Senate Minority Leader Mitch McConnell R-KY speaks to the media after a Republican policy luncheon … [+] at the US Capitol in Washington, DC. (Photo by MANDEL NGAN / AFP) (Photo by MANDEL NGAN/AFP via Getty Images)

AFP via Getty Images

Republicans are expected to gain enough seats in the November 8 midterm elections to capture majorities in both chambers of Congress. A shift back to Republican control could complicate President Joe Biden’s energy policy priorities, but it would undoubtedly provide a boost to energy security advocates.

The Biden administration’s energy policies have prioritized a climate agenda that has contributed to supply scarcity and soaring costs for consumers. The White House’s answer to the energy crisis has so far been to attack America’s oil and natural gas producers, demanding increased production and threatening higher taxes.

Such bully-pulpit leadership from the White House isn’t enough to calm energy markets that are skittish over runaway inflation, Russian aggression in Europe, a standoff with China, and a global pandemic that won’t go away.

Current polling shows Republicans with an 84 in 100 chance to take back the U.S. House of Representatives, according to polling website FiveThirtyEight. The battle for control of the Senate is tighter, with Republicans holding a 52 in 100 shot of winning control of the upper chamber.

While Republican candidates have been gaining in the polls as Election Day approaches, the most likely outcome is a closely divided Congress with small Republican majorities. But even slim Republican majorities can create headwinds for President Biden’s agenda.

Under Biden’s presidency, retail gasoline prices surged to a record $5 a gallon in June. Prices at the pump are about $3.75 a gallon today, which is still 60% above where they were when Biden took office on January 6, 2021. Gas prices are poised to push higher before the end of the year due to tight global supply and rising geopolitical risks, including the Ukraine war and mounting sanctions on Russia, a top oil and gas producer.

It’s not just the price of gasoline that’s a problem, though. The diesel situation is even worse. Meanwhile, the U.S. Energy Information Administration (EIA) expects heating costs to soar this winter – with households forecast to spend nearly 30% more for natural gas and heating oil and 10% more for electricity.

Republicans are expected to upend Biden’s anti-fossil fuel agenda, which has seen the President recently threaten a windfall profit tax on domestic producers that would hamper investment in new oil and gas supplies.

Biden doesn’t have the political support in Congress now for such a tax, never mind when a new legislature convenes with increased Republican membership.

Biden administrators at the Environmental Protection Agency (EPA), Federal Energy Regulatory Commission (FERC), and Securities and Exchange Commission (SEC) have been critical of the domestic oil and gas industry. They have slow-walked new oil and gas lease sales, blocked drilling permits, and slowed approvals of pipelines. Such moves have created an anti-investment atmosphere in the traditional energy sector.

As the election approaches, Biden has grown more desperate to reduce consumer prices at the pump. The White House has drained the Strategic Petroleum Reserve (SPR) – America’s emergency oil stockpile – and courted oil-producing countries with horrible human rights records that promote terrorism.

Somewhere along the line, the President forgot that America is the world’s largest oil and gas producer – with a far better track record of producing energy in an environmentally responsible way than Iran or Venezuela.

Even with control of the House, Republicans could challenge the White House’s energy policies and push for a return to the energy priorities of the previous administration.

That includes the White House’s fraught relationship with Saudi Arabia, the leader of the OPEC cartel, which ignored Biden’s calls for an increase in global oil supplies, instead opting recently to cut production by 2 million barrels a day.

Congressional action on so-called NOPEC legislation, which would allow the U.S. Department of Justice to sue OPEC members on antitrust grounds as members of a monopoly, could come up for a vote in early 2023.

The issues troubling the U.S.-Saudi relationship do not fall neatly along party lines. Criticisms of Riyadh tend to be louder on the Democratic side, and former President Donald Trump was widely seen to have better relations with the kingdom. But Iowa’s Republican Senator Chuck Grassley has long led the charge to pass anti-OPEC legislation.

Trump’s continued influence over the Republican Party could prompt a more powerful Republican Congress to press for better relations with OPEC again. It’s hard to say how this one will fall, but it will be more difficult politically for Biden to veto or lobby against a vote on NOPEC than it has been for past presidents.

Biden’s crowning climate achievement, the Inflation Reduction Act (IRA), remains a GOP lightning rod. And while there is a high hurdle to paring back the law, Republicans can be expected to go to great lengths to expose its flaws.

Republicans remain extremely unhappy with the passage of the Democratic spending bill, which contained $369 billion in clean energy spending. House GOP lawmakers have gone so far as to repeal the law, which Biden signed in August, a central policy plank for the next Congress. If Republicans win control of the House, that means many hearings and bills centered around dismantling the IRA.

Among the most vulnerable of the IRA’s energy provisions are the new methane tax on oil and gas operations and the minimum corporate tax of 15% on income. While Congress has wide latitude regarding tax provisions, Republicans would have to win both chambers to repeal the provisions successfully. Even then, they are not likely to capture the two-thirds majority needed to overcome a presidential veto. Still, hefty GOP House oversight of federal agencies charged with implementing the law — and their budgets — could slow things down.

There is much at stake in energy at the state level in this election, too.

Republican wins in crucial producing states could exacerbate GOP pushback against environmental, social, and governance (ESG) issues. Political rhetoric around the clean energy transition in Washington is at a palpable high, which climate hawks fear could trickle down to state-level politics, widening the band of anti-ESG states.

Related debates have emerged in critical races, including gas-rich Pennsylvania. In the state’s closely watched Senate race, Republican candidate Mehmet Oz has vowed to cast aside the Biden administration’s “woke agenda” and ensure that capital flows to oil and gas projects are uninterrupted. And an SEC climate risk disclosure rule, also said to be on the GOP’s chopping block, is yet to be finalized.

Meanwhile, several tight gubernatorial races carry climate and energy implications, where a power change would almost guarantee a shift in state-level policy in those arenas. States to watch are Oklahoma, New Mexico, and Oregon.

Cat Clifford, CNBC climate tech and innovation reporter, at Helion Energy on October 20.

Photo taken by Jessie Barton, communications for Helion Energy, with Cat Clifford’s camera.

On Thursday, October 20, I took a reporting trip to Everett, Wash., to visit Helion Energy, a fusion startup that has raised raised nearly $600 million from a slew of relatively well known Silicon Valley investors, including Peter Thiel and Sam Altman. It’s got another $1.7 billion in commitments if it hits certain performance targets.

Because nuclear fusion has the potential to make limitless quantities of clean energy without generating any long-lasting nuclear waste, it’s often called the “holy grail” of clean energy. The holy grail remains elusive, however, because recreating fusion on earth in a way that generates more energy that is required to ignite the reaction and can be sustained for an extended period of time has so far remained unattainable. If we could only manage to commercialize fusion here on earth and at scale, all our energy woes would be solved, fusion proponents say.

Fusion has also been on the horizon for decades, just out of reach, seemingly firmly entrenched in a techno-utopia that exists only in science fiction fantasy novels.

David Kirtley (left), a co-founder and the CEO at Helion, and Chris Pihl, a co-founder and the chief technology officer at Helion.

Photo courtesy Cat Clifford, CNBC.

But visiting Helion Energy’s enormous workspace and lab pulled the idea of fusion out of the completely fantastical and into the potentially real for me. Of course, “potentially real” doesn’t mean that fusion will be a commercially viable energy source powering your home and my computer next year. But it no longer feels like flying a spaceship to Pluto.

As I walked through the massive Helion Energy buildings in Everett, one fully operational and one still under construction, I was struck by how workaday everything looked. Construction equipment, machinery, power cords, workbenches, and countless spaceship-looking component parts are everywhere. Plans are being executed. Wildly foreign-looking machines are being constructed and tested.

The Helion Energy building under construction to house their next generation fusion machine. The smokey atmosphere is visible.

Photo courtesy Cat Clifford, CNBC.

For the employees of Helion Energy, building a fusion device is their job. Going to the office every day means putting part A into Part B and into part C, fiddling with those parts, testing them, and then putting them with more parts, testing those, taking those parts apart maybe when something doesn’t work right, and then putting it back together again until it does. And then moving to Part D and Part E.

The date of my visit is relevant to this story, too, because it added a second layer of strange-becomes-real to my reporting trip.

