A CryptoQuant Analyst has identified a significant systemic buying trend in Ethereum, suggesting a rising influx of strategic investments into the blockchain network.

Analyst Reveals Ethereum Systemic Buying Trend

A crypto market observer and a contributing analyst at CryptoQuant, Maarten Regterschot has taken to X (formerly Twitter) to publish a systemic buying trend he witnessed in Ethereum. The analyst presented a chart indicating that one or more investors have been engaging in Time Weighted Average Price (TWAP) buying on Ethereum futures.

Regterschot stated that the linear increase in open interest in Ethereum suggests that there has been systemic buying of ETH assets for an extended period of time. He revealed that approximately $700 million has already been added to the market.

“Someone(s) are TWAP-buying on Ethereum futures. This linear growth in open interest indicates systematic buying over a certain period. There is $700 million added so far,” Regterschot said.

Systemic buying in this context involves crypto investments made at regular and periodic intervals. TWAP on the other hand is the measure of an asset’s average price over a specific time period.

This systemic buying trend suggests a growing demand for ETH by investors over a long period. The trend also coincides with the latest Ethereum developments in the crypto space, including the growing applications on Ethereum Spot ETFs and its potential approval by the United States Securities and Exchange Commission (SEC).

The analyst has not revealed insights into the motives behind this systemic buying of Ethereum. However, the developments could become a catalyst for a potential bullish momentum for Ethereum (ETH).

ETH Price Holds $2000 Mark

The price of Ethereum has seen multiple upticks within the last few months, allowing the cryptocurrency to finally cross the $2,000 mark. According to CoinMarketCap, Ethereum’s price is up by 2.3% and trading at $2,062 at the time of writing. Although its overall market capitalization is down by 23.31%, the cryptocurrency has been experiencing a fair amount of price increases recently.

As the potential approval of Ethereum Spot ETFs by the US SEC looms next year, many investors are currently holding their crypto assets as they gear up for a possible bull run. There have also been several optimistic price projections for the ETH token. Some analysts have predicted that the price of the cryptocurrency will reach $2,250 if it succeeds in crossing multiple resistance levels.

BlackRock has joined the Ethereum Spot ETF race as the asset management company has officially applied to the US SEC and is currently waiting for approval.

The asset management company submitted the application on November 15, however, BlackRock has stated it formed the Trust as early as November 9.

According to BlackRock, the iShares Ethereum Trust would be used to facilitate the ownership of Ether through the issuance of shares, allowing investors to own a fractional undivided beneficial interest in the net assets of the Trust.

“The Trust was formed as a Delaware statutory trust on November 9, 2023. The purpose of the Trust is to own ether transferred to the Trust in exchange for Shares issued by the Trust. Each Share represents a fractional undivided beneficial interest in the net assets of the Trust. The assets of the Trust consist primarily of ether held by the Ether Custodian on behalf of the Trust,” BlackRock said in its filing.

The crypto community has remained enthusiastic that the regulatory agency would eventually approve the pending ETF applications, as this could significantly push the growth and development of the crypto ecosystem as well as the cryptocurrencies involved.

Ethereum Price Surges

The price of Ethereum is on the rise following BlackRock’s Ethereum ETF filing. The cryptocurrency’s price climbed almost 2% moving to $2,080 at some point following the announcement of the filing.

The sharp reaction has caused a stir in the cryptocurrency community, as investors gear up for a potential bull run if the US SEC gives its official authorization of Ethereum Spot ETFs.

The price of Bitcoin has also been growing steadily as new companies apply for Spot Bitcoin ETFs. Currently, Bitcoin’s price is trading at $36,408, while ETH is down from its initial surge and trading at $1,952.

The crypto ecosystem is presently watching closely for more updates on the US SEC’s ETF filing approvals and the price changes that follow them.

Following BlackRock’s official filing of Spot Ethereum with Nasdaq, reports have confirmed that BlackRock’s Ether ETF plan has been confirmed by Nasdaq and is on its way to the US SEC to gain final approval.

BlackRock Ethereum Spot ETF Confirmed

American multinational investment company, BlackRock has been making waves in the crypto space after news spread of NASDAQ listing the investment firm’s Ethereum Spot ETF, iShares Ether Trust in Delaware.

“BlackRock’s Ethereum ETF confirmed. They just submitted a 19b-4 filing with Nasdaq,” Bloomberg Research Analyst, Jeff Seyffart stated.

While BlackRock’s Spot Bitcoin ETF proposal remains to be approved by the United States Securities and Exchange Commission (SEC), the $9 trillion asset management company has placed its focus on Ethereum Spot ETFs while it waits for the SEC’s final decision on Spot Bitcoin ETFs.

