Coinbase Global Inc. late Thursday reported a wider quarterly loss and a 54% drop in revenue, saying the headwinds for its business will continue and likely intensify next year.

Coinbase COIN, -8.09%

said it lost $545 million, or $2.43 a share, in the quarter, swinging from earnings of $406 million, or $1.62 a share, in the year-ago period.

Revenue dropped to $576 million from $1.24 billion a year ago.

Analysts surveyed by FactSet expected the crypto exchange to report a loss of $2.38 a share on revenue of $641 million.

Shares traded lower immediately after the report, but at last check were rising more than 8% in the extended session.

The quarter was “mixed” for Coinbase, the company said in a letter to shareholders. “Transaction revenue was significantly impacted by stronger macroeconomic and crypto market headwinds, as well as trading volume moving offshore.”

On the plus side, Coinbase saw “strong growth in our subscription and services revenue,” it said.

Those headwinds, however, continued to impact transaction revenue, which was down 44% quarter on quarter, Coinbase said in the letter.

Trading volume dropped to $159 billion in the quarter from $217 billion in the second quarter.

“For 2022, we remain cautiously optimistic that we will operate within the $500 million adjusted EBITDA loss guardrail that we previously communicated,” the company said. That assumes that the crypto market does not deteriorate further, it said.

For next year, however, Coinbase is “preparing with a conservative bias and assuming that the current macroeconomic headwinds will persist and possibly intensify,” the company said.

Ever since Starbucks Corp. rolled out longer-term financial targets in September, Wall Street has wondered how the coffee chain might meet what analysts say were ambitious goals, as rising prices drain consumer spending. For at least the year ahead, executives on Thursday called out three ways to get there: higher prices, younger customers and cold, customizable beverages.

For the fiscal year ahead, executives for the coffee chain on Thursday said they expected global same-store sales to be “near the high end” of its long-term target of between 7% to 9% growth. FactSet expects growth of 8.6%.

When an analyst asked what gave management confidence in that target, interim Chief Executive Howard Schultz said that its coffee was an “affordable luxury,” and that it was armed with a loyalty program that it didn’t have in years past. And they said its customers were getting younger, not older.

“Not only has it gotten younger, but that young, Gen Z customer tends to have significantly more discretionary money at their disposal,” he said. “And their loyalty to Starbucks has been quite significant and predicted.”

He said Starbucks SBUX, +0.12%

had raised prices by nearly 6% over the past 12 months and hadn’t seen demand subside. And he said cold coffee beverages made up 76% percent of total drink sales in its U.S. company-owned stores. In the fourth quarter, more than half of beverages overall in those stores were customized, leading to $1 billion in sales a year for add-on syrups, foams and other ingredients.

“I think customization, which we spoke a lot about in our prepared remarks, is obviously giving us the ticket is becoming more accretive,” he said.

Management said they expect U.S. same-store sales growth of 7% to 9% for the year ahead. For China, they’re banking on “outsize” growth for the metric — interrupted by a decrease in the first-quarter — as the nation potentially emerges from pandemic-related lockdowns.

For overall revenue, they expect gains of between 10% and 12%. Management also said they would resume their buyback program in fiscal 2023.

Even as the Federal Reserve tries to chart a path to lower prices, Starbucks is the latest company to say it still has “pricing power,” or the ability to charge customers more. Snack maker Mondelez International MDLZ, -0.93%,

earlier in the week, said it planned to raise prices through next year. Similarly, its own chief executive also described its snacks as an “affordable indulgence.”

Prior to the call, Starbucks reported fiscal fourth-quarter results that beat expectations, helped by a boost in U.S. sales and higher prices.

The coffee chain reported net income of $878 million, or 76 cents a share, compared with $1.76 billion, or $1.49 a share, in the same quarter last year. Revenue rose 3% to $8.4 billion, compared with $8.15 billion in the prior-year quarter.

Same-store sales rose 7% worldwide, helped largely by bigger ticket sizes, even as actual transaction volume remained muted. They were up 11% in the U.S. But international same-store sales fell 5%, with a 16% drop in China.

Excluding restructuring, impairment and other costs, Starbucks earned 81 cents per share, compared with 99 cents a year earlier. U.S. members of its loyalty program who were active for three months rose 16% to 28.7 million.

