[ad_1]

U.K. retail sales fell 0.9% in September vs. expectations for 0.4% drop

[ad_2]

[ad_1]

The numbers: Home sales in September fell to the lowest level since 2010, as high mortgage rates continue to hammer the housing market.

Aside from low inventory, rising rates are eroding buyers’ purchasing power, and drying up demand. Sales of previously owned homes fell by 2% to an annual rate of 3.96 million in September, the National Association of Realtors said Thursday.

That’s the number of homes that would be sold over an entire year if sales took place at the same rate every month as they did in September. The numbers are seasonally adjusted.

The drop in sales was slightly better than what Wall Street was expecting. They forecasted existing-home sales to total 3.9 million in September.

Compared to September 2022, home sales are down by 15.4%.

Key details: The median price for an existing home in September rose for the third month in a row to $394,300. Prices are up 2.8% from a year ago. That was the highest price for the month of September since NAR began tracking the data.

Home prices peaked in June 2022, when the median price of a resale home hit $413,800.

Around 26% of properties are being sold above list price, the NAR noted.

The total number of homes for sale in September fell by 8.1% from last year, to 1.13 million units. Housing inventory for the month of September was the lowest since 1999, when the NAR began tracking the data.

Homes listed for sale remained on the market for 21 days on average, up from the previous month. Last September, homes were only on the market for 19 days.

Sales of existing homes rose only in the Northeast in September, as compared with the previous month, by 4.2%. The median price of a home in the region was $439,900.

All-cash buyers made up 29% of sales, highest since January 2023. The share of individual investors or second-home buyers was 18%. About 27% of homes were sold to first-time home buyers.

Big picture: The U.S. housing market is in the midst of a serious slowdown that is primarily driven by high mortgage rates. High rates spook home buyers, drying up demand, and high rates also deter homeowners from selling since they may have to purchase another home. For a homeowner with a 3% mortgage rate for the next few decades, there’s little incentive to move.

And the residential sector is likely to see sales fall further in October’s data, as the 30-year mortgage inches even higher. Demand for mortgages has collapsed, and some outlets like Mortgage News Daily are quoting a rate of 8% for the 30-year.

Existing-home sales in 2023 could fall to the slowest pace since the housing bubble burst in 2008, real-estate brokerage Redfin said on Thursday, at a 4.1 million pace.

What the realtors said: “Mortgage rates and limited inventory has been the story throughout this year — no different this month, other than the fact that interest rates are moving higher,” said Lawrence Yun, chief economist at the National Association of Realtors.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” he added. “We don’t want the Fed to overdo it and cause great harm to real estate.”

Yun also questioned whether there will be a “fundamental change” or a temporary one to the “American way of life” due to the slowdown in sales.

Market reaction: Stocks were down in early trading on Thursday. The yield on the 10-year note

BX:TMUBMUSD10Y

rose above 4.9%.

[ad_2]

[ad_1]

Call it the mystery of the rising 10-year yield—and it’s led investors straight to the so-called ‘ Treasury Term Premium .’

[ad_1]

Developing story. Check back for updates.

The numbers: Sales at U.S. retailers jumped a bigger-than-expected 0.7% in September in a sign households have enough buying power to keep the economy expanding.

The increase was spurred by strong demand at auto dealers and Internet stores. Higher gas prices also played a role, however.

Economists polled by The Wall Street Journal had forecast a 0.2% increase in sales.

Retail sales represent about one-third of all consumer spending and usually offer clues on the strength of the economy.

Yet September also falls between the busy back-to-school and holiday-shopping seasons and tends to reveal less about how consumers are doing.

Key details: Auto dealers posted a 1% gain in sales and helped to inflate the headline number. Auto sales account for about 20% of all retail sales.

Receipts at gas stations also rose nearly 1%, but that largely reflected higher gas prices. That’s not a good thing for households.

Retail sales advanced a still-robust 0.6% when car dealers and gas stations are set aside, which gives a better idea of consumer demand.

Sales at internet retailers stayed on a hot streak. They rose 1.1%.

Sales climbed 0.9%% at bars and restaurants. Restaurant sales tend to rise when the economy is healthy and Americans feel secure in their jobs. Sales decline during times of economic stress.

Over the past year, restaurant sales have surged 9.2% — more than twice as fast as inflation.

On the negative side of the ledger, sales fell at big-box electronics stores, clothing stores and home centers such as Home Depot

HD,

and Lowe’s

LOW,

Sales in August were also revised up to show a 0.8% increase instead of 0.6%.

Big picture: The retail sales report is the latest to suggest the economy is still expanding at solid pace and perhaps not decelerating as much as the Federal Reserve would like to help slow the rate of inflation.

Consumer spending has stayed fairly healthy because of rising wages and the lowest unemployment rate in decades. What’s more, incomes are finally increasing faster than inflation for the first time in a few years.

Yet higher interest rates are pinching households and businesses and are bound to slow the economy in the months ahead. If so, retail spending is also likely to soften.

Looking ahead: “Consumer spending shows little sign of flagging, especially when purchases increased on everything from durable goods, such as autos, to the least durable goods, food and drink at bars and restaurants,” said Robert Frick, corporate economist at Navy Federal Credit Union.

“As long as the jobs market remains healthy, consumers should have the cash and confidence to maintain spending.”

Market reaction: Before the markets opened, the Dow Jones Industrial Average

DJIA

and S&P 500

SPX

were set to open lower in Tuesday trades.

[ad_2]

[ad_1]

Rep. Jim Jordan made progress Monday in his push to become the next speaker of the House of Representatives, winning endorsements from some fellow Republicans who just last week had refused to back him.

The narrowly divided chamber of Congress is expected to vote around noon Eastern Tuesday to select a speaker, with the move coming after former Speaker Kevin McCarthy was ousted two weeks ago and after No. 2 House Republican Steve Scalise ended his bid for the post last week.

GOP Rep. Ann Wagner of Missouri, who previously said a Jordan speakership was a non-starter for her, switched her stance on Monday. She said in a post on X that her colleague from Ohio “has allayed my concerns about keeping the government open with conservative funding, the need for strong border security, our need for consistent international support in times of war and unrest … as well as the need for stronger protections against the scourge of human trafficking and child exploitation.”