On October 20, the Seattle Everett region was blanketed in dangerous levels of wildfire smoke. The air quality index for Everett was 254, making it the worst air quality in the world at that time, according to IQAir.

Helion Energy’s building under construction to house the seventh generation fusion machine on a day when wildfire smoke was not restricting visibility.

Photo courtesy Helion Energy

“Several wildfires burning in the north Cascades were fueled by warm, dry, and windy weather conditions. Easterly winds flared the fires as well as drove the resulting smoke westwards towards Everett and the Seattle region,” Christi Chester Schroeder, the Air Quality Science Manager at IQAir North America, told me.

Global warming is helping to fuel those fires, Denise L. Mauzerall, a professor of environmental engineering and international affairs at Princeton, told me.

“Climate change has contributed to the high temperatures and dry conditions that have prevailed in the Pacific Northwest this year,” Mauzerall said. “These weather conditions, exacerbated by climate change, have increased the likelihood and severity of the fires which are responsible for the extremely poor air quality.”

It was so bad that Helion had told all of its employees to stay home for the first time ever. Management deemed it too dangerous to ask them to leave their houses.

The circumstances of my visit set up an uncomfortable battle. On the one hand, I had a newfound sense of hope about the possibility of fusion energy. At same time, I was wrestling internally with a deep sense of dread about the state of the world.

Pihl has worked on fusion for nearly two decades now. He’s seen it evolve from the realm of physicist academics to a field followed closely by reporters and collecting billions in investments. People working on fusion have become the cool kids, the underdog heroes. As we collectively blow past any realistic hope of staying within the targeted 1.5 degrees of warming and as global energy demand continues to rise, fusion is the home run that sometimes feels like the only solution.

“It’s less of a academic pursuit, an altruistic pursuit, and it’s turning into more of a survival game at this point I think, with the way things are going,” Pihl told me, as we sat in the empty Helion offices looking out at a wall of gray smoke. “So it’s necessary. And I am glad it is getting attention.”

CEO and co-founder David Kirtley walked me around the vast lab space where Helion is working on constructing components for its seventh-generation system, Polaris. Each generation has proven out some combination of the physics and engineering that is needed to bring Helion’s specific approach to fusion to fruition. The sixth-generation prototype, Trenta, was completed in 2020 and proved able to reach 100 million degrees Celsius, a key milestone for proving out Helion’s approach.

Polaris is meant to prove, among other things, that it can achieve net electricity — that is, to generate more than it consumes — and it’s already begun designing its eighth generation system, which will be its first commercial grade system. The goal is to demonstrate Helion can make electricity from fusion by 2024 and to have power on the grid by the end of the decade, Kirtley told me.

Cat Clifford, CNBC climate tech and innovation reporter, at Helion Energy on October 20. Polaris, Helion’s seventh prototype, will be housed here.

Photo taken by Jessie Barton, communications for Helion Energy, with Cat Clifford’s camera.

Some of the feasibility of getting fusion energy to the electricity grid in the United States depends on factors Helion can’t control — establishing regulatory processes with the Nuclear Regulatory Commission, and licensing processes to get required grid interconnect approvals, a process which Kirtley has been told can range from a few years to as much as ten years. Because there are so many regulatory hurdles necessary to get fusion hooked into the grid, Kirtley said he expects their first paying customers are likely to be private customers, like technology companies that have power hungry data centers, for example. Working with utility companies will take longer.

One part of the Polaris system that looks perhaps the most otherworldly for a non fusion expert (like me) the Polaris Injector Test, which is how the fuel for the fusion reactor will get into the device.

Arguably the best-known fusion method involves a tokamak, a donut-shaped device that uses super powerful magnets to hold the plasma where the fusion reaction can occur.An international collaborative fusion project, called ITER (“the way” in Latin), is building a massive tokamak in Southern France to prove the viability of fusion.

Helion is not building a tokamak. It is building a long narrow device called a Field Reversed Configuration, or FRC, and the next version will be about 60 feet long.

The fuel is injected in short tiny bursts at both ends of the device and an electric current flowing in a loop confines the plasma. The magnets fire sequentially in pulses, sending the plasmas at both ends shooting towards each other at a velocity greater than one million miles per hour. The plasmas smash into each other in the central fusion chamber where they merge to become a superhot dense plasma that reaches 100 million degrees Celsius. This is where fusion occurs, generating new energy. The magnetic coils that facilitate the plasma compression also recover the energy that is generated. Some of that energy is recycled and used to recharge the capacitors that originally powered the reaction. The additional extra energy is electricity that can be used.

This is the Polaris Injector Test, where Helion Energy is building a component piece of the seventh generation fusion machine. There will be one of these on each side of the fusion device and this is where the fuel will get into the machine.

Photo courtesy Cat Clifford, CNBC.

Kirtley compares the pulsing of their fusion machine to a piston.

“You compress your fuel, it burns very hot and very intensely, but only for a little bit. And the amount of heat released in that little pulse is more than a large bonfire that’s on all the time,” he told me. “And because it’s a pulse, because it’s just one little high intensity pulse, you can make those engines much more compact, much smaller,” which is important for keeping costs down.

The idea is actually not new. It was theorized in the 1950s and 60s, Kirtley said. But it was not possible to execute until modern transistors and semiconductors were developed. Both Pihl and Kirtley looked at fusion earlier in their careers and weren’t convinced it was economically viable until they came to this FRC design.

Another moat to cross: This design does use a fuel that is very rare. The fuel for Helion’s approach is deuterium, an isotope of hydrogen that is fairly easy to find, and helium three, which is a very rare type of helium with one extra neutron.

“We used to have to say that you had to go into outer space to get helium three because it was so rare,” Kritley said. To enable their fusion machine to be scaled up, Helion is also developing a way to make helium three with fusion.

There is no question that Helion has a lot of steps and processes and regulatory hurdles before it can bring unlimited clean energy to the world, as it aims to do. But the way it feels to walk around an enormous wide-open lab facility — with some of the largest ceiling fans I have ever seen — it seems possible in a way that I hadn’t ever felt before. Walking back out into the smoke that day, I was so grateful to have that dose of hope.

But most people were not touring the Helion Energy lab on that day. Most people were sitting stuck inside, or putting themselves at risk outside, unable to see the horizon, unable to see a future where building a fusion machine is a job that is being executed like a mechanic working in a garage. I asked Kirtley about the battling feeling I had of despair at the smoke and hope at the fusion parts being assembled.

“The cognitive dissonance of sometimes what we see out in the world, and what we get to build here is pretty extreme,” Kirtley said.

“Twenty years ago, we were less optimistic about fusion.” But now, his eyes glow as he walks me around the lab. “I get very excited. I get very — you can tell — I get very energized.”

Other young scientists are also excited about fusion too. At the beginning of the week when I visited, Kirtley was at the American Physics Society Department of Plasma Physics conference giving a talk.

“At the end of my talk, I walked out and there were 30 or 40 people that came with me, and in the hallway, we just talked for an hour and a half about the industry,” he said. “The excitement was huge. And a lot of it was with younger engineers and scientists that are either grad students or postdocs, or in the first 10 years of their career, that are really excited about what private industry is doing.”

“To force poor countries to repay a loan to cope with a climate crisis they hardly caused is profoundly unfair. Instead of supporting countries that are facing worsening droughts, cyclones and flooding, rich countries are crippling their ability to cope with the next shock and deepening their poverty.” Credit: Credit: Manipadma Jena/IPS.

by Baher Kamal (madrid)

Inter Press Service

MADRID, Nov 04 (IPS) – Just a few days ahead of the UN Climate Conference (COP27) in Egypt (6-18 November), new revelations show how far rich, industrialised countries –those who contribute most to the growing catastrophes- have been lying over their real contributions to climate finance.

The report estimates between just 21-24.5 billion US dollars as the “true value” of climate finance provided in 2020, against a reported figure of 68.3 billion US dollars in public finance that rich countries said was provided (alongside mobilised private finance bringing the total to 83.3 billion US dollars).

The global climate finance target is supposed to be 100 billion US dollars a year, an amount which is slightly more than the 83 billion US dollars the world’s biggest nuclear powers spent in one single year– 2021, on such weapons of mass destruction.