Analysts polled by FactSet expected Starbucks to report adjusted earnings per share of 72 cents, on revenue of $8.323 billion. Same-store sales were expected to rise 4.2%.

Shares rose 2.4% after hours.

As with other restaurants and retailers, Starbucks’ sales this year have been helped by price increases. Analysts have also said higher-income consumers, who might not mind higher prices as much, as well as demand for cold beverages, have propelled demand. While China’s COVID-19 restrictions have weighed on sales, analysts say demand trends are strong elsewhere.

“The U.S. business is humming, and the China risk is increasingly understood,” Wedbush analyst Nick Setyan wrote in a research note ahead of Starbucks’ earnings.

The earnings report comes as Starbucks battles a nascent unionization push at some of its stores. Some bargaining efforts between the company and the union members have stalled, amid allegations from both of bad-faith negotiations. The company over the past year has spent more to raise employee pay and rolled out other incentives at non-union stores.

Starbucks stock has tumbled 27% so far this year. The S&P 500 Index SPX, -1.06%,

by comparison, is down around 22%.

Qualcomm Inc. shares fell in the extended session Wednesday following the chip maker’s poor outlook, and estimates of about two months or more of inventory it needs to clear in its core business.

On the call with analysts, Chief Executive Cristiano Amon said the accelerated weak demand was related to “macro economic headwinds and the prolonged COVID in China,” and “the rapid deterioration in demand and easing of supply constraints” across the chip industry.” would take out about 80 cents a share in first-quarter earnings.

“It’s the major factor,” Amon told analysts on the call. “It’s mostly a handset consumer story.” Earnings for the first quarter, as a results, would take a hit of 80 cents a share, the company said.

Another big factor is that companies are just spending less. Amon said “companies across the board had much higher inventory policies, supply chain got resolved, and you got that macro economic uncertainty, you have a drawdown trying to bring inventory to a different level than it was during the situation of demand constraint.”

Qualcomm forecast first-quarter earnings of $3 to $3.30 a share on revenue of $9.2 billion to $10 billion, while the Street estimated $3.43 a share on revenue of $12.02 billion.

Chief Financial Officer Akash Palkhiwala told analysts there is about eight to 10 weeks of elevated in the channel. In the meantime, Qualcomm was instituting a hiring freeze, and looking into cost-saving measures, execs told analysts.

While handset-chip sales surged 40% to a record $6.57 billion from a year ago, topping the Street’s expectation of $6.55 billion, the company’s forecast indicates a big glut in inventory in Qualcomm’s CDMA Technologies unit, the one that includes handset and RF chips as well as chips for autos and Internet of Things.

Qualcomm expects QCT sales of $7.7 billion to $8.3 billion, and sales from Qualcomm’s technology licensing, or QTL, segment of $1.45 billion to $1.65 billion. Analysts had forecast forecast $10.42 billion in QCT sales and QTL revenue of $1.71 billion.

Qualcomm reported fourth-quarter QCT revenue of $9.9 billion, a 28% gain from a year ago. Analysts had estimated $9.84 billion, based on the company’s forecast of $9.5 billion to $10.1 billion.

Fourth-quarter auto-chip sales zoomed up 58% to a record $427 million, and Internet of Things, or IoT, sales rose 24% to a record $1.92 billion. The Street was expecting auto sales of $362.4 million, and IoT sales of $1.82 billion.

Revenue from the QTL segment fell 8% to $1.44 billion compared with Wall Street estimates of $1.58 billion, based on a company forecast of $1.45 billion to $1.65 billion.

The company reported fiscal fourth-quarter net income of $2.87 billion, or $2.54 a share, compared with $2.8 billion, or $2.45 a share, in the year-ago period. The chip maker reported adjusted earnings, which exclude stock-based compensation expenses and other items, of $3.13 a share, compared with $2.55 a share in the year-ago period. Total revenue for the third quarter rose to $11.4 billion from $9.34 billion in the year-ago period.

Analysts had estimated earnings of $3.13 a share on revenue of $11.32 billion, based on Qualcomm’s forecast of $3 to $3.30 a share on revenue of $11 billion to $11.8 billion.