Similarly, GOP Rep. Mike Rogers of Alabama, who chairs the House Armed Services Committee, announced in a post on X that he was backing Jordan after saying last week that there was nothing that Jordan could do to win his support. Rogers pointed to an accord on an annual Pentagon bill, the National Defense Authorization Act, saying he and Jordan had “agreed on the need for Congress to pass a strong NDAA, appropriations to fund our government’s vital functions, and other important legislation like the Farm Bill.”

Republican Rep. Vern Buchanan of Florida offered his support for Jordan as well on Monday, though he noted that he’s “deeply frustrated by the way this process has played out.” Another endorsement came from GOP Rep. Ken Calvert of California, who chairs the House Appropriations Committee’s defense subpanel.

Jordan — who has been endorsed by former President Donald Trump — sent a letter to his colleagues in which he called for coming together after a chaotic two weeks, saying: “It is time we unite to get back to work on behalf of the American people.” The congressman, a co-founder of the hardline House Freedom Caucus and chairman of the House Judiciary Committee, also told CNN that he was confident about Tuesday’s vote, saying: “I feel good about it.”

Analysts have been warning that the process of finding a replacement for McCarthy is preventing the House from addressing crucial matters, such as avoiding a government shutdown next month and supporting Israel in its war against Hamas.

House Republicans made Jordan their nominee for speaker on Friday, but he drew just 124 votes while 81 lawmakers backed another candidate for speaker, GOP Rep. Austin Scott of Georgia. In another round of voting on Friday, Jordan still had 55 colleagues voting against him, but he now appears to be flipping some of them to his side.

One betting market, Smarkets, was giving Jordan a 33% chance of becoming speaker.

Having Jordan as speaker could mean a 1% cut in defense

ITA

and non-defense spending, noted Philip Wallach, senior fellow at the American Enterprise Institute, a conservative think tank. That’s because this year’s debt-limit deal includes a provision that calls for such reductions if there aren’t bipartisan agreements on a dozen funding bills before Jan. 1 and instead a reliance on short-term measures known as continuing resolutions, or CRs.

“It is now clear,” Wallach said during an AEI event on Monday, that Jordan’s “plan is to have us live off continuing resolutions and implement this 1% cut.”

“That’s a concrete thing where he could say, ‘Well, we’re moving in the right direction. We’ve taken a hard stand,’” the AEI expert added.

The CEO of one financial advisory firm also sees standoffs in the future.

“We expect the next U.S. speaker will be less inclined to make deals than McCarthy; in many ways it makes more sense for them, politically, not to be a deal-maker in the current environment,” said deVere Group’s Nigel Green in a statement.

“We believe that a U.S. government shutdown is now more likely with a new speaker of the House, and this has the potential to create a domino effect in global financial markets

SPX.

”

BTIG analysts Isaac Boltansky and Isabel Bandoroff said the speaker drama suggests that next year’s election will also be full of twists and turns.

“We have followed every twist and turn of the speakership race, and there is only one takeaway we can share with absolute certainty: This confirms that the 2024 election cycle will be exhausting, volatile, and just downright weird from beginning to end,” they wrote in a note.

COMP

closed higher Monday, as investors looked ahead to earnings season and unwound the flight-to-safety trades seen last week on fears the Israel-Hamas war could escalate into a wider conflict.

[ad_2]

[ad_1]

PHILADELPHIA — High mortgage rates are hammering home buyers, but expect rates to fall over the next year, one industry group says.

Mortgage rates are over 7.5% as of mid-October, but expect rates to fall to 6.1% by the end of 2024, according to a forecast by the Mortgage Bankers Association. The group also expects the 30-year mortgage rate to fall to 5.5% by the end of 2025.

A big driver pushing down rates will be a slowing U.S. economy, Mike Fratantoni, chief economist and senior vice president at the MBA, said during the group’s annual convention in Philadelphia on Sunday.

Not only is the group expecting a recession in the first half of 2024, but the MBA also forecasts unemployment to rise and inflation to slow, which are signs of a weakening U.S. economy. That will, in turn, push rates down, as the market will expect the Fed to back off on hiking interest rates, they said.

“The Fed’s hiking cycle is likely nearing an end, but while Fed officials have indicated that additional rate hikes might not be needed, rate cuts may not come as soon or proceed as rapidly as previously expected,” Fratantoni said.

Consequently, mortgage lenders could see origination volume to increase 19% in 2024, to $1.95 trillion from the $1.64 trillion expected this year. Purchase originations are expected to rise by 11%, the MBA said.

The pandemic years were boom times for the mortgage industry. 2021 was a record year, when $4.4 trillion in mortgages were originated.

But after the Fed began hiking interest rates in the middle of 2022, surging rates have put a damper on home-buying activity. Homes are far more expensive to purchase due to high rates, with the median principal and interest payment rising to $2,170 in August, compared to $1,284 in August 2021, according to MBA data.

Fratantoni on Sunday said that he believed the “Fed is done” with rate hikes. There are two Fed meetings left this year. The MBA said it does not expect the Fed to hike interest rates in November, and to potentially hold off in December, depending on the data.

But for now, lenders should brace for “a little bit more pain” for the next few months, which is generally a slower season for home sales, until a turnaround at the end of spring in 2024, Marina Walsh, vice president of industry analysis at the MBA, said during a presentation.

Home prices will still continue to rise over the next three years, the MBA added, due to the persistence of tight inventory.

Millennials are entering their prime home-buying years, said Joel Kan, deputy chief economist at the MBA, which will keep prices from falling.

“The forecast is for low single-digit growth over the next few years supported by [low] inventory,” he said. “We’re not expecting national declines yet.”

[ad_2]

[ad_1]

The volatility in the world’s biggest bond market in recent weeks has been too much for U.S. stocks to handle as investors come to terms with the likelihood that interest rates will remain high deep into 2024 until underlying inflationary pressures ease.

The U.S. Treasury market, the bedrock of the global financial system, has been hammered by repeated selling since late September, sending the yields on the 10-year and 30-year Treasurys to levels last seen when the economy was moving toward the financial crisis in 200, before yields fell again in the past week.

