The approval of spot bitcoin ETFs will be a key step forward but it’s unlikely that the bigger regulatory picture will be resolved any time soon in the United States, write Steve Scott and AJ Nary, of BitGo.

Konstantin Postumitenko/Prostock-studio – stock.adobe.com

Why? Another round of application rejections is likely given the continuedlack of clear market structure that led to the downfall of cryptocurrency exchange FTX earlier last year. In other words, the lack of separation of custody and trading will continue to serve as a stumbling block for approval until it is fully addressed. To change that trajectory, ETF applicants will likely need to demonstrate to the Securities and Exchange Commission that their assets will be custodied with one provider — ideally with a qualified custodian — and traded using a different entity.

So, moving beyond the hype into reality, we won’t see a bitcoin ETF approved until this market structure is reflected in the applications submitted to the SEC.

Whichever application is approved first will almost certainly help that firm to gain significant market share of the new product and its associated liquidity, which could total in the hundreds of billions of dollars. So, money managers have a clear and vested interest in getting the initial approval.

The SEC approved the first bitcoin futures ETF in October 2021, raising hopes for a rapid approval of the related investment vehicle — spot bitcoin ETFs — but a speedy approval didn’t take place. Since then, numerous money managers have applied for approval with two of the front-runners — BlackRock and Grayscale Investments — gaining large amounts of the news coverage.

In June 2023, BlackRock, the world’s largest money manager with $9T+ in assets under management, submitted an application that changed the trajectory by including a surveillance-sharing agreement with Nasdaq to address SEC concerns. Because of their experience with the ETF product and how they’ve only had one application rejected, people in the industry are watching to see if their approach works. Since this application was submitted, many other well-known investment management companies have since filed spot bitcoin ETF applications that follow BlackRock’s model.

Grayscale, the world’s largest crypto asset manager by assets under management, is also garnering plenty of attention in the news. After the SEC rejected an application from them for a spot bitcoin ETF because of price discovery issues — and after a court ruled in favor of Grayscale — the SEC has indicated that they will not challenge that court ruling.

Grayscale is taking an uplist approach as they continue to seek approval, which would involve moving their securities listings from an off-brand stock exchange to one in the mainstream: from the OTCQX to the NYSE. The advantage of this strategy: Grayscale gets its spot bitcoin ETF to market more quickly and could help them to gain the bulk of the initial liquidity flowing into the new market product.

Regardless of which asset management company gains first approval — which, whoever it is, will require the separation of custody and trading functions — a group of investment companies’ applications for spot bitcoin ETFs that satisfy this requirement could be approved in rapid succession or even all at once. Predicting how quickly this will occur is a purely speculatory exercise.

Approval for spot bitcoin ETFs will be an important step forward for crypto to become more enmeshed in the mainstream investment ecosystem and to validate crypto’s place within the broader financial system. ETFs are popular investment vehicles, more affordable than many other options and less complicated than ETF futures with levels of liquidity that many investors desire — and spot bitcoin ETFs can serve as a seamless and secure entry point for investors who are new to crypto and can create a new way to diversify portfolios. A spot bitcoin ETF will be a security, making it easy to buy and sell without the investor needing to hold the actual bitcoin.

Some investors will likely stick with this connection point to crypto while others will expand their digital asset investments. They may stretch their exposure through spot ethereum ETFs upon their approval along with other digital asset investment opportunities.

The approval of spot bitcoin ETFs will be a key step forward but it’s unlikely that the bigger regulatory picture will be resolved any time soon in the United States. Because bitcoin is the only digital asset considered a commodity at this time, a spot bitcoin ETF won’t likely pave a quick path to, say, an ETF basket of crypto assets. But it will be an ideal first step, giving advisors and investors a chance to make the transition into this new asset class — crypto in the form of bitcoin — in a familiar vehicle: ETFs.

These became popular following the financial crisis in 2008/2009 to entice investors to buy preferred shares despite low interest rates at that time. They generally “reset” every five years with the dividend rate for the next five years based on a premium over the 5-year Government of Canada bond rate at the time. Rate reset preferred shares currently represent 73% of the Canadian preferred share market.

2. Perpetual preferred shares

These represent 25% of the Canadian preferred share market. Perpetuals have no reset date. Their dividend rate is set when they are issued, and they continue in perpetuity.

3. Floating or variable rate preferred shares

These are like rate resets in that the rate changes, but those changes are more frequent—typically quarterly. The rate is generally based on a premium to the 3-month Government of Canada treasury bill rate. Together, floating/variable rate and convertible preferred shares represent less than 3% of the Canadian preferred share market.

4. Convertible preferred shares

A convertible security can be converted into another class of securities of the issuer. For example, a convertible preferred share may be convertible into common shares of the company that issued the shares.

Preferred shares Indexes for Canadian investors

The S&P/TSX Preferred Share Index is currently 57% financials, 20% energy and 12% utilities. Communication services, real estate, and consumer staples makes up the remainder of the market. The financials are tilted slightly more towards banks than insurance companies.

The current distribution yield of the S&P/TSX Preferred Share Index is about 6.1%. This is the dividend income an investor might anticipate over the coming year. The trailing 12-month yield is about 5.9%. These are attractive rates, Mario, but you can earn comparable rates in guaranteed investment certificates (GICs) with no risk or volatility. So, the high yields need to be put into perspective.

What to do with preferred shares at a loss

One consideration, Mario, is if you own your preferred shares in a taxable non-registered account, you could sell them to trigger a loss, if you have other investments that you have sold or intend to sell for a capital gain.

“Tax loss selling” is when you sell an investment for a loss to harvest the tax benefit of that loss. You can claim capital losses against capital gains in the current year. If you have a net capital loss for all investments sold in your taxable accounts in a given year, you can carry that loss back to offset capital gains income you paid tax on in the previous three years. Or you can carry the loss forward to use in the future against capital gains.

So, given that context, we’re pretty proud of how these predictions held up.

Inflation will continue to dominate the news

“People who are unemployed feel the unemployment rate: but everyone feels the inflation rate.

“Nothing gets people’s attention faster than paying higher prices for housing, gas and groceries. That’s what makes it such a tempting news story to keep reporting on. It also makes it almost impossible for politicians and policy makers to ignore.

“Until the inflation rate comes down, to at least 4% (it’s currently 6.8%), I don’t see most investment commentators talking about much else.”

OK, admittedly, I started with a layup. Given how important inflation and interest rates are to the pricing of assets in almost every market, it was a high-probability bet that this would dominate markets in 2023. That said, it’s undeniable that the rapid pace of interest-rate rises took up most of the oxygen in the room this year. Over the last few months inflation has been coming down to the 3% to 4% level. And, as predicted, we’re finally seeing some other stories emerge. This week, for example, the Bank of Canada (BoC) announced a headline inflation rate of 3.1% and it failed to lead the news anywhere I looked (despite being slightly higher than predicted).

The Russian invasion remains predictably unpredictable

“None of the experts I read about a year ago predicted Russia would invade its neighbours and send geopolitical shockwaves reaching every corner of the planet.

“None of the experts I read about 10 months ago predicted the Ukrainian military response would be able to stand up to the Russian war machine for more than a few days.

“At some point maybe it would be best to admit that the experts really have no idea where this conflict is headed. Despite the tragic loss of life and catastrophic disruption of society, it seems to me that there is little evidence that either side will back down as we enter 2023.

“If—and this appears the more likely situation—the war drags on or escalates, it becomes difficult to quantify the damage inflicted on economies, like Germany’s, which are so dependent on Russia’s energy.

“Sure, demand destruction and the Green Revolution are coming… eventually… and at substantial cost. Even scarier is the unpredictable nature of the response to food shortages in desperate countries around the world. Generally speaking, food riots aren’t good for business (or humanity).”

It’s not fun predicting that war will be awful. The tragedy taking place in Ukraine continues to be a struggle for all parties involved, and I don’t think we’re much closer to a long-term peace than we were at this time last year. The war has definitely contributed to high food costs around the world and continues to be quite disruptive within specific industries.

That said, much of Europe adapted to new energy supply chains more quickly than originally anticipated. A new market equilibrium appears to have been established, but there is no question that the war continues to be a worldwide drain on resources and, more importantly, an absolute tragedy.

The much-talked-about recession will continue to be talked about

“At this point, I feel like we might forecast a recession forever.

“Whether a recession will ever actually arrive or not is another story.