Furthermore, “the combined profits of the largest energy companies in the first quarter of this year are close to 100 billion US dollars,” said already last august the UN Secretary-General António Guterres, adding that it was “immoral” that major oil and gas companies are reporting “record profits”, while prices soar.

“Very misleading”

Moreover, “rich countries’ contributions not only continue to fall miserably below their promised goal but are also very misleading in often counting the wrong things in the wrong way. They’re overstating their own generosity by painting a rosy picture that obscures how much is really going to poor countries,” said Nafkote Dabi, Oxfam International Climate Policy Lead.

Mostly loans

“Our global climate finance is a broken train: drastically flawed and putting us at risk of reaching a catastrophic destination. There are too many loans indebting poor countries that are already struggling to cope with climatic shocks.”

There is too much “dishonest” and “shady” reporting. The result is the most vulnerable countries remain ill-prepared to face the wrath of the climate crisis, warned Dabi.

Rich countries’ “manipulation”

Oxfam research found that instruments such as loans are being reported at face value, ignoring repayments and other factors. Too often funded projects have less climate focus than reported, making the net value of support specifically aiming at climate action significantly lower than actual reported climate finance figures.

Currently, loans are dominating over 70% provision (48.6 billion US dollars) of public climate finance, adding to the debt crisis across developing countries.

“To force poor countries to repay a loan to cope with a climate crisis they hardly caused is profoundly unfair. Instead of supporting countries that are facing worsening droughts, cyclones and flooding, rich countries are crippling their ability to cope with the next shock and deepening their poverty.”

Least Developed Countries’ external debt repayments reached 31 billion US dollars in 2020.

Such ‘funding’ is primarily based on loans

“A climate finance system that is primarily based on loans is only worsening the problem. Rich nations, especially the heaviest-polluting ones,” said Dabi.

A key way to prevent a full-scale climate catastrophe is for developed nations to fulfil their 100 billion US dollars commitments and genuinely address the current climate financing accounting holes. “Manipulating the system will only mean poor nations, least responsible for the climate crisis, footing the climate bill,” said Dabi.

Stalling all efforts

Other findings by this global confederation which includes 21 member organisations and affiliates reveal that an average of 189 million people per year have been affected by extreme weather-related events in developing countries since 1991 – the year that a mechanism was first proposed to address the costs of climate impacts on low-income countries.

The report, The Cost of Delay, by the Loss and Damage Collaboration – a group of more than 100 researchers, activists, and policymakers from around the globe – highlights how rich countries have repeatedly stalled efforts to provide dedicated finance to developing countries bearing the costs of a climate crisis they did little to cause.

Six fossil fuel companies

“Analysis shows that in the first half of 2022 six fossil fuel companies combined made enough money to cover the cost of major extreme weather and climate-related events in developing countries and still have nearly $70 billion profit remaining.”

The report reveals that 55 of the most climate-vulnerable countries have suffered climate-induced economic losses totalling over half a trillion dollars during the first two decades of this century as fossil fuel profits rocket, leaving people in some of the poorest places on earth to foot the bill.

Super profits. And massive deaths

It also reveals that the fossil fuel industry made enough super-profit between 2000 and 2019 to cover the costs of climate-induced economic losses in 55 of the most climate-vulnerable countries, almost sixty times over.

The report estimates that since 1991, developing countries have experienced 79% of recorded deaths and 97% of the total recorded number of people affected by the impacts of weather extremes.

The analysis also shows that the number of extreme weather and climate-related events that developing countries experience has more than doubled over that period with over 676,000 people killed.

The entire continent of Africa produces less than 4% of global emissions and the African Development Bank reported recently the continent was losing between five and 15% of its Gross Domestic Product (GDP) per capita growth because of climate change.

Enormous gains

Lyndsay Walsh, Oxfam’s Climate policy adviser and co-author of the report said: “It is an injustice that polluters who are disproportionately responsible for the escalating greenhouse gas emissions continue to reap these enormous profits while climate-vulnerable countries are left to foot the bill for the climate impacts destroying people’s lives, homes and jobs.”

Aerial view of the community water system located in the canton of El Zapote, in the municipality of Suchitoto in central El Salvador. Mounted on the roof are the 96 solar panels that generate the electricity needed to power the entire electrical and hydraulic mechanism that brings water to more than 2,500 families in this rural area of the country, which in the 1980s was the scene of heavy fighting during the Salvadoran civil war. CREDIT: Alex Leiva/IPS

by Edgardo Ayala (suchitoto, el salvador)

Inter Press Service

SUCHITOTO, El Salvador, Nov 03 (IPS) – The need for potable water led several rural settlements in El Salvador, at the end of the 12-year civil war in 1992, to rebuild what was destroyed and to innovate with technologies that at the time seemed unattainable, but which now benefit hundreds of families.

Several communities located in areas that were once the scene of armed conflict are now supplied with water through community systems powered by clean energy, such as solar power.

“The advantage is that the systems are powered by clean, renewable energies that do not pollute the environment,” Karilyn Vides, director of operations in El Salvador for the U.S.-based organization Companion Community Development Alternatives (CoCoDA), told IPS.

Hope where there was once war

The organization, based in Indianapolis, Indiana, has supported the development of 10 community water systems in El Salvador since 1992, five of them powered by solar energy.

These initiatives have benefited some 10,000 people whose water systems were destroyed during the conflict. Local residents had to start from scratch after returning years later.

A local resident of the Sitio el Zapotal community in El Zapote canton, El Salvador, turns on the tap to fill his sink to collect the water he will need for the day. A total of 10,000 people have benefited from the five solar-powered community water projects in El Salvador since 2010. CREDIT: Edgardo Ayala/IPS

This small Central American country experienced a bloody civil war between 1980 and 1992, which left some 75,000 people dead and more than 8,000 missing.

“Before leaving their communities, some families had water systems, but when they returned they had been completely destroyed, and they had to be rebuilt,” Vides said, during a tour by IPS to the Junta Administradora de Agua Potable or water board in the canton of El Zapote, Suchitoto municipality, in the central Salvadoran department of Cuscatlán.

In El Salvador, the term Junta Administradora de Agua Potable refers to community associations that, on their own initiative, manage to drill a well, build a tank and the entire distribution structure to provide service where the government has not had the capacity to do so.

There are an estimated 2,500 such water boards in the country, which provide service to 25 percent of the population, or some 1.6 million people, according to local environmental organizations.

But most of the water boards operate with hydroelectric power provided by the national grid, while the villages around Suchitoto have managed, with the support of CoCoDA and local organizations, to run on solar energy.

The community water project in the Salvadoran community of Sitio El Zapotal was driven by the efforts of local residents and international donors. At the foot of the catchment tank stand Karilyn Vides of CoCoDA, consultant and former guerrilla fighter René Luarca (front) – a member of the project’s water board – and former guerrilla Luis Antonio Landaverde (left), together with two technicians. CREDIT: Edgardo Ayala/IPS

This area is located on the slopes of the Guazapa mountain north of San Salvador, which during the civil war was a key stronghold of the then guerrilla Farabundo Martí National Liberation Front (FMLN), now a political party that governed the country between 2009 and 2019.

Some of the people behind the creation of the water board in the canton of El Zapote were part of the guerrilla units entrenched on Guazapa mountain.

“This area was heavily bombed and shelled, day and night,” Luis Antonio Landaverde, 56, a former guerrilla fighter who had to leave the front lines when a bomb explosion fractured his leg in July 1985, told IPS.

“A bomb dropped by an A37 plane fell nearby and broke my right leg, and I could no longer fight,” said Landaverde, who sits on the El Zapote water board.

The Junta de Agua del Cantón El Zapote, in central El Salvador, is the largest solar-powered community water project in the country, although it uses electricity from the national grid, from hydroelectric sources, as backup. CREDIT: Edgardo Ayala/IPS

Peasant farmers in the technological vanguard

At the end of the war in 1992, communities in the foothills of Guazapa began to organize themselves to set up their community water systems, at first using the national power grid, generated by hydroelectric sources.

Then they realized that the cost of the electricity and bringing the grid to remote villages was too high, and necessity and creativity drove them to look for other options.

