What comes next is a mystery, but I’d like to share a note of appreciation as 2025 fades into history.

If you came to Greater Los Angeles from Mexico, by way of Calexico, Feliz Navidad.

If you once lived in Syria, and settled in Hesperia, welcome.

If you were born in what once was Bombay, but raised a family in L.A., happy new year.

I’m spreading a bit of holiday cheer because for immigrants, on the whole, this has been a horrible year.

Under federal orders in 2025, Los Angeles and other cities have been invaded and workplaces raided.

Immigrants have been chased, protesters maced.

Livelihoods have been aborted, loved ones deported.

With all the put-downs and name-calling by the man at the top, you’d never guess his mother was an immigrant and his three wives have included two immigrants.

Not to be outdone, Homeland Security chief Kristi Noem proposed a travel ban on countries that are “flooding our nation with killers, leeches and entitlement junkies.”

The president’s shtick is to rail mostly against those who are in the country without legal standing and particularly those with criminal records. But his tone and language don’t always make such distinctions.

The point is to divide, lay blame and raise suspicion, which is why legal residents — including Pasadena Mayor Victor Gordo — have told me they carry their passports at all times.

In fact, thousands of people with legal status have been booted out of the country, and millions more are at risk of the same fate.

In a more evolved political culture, it would be simpler to stipulate that there are costs and benefits to immigration, that it’s human nature to flee hardship in pursuit of better opportunities wherever they might be, and that it’s possible to enact laws that serve the needs of immigrants and the industries that rely on them.

But 2025 was the year in which the nation was led in another direction, and it was the year in which it became ever more comforting and even liberating to call California home.

The state is a deeply flawed enterprise, with its staggering gaps in wealth and income, its homelessness catastrophe, housing affordability crisis and racial divides. And California is not politically monolithic, no matter how blue. It’s got millions of Trump supporters, many of whom applauded the roundups.

But there’s an understanding, even in largely conservative regions, that immigrants with papers and without are a crucial part of the muscle and brainpower that help drive the world’s fourth-largest economy.

That’s why some of the state’s Republican lawmakers asked Trump to back off when he first sent masked posses on roundups, stifling the construction, agriculture and hospitality sectors of the economy.

When the raids began, I called a gardener I had written about years ago after he was shot in the chest during a robbery attempt. He had insisted on leaving the hospital emergency room and going back to work immediately, with the bullet still embedded in his chest. A client had hired him to complete a landscaping job by Christmas, as a present to his wife, and the gardener was determined to deliver.

When I checked in with the gardener in June, he told me he was lying low because even though he has a work permit, he didn’t feel safe because Trump had vowed to end temporary protected status for some immigrants.

“People look Latino, and they get arrested,” he told me.

He said his daughter, whom I’d met two decades ago when I delivered $2,000 donated to the family by readers, was going to demonstrate in his name. I met up with her at the “No Kings” rally in El Segundo, where she told me why she wanted to protest:

“To show my face for those who can’t speak and to say we’re not all criminals, we’re all sticking together, we have each other’s backs,” she said.

Mass deportations would rip a $275-million hole in the state’s economy, critically affecting agriculture and healthcare among other industries, according to a report from UC Merced and the Bay Area Council Economic Institute.

“Deportations tend to raise unemployment among U.S.-born and documented workers through reduced consumption and disruptions in complementary occupations,” says a UCLA Anderson report.

I’m a California native whose grandparents were from Spain and Italy, but the state has changed dramatically in my lifetime, and I don’t think I ever really saw it clearly or understood it until I was asked in 2009 to address the freshman convocation at Cal State Northridge. The demographics were similar to today’s — more than half Latino, 1 in 5 white, 10% Asian and 5% Black. And roughly two-thirds were first-generation college students.

I looked out on thousands of young people about to find their way and make their mark, and the students were flanked by a sprinkling of proud parents and grandparents, many of whose stories of sacrifice and yearning began in other countries.

That is part of the lifeblood of the state’s culture, cuisine, commerce and sense of possibility, and those students are now our teachers, nurses, physicians, engineers, entrepreneurs and tech whizzes.

If you left Taipei and settled in Monterey, said goodbye to Dubai and packed up for Ojai, traded Havana for Fontana or Morelia for Visalia, thank you.

Hassle-free returns may be a thing of the past, and if you’re staring at a stack of unwanted Christmas gifts, you may have to think twice before mailing them back.

Several major retailers are now charging customers to return items even if they are unopened and in perfect condition.

Macy’s now charges $9.99 for mail-in returns, while TJ Maxx and Marshalls each charge $11.99.

J. Crew charges $7.50 for mail-in returns, Abercrombie & Fitch charges $7, H&M charges $3.99 and Zara charges $4.95.

It can now cost as much as $45 to return certain electronics at Best Buy.

Amazon has also tightened its policy, charging some customers unless they use its box-free, in-person drop-off option.

According to a report from the National Retail Federation, Americans will return an estimated $850 billion worth of items to stores this year. And nearly 20% of all the things U.S. consumers purchase online are returned, according to the NRF.

David Sobie, who co-founded Happy Returns, a company that uses artificial intelligence robots to help make returns easier, says that the White House’s tariff policies could be to blame.

“Merchants now are under a tremendous amount of cost pressure,” Sobie told CBS News. “…They’re really trying to offset some of the costs that they face in returns by asking shoppers to share some of the burden.”

Sobie advises that the best way to avoid the fees is “to read the retailer’s return policy before you check out in the first place.”

Hassle-free returns may be a thing of the past, and if you’re staring at a stack of unwanted Christmas gifts, you may have to think twice before mailing them back. Dave Malkoff reports.

NEW YORK — The shopping rush leading up to Christmas is over and in its place, like every year, another has begun as millions of people hunt for post-holiday deals and get in line to return gifts that didn’t fit, or didn’t hit quite right.

Holiday spending using cash or cards through Sunday has topped last year’s haul, according to data released this week by Visa’s Consulting & Analytics division and Mastercard SpendingPulse.