“With inflation in the U.S. falling to an annualized rate of 3.7% over the last three months, I’d argue we’re not only past peak inflation, but are actually well on our way to some sort of ‘new normal.’ With a substantial lag between when monetary policy is announced, and when its full effects are felt, we might not need a recession to lower inflation despite all of the headlines.

“Of course, I continue to refer to the fact that whether we see two quarters of -0.1%, and -0.1% GDP shrinkage, or a quarter of -0.3% growth followed by a quarter of 0.2% growth, the distinction of ‘recession or not’ is irrelevant. The first scenario is a technical recession by most definitions. The second scenario is just a bad quarter followed by a less bad quarter. Whether we have a recession or not really isn’t that important in the long term.

“Have the asset markets (such as stock or property markets) in which I’ve invested my money already anticipated the bad stuff coming by ‘pricing it in’?

“Almost assuredly.

“Remember that the stock market and the economy are not the same thing. Professional investors look past current events—they’re aware of the recency bias. They foresaw some rough waters ahead throughout 2022, but that doesn’t mean 2023 will also be so bleak.”

Given the gross domestic product (GDP) situation Canada announced two weeks ago, we’re comfortable saying we knocked this one out of the park. Considering how many experts were predicting a recession at the end of 2022 and calling for falling markets, the theory that markets had priced in a pretty rough ride was the correct one.

But 2023 has been different. Aside from a few prominent scandals, it’s been a year of resurgence and renewed investor interest. The price of bitcoin (BTC) has risen from about $16,500 at the start of the year to about $41,300, as of Dec. 18, 2023—an eye-popping gain of about 150%. But is crypto too volatile to invest in—especially if you’re a conservative investor? Is it worth exploring, or should you stay away from all the hype?

What are cryptocurrencies? A quick refresher for Canadian investors

Cryptocurrency is a form of digital money based on blockchain technology, which securely and permanently records transactions in a digital ledger. Unlike traditional fiat currency, crypto isn’t created, managed or backed by banks. Bitcoin, for example, operates on a multitude of computers around the world (called “nodes”) that run a specific algorithm. Together, they contribute massive amounts of computing power to create new coins, process transactions and maintain the decentralized ledger of these transactions.

In the past, Canadian crypto investors bought coins, or fractions of coins, via crypto exchanges. Today, you can invest in exchange-traded funds (ETFs) that hold bitcoin and ethereum, making crypto more accessible to a wide range of investors.

The potential benefits of investing in crypto

Many Canadian investors remain cautious about crypto, wary of the dizzying volatility of crypto prices. Nonetheless, crypto is quickly emerging as an asset class for some long-term investors, exemplified by Fidelity’s All-in-One ETFs—which blend a small yet potentially impactful allocation of 1% to 3% of cryptocurrency into diversified portfolios of stocks and bonds. Adding a sprinkling of crypto assets to your portfolio could have these advantages:

Diversification and hedging against traditional markets

Diversification has typically meant allocating your portfolio to a certain percentage of stocks and bonds. However, bonds have had a torrid couple of years, and high inflation rates are spooking stock markets. So, investors are seeking fresh ideas. Diversifying with crypto could be promising because—although volatile and risky in itself—crypto does not suffer from all the same systemic risks that some stocks and bonds do. However, investors need to consider other crypto risks, such as regulatory uncertainty and technology risks.

Potential for higher returns

In diversified portfolios, stocks have so far been the growth engine. But, with crypto offering higher historical returns over the past 10 years, even a small allocation of 1% to 3% to crypto can potentially enhance an ETF’s returns.

A slice of the future

A small allocation to crypto gives you a slice of (what could be) the future of money and investments. Nobody knows how big the crypto market will be in 10 years and what role crypto will play in the future. A Fidelity All-in-One ETF with a small 1% to 3% allocation to crypto allows you to participate in the (possible) future without managing or storing it yourself.

Pure crypto ETFs vs. all-in-one ETFs

Fidelity’s All-in-One ETFs allocate 1% to 3% to crypto. It’s a low percentage, but BTC has delivered annualized gains of over 50% over the last five years, so even a small allocation can give your investments a big boost. While many Canadian investors will be content with this 1% to 3% crypto allocation, some experienced investors may want to manage their crypto allocation themselves—with the ability to increase or decrease their crypto allocation independently. For these investors, there’s the Fidelity Advantage Bitcoin ETF, which invests substantially all of its holdings in bitcoin. In fact, Fidelity’s All-in-One ETFs gain exposure to BTC through this very ETF. Here’s an overview of Fidelity’s All-in-One ETFs that include crypto in their neutral asset allocation mix (as at Oct. 31, 2023).

Both types of investments are subject to tax in your taxable accounts, like non-registered or corporate accounts. Tax-free savings accounts (TFSAs) are tax-free, so you don’t receive tax slips for TFSA investments, nor do you report the income or capital gains on your tax return.

Does the ACB of TFSA investments matter?

You ask about calculating the adjusted cost base (ACB) in your TFSA. Knowing the ACB is necessary in taxable accounts, but not in your TFSA. The ACB determines whether you’re selling an investment for a capital gain or a capital loss. Your brokerage often calculates the ACB for you, representing your purchases of the investment, including reinvested dividends or other adjustments.

In this respect, ETFs are similar to mutual funds, Barbara. Typically, they are structured as trusts and come with T3 slips, though some are corporations that come with T5 slips.

When are T3 slips typically issued?

Mutual fund and ETF issuers have until March 31 to provide T3 slips to investors, which is one of the challenges of investing in these funds. With the March 31 deadline, some investors don’t receive their T3 slips until April. So, it may be tough to file your tax return in March, unless you’re open to the possibility of filing an adjustment to your tax return for any late T3 slips.

Mutual fund and ETF trusts generally flow through all of their income and capital gains to investors. This means that if the fund buys and sells underlying assets for a capital gain, that capital gain is reported by the investor and taxable to them. This can result in a capital gain even if the investor has not sold any of their units of the fund.

For a Canadian investor, Barbara, one key distinction between mutual funds and ETFs is that ETFs can be purchased on a foreign stock exchange. Mutual funds are domiciled in Canada and are in Canadian dollars. A Canadian investor can buy ETFs that trade in the U.S. in U.S. dollars. This introduces foreign-exchange calculations to the taxation of these investments in taxable accounts.

How U.S.-dollar ETFs are taxed in Canada

When you sell a U.S.-dollar ETF, you need to report the sale in Canadian dollars based on the prevailing exchange rate at that time. You also need to calculate your cost in Canadian dollars based on the exchange rate—or rates—at the time of purchase. This can make for a little more work, especially if your ETF distributions are being reinvested.

While saving for retirement is a top priority for half of employed Canadians, many of us (44%) did not actually set aside money for it in the past year, according to the Canadian Retirement Survey from the Healthcare of Ontario Pension Plan (HOOPP). And, nearly half of Canadians (47%) haven’t made or are not planning to make any contributions to their retirement investments, either, a TD retirement survey says.

Younger Canadians especially struggle with this dilemma. Despite nearly 70% of Canadians under 35 worrying about the cost of living, whether their income will keep up with inflation (67%) and housing affordability (65%), we still place a high value on saving for retirement. The HOOPP survey found that half of Canadians (51%) under 35 would give up a higher salary to get a better pension.

How much does the average young Canadian have saved for retirement?

If you’re wondering how your savings stack up, as of 2019, the average Canadian under 35 had $9,905 in RRSPs, locked-in retirement accounts (LIRAs) and other retirement savings plans combined, and $8,395 in tax-free savings accounts (TFSAs), according to Statistics Canada.

It’s important to know the difference between “saving” for retirement and “investing” for retirement. If you simply deposit money into an interest-paying registered account like a TFSA or an RRSP, it will typically earn about 3% to 4% interest. But you can also hold investments in these accounts, if you set them up that way. Investments can increase in value over time, whereas with a savings account, you can benefit from compound interest. A key caveat here is the risk/return trade-off: stocks have higher potential returns, but also higher risk compared to, say, a bond or a guaranteed investment certificate (GIC). So, it’s important to understand your risk tolerance before you start investing.

If you’re just getting started, or your savings are less than the average above, you can still make a plan and catch up. To help you, and myself, I spoke to a few money experts about the best ways to save for retirement in Canada during challenging economic times.

Ask yourself: How much am I able to save for retirement?

If you’re paying off student loan debt or working in your first job after graduation, you might wonder whether it’s worth it to start building your retirement savings while you’re still getting your financial footing.