Back in September a bond market selloff was fueled by a hawkish outlook from the Federal Reserve, along with mounting concern about the U.S. fiscal deficit and federal debt amid the potential for a government shutdown if a budget for the 2024 fiscal year is not settled by mid-November.

Earlier this week though, increased uncertainty about the conflict in the Middle East propelled demand for safer assets and caused longer-term bond prices to jump and their yields to fall.

Then, on Thursday, a Treasury bond auction which saw a pullback in demand despite notably higher yields, sent longer-term rates higher again while investors were already digesting inflation data that showed consumer prices remained elevated in September. The U.S. stocks fell and booked their worst day in five sessions on Thursday.

Investors are now wondering what it will take for interest rates and bond yields to fall in the months ahead and whether a retreat in yields could eventually push stocks higher to rally into the year-end.

Tim Hayes, chief global investment strategist at Ned Davis Research, said “excessive pessimism” in the bond market is setting up for a relief rally both in stock and bond prices as “there’s not as much inflationary pressures as the market has been pricing in,” he told MarketWatch in a phone interview on Thursday.

Hayes said his team found the bond sentiment data has started to reflect a “decisive reversal” away from too much pessimism in the Treasury market which could send bond yields lower and boost equities given the inverse correlations between the S&P 500

SPX

and the 10-year Treasury note yield

BX:TMUBMUSD10Y.

See: Here is what needs to happen for the S&P 500 to hold on to this year’s gains

Meanwhile, some analysts said disinflation may not be enough for the Federal Reserve to drop its “higher-for-longer” interest rate narrative which was primarily responsible for the big spike in yields since September.

The economy needs a slowdown in the consumer sector for some relaxation in the Fed’s “higher-for-longer” narrative and to maybe push policymakers to adopt a more flexible outlook for its long-term guidance, said Thierry Wizman, global FX and interest rates strategist at Macquarie.

“Of course, the Fed right now is certainly not saying anything that’s remotely suggestive of ‘high-for-long’ being taken away or being removed or negated, so I don’t expect yields to fall a lot unless we start to get reasons to believe the Fed is going to remove that narrative based on the economic data,” Wizman told MarketWatch via phone.

However, Wizman said he is confident that the U.S. consumption data will weaken over the next few months when major consumer-product and -service companies start to provide guidance for the fourth quarter, and when U.S. consumers, which have been trapped in a web of conflicting signals on the health of the economy, open their wallet for the holiday shopping season.

“This will produce some weakness on the consumer side of the market and there’s no doubt the slowdown will be more pronounced than most people expect in the economy, [but] that will be the positive scenario for bonds,” said Marco Pirondini, head of U.S. equities at Amundi U.S., in an interview with MarketWatch.

However, that also means investors should not be “too anxious to buy dips in the stock market” because it would be very unusual if the stock market doesn’t see “multiple compression” with Treasury yields at 16-year highs, Wizman said. “Stocks would still look too rich even if the Fed drops the ‘higher-for-longer’ narrative in the first quarter of 2024.”

See: Fed skips rate hike for now, but doesn’t rule out another increase this year

The “higher-for-longer” mantra is an idea Fed officials have tried to get the market to absorb in recent months, with Fed Chair Powell hardening his rhetoric at the September FOMC meeting, pointing potentially to more rate hikes or, more importantly, interest rates that stay higher for longer.

Fed officials saw interest rates coming down to 5.1% in 2024, higher than June’s outlook for rates to finish next year at 4.6%, according to the latest Summary of Economic Projections at the September policy meeting.

See: Stock-market moves show bond traders are still in charge as yields renew rise

However, Wizman characterized the “higher-than-longer” narrative as a “publicity stunt,” as he thought Fed officials simply wanted to signal to the market that they were frustrated that financial conditions hadn’t measurably tightened enough in 2023, so they utilized the narrative to get rising Treasury yields to do some of the “heavy lifting.”

“… Fed officials are not really serious about ‘higher-for-longer’ – they just did it to drive long-term yields higher for now,” he added.

If a slowdown in the consumer sector of the economy and ongoing disinflation are powerful enough to sap Fed’s rate expectations, Treasury yields could continue to decline without having to have a calamity or big recession in the U.S. economy to drive investors back to the safe-haven assets like Treasurys, strategists said.

See: U.S. stock-market seasonality suggests a potential rally in the fourth quarter. Why this time might be different.

Meanwhile, stock-market seasonality may also help lift sentiment. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the large-cap S&P 500 index up nearly 80% of the time dating back to 1950 and gaining more than 4% on average.

The S&P 500 has risen 0.9% so far in the fourth quarter, while the Dow Jones Industrial Average

DJIA

is up 0.5% and the Nasdaq Composite

COMP

has advanced 1.4% in October, according to FactSet data.

“So you have this situation where sentiment got stretched and now sentiment is reversing with more confidence that bond yields have reached their peak, so equities can rally moving into the end of the year, and that should start to become increasingly evident,” said Hayes.

The yield on the 10-year Treasury note dropped 8.2 basis points to 4.628% on Friday, while the yield on the 30-year Treasury

BX:TMUBMUSD30Y

declined by 9.2 basis points to 4.777%. The 30-year yield fell 16.4 basis points this week, its largest weekly drop since the period that ended March 10, according to Dow Jones Market Data.

[ad_2]

[ad_1]

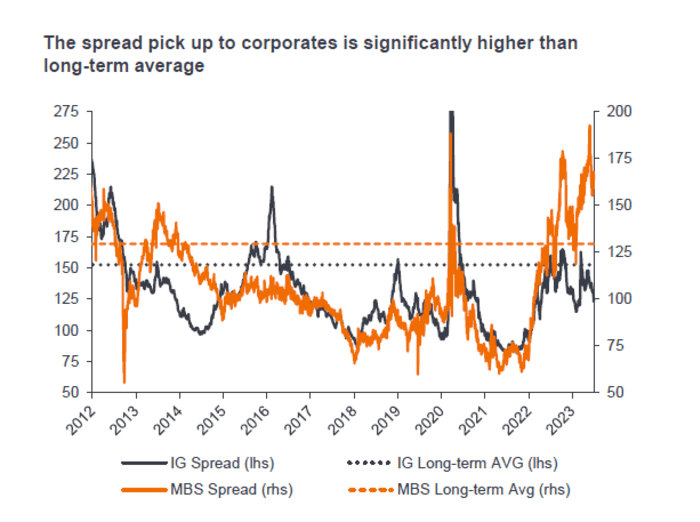

U.S. homes may be wildly unaffordable for first-time buyers, but mortgage bonds backed by those same properties could be dirt cheap.

