Things tend to slow down for the holidays. The stock market isn’t there yet.

With Christmas just a couple of weeks away, it’s easy to look ahead to candy canes, caroling, and presents under the tree, but there’s still work to be done. The coming week certainly won’t be boring, with highly anticipated inflation data and a Federal Reserve decision on back-to-back days. The two events will do much to determine the direction of the market for the coming weeks—a deeper slide or a resumption of the Santa Claus rally.

U.S. stocks finished Friday’s choppy session with modest losses, capping off the worst week for stocks since September after a report on wholesale-price inflation challenged assumptions about slowing inflation in the U.S. The Dow Jones Industrial Average dropped 2.8% this week, its biggest pullback since at least the week ended Sept. 30, according to FactSet data. The blue-chip index finished Friday’s session DJIA, -0.90%

down 305.02 points, or 0.9%, at 33,476.46. The S&P 500 SPX, -0.73%

shed 29.13 points, or 0.7%, to 3,934.38, capping off a weekly drop of 3.4%, its biggest pullback since September. The Nasdaq Composite COMP, -0.70%

fell 77.39 points, or 0.7%, to 11,004.62.

Despite worries about inflation and an impending recession, there is at least one sign that some bullish market technical analysts might latch onto.

An upbeat golden cross appears to be forming in the Dow Jones Industrial Average DJIA, -0.90%,

more than nine months after a bearish death cross formed back in March, as the hawkish agenda of the Federal Reserve shattered bullishness on Wall Street.

A golden cross occurs when the 50-day moving average for an asset price trades above the 200-day MA, while a death cross, comparatively, is when the 50-day falls below the long-term average.

The 50-day moving average for the Dow stands at 32,200.32, at last check Friday afternoon, while the 200-day sits at 32,460.71, a roughly 260-point difference that could be traversed in the coming week or two, based on its current trajectory.

FactSet

A golden cross would mark the first for the Dow industrials since 2020 of August, according to Dow Jones Market Data.

The bullish chart formation also would appear at an odd time for investors, with an apparent uptrend materializing in the stock market, even as the threat of a recession in 2023 grows.

On top of that, MarketWatch columnist Mark Hulbert concludes that the U.S. stock market on average has performed no better in the wake of a golden crosses as it did at other times.

In many cases, a golden cross can help put an asset’s move into perspective, however, they tend to be well telegraphed.

Interestingly, the recession is also being widely predicted and some don’t think investors are getting the memo. As BlackRock notes, investors aren’t reflecting the damage that is to come, particularly as earnings expectations from American companies are right-sized.

So, it might be worth it for investors to take any golden crosses in assets with a grain of salt.

So far, the Dow industrials have outperformed over the past three months, up about 5%, compared with a decline of 2.5% for the S&P 500 SPX, -0.73%

and an 8.2% drop for the Nasdaq Composite COMP, -0.70%.

Over the past three months, the Dow industrials have recent in aggregate on the back of gains in shares of Caterpillar CAT, -1.56%,

Boeing Co. BA, +0.20%

Merck & Co. MRK, -1.86%,

IBM IBM, -0.47%

and Travelers Cos. TRV, -1.10%.

For the year so far, the Dow is down 7%, while the S&P 500 is off 17% and the Nasdaq is down nearly 30%.

The numbers: The University of Michigan’s gauge of consumer sentiment rose to a preliminary December reading of 59.1 from a November reading of 56.8.

Economists polled by the Wall Street Journal had expected a December reading of 56.5.

Inflation expectations over the next year fell to 4.6% from 4.9% last month. It is the lowest since September 2021. Five-year inflation expectations remained steady at 3%.

Key details: A gauge of consumer’s views of current conditions rose to 60.2 in December from 58.8 in November, while an indicator of expectations for the next six months rose to 58.4 from 55.6 last month.

Big picture: Economists think falling gasoline prices are behind the improvement in confidence.

The national average retail price for a gallon of gas is now $3.33, down $1.69 from June, according to White House data.

Still, high inflation has consumers remain in a relatively dour mood. The index is only marginally above the record low of 50 in June. By comparison, the consumer sentiment index was 101 in February of 2020.

Looking ahead: “High prices coupled with ongoing aggressive rate hikes will be a headwind for consumers and sentiment going forward,” said Rubeela Farooqi, chief U.S. economist at High Frequency Economics.

SPX, -0.73%

were higher on Friday on the back of hotter-than-expected wholesale inflation in November. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.583%

rose to 3.54%.

The number: U.S. wholesale prices rose 0.3% in November, the Labor Department said Friday.

Economists polled by The Wall Street Journal has forecast a 0.2% gain.

This is the third straight 0.3% monthly gain in the PPI index. Inflation in October and September was also revised up from the prior estimate of a 0.2% gain.

The core producer price index, which excludes volatile food, energy and trade prices, also rose 0.3% in November, up from a 0.2% gain in the prior month.

The increase in producer prices over the past 12 months slowed to 7.4% gain from 8.1% in the prior month. This is down from the peak of 11.7% in March.

Over the past year, core prices rose 4.9%, down from 5.4% in October.

Key details: The cost of energy fell 3.3% in November after a 2.3% gain in the prior month.

Food prices jumped 3.3% after a 0.8% increase in the prior month.

The cost of trade services jumped 0.7% in November after two straight monthly declines.

Big picture: Although hotter than expected in November, inflation at the wholesale level is showing steady deceleration from the peak in March.

The market is more focused on consumer price inflation report, which will be released next Tuesday, one day before the Fed’s decision on interest rates.

Market reaction: Stock futures DJIA, -0.25%

turned lower on the upside surprise to the monthly gain. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.533%

jumped to 3.5%.

What worked well during the years-long bull market through 2021 — a focus on growth, regardless of price — has ground to a halt this year. The rebirth of the value style of investing — and modest valuations overall — has taken hold.

The approach taken by the Invesco S&P 500 GARP ETF has paid off through both bull and bear markets.