Seun Adeyemi, Certified Financial Planner at True Wealth Advisors in Toronto, says that you should start saving for retirement as soon as possible—preferably, as soon as you have an income. “That makes the journey to retirement a lot easier, because your money has more time to grow,” he says. He does recommend, though, to prioritize paying off any debt besides mortgage debt first—especially if you have high-interest debt like credit cards.

“On credit cards, you’re paying 19% to 24% [interest] on your debt, and even if you have an amazing [investment] portfolio that’s generating 10% to 15% returns, you’re still underwater because you’re paying a higher interest on your credit card,” Adeyemi says. People can usually save for retirement while managing mortgage debt, he says, as long as they are on top of their payments and don’t get further into debt.

BlackRock revises spot Bitcoin ETF to enable easier access for banks

BlackRock has revised its spot Bitcoin exchange-traded fund (ETF) application to make it easier for Wall Street banks to participate by creating new shares in the fund with cash rather than just crypto. The new in-kind redemption “prepay” model will allow banking giants such as JPMorgan or Goldman Sachs to act as authorized participants for the fund, letting them circumvent restrictions that prevent them from holding Bitcoin or crypto directly on their balance sheets.

El Salvador expects to sell out Bitcoin ‘Freedom Visa’ by end of year

El Salvador’s National Bitcoin Office says its $1 million Freedom Visa program has already received hundreds of inquiries since its launch on Dec. 7 and expects it to sell out before the end of 2023. Launched by the local government in partnership with stablecoin issuer Tether, the Freedom Visa is a citizenship-by-donation program that grants a residency visa and pathway to citizenship for 1,000 people willing to make a $1 million Bitcoin or Tether donation to the country. The program is limited to 1,000 slots per calendar year.

Sam Bankman-Fried’s lawyer says FTX fraud trial was “almost impossible” to win: Report

The lawyer responsible for Sam “SBF” Bankman-Fried’s criminal trial defense has admitted that the case was “almost impossible” to win from the outset. During an interview, Stanford Law School professor David Mills said he recommended the legal defense of SBF admit to the allegations of witnesses and state prosecution and convince the jury that Bankman-Fried intended to save the company. Mills also disclosed that he had agreed to lend his expertise to Bankman-Fried’s defense at the behest of the FTX CEO’s parents, and described Bankman-Fried “as the worst person I’ve ever seen do a cross-examination.”

Yearn.finance pleads arb traders to return funds after $1.4M multisig mishap

Yearn.finance is hoping arbitrage traders will return $1.4 million in funds after a multisignature scripting error resulted in a large amount of the protocol’s treasury being drained. The error occurred while Yearn was converting its yVault LP-yCurve — earned from performance fees on vault harvests — into stablecoins on the decentralized exchange CoW Swap. Yearn suffered significant slippage when it received 779,958 DAI yVault tokens from the trade, resulting in a 63% drop in the liquidity pool value.

SEC pushes deadline for decision on Invesco Galaxy spot Ethereum ETF to 2024

The United States Securities and Exchange Commission has delayed its decision on whether to approve or reject a spot Ether ETF proposed by Invesco and Galaxy Digital. The companies filed the spot ETH ETF application in September. The proposed spot crypto investment vehicle is one of many being considered by the commission, which, to date, has never approved an ETF with direct exposure to Ether, Bitcoin or other cryptocurrencies.

Winners and Losers

At the end of the week, Bitcoin (BTC) is at $42,222, Ether (ETH) at $2,250 and XRP at $0.62. The total market cap is at $1.6 trillion, according to CoinMarketCap.

Among the biggest 100 cryptocurrencies, the top three altcoin gainers of the week are Bonk (BONK) at 131.38%, WOO Network (WOO) at 78.34% and Helium (HNT) at 77.66%.

The top three altcoin losers of the week are Terra Classic (LUNC) at -15.84%, Sei (SEI) at -14.48% and Pepe (PEPE) at -12.10%.

‘No excuse’ not to long crypto: Arthur Hayes repeats $1M BTC price bet

Bitcoin and altcoins are a no-brainer bet in the current macro climate, Arthur Hayes says. In a post on X (formerly Twitter) on Dec. 14, the former CEO of exchange BitMEX said that investors have “no excuse” to short crypto.

Going long on crypto is the key to success as markets bet on the United States Federal Reserve lowering interest rates next year, Hayes argues. “At this point, there is no excuse not to be long crypto,” part of his post stated.

“How many more times must they tell you that the fiat in your pocket is a filthy piece of trash,” he wrote. Hayes further reiterated a longstanding $1 million BTC price prediction as a result of macro tides eroding the value of national currencies.

FUD of the Week

Ledger patches vulnerability after multiple DApps using connector library were compromised

The front end of multiple decentralized applications using Ledger’s connector were compromised on Dec. 14. Ledger announced that it had fixed the problem three hours after the initial reports about the attack. Protocols affected include Zapper, SushiSwap, Phantom, Balancer and Revoke.cash, stealing at least $484,000 in digital assets. The attacker utilized a phishing exploit to gain access to the computer of a former Ledger employee. The hack sparked criticism about Ledger’s security approach.

Bitcoin inscriptions added to US National Vulnerability Database

The National Vulnerability Database flagged Bitcoin’s inscriptions as a cybersecurity risk on Dec. 9, calling attention to the security flaw that enabled the development of the Ordinals Protocol in 2022. According to the database records, a datacarrier limit can be bypassed by masking data as code in some Bitcoin Core and Bitcoin Knots versions. As one of its potential impacts, the vulnerability could result in large amounts of non-transactional data spamming the blockchain, potentially increasing network size and adversely affecting performance and fees.

SafeMoon falls 31% in five hours after filing for Chapter 7 bankruptcy

The token of decentralized finance protocol SafeMoon has fallen 31% in five hours after the company behind it filed for bankruptcy. SafeMoon officially applied for Chapter 7 bankruptcy, also known as “liquidation bankruptcy,” on Dec. 14. The latest blow comes only a month after the U.S. Securities and Exchange Commission charged SafeMoon and its executives with violating securities laws in what the regulator described as “a massive fraudulent scheme.” Several former SafeMoon supporters expressed frustration on Reddit regarding the bankruptcy, alleging they were rug-pulled by the SafeMoon developers.

ETFs may have lower management fees than comparable mutual funds. And, with such a wide variety of ETFs with different asset allocations to choose from—including funds that combine equities with fixed income and even cryptocurrency—there are ETFs for a range of investors, from conservative to aggressive. You can choose ETFs that try to replicate an entire stock index, such as the S&P 500, or focus on a specific sector or geographical region. Most ETFs are passively managed, but a growing number of funds are actively managed.

In Canada, Fidelity Investments offers a variety of ETFs for investors with different investment objectives, time horizons and tolerance for risk. Investors can consider ETFs in the following categories:

Equity ETFs invest in stocks across a broad range of sectors, market capitalizations and geographies.

Fixed income ETFs invest in bonds and can be used to generate income, with the potential for capital preservation.

Balanced or multi-asset ETFs invest across asset classes, including stocks and bonds.

A sustainable ETF that invests in companies with favourable environmental, social and governance characteristics.

Digital asset ETFs have direct exposure to cryptocurrency, such as bitcoin and ether.

On this page, we’ll share articles to help you learn about and evaluate ETFs for your investment portfolio. Check back often for more insights.

How many ETFs can Canadian investors own? ETFs offer Canadian investors an appealing combination of convenience, diversification and low fees. But how many ETFs should you own, and which ones?

What investments can I put in my TFSA? The TFSA contribution limit for 2024 was recently announced. TFSAs can hold more than just cash. Get to know your TFSA investment options, including some Fidelity All-in-One ETFs that offer portfolio diversification.

This is a paid post that is informative but also may feature a client’s product or service. These posts are written, edited and produced by MoneySense with assigned freelancers and approved by the client.

Commissions, trailing commissions, management fees, brokerage fees and expenses may be associated with investments in mutual funds and ETFs. Please read the mutual funds or ETF’s prospectus, which contains detailed investment information, before investing. Mutual funds and ETFs are not guaranteed. Their values change frequently, and investors may experience a gain or a loss. Past performance may not be repeated.

The statements contained herein are based on information believed to be reliable and are provided for information purposes only. Where such information is based in whole or in part on information provided by third parties, we cannot guarantee that it is accurate, complete or current at all times. It does not provide investment, tax or legal advice, and is not an offer or solicitation to buy. Graphs and charts are used for illustrative purposes only and do not reflect future values or returns on investment of any fund or portfolio. Particular investment strategies should be evaluated according to an investor’s investment objectives and tolerance for risk. Fidelity Investments Canada ULC and its affiliates and related entities are not liable for any errors or omissions in the information or for any loss or damage suffered.