“I was already very involved in alternative energy, and we thought that bringing in electricity would be as expensive as installing a solar energy system,” René Luarca, one of the architects of the use of sunlight in the community systems, told IPS.

The first solar-powered water system was built in 2010 in the Zacamil II community, in the Suchitoto area, benefiting some 40 families.

And because it worked so well, four similar projects followed in 2017.

Two were carried out around that municipality, and another in the rural area of the department of Cabañas, in the north of the country.

Given the project’s success, an effort was even made to develop a similar system in the community of Zacataloza, in the municipality of Ciudad Antigua, in the department of Nueva Segovia in northwestern Nicaragua.

The total investment exceeded 200,000 dollars, financed by CoCoDA’s U.S. partner organizations.

However, these were smallscale initiatives, benefiting an average of 100 families per project.

“There were eight panels, they were tiny, like little toys,” said Luarca, 80, known in the area as “Jerry,” his pseudonym during the war when he was a guerrilla in the National Resistance, one of the five organizations that made up the FMLN.

Then came the big challenge: to set up the project in the canton of El Zapote, which would require more panels and would provide water to a much larger number of families.

“This has been the biggest challenge, because there are no longer four panels – there are 96,” said Luarca.

A valve connected to the pump of the community water system in central El Salvador measures the pressure at which the liquid is being pumped to a catchment tank, located on a hill five kilometers away. The water flows down by gravity to the beneficiary families, who pay a monthly fee of six dollars for 12 cubic meters of water. CREDIT: Edgardo Ayala/IPS

The water system in El Zapote is a hybrid setup. This allows it to use solar energy as the main source, but it is backed up by the national grid, fueled by hydropower, when there is no sunshine or there are other types of failures.

“Since it is a fairly large system, it is not 100 percent solar, but is hybrid, so that it has both options,” explained Eliseo Zamora, 42, who is in charge of monitoring the operation of the equipment.

Using the pump, driven by a 30-horsepower motor, water is piped from the well to a tank perched on top of a hill, about five kilometers away as the crow flies.

From there, water flows by gravity down to the villages through a 25-kilometer network of pipes that zigzag under the subsoil, until reaching the families’ taps.

The project started when the armed conflict ended, but it took several years to buy the land, with resources from the six communities involved, and to acquire the machinery for the hydraulic system. It began operating in 2004 with electricity from the national grid, before CoCoDA switched to supporting the solar infrastructure.

For the installation of the panels and the adaptation of the system, the water board contributed 14,000 dollars, part of it from the hours worked by the villagers.

The new solar power system was inaugurated in June 2022 and benefits some 10 communities in the area – more than 2,500 families.

The service fee is six dollars per month for 12 cubic meters of water. For each additional cubic meter, the users are charged 0.55 cents.

“Our water is excellent, it is good for all kinds of human consumption,” the president of the water board, Ángela Pineda, told IPS.

How good is a company’s chief executive officer at investing your money most efficiently? This is an important question for long-term investors. It may underline the difference between a steady long-term performer and a flash in the pan.

And Apple Inc. AAPL, -4.24%

now makes up 7% of the SPDR S&P 500 ETF Trust SPY, -1.03%,

the first and largest exchange-traded fund (with $360 billion in assets), which tracks the benchmark S&P 500 SPX, -1.06%.

That’s close to an all-time record, and the iPhone maker has a whopping 14.1% position in the Invesco QQQ Trust QQQ, -1.95%,

which tracks the Nasdaq-100 Index NDX, -1.98%.

Looking at the full Nasdaq Index COMP, -1.73%,

which has 3,747 stocks, Apple takes a 13.5% position.

Apple now makes up 7.3% of the S&P 500 by market capitalization, close to the 8% record it set late in September.

FactSet

This is very much an Apple stock market, with the company topping the broad indexes that are weighted by market capitalization. You are likely to be invested in the company indirectly. You also might be feeling Apple’s impact in other ways. Apple’s App Store ecosystem drives more than $600 billion in annual revenue for developers.

Tim Cook’s tenure as Apple’s CEO has been nothing short of breathtaking when measured by the company’s financial performance. Apple is not one of the fastest-growing companies when measured by sales or earnings — it is too big for that. But its excellent stock performance has reflected Cook’s ability to deploy invested capital with improving efficiency. Cook has also been a market trendsetter in other important ways. He has Apple repurchasing $90 billion of its shares annually, setting the pace for stock buybacks in the market. Cook’s steady hand has also helped Apple withstand the market’s tech wreck and remain a stable pillar for the teetering Nasdaq Composite index generally. For all these reasons, Cook has earned a spot on the MarketWatch 50 list of the most influential people in markets.

Apple keeps improving by this important measure

Investors in the stock market are looking for growth over the long term. The best measure of that is whether or not a company’s share price goes up or down. But Cook isn’t just managing Apple’s stock. Digging a bit deeper into the company’s actual operating performance can provide some insight into what a good job Cook has done.

What should a corporate manager focus on? The stock price? How about the most efficient and most profitable way to provide goods and services? There are different ways to do this, and Apple has focused on quality, reliability and excellent service to build customer loyalty.

Apple’s commitment can be experienced by anyone who calls the company for customer service. It is easy to get through to a well-trained representative who will solve your problem. How many companies can say that at a time when it seems many companies cannot even handle answering the phone?

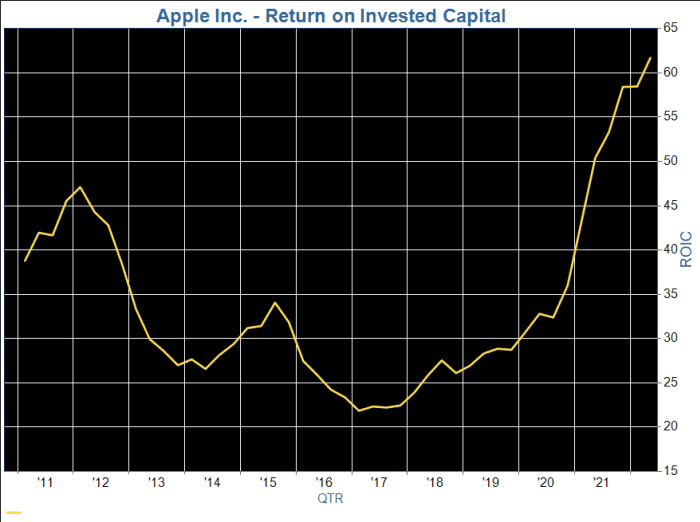

Apple’s returns on invested capital have increased markedly over the past six years.

FactSet

A company’s return on invested capital (ROIC) is its profit divided by the sum of the carrying value of its common stock, preferred stock, long-term debt and capitalized lease obligations. ROIC indicates how well a company has made use of the money it has raised to run its business. It is an annualized figure, but available quarterly, as used in the chart above.

The carrying value of a company’s stock may be a lot lower than its current market capitalization. The company may have issued most of its shares long ago at a much lower share price than the current one. If a company has issued shares recently or at relatively high prices, its ROIC will be lower.

A company with a high ROIC is likely either to have a relatively low level of long-term debt or to have made efficient use of the borrowed money.

Among companies in the S&P 500 that have been around for at least 10 years, Apple placed within the top 20 for average ROIC for the previous 40 reported fiscal quarters as of Sept. 1.

As you can see on the chart, Apple’s ROIC has improved dramatically over the past five years, even as the wide adoption of the company’s products and services has led to an overall slowdown in sales growth.

A quick comparison with other giants in the benchmark index

It might be interesting to see how Apple stacks up among other large companies, in part because some businesses are more capital-intensive than others. For example, over the past four quarters, Apple’s ROIC has averaged 52.9%, while the average for the S&P 500 has been a weighted 12.1%, by FactSet’s estimate.