The news of the Nasdaq Ethereum ETF filing comes as a major development for BlackRock’s move into the ETF world. Although the investment company remains tight-lipped on the ETH ETF reports flowing through the space, the possibility of an Ether Spot ETF approval could be a sign of the SEC’s approval of Spot Bitcoin ETFs in the future.

Many crypto enthusiasts have predicted that the US SEC may continue its efforts to stop the growth of Spot Bitcoin ETFs by declining BlackRock’s Ether Spot ETF filing.

However, in the case the regulatory body does approve the asset management company’s Ethereum Spot ETF, the SEC could be faced with potential contradictions in its decision-making processes. The acceptance of ETH Spot ETFs would stand in stark contrast to the previous disapproval of Spot Bitcoin ETFs.

Presently, the crypto community has been largely positive, as market metrics signal a potential rally for altcoins following BlackRock’s Ethereum Spot ETF confirmation.

A crypto member has stated that the asset management company’s move into Ether Spot ETFs indicates strategic confidence in securing approval for Spot Bitcoin ETF in the future.

ETH Price Skyrockets

Following the news of NASDAQ registering BlackRock’s Ethereum Spot ETF, the price of ETH has increased by over 9% and is currently trading at $2,086.92 according to CoinMarketCap.

Reports of the Ethereum Spot ETF filing have sparked a rally in the cryptocurrency, topping over $2,000 for the first time since April this year. ETH’s market volume has also increased by 171.53%.

Many crypto investors are looking forward to more positive developments in the cryptocurrency regarding Ethereum Spot ETFs as an official approval may indicate a potential long-term bull run for ETH.

Going by the handle “@bkiepuszewski,” one X user contends that the transaction processing speed (TPS) metric analysts rely on to measure how fast a blockchain network like Ethereum or the BNB Chain processes transactions is flawed.

Laying out reasons on X, the decentralized finance (DeFi) researcher is convinced that using an alternative metric, the User Ops per second (UOPS), could paint a clearer picture of how well a blockchain is utilized at all times.

Measuring Network Utilization

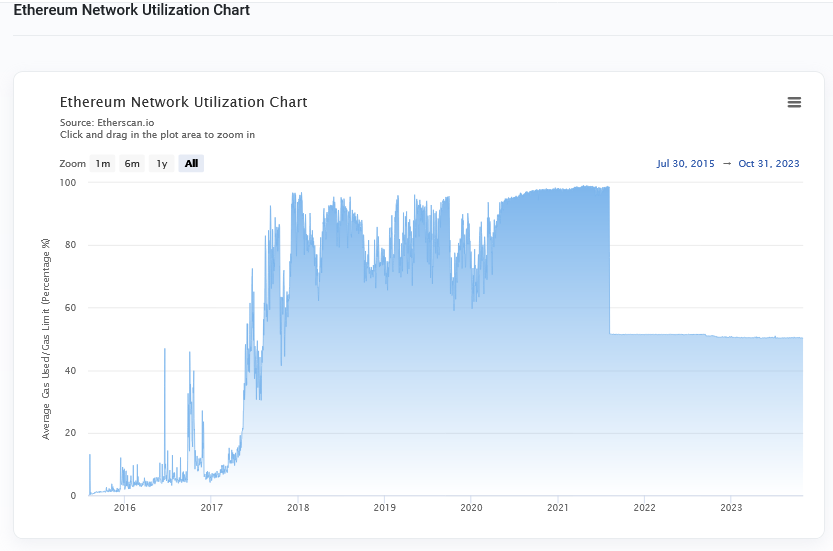

Typically, blockchain utilization measures how much a given network, for instance, Bitcoin or Ethereum, is being used at a given point. This is critical because it can be used to measure adoption levels since those with higher utilization rates tend to have a broader, active base, which can make it successful over the long haul.

To gauge activity, this metric considers the number of transactions processed every second when dealing with simple transfers or the total value locked (TVL) when dealing with smart contracts deployed.

As of November 1, the average network utilization rate in Ethereum, based on Etherscan data, is around 50%, down from about 100% registered in 2021. Meanwhile, the Bitcoin Transactions Per Day as of early November stood above 433,000, a nearly 2X increase from late October.

Usually, in the case of Bitcoin, considering it is a transactional layer, whenever prices rise, more BTC-related transactions are expected as users hope to increase the emerging trend.

Whether the UOPS system will be adopted in the long term remains to be seen. However, what’s clear is that the UOPS will consider the number of user operations that the network in question can process every second, all while factoring in the level of complexity of that transaction.

Out of the UOPS, analysts will instantaneously know how well the blockchain can handle user load without the risk of congestion, as usually is the case in Ethereum when markets are trending higher.