Jaclyn Law is MoneySense’s managing editor. She has worked in Canadian media for over 20 years, including editor roles at Chatelaine and Abilities and freelancing for The Globe and Mail, Report on Business, Profit, Reader’s Digest and more. She completed the Canadian Securities Course in 2022.

Binance founder CZ must stay in US until sentencing, judge orders

Binance founder Changpeng “CZ” Zhao has been ordered to stay in the United States until his sentencing in February, with a federal judge determining there’s too much of a flight risk if the former crypto exchange CEO is allowed to return to the United Arab Emirates. On Dec. 7, Seattle District Court Judge Richard Jones ordered Zhao to stay in the U.S. until his Feb. 23, 2024 sentencing date. He faces up to 18 months in prison after pleading guilty to money laundering on Nov. 21 and has agreed not to appeal any potential sentence up to that length.

House committee passes bill to ‘preserve US leadership’ in blockchain

A United States Congress committee has unanimously passed a pro-blockchain bill, which would task the U.S. commerce secretary with promoting blockchain deployment and thus potentially increase the country’s use of blockchain technology. The act covers an array of actions the commerce secretary must take if passed, including making best practices, policies and recommendations for the public and private sector when using blockchain tech. The bill will now go to the House for a vote. If passed, it must also pass in the Senate before returning for final congressional and presidential approval.

SEC pushes deadline to decide on Grayscale spot Ether ETF

The United States Securities and Exchange Commission has delayed its decision on whether to approve or reject a spot Ether exchange-traded fund (ETF) offering from asset manager Grayscale. In a notice, the SEC said it would designate a longer period for considering a proposed rule change that would allow NYSE Arca to list and trade shares of the Grayscale Ethereum Trust. Grayscale first filed with the SEC to convert shares of its Grayscale Ethereum Trust into a spot Ether ETF in October, adding its name to the list of companies awaiting a decision from the regulator.

Elon Musk’s xAI files with SEC for private sale of $1B in unregistered securities

Elon Musk’s X-linked artificial intelligence modeler, xAI, has an agreement for the private sale of $865.3 million in unregistered equity securities, according to a filing with the United States Securities and Exchange Commission made on Dec. 5. The company is seeking to raise $1 billion. XAI’s product, a chatbot called Grok, has recently rolled out to X’s Premium+ subscribers. Musk announced the launch of xAI in July and claimed its goal was to “understand the universe.”

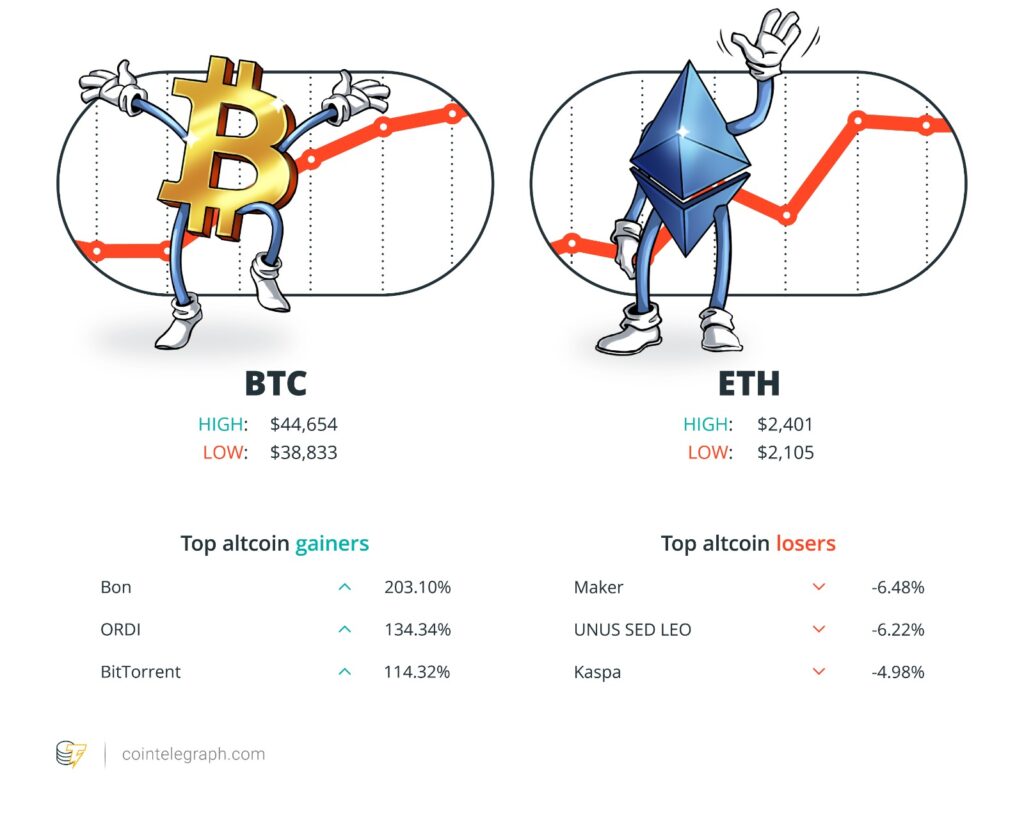

Bitcoin new high set for late 2024, Binance to lose top spot — VanEck

Bitcoin will hit a new all-time high in late 2024 because of a long-feared United States recession and regulatory shifts after the next U.S. presidential election, asset manager VanEck predicts. The firm is confident that the first spot Bitcoin ETFs will be approved in the first quarter of 2024. However, it also made a gloomy prediction for the general U.S. economy. VanEck is among several firms, including BlackRock and Fidelity, that are vying for an approved spot Bitcoin ETF. VanEck also believes that the BTC halving, due in April or May, “will see minimal market disruption,” but there will be a post-halving price rise.

Winners and Losers

At the end of the week, Bitcoin (BTC) is at $44,402, Ether (ETH) at $2,364 and XRP at $0.66. The total market cap is at $1.65 trillion, according to CoinMarketCap.

Among the biggest 100 cryptocurrencies, the top three altcoin gainers of the week are Bonk (BONK) at 203.10%, ORDI (ORDI) at 134.34% and BitTorrent (BTT) at 114.32%.

The top three altcoin losers of the week are Maker (MKR) at -6.48%, UNUS SED LEO (LEO) at -6.22% and Kaspa (KAS) at 4.98%.

“It takes a community and the whole industry to figure out how to better educate people. That’s the hard part. It’s not a technology issue; it’s an operational problem.”

In a post on X (formerly Twitter) on Dec. 7, entrepreneur Alistair Milne noted that should current performance continue, Bitcoin will witness a crossover of two weekly moving averages (MAs), which have never delivered such a bull signal before.

The 50-week and 200-week MAs are key trendlines for Bitcoin traders and analysts alike. The latter is the ultimate bear market support level, and it has so far never decreased in value.

BTC price strength is on the way to taking the 50-week MA trendline above the 200-week counterpart. Known as a “golden cross,” on lower timeframes, this is considered a classic bullish signal, and for Milne, the impetus is that considerable upside could be in store should the phenomenon play out.

“The 50-week moving average will now soon cross back above the 200-week MA making a ‘golden cross’ for the 1st time. QED: Early bull market,” he wrote.

FUD of the Week

Crypto is for criminals? JPMorgan has been fined $39B and has its own token

JPMorgan Chase CEO Jamie Dimon is being criticized by the crypto community after claiming Bitcoin and cryptocurrency’s “only true use case” is to facilitate crime. However, according to Good Jobs First’s violation tracker, JPMorgan is the second-largest penalized bank, having paid $39.3 billion in fines across 272 violations since 2000. About $38 billion of these fines came under Dimon’s watch, who has been CEO since 2005.

British regulator adds Justin Sun-linked Poloniex to warning list after $100M hack

The United Kingdom’s Financial Conduct Authority (FCA) has added crypto exchange Poloniex to its warning list of non-authorized companies. The Seychelles-based exchange is one of the three companies owned by or affiliated with entrepreneur Justin Sun that have suffered four hacks in the last two months. The warning to Poloniex was published on the FCA’s website on Dec. 6. It doesn’t offer a reason but says that “firms and individuals cannot promote financial services in the UK without the necessary authorization or approval.”