But growing unease over the U.S. economy and higher prices in part due to President Donald Trump’s tariffs have altered the behavior of some Americans. More are hitting thrift stores or other discounters in place of malls, according to data from Placer.ai. The firm tracks people’s movements based on cellphone usage.

And they’re sticking more closely to shopping lists and doing more research before buying. That may explain why returns so far are down compared with last year, according to data from Adobe Analytics.

Here are three trends that defined the holiday shopping season so far:

Americans are still spending on gifts, yet increasingly that shopping is taking place at thrift and discount stores, according to data from Placer.ai.

That’s likely forcing traditional retailers such as department stores to fight harder for customers, Placer.ai said.

Clothing and electronics that traditionally dominate holiday sales did have a surge but struggled to grow, according to Placer.ai. Both goods are dominated by imports and thus, vulnerable to tariffs.

For example, traffic doubled in department stores during the week before Christmas, from Dec. 15 through Sunday, compared with the average shopping week this year. But traffic in the week before Christmas this year fell 13.2% compared with 2024.

Traffic surged 61% at traditional sellers of only clothing in the week before the holiday compared with the rest of the year. But again, compared with the runup to Christmas last year, sales slid 9%.

Some of that lost traffic may have migrated to the so-called off-price stores— chains like TJ Maxx. That sector had a sharp seasonal traffic bump of 85.1% and a gain of 1.2% in the week before the holiday.

But it was thrift stores that were red hot, with traffic jumping nearly 11% in the week before Christmas compared with last year.

“Whether hunting for a designer deal or uncovering a one-of-a-kind vintage piece, consumers increasingly favored discovery-driven experiences over the standardized assortments of traditional retail,” Shira Petrack, head of content at Placer.ai, said in a blog post Friday.

In the past it may have seemed gauche to gift your mother a gently used sweater or a pair of pants from a local thrift store, but seemingly not so amid all of the economic uncertainty and rising prices, according to Placer.ai.

Through the second half of 2025, thrift stores have seen at least a 10% increases in traffic compared with last year. That suggests that environmental concerns as well as economic issues are luring more Americans to second-hand stores, Placer.ai said. Visits to thrift stores generally do not take off during the holidays, yet in the most recent Black Friday weekend, sales jumped 5.5%, Placer.ai. reported.

In November, as customer traffic in traditional apparel stores fell more than 3%, traffic in thrift stores soared 12.7%, according to Placer.ai.

The thrift migration has altered the demographics of second-hand stores. The average household income of thrift customers hit $75,000 during October and November of this year, a slight uptick from $74,900 last year, $74,600 in 2023 well above the average income of 74,100 in 2022, based on demographic data from STI:PopStats combined with Placer.ai data.

U.S. sales at thrift chain Savers Value Village’s rose 10.5% in the three months ended Sept. 27 and the momentum continued through October, store executives said in late October.

“High household income cohort continues to become a larger portion of our consumer mix,” CEO Mark Walsh told analysts. “It’s trade down for sure, and our younger cohort also continues to grow in numbers. ”

For the first six weeks of the holiday season, return rates have dipped from the same period a year ago, according to Adobe Analytics.

That suggests that shoppers are doing more research before adding something to their shopping list, and they’re being more disciplined in sticking to the lists they create, according to Vivek Pandya, lead analyst at Adobe Digital Insights.

“I think it’s very indicative of consumers and how conscientiously they’ve purchased,” Pandya said. “Many of them are being very specific with how they spend their budget.”

From Nov. 1 to Dec. 12, returns fell 2.5% compared with last year, Adobe reported. In the seven days following Cyber Week — the five shopping days between Thanksgiving and Cyber Monday, returns fell 0.1%.

From the Nov. 1 through Dec. 12, online sales rose 6% to $187.3 billion, on track to surpass its outlook for the season, Adobe reported.

Between Dec. 26 to Dec. 31, returns are expected to rise by 25% to 35% compared with returns between Nov. 1 through Dec. 12, Adobe said, and it expects returns to remain elevated through the first two weeks of January, up 8% to 15%.

This is the first year that Adobe has tracked returns.

Still, the last week of December sees the greatest concentration of returns: one out of every eight returns in the 2024 holiday season took place between Dec. 26 and Dec 31, a trend expected to persist this year, Adobe said.

The founder of Arts Economics discusses how globalization, new wealth demographics and online sales are reshaping the balance of power in the art world. Paul McCarthy, Courtesy of Arts Economics

Clare McAndrew, featured on this year’s Art Power Index, has done what many thought impossible: she quantified the art market. As the founder of Arts Economics and author of the annual Art Basel and UBS Art Market Report, McAndrew has become the industry’s de facto oracle, translating the art world’s opaque dynamics into data points, patterns and insights. When her report lands each spring, its results ripple across the market—from charting the health of global sales, identifying emerging regions and revealing the settlement behind the numbers.

Over two decades, McAndrew has redefined how the art trade understands itself, applying the rigor of economics to a sector often governed by instinct and perception. Her analyses have shown how concentrated wealth, demographic change and globalization have remodeled the market’s power structures, and how resilience increasingly comes from its peripheries, not its peaks.

This past year was a pivotal one for the global art economy, marked by softening sales at the top end, a surge of activity in the sub-$50,000 segment and a generational shift driven by Gen Z and women collectors. New technologies, direct-to-artist sales and global diversification are transforming the market’s infrastructure, she reports, while also questioning how the boundaries of art are defined as luxury goods and collectibles enter the fold. McAndrew has emerged as an economist who helps markets evolve by revealing how confidence, perception and access shape value in ways that pure data cannot.

What do you see as the most transformative shift in the art world power dynamics over the past year, and how has it impacted your own work or strategy?

Sales in the art market for many years have been driven by an intense focus on a very small number of artists at the high end, which has escalated their prices, while creating higher barriers to entry for new artists and a winner-take-all type market scenario, where the works of the most famous artists are demanded the most, while emerging artists and the galleries and businesses that support them find it harder to generate sales and build careers. Alongside this, as most of what the mainstream media reports on is the multi-million dollar sums paid for this very small number of artists’ works, new buyers are led to believe that the art market is out of their reach, and that you can only get a quality work of art if you have a budget of over $1 million or so, when in fact there are so many other less publicized artists and works available at much lower prices.