The Rise Of Ethereum Layer-2s

At the same time, according to @bkiepuszewski, using UOPS instead of TPS brings clarity considering the widespread use of layer-2 solutions, including OP Mainnet, Base, and StarkNet, which bundles transactions offline before confirming them on the mainnet as a single transfer. The more dapps choose layer-2 solutions, the more flawed blockchain throughput calculation will be if TPS guides.

Presently, more developers are opting for layer-2 as their base to avoid scaling issues while accessing the latitude to deploy intensive dapps such as social media platforms, as seen with Friend.tech. According to L2Beat, Arbitrum and OP Mainnet have TVLs of over $6.5 and $2.9 billion, respectively.

Ethereum venture capitalists (VCs) are “not stupid” and know that investing in the world’s largest smart contract platform won’t result in the “multiples” they desire, according to a crypto user. Going by the handle R89Capital, claims that VCs are now looking at Ethereum layer-2 assets as vehicles to exit the market, dumping “Ponzi tokens.”

Ethereum VCs Exiting ETH For “Ponzi” Tokens?

The user opines that the primary reason why ETH prices may not surge in multiples like emerging tokens, including meme coins like PEPE, for instance, is because of the relatively large market cap.

According to trackers on October 31, ETH has a market cap of over $215.8 billion and is the second largest after Bitcoin (BTC). Typically, coins with higher market caps are harder to manipulate and usually have found more institutional adoption than emerging tokens.

This is because projects with higher market cap are more liquid, have more name recognition, and have seen more adoption. Even so, while they are easier to buy in the second market due to the higher levels of liquidity, they tend to be less volatile than low market cap tokens.

These low-market tokens can also be held for speculative reasons primarily due to their upside potential, especially in trending markets. This means that low-market tokens, regardless of the issuing platform, appeal to profit-seeking speculators, not due to underlying fundamentals.

R89Capital aligns with this preview to allege that VCs, looking to recoup their investment, are launching Ponzi tokens on general-purpose layer-2 platforms before dumping them for ETH and eventually exiting for USD.

In this case, Ponzi tokens, as claimed, are low-market coins that can be meme coins or other well-marketed projects. These tokens have higher upsides, are liquid enough, and can be sold for ETH in layer-2 decentralized exchanges or popular ramps like Binance or Coinbase.

The Ethereum Technical Debt: Scaling Remains A Big Issue

Still, R89Capital didn’t mention which layer-2 projects are “Ponzis” but said the primary reason ETH is capped is due to Ethereum’s technical debt.

Over the years, Ethereum developers have been launching new products and scaling solutions, of which the transition from a proof-of-work to a proof-of-stake system and adoption of layer-2 solutions stand out. Even so, scaling remains a challenge impacting user experience, especially when token prices begin rallying.

It is not unusual for gas fees on Ethereum to spike to double-digits in a bull market, discouraging deployment while catalyzing migration of some transactions to competing platforms like Solana or layer-2 scaling solutions like Base or Optimism.

The Ethereum supply on exchanges has been on a steady decline since the FTX crash happened back in 2022. This was triggered by a growing distrust for centralized exchanges and investors choosing to self-custody their tokens as a result. The constant decline has now seen the Ethereum being held on exchanges fall to the lowest point since its inception.

Available ETH On Exchanges Fall To Genesis Levels

When the Ethereum network was first launched back in 2015, the available ETH on exchanges was very low due to it being a new player. The exchange balances would steadily rise over the next few years as the digital asset gained widespread acceptance and began trading on countless exchanges.

However, there has been a shift in the tide where crypto investors are now choosing to hold their ETH in private wallets rather than leaving them on exchanges. The result of this is now there is only 8.41% of the total ETH circulating supply available on exchanges.

On-chain data tracker Santiment points out that this is the lowest that Ethereum exchange balances have been since Genesis in 2015. “Prices crossed $1,850 for the first time since August 15th, and the now 8.41% of $ETH supply on exchanges is the lowest since #genesis in 2015. Whale transactions also hit a 6-month high,” Santiment said in an X post.

The move away from exchanges coincides with a rapid increase in price which suggests that holder accumulation has played a major role in the digital asset’s recovery. And if exchange balances continue to fall, meaning less willingness to sell off ETH and lower sell pressure, the value could continue to soar.

Now that the $1,700 resistance has been cleared by Ethereum bulls, they have begun to turn their attention toward much higher price points. The next significant resistance lies at $1,850 as was demonstrated on Tuesday when the bulls were rejected from that level. So $1,850 is the first price trade foo clear in the bid to establish a stronger bull trend.

Next on the list is the $1,920 level where a major roadblock is expected to happen for the ETH price. This will be one of the last defenses of the bears to prevent a full-blown bull rally and bulls are sure to run into a lot of resistance at this level.

Last but not least is the $2,000 mark which has eluded bulls for the better part of this year. It is arguably the most significant price level for Ethereum right now that could signal an end to the bleed. So ETH bulls will need to reclaim this level from the bears and turn it into support.