Here are the 10 companies in the S&P 500 reporting the highest annual sales for their most recent full fiscal years, with a comparison of average ROIC over the past 40 reported quarters:

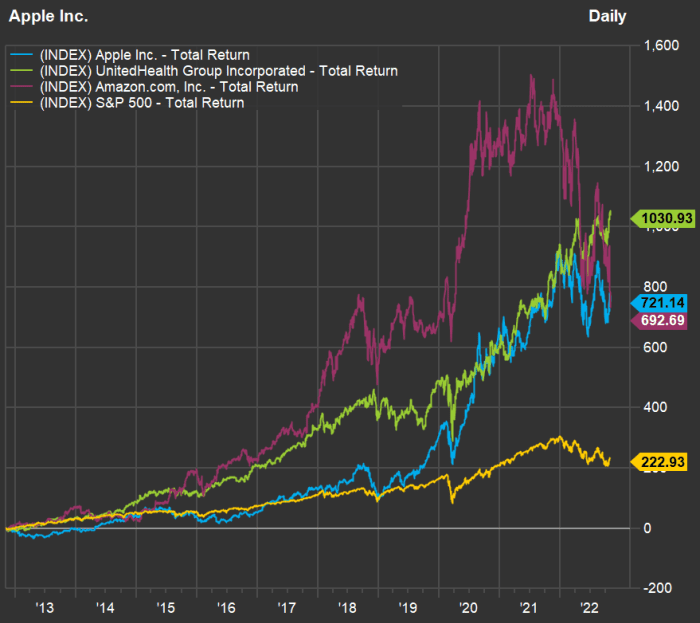

Among the largest 10 companies in the S&P 500 by annual sales, Apple takes the top ranking for average ROIC over the past 10 years, while ranking second for total return behind UnitedHealth Group Inc. UNH, +0.03%

and ahead of Amazon.com Inc. AMZN, -3.06%.

UnitedHealth has been able to remain at the forefront of managed care during the period of transition for healthcare in the U.S., in the wake of President Barack Obama’s signing of the Affordable Care Act into law in 2010.

Here’s a chart showing 10-year total returns for Apple, UnitedHealth Group, Amazon and the S&P 500:

FactSet

Apple is only slightly ahead of Amazon’s 10-year total return. But what is so striking about this chart is the volatility. Apple has had a smoother ride. During the bear market of 2022, Apple’s stock has declined 18%, while the S&P 500 has gone down 20%, the Nasdaq has fallen 32% (all with dividends reinvested) and Amazon has dropped 45%.

The broad indexes would have fared even worse so far this year without Apple.

LIVERPOOL, England — On the long picket line outside the gates of Liverpool’s Peel Port, rain-soaked dock workers warm themselves with cups of tea as they listen to 1980s pop.

Dozens of buses, cars and trucks honk in solidarity as they pass.

Dockers’ strikes are not new to Liverpool, nor is depravation. But this latest walk-out at Britain’s fourth-largest port is part of something much bigger, a great wave of public and private sector strikes taking place across the U.K. Railways, postal services, law courts and garbage collections are among the many public services grinding to a halt.

The immediate cause of the discontent, as elsewhere, is the rising cost of living. Inflation in the United Kingdom breached the 10 percent mark this year, with wages failing to keep pace.

But the U.K.’s economic woes long predate the current crisis. For more than a decade, Britain has been beset by weak economic growth, anaemic productivity, and stagnant private and public sector investment. Since 2016, its political leadership has been in a state of Brexit-induced flux.

Half a century after U.S. Secretary of State Henry Kissinger looked at the U.K.’s 1970s economic malaise and declared that “Britain is a tragedy,” the United Kingdom is heading to be the sick man of Europe once again.

The immediate cause of Liverpool dockers’ discontent that brought them to strike is the rising cost of living. | Christopher Furlong/Getty Images

Here in Liverpool, the “scars run very deep,” said Paul Turking, a dock worker in his late 30s. British voters, he added, have “been misled” by politicians’ promises to “level up” the country by investing heavily in regional economies. Conservatives “will promise you the world and then pull the carpet out from under your feet,” he complained.

“There’s no middle class no more,” said John Delij, a Peel Port veteran of 15 years. He sees the cost-of-living crisis and economic stagnation whittling away the middle rung of the economic ladder.

“How many billionaires do we have?” Delij asked, wondering how Britain could be the sixth-largest economy in the world with a record number of billionaires when food bank use is 35 percent above its pre-pandemic level. “The workers put money back into the economy,” he said.

What would they do if they were in charge? “Invest in affordable housing,” said Turking. “Housing and jobs.”

Falling behind

The British economy has been struck by particular turbulence over recent weeks. The cost of government borrowing soared in the wake of former PM Liz Truss’ disastrous mini-budget on September 23, with the U.K.’s central bank forced to step in and steady the bond markets.

But while the swift installation of Rishi Sunak, the former chancellor, as prime minister seems to have restored a modicum of calm, the economic backdrop remains bleak. Spending and welfare cuts are coming. Taxes are certain to rise. And the underlying problems cut deep.

U.K. productivity growth since the financial crisis has trailed that of comparator nations such as the U.S., France and Germany. As such, people’s median incomes also lag behind neighboring countries over the same period. Only Russia is forecast to have worse economic growth among the G20 nations in 2023.

In 1976, the U.K. — facing stagflation, a global energy crisis, a current account deficit and labor unrest — had to be bailed out by the International Monetary Fund. It feels far-fetched, but today some are warning it could happen again.

The U.K. is spluttering its way through an illness brought about in part through a series of self-inflicted wounds that have undermined the basic pillars of any economy: confidence and stability.

The political and economic malaise is such that it has prompted unwanted comparisons with countries whose misfortunes Britain once watched amusedly from afar.

“The existential risk to the U.K. … is not that we’re suddenly going to go off an economic cliff, or that the country’s going to descend into civil war or whatever,” said Jonathan Portes, professor of economics at King’s College London. “It’s that we will become like Italy.”

Portes, of course, does not mean a country blessed with good weather and fine food — but an economy hobbled by persistently low growth, caught in a dysfunctional political loop that lurches between “corrupt and incompetent right-wing populists” and “well-intentioned technocrats who can’t actually seem to turn the ship around.”

“That’s not the future that we want in the U.K,” he said.

Reviving the U.K.’s flatlining economy will not happen overnight. As Italy’s experience demonstrates, it’s one thing to diagnose an illness — another to cure it.

Experts speak of an unbalanced model heavily reliant upon Britain’s services sector and beset with low productivity, a result of years of underinvestment and a flexible labor market which delivers low unemployment but often insecure and low-paid work.

“We’re not investing in skills; businesses aren’t investing,” said Xiaowei Xu, senior research economist at the Institute for Fiscal Studies. “It’s not that surprising that we’re not getting productivity growth.”

But any attempt to address the country’s ailments will require its economic stewards to understand their underlying causes — and those stretch back at least to the first truly global crisis of the 21st century.

Crash and burn

The 2008 financial crisis hammered economies around the world, and the U.K. was no exception. Its economy shrunk by more than 6 percent between the first quarter of 2008 and the second quarter of 2009. Five years passed before it returned to its pre-recession size.

For Britain, the crisis in fact began in September 2007, a year before the collapse of Lehman Brothers, when wobbles in the U.S. subprime mortgage market sparked a run on the British bank Northern Rock.

The U.K. discovered it was particularly vulnerable to such a shock. Over the second half of the 20th century, its manufacturing base had largely eroded as its services sector expanded, with financial and professional services and real estate among the key drivers. As the Bank of England put it: “The interconnectedness of global finance meant that the U.K. financial system had become dangerously exposed to the fall-out from the U.S. sub-prime mortgage market.”

The crisis was a “big shock to the U.K.’s broad economic model,” said John Springford, from the Centre for European Reform. Productivity took an immediate hit as exports of financial services plunged. It never fully recovered.

“Productivity before the crash was basically, ‘Can we create lots and lots of debt and generate lots and lots of income on the back of this? Can we invent collateralized debt obligations and trade them in vast volumes?’” said James Meadway, director of the Progressive Economy Forum and a former adviser to Labour’s left-wing former shadow chancellor, John McDonnell.

A post-crash clampdown on City practises had an obvious impact.

“This is a major part of the British economy, so if it’s suddenly not performing the way it used to — for good reasons — things overall are going to look a bit shaky,” Meadway added.

The shock did not contain itself to the economy. In a pattern that would be repeated, and accentuated, in the coming years, it sent shuddering waves through the country’s political system, too.