These really high-priced sales were critical in driving the recovery of the market from the pandemic, particularly sales of ultra-contemporary and contemporary art, which outperformed other segments by a significant margin. However, a significant shift over the last year is that these are the two areas that have now slowed down the most. The segment of artworks sold for over $10 million has softened both in terms of volumes and value, and some of the bigger businesses have come under more pressure than some of the smaller ones. While this might not radically transform the market’s power dynamics overnight, it has at least shifted the focus away from that very narrow high end and the tiny share of artists it supports. Although some of the recent narrative around the market has been negative—focusing on a lack of eight- and nine-digit sales—there have actually been a growing number of transactions taking place, albeit at lower price levels, which is a positive development.

As the art market and industry continue to evolve, what role do you believe technology, globalization and changing collector demographics will play in reshaping traditional power structures?

My latest report on global collecting highlights the increasingly significant presence of female artists in the market and the growing influence of women as collectors, facilitated in part by shifts in the distribution and growth of wealth. Our research also uncovered the growing dominance of young Gen Z collectors, who were the most active across many of the fine art and collectibles segments. As wealth shifts towards these segments (including large vertical and horizontal transfers of inherited wealth), their preferences will become more dominant and how they want to buy and engage with the market will have a greater impact.

In terms of globalization, one of the key factors supporting the current size and ongoing development of the market is its increasingly global infrastructure, with sales of art literally all around the world and the emergence of a number of new art markets developing over the last 20 years in Asia, the Middle East, Africa and other regions. The global distribution of the art market has altered substantially.

From the 1960s, when Paris lost its central position in the art market, the U.S. dominated sales alongside the U.K., with London and New York accounting for at least three-quarters of the market during the 1980s and 1990s. One of the biggest changes came around 2004/2005 when China emerged as a global player, and with a huge boom in sales there while the rest of the world was suffering in the fallout from the Global Financial Crisis (GFC), making it (temporarily) the biggest market in the world in 2011 (albeit by a small margin). This was made all the more remarkable by the fact that until the death of Mao in 1976, it had been illegal to even own or exchange works of art in China. This injection of sales and the much more global nature of the art market have really protected its aggregate value from downside risks and helped it bounce back much quicker from crises and recessions.

In the market recession in the early 1990s, when it was so solely dominated by the U.S and Europe, it took almost 15 years for the market to get back on its feet, but post-GFC and post-Covid, the bounce back has been much quicker as sales are diversified across so many different regions and segments.

Looking ahead, what unrealized opportunity or unmet need in the art ecosystem are you most excited to tackle in the coming year, and what will it take to make that vision a reality?

There are so many interesting questions to look into about where the market is going, but from a methodological point of view, for my research, one of them I’m trying to focus on going forward relates to defining the boundaries of the market.

I have concentrated most of my research on the traditional art businesses (auction houses and dealers), but there are now a lot more agents involved in the market—artists are selling more directly, with disintermediation enabled through social media and online selling, collectors selling directly to each other, plus other platforms and agents outside of galleries and auction houses. How we account for and measure these sales will become increasingly important in understanding the activity in the sector as a whole, especially when we’re trying to assess its economic and social impact.

There are also continuing changes in what’s being sold in the “art” market, with an expanding range of collectibles and luxury products being sold by dealers and at auction houses, or even within “art”—new digital mediums and channels for accessing these works. The traditional mediums still dominate by value for now, but that could change in the future, and how we measure and expand those boundaries will be a continuing focus for my research in collaboration with academics and experts in the art market over the next few years.

What inspired you to want to bring greater transparency and reliability to a field often described as opaque, mysterious or relationship-driven?

When I first started out, my earliest reports focused on artists, looking at ways they could build better careers (or even just earn a viable income) and how government policies might help or hold them back. I uncovered early in this research that one of the best ways for them to succeed financially was to have a healthy and active market for their work, so my research pivoted to the art trade.

It became clear from working with dealers and auction houses that when they were approaching governments asking for help or changes in regulations to boost the trade, the first questions they would get asked were things like how big is the market, and how many people does it employ. There was a glaring lack of any of this objective industry benchmarking data to answer those questions, which inspired me to try to fill those gaps.

While there is some good, large-scale public data on auctions and exhibitions, many of the transactions in the market are private, so we have to use a very mixed methodological approach, relying heavily on surveys, sentiment testing and other qualitative research methods (alongside quantitative analysis) to build a better picture of the market.

I have increasingly embraced the importance of more qualitative methods and subjective expertise, which is quite different than when I came out of academia and believed that quants, data and econometric modelling could solve most of the market’s problems.All of the metrics and analytical tools that have been developed in the last decade or two in the art market are very useful, as is the increasing amount of data available, but their practical applications in guiding specific decisions have real limits, especially for collectors. There is still nothing really to replace the much more subjective advice you might get from an artist or dealer or advisor to guide the choice of one work over another, so expertise and relationships are still important.

After years of analyzing cycles of boom, correction and resilience, what have you learned about how confidence and optimism—or lack thereof—shape the art market differently than traditional financial markets?

Confidence is critical in the art market, and it relates to one of its most important features—that it is essentially supply-driven. Even if there is really strong demand around, there will only ever be a limited number of total works available on the market at any particular point in time, for all deceased artists, but for living artists too, where there are limits on how much they can really “make to order” in the short run. Rather than being driven by the costs of production or the availability of inputs, art prices are driven by their scarcity value—the factor that increases their relative price based on their low or fixed supply. And because of this scarcity in the market, prices for certain works can catapult up to really high levels when they come onto the market, as buyers try to grasp the really limited opportunities to acquire them.

Things like commodities are traded virtually every second, but in the art market, it’s much slower, and many works have a long market cycle. It can be 20 to 40 years before a work appears again, and some never do. The fact that opportunities to purchase certain works are so limited adds to the scarcity value, and works that are fresh to market or have been kept in private collections for years, for example, can spark a frenzy of interest and generate huge prices when they come up for sale. Increased supply (works coming up for sale) can have a positive, upward effect on prices (and the value of aggregated sales), which is obviously very different from other asset markets where increases in supply drive prices downward.