Ethereum (ETH) has so far relatively underperformed in comparison to the flagship cryptocurrency Bitcoin. However, that could change soon enough as a crypto analyst has predicted the second-largest crypto token by market to gain some momentum soon enough.

Ethereum To Hit $1900

In a post shared on his X (formerly Twitter) platform, prominent crypto analyst Ali Martinez mentioned that Ethereum could rise to as high as $1,900. His prediction was based on data that he had pulled up from the chart which he shared in his post.

The chart (a 3-day timeframe) featured an ascending triangle pattern, which usually represents a bullish formation. According to Ali, Ethereum is “poised” to rebound off the hypotenuse of the ascending triangle. Most importantly, for Ethereum to go as high as $1,900, the analyst noted that It has to experience a “firm close” above the 18-day SMA (Simple Moving Average).

ETH getting ready to breakout | Source: X

If that happens, Ethereum could hit $1,800 and further rise to $1,900 based on Ali’s predictions. It is worth mentioning that the last time Ethereum hit $1,900 was back in July 2023. A rise to that price again will represent about an %18 increase from its current price of $1,600.

Ali also had something to say about the flagship cryptocurrency, Bitcoin. In a subsequent post, he noted that the crypto token could see a correction to $28,800; a prediction he made based on the TD Sequential from a 4-hour chart.

Bitcoin rose to as high as $30,000 on October 20, with many speculating that a Spot Bitcoin ETF approval could be on the way, something that represents a bullish momentum for Bitcoin and the crypto market in general.

Data from TradingView shows that Bitcoin’s dominance has been on the rise this year, with the token currently boasting over 52% coin dominance in the crypto market. Interestingly, it has steadily risen since the Ethereum Merge occurred.

This is significant considering that many speculated that ‘the Flippening’ could happen after the Merge, where Ethereum overtakes Bitcoin to become the most dominant crypto token. However, that hasn’t happened so far, with Ethereum’s move from proof-of-work to proof-of-work being seen as ‘disastrous’ for the crypto token.

Bitcoin and Ethereum, however, share the podium when it comes to the best-performing assets of the year. Both crypto tokens are said to have outperformed the NASDAQ, S&P500, and Gold. Bitcoin has seen an %80 increase year-to-date (YTD), while Ethereum has seen a %35 increase YTD.

Featured image from Analytics Insight, chart from Tradingview.com

The Ethereum initial coin offering (ICO), which took place in 2014, represents one of the most significant events in the history of cryptocurrency. As the network had not begun generating tokens autonomously, the ICO event allowed early investors and enthusiasts to accumulate ETH, currently the second-largest cryptocurrency by market cap.

Latest on-chain data shows that one of the ICO participants has become active for the first time in more than eight years, transferring their pre-mined stash of Ether tokens to different addresses on Saturday, October 21.

💤 A dormant pre-mine address containing 2,000 #ETH (3,198,920 USD) has just been activated after 8.2 years!https://t.co/0Mpx77N5fs

According to blockchain data tracker Lookonchain, the address, which was part of the Ethereum Genesis, initially received 2,000 ETH over eight years ago. At the time, the Ether tokens were purchased for $620 at an ICO price of $0.31 per token. On Saturday, the ETH tokens in question changed wallets for the first time.

An #Ethereum#ICO participant woke up after 8.2 years of dormancy and transferred all 2,000 $ETH($3.2M currently) to 4 addresses 10 mins ago.

The wallet holding the pre-mined stash of ETH had been dormant for exactly 8.2 years (July 2015). Thanks to the exponential growth of Ethereum and the entire crypto market, the value of these holdings has grown to nearly $3.2 million at the current price.

In the X (formerly Twitter) post, Lookonchain highlighted that the ICO participant transferred the Ethereum tokens to four different addresses. About 500 Ether tokens were sent to each address, with minutes separating the transactions.

It remains to be seen whether the wallet owner is preparing to sell the tokens, stake on the network, or carry out other transactions. In the event of a sell-off, though, the price of ETH may experience momentary downward pressure.

Large transfers from early ICO participants are not exactly common occurrences, but there have already been a couple of similar transactions in 2023. Notably, an ICO participant moved $116 million worth of pre-mined ETH to a Kraken exchange address in July.

