Hong Kong

CNN

—

Starting at $53,000 for a space not much larger than a shoebox, it is a pricey place to stay, even in a city famed for the world’s most expensive property market.

But then the ornate white marble interiors of the 12 story Shan Sum tower in Hong Kong are not aimed at your average sort of buyer. They are meant for a more discerning type of customer altogether, one seeking that little something extra: a resting spot for the afterlife.

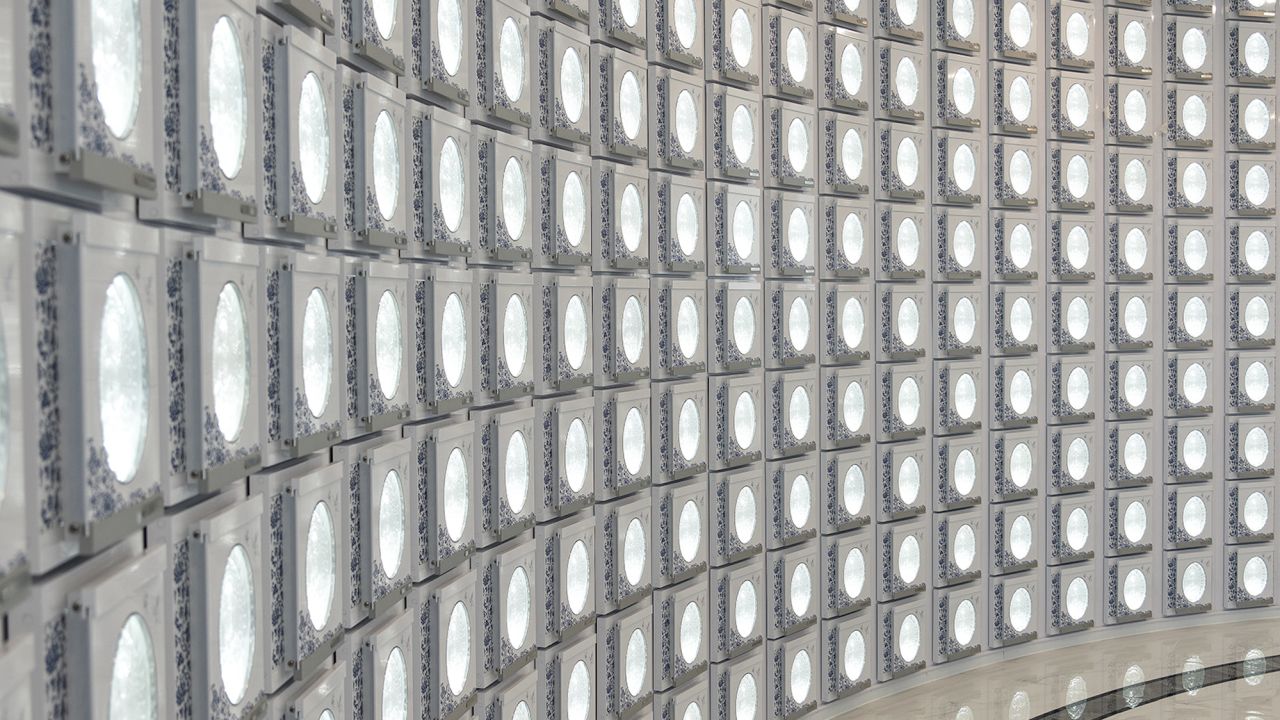

This privately run high-rise columbarium, housed in a wavy, fan-shaped building designed by a German architect, is meant to store the cremated remains of 23,000 people. And it doesn’t come cheap.

In addition to its single urn entry units, niches that can store two urns can go for up to $76,000 (HK$598,000), while family units that can house the ashes of up to eight people reach as much as $430,000 (HK$3.38 million).

With standard niches measuring about one cubic square foot, it could be argued that a spot in this tower is relatively more costly than the city’s most expensive property for the living – a mansion in the ultra exclusive area of The Peak that in March attracted a bid of US$32,000 per square foot.

But Shan Sum, which is tucked away in an old industrial district of Kwai Chung is not even Hong Kong’s most expensive place for the dead.

According to Hong Kong’s Consumer Council, the most expensive niche of all is at a temple-like complex in the northern outskirts of Fanling. That auspicious resting spot goes for $660,000 (HK$5.2 million) – and that figure doesn’t even include the management fees of at least $25,000 (HK$200,000) to cover the upkeep and surcharges.