What this means is that vendor confidence and optimism about the market is key—how potential sellers view the state of the market and whether or not they should put works up for sale really often determines what happens as much as or more than prevailing demand.

On the secondary art market, supply is often generated by some exogenous event (like one of the famous “d’s”—divorce, disaster, death or debt), but where there’s a choice on the timing of the sale, it will often be down to perceptions of the strength of the market. The market can literally talk itself in and out of cycles to some extent.

The top end of the art market is increasingly polarised, with a very small number of artists capturing a large share of value. What risks does this concentration pose for the long-term resilience of the broader market?

This has been an ongoing issue in the market with an intense focus on a very small number of artists at the high end, which has driven up their prices, while creating higher barriers to entry for new artists and a winner-take-all type market scenario. One way to reduce risk and search and validation costs for those buyers unfamiliar with the market is to only purchase well-recognized works or those by really famous artists.

By doing that, you’re basically relying on the established preferences of previously successful buyers who have already bought that artist’s work, reducing their risks and insecurities about relying on your own taste in making the right choice. Collectively, these risk-reducing techniques tend to reinforce the “superstar phenomenon” in the art market, whereby the works of the most famous artists (living or dead) are demanded the most and achieve by far the highest prices in the market, while emerging artists face ever higher hurdles in gaining entry. This isn’t new, and it’s not only in the art market.

In the 1980s, American economist Sherwin Rosen pioneered the study of the economics of superstars and believed that some superstar artists or ‘masters’ reached their position justly because they were more talented, but the differences in their talent versus those less successful were much less than the differences in success. He also felt that some were, in fact, no more talented than their less-recognized peers, but their greater success was driven by the need of consumers for common tastes and culture or to “consume as others are consuming.” The problem associated with the superstar ethos in the art market is not just that it drives up prices, but also that it can deprive other artists of the opportunity to work by concentrating demand.

Alongside this, a lot of the media focus on art is just on the multi-million dollar sums paid for a very small number of artists, so a lot of new buyers can think that the art market is out of their reach, and that you can only get a quality work of art if you have a budget of over $1 million or so, when in fact there’s a huge range of prices and great works available at much lower levels.

I have been looking, in my research, on collecting at the parallel issue in the infrastructure of wealth. In the art market, like other luxury goods, discretionary purchasing power is enabled by greater wealth, and that in turn empowers growth in sales. Over the last couple of years, more wealth has been concentrated in the top 1 percent of society and greater wealth inequality is often linked to stronger purchasing in luxury markets across regions and over time. A higher concentration of wealth in the top percentiles has been a key factor driving strong sales and rising prices at the top of the art market in the past.

While this is most obviously linked to more purchasing by the wealthiest in society, who are more active in luxury markets, inequality can also shift demand in lower wealth tiers. In some cases, more unequal societies can create heightened status competition and anxiety as people become more sensitive to their position in the social and economic hierarchy. This can lead to greater ‘conspicuous consumption’ among those in lower-wealth tiers too, as people try to keep up, or bridge the gap, by imitating the lux spending habits of the wealthy. While this can boost sales in the lower end of art and other luxury markets, it has a range of potentially negative complications, not least being more consumer borrowing and debt accumulation.

As inequality becomes more pronounced, it can also lead to giving up, rather than keeping up, if the perception of upward mobility seems less hopeful or just less attractive. In the extreme, increases in inequality could endanger the market’s potential for long-term development. If consumers in wealth tiers below the very top engage less—or never even start collecting—the market could narrow further and value concentrate more at the top, and this is a segment that recent years have shown to be highly susceptible to wider risks and growth limitations.

On a positive note, while the aggregate figures show that the market has declined by value for two years, the most positive developments have been the growth of sales at the lower and more affordable ends of the market, with the number of artworks sold for prices in the sub-$50,000 expanding, and evidence of success by both dealers and auction houses in reaching new buyers, giving the market a broader and more diversified base for sales. This doesn’t really get focused on, though, in the press, which tends to only look at the big figures, which are so skewed by the tiny, narrow high end.

With the rise of digital channels, new collectible categories and luxury products entering the ‘art’ market—and younger collectors looking beyond traditional fine art, do you have plans to adapt your research and reporting frameworks to capture these newer forms of value and transaction?

Yes, I’m going to be starting new research on the secondary collectibles market that I’m hoping to publish in 2026. It’s a huge market and there’s strong evidence of an expansion in interest in this area over the last few years, especially with young collectors. In my recent research on HNW collectors, about 60 percent of their spending by value over the last year was on fine art, and 40 percent was on collectibles. For Gen Z collectors, just over half of the average spend was collectibles, and their levels were more than five times any other generation group on things like collectible luxury handbags and sneakers.

While some of the diversification in spending might be a reaction to the uncertain environment we’ve been in, it’s also part of a longer-term shift in what people buy, but also how they access the market. Within the art market, we’ve seen a big advance in digital sales following the pandemic, with e-commerce increasing from 9 percent of total sales by value in 2019 to 25 percent in 2020. Although this did settle back a little, the change seems to be more permanent, with a share of 18 percent last year, below the peak, but still double the share of 2019 or any year prior to that. It’s interesting as this is coming alongside greater art fair attendance and gallery exhibition visits compared to prior to the pandemic, so while collectors still want to visit exhibitions and see works in person, when targeting a specific work to purchase, they have become increasingly comfortable with doing so online.

Online channels are key entry points to the market for new buyers too. They have been consistently identified as the main source of new buyers for auction houses, and almost half of the sales dealers made online in 2024 were to new buyers. The expansion of the volume of transactions over the last few years has been facilitated by greater reach through e-commerce, despite the fact that the highest-value sales remained offline.

Outside the traditional art market, there are also more sales taking place directly with artists, on artist-based platforms and between other private agents. Dealers are still the most used channels for buying art in the surveys we conducted on HNW collectors, but there was a big gain in direct sales with artists, with over a third having bought directly from the online, through social media or through a visit to their studios.