Let’s begin with a 10-year chart comparing total returns with dividends reinvested for the Invesco S&P 500 GARP ETF SPGP, +0.67%

and the SPDR S&P 500 ETF Trust SPY, +0.78%,

which tracks the benchmark S&P 500:

FactSet

So far this year, SPGP is down 12%, while SPY is down 16%. But the long-term chart shows significant and consistent outperformance for SPGP, even during the bull market.

The S&P 500 GARP Index

GARP stands for “growth at a reasonable price.” SPGP tracks the S&P 500 GARP Index, which is reconstituted and rebalanced twice a year, on the third Fridays of June and December. The next change occurs Dec. 16.

S&P Dow Jones Indices assigns a growth score to each component of the S&P 500 by averaging the three-year compound annual growth rate (CAGR) for earnings and sales per share.

The top 150 components of the S&P 500 by growth score are eligible for inclusion in the GARP index. Those 150 are ranked by “quality/value composite score,” which is the average of these three ratios:

Financial leverage — total debt to book value.

Return on equity — trailing 12 months’ earnings per share divided by book value per share.

Earnings-to-price — 12 months’ earnings per share divided by the share price.

The top 75 of the 150 by QV rankings are then included in the GARP index and weighted by the growth score, with portfolio weightings ranging from 0.5% to 5%.

There is a weighting limitation of 40% to any one of the 11 S&P sectors.

Addressing concentration risk

The benchmark S&P 500 Index SPX, +0.75%

is weighted by market capitalization, which means it is more heavily concentrated than you might expect — success is rewarded, with rising stocks more heavily weighted over time.

That can backfire during a bear market, with Amazon.com Inc. AMZN, +2.14%

down 47% and Tesla Inc. TSLA, -0.34%

down 51% this year, to name two prominent examples.

Looking at the SPDR S&P 500 ETF Trust SPY, +0.78%,

which is the first and largest exchange traded fund and tracks the benchmark index by holding all of its components, six companies (Apple Inc. AAPL, +1.21%,

Microsoft Corp. MSFT, +1.24%,

Amazon, both common share classes of Alphabet Inc. GOOGL, -1.30%

That percentage has come down this year, but a lot of risk remains concentrated in a handful of companies. (Apple alone makes up 6.4% of the SPY portfolio. Tesla is now the ninth-largest holding, making up 1.4% of the portfolio.)

One way to address high concentration in an index fund is to use an equal-weighted approach, which Mark Hulbert recently discussed.

For the Invesco S&P 500 GARP ETF, the underlying index’s selection methodology has resulted in much less portfolio concentration than we see in SPY, with the top five holdings making up 10.9% of the portfolio.

U.S. stock indexes are wavering between small gains and losses on Wall Street Wednesday, struggling to gain ground after a four-day losing streak amid worries about the chances of an economic downturn in coming months.

How are stock-index futures trading

S&P 500 SPX, -0.16%

dropped 14 points, or 0.3%, to 3,927

Dow Jones Industrial Average DJIA, +0.08%

shed 70 points, or 0.2%, to 33,528, after rallying over 145 points earlier in the session

Nasdaq Composite COMP, -0.50%

fell 83 points, or 0.8% to 10,931

On Tuesday, the Dow Jones Industrial Average fell 351 points, or 1.03%, to 33596, the S&P 500 declined 58 points, or 1.44%, to 3,941, and the Nasdaq Composite dropped 225 points, or 2%, to 11,015.

What’s driving markets

A four-day losing streak, during which the S&P 500 index has lost 3.4%, showed little sign of being snapped Wednesday as investors continued to assess the potential economic damage inflicted by high inflation and the Federal Reserve’s campaign to damp it by raising interest rates. U.S. stock indexes extended losses in midday trade despite regaining some ground in the morning session.

“The recent run of macro data points in the U.S. continues to underscore relatively solid economic trends. And combined with the recent easing in financial conditions, it may trigger a need for the Fed to push back in December. Put another way, the dove camp is feeling some pain,” said Stephen Innes, managing partner at SPI Asset Management.

Jim Reid, strategist at Deutsche Bank , noted that the S&P 500 had now lost ground in the last seven out of eight sessions. “In fact, the latest moves for the S&P mean it’s now unwound the entirety of the rally following Fed Chair Powell’s [supposedly dovish] speech last week, which makes sense on one level given he didn’t actually say anything particularly new.”

The S&P 500 has fallen 17.2% in 2022 as the Federal Reserve has driven borrowing costs sharply higher in an effort to tame inflation that has been running at the fastest pace in 40 years.

“Fears are growing that economies are in for a rough time ahead as feverish inflation and the bitter interest rate medicine being used to bring it down take effect,” said Susannah Streeter, senior investment and markets analyst, Hargreaves Lansdown.

“Worries deepened amid warnings from U.S. banking and media sectors that navigating through the storm would not be easy, while the latest data has shown China’s trade has been sideswiped by a drop in global demand and zero-COVID policies. Despite today’s easing of restrictions it’s clear China’s COVID nightmare is not at an end,” Streeter added.

China on Wednesday announced a series of measures rolling back some of its most draconian anti-COVID-19 restrictions. People who test positive for the virus will be able to isolate at home rather than in overcrowded and unsanitary field hospitals, and schools where there have been no outbreaks must return to in-class teaching, according to the National Health Commission.

The Hang Seng index HSI, -3.22%

in Hong Kong fell 3.2%, while the CSI 300 000300, -0.25%

dropped 0.2%, suggesting investors had already discounted Beijing’s more relaxed COVID stance.

However, long time bull Tom Lee, head of research at Fundstrat, reckons equities will benefit in coming weeks as investors start to get greater clarity on when the Fed may stop tightening policy.

“We don’t think the end of the inflation war in 2022 is the Fed cutting rates. It is when Fed and markets see sufficient progress in inflation to remove the upside risks to higher rates. We think this could happen as early as the November CPI report. This will be released on 12/13,” Lee wrote in a note.