Such an investment might still not seem too bad, given the long-term horizon of the afterlife, but private columbariums like Shan Sum are not offering a resting place for eternity. Ashes can be stored there only for the duration of the facility’s private license, which is issued by Hong Kong government. These licenses have a limit of 10 years and can take years of inspections to obtain. Shan Sum’s runs through 2033.

Even so, at Shan Sum – whose name translates to “benevolent heart” – it’s more than just the urn space you pay for.

Its architect Ulrich Kirchhoff told CNN there is an accessible rooftop and winding balconies lined with pocket gardens for families visiting their ancestors, while about a fifth of the building’s area is open space.

It has also been designed with aesthetics in mind, with its wavy, high-rise profile intended to mimic traditional Chinese graveyards and their preferred location on mountainsides to attract good Feng Shui.

There are hints of modernity, too, such as dehumidifiers and air-conditioning systems and even an app through which families pre-book a time slot to bring offerings to deceased ancestors.

The tower is the brainchild of Margaret Zee, a septuagenarian businesswoman who made her fortune in the jewelry and real estate businesses and now runs a charitable foundation in her name.

Paying respect to the dead is important in Chinese culture, Zee told CNN, and many people are willing to go all out to honor the tradition.

“Our loved ones’ last journey is not just so they can cross over to the afterlife, but it’s also for us who are left here on Earth to bid them farewell,” Zee said. “It’s not only to lay them to rest, but to give peace to those they’ve departed from.”

Zee realized there was a shortage of homes to honor the dead when she struggled to find a place to hold a memorial for and bury her late husband in 2007 and she felt compelled to act.

In Hong Kong, the same mismatch of supply and demand that has driven up real estate prices to nosebleed levels also affects columbariums.

Essentially, in a city home to more than 7 million people and some of the world’s most densely populated neighborhoods, competition for space is heating up – for both the living and the dead.

While Hong Kong is not a small place – its area of 1,110 square kilometers is about 1.4 times the size of New York City – its mountainous terrain makes much of its land unsuitable for development.

With space at a premium, property developers have traditionally favored high-rise towers that – not unlike the Shan Sum building – can pack in as many plots as possible. As a consequence, the average home size is just 430 square feet, according to the 2021 census, among the tiniest in the world, even though average home prices are north of a million dollars.

This squeeze on space continues in the afterlife, exacerbated by Hong Kong’s rapidly aging population. More than one in five Hong Kongers is over 65, according to census data, and that number is projected to jump to more than one in three by 2069.

Even though more than 90% of Hong Kongers opt for cremation, space to store their remains is running out. This is partly because, rather than scattering the ashes, traditionally minded Chinese prefer a physical place where they can pay respects and give offerings to the dead.

With the city’s death rate running at about 46,000 per year (roughly double the capacity of Shun Sum) in the past decade urn capacity has at times struggled to keep up.

There are currently just under 135,000 public niches available in government-run facilities, where a 20-year lease goes for about $300, but competition for these is fierce and in recent years some families have reported waiting years to get a spot.

The response by the government has been two-fold, boosting the number of public facilities while also approving the licenses of 14 privately-run columbarium operators, including Shan Sum, since 2017.

A spokesperson for the Food and Environmental Hygiene Department told CNN that between 2020 and 2022, around 77,000 urns had been allocated a niche “without the need to wait.” Another four new locations to be completed by 2025 would provide a further 167,000 units.

“There is a marked improvement in the supply of public niches over the past few years. As of now, the supply of public niches is adequate,” the spokesperson said.

Still, as with many things in this commercially-minded city, where the median monthly wage is just US$2,400 but there are plenty of billionaires (more than 100, according to Wealth X, a company that tracks high-net-worth individuals), there are options for those eager to splash out on something a little more distinguished.

And that’s where places like Shan Sum really come in to their own.

At the tower in Kwai Chung different floors are dedicated to different religions to suit a range of death customs, said Pan Tong, Zee’s son and the operational director of the building.

For instance, he says, there are light and bright airy nooks designed to appeal to Buddhists and a section for followers of Guanyin, the Chinese goddess of mercy, whose image adorns the doors of the small compartments.

There is even a separate secular floor, where each compartment has a Chinese-style “roof” and double doors decorated with gold coins to symbolize a prosperous afterlife.

“I really had to imagine myself as someone ‘living’ inside one of these niches, and think about what kind of home I wanted to stay at when I’m gone,” Tong said.