The business turning rejected produce into savings and cutting food waste – CBS News

Watch CBS News

Abhi Ramesh launched Misfits Market in 2018, an online grocery store that buys rejected produce from farmers and packages it for sale across the country. Skyler Henry reports.

BANGKOK — Asian shares were mixed Thursday in thin holiday trading, with most markets in the region and elsewhere closed for Christmas.

In Tokyo, the Nikkei 225 lost less than 0.1% to 50,317.43. It has gained nearly 30% this year.

The dollar slipped to 155.70 Japanese yen from 155.94 yen. The euro was unchanged at $1.1780.

Markets in mainland China advanced, with the Shanghai Composite index up 0.3%. Hong Kong’s exchange was closed.

Investors were encouraged by a statement by the People’s Bank of China, China’s central bank, promising to ensure adequate money supply to support financing, economic growth and inflation targets. Earlier in the week, the PBOC had opted to keep its key short-term lending rates unchanged.

Shares fell in Thailand and Indonesia.

On Wednesday, the S&P 500 index rose 0.3% to 6,932.05 and the Dow Jones Industrial Average added 0.6% to close at 48,731.16. The Nasdaq composite added 0.2% to 23,613.31

Trading was extremely light as markets closed early for Christmas Eve and will be closed for Christmas on Thursday. Roughly 1.8 billion shares traded on the New York Stock Exchange on Wednesday, which is roughly a third of the average trading day.

U.S. markets will reopen for a full day of trading on Friday, though volumes will likely remain light this week with most investors having closed out their positions for the year.

The S&P 500 is up more than 17% this year, as investors have embraced the deregulatory policies of the Trump administration and been optimistic about the future of artificial intelligence in helping boost profits for not only technology companies but also for Corporate America.

Much of the focus for investors for the next few weeks will be on where the U.S. economy is heading and where the Federal Reserve will move interest rates. Investors are betting the Fed will hold steady on interest rates at its January meeting.

The U.S. economy grew at a surprisingly strong 4.3% annual rate in the third quarter, the most rapid expansion in two years, driven by consumers who continue to spend despite strong inflation. There have also been recent reports showing shaky confidence among consumers worried about high prices. The labor market has been slowing and retail sales have weakened.

The number of Americans applying for unemployment benefits fell last week and remain at historically healthy levels despite some signs that the labor market is weakening.

U.S. applications for jobless claims for the week ending Dec. 20 fell by 10,000 to 214,000 from the previous week’s 224,000, the Labor Department reported Wednesday. That’s below the 232,000 new applications forecast of analysts surveyed by the data firm FactSet.

Dynavax Technologies soared 38.2% after Sanofi said it was acquiring the California-based vaccine maker in a deal worth $2.2 billion. The French drugmaker will add Dynavax’s hepatitis B vaccines to its portfolio, as well as a shingles vaccine that is still in development.

Novo Nordisk’s shares rose 1.8% after the weight-loss drug company got approval from U.S. regulators for a pill version of its blockbuster drug Wegovy. However, Novo Nordisk shares are still down almost 40% this year as the company has faced increased competition for weight-loss medications, particularly from Eli Lilly. Shares of Eli Lilly are up 40% this year.

U.S. crude oil closed at $58.35 a barrel and Brent crude finished at $61.80 a barrel.

WASHINGTON — The average rate on a 30-year U.S. mortgage ticked down modestly this week, remaining in the same narrow range of the past two months.

The average long-term mortgage rate fell to 6.18% from 6.21% last week, mortgage buyer Freddie Mac said Wednesday. A year ago, the rate averaged 6.85%.

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners refinancing their home loans, rose this week. The rate averaged 5.50%, up from 5.47% last week. A year ago it averaged 6%, Freddie Mac said.

Mortgage rates are influenced by several factors, from the Federal Reserve’s interest rate policy decisions to bond market investors’ expectations for the economy and inflation. They generally follow the trajectory of the 10-year Treasury yield, which lenders use as a guide to pricing home loans.

The 10-year yield was at 4.15% at midday Wednesday, up modestly from last week’s 4.12%.

The average rate on a 30-year mortgage has been mostly holding steady in recent weeks since Oct. 30 when it dropped to 6.17%, its lowest level in more than a year.

Mortgage rates began easing in July in anticipation of a series of Fed rate cuts, which began in September and continued this month.

The Fed doesn’t set mortgage rates, but when it cuts its short-term rate that can signal lower inflation or slower economic growth ahead, which can drive investors to buy U.S. government bonds. That can help lower yields on long-term U.S. Treasurys, which can result in lower mortgage rates.

Even so, Fed rate cuts don’t always translate into lower mortgage rates.

Home shoppers who can afford to pay cash or finance at current mortgage rates are in a more favorable position than they were a year ago. Home listings are up sharply from last year, and many sellers have resorted to lowering their initial asking price as homes take longer to sell, according to data from Realtor.com.

Still, affordability remains a challenge for many aspiring homeowners, especially first-time buyers who don’t have equity from an existing home to put toward a new home purchase. Uncertainty over the economy and job market are also keeping many would-be buyers on the sidelines.

Sales of previously occupied U.S. homes rose in November from the previous month, but slowed compared to a year earlier for the first time since May despite average long-term mortgage rates holding near their low point for the year. Through the first 11 months of this year, home sales are down 0.5% compared to the same period last year.

Economists generally forecast that the average rate on a 30-year mortgage will remain slightly above 6% next year.

The U.S. economy has been tested by a barrage of challenges in 2025, from sharply higher U.S. tariffs that drove up inflation and rattled consumer confidence, to rising unemployment amid a slowdown in hiring.

Despite those headwinds, the economy has continued to chug along, defying early-year warnings from some economists that the nation could be headed for a recession or that the Trump administration’s tariffs would reignite runaway inflation.

The biggest surprise of the year has been the economy’s durability, according to experts. Economic growth has surged to its fastest pace in two years, inflation has risen less than feared and the stock market has climbed to fresh highs.

“This has been another year of resilience for the economy,” Oxford Economics chief U.S. economist Michael Pearce told CBS News. “The economy has grown at a pretty steady pace.”