ETH Price Overview

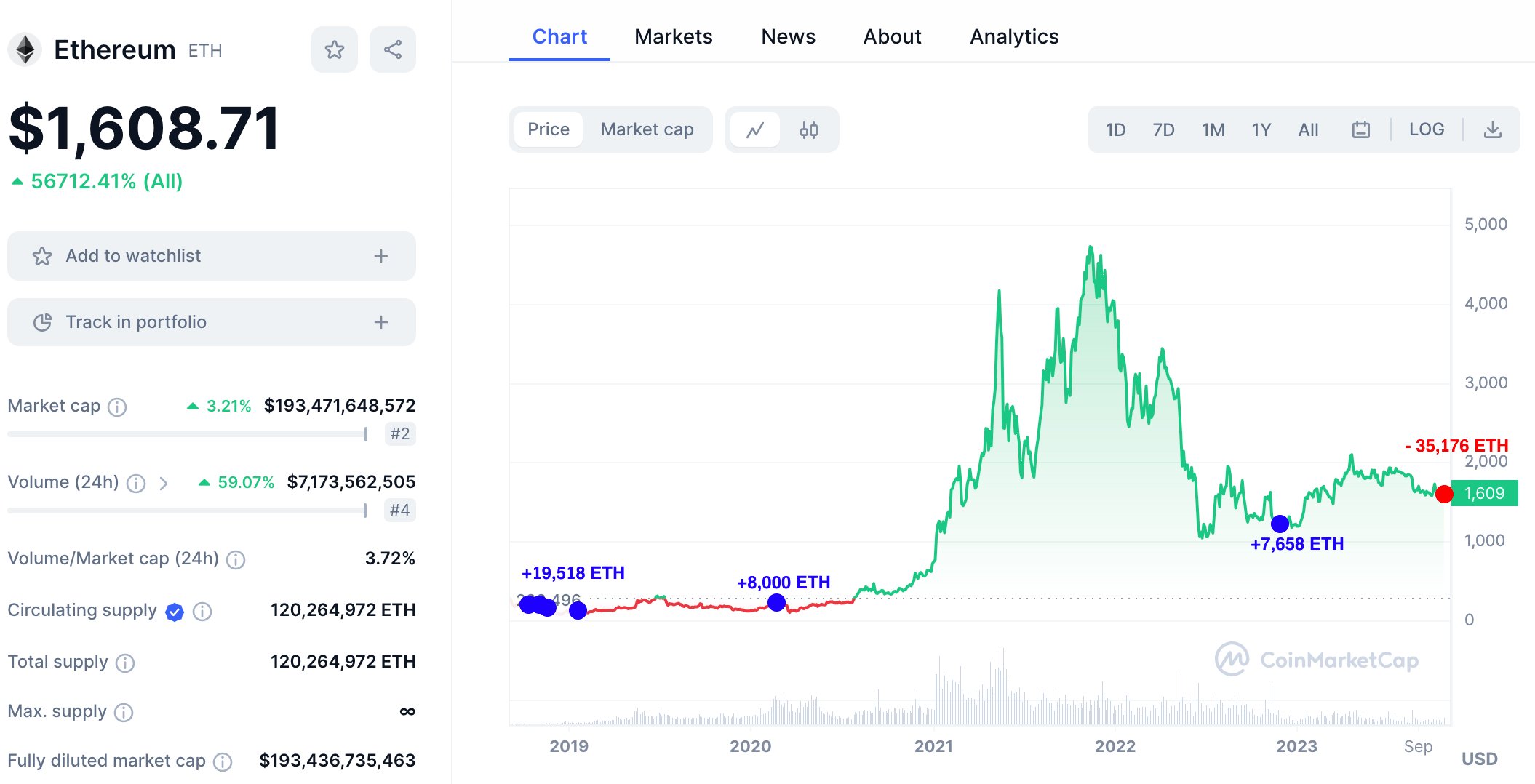

As of this writing, Ethereum’s price stands at $1,605, reflecting a 0.7% decline in the past day. This comes on the back of a week where the value of ETH showed signs of recovery, registering a 3.8% price increase in the past seven days.

The past week was dominated mainly by the optimistic performance of Bitcoin and the false news of a spot ETF approval. This positive run of BTC, however, eventually rubbed on the broader cryptocurrency market, including the price of Ethereum.

Ethereum price hovers around the $1,600 mark on the daily timeframe | Source: ETHUSDT chart on TradingView

Featured image from The Economic Times, chart from TradingView

Data from Lookonchain, a blockchain analytics platform, on October 20, shows that one Ethereum (ETH) whale is actively moving coins to Kraken, a crypto exchange, and appears to be selling. The unidentified whale deposited 35,176 ETH, worth over $56.5 million when writing, and withdrew $10 million in USDT hours later. USDT is the world’s most liquid stablecoin, tracking the value of the USD.

Ethereum Whale Selling On Kraken

Still, it is not immediately clear whether the whale ended up selling the whole stash and only choosing to withdraw $10 million. What’s evident is that the unknown whale has been actively accumulating Ethereum for some years before deciding to take profit.

Looking at market trends, the whale appears to be taking profit and exiting. Often, when coins are moved to centralized crypto exchanges, market participants interpret the event as net bearish. This can impact sentiment, even forcing prices lower, especially if the broader crypto market is falling.