The 2010 election was fought on how to best repair Britain’s broken economy. In 2009, the U.K. had the second-highest budget deficit in the G7, trailing only the U.S., according to the U.K. government’s own fiscal watchdog, the Office for Budget Responsibility (OBR).

The Conservative manifesto declared “our economy is overwhelmed by debt,” and promised to close the U.K.’s mounting budget deficit in five years with sharp public sector cuts. The incumbent Labour government responded by pledging to halve the deficit by 2014 with “deeper and tougher” cuts in public spending than the significant reductions overseen by former Conservative Prime Minister Margaret Thatcher in the 1980s.

The election returned a hung parliament, with the Conservatives entering into a coalition with the Liberal Democrats. The age of austerity was ushered in.

Austerity nation

Defenders of then-Chancellor George Osborne’s austerity program insist it saved Britain from the sort of market-led calamity witnessed this fall, and put the U.K. economy in a condition to weather subsequent global crises such as the COVID-19 pandemic and the fallout from the war in Ukraine.

“That hard work made policies like furlough and the energy price cap possible,” said Rupert Harrison, one of Osborne’s closest Treasury advisers.

Pointing to the brutal market response to Truss’ freewheeling economic plans, Harrison praised the “wisdom” of the coalition in prioritizing tackling the U.K.’s debt-GDP ratio. “You never know when you will be vulnerable to a loss of credibility,” he noted.

But Osborne’s detractors argue austerity — which saw deep cuts to community services such as libraries and adult social care; courts and prisons services; road maintenance; the police and so much more — also stripped away much of the U.K.’s social fabric, causing lasting and profound economic damage. A recent study claimed austerity was responsible for hundreds of thousands of excess deaths.

Under Osborne’s plan, three-quarters of the fiscal consolidation was to be delivered by spending cuts. With the exception of the National Health Service, schools and aid spending, all government budgets were slashed; public sector pay was frozen; taxes (mainly VAT) rose.

But while the government came close to delivering its fiscal tightening target for 2014-15, “the persistent underperformance of productivity and real GDP over that period meant the deficit remained higher than initially expected,” the OBR said. By his own measure, Osborne had failed, and was forced to push back his deficit-elimination target further. Austerity would have to continue into the second half of the 2010s.

Many economists contend that the fiscal belt-tightening sucked demand out of the economy and worsened Britain’s productivity crisis by stifling investment. “That certainly did hit U.K. growth and did some permanent damage,” said King’s College London’s Portes.

“If that investment isn’t there, other people start to find it less attractive to open businesses,” former Labour aide Meadway added. “If your railways aren’t actually very good … it does add up to a problem for businesses.”

A 2015 study found U.K. productivity, as measured by GDP per hour worked, was now lower than in the rest of the G7 by a whopping 18 percentage points.

“Frankly, nobody knows the whole answer,” Osborne said of Britain’s productivity conundrum in May 2015. “But what I do know is that I’d much rather have the productivity challenge than the challenge of mass unemployment.”

‘Jobs miracle’

Rising employment was indeed a signature achievement of the coalition years. Unemployment dropped below 6 percent across the U.K. by the end of the parliament in 2015, with just Germany and Austria achieving a lower rate of joblessness among the then-28 EU states. Real-term wages, however, took nearly a decade to recover to pre-crisis levels.

Economists like Meadway contend that the rise in employment came with a price, courtesy of Britain’s famously flexible labor market. He points to a Sports Direct warehouse in the East Midlands, where a 2015 Guardian investigation revealed the predominantly immigrant workforce was paid illegally low wages, while the working conditions were such that the facility was nicknamed “the gulag.”

The warehouse, it emerged, was built on a former coal mine, and for Meadway the symbolism neatly charts the U.K.’s move away from traditional heavy industry toward more precarious service sector employment. “It’s not a secure job anymore,” he said. “Once you have a very flexible labor market, the pressure on employers to pay more and the capacity for workers to bargain for more is very much reduced.”

Throughout the period, the Bank of England — the U.K.’s central bank — kept interest rates low and pursued a policy of quantitative easing. “That tends to distort what happens in the economy,” argued Meadway. QE, he said, is a “good [way of] getting money into the hands of people who already have quite a lot” and “doesn’t do much for people who depend on wage income.”

Meanwhile — whether necessary or not — the U.K.’s austerity policies undoubtedly worsened a decades-long trend of underinvestment in skills and research and development (Britain lags only Italy in the G7 on R&D spending). At British schools, there was a 9 percent real terms fall in per-pupil spending between 2009 and 2019, according to the Institute for Fiscal Studies’ Xu. “As countries get richer, usually you start spending more on education,” Xu noted.

Two senior ministers in the coalition government — David Gauke, who served in the Treasury throughout Osborne’s tenure, and ex-Lib Dem Business Secretary Vince Cable — have both accepted that the government might have focused more on higher taxation and less on cuts to public spending. But both also insisted the U.K had ultimately been correct to prioritize putting its public finances on a sounder footing.

It was February 2018 before Britain finally achieved Osborne’s goal of eliminating the deficit on its day-to-day budget.

Austerity was coming to an end, at last. But Osborne had already left the Treasury, 18 months earlier — swept away along with Cameron in the wake of a seismic national uprising.

***

David Cameron had won the 2015 election outright, despite — or perhaps because of — the stringent spending cuts his coalition government had overseen, more of which had been pledged in his 2015 manifesto. Also promised, of course, was a public vote on Britain’s EU membership.

The reasons for the leave vote that followed were many and complex — but few doubt that years of underinvestment in poorer parts of the U.K. were among them.

Regardless, the 2016 EU referendum triggered a period of political acrimony and turbulence not seen in Westminster for generations. With no pre-agreed model of what Brexit should actually entail, the U.K.’s future relationship with the EU became the subject of heated and protracted debate. After years of wrangling, Britain finally left the bloc at the end of January 2020, severing ties in a more profound way than many had envisaged.

While the twin crises of COVID and Ukraine have muddled the picture, most economists agree Brexit has already had a significant impact on the U.K. economy. The size of Britain’s trade flows relative to GDP has fallen further than other G7 countries, business investment growth trails the likes of Japan, South Korea and Italy, and the OBR has stuck by its March 2020 prediction that Brexit would reduce productivity and U.K. GDP by 4 percent.

Perhaps more significantly, Brexit has ushered in a period of political instability. As prime ministers come and go (the U.K. is now on its fifth since 2016), economic programs get neglected, or overturned. Overseas investors look on with trepidation.

“The evidence that the referendum outcome, and the kind of uncertainty and change in policy that it created, have led to low investment and low growth in the U.K. is fairly compelling,” said professor Stephen Millard, deputy director at the National Institute of Economic and Social Research.

Beyond the instability, the broader impact of the vote to leave remains contentious.

Portes argued — as many Remain supporters also do — that much harm was done by the decision to leave the EU’s single market. “It’s the facts, not the uncertainty that in my view is responsible for most of the damage,” he said.

Brexit supporters dismiss such claims.

“It’s difficult statistically to find much significant effect of Brexit on anything,” said professor Patrick Minford, founder member of Economists for Brexit. “There’s so much else going on, so much volatility.”

Minford, an economist favored by ex-PM Truss, acknowledged that “Brexit is disruptive in the short run, so it’s perfectly possible that you would get some short-run disruption.” But he added: “It was a long-term policy decision.”

Where next?

Plenty of economists can rattle off possible solutions, although actually delivering them has thus far evaded Britain’s political class. “It’s increasing investment, having more of a focus on the long-term, it’s having economic strategies that you set out and actually commit to over time,” says the IFS’ Xu. “As far as possible, it’s creating more certainty over economic policy.”

But in seeking to bring stability after the brief but chaotic Truss era, new U.K. Chancellor Jeremy Hunt has signaled a fresh period of austerity is on the way to plug the latest hole in the nation’s finances. Leveling Up Secretary Michael Gove told Times Radio that while, ideally, you wouldn’t want to reduce long-term capital investments, he was sure some spending on big projects “will be cut.”

This could be bad news for many of the U.K.’s long-awaited infrastructure schemes such as the HS2 high-speed rail line, which has been in the works for almost 15 years and already faces a familiar mix of local resistance, vested interests, and a sclerotic planning system.

