[ad_1]

Corporations, it seems, are just really, really good at making larger-than-ever profits. There are many reasons for fatter margins. It could be innovative new products and services, lower taxation, decreasing competition, willingness of consumers to pay higher prices, and so on. The bottom line is that the stock market will certainly pull back at some point (as it did this week). And there are solid reasons why companies are worth more now than they were, say, a few years ago.

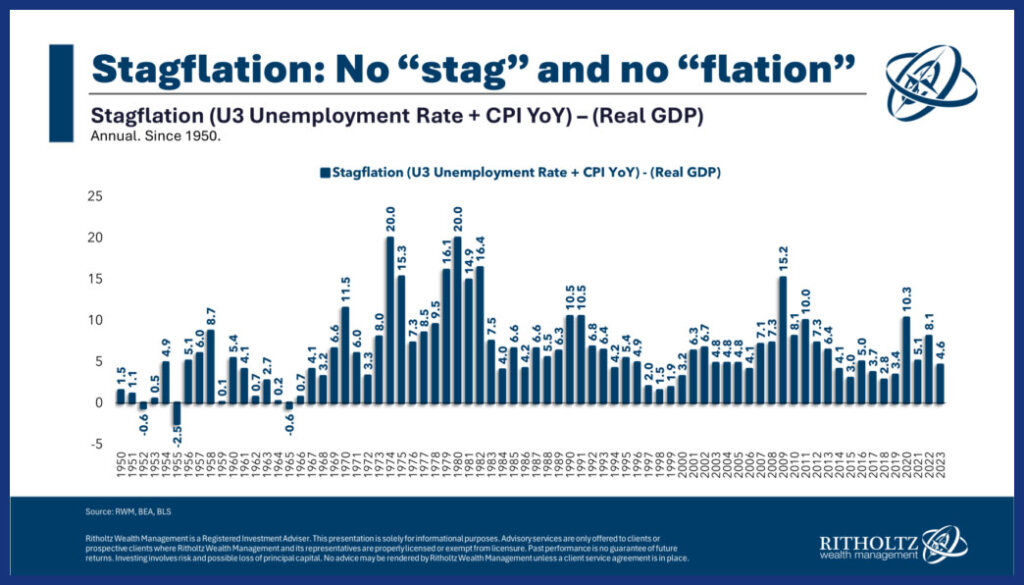

Stagflation’s disappearing act

Back in spring/summer of 2022, all the “cool” writers were predicting a scary-sounding future of stagflation. We, on the other hand, were a bit more skeptical. We felt that these worst-case economic scenarios were just around the corner.

So, two years later, are we fearing unemployment rates may shoot through the roof? Are we fearing a shrinking GDP? (Gross domestic product, that is.)

Barry Ritholtz doesn’t think so. He’s the co-founder, chairman and chief investment officer of Ritholtz Wealth Management LLC, in New York City.

The above chart illustrates what economists call the “misery index.” It’s a rough approximation of measuring stagflation.

You’ll notice that while things weren’t exactly great in 2020 and 2022, they weren’t historically bad either. Last year was downright tame, and (spoiler alert!) we’re probably in for another not-so-miserable year for 2024.

Note, though, that this features American data. While Canada’s misery index isn’t quite as upbeat as the USA’s, Canada still sits below long-term averages.

Sure, the cost of living is up in for Canadians and Americans. But so are wages. And unemployment in the USA is at 60-year lows. While growth in Canada has been “anemic,” we haven’t experienced the deep recession folks were worried about over the last couple of years. Growth in the U.S. has been excellent. And inflation has steadily trended downward in both countries.

[ad_2]

Kyle Prevost

Source link