Deposits to Kraken| Source: Lookonchain on X

According to Lookonchain, the whale accumulated 35,176 ETH on Kraken at an average price of around $415. When the address chose to liquidate, its realized profit was approximately $41.8 million. Ethereum prices have more than quadrupled the average entry price at spot rates, meaning the whale remains “in green” despite recent market gyrations.

Ethereum whale accumulating| Source: Lookonchain on X

Since prices have been primarily dicey, moving horizontally and occasionally posting sharp falls, the whale might have chosen to exit. Even so, it could not be ascertained what motivated the ETH holder to sell when sentiment is overly improving across the crypto scene.

Presently, Ethereum traders are bullish, expecting prices to increase in the sessions ahead. Notably, as of October 20, prices were relatively firm and rising. To illustrate, Ethereum is up roughly 3%, and bulls are soaking selling pressure. At the same time, the coin is up 5% from October 2023 lows.

Traders Bullish, Will ETH Clear $2,000?

Ethereum price charts show that the immediate resistance level in the medium term is at around $1,750, recorded in early October. On the flip side, support is at $1,530. A bullish breakout at the back of rising volumes pushing the coin above the resistance level may trigger more demand, propelling it toward the psychological $2,000 level.

In early October, the United States Securities and Exchange Commission (SEC) approved several Ethereum Futures Exchange-Traded Funds (ETFs), including VanEck Ethereum Strategy ETF (EFUT) and ProShares Ether Strategy ETF (EETH). Analysts interpreted this decision as a boost for ETH since it allowed institutions to have a regulated way of investing in Ethereum without necessarily having to buy and store the coins by themselves.

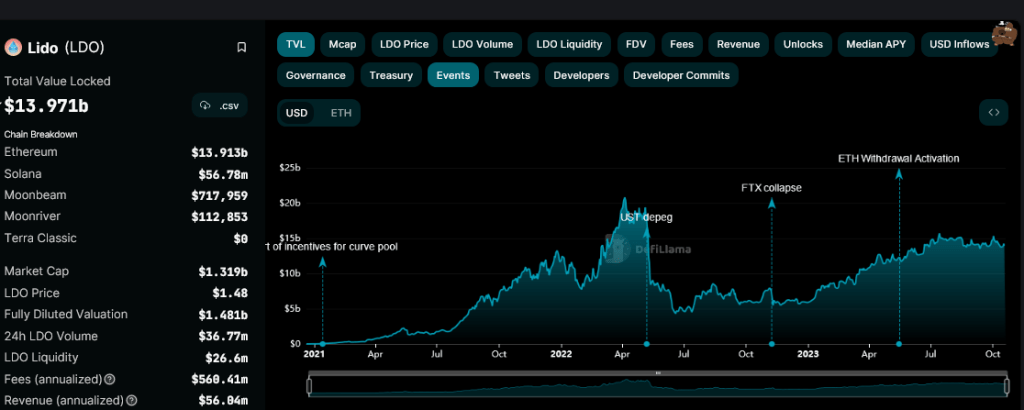

The total amount of Ethereum (ETH) staked on Lido Finance, one of the many liquidity staking protocols available, has risen steadily over the past few years. Surprisingly, revenue accrued by the platform (compared to staking rewards distributed) remains comparatively low.

Lido Finance Revenue Isn’t Growing As Fast As Expected

Looking at Token Terminal data shared on October 19, the blockchain analytic platform observed that while staking rewards paid, counted as “fees” by Lido Finance grew from less than $10 million in early 2021 to over $60 million in June 2023, revenue has grown at a much slower pace. To illustrate, Lido Finance’s average revenue is roughly less than $5 million during this period.

Lido Finance fees versus revenue| Source: Token Terminal

Overall, Lido Finance is a liquidity staking protocol that supports the staking of multiple proof-of-stake (PoS) coins like Ethereum (ETH) without necessarily locking them up. Users can concurrently earn staking rewards while accessing their hard-earned ETH–or any other coin supported.

The protocol issues another derivative, stETH, for every ETH staked to achieve this. This token can be freely traded on exchanges. It can even be used as collateral for users keen on taking trustless loans on supported platforms.

Ethereum recently shifted to be a proof-of-stake blockchain to be greener and conserve the environment. This transition was a boon for protocols that supported the first smart contract platform to confirm transactions and remain secure, especially after the activation of Shanghai in April 2023.

The Shanghai upgrade allowed Ethereum validators to withdraw their staked ETH for the first time, permitting them to use alternatives, of which Lido Finance, looking at total value locked (TVL), was preferred. As of October 19, Lido Finance had a TVL of $13.913 billion, most of it being assets on Ethereum.

