has been inverted for a while, with short-term Treasurys offering higher rates than longer-term ones. The situation is being monitored by investors because historically such inversion has preceded a recession.

“If we were nervous about growth we would be buying the 10-year part of the curve or the 30-year part of the curve,” said Camporeale. “But we are not doing that right now.”

As for asset allocation, he said he’s now neutral stocks and overweight U.S. high-yield credit, particularly bonds with shorter durations of one to three years.

Camporeale sees junk bonds as a “nice” trade as he is not expecting a recession in the next 12 months and they are providing “enticing” yields versus the U.S. equity market, which probably has most of its returns in “versus what we think you get through the rest of the year.”

The S&P 500 index was up 11.7% this year through September, FactSet data show.

While watching for any signs of deterioration in the labor market, Camporeale said he now anticipates the earliest the Fed may cut rates is in the second half of next year. To his thinking, the recent move higher in 10-year Treasury yields was appropriate “in a world where maybe the yield curve has to re-steepen.”

‘Pain trade’

Bond prices in the U.S. broadly dropped in September along with the stocks.

The iShares Core U.S. Aggregate Bond ETF

AGG

was down 2.6% last month on a total return basis, bringing its total loss for the third quarter to 3.2%, according to FactSet data. That was the fund’s worst quarterly performance since the third quarter of 2022.

The ETF, which tracks an index of investment-grade bonds in the U.S. such as Treasurys and corporate debt, has lost 1% on a total return basis so far this year through September, FactSet data show. Meanwhile, the iShares 20+ Year Treasury Bond ETF

TLT

has seen a total loss of 9% over the same period.

“Few investors want to call the top for peak rates,” said George Catrambone, head of fixed income at DWS, in a phone interview. Some bond investors had started to extend into long-term Treasurys in July. “That’s been the pain trade, I think, ever since then,” said Catrambone.

As for the equity market, the speed of the move up in 10-year Treasury yields hurt stocks, with the rate climbing “well beyond what many assumed would be the upper end,” according to Liz Ann Sonders, chief investment strategist at Charles Schwab.

With higher rates pressuring equity valuations, “clearly what’s going to matter is third-quarter-earnings season, once that kicks in” during October, she said by phone. Company “earnings are going to have to start to do some more heavy lifting.”