US senators target crypto in bill enforcing sanctions on terrorist groups

A bipartisan group of lawmakers in the United States Senate introduced legislation aimed at countering cryptocurrency’s role in financing terrorism, explicitly citing the Oct. 7 attack by Hamas on Israel. The bill would expand U.S. sanctions to include parties funding terrorist organizations with cryptocurrency or fiat. According to Senator Mitt Romney, the legislation would allow the U.S. Treasury Department to go after “emerging threats involving digital assets.”

Lawmakers’ fear and doubt drives proposed crypto regulations in US

If the Digital Asset Anti-Money Laundering Act were to become law, many cryptocurrency providers would have to learn how to comply with the same regulations as traditional financial institutions.

Expect ‘records broken’ by Bitcoin ETF: Brett Harrison (ex-FTX US), X Hall of Flame

For Canadian investors who have achieved significant taxable capital gains, now is the time to implement a tax-loss selling strategy—the most effective way to find tax savings.

What is tax-loss selling in Canada?

Tax-loss selling is an investing strategy designed to offset taxable capital gains and reduce your tax bill. It involves selling investments to trigger a capital loss and claiming them against capital gains.

Definition of tax-loss harvesting

Tax-loss harvesting, or tax-loss selling, is a strategy for reducing tax in non-registered accounts. Investors sell money-losing investments, triggering capital losses they can use to offset capital gains incurred the same year. Tax losses can also be carried back three years or carried forward indefinitely. When using this strategy to save on taxes, take care to avoid triggering the superficial loss rule.

In Canada, when you sell appreciable assets such as stocks, bonds, precious metals, real estate, or other property for more than the purchase price of the investment plus any acquisition costs—a.k.a. the adjusted cost base (ACB)—this is called a capital gain.

The math is pretty straightforward. If you bought a stock for $100 and sold it for $200, the capital gain is $100. The Canada Revenue Agency (CRA) requires you to report the capital gain as income on your tax return for the year the asset was sold. And, 50% of its value is considered taxable, based on the rate of your income tax bracket.

On the flip side, when you sell an investment for less than its ACB, this is considered a capital loss. The CRA allows Canadian taxpayers to use capital losses to offset any capital gains.

Unlike capital gains, capital losses can be reported on your tax return in any of the three years prior to the loss or to offset future capital gains. Capital losses have no expiration date.

As an investment advisor in Canada, I track my clients’ portfolios throughout the year to have a clear view of their capital gains’ position and opportunities to minimize tax. That’s when tax-loss selling comes into play.

The S&P 500 (index of the 500 largest U.S. stocks) was up over 8%. That’s significantly better than its November average of 1.54% going back to 1950. November is historically the best month in the U.S. stock market.

The Toronto Stock Exchange’s S&P/TSX composite index was up 7.2% in November. There are only five single months since 2002 when there was a higher return: November 2020, April 2020, January 2019, May 2009, March 2009. By the way, January 2023 was pretty great too at 7.13%.

Stock markets across the globe also did pretty well in November, with an all-world index up 9%.

Remember, the stock market goes up most of the time.

It pays to be an optimist!

Forget “girl math,” here’s “old man math”

One of the most popular personal finance gurus of all time is Dave Ramsey. He’s incredible at promotion, and he’s written more books than the number of times a Canadian NHL team has ever won the Stanley Cup. Ramsey hosts radio shows, appears constantly on network TV, and is generally a one-man financial content machine.

But, does any of this mean that Ramsey actually gives good advice?

I’m sure there is someone somewhere who Ramsey has helped. But the number of times he makes absolutely outlandish, nonsensical claims is incredible. Thanks to Dollars and Data for the assist, here’s his latest take, which is an unedited quote from Ramsey’s show.

The Office of the Superintendent of Financial Institutions (OSFI) issued a ruling on Oct. 31, 2023, that requires banks taking deposits from ETF issuers to have 100% of the capital needed to support those deposits in case they get rapidly withdrawn.

The most popular HISA ETFs

The reason for HISA ETFs’ popularity with investors is not hard to see. After a couple of the worst years ever for fixed income, they present a place to park your money with essentially zero volatility, combined with yields tracking ever-higher interest rates (now more than 5%). Not only do these funds find some of the best deals in savings accounts for you, but you can also buy and sell them on a whim.

As of Oct. 31, the CI High Interest Savings ETF (CSAV) ranked as the fourth largest ETF in Canada, with $8.7 billion in assets under management, CEFTA figures show. And HISA ETFs’ appeal seems undiminished, even as fixed income reasserts its position in investors’ portfolios with interest rates expected to top out soon, if they haven’t done so already. Over the month of October, the Horizons High Interest Savings ETF (CASH) and CSAV were the number two and number three ETFs in Canada, respectively, in net inflows.

Are HISA ETFs safe?

The sudden shift of capital into HISA ETFs caught the attention of the OSFI, which oversees banks operating across the country. The regulator was concerned about the potential for instability in the banking system should investors withdraw their money as fast as, or faster than, they deposited it, as the ETF format enables them to do. The OSFI undertook a public consultation process last spring, considering “systemic concerns with contagion, potential for regulatory arbitrage, and the absence of guarantees or deposit insurance typically found with traditional savings accounts,” it said in its ruling on Hallowe’en.

When new regulations around HISA ETFs take effect

The OSFI ruled that, as of Jan. 31, 2024, “any deposit-taking institutions exposed to such funding must hold sufficient high-quality, liquid assets, such as government bonds, to support all HISA ETF balances that can be withdrawn within 30 days.”

What it means for Canadian investors

While the decision is directed at the banks offering HISAs, it will have indirect effects on the ETFs holding these savings accounts. Some Canadian investors have expressed concern that the new rules might restrict the number of banks taking deposits from fund companies and might constrain yields as a result.

An analysis by TD Securities suggested yields would drop around half a percentage point come January. However, Naseem Husain, senior vice president and ETF strategist at Horizons ETFs, emphasizes the upside of regulatory clarity.

“At the end of the day, the OSFI decision regulates and confirms the ongoing viability of HISA ETFs, ensuring they’re here to stay and will continue to be a viable investment option,” says Husain. “This decision will likely lead to greater competition in the space from a product perspective, and that could incentivize more investors to consider using HISA ETFs in their portfolios.”

Ideally, your grandchild or grandchildren will have an RESP. Perhaps your own kids have already opened one for them. If not, you can open an RESP—in fact, anyone can become a “subscriber,” including parents, guardians, grandparents, other relatives, and friends. A child can be the “beneficiary” of multiple RESPs, but here’s the key detail to note: the lifetime RESP contribution limit per child is $50,000. Any excess contributions will be taxed, so it’s important for contributors to coordinate their efforts.

An overview of RESPs

If you’re new to RESPs, here are some common questions (and the answers) about these plans:

What is an RESP? RESPs are registered savings and/or investment accounts, meaning they’re registered with the Canadian government and they offer tax advantages.

What can RESPs be used for? Your grandchild(ren) will be able to use their RESP to pay for tuition plus a wide range of other educational expenses: accommodations, textbooks, school supplies, transportation, and more.

Where can I open an RESP? At a bank or an investment firm, including providers that specialize in RESPs, like Embark. You will need your grandchild’s social insurance number (SIN)—another good reason to coordinate with their parents.

Are RESPs taxed? Money and investments held inside an RESP grow tax-sheltered. The grants and growth—including interest, dividends and capital gains—aren’t taxed until withdrawn, and then they’re taxed at the beneficiary’s (child’s) marginal tax rate. (This will likely be very low since they’re in school.)

Do I get a tax deduction for contributing to an RESP? No. But you also don’t pay tax when you withdraw the money you contributed.

Why else should I open an RESP? The biggest incentive for opening an RESP is free government grants. Through the Canada Education Savings Grant (CESG), the Canadian government will match 20% of your contributions, up to $500, in a given year, up to a lifetime limit of $7,200. In addition to the CESG, families below a certain income threshold may also qualify for additional government grants, called the Additional Canada Education Saving Grant (ACES) and the Canada Learning Bond (CLB). The CLB grant does not require plan subscribers to make any contributions. Families living in certain provinces (Quebec and British Columbia) can also apply for other grants. Read more about government RESP grants.

What if I have multiple grandchildren? You or the children’s parents can open a family RESP. Keep in mind that all children within the RESP must be related by blood or adoption (siblings). This means that as a grandparent, if you have multiple grandchildren (who are not all siblings), each group will need their own RESP. The grants and growth in a family RESP can be shared among beneficiaries—very helpful if one child’s education costs more than another’s.