Shocks from the Federal Reserve’s dramatic rate increases have walloped the $8.9 trillion agency mortgage-bond market, the main artery of U.S. housing finance for almost the past two decades.

Spreads, or compensation for investors, have hit historically wide levels, even through the sector is underpinned by home loans that adhere to the stricter government standards set in the wake of the subprime-mortgage crisis.

Bond prices also have tumbled, sinking from a peak above 106 cents on the dollar to below 98, despite guarantees that mean investors will be fully repaid at 100 cents on the dollar.

Bloomberg, Goldman Sachs Global Investment Research

“It’s really, really struggled,” Nick Childs, portfolio manager at Janus Henderson Investors, said of the agency mortgage-bond market during a Thursday talk on the firm’s fixed-income outlook.

Yet Childs and other investors also see big opportunities brewing. While mortgage bonds have gotten cheaper with the sector’s two anchor investors on the sidelines, the stalled housing market should breed scarcity in the bonds, which could help lift the sector out of a roughly two-year slump.

Prices have tumbled since rate shocks hit, but also since the Fed continued winding down its large footprint in the sector by letting bonds it accumulated to help shore up the economy roll off its balance sheet.

Banks awash in underwater securities have pulled back too. The repricing of similar bonds helped hasten the collapse of Silicon Valley Bank in March.

“Banks have been not only absent, but selling,” said Childs, who helps oversee the Janus Henderson Mortgage-Backed Securities exchange-traded fund

JMBS,

an actively managed $2 billion fund focused on highly rated securities with minimal credit risk.

“But we’re moving into an environment where supply continues to dwindle,” he said, given anemic refinancing activity and the dearth of new home loans being originated since 30-year fixed mortgage rates topped 7%.

The bulk of all U.S. mortgage bonds created in the past two decades have come from housing giants Freddie Mac

FMCC,

Fannie Mae

FNMA,

and Ginnie Mae, with government guarantees, making the sector akin to the $25 trillion Treasury market. But unlike investors in Treasurys, investors in mortgage bonds also earn a spread, or extra compensation above the risk-free rate, to help offset its biggest risk: early repayments.

While homeowners typically take out 30-year loans, most also refinanced during the pandemic rush to lock in ultralow rates, instead of continuing to make three decades of payments on more expensive mortgages. If someone refinances, sells or defaults on a home, it leads to repayment uncertainty for bond investors.

“To put this another way, the biggest risk to mortgages is now off the table, yet spreads are at or near historic wides,” said Sam Dunlap, chief investment officer, Angel Oak Capital Advisors, in a new client note.

That spread is now far above the long-term average, topping levels offered by relatively low-risk investment-grade corporate bonds.

Janus Henderson Investors

Agency mortgage bonds typically are included in low-risk bond funds and can be found in exchange-traded funds. While they have been hard hit by the sharp selloff in long-dated Treasury bonds

BX:TMUBMUSD10Y

BX:TMUBMUSD30Y,

there has also been hope that the worst of the storm could be nearly over.

Goldman Sachs credit analysts recently said they favored the sector but warned in a weekly client note that it still faces “high rate volatility and a dearth of institutional demand.”

As evidence of the U.S. bond selloff, the popular iShares 20+ Year Treasury Bond ETF

TLT

recently sank to its lowest level in more than a decade. It also was on pace for a negative 10% total return on the year so far, according to FactSet. Janus Henderson’s JMBS ETF was on pace for a negative 2.7% total return on the year through Friday.

“Frankly, why they fit portfolios so well is that because the government backs agency mortgages, there is no credit risk,” Childs said. “So if a borrower defaults, you get par back on that. It just comes through as a typical payment.”

[ad_2]

[ad_1]

U.S. stocks closed mostly lower Friday, but the Dow Jones and S&P 500 posted weekly gains, as the Israel-Gaza war appeared to escalate heading into the weekend. The Dow Jones Industries

DJIA,

rose about 39 points, or 0.1%, on Friday, ending near 33,670, according to preliminary FactSet data. The S&P 500 index

SPX,

fell 0.5% and the Nasdaq Composite Index

COMP,

closed 1.2% lower. The S&P 500’s energy segment outperformed Friday, gaining 2.3%, as U.S. benchmark crude surged nearly 6% after Israel ordered more than a million people in Gaza to evacuate to the south. Treasury yields fell, with the 10-year Treasury

TMUBMUSD10Y,

rate retreating to 4.628% Friday, snapping a 5-week yield climb, according to Dow Jones Market Data. Bond prices and yields move in the opposite direction. Investors bought other haven assets too, including gold

GC00,

and the U.S. dollar

DXY,

Wall Street’s “fear gauge”

VIX,

also touched its highest level in more than a week. Even so, the Dow Jones booked at 0.8% weekly gain, the S&P 500 advanced 0.5% and the Nasdaq fell 0.2%.

[ad_2]

[ad_1]

Many borrowers with subprime credit have been paying 17% to 22% rates on new auto loans this year as the Federal Reserve’s inflation fight takes a toll on lower-income households.

That borrowing range reflects the average cost, or annual percentage rate, for a loan in recent subprime auto bond deals, according to Fitch Ratings, an increase from last year’s average APR of closer to 14%.

Higher borrowing costs can mean households need to put more of their income into monthly auto payments, ramping up the risks of late payments, defaults and car repossessions. Those risks, however, have yet to make investors flinch.

The subprime auto sector already has cleared almost $30 billion of new bond deals this year, according to Finsight, a pace that’s slightly below volumes from the past two years, but still above historical levels since 2008.

Finsight

“I do believe there has to be a reckoning if rates stay higher for longer,” said Tracy Chen, a portfolio manager on Brandywine Global Asset Management’s global fixed income team.