“We have a real problem in the sense that the only way to really durably raise productivity growth for this country is for investments to pick up,” said Springford, from the Centre for European Reform. “And the headwinds to that are quite significant.”

For dock workers at Liverpool’s Peel Port, the prospect of a fresh round of austerity amid a cost-of-living crisis is too much to bear. “Workers all over this country need to stand up for themselves and join a union,” insisted Delij.

For him, it’s all about priorities — and the arguments still echo back to the great crash of 15 years ago. “They bailed the bankers out in 2007,” he said, “and can’t bail hungry people out now.”

There are over 8,500 coal power plants in the world, with over 2,100 GWs of capacity. These plants generate about 10 gigatons of CO2 emissions per year, nearly 30% of the global total. Credit: Bigstock

Opinion by Philippe Benoit, Chandra Shekhar Sinha (washington dc)

Inter Press Service

WASHINGTON DC, Nov 02 (IPS) – Report after report highlights that we can only achieve the greenhouse gas (GHG) emission reductions required by the climate goals of the Paris Agreement if much of the existing coal power generation capacity is retired early. To this end, one concept that deserves greater consideration is conducting an auction for early retirement of coal power plants worldwide: a global coal retirement auction. This article sets out the broad outlines of how this global auction might operate.

Accordingly, climate/development organizations, like the Asian Development Bank (ADB), the World Bank, the IEA and RMI, are exploring programs to effect the early retirement of these coal plants.

But closing these plants presents two important challenges. First, retiring these plants removes electricity production that many countries rely upon for their economic development … production that would need to be replaced with preferably low-carbon sources. Second, owners are generally unwilling to shutter revenue-generating plants and want financial compensation for the returns they would forego from the premature retirement of their asset. This article addresses this second constraint.

There are various regulatory mechanisms that can be used to push early retirement, such as mandating closure of plants or imposing a carbon tax or other cost that makes operating the plant uneconomic.

But what’s a fair price? Perhaps, however, that’s not the right question. Rather, at what price are the owners willing to shutter their plants? Given that there are more than 8,500 coal power plants operating with different technical and revenue characteristics, and over 2,000 plant owners in diverse financial situations following distinctive corporate strategies (including numerous state-owned enterprises), the answer will vary.

A technique that has been used in this type of context of multiple actors is an “auction”. While in the traditional context, a seller looks to get the highest price from multiple possible buyers through an auction, in this case, we have a buyer that is interested in paying the lowest price to different plant owners (i.e., the sellers) for the retirement of their coal plants.

The reverse auction mechanism could be used to solicit proposals from coal power plant owners as to the price at which they would be willing to close their plant. Conceptually, this could be done on the basis of MWs of installed power generation capacity. Under the auction, an interested coal plant owner would offer to sell — more specifically, to shutter — their MWs of plant capacity by a fixed time at a proposed price.

Importantly, the climate benefit sought by the auction is not from the decommissioning of MWs of capacity itself, but rather from the GHG emissions that would be avoided by retiring that capacity. Accordingly, for any coal retirement tender, it will be necessary to estimate the level of emissions that would be avoided.

This determination will be based on several factors, including the particular plant’s efficiency, remaining operational life and other technical characteristics, the type of coal used, and the amount of electricity production projected to be foregone through early retirement given the power system’s expected demand for electricity from that plant.

Tenders should include sufficient information to evaluate these items and, by extension, the level of avoided emissions and related climate benefit to be produced from the proposed retirement. This, in turn, will drive how much the auction buyer should be willing to pay for the tender.

Moreover, because it would be largely counter-productive from a climate perspective to pay to retire existing coal plants to see that money used directly (or indirectly) to build new fossil fuel generation, the tender by the plant owner would need to be accompanied by an undertaking not to reinvest in new fossil fuel generation.

As has been repeatedly explained, CO2 emissions have a global impact that is essentially unaffected by the geographic location of the emitting plant. Given this global nature of emissions, the auction would likewise be conducted at a worldwide level as a global auction. From India to Indonesia, from South Africa to South Korea, from Poland to Australia, any plant anywhere would be eligible to participate in the global auction.

Given this scope, an international organization like the United Nations or a multilateral development bank would be well positioned to provide the platform for this auction. One could imagine a system where the auction bidding process sets out eligibility criteria for projects, the methodology for estimating GHG emission reductions, and other key bid-submission parameters.

Significantly, while the bidding process would be managed on an integrated basis, the funding and selection of winners need not be. Rather, a system that allows for the matching of interested coal retirement buyers with individual plant owners could be used.

For example, buyers and their funding could be mobilized on a plant-by-plant basis based on information submitted by the plant owner through the auction process. Indeed, many potential funders have areas of focus that could lead them to be attracted to retiring coal assets only in certain countries (e.g., funders interested in a targeted set of developing countries). The proposed auction structure could accommodate these preferences. Moreover, the global auction could also operate in association with country-specific approaches.

One potential source of funding for coal retirements tendered under the auction is the potentially large amounts of capital to be mobilized through expanded carbon credit mechanisms under development. Tapping into these mechanisms might require establishing defined project eligibility criteria, frameworks for calculating GHG emissions reductions, and associated monitoring and verification systems to enable payments for emission reductions at the time of decommissioning based on a price for emission reduction (“carbon”) credits.

It is also important to recall the first constraint noted earlier, namely that countries, and particularly developing countries, will need more electricity to power further economic and social development. Accordingly, any global auction to retire coal plants needs to be coupled with a program to fund new renewables electricity generation.

Climate change is a global challenge affected by GHG emissions from anywhere. We need to reduce emissions from coal power generation and that requires some program to encourage and entice owners to shutter their plants. A global auction, conducted by the United Nations or a similar international organization, would help to identify opportunities where willing plant owners and interested funders can make a deal.

Philippe Benoit has over 20 years working on international energy, finance and development issues, including management positions at the World Bank and the International Energy Agency. He is currently research director at Global Infrastructure Analytics and Sustainability 2050.

Chandra Shekhar Sinha is an Adviser in the Climate Change Group at the World Bank and works on climate and carbon finance. He previously worked at JPMorgan, TERI-India, UNDP, and the Kennedy School of Government at Harvard University.

Vicki Hollub’s Occidental Petroleum controls the biggest piece of the most important area for oil production in the United States. Not so long ago, an oilman in a position like that—and it would’ve been a man, before Hollub came along—would have gone for broke, turning up production to its physical limits.

Not Hollub. Occidental produces on average the equivalent of about 1.15 million barrels of oil a day, and that’s more than enough to turn a profit. The company can make money as long as oil prices are above $40 a barrel. They’ve been above $80 for almost all of this year, as the war in Ukraine takes a toll on global markets and the Saudi-led oil cartel OPEC now slashes production.

“We don’t feel like we’re in a national crisis right now,” Hollub told MarketWatch in an interview. And that means Hollub can keep executing on her plans: making shareholders happy by paying down debt and buying back shares. “When you have such a low break-even, to me there’s no pressure to increase production right now, when we have these other two ways that we can increase shareholder value,” Hollub said.

That market-focused logic puts her at odds with President Biden, who is acting like there is a national energy crisis ongoingprecisely because of what oil CEOs like Hollub are doing. The size of oil companies’ profits is outrageous, Biden said Monday. They’re raking in cash not because of innovation or investment but as a windfall from the war in Ukraine, Biden said. “Rather than increasing their investments in America or giving American consumers a break, their excess profits are going back to their shareholders and to buying back their stock, so the executive pay is — are going to skyrocket,” Biden said. He has ordered releases from the Strategic Petroleum Reserve to keep down gas prices and asked Congress to tax oil-company profits.

But Hollub is single-mindedly focused on seizing the moment to improve the company’s financial position. Occidental still has significant debt left over from a challenging acquisition Hollub spearheaded before the pandemic. In the second quarter alone, the company used its windfall to repay $4.8 billion in debt. If Biden called, she’d listen, but she hasn’t spoken to him one-on-one. Hollub said she’d spoken to the administration through Energy Secretary Jennifer Granholm. (“She doesn’t know the industry very well right now, but it’s because she hasn’t been in her job very long,” Hollub said.) The White House and the Department of Energy did not return requests for comment.