How long can an RESP stay open? A very long time: 35 years. But it’s important to pay attention to the annual RESP deadline of Dec. 31, if you want to maximize government grants.

What’s the best way to get the maximum RESP grant?

To get the maximum CESG amount of $7,200, it’s a good idea to plan for RESP contributions. This is helpful both for organizing your own finances and for coordinating between contributors, including your grandchildren’s parents. You could even automate your contributions, to make it easier to stick to a consistent schedule.

First, let’s look at how to get the maximum of $500 in CESG in a given year. The government matches 20% on the first $2,500 annually, so a child’s RESP contributors would need to put in $2,500 to get $500 in CESG each year. Collectively, you can contribute more than $2,500 in any year—there’s no limit to annual RESP contributions (not exceeding the $50,000 lifetime limit)—but the maximum CESG per year is $500.

To get the maximum lifetime CESG amount of $7,200 for the child, the RESP contributors will need to put in $2,500 per year for 14 years, and then another $1,000 when the child is age 15. If you don’t contribute $2,500 in a certain year, you can catch up the following year, but note that the maximum CESG in one year is $1,000—meaning you can only catch up one year at a time.

Call in the experts

If you need guidance on planning RESP contributions, maximizing government grants and adjusting RESP investments over time, talk to the Education Savings Specialist at Embark. Right now, Embark has a special offer for MoneySense readers: Start an account using the promo code MONEYSENSE100 and it will contribute $100 to your grandchild’s education when you save $200. Visit Embark* for details.

This is a paid post that is informative but also may feature a client’s product or service. These posts are written, edited and produced by MoneySense with assigned freelancers and approved by the client.

What does the * mean?

If a link has an asterisk (*) at the end of it, that means it’s an affiliate link and can sometimes result in a payment to MoneySense (owned by Ratehub Inc.) which helps our website stay free to our users. It’s important to note that our editorial content will never be impacted by these links. We are committed to looking at all available products in the market, and where a product ranks in our article or whether or not it’s included in the first place is never driven by compensation. For more details read our MoneySense Monetization policy.

Andrew Lo is the CEO of Embark, Canada’s education savings and planning company. As a fintech leader for over 30 years, he’s focused on making the best financial services available to Canadians.

In the past few years, several economists argued about whether the definition of recession should be that simple. Now, there’s also the term “technical recession” to describe two consecutive quarters of a contracting GDP, while reserving the generalized term “recession” for a vague set of parameters that include unemployment and whatever else they want to include.

Three months ago, Statistics Canada told us that our GDP had contracted 0.2% from April to June.

On Thursday, Statistics Canada said our GDP had contracted 0.3% from July to September.

So, obviously we’re in a recession, or at least we’re in a technical recession, right?!

Nope.

In its Q3 announcement, Statistics Canada revised its second-quarter GDP measure. To me, it says: “Yeah, so we had another look at the numbers, and, uh, it turns out instead of a slight contraction of GDP, we actually had a very small growth in GDP. So, if you look at the six months from April to September, there was a very small overall shrinkage in Canada’s GDP, we’re not in a ‘technical recession’.”

The much bigger story here could be that Canada’s large immigration numbers are creating an overall GDP number irrelevant to the average Canadian. After all, most people want economic reporting to explain if their own personal situation is likely to get better or worse.

That’s not to say that increased immigration is a problem or that it has a negative economic effect. I personally feel quite the opposite.

It’s simply a question of how to explain math to Canadians. Whether Canada’s economy grows by 0.2% or shrinks by 0.2% from quarter to quarter is much less important than the fact we’re increasing population by 2.7% per year, and getting nowhere near the level of GDP growth. If our collective economic pie is staying essentially the same size (or perhaps growing very slowly), but we’re cutting it into more and more pieces at an increasing rate, then the most relevant statistic isn’t GDP. Rather it’s the real GDP per capita.

US officials announce $4.3B settlement with Binance, plea deal with CZ

Binance and its co-founder, Changpeng “CZ” Zhao, have reached a settlement over criminal and civil cases with the United States Department of Justice. CZ will plead guilty to one felony charge as part of the negotiated agreement. Attorney General Merrick Garland announced the settlement, claiming Binance’s policies allowed criminals involved in illicit activities to move “stolen funds” through the exchange. As part of the settlement, CZ announced on X (formerly Twitter) that he had stepped down as CEO and that Binance’s global head of regional markets, Richard Teng, will assume the position. He added he was “proud to point out” that U.S. officials didn’t allege that Binance misappropriated funds or manipulated markets. CZ was released on bail and is battling government efforts to bar his return to the United Arab Emirates to be with his family. His sentencing is scheduled for February.

BlackRock met with SEC officials to discuss spot Bitcoin ETF

Representatives from BlackRock and Nasdaq met with the U.S. Securities and Exchange Commission (SEC) to discuss the proposed rule allowing the listing of a spot Bitcoin exchange-traded fund (ETF). BlackRock provided a presentation detailing how the firm could use an in-kind or in-cash redemption model for its iShares Bitcoin Trust. Many reports have suggested the SEC could be nearing a decision on a spot BTC ETF for listing on U.S. markets. SEC officials also met with Grayscale representatives this week to discuss the listing of a Bitcoin ETF. BlackRock is one of many firms with spot crypto ETF applications in the SEC pipeline awaiting a response, including Fidelity, WisdomTree, Invesco Galaxy, Valkyrie, VanEck and Bitwise.

Bitcoin user pays $3.1M transaction fee for 139 BTC transfer

A Bitcoin user paid $3.1 million in fees for transferring 139.42 BTC. The transaction fee is the eighth-highest in Bitcoin’s 14-year history. A wallet address tried transferring 139.42 BTC only to pay more than half the actual value of the transaction fee. The destination address received only 55.77 BTC. The mining pool Antpool captured the absurdly high mining fee on block 818087. This is the largest Bitcoin transaction fee ever paid in dollar terms, knocking off Paxos’s September transfer of $500,000.

SEC sues Kraken alleging it’s an unregistered exchange, mixes user funds

The U.S. Securities and Exchange Commission has sued Kraken, alleging it commingled customer funds and failed to register with the regulator as a securities exchange, broker, dealer and clearing agency. Additionally, the SEC alleged Kraken’s business practices and “deficient” internal controls saw the exchange commingle up to $33 billion worth of customer assets with its own. The SEC said this resulted in a “significant risk of loss” for its clients. In a follow-up blog post, Kraken said the SEC’s commingling accusations were “no more than Kraken spending fees it has already earned,” and the regulator doesn’t allege any user funds are missing.

Appeals court rejects Sam Bankman-Fried’s bid for release

Sam Bankman-Fried will stay jailed after failing to convince a United States appellate court that he should be freed while his legal team appeals his conviction. Government prosecutors accused Bankman-Fried of leaking Caroline Ellison’s journals to The New York Times in July, which caused his bail to be revoked by a New York District Court. Bankman-Fried was found guilty of seven fraud and money laundering-related charges on Nov. 2. The former FTX CEO will remain behind bars while he awaits his sentencing on March 28 next year.

Winners and Losers

At the end of the week, Bitcoin (BTC) is at $37,710, Ether (ETH) is at $2,079, and XRP is at $0.62. The total market cap is at $1.43 trillion, according to CoinMarketCap.

Among the biggest 100 cryptocurrencies, the top three altcoin gainers of the week are Blur (BLUR) at 99.25%, FTX Token (FTT) at 39.05% and KuCoin Token (KCS) at 24.82%.

The top three altcoin losers of the week are Celestia (TIA) at -19.89%, ORDI (ORDI) at -17.63% and THORChain (RUNE) at -15.53%.

“We, the employees of OpenAI, have developed the best models and pushed the field to new frontiers, [but] the process through which you terminated Sam Altman […] has jeopardized all of this work and undermined our mission and company.”

‘Enjoy sub-$40K Bitcoin’ — PlanB stresses $100K average BTC price from 2024

Bitcoin buyers should enjoy the chance to add to their stack below $40,000, according to PlanB, pseudonymous creator of the stock-to-flow family of BTC price models. He believes Bitcoin will rise much higher than its recent 18-month highs.

Bitcoin bear market bottoms are characterized by the spot price dipping below the realized price, while bull markets begin once the spot crosses the two-year and five-month realized price levels. BTC/USD is now once again above all three realized price iterations.

“Enjoy sub-$40k bitcoin … while it lasts,” PlanB commented on an accompanying chart.