“And if November CPI is soft, we think this will support a strong year-end rally. Admittedly, a 10% move between now and [year end] seems a stretch given the S&P 500 is around 4,000 but… the broader point is we see stocks having positive skew given the cautious positioning of investors and the possibility of very favorable incoming inflation reports,” Lee added.

On the U.S. economic front, nonfarm productivity, which measures hourly output change per worker, rose at a 0.8% annualized rate last quarter, the Labor Department said on Wednesday. Unit labor costs, the price of labor per single unit of output, climbed by a smaller 2.4% annual pace in the third quarter, compared to the preliminary 3.5% increase.

What companies are in focus

Carvana Co. CVNA, -31.45%

shares slumped 33% after creditors led by Apollo Global Management Inc. and Pacific Investment Management Co. inked an agreement to team up in credit talks with the used car dealer in a move to avoid the conflicts that have arisen in other debt restructurings.

Lowe’s LOW, +3.05%

shares gained 2.1% after the company announced a new $15 billion share repurchase program and the home improvement retailer reaffirmed its full-year forecast.

Chinese electric vehicle stocks NIO Inc. NIO, -4.87%

and XPeng Inc. XPEV, -7.74%

dropped over 6.2% and 8.2%, respectively, despite news of the country easing some COVID-19 restrictions on production and travel.

Monday served as another smackdown for investors who are banking on a Goldilocks economy and a less aggressive Fed.

Some are now not ruling out a Grinch-like turn from the central bank — a 0.75% hike next week instead of the 0.50% markets have been pinning hopes on — following strong data on services, jobs and wages.

It all goes along with the theme of 2022 — expect the unexpected. The relief of moving out of a crippling pandemic was quickly replaced by the biggest war on Europe’s shores in decades, that sparked worldwide inflation surges.

What comes next is anyone’s guess and that brings us to our call of the day via Saxo Bank’s annual “Outrageous Predictions” for 2023.

While some of these will sound crazy, note that the Saxo team, led by Chief Investment Officer Steen Jakobsen, have nailed a few wild prophecies in the past decade. Those include: a Brexit prediction in 2015, a 25% drop for the S&P 500 from its 2007 high in 2008, a tripling of Bitcoin’s value forecast in 2017.

The focus for 2023’s prediction is that “a return to the disinflationary prepandemic dynamic is impossible because we have entered into a global war economy, with every major power across the world now scrambling to shore up their national security on all fronts; whether in an actual military sense, or due to profound supply-chain, energy and even financial insecurities that have been laid bare by the pandemic experience and Russia’s invasion of Ukraine,” says Jakobsen.

As for those predictions, here we go:

Gold crosses $2,075 then rockets to $3,000 on unstoppable inflation. “Fed policy tightening and quantitative tightening drives a new snag in U.S. treasury markets that forces new sneaky ‘measures’ to contain Treasury market volatility that really amounts to new de facto quantitative easing,” says Saxo. And China’s end of zero-COVID drives up demand, commodity prices and inflation.

Widespread price controls to cap official inflation due to war economy mentality. “In 2023, expect broadening price and even wage controls, maybe even something like a new National Board for Prices and Incomes being established in the U.K. and the U.S.,” said Saxo. Market fallout? Fuel for gold’s GC00, +0.19%

climb.

There’s a new reserve asset in town. Non U.S.-allied countries move away from the U.S. and IMF to create an “international clearing union (ICU) and a new reserve asset, called the Bancor (currency code KEY)” that borrows from economist John Maynard Keynes idea of resisting U.S. power over the international monetary system. Nonaligned central banks slash U.S. dollar reserves, Treasury yields soar and the dollar DXY, +0.09%

drops 25% against a basket of currencies that trade with Bancor.

Japan pegs USDJPY to 200. Pressure intensifies on the already weak yen USDJPY, +0.04%

into 2023 as currency intervention fails and inflation soars. The government resets the financial system, erasing all debt, recapitalizing banks, as trillions of yen return to Japan shores. But the yen still weakens by year-end.

A $10 trillion-dollar Manhattan project. A team of major tech leaders form a mega research-and-development effort for energy infrastructure and ground-breaking technologies — the Third Stone. Companies tied to the project soar in an overall weak environment for investing.

Tax haven ban kills private equity. The OECD launches a full ban on the biggest tax havens in the world in 2023 and in the U.S., carried interest tax as capital gains is shifted to ordinary income. It’s a body blow for private equity and venture capital — the valuation of publicly listed private-equity firms fall 50%.

The rest of their predictions are here, such as the formation of an EU Armed Forces in 2023 and an “UnBrexit” referendum.

Powell Industries POWL, +19.11%

stock is up 9% after the electrical equipment maker’s well-received results and new orders. Within software Sumo Logic SUMO, +11.65%

and GitLab shares GTLB, +5.71%

are surging on upbeat results and forecasts.

Headed into the holidays, consumers are using savings and credit, says a team of Jefferies analysts led by Corey Tarlowe. “The savings rate continues to trend lower and credit card balances are growing +15% Y/Y. We believe these trends indicate that the consumer is stretched.”

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

U.S. stocks are on track for their worst daily pullback in nearly a month on Monday as the S&P 500 traded below 4,000. Equity prices have been rattled by stronger-than-expected economic data, which market strategists say could inspire the Federal Reserve to hike interest-rates more aggressively. The S&P 500 SPX, -1.79%

fell 82 points, or 2%, to 3,988. The Dow Jones Industrial Average DJIA, -1.40%

fell 540 points, or 1.6%, to 33,889. The Nasdaq Composite COMP, -1.93%

fell 254 points, or 2.2%, to 11,206. All three indexes were on track for their worst day since at least Nov. 9, according to FactSet data. Meanwhile the Russell 2000 RUT, -2.78%

was down 55 points, or 2.9%, to 1,837, on track for its biggest drop since Nov. 2.