Figuring out when the tumult might hit has proven difficult. Instead of slowing, the economy has shown resilience despite the Fed lifting its policy rate to a 22-year high of 5.25% to 5.5%. The central bank also indicated it might need to keep rates higher for some time to fight inflation. Longer-duration bond yields, as a result, have pushed higher, but still hover below 5%.

Inflation eats away at paychecks, especially those of lower-wage workers, a problem the Fed hopes to solve by keeping borrowing rates elevated. A gauge of inflation out Thursday showed consumer prices were steady at a 3.7% yearly rate in September, above the Fed’s 2% target.

“This recession has been on everyone’s mind for the past three years,” Chen said. While she thinks the economy will likely contract in the middle of 2024, a lot of damage could be done before that. “The longer rates stay here, the harder the landing.”

For now, the Fed is widely expected to hold rates steady at its next meeting in November. “Fed policy makers are now shifting their focus from ‘how high’ to raise the policy rate to ‘how long’ to maintain it at restrictive levels,” said EY Chief Economist Gregory Daco, in emailed comments.

Stocks were flat to slightly higher in choppy trade at midday Thursday after the inflation report came in hotter than forecast, with the Dow Jones Industrial Average

DJIA

near unchanged and the S&P 500 index

SPX

up 0.2%.

Past recessions and the burden of higher interest costs typically hit lower-wage workers harder, making subprime credit a canary in the coal mine for the rest of financial markets. Even so, investors in subprime auto bonds have yet to demand significantly more spread, or compensation, to offset potentially higher defaults among these borrowers.

Related: Subprime auto defaults on path toward 2008 crisis levels, say portfolio managers

Take the AAA rated 2-year slice of a new bond deal issued in mid-October by one of the subprime auto sector’s biggest players. It priced at a spread of 115 basis points above relevant risk-free rate, up from a spread of 90 basis points on a similar bond issued in August, according to Finsight, which tracks bond data.

When factoring in Treasury rates, the yield on the bonds bumped up to about 6% and 5.7%, respectively. The shot at higher returns and low delinquencies in subprime auto bonds have likely helped with investor confidence. The rate of subprime auto loans at least 60-day past due in bond deals was about 5% in September, according to Intex, up from historic lows around 2.5% two years ago.

“I think people still feel confident,” Chen said of subprime auto bonds. When putting a recent bond out on a Wall Street list to gauge its market value, she said bids come in right away.

[ad_2]

[ad_1]

U.S. stocks booked a 3-session win streak Tuesday as oil prices and bond yields retreated. The Dow Jones Industrial Average

DJIA,

climbed about 134 points, or 0.4%, ending near 33,739, according to preliminary FactSet data. That was the longest streak of straight wins for the blue-chip index in a month, and the best three days of gains since late August, according to Dow Jones Market Data. The S&P 500 index

SPX,

advanced 0.5% and the Nasdaq Composite Index

COMP,

gained 0.6%. It was the third session in a row of gains for all three indexes. The brighter backdrop for stock market came as oil prices

CL00,

and bond yields

TMUBMUSD10Y,

retreated and after Raphael Bostic, head of the Atlanta Fed, said he didn’t think additional rate hikes were needed to bring inflation down to the central bank’s 2% annual target, but also that he still sees rates staying high for a “long time.”

[ad_2]

[ad_1]

Emerging-market stocks are coming off a tough quarter after facing down a triple threat of rising Treasury yields, a stronger U.S. dollar, and a lackluster recovery in China’s economy and markets.

But amid the pain, some see opportunity for a lasting rebound.

The iShares MSCI Emerging Markets ETF

EEM,

which tracks the widely followed MSCI Emerging Markets Index, fell 4.1% during the quarter ended in September, outpacing a 3.7% decline for the S&P 500

SPX,

the deeply liquid U.S. benchmark. Both benchmarks endured their worst performance in a year.

It is just the latest chapter in what has been a decade of persistent underperformance during both good times and bad. The EM ETF fell 22.4% amid the global equity-market rout in 2022, compared with a 19.4% drop for the S&P 500, FactSet data show.

But while the selloff in Chinese stocks has dominated headlines this year, some corners of the emerging markets universe have held up surprisingly well. Greek and Mexican stocks have even outperformed U.S. stocks in dollar terms, while other major markets like Brazil and India are trailing by only a modest margin.

This hasn’t gone unnoticed by Wall Street, where some are advising clients to consider expanding their exposure to markets once deemed too risky for many U.S. investors saving for retirement.

In a research note shared with MarketWatch, a team of equity strategists at Goldman Sachs Group

GS,

pointed out that emerging-market stocks excluding China had outperformed developed-market stocks excluding the U.S. so far this year.

Meanwhile, dissatisfaction with lofty valuations in the U.S., well as the prospect of another recession potentially looming around the corner have helped to embolden portfolio managers to seek out better returns elsewhere.

| Country ETF | Ticker | Performance YTD (USD) |

| Brazil | EWZ | +9.2% |

| India | INDA | +7% |

| South Korea | EWY | +4% |

| Colombia | GXG | +2.5% |

| Chile | ECH | -7.6% |

| Mexico | EWW | +13% |

| China | MCHI | -7.6% |

| Indonesia | EIDO | -2% |

| Saudi Arabia | KSA | +0.3% |

| Greece | GREK | +22% |

| MSCI Emerging Markets | EEM | +0.8% |

| U.S. (S&P 500 index) | SPX | +13% |

Over the past 10 years, rock-bottom interest rates helped U.S. stocks best practically all comers. During the 10 years through Monday’s close, the S&P 500 has risen 161.8% excluding dividends, while the MSCI ACWI Index

ACWI,

a broad index of developed- and emerging-market stocks, gained nearly 74%, according to Dow Jones Market Data.

Emerging markets performed pretty poorly by comparison, with the MSCI EM Index down 9.6%.

But just because EM stocks have lagged their developed-world peers for a decade doesn’t mean they are doomed to repeat this dismal performance forever. Some pointed to the torrid gains for Japanese stocks in 2023 as an example of how a market that trailed the U.S. for decades can see its prospects suddenly brighten.

Japan’s Nikkei 225

NIY00,

has risen more than 21% since the start of the year in U.S. dollar terms, according to FactSet.

To that end, a chorus of investment bank equity strategists along with big-name investors like GMO’s Jeremy Grantham have said a similar dynamic could play out in emerging markets.