Asked whether the market should expect lower levels from here, PlanB would not be drawn, saying that he simply expected an average BTC price of at least $100,000 between 2024 and 2028 — Bitcoin’s next halving cycle.

FUD of the Week

HTX to restore services ‘within 24 hours’ after $30M hack

Crypto exchange HTX, formerly known as Huobi Global, resumed deposits and withdrawals within 24 hours after suffering a $30 million exploit on Nov. 22. The exploit was reported to be $13.6 million around the time of the incident, but has since increased in value. HTX’s hot wallets were compromised alongside a coordinated $86.6 million attack against the HTX Eco (HECO) Chain bridge, consisting of HTX, Tron and BitTorrent. The company has promised to fully compensate users for any losses incurred as a consequence of the hack.

CZ an ‘unacceptable risk of flight,’ should stay in US: DOJ

United States prosecutors are trying to stop former Binance boss Changpeng “CZ” Zhao from leaving the country, expressing concern about his potential flight risk. The government requested a review and overturn of a judge’s decision that would allow Zhao to return to his home in the United Arab Emirates (UAE) on a $175 million bond under the condition that he returns to the U.S. two weeks before his February 2024 sentencing. In a proposed order, prosecutors wrote that Zhao “presents an unacceptable risk of flight,” arguing that his ties and favored status in the UAE, along with the country’s lack of an extradition treaty with the U.S., are reasons to block him from leaving the country.

KyberSwap hacker offers $4.6M bounty for return of $46M loot

The decentralized exchange KyberSwap has offered a 10% bounty reward to the hacker who stole $46 million on Nov. 22 and left a note of negotiation. The exchange wants 90% of the loot returned. The hacker made away with roughly $20 million in Wrapped Ether, $7 million in wrapped Lido-staked Ether and $4 million in Arbitrum tokens. The hacker then siphoned the loot across multiple chains, including Arbitrum, Optimism, Ethereum, Polygon and Base.

This is your brain on crypto: Substance abuse grows among crypto traders

According to some addiction experts, the high-stress atmosphere of cryptocurrency trading can provide a perfect environment for substance abuse.

Michael Saylor’s a fan, but Frisby says bull run needs a new guru: X Hall of Flame

Bitcoin enthusiast Dominic Frisby has a wild journey, from penning one of the first-ever Bitcoin books to plastering “Bitcoin fixes this” on the Bank of England.

6 Questions for Alex O’Donnell about financial journalism and the future of DeFi

In a report full of positive figures, perhaps the most impressive highlight was that data centre revenue (mostly from cloud infrastructure providers like Amazon and Microsoft) was up 279%, to USD$14.51 billion. Only a few years ago, Nvidia was basically known as a fairly simple (albeit still profitable) company that made computer chips for video games. As long as it maintained its competitive advantage on AI chips, it essentially has license to print ever-increasing amounts of money. We’ll see how long it takes the other chip heavyweights to catch up.

The fly in the ointment of Nvidia’s earnings report, though, was a warning that export restrictions from China and other countries were going to have a negative effect on the fourth quarter’s bottom line.

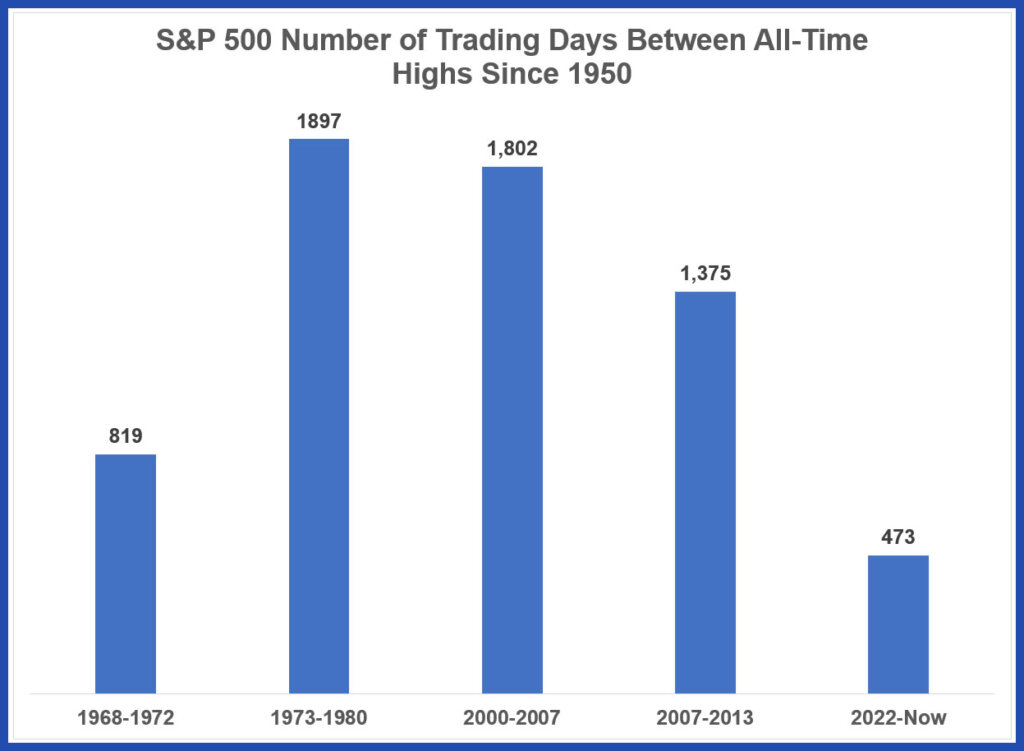

When should we expect the stock market to hit new highs?

Ben Carlson is back, on A Wealth of Common Sense, with an interesting look at how often the U.S. stock market breaks its previous all-time high.

With all the negative news headlines these days, you might be forgiven for assuming things must be pretty rough at the moment. Heck, you might even have thought we were a long way away from a new market high.

The truth is the U.S. stock market is fast approaching its all-time high. And it looks like this gap between market peaks will be the fifth longest on record. In other words, the recent bear market has caused substantial pain, but it’a far from the worst-case scenario.

In Canada, the TSX Composite index index hit 22,213 in April of 2022. Today, we sit at about 20,114, so we’re still down about 10% from all-time highs. That said, we wouldn’t bet against the Canadian stock market crashing through that ceiling in early 2024. (Predictions column to come soon!)

It’s also important to remember that the companies that make up Canada’s stock market index pay out higher annual dividends than their U.S. counterparts. That isn’t reflected in these index comparisons.

Of course, one might want to consider that while stock prices are bouncing back they’re still pretty far away on a “real” basis if we adjust for inflation. In other words, if you’re selling stocks to pay for life’s expenses, then you will have to sell more of those stocks (even if they’re back up to 2022 levels) to buy the same stuff that you used to. That price difference is obviously due to the high inflation rates the last couple of years.

Target shareholders finally avoid slings and arrows

The big headlines in U.S. retail this week centred around Target shares seeing a massive 18% spike, while Walmart shares came down over 8% after Thursday’s earnings announcement. However, we look behind those headlines to the context of those moves to get the real story.

U.S. Retail earnings highlights

All earnings numbers in this section are in USD.

Walmart (WMT/NYSE): Earnings per share of $1.53 (versus $1.52 predicted). Revenue of $160.80 billion (versus $159.72 billion estimate).

Home Depot (HD/NYSE): Earnings per share of $3.81 (versus $3.76 predicted). Revenue of $37.71 billion (versus $37.6 billion estimate).

Target (TGT/NYSE): Earnings per share of $2.10 (versus $1.48 predicted). Revenue of $25.4 billion (versus $25.24 billion estimate).

Macy’s (M/NYSE): Earnings per share of $0.21 (versus $0.00 predicted). Revenue of $4.86 billion (versus $4.82 billion estimate).

While the quarter was obviously a great redemption story for Target, these volatile stock moves were based on sky-high expectations for Walmart (the stock hit an all-time high this week before the earnings announcement) and a relatively terrible year for Target so far. It’s still down over 14% year to date even after the earnings bump.

Target’s C-suite commented that its improved margins were due to progress made on inventory management and reducing expenses, as well as reduced shrinkage (theft).

Walmart’s team stated the company is still worried about pressure on the U.S. consumer despite higher online sales (24% increase in the U.S. and 15% worldwide this year) and increased grocery revenues.

Walmart CEO Doug McMillon believes price relief might soon be in the cards, saying that general merchandise and grocery prices should, “start to deflate in the coming weeks and months.” He said, “In the U.S., we may be managing through a period of deflation in the months to come. And while that would put more unit pressure on us, we welcome it, because it’s better for our customers.”