Yet Pearce hastens to add that the economy, although it has navigated some tricky waters, is “not spectacular” as the year comes to a close, assigning it a grade of a B or B-. Other experts who spoke with CBS News also graded the economy in the B range.

That may strike many consumers as generous. Three-quarters of Americans surveyed by CBS News earlier this month said they would give the U.S. economy a C, D or F, while just 25% assigned it an A or a B. Recent consumer confidence surveys also indicate that many Americans are downbeat about the economy, mainly due to stubbornly high prices.

The disconnect partly reflects the differences in how consumers and economists tend to judge the nation’s economic performance. While financial pros tend to focus on macroeconomic indicators such as GDP, inflation and unemployment, consumers are more likely to assess the economy based on pocketbook issues like food prices and health care costs — both of which have risen in 2025.

The White House said the economy has improved from last year under former President Joe Biden.

“Although much work remains, the American economy is leaps… better now than it was a year ago under Joe Biden: cooled inflation, private-sector job growth, cheaper essentials like gas, lower taxes, and trillions in investments flowing in to make and hire in America,” White House spokesman Kush Desai said in a statement to CBS News.

He added, “As President Trump’s economic agenda continues taking effect, Americans can rest assured that 2026 will be even better.”

A turbulent year

The economy has been marked by pronounced volatility and uncertainty in 2025, ranging from the Trump administration’s wide-ranging tariffs to an alarming downturn in growth in the first three months of the year.

“It’s rare that we’ve seen a president come in and, with a unified Congress, have such immediate impacts on the economy,” Pearce said. “Not all of those are impacting the economy right away, but we’ve seen a lot of those policies generate a lot of uncertainty.”

For instance, the Republicans’ “big beautiful bill” act, signed into law by Mr. Trump on July 4, will likely impact the economy in 2026, with consumers expected to receive juicier tax refunds.

Other effects of the new law could work against some consumers. Perhaps most concerning is the expiration of Affordable Care Act enhanced tax credits, which experts warn will sharply drive up health insurance premiums for millions of Americans.

Meanwhile, it’s been a banner year for investors as the boom in artificial intelligence pushed the stock market to a succession of record highs. At the same time, the bullish sentiment on Wall Street has fueled questions about whether a possible AI bubble could turn to bust if the enormous investment in the technology fails to deliver the promised gains in productivity and corporate profits.

Life on the “K”

Economic turmoil often impacts consumer sentiment, making people feel less confident about their finances, economists have long noted. That dynamic has led experts to describe the economy this year as “K-shaped,” in which higher-income consumers spend robustly — thanks in part to the strong stock market — even as lower- and middle-income consumers pull back.

And it’s no wonder. Although inflation has cooled since peaking at a 40-year high in 2022, prices remain elevated, squeezing many Americans and making it hard for them to cover even basic expenses, Mark Luschini, chief investment strategist at wealth management firm Janney Montgomery Scott, told CBS News.

It isn’t just routine purchases that are straining consumers — it’s also the barriers in the way today of reaching once ordinary financial goals, such as buying a first home, saving for retirement or even just paying off debt, added Chen Zhao, head of economic research at online real estate firm Redfin.

When it comes to homeownership, evidence of that barrier is visible in the median age of first homebuyers today — that hit 40 this year, a record high, according to the National Association of Realtors. With home values near all-time highs and mortgage rates hovering around 6.3%, many younger Americans are feeling priced out, she said.

“This situation that we’re in right now, where [housing] affordability has gotten to be the worst it’s really ever been in recent memory — and significantly worse than before the pandemic — it’s really unfortunate for the younger generation,” Zhao said. “It means delaying the American dream for a lot of folks.”

In 160 U.S. cities, at least one-fifth of middle-class residents can’t afford to live in that area, after factoring in local income levels and price differences, according to Brookings, a nonpartisan think tank.