Equity strategists like Bank of America’s Michael Hartnett and Barclays Emmanuel Cau have urged clients to look beyond the U.S. for returns. According to a research report from Cau and his team, emerging markets offer “better tactical risk-reward.” Hartnett told clients that U.S. stocks appear extremely overvalued compared with the rest of the world, and that it is time to diversify away from the U.S.

“From the perspective of relative performance, the U.S. market has been really strong the past 10 years. It wasn’t like that the prior 20 years, and at some point, a reversion will happen,” said Dina Ting, head of global index portfolio management at Franklin Templeton, during an interview with MarketWatch.

“That is helping to make the case for international markets.”

With the possible exception of India, emerging-market stocks generally enjoy much lower valuations compared with their counterparts in the U.S.

That is according to a table of valuations and projected returns shared by analysts at Goldman. Many local equity markets enjoy forward price-to-earnings ratios below 10. By comparison, the S&P 500, considered the U.S. benchmark, presently enjoys a forward price-to-earnings ratio of 18.11, according to FactSet.

| Country | NTM P/E | 12-month return forecast (USD) |

| Brazil | 7.5 | +35% |

| Mainland China | 9.4 | +23% |

| Mexico | 10.7 | +27% |

| India | 20 | +8% |

| Colombia | 4.6 | +55% |

| Egypt | 6.7 | 0% |

| South Korea | 11.1 | 36% |

| Indonesia | 13.8 | +20% |

| Chile | 8 | +37% |

| Saudi Arabia | 14.9 | +13% |

| Total EM | 11.3 | +27% |

Developing economies have more rosy growth prospects, according to the International Monetary Fund, which released its latest batch of projections on Tuesday.

As a group, the IMF expects developing economies to grow by 4% in 2024, compared with 1.4% for a group of advanced economies that includes the U.S.

As Ting and other portfolio managers have pointed out, financials, producers of consumer goods and other industries are accounting for a growing share of emerging-market equity benchmarks. After so many years of being so heavily weighted toward China, and the commodity space, more diversity is seen as a welcome development.

Although few, if any, emerging-market economies enjoy the trifecta of rule of law, deeply liquid capital markets, and institutional independence that investors take for granted in the U.S., progress has been made. Ting cited India as a great example of a country that’s recently made major strides toward becoming more friendly toward international investors.

At the same time, paralysis in the U.S. Congress has raised concerns about potential political instability diminishing the attractiveness of the U.S. As House speakers are deposed and budget battles rage, some on Wall Street expect Moody’s Investors Service could join Fitch Ratings and S&P Global Ratings in stripping the U.S. of its AAA credit rating, as the agency has threatened to do.

Central banks in Mexico, Brazil and India have also had far less trouble tamping down inflation compared with the Federal Reserve, which also bodes well for future equity returns.

“In India and other emerging markets, certainly Brazil and others, their central banks have been much further ahead than the U.S. in fighting inflation,” said Ashish Chugh, a portfolio manager of long-only and long-short global emerging market equity strategies at Loomis, Sayles & Co.

“The U.S. government handed out free money during COVID-19, but these emerging-market countries didn’t do that. They gave out food and other stuff, but they didn’t send checks in the mail. Because of that, you didn’t have as big of an inflation problem.”

While emerging markets have matured in many ways, the sheer number of disparate economies and governments can make risk management difficult. The emerging-market space as defined by MSCI consists of two dozen countries.

Chinese stocks are still the most heavily represented in popular EM equity indexes like the MSCI Emerging Markets index, which is roughly 30% weighted toward the world’s second-largest economy.

Many investors in the West are already familiar with the risks of investing in China, including those emanating from China’s authoritarian system to the fallout from burgeoning geopolitical tensions with the U.S. But the potential pitfalls of investing in India or Brazil may not be quite as well understood.

That is why Zak Smerczak, an analyst and portfolio manager specializing in global equities at Comgest, would advise newcomers interested in the sector to start by investing in only the most established companies, even if their valuations don’t look quite as attractive.

“Being selective is the key,” he said during an interview with MarketWatch. “Making a broad investment in emerging markets right now seems risky to us, but there are pockets of opportunities and in specific companies.”

[ad_2]

[ad_1]

Some say it’s the fear of stagflation.

Some say it’s chaos on Capitol Hill.

Some say it’s turmoil in the Middle East.

But we all know the real reason the stock market is so crummy, right?

It’s October! Of course stocks are down!

It is a bizarre, inexplicable, and yet undeniable, fact that, throughout history, Wall Street has produced almost all of its gains during the winter months of the year — from Nov. 1 to April 30. It is an even more bizarre, inexplicable and yet undeniable fact that the rest of the world’s stock markets have done the same thing.

The so-called summer months, meaning the half of the year from May 1 to Halloween, have generally given you bupkis or worse.

Around the world, over the course of centuries of recorded financial history, stock-market returns have averaged four full percentage points higher from November to April than from May to October, report researchers Ben Jacobsen at Tilburg University and Cherry Yi Zhang at Nottingham University’s Business School in China. This so-called Halloween Effect seems “remarkably robust,” they concluded, after studying the financial returns of 114 different countries going back as far as they could find reliable monthly data — starting with the stock market in 1693 London.

Even more extreme: In the 65 countries for which they had extensive data both about the stock market and about short-term interest rates, it’s fair to say you would have been better off selling your stocks on May 1, putting the money in the bank, then taking it out again at the end of October and buying back your stocks (ignoring fees and taxes, of course).

“In none of the 65 countries for which we have total returns and short-term interest rates available — with the exception of Mauritius — can we reject a Sell in May effect based on our new test. Only for Mauritius do we find evidence of significantly positive excess returns during summer.”

Italics mine. Mauritius?

The Dow Jones Industrial Average

DJIA

is now lower than it was at the end of April. So is the Russell 2000

RUT

index of small-cap U.S. stocks. The benchmark international stock index, the MSCI EAFE, is down about 6%. Japan’s Nikkei

NIY00,

is slightly up, as the yen has tanked.

The S&P 500

SPX

is hanging on to a small gain, but that is only because of the early summer gains of a few tech titans. The average S&P stock is down about 2.5% since the end of April — while an investment in no-risk Treasury bills is up more than 2%.