The stock market’s bounce off the October lows is running out of room, and it is time to take profits, according to Morgan Stanley’s Michael Wilson.

The chief equity strategist who correctly predicted this year’s stock-market selloff, now expects the S&P 500 SPX, -1.79%

to resume declines from the beginning of the year, after the benchmark last week crossed above its 200-day moving average.

“This makes the risk-reward of playing for more upside quite poor at this point, and we are now sellers again,” a team of strategists led by Wilson wrote in a Monday note.

Wilson went from one of Wall Street’s most outspoken bears to a tactical bull in October, when he anticipated a December rally of U.S. equities with the S&P 500 reaching up to 4,150 points. However, as the large-cap index now trades near the bank’s original tactical target range of 4,000 to 4,150, the strategist said investors should consider taking profits and get prepared for the new bear-market lows.

Wilson also said in November the S&P 500 will set a new price trough of 3,000 to 3,300 in the first quarter of 2023, before jumping back to the 3,900-level by the end of the year.

From a very short-term perspective, Wilson and his team think the S&P 500 could achieve 4,150, or about 3.8% above current levels, “over the next week or so.” However, a break of recent intraday lows of 3,938 would provide some confirmation the bear market is ready to reassert the downtrend in earnest, Wilson said.

Morgan Stanley’s bearish call was echoed by other Wall Street banks. JP Morgan Chase & Co.’s Marko Kolanovic, once one of Wall Street’s most vocal bulls, called for equity prices to stumble early next year. He also argued that the rebound in stocks was overdone after October. Meanwhile, strategists at BofA Global Research said it is time to sell the stock-market rally ahead of a potential surge in the unemployment rate next year.

Wilson recommends investors stay defensive in healthcare, staples and utilities as falling rates from here should be viewed as “a growth negative rather than valuation/Fed pause positive.” In addition, growth stocks are unlikely to benefit from falling rates because of the risk to corporate earnings, especially for tech and consumer-oriented companies, which are large weights in growth indices.

An obscure and arcane economic indicator suggests that Federal Reserve Chairman Jerome Powell was wrong when he said at his Nov. 30 news conference that “There is a path to a soft, a softish landing” for the U.S. economy.

This indicator traces to the large divergence between consumers’ views about the economy in general and their immediate personal financial circumstances in particular. A recession has occurred each time over the past four decades in which this divergence even approached its current level.

To measure this divergence, this indicator focuses on the Conference Board’s Consumer Confidence Index (CCI) and the University of Michigan’s Consumer Sentiment Survey (UMI). While there is some overlap between what these two indices measure, there is a significant difference in emphasis, according to James Stack of InvesTech Research, from whom I first heard about this indicator. The CCI more heavily reflects consumers’ attitudes towards the overall economy, according to Stack, while the UMI is more heavily weighted towards their immediate personal circumstances.

Perhaps not surprisingly, the CCI currently is higher than the UMI. Even as American consumers’ attitudes towards their immediate financial situations continue to sour, due to everything from inflation to higher mortgage rates to a softening housing market, the overall economy has proven to be remarkably resilient. Yet more evidence of this resilience was the Dec. 2 jobs report, in which the Labor Department reported the creation of a much-higher-than-expected number of new jobs.

What is more surprising is the magnitude of the current divergence. According to the latest data releases from the Conference Board and the University of Michigan in late November, the CCI is 43.4 percentage points higher than the UMI. That’s close to a record; the latest reading stands at the 98th percentile of all monthly readings of the past four decades.

Furthermore, as you can see from the chart above, a recession was in the economy’s not-too-distant future (shadowed bars) the past four times this difference rose to even 25 percentage points.

Consumer sentiment and the stock market

Stark as this chart’s correlations are, it’s difficult for a sample with just four observations to be statistically significant. To test this indicator’s potential, I next measured its ability to predict the S&P 500’s SPX, -1.96%

inflation-adjusted total return over the subsequent one- and five-year periods. The table below reflects data since 1979, which is when monthly data for both of these consumer indices first began to be reported.

When divergence between CCI and UMI was…

S&P 500’s average total real return over subsequent 12 months

S&P 500’s average total real return over subsequent 5 years (annualized)

In the highest 10% of monthly readings since 1979

-0.4%

-3.1%

In the lowest 10% of monthly readings since 1979

+14.3%

+14.8%

The differences shown in this table are statistically significant at the 95% confidence level that statisticians often use when determining if a pattern is genuine.

The bottom line? It’s not good news, for the economy in general or the U.S. stock market in particular, that consumers are so much more upbeat about the overall economy than they are about their immediate financial circumstances.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

S Naren, ED & CIO, ICICI Prudential AMC says he is positive on debt as it has become an attractive asset class given the higher yields amid rising interest rates. He is also positive on manufacturing, healthcare and financial services when it comes to equities. In a freewheeling interview he shares with Business Today what will define the markets in 2023.

BT: What is your big call on asset classes?

S Naren: Given the widespread belief that investors should only participate in equities, the big call is that investors should also invest in debt. In India, credit has grown by 20 lakh crore over the past year, and the government has a net borrowing programme of 12 lakh crore, of which 6 lakh crore will come from the insurance industry and other sources. The banks must provide the remaining borrowing of almost Rs 6 lakh crore. In the meanwhile, the deposit growth is just Rs 15 lakh crore of the required Rs 26 lakh crore. So, there is essentially a funding shortage in the debt market. In the past, asset classes with low investor interest have performed well in the short to medium term. A similar trend was visible in telecom, metals and PSUs as well three years back. Investors were reluctant to invest in these sectors and those are the very sectors which have delivered robust returns now.

However, given our call on debt, this does not mean that we are negative on equities. What we are saying is that we are positive on debt as it has become an attractive asset class given the higher yields amid rising interest rates. Also, debt is interesting based on the investment theory that one should invest in those asset classes which are facing a lack of investor interest. Here, investors can consider categories like dynamic bond, credit risk, savings, ultra-short for debt allocation requirements.