Hiring slowdown

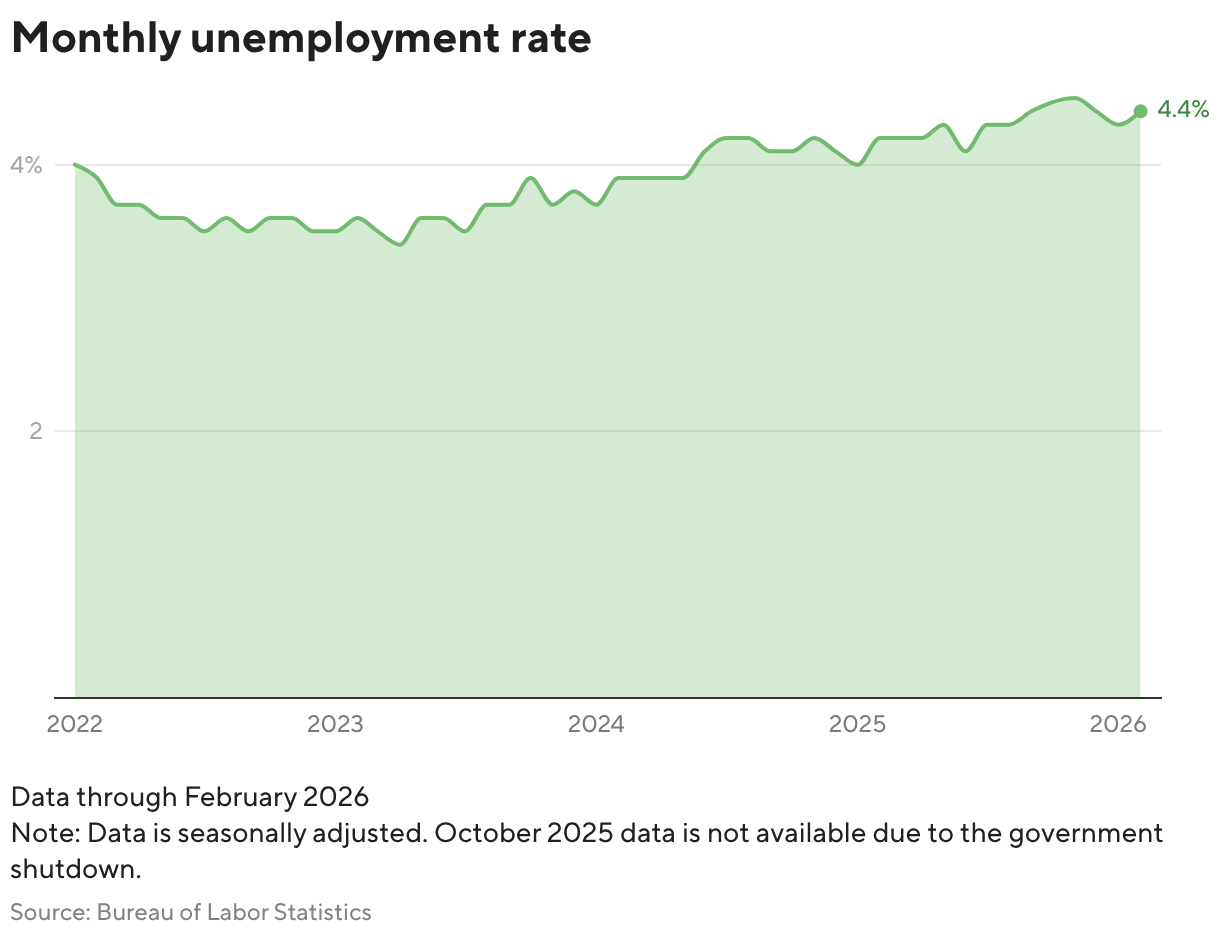

Another pressure point is the labor market, where hiring has slowed throughout 2025. The U.S. unemployment rate rose to 4.6% in November, its highest level in four years.

Layoffs also jumped to 1.1 million this year through November, up 54% from a year earlier and the highest level since 2020, according to outplacement firm Challenger, Gray & Christmas.

While job seekers are finding it tougher to get a foothold in today’s labor market, it’s proving particularly challenging for young people, who are facing a decline in job listings and competition from more experienced workers, experts said.

Cooling job growth in the second half of the year is partially a reflection of persistent economic uncertainty, which has led many businesses to throttle hiring. Some businesses are also trimming jobs as they invest in AI, which can perform some tasks previously handled by employees.

“Any type of uncertainty is going to lead to slower business decisions, whether it’s hiring or investment,” Greg Daco, chief economist at consulting firm EY-Parthenon, told CBS News.

Labor market headwinds in 2025 have prompted the Federal Reserve to cut its benchmark interest rate three straight times since September. By lowering borrowing costs, the Fed is aiming to encourage businesses to expand and hire.

Slower hiring and rising layoffs could pose a risk to consumer spending, which drives nearly two-thirds of economic activity, economists note.

“A slower labor market leads to slower income growth, which eventually ends up pulling consumer spending lower,” Daco said.

Muted tariff impact

One of the biggest economic surprises of 2025 came with President Trump’s sweeping tariffs, announced in April on what he termed “liberation day.” The plan caused U.S. stocks to plunge and stoked fears that the levies would reignite inflation.

Yet despite such concerns, tariffs so far have had a more muted impact on inflation than initially feared. That’s partly because U.S. companies, which pay the import duties to the federal government, stockpiled goods before the tariffs kicked in and absorbed some of the costs rather than passing them on to consumers.

“Generally speaking, the economy outperformed expectations in the face of several large supply shocks,” Daco said.

Still, inflation remains sticky. The Consumer Price Index, which stood at 3% in January, remains near the same level as of November. Oxford Economics’ Pearce estimates that the stepped-up import duties added 0.5 percentage points to the nation’s inflation rate this year.

HONG KONG — Asian markets mostly advanced Wednesday after the benchmark S&P 500 closed at another record high following a report that the U.S. economy grew at an unexpectedly strong 4.3% annual rate in July to September.

The U.S. government’s first estimate of growth for the third quarter showed inflation remained high, while a separate report said consumer confidence faded further in December. The U.S. economy expanded at a 3.8% annual pace in April-June.

Trading in Asia was thin, with many global markets due to be closed Thursday for Christmas. Markets in the U.S. will end early Wednesday for Christmas Eve and stay closed for Christmas.

Tokyo’s Nikkei 225 was unchanged at 50,411.10 and South Korea’s Kospi slipped 0.1% to 4,113.83.

In Chinese markets, Hong Kong’s Hang Seng gained 0.2% to 25,818.93. The Shanghai Composite index edged 0.2% higher, to 3,929.25.

In Australia, the S&P/ASX 200 slipped nearly 0.4% to 8,762.70.

Markets in Hong Kong and Australia closed early due to Christmas Eve.

Taiwan’s Taiex picked up less than 0.1% while the Sensex in India gained 0.1%.

Gold and silver extended their rally after hitting record highs this week driven by heightened geopolitical tensions. The price of gold rose 0.4% early Wednesday to $4,525.50 per ounce, adding to gains of about 70% for the year. Silver rose 1.8%.

U.S. futures edged lower early Wednesday.

On Tuesday, big gains for tech stocks pushed the S&P 500 up 0.5%, even though most stocks in the index fell. It closed at 6,909.79. The Dow Jones Industrial Average added 0.2% to 48,442.41, while the Nasdaq composite rose 0.6% to 23,561.84.

Nvidia advanced 3% and Google’s parent company, Alphabet, edged up 1.5%.

The government’s update on the economy showed inflation hovering higher than the central bank prefers. The Federal Reserve’s favored inflation gauge — called the personal consumption expenditures index, or PCE — climbed to a 2.8% annual pace last quarter, up from 2.1% in the second quarter.

On Wednesday, the Labor Department will release its weekly data on applications for jobless benefits, which stands as a proxy for U.S. layoffs.

Investors are betting the Fed will hold steady on interest rates at its January meeting. Recent reports show high inflation and shaky confidence among consumers worried about high prices. The labor market has been slowing and retail sales have weakened.

In other dealings early Wednesday, the dollar continued to fall against the Japanese yen, after officials said they could intervene with excessive moves in the yen. The dollar was trading Wednesday at 155.96 yen, down from 156.17 yen.