Meanwhile, let the record show that, over the same period, according to the record keepers at MSCI, the stock market in Mauritius is up 12%.

Booyah!

Every time I write about this Halloween or “sell in May” effect, I make the same two points, and I make no apologies for repeating them here, because they are unavoidable.

The first is that, every spring, after looking at this data, I am tempted to sell all my stocks at the end of April, and every year I don’t, because I think it’s absolutely ridiculous. (And someone on Wall Street who is much smarter than me usually persuades me not to.) And most years I end up kicking myself for not doing it.

The second is to recall the old economists’ joke: “I don’t care if it works in practice! Does it work in theory?” Selling in May — or, sure, the Halloween Effect — has absolutely no reason that anyone can find for working in theory. But apparently, it works in practice — which is pretty much where we are now.

Does this mean stocks are going to rally? It’s anyone’s guess. It would be crazy if it were that simple. But, then, the whole Halloween Effect is crazy.

If history is any guide, now is the time to buy stocks, not sell them, because the next six months are likely to be the time when they make you money. And if history isn’t any guide, well, aren’t we all sunk anyway?

[ad_2]

[ad_1]

By Michael Susin

Retail sales growth in the U.K. slowed in September despite a fall in inflation as the high cost of living continues to put households’ budget under pressure, according to the latest sales-monitor report from the British Retail Consortium published on Tuesday.

Total retail sales for the five weeks to Sept. 30 increased by 2.7% compared with the prior month, when it saw growth of 4.1%, and was at the same level as the three-month average growth, the report said. In September last year, retail sales were up 2.2%.

Food sales rose 7.4% over the three months to September, while non-food sales further decreased 1.2%.

“Big ticket items such as furniture and electricals performed poorly as consumers limited spending in the face of higher housing, rental and fuel costs. The Indian summer also meant sales of autumnal clothing, knitwear and coats, have yet to materialize,” BRC Chief Executive Helen Dickinson said in a note.

Looking ahead, retailers are getting ready for the ‘Golden Quarter’ amid fierce competition that is likely to bring earlier and abundant promotions ahead of Christmas, KPMG U.K. Head of retail Paul Martin said.

“Consumers will continue to seek out good deals, with price driving purchasing decisions. This is likely to be one of the most important golden quarters that we have seen in years, as for some in the sector, it could very much determine their future,” he adds.

Dickinson highlighted that retailers’ efforts might be challenged by the 400 million pounds ($489.6 million) increase in business rates expected next year, and urged Chancellor Jeremy Hunt to scrap the rates rise in the upcoming budget statement.

Write to Michael Susin at michael.susin@wsj.com

[ad_2]

[ad_1]

Wall Street on Monday shook off a bout of selling sparked by the Israel-Gaza war.

That’s in keeping with the historical tendency of investors to look past geopolitical conflict and human tragedy, but it isn’t necessarily the last word. That last word will likely belong to oil traders.

“Oil rallied today yet remains below the near-term peak from last month. If oil prices rise higher for longer, the global economy could feel a resurgence of inflation during a period when investors are hoping inflation is clearly decelerating,” said Jeffrey Roach, chief economist for LPL Financial, in emailed comments.

Roach also noted that, in general, markets tend to have difficulty pricing the difference between a temporary shock and a permanent shock.

For now, however, the jump in oil prices isn’t signaling a permanent shock. Sure, Brent crude

BRN00,

the global benchmark, jumped 4.2% on Monday to end at $88.15 a barrel, while West Texas Intermediate crude

CL.1,

CL00,

surged $3.59, or 4.3% to $86.38 a barrel — the biggest one-day jump for both grades since April 3.

See: Here’s what Israel-Gaza war means for oil prices as fighting continues

The jump was impressive, but it comes after a big pullback last week that saw both WTI and Brent retreat from 2023 highs near $100 a barrel.

So if crude can manage to close above those highs — $93.68 a barrel for WTI — investors across other markets will likely take notice.

What would it take to drive crude back toward the highs? The focus is on Iran.

The Wall Street Journal on Sunday reported that Iranian security officials helped plan the attack by Hamas. The Israeli military has said there is no concrete evidence of Iranian involvement, according to news reports.

A direct role by Iran, a longtime ally of Hamas, would raise the threat of a broader conflict.

Some analysts have put Iranian crude production at more than 3 million barrels a day and exports above 2 million barrels a day — the highest levels since the Trump administration pulled the U.S. out of the Iranian nuclear accord in 2018, according to the Wall Street Journal. Sales fell to around 400,000 barrels a day in 2020 as the U.S. reimposed sanctions.

“If Israel discovers that Iran played a role in Hamas’ attack, it could retaliate militarily. At the very least, any warming of relations between Iran and the West is now on hold and this will limit incremental oil supply,” said Nicholas Colas, co-founder of DataTrek Research, in a Monday note.

It’s a reminder that “while neither Israel nor Gaza are major oil producers, everything that happens geopolitically in the Middle East invariably ends up affecting oil prices,” he said.

The potential for a broader conflict could lead to a “sharp market correction,” argued Olivier d’Assier, head of applied research, APAC, at Axioma.

The scale of the conflict, the largest since the Yom Kippur War 50 years ago, renders comparisons with how markets have shaken off past geopolitical incidents, but they may be irrelevant in terms of stress testing, he argued.

“The closest historical scenarios we could use would be 9/11 and the start of the Ukraine war. But because both took place on Western soil, they might not be adequate,” d’Assier said.

On Monday, however, remarks by Federal Reserve officials ultimately trumped the rise in crude prices and jitters over the Middle East. Dallas Fed President Lorie Logan and Fed Vice Chair Philip Jefferson both noted the rise in long-term Treasury yields and their role in tightening financial conditions, which investors took as a signal the Fed may not be as likely to further raise interest rates.

See: An Israel-Hamas war could change what the Fed does about interest rates

Stocks turned north after a morning dip, with the Dow Jones Industrial Average

DJIA

rising nearly 200 points, or 0.6%, while the S&P 500

SPX

also advanced 0.6% and the Nasdaq Composite

COMP

gained 0.4%.