BT: For 2023, what should be the takeaways for retail investors?

S Naren: Our mantra for 2022 was about practicing asset allocation and being systematic with equity investing. Now, in 2023, we are continuing the same and have added that investors should consider investing in debt mutual fund.

BT: Does this mean tilting asset allocation towards debt?

S Naren: No, we are not asking investors to tilt their portfolios towards debt. Because of the low returns debt funds generated in the past, investors should not ignore the future potential opportunities that exist in debt funds. Over the last two years, retail investors largely opted for equity and hybrid funds. Barring debt index funds, there was hardly any net inflows into debt mutual funds. Apart from this, investors should continue with equity SIPs and stick to investing within the asset allocation framework.

BT: Over last few years, the return from debt mutual funds was around 4 per cent. When you say invest in debt funds, what kind of returns should one expect going forward?

S Naren: There is a better opportunity to generate risk-adjusted returns in debt today compared to the past three years. Before 2020, similar was the case with metals and PSUs on the equity side, with rates poised to rise, the debt outlook is set to improve.

We also have to remember that between 2008 and 2021, we had 13 years of quantitative easing by the global central banks. During this time, corporate India could easily borrow at very low rates (close to zero) globally. Today, that is no longer the case given that banks have moved on to quantitative tightening and rates have risen. This would translate to corporates borrowing more domestically which is another reason debt becomes interesting.

BT: What is your outlook on equity markets?

S Naren: We believe India presents a very good structural story, stable economy, and hence is currently overvalued. Between large cap, mid cap and small cap, we are positive on large cap and flexi cap category at this point in time. Post the sharp selling by FIIs, large caps are better placed on valuation terms than mid and small caps. Given this setup, staggered investing via SIP is likely to aid investors in their wealth creation journey.

BT: From your basket of funds, what funds would you recommend to investors?

S Naren: If one is investing through SIP then they can consider investing in aggressive categories like mid cap, flexi cap, value, special situation or small cap to benefit from the potential volatility in these pockets. On the other hand, if you are considering lump sum investment, then we prefer asset allocation oriented or hybrid category offerings given that equity markets are not cheap. Debt can also be considered for lump sum, particularly the shorter duration and accrual strategy schemes.

BT: Going forward what strategy would you recommend? Will it be momentum or value?

S Naren: It is tough to gauge whether momentum or value will deliver in the year ahead. At this point, we believe investors should focus on asset allocation strategies. Three years back, value was very cheap which is not the case now. We believe that as the US Fed stops hiking rates, precious metals like gold and silver are likely to do well. We were of the view that this call will play out in a protracted manner, but some of the precious metals have already rallied significantly.

BT: What themes are you looking at for 2023? Especially in the light of government’s focus on manufacturing?

S Naren: We are positive on manufacturing, healthcare and financial services. From a 12 to 18-month perspective, we believe systematic investing in export-oriented themes like IT could deliver returns as recession fears would have abated by then.

BT: Post the last Fed rate hike, RBI MPC is due this month. Do you think they will increase the rate or are we near the terminal of peak rates?

S Naren: We expect rate hike by both the RBI and the US Fed in the next round of meetings. But after this, it remains to be seen how fast the central banks will raise rates going forward. In India we believe trade balance is more of a concern than inflation unlike the Western world. We could manage inflation better because India did not engage in excess be it in terms of either printing too much money or reducing interest rates to near zero. However, the slowdown in advanced economies and rise in oil prices is negatively impacting our trade deficits.

Hedge-fund titan Bill Ackman appears to be walking back comments he made via Twitter last week about Sam Bankman-Fried that some interpreted as implicit support for the 30-something who presided over one of the most epic bankruptcies in financial markets in recent memory.

Last week, Ackman tweeted that Bankman-Fried’s statements made during a widely watched interview, streamed to New York from the crypto founder’s location in the Bahamas, was “believable.”

“Many have interpreted my tweet to mean that I am defending SBF or somehow supporting him. Nothing could be further from the truth,” Ackman wrote Saturday, referring to Bankman-Fried by his initials SBF.

Ackman went on to describe the implosion of Bankman-Fried’s crypto exchange FTX, and some of its associated businesses, as “at a minimum, the most egregious, large-scale case of business gross negligence that I have observed in my career.”

Ackman, who is the chief executive of Pershing Square Capital, a prominent investor in traditional markets, and an advocate of crypto, last week, tweeted this message following the widely watched interview of Bankman-Fried at the New York Times Dealbook Summit:

“Call me crazy, but I think SBF is telling the truth.”

Ackman has been chastised by some for seemingly offering verbal succor to a person who some have accused of, at the least, an epic mismanagement of client assets.

Speaking against the wishes of his lawyers, Bankman-Fried on Wednesday, during the Dealbook interview, admitted to making mistakes but said that he never intended to mingle client funds with those of the firm to make leveraged bets on crypto via hedge fund Alameda Research, which he founded before he started FTX.

“I didn’t know exactly what was going on,” Bankman said at the time.

At least one response to Ackman’s Saturday tweet, questioned whether the hedge funder might be responding to blowback from his own clients.

It isn’t the first time that Ackman has cast Bankman-Fried’s actions in a positive light. As the implosion of FTX was unfolding, Ackman said, in a now-deleted tweet, that he’d never before seen a CEO take responsibility as the crypto exchange operator did and that he wanted to give him “credit” for his actions. “It reflects well on him and the possibility of a more favorable outcome” for FTX, he wrote.

On Saturday, one Twitter user asked Ackman if had any ties to Bankman-Fried, which the investor bluntly said he doesn’t.

Bankman-Fried had been viewed as a financial darling inside and outside the crypto industry until his empire collapsed on Nov. 11 and it was revealed that affiliated hedge fund Alameda lost billions in FTX client money in leveraged crypto bets.