Hollub says she’s just following the market. “If demand goes down, we reduce production, if it goes up, we increase.” Oil prices have fluctuated rapidly over the year, and with a recession widely anticipated in the near future, demand could drop, Hollub said. Biden’s releases of oil from the SPR, she added, may have reduced gasoline prices, but at a cost to national security. “The SPR should be reserved for emergency situations, and you never know when those might come,” Hollub said.

Hollub’s message may not be politically convenient, but it’s exactly what her shareholders want to hear. Occidental OXY, -2.29%

is America’s hottest stock and has returned 150% this year, making it the top-performing company in the S&P 500 SPX, -0.65%.

Investors who bought shares of Occidental in January and held them through today would have more than doubled their money, even as the broader market has crashed. Warren Buffett’s Berkshire Hathaway has gone on a buying spree this year, and now owns more than 20% of Occidental’s shares. How Hollub got here constitutes America’s greatest corporate saga in recent years, from her 2019 debt-fueled decision to buy bigger rival Anadarko Petroleum over the vocal objections of activist investor Carl Icahn, to the pandemic-induced collapse in oil prices that almost bankrupted Occidental, and Buffett’s extension, removal, and re-extension of support.

With Occidental now on solid financial footing, Hollub is continuing to leave a mark on the oil industry and the world, landing her on the MarketWatch 50 list of the most influential people in markets. Hollub’s tangles with the wise men of Wall Street have left her savvier about how to manage her business. Stung by previous boom-and-bust cycles, Hollub has helped lead America’s oil frackers away from being “swing producers” that could counter the war-driven increase in energy prices, as she paid down debt and returned cash to shareholders through dividends and stock buybacks instead of plowing some of that money into shale oil fields. She is also pushing investment into Occidental’s massive new carbon-capture effort.

More than anything, Hollub is focused on guys like Bill Smead, founder of Smead Capital Management, who is a long-term investor in Occidental and a Hollub fan. “She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us,” he said.

With that kind of backing, Hollub is planning to put Occidental in the driver’s seat of the massive national economic transition induced by climate change. She is positioning Occidental to be the company of the energy transition, one geared not to the free-for-all economy of the last century or some carbonless vision of the next, but the oil company for right now. She might even stop drilling new oil wells entirely.

“Now we feel like we control our own destiny,” Hollub said.

For the chief executive of a company that’s having a banner year on Wall Street while investors choke down generational losses, Hollub seems to constantly be on the alert for threats. Talking through the company’s prospects, she repeats a certain phrase: “I know that this will ultimately get me in trouble, but…”

Trouble? Hollub and Occidental have known their share.

The drama surrounding Occidental’s 2019 acquisition of Anadarko would make for a good boardroom thriller—or at least a lively business-school case study. Anadarko had big assets in the crucial Permian Basin region of Texas and New Mexico, where horizontal drilling in shale rock had reinvigorated an aging oil field into the nation’s biggest production zone.

Hollub and her team made an offer to buy Anadarko after months of research. She thought she had a deal locked, only to hear on the radio that Anadarko had announced plans to combine with Chevron. She nearly drove off the road, Texas Monthly recounts.

Hollub turned to Buffett for help. He agreed to what was effectively a $10 billion loan at 8% interest, in the form of preferred shares, along with warrants that allow Berkshire Hathaway, Buffett’s company, to buy more common stock. That got Hollub what she wanted, but many on Wall Street hated it. “The Buffett deal was like taking candy from a baby and amazingly she even thanked him publicly for it!” Icahn wrote in a letter to his fellow shareholders. Icahn had bought a slug of Occidental’s shares and, in the ensuing months, the billionaire investor led a shareholder campaign against Hollub, insisting that she needed stronger board oversight. Icahn allies were made Occidental directors.

In 2020, as COVID-19 flattened the global economy, deeply indebted Occidental was forced to cut its dividend for the first time in decades. Buffett sold his stock. At Icahn’s urging, the company issued 113 million warrants to its shareholders, allowing them to buy shares at $22, at a time when the stock was trading at $17. Gary Hu, one of the Icahn directors on Occidental’s board, pointed to those warrants as evidence of their success. “Our involvement in Occidental represented activism at its finest,” said Hu.

Hollub flatly disagrees. Icahn saw an opportunity to make an easy profit in derailing the Anadarko deal, Hollub said. “And what he expected is that we would lose and he would benefit from that. Since that didn’t happen, he managed to maneuver his way onto the board.” Icahn’s representatives on the board came to Hollub with a number of plans, including the warrants. She felt that one wouldn’t do any harm. “So that’s what we agreed to, but yeah, the other 10 or so weird things, we didn’t do.”

““She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us.””

— Bill Smead, founder of Smead Capital Management

Former Occidental CEO Stephen Chazen returned to chair the board at Icahn’s insistence. Icahn and Occidental ultimately reached a settlement. His board members left, and the activist sold his common shares earlier this year. Chazen passed away in September. The experience embittered both sides, but there is one point of agreement: Hollub will do as she sees fit. “We were clearly wrong about the board’s ability to restrain Vicki’s ambitions,” Hu said.

Icahn made a $1.5 billion profit. At a MarketWatch event in September, Icahn said he still holds the warrants. But he hasn’t let go of the issues that motivated him to push into Occidental in the first place, though he insists he has no problem with Hollub personally. He likened her to a kid who got lucky gambling in Vegas. “The system allowed her to do it. And she’s just one small example of what is wrong with corporate governance.”

But as Icahn has himself shown, the system of corporate money in America is malleable. Its players can learn the rules of the game and adapt. Quarter after quarter since the dark days of the pandemic, Hollub turned up on corporate earnings calls pledging to keep cash flows strong, to invest in the highest-returning assets, and not to fall into the trap of overinvesting in debt-fueled or expensive production capacity, as so many failed shale producers have done in the past. She’s driven the company’s debt from nearly $40 billion following the Anadarko acquisition to less than $20 billion today. She increased the company’s dividend earlier this year. Along the way she transformed from market pariah to textbook CEO.

Hollub and other CEOs who run America’s biggest shale-oil producers have learned from the industry’s past mistakes. After proving a decade ago they could successfully extract shale oil, many U.S. oil producers were cheered on by growth and momentum stock investors as they borrowed billions to ramp up production, only to have those same investors abandon them after Saudi Arabia induced a plunge in oil prices. In the years that followed, U.S. shale-oil producers cultivated a new set of more value-oriented shareholders by promising they would share in profits through dividends and stock buybacks. Hollub and many of those other CEOs are not interested in chasing unrestrained growth again.

The world’s most famous value investor is now also on board. For Buffett, an earnings call Hollub led in February was the turning point. “I read every word, and said this is exactly what I would be doing. She’s running the company the right way,” Buffett told CNBC. Berkshire Hathaway BRK.A, +0.15%

started buying Occidental stock soon after. In August, federal regulators gave Buffett’s company permission to buy up to half of the company. (Asked for comment, a representative of Berkshire Hathaway asked for questions by email but did not respond to them.)

The markets are rife with speculation that Buffett will go all the way and purchase the entire company, though neither Hollub nor Berkshire have said as much. Hollub said simply that Buffett is bullish on oil, so she expects him to invest for the long haul. A Buffett buyout wouldn’t necessarily be a win for the investors who’ve hung on as Occidental’s stock price has recovered. “I’d probably make more money if he doesn’t buy it,” said Smead.

Warren Buffett is back to betting on Hollub and bought 20% of Occidental’s stock this year.

Johannes Eisele/Agence France-Presse/Getty Images

Where Hollub might cause real trouble is in the fight to keep carbon dioxide out of the earth’s atmosphere. That’s not because she’s a climate-denier. Far from it. Like many of her fellow oil-and-gas CEOs in recent years, Hollub has come to see climate change not as a threat to the business, but as an opportunity to be managed.

“I know some people don’t want oil to be produced for very long, but it’s going to be,” Hollub said. For that to change, people have to start using less oil. “It’s not that the more supply we generate, then the more that people are gonna use. It’s all driven by demand,” she said. And even with an electric vehicle in every driveway, we’d still need to extract oil to produce plastics and to create airplane fuel, among other projects that fall under the category of hard-to-abate emissions.