Lido Finance TVL| Source: DeFiLlama

Ethereum Centralization Concerns: How Will This Be Addressed?

Lido Finance makes staking more accessible to everyone while concurrently enhancing liquidity. However, the revenue generated appears low versus the amount of staking rewards distributed to stakers, most of whom are from Ethereum. Part of the revenue the network generates is also distributed to LDO holders and node operators. Whether the liquidity staking protocol plans to increase the 10% fee charged to increase revenue earned remains to be seen.

Presently, there are concerns that Lido Finance’s role on Ethereum could lead to centralization. Ethereum has been accused of being “centralized,” mainly in how it is built. Critics assert that the reliance on its co-founder, Vitalik Buterin, for endorsement and guidance could slow down development in the future.

Zerodha founder and CEO Nithin Kamath has hailed the Indian capital market infrastructure and regulations and said the entire system does not get enough credit for being among the best globally. In a LinkedIn post that has gone viral, Kamath talked about the crypto world and that brokers and exchanges can act as banks in most markets.

He added, “In India, all securities are held by the customer at the depository. All unused funds are sent back monthly/quarterly and one client’s funds can’t be used to fund another. In most markets, brokers can hold customer securities and funds indefinitely and use them any way they want.”

The Zerodha founder went ahead and commended the Securities and Exchange Board of India (SEBI) for their efforts aimed at protecting the interests of the retail investors by reducing risks and making markets safer.

Kamath’s comments come after a deal between crypto exchanges FTX and Binance collapsed. The deal was touted as an emergency rescue in the world of cryptocurrencies as investors pulled their money back from risky assets.

Binance said in a statement accessed by news agency Reuters, “As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com.”

After this, FTX CEO Sam Bankman-Fried said in a message to employees, “I’m working, as quickly as I can, on the next steps here. I wish I could give you all more clarity than I can.”

Meanwhile, cryptocurrency market-cap saw a decline of 7.82 per cent to $835.16 billion. Key tokens such as Bitcoin and Ethereum also fell to $16,612.50 and $1,181.61 respectively. Market cap of Bitcoin and Ethereum stands at $319.67 billion and $145.09 billion at the time of writing this story, according to coinmarketcap.com.

The luna price, which was trading as high as $100 per luna just last month, crashed to near zero this week—causing the algorithmic stablecoin UST to completely lose its peg to the U.S. dollar—amid a $1 trillion crypto crash that sent the bitcoin price down by over 20%.

Now, the chief executive of UST and luna developer Terraform Labs, Do Kwon, has pitched a revival plan that could see ownership in the network distributed across UST and luna holders—causing the luna price to surge over 1,000% as traders bet the project could recover.

Want to stay ahead of the market and understand the latest crypto news? Sign up now for the free CryptoCodex—A daily newsletter for crypto investors and the crypto-curious

The chief executive of Terraform Labs Do Kwon pitched a “revival plan” for luna and the algorithmic … [+] stablecoin UST following the blockchain ecosystem’s collapse.

“While UST has been the central narrative of Terra’s growth story over the last year, the Terra ecosystem and its community is what is worth preserving,” Kwon wrote in a post on a Terra discussion forum, adding the Terra community “must reconstitute the chain to preserve the community and the developer ecosystem.”

The reconstitute—effectively a restart of the terra blockchain—would create 1 billion tokens to be distributed among various community stakeholders, with 40% going to luna holders before the UST de-pegging, 40% to go to UST holders “pro-rata at the time of the new network upgrade,” 10% to luna holders before the chain halt, and 10% to the “Community Pool to fund future development.”

The blockchain underpinning luna and UST was shut down multiple times this week to “prevent governance attacks” following “severe [luna] inflation.”

Terraform Labs and the Luna Foundation Guard, tasked with supporting UST, this week printed several billion luna tokens—increasing the luna supply from 340 million last week to 6.5 trillion—in a failed attempt to maintain the UST peg to the dollar.

The luna price has fallen by almost 100% over the last week, sparking a bitcoin and crypto crisis.

Coinbase

“Terra needs a community to continue to grow and make its blockspace valuable again—the only way to do this is to make sure that token holders before the attack commenced, the most loyal community members and builders, stick around to keep providing value,” Kwon wrote, adding, the ecosystem will not survive “in its current state.”

In a follow-up tweet thread, Kwon said he’s “heartbroken” about the collapse of luna and UST but said he’s confident the “community will form consensus around the best path forward for itself and find a way to rise again.”

Others in the crypto community have also suggested the project could still survive in some form with Binance chief executive Changpeng Zhao, often known simply as CZ, saying there has been “progress” made.

“Luna blockchain resumed, no more minting,” CZ posted to Twitter. “And deposits, withdrawals and trading resumed. Trading is important for existing holders.”