John Ray, the new chief executive of FTX, in a filing to the U.S. Bankruptcy Court for the District of Delaware, described the state of the crypto platform “as a complete failure of corporate controls and such a complete absence of trustworthy financial information.”

The November U.S. jobs report on Friday showed the U.S. economy gained 261,000 jobs last month, with the unemployment rate holding steady at 3.7%.

Economists polled by the Wall Street Journal had expected an addition of 200,000 jobs.

Wages jumped 0.6% in November, double the expected pace.

Below are some initial reactions from economists and other analysts as U.S. stocks DJIA, -0.20%

SPX, -0.37%

traded lower and the yield on the 10-year Treasury note TMUBMUSD10Y, 3.569%

jumped following the data on nonfarm payrolls.

“You probably want to revise your view on inflation and it’s overall dynamic more based on today’s job report than any other data report this entire year. And not in a favorable direction,” The report dashes hopes wage growth was cooling, said Jason Furman, economics professor at Harvard and former Obama White House economist, in a tweet.

“A stronger than expected 263,000 monthly payroll print plus the spike in wages…will reinforce the Fed’s assessment that the labor market remains very overheated, and rates will need to go higher for longer in order to bring it back into balance,” said Krishna Guha, vice chairman of Evercore ISI.

“The Fed will not like the renewed strength in wages,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

“The U.S. labor market has lost some momentum this year, but it’s still speeding ahead as we approach the new year. Continue to underestimate the momentum in the U.S. labor market at your own peril. Job gains continue to be added at a pace that would have drawn cheers in 2019. The labor market might encounter some bumps in the road next year, but it’s heading into 2023 cruising,” said Nick Bunker, head of economic research at the Indeed Hiring Lab.

Golden Dragon China ETF pulls back after record monthly rally in November

The Invesco Golden Dragon China ETF started December with a pullback, after enjoying a record monthly rally in November amid increasing signs that China was starting to back off from the zero-COVID policy. The ETF, which tracks American depositary shares (ADS) of China-based companies that only list in the U.S., slipped 0.9% in premarket trading Thursday, after running up 9.6% on Wednesday and 41.8% in November. The pullback comes as futures for the S&P 500 tacked on 0.4%, after the index jumped 3.1% on Wednesday. The Golden Dragon ETF’s biggest decliner ahead of Thursday’s open was electric vehicle maker XPeng Inc.’s stock, which dropped 6.0% after rocketing a daily record 47.3% on Wednesday. Elsewhere, shares of Nio Inc. fell 2.0%, Alibaba Group Holding Ltd. shed 2.5%, Li Auto Inc. gave up 3.6%, Tencent Music Entertainment Inc. declined 0.9% and Pinduoduo Inc. was down 2.3%.

After outperforming both the S&P 500 and Nasdaq Composite in November, the Dow Jones Industrial Average has exited bear-market territory, based on oft-cited criteria, on the final trading day of the month.

But before investors get too excited about a new bull market for equities, there’s plenty of reason for caution.

The Dow DJIA, +2.18%

finished Wednesday’s session at its highest closing level since April 21, according to Dow Jones Market Data. Thanks to the gains spurred by Fed Chairman Jerome Powell’s comments at the Brookings Institution, the blue-chip gain has now risen 20.4% from its Sept. 30 closing low, meaning it has technically exited bear-market territory. It’s the only major equity index to do so.

Typically, when a given index or asset has risen 20% or more off a recent bear-market low, it is said to have technically exited bear-market territory.

Throughout the history of financial markets, there have been many examples where stocks have rallied during a bear market, only to eventually turn lower and erase all of those gains.

During drawn-out recessionary bear markets, stocks often rip higher, only to see their gains fizzle again and again. This has already happened more than three times since the start of 2022, including notable counter-rallies that occurred in March, in July and August, and again since mid-October, according to FactSet data.

Looking further back, market history over the last couple of decades is replete with similar examples, as MarketWatch has reported.

Following the bursting of the dot-com bubble, the Nasdaq Composite endured at least seven rallies of 20% or more before reaching its ultimate cycle low in 2002.

Market strategists are especially cautious considering that the Fed still raising interest rates, although Fed Chairman Jerome Powell suggested on Wednesday that senior Fed officials will likely opt for a smaller hike in December after four consecutive 75 basis point hikes — remarks that helped fuel a broad stock-market surge.

This ultimately underscores a simple point: it’s difficult to say when a bear market has truly ended, since the start of a new bull market is often only crystal-clear in retrospect — not unlike the challenge of determining the start of a recession.

A similar precept holds true for the economy. While consecutive quarters of contracting gross domestic product are often described as a “technical” recession, this is not the criteria used by the National Bureau of Economic Research when determining whether the U.S. economy is actually in recession or not.

As the Dow charged higher late last week, one UBS markets strategist warned that investors should anticipate more volatility.

“We remain skeptical that the recent rally marks the start of a new market regime. The priority of the Fed is likely to remain the fight against inflation, pending a more consistent stream of softer prices and employment data. Against this backdrop, we favor adding to defensive assets in both equity and fixed-income markets,” said Mark Haefele, chief investment officer at UBS Global Wealth Management.

The blue-chip gauged finished Wednesday’s session at 34,589.77, having risen 737.24 points, or 2.2%. The S&P 500 SPX, +3.09%

and Nasdaq COMP, +4.41%

also recorded strong gains of 3.1% and 4.4%. It was the best session for all three indexes in roughly three weeks.

The U.S.-listed shares of China-based electric vehicle maker XPeng Inc. skyrocketed Wednesday, as investors cheered changes in China’s COVID policy while shrugging off weak third-quarter results and a downbeat outlook.

The stock XPEV, +45.44%

charged up 45.0% in midday trading, enough to pace all gainers on the New York Stock Exchange. It was also headed for the biggest one-day gain since going public in August 2020, surpassing the previous record advance of 33.9% on Nov. 23, 2020.