For now, market participants appear set to look ahead to economic data later this week, including September consumer-price index and producer-price index readings.

[ad_2]

[ad_1]

U.S. stocks booked back-to-back gains on Monday, despite rising oil prices and a deadly weekend assault on Israeli by Hamas that left hundreds dead. The Dow Jones Industrial Average

DJIA,

rose about 197 points, or 0.6%, ending near 33,604, shaking off earlier weakness, while the S&P 500 index

SPX,

advanced 0.6% and the Nasdaq Composite Index

COMP,

gained 0.4%, according to preliminary FactSet data. U.S. benchmark oil prices

CL00,

rose 4.3% to $86.38 a barrel as traders gauged potential implications of the Israel-Gaza war on crude supplies from the Middle East. Investors also flocked to haven assets, including gold

GC00,

and the U.S. dollar

DXY,

while cash trading in the $25 trillion Treasury market was closed for the Columbus Day and Indigenous Peoples Day holiday. Israel on Monday seal off the Gaza Strip from food, fuel and other supplies as the conflict between Israel and Hamas intensified, according to the Associated Press.

[ad_2]

[ad_1]

U.S. stocks saw a surprising bounce on Friday, culminating in the S&P 500 index’s biggest intraday comeback since the March banking crisis, even though a monthly jobs report for September came in much higher than expected.

So, are investors no longer worried about the Federal Reserve’s inflation fight or higher interest rates wrecking the U.S. economy?

“Stocks initially sold off on the blockbuster jobs report which indicates the Fed may not be done,” said Gina Bolvin, president of Bolvin Wealth Management Group. “However, after digesting the strong labor market is still strong, stocks rallied. And why shouldn’t they? Will good news- finally – be good news?”

Bolvin said part of the rally could be seasonal, with September typically being a rough months for stocks. There also has been increased optimism that the earnings recession for American corporations may be over, she said.

Analysts are predicting corporate earnings growth rates of 5.9% for the fourth quarter for S&P500 companies, according to John Butters, senior earnings analyst at FactSet. Estimates are for the third-quarter of 2023 after the stock index’s fourth straight quarterly earnings decline on a year-over-year basis.

At Friday’s session lows, the S&P 500 index

SPX

was down 0.9%, but it ended up posting a 1.2% advance, its largest intraday comeback since March 24, 2023, according to Dow Jones Market Data. The Dow Jones Industrial Average

DJIA

booked a 0.9% gain and the Nasdaq Composite Index

COMP

rose 1.6% higher.

“The movement in stocks today is certainly encouraging given yields are up as well,” said Chris Fasciano, portfolio manager, Commonwealth Financial Network. “But we will need to see follow through next week.”

The yield on 10-year Treasury

BX:TMUBMUSD10Y

note rose for five straight weeks in a row to 4.783% on Friday, while the 30-year yield

BX:TMUBMUSD30Y

rose to 4.941%, according to Dow Jones Market Data.

Read: Why 5% bond yields could wreak havoc on the market

While the U.S. stock-market will be open for business on Monday, the bond market will be closed for Columbus Day and Indigenous Peoples Day holiday, giving investors somewhat of a pause before a big week of economic data that could shape the Fed’s next decision on interest rates.

“Ultimately, stocks and bonds will take their cues next week from the economic releases,” Fasciano told MarketWatch.

Key items on the calendar for the week will be September inflation reports, with the producer-price index on Wednesday and the consumer-price index due Thursday. In between, Fed minutes of its policy meeting in September also are due to be released Wednesday.

“That makes next week an important week for the future direction of both the bond and equity markets as the Fed will certainly be focused on those reports prior to their next meeting on Oct. 31-Nov. 1,” Fasciano said.

[ad_2]

[ad_1]

U.S. stocks saw a surprising bounce on Friday, culminating in the S&P 500 index’s biggest intraday comeback since the March banking crisis, even though a monthly jobs report for September came in much higher than expected.

So, are investors no longer worried about the Federal Reserve’s inflation fight or higher interest rates wrecking the U.S. economy?

“Stocks initially sold off on the blockbuster jobs report which indicates the Fed may not be done,” said Gina Bolvin, president of Bolvin Wealth Management Group. “However, after digesting the strong labor market is still strong, stocks rallied. And why shouldn’t they? Will good news- finally – be good news?”

Bolvin said part of the rally could be seasonal, with September typically being a rough months for stocks. There also has been increased optimism that the earnings recession for American corporations may be over, she said.

Analysts are predicting corporate earnings growth rates of 5.9% for the fourth quarter for S&P500 companies, according to John Butters, senior earnings analyst at FactSet. Estimates are for the third-quarter of 2023 after the stock index’s fourth straight quarterly earnings decline on a year-over-year basis.

At Friday’s session lows, the S&P 500 index

SPX

was down 0.9%, but it ended up posting a 1.2% advance, its largest intraday comeback since March 24, 2023, according to Dow Jones Market Data. The Dow Jones Industrial Average

DJIA

booked a 0.9% gain and the Nasdaq Composite Index

COMP

rose 1.6% higher.

“The movement in stocks today is certainly encouraging given yields are up as well,” said Chris Fasciano, portfolio manager, Commonwealth Financial Network. “But we will need to see follow through next week.”

The yield on 10-year Treasury

BX:TMUBMUSD10Y

note rose for five straight weeks in a row to 4.783% on Friday, while the 30-year yield

BX:TMUBMUSD30Y

rose to 4.941%, according to Dow Jones Market Data.

Read: Why 5% bond yields could wreak havoc on the market

While the U.S. stock-market will be open for business on Monday, the bond market will be closed for Columbus Day and Indigenous Peoples Day holiday, giving investors somewhat of a pause before a big week of economic data that could shape the Fed’s next decision on interest rates.

“Ultimately, stocks and bonds will take their cues next week from the economic releases,” Fasciano told MarketWatch.

Key items on the calendar for the week will be September inflation reports, with the producer-price index on Wednesday and the consumer-price index due Thursday. In between, Fed minutes of its policy meeting in September also are due to be released Wednesday.

“That makes next week an important week for the future direction of both the bond and equity markets as the Fed will certainly be focused on those reports prior to their next meeting on Oct. 31-Nov. 1,” Fasciano said.

[ad_2]