The luna and UST collapse this week came amid a bitcoin, ethereum and wider crypto market downturn that made UST vulnerable, with some speculating there may have been an orchestrated attack on the stablecoin.

“The pullback in general markets created the conditions for an attack on UST, which was inherently fragile,” Cory Klippsten, the founder and CEO of bitcoin-buying app Swan Bitcoin, said in a Telegram message, adding, “the effects of the unwind are wide reaching, and the ultimate magnitude still unknowable.”

Bitcoin, ethereum and cryptocurrency prices have swung wildly over the last week as Russia’s invasion of Ukraine sends shockwaves through global markets—adding to fears of a “cataclysmic market shift.”

The bitcoin price fell under $35,000 per bitcoin this week before rebounding sharply. Ethereum and other major cryptocurrencies have been equally as volatile as “extreme fear” grips investors.

Now, traders are braced for severe gyrations after Russia was kicked off the world’s main international payments network SWIFT, with a former Russian Central Bank deputy chairman warning of “catastrophe” on the Russian currency market.

The bitcoin price has fallen sharply in recent months with the Russia invasion of Ukraine causing … [+] further volatility for bitcoin, ethereum and other cryptocurrencies.

SOPA Images/LightRocket via Getty Images

“It means there is going to be a catastrophe on the Russian currency market on Monday,” Sergei Aleksashenko told Reuters. “I think they will stop trading and then the exchange rate will be fixed at an artificial level just like in Soviet times.”

On Saturday, the U.S., the E.U., the U.K., France, Germany, Italy, and Canada announced in a joint statement they would penalize Russia’s central bank and exclude some Russian banks from the SWIFT messaging system, used for trillions of dollars worth of transactions around the world, and designed to “prevent the Russian Central Bank from deploying its international reserves in ways that undermine the impact of our sanctions.”

It’s thought Russia holds about $300 billion of foreign currency offshore—enough to disrupt money markets if it’s frozen by sanctions or moved suddenly to avoid them, according to a Credit Suisse report reported by Bloomberg.

Bitcoin, ethereum and crypto prices had recovered along with stock markets toward the end of this week as traders came to terms with Russian sanctions. However, it’s thought the latest measures could trigger fresh volatility, with soaring commodity prices and inflation fears rattling investors in recent weeks.

Bitcoin’s extreme price volatility at a time when the gold price has climbed has undermined the popular narrative that bitcoin has begun acting as digital gold, a so-called safe-haven asset that investors flee to in times of perceived risk—though some bitcoin and crypto investors remain confident.

“In contrast to major stock indices, bitcoin hasn’t actually recorded a lower low [this week],” Mikkel Morch, executive director at digital asset Fund ARK36, wrote in an emailed note. “This small detail could be of great significance in terms of the talk around bitcoin as a safe haven asset.”

Despite the bitcoin, ethereum and crypto price recovery, fears persist that the bitcoin price could fall back again.

“The situation is still volatile and the $40,000 levels are still the resistance,” Morch added. “Unless bitcoin meaningfully breaks this barrier, revisiting the range lows or even the $30,000 support is still very much on the table in the short term.”

“If the situation in Ukraine escalates even more bitcoin may fall below $30,000 as investors leave for defensive assets,” Alex Kuptsikevich, senior financial analyst at FxPro, said in emailed comments, pointing to reports Russia could use cryptocurrency to circumvent sanctions. “Otherwise, the country will not survive the growing sanctions pressure from Western countries.”

The bitcoin price fell to lows not seen since a major crypto crash last month as fears mount over … [+] the knock-on effects of Russia’s invasion of Ukraine. Ethereum and other cryptocurrencies have also swung wildly.

Coinbase

However, others in the bitcoin and crypto community think its unlikely bitcoin could be used by Russia to evade global sanctions.

“The suggestion that Russia could use bitcoin to evade sanctions is mostly an exaggeration by the media,” Cory Klippsten, the chief executive of bitcoin-buying app Swan Bitcoin, said via Telegram.

“Technically, Russia could use bitcoin given its permissionless, open nature, but there are methods for agencies to trace bitcoin transactions. It’s important to note that bitcoin is a technology that can be accessed by anyone, no matter if you agree with their actions or not.”

Almost $14 million has so far been donated to the Ukrainian war effort through anonymous bitcoin donations, according to researchers at Elliptic, a blockchain analysis company.

On Saturday, the official Twitter account of the Ukraine government posted: “Stand with the people of Ukraine. Now accepting cryptocurrency donations. bitcoin, ethereum and USDT”—a stablecoin pegged to the U.S. dollar. Addresses for two cryptocurrency wallets collected millions of dollars in bitcoin, ethereum within just a few hours.

“Across the globe, demand for bitcoin continues to increase as the need for a decentralized, censorship-resistant store of value becomes more evident by the day,” added Klippsten.