The rally comes even after XPeng reported a wider-than-expected loss for the third-straight quarter, missed on revenue for the first time and said it expected fourth-quarter revenue to fall 40% to 44% from a year ago while the FactSet consensus called for just a 4.4 decline.

Instead, investors seemed China appeared to move toward easing its zero-COVID policy, amid growing social unrest and a slowing economy. China’s government said Tuesday that it would renew its push to vaccinate the elderly, and said it would amend COVID control measures.

XPeng’s stock rally also comes at a time when investor sentiment had soured. Earlier this week, Jefferies analyst Johnson Wan downgraded the EV maker, citing recent “missteps” by the company at a time that the “honeymoon stage” for EVs in China was coming to an end.

In addition, short interest, or bearish bets on XPeng’s stock, was 5.7% of the public float, or freely tradable shares, based on the latest available exchange data. That compares with short interest as a percent of float for China-based rivals Nio Inc. NIO, +20.14%

at 4.1% and Li Auto Inc. LI, +18.35%

at 4.7%.

For Tesla Inc. TSLA, +2.12%,

which generated $5.13 billion in revenue from China in its latest quarter, or about 24% of total revenue, short interest as a percent of float was 2.9%.

XPeng’s stock has soared 60.7% in November but has still tumbled 41.7% over the past three months. In comparison, the Invesco Golden Dragon China exchange-traded fund PGJ, +8.98%

has shed 11.7% the past three months while the S&P 500 index SPX, +0.62%

has slipped 1.1%.

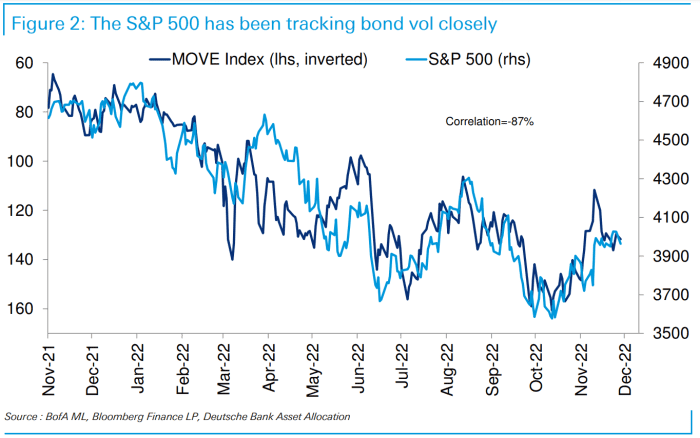

Anyone watching the market knows stocks have been hammered since the Federal Reserve began in March what has turned into an aggressive series of interest rate hikes, but strategists at Deutsche Bank say they might be surprised to learn that those rate hikes probably aren’t the culprit.

The S&P 500 SPX, -0.16%

has seen a return of negative 16.1%, at its current level, since the rate increases began. That’s the worst performance for an extended cycle of rate hikes since at least the late 1950s, according to a team led by Chief Strategist Binky Chadha in a Monday note (see chart below).

Deutsche Bank

The chart highlights what may be a surprise to many investors: rate hike cycles, historically, haven’t been a negative for stocks. Of the 11 previous hiking cycles dating back to 1958-59, only two (1994-95 and 1973), produced negative returns. On average, rate-hike cycles have produced a 9% return for the S&P 500.

Any misconception that rate-hike cycles have tended to be negative for stocks was probably reinforced by the market’s ugly 2022 performance, but a closer look at the tape shows why that conclusion doesn’t hold up, Chadha and his team wrote:

In contrast to most historical rate hiking cycles, which saw a positive correlation between Fed rates and equities (median +61%; 8 of 10 positive), this cycle has seen it run strongly negative (-68%). This negative correlation naturally suggests higher rates lowered equities, reinforcing the widely held belief. A closer look though reveals that the S&P 500 has been at current levels 4 times over the last 5 months, while rates have been successively and notably higher each time, with the 2y yield up 175bps (basis points) from the first time. This contradicts the view that higher rates drove the S&P 500 selloff, or at least show that the last 175bps higher in rates have not lowered the S&P 500.

So if sharp interest rate rises aren’t the driver, what is behind the selloff?

The Deutsche Bank analysts suspect it’s more about volatility in the bond market, which has seen a sustained rise since the Fed began raising rates. That’s unusual, they said, with rates volatility typically spiking in the run-up to and around the initial Fed hike and around changes in the speed of hikes during the cycle, then quickly dissipating.

Treasury-yield volatility, as measured by the ICE BofA MOVE Index, hasn’t tended to rise in a sustained manner during rate-hike cycles, they wrote, with the one exception being the 1973 hiking cycle, which was the only one that also saw a significant stock-market selloff.

Indeed, when rates and rate volatility have diverged in the current cycle, the stock market has inversely tracked the move in volatility rather than the level of yields, the analysts noted. For examples, they pointed to June, when volatility rose and equities fell sharply while yields rose modestly; August, when yield volatility fell even as yields rose; and the recent stretch, which has seen equities rally alongside a decline in yield volatility while yields have been rangebound (see chart below).

Deutsche Bank

“The selloff in equities during this rate hiking cycle has been driven, in our reading more by rising rates vol than it has by the higher level of rates, in what is a strong parallel with the only other rate hiking cycle (1973) that previously saw equities fall significantly,” the strategists wrote. “Vol” is market shorthand for volatility.

So the key question for investors is whether yield volatility will fall. Chadha and his team think it probably will, for two reasons: a slower and more “deliberate” speed of Fed hikes ahead; and the fact that rates have already seen a significant rise, pushing them closer to where they will peak, even if they will get there only gradually.

Volatility across asset classes tends to be highly correlated, they said, and paced by a common driver, which in this case has been the result of frequent changes in Fed guidance and the speed of rate hikes.