The euro slipped to $1.1793 from $1.1796.

Oil prices edged higher as traders kept an eye on risks of supply disruptions in Venezuela and Russia.

U.S. benchmark crude oil added 7 cents to $58.45 per barrel. Brent crude edged 3 cents higher, to $61.90 per barrel.

___

AP Business Writer Damian J. Troise contributed to this story.

Between now and 2030, about 10,000 Americans will turn 65 every single day, giving rise to a term known as the “sandwich generation” — adults who find themselves caring for their aging parents while still raising their own children. CBS News spoke to one woman about her struggles.

WASHINGTON (AP) — The U.S. economy economy expanded at a strong 4.3% annual rate from July through September as consumer spending, exports and government spending all grew.

Tuesday’s report from the Commerce Department said U.S. gross domestic product — the economy’s total output of goods and services — up from its 3.8% growth rate in the April-June quarter.

Analysts surveyed by the data firm FactSet forecast growth of 3% in the period.

However, inflation remains higher than the Federal Reserve would like.

The Fed’s favored inflation gauge — called the personal consumption expenditures index, or PCE — climbed to a 2.8% annual pace last quarter, up from 2.1% in the second quarter.

American consumers in December remained downbeat about the state of the economy, a new survey shows.

The Conference Board, a nonprofit group representing businesses, said Tuesday that its consumer confidence index fell 3.8 points to 89.1 in December, from November’s upwardly revised reading of 92.9. The latest figures are close to the group’s reading in April, when President Trump announced tariffs on dozens of U.S. trading partners.

“Despite an upward revision in November related to the end of the shutdown, consumer confidence fell again in December and remained well below this year’s January peak. Four of five components of the overall index fell, while one was at a level signaling notable weakness,” Dana Peterson, chief Economist at The Conference Board, said in a statement.

A measure of Americans’ short-term expectations for their income, business conditions and the job market remained stable at 70.7, but still well below 80, the marker that can signal a recession ahead. It was the 11th consecutive month that reading has come in under 80.

Consumers’ assessments of their current economic situation tumbled 9.5 points to 116.8. Write-in responses to the survey showed that prices and inflation remained consumers’ biggest concern, along with tariffs.

Perceptions of the job market also declined this month. The conference board’s survey reported that 26.7% of consumers said jobs were “plentiful,” down from 28.2% in November. Also, 20.8% of consumers said jobs were “hard to get,” up from 20.1% last month.

“Consumers’ write-in responses on factors affecting the economy continued to be led by references to prices and inflation, tariffs and trade and politics,” Peterson said. “However, December saw increases in mentions of immigration, war and topics related to personal finances — including interest rates, taxes and income, banks, and insurance.

Americans remain generally sour about the economy, with most grading the nation’s economic performance this year as either a “C” or “D” or worse, according to a recent CBS News poll.

“Consumer confidence continued to tumble at the end of the year, as higher prices, a weaker labor market and the waning impact of the government shutdown weighed on household perceptions of the economy,” Matthew Martin, senior U.S. economist at investment adviser Oxford Economics, said in a report.

“Consumers’ perceptions of the current state of the economy are at their lowest point in five years,” he added.

Consumers still spending

Consumer sentiment continued to ebb last month even as the economy accelerated. Federal data released on Tuesday showed the nation’s gross domestic product expanded at a blistering 4.3% annual pace in the third quarter, up from 3.8% in the previous quarter and the strongest rate of growth in two years.

“The latest GDP data confirm that even though consumer confidence is slipping, consumers are still spending,” Carl Weinberg, chief economist at High Frequency Economics, said in a report. “The disconnect must mean that incomes are rising briskly. But the payroll report says incomes are slowing. So the data are not sending a clear message right now.”

Consumer spending accounts for roughly two-thirds of economic activity.

Last week, the Labor Department reported that the U.S. economy gained a healthy 64,000 jobs in November but lost 105,000 in October. The unemployment rate rose to 4.6% last month, the highest since 2021. Since March, job creation has fallen to an average 35,000 a month, compared to 71,000 in the year ended in March.

WASHINGTON — Consumers confidence in the economy was shaken in December as Americans grow anxious about high prices and the impact of President Donald Trump’s sweeping tariffs.

The Conference Board said Tuesday that its consumer confidence index fell 3.8 points to 89.1 in December from November’s upwardly revised reading of 92.9. That is close to the 85.7 reading from April, when Trump rolled out his import taxes on U.S. trading partners.

A measure of Americans’ short-term expectations for their income, business conditions and the job market remained stable at 70.7, but still well below 80, the marker that can signal a recession ahead. It was the 11th consecutive month that reading has come in under 80.

Consumers’ assessments of their current economic situation tumbled 9.5 points to 116.8.

Write-in responses to the survey showed that prices and inflation remained consumers’ biggest concern, along with tariffs, despite repeated claims by President Trump that inflation is a hoax.

Perceptions of the job market also declined this month.

The conference board’s survey reported that 26.7% of consumers said jobs were “plentiful,” down from 28.2% in November. Also, 20.8% of consumers said jobs were “hard to get,” up from 20.1% last month.

Last week, the government reported that the U.S. economy gained a healthy 64,000 jobs in November but lost 105,000 in October. Notably, the unemployment rate rose to 4.6% last month, the highest since 2021.

The country’s labor market has been stuck in a “low hire, low fire” state, economists say, as businesses stand pat due to uncertainty over Trump’s tariffs and the lingering effects of elevated interest rates. Since March, job creation has fallen to an average 35,000 a month, compared to 71,000 in the year ended in March. Fed Chair Jerome Powell said recently that he suspects those numbers will be revised even lower.

Despite the broad pessimism, the proportion of those surveyed who think a recession in the next year is is unlikely grew.

The December survey showed that respondents’ views of their family’s current financial situation sank into negative territory for the first time in close to four years. On the flip side, expectations about their future financial situation were the most positive since January.

Also Tuesday, the government reported that the economy expanded at a 4.3% annual rate in the third quarter, though economists expect a much more sluggish fourth quarter.