We’re fairly certain that Walmart will be able to resist that “unit pressure” and that it will manage to satisfy both shareholders and customers, given its track record over the years.

CPI goes down, stocks go up

If you needed confirmation that U.S. interest rates are still foremost on investors’ minds, this week’s Consumer Price Index (CPI) from the U.S. Department of Labor was a big checkmark. Stocks rallied after Wednesday’s news that headline CPI was down to 3.2% annually (before coming down slightly later in the day’s trading session).

Core CPI (which excludes food and energy prices) is still at a 4% annual rate of increase.

Both the headline CPI and core CPI numbers were lower than anticipated Wall Street estimates, which led to market optimism.

Gasoline costs were down 5.3% annually.

Shelter costs were up 6.7% annually and were a major part of the overall headline inflation raise.

Travel-related categories ,such as hotel pricing and air travel, were also down substantially.

Used vehicles are down 7.1% from a year ago.

With unemployment rising from 3.2% to 3.9%, there should be less pressure to increase wages in most sectors going forward, thus contributing to a reduction in both headline CPI and core CPI.

Market watchers at CME Group report that the chances of any immediate interest rate hikes by the U.S. Fed have declined to nil. As you might expect, this confidence drove down long-term bond rates and raised future expectations for corporate earnings (and share prices).

To help you decide, let’s take a historical look at the returns of investments and 30-day Canadian Treasury bills, after inflation. Currently, the 30-day CND T-Bill yield is 5.04%, a little less than your promo rate on the high interest savings.

Historical inflation-adjusted returns from 2003 to 2022

All figures are in Canadian dollars, even the S&P 500 Index, and are adjusted for inflation.

The main purpose of investing in equities is to grow your money faster than the rate of inflation. And the reason you want to do this is to protect your purchasing power. That’s so what you can purchase today you could purchase in the future for the same inflation-adjusted dollar.

When you look at the chart above you can see that both the S&P 500 and TSX had positive, after inflation returns over the last 5-, 10-, and 20-year time frames. Both, however, have a big negative return in 2022, and that is the risk part you are concerned about.

Look at the T-Bill returns after inflation. They are all negative, and that is before adjusting for tax, which would make the returns even lower. What’s not shown in the table, though, is that if you invested the $100,000 in the T-Bills, you would not have seen it drop in value. You would always have, at a minimum, $100,000.

No risk, right? Not exactly.

Are there any risks with interest income? Is inflation a risk?

The risk with holding T-Bills, and I would add HISAs and guaranteed investment certificates (GICs), too, is that the rate of growth may not keep pace with inflation. So, although it seems you’re not taking a risk, you do risk purchasing power. That’s a different type of risk than what you mentioned. In cases where inflation is not a big concern, a HISA or a GIC can make sense. Examples of such situations may include saving for a near term purchase, transitioning from accumulation to decumulation, or as you age and get closer to death.

The other reason you may want to include savings in your portfolio is because there’s no way to know for sure when equity investments will be positive. The table above shows equities were positive over the last 5, 10 and 20 years. But that’s not always the case.

The humanitarian crises taking lives and garnering headlines are heart-wrenching—particularly for Canadians who have family and friends in the affected regions. More broadly, no one knows for sure how these crises will affect global economies, access to resources and financial markets. It’s understandable that investors are scared and making investment decisions based on their fear. Some people are selling their equities and leaving the markets. As an advisor, it’s my job to help take the emotion out of investing.

We know from previous wars, terrorist attacks, pandemics and other terrible events that people, governments and markets are resilient, and can even become stronger than they were before. This happened after 9/11, the global financial crisis and the global COVID-19 pandemic. The historical evidence suggests that the best thing investors can do when the world experiences a crisis is to separate feelings about the tragedy from the facts about the businesses you’re invested in and look for buying opportunities.

Impact of global crises on investments

The impact of wars and other traumatic events on the markets tend to be relatively short-lived. That’s because unlike fiscal policy—such as raising interest rates—the events themselves are not “economic” in nature.

For example, if war breaks out in an oil-producing country, will that affect the price of oil? Theoretically, it shouldn’t, because other, larger producers can offset any lost supply from the war-torn country.

But, as we know, perception can be more powerful than reality when it comes to the stock market. The initial, automatic reaction could be a spike in oil prices—and then prices should adjust with time.

What is a Canadian investor to do?

So, what do you do as an investor in Canada? Not an awful lot. As investment advisors, we get paid to grow people’s wealth. When markets sell off for reasons that are more temporary than related to economics and performance, it’s important to take emotion out of decision-making and not go into panic mode about your investments.

Markets may dip, but they don’t usually collapse. It’s possible your portfolio’s value may drop for a period of time. In the past, after a crisis has ended—and regardless of the outcome—the markets have regained stability, and investment returns have bounced back.

A crisis investment strategy

My best advice in the face of a world crisis: Stay calm, take a deep breath and focus on the fundamentals. Keep your risk profile front and centre, and think about where you want to put your money. My approach is to be sector agnostic and look for good value wherever I can find it.

Disney (and most U.S. companies) surprise to the upside

With 88% of companies in the S&P 500 having now reported results, nearly 9 in 10 have surpassed earnings estimates. Consumers continue to feel worse about the economy, and companies just continue to make more money. It’s quite an odd time to try to make sense of the markets.

U.S. earnings highlights

This is what two American companies reported this week. All figures below are in U.S. dollars.

Uber (UBER/NASDAQ): Earnings per share of $0.10 (versus $0.12 predicted), and revenues of $9.29 billion (versus $9.52 billion predicted).

Disney (DIS/NYSE): Earnings per share of $0.82 (versus $0.70 predicted), and revenues of $21.24 billion (versus $21.33 billion predicted).

Disney’s outperformance was chiefly due to ESPN+ subscriptions and continued revenue increases at theme parks. Investors appear to be big supporters of CEO Bob Iger’s announcement that Disney will “aggressively manage” its costs and will now be targeting $7.5 billion in cost reductions (up from a $5.5 billion target earlier in the year). Shares were up 4% in after-hours trading on Wednesday.

“As we look forward, there are four key building opportunities that will be central to our success: achieving significant and sustained profitability in our streaming business, building ESPN into the preeminent digital sports platform, improving the output and economics of our film studios, and turbocharging growth in our parks and experiences business.”

— Disney CEO Bob Iger

Uber, on the other hand, had a more subdued day. The earnings miss was contextualized by CEO Dara Khosrowshahi, when he pointed out that gross bookings for people-moving mobility were up 31% year over year (YOY), while UberEats gross bookings were up 18% YOY. The markets appeared to agree with Khosrowshahi’s spin, as shares were up 3% on Tuesday, despite the earnings news.

Canadian fossil fuels profitable—for now

Despite a United Nations report stating that Canadian fossil fuels should be kept in the ground, the sector continued right on pumping out profits this quarter.

Canadian earnings highlights

Here’s what came out of the earnings report.

Keyera Corp. (KEY/TSX): Earnings per share of $0.36 (versus $0.50 predicted). Revenue of $1.46 billion (versus $1.60 billion estimate).

TC Energy Corp. (TRP/TSX): Earnings per share of $1.00 (versus $0.98 predicted). Revenue of $3.94 billion (versus $3.91 billion estimate).

Suncor Energy Inc. (SU/TSX): Earnings per share of $1.52 (versus $1.36 predicted). Revenue of $12.64 billion (versus $12.85 billion estimate).

While accounting changes at Keyera resulted in an earnings-per-share miss, shareholders appeared to take the news in stride. Share prices were down less than 1% on Wednesday. Management highlighted the Pipestone expansion being on track and to be completed in the next two months, as well as a recent credit upgrade. The company was in great shape going forward. With net debt to adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) at 2.5 times, the company is on the conservative side of its 2.5- to 3-times target range.

TC Energy was up nearly 1% on the day after positive earnings news and the announcement that the new Coastal GasLink was completed ahead of the year-end target. Management also stated that it is taking steps to strengthen the company’s balance sheet, including selling off $5.3 billion in asset sales that will be used to pay down debt.

Despite total barrels of oil produced falling from 724,100 to 690,500 in last year’s third quarter, Suncor outperformed expectations and shares rose 3.7% on Thursday. Investors were forgiving in the decrease of adjusted earnings due to lower crude oil prices and increased royalties.

The company attributed the decrease in adjusted earnings to lower crude prices and a weaker business environment, as well as increased royalties and decreased sales volumes due to international asset divestments.