That means a decline in yield volatility should see a decline in stock-market volatility, with systematic strategists set to raise equity exposure from extremely low levels and indicating the market rally has further to go, they said.

Stocks were slightly lower in lackluster trade Tuesday, with the S&P 500 down 0.2%, while the Dow Jones Industrial Average DJIA, +0.01%

was off around 25 points, or 0.1%.

Income-seeking investors are looking at an opportunity to scoop up shares of real estate investment trusts. Stocks in that asset class have become more attractive as prices have fallen and cash flow is improving.

Below is a broad screen of REITs that have high dividend yields and are also expected to generate enough excess cash in 2023 to enable increases in dividend payouts.

REIT prices may turn a corner in 2023

REITs distribute most of their income to shareholders to maintain their tax-advantaged status. But the group is cyclical, with pressure on share prices when interest rates rise, as they have this year at an unprecedented scale. A slowing growth rate for the group may have also placed a drag on the stocks.

And now, with talk that the Federal Reserve may begin to temper its cycle of interest-rate increases, we may be nearing the time when REIT prices rise in anticipation of an eventual decline in interest rates. The market always looks ahead, which means long-term investors who have been waiting on the sidelines to buy higher-yielding income-oriented investments may have to make a move soon.

During an interview on Nov 28, James Bullard, president of the Federal Reserve Bank of St. Louis and a member of the Federal Open Market Committee, discussed the central bank’s cycle of interest-rate increases meant to reduce inflation.

When asked about the potential timing of the Fed’s “terminal rate” (the peak federal funds rate for this cycle), Bullard said: “Generally speaking, I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation.”

Fed’s Bullard says in MarketWatch interview that markets are underpricing the chance of still-higher rates

In August we published this guide to investing in REITs for income. Since the data for that article was pulled on Aug. 24, the S&P 500 SPX, -0.29%

has declined 4% (despite a 10% rally from its 2022 closing low on Oct. 12), but the benchmark index’s real estate sector has declined 13%.

REITs can be placed broadly into two categories. Mortgage REITs lend money to commercial or residential borrowers and/or invest in mortgage-backed securities, while equity REITs own property and lease it out.

The pressure on share prices can be greater for mortgage REITs, because the mortgage-lending business slows as interest rates rise. In this article we are focusing on equity REITs.

Industry numbers

The National Association of Real Estate Investment Trusts (Nareit) reported that third-quarter funds from operations (FFO) for U.S.-listed equity REITs were up 14% from a year earlier. To put that number in context, the year-over-year growth rate of quarterly FFO has been slowing — it was 35% a year ago. And the third-quarter FFO increase compares to a 23% increase in earnings per share for the S&P 500 from a year earlier, according to FactSet.

The NAREIT report breaks out numbers for 12 categories of equity REITs, and there is great variance in the growth numbers, as you can see here.

FFO is a non-GAAP measure that is commonly used to gauge REITs’ capacity for paying dividends. It adds amortization and depreciation (noncash items) back to earnings, while excluding gains on the sale of property. Adjusted funds from operations (AFFO) goes further, netting out expected capital expenditures to maintain the quality of property investments.

The slowing FFO growth numbers point to the importance of looking at REITs individually, to see if expected cash flow is sufficient to cover dividend payments.

Screen of high-yielding equity REITs

For 2022 through Nov. 28, the S&P 500 has declined 17%, while the real estate sector has fallen 27%, excluding dividends.

Over the very long term, through interest-rate cycles and the liquidity-driven bull market that ended this year, equity REITs have fared well, with an average annual return of 9.3% for 20 years, compared to an average return of 9.6% for the S&P 500, both with dividends reinvested, according to FactSet.

This performance might surprise some investors, when considering the REITs’ income focus and the S&P 500’s heavy weighting for rapidly growing technology companies.

For a broad screen of equity REITs, we began with the Russell 3000 Index RUA, -0.04%,

which represents 98% of U.S. companies by market capitalization.

We then narrowed the list to 119 equity REITs that are followed by at least five analysts covered by FactSet for which AFFO estimates are available.

If we divide the expected 2023 AFFO by the current share price, we have an estimated AFFO yield, which can be compared with the current dividend yield to see if there is expected “headroom” for dividend increases.

For example, if we look at Vornado Realty Trust VNO, +1.03%,

the current dividend yield is 8.56%. Based on the consensus 2023 AFFO estimate among analysts polled by FactSet, the expected AFFO yield is only 7.25%. This doesn’t mean that Vornado will cut its dividend and it doesn’t even mean the company won’t raise its payout next year. But it might make it less likely to do so.

Among the 119 equity REITs, 104 have expected 2023 AFFO headroom of at least 1.00%.

Here are the 20 equity REITs from our screen with the highest current dividend yields that have at least 1% expected AFFO headroom:

Click on the tickers for more about each company. You should read Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

The list includes each REIT’s main property investment type. However, many REITs are highly diversified. The simplified categories on the table may not cover all of their investment properties.

Knowing what a REIT invests in is part of the research you should do on your own before buying any individual stock. For arbitrary examples, some investors may wish to steer clear of exposure to certain areas of retail or hotels, or they may favor health-care properties.

Largest REITs

Several of the REITs that passed the screen have relatively small market capitalizations. You might be curious to see how the most widely held REITs fared in the screen. So here’s another list of the 20 largest U.S. REITs among the 119 that passed the first cut, sorted by market cap as of Nov. 28:

U.S. stocks finished sharply lower on Monday as several senior Federal Reserve officials hurt demand for stocks with hawkish commentary, while worries about the burgeoning protest movement in China rippled across global markets. The S&P 500 SPX, -1.54%

finished down 62.17 points, or 1.5%, to 3,96395. The Dow Jones Industrial Average DJIA, -1.45%

closed off 497.57 points, or 1.5%, to 33,849.46. The Nasdaq Composite COMP, -1.58%

closed 176.86 points, or 1.6%, lower at 11,049.50.