Year to date, Qualcomm shares are down 38%, compared with a 41% decline for the PHLX Semiconductor Index SOX, -3.09%,

a 21% decline by the S&P 500 index SPX, -2.50%

and a 33% drop by the tech-heavy Nasdaq Composite Index COMP, -3.36%.

Roku Inc. shares plummeted 19% in after-hours trading Wednesday after the streaming company topped expectations with its latest results but gave a weaker-than-anticipated outlook for the holiday quarter as economic conditions could further “degrade advertising budgets.”

For the fourth quarter, Roku executives anticipate $800 million in revenue and a loss of $135 million on the basis of adjusted Ebitda. The FactSet consensus called for $899 million in revenue as well as a $48 million adjusted Ebitda loss.

“As we enter the holiday season, we expect the macro environment to further pressure consumer discretionary spend and degrade advertising budgets, especially in the TV scatter market,” the company said in its shareholder letter. “We expect these conditions to be temporary, but it is difficult to predict when they will stabilize or rebound.”

Chief Financial Officer Steve Louden shared on a call with reporters following the release that the company’s forecast “reflects the fact that we see a lot of challenges in the macro environment.”

He explained that Roku tends to be more exposed to the scatter ad market — which represents ads bought during the quarter — than the typical TV network. Scatter spending is easy for marketers to turn on, but also easier for them to turn off, he noted.

The forecast overshadowed the results from Roku’s third quarter, which were broadly better than expected.

The company posted a net loss of $122.2 million, or 88 cents a share, whereas it logged net income of $68.9 million, or 48 a share, in the year-earlier period. Analysts tracked by FactSet were expecting a $1.29 loss on a per-share basis.

Roku also reported a loss of $34 million on the basis of adjusted earnings before interest, taxes, depreciation and amortization. The company had posted positive adjusted Ebitda of $130 million in the year-before quarter. The FactSet consensus was for a $74 million loss on the non-GAAP metric.

Revenue rose to $761 million from $680 million, while analysts were anticipating $696 million.

The company generated $670 million in platform revenue and $91 million in player revenue. Analysts were expecting platform revenue of $613 million and player revenue of $87 million.

Roku had 65.4 million active accounts in the latest quarter, up from 63.1 million in the second quarter. Average revenue per user was $44.25 on a trailing-12-month basis, compared with $44.10 in the second quarter and $40.10 in the prior year’s third quarter.

Analysts were anticipating 64 million active accounts and $43.40 in average revenue per user.

Louden noted on the media call that the account numbers “outperformed expectations.” The company has seen “strong sales of smart TVs both in the U.S. and internationally,” with Louden adding that “it’s hard to tell how much is driven by a shift back to home or back to streaming, which is a very good value proposition if money is tight.”

Viewers spent 21.9 billion hours streaming content through Roku’s platform in the period. The FactSet consensus was for 20.9 billion hours streamed.

“That changes their focus a bit from only thinking about subscribers to thinking about engagement” and he sees Roku’s team members as “experts in understanding how consumers look at that.”

The company also noted in its shareholder letter that CFO Louden intends to leave Roku at some point in 2023 after helping to recruit and train his successor.

Qualcomm Inc. shares fell in the extended session Wednesday following the chip maker’s poor outlook, and estimates of about two months or more of inventory it needs to clear in its core business.

On the call with analysts, Chief Executive Cristiano Amon said the accelerated weak demand was related to “macro economic headwinds and the prolonged COVID in China,” and “the rapid deterioration in demand and easing of supply constraints” across the chip industry.” would take out about 80 cents a share in first-quarter earnings.

“It’s the major factor,” Amon told analysts on the call. “It’s mostly a handset consumer story.” Earnings for the first quarter, as a results, would take a hit of 80 cents a share, the company said.

Another big factor is that companies are just spending less. Amon said “companies across the board had much higher inventory policies, supply chain got resolved, and you got that macro economic uncertainty, you have a drawdown trying to bring inventory to a different level than it was during the situation of demand constraint.”

Qualcomm forecast first-quarter earnings of $3 to $3.30 a share on revenue of $9.2 billion to $10 billion, while the Street estimated $3.43 a share on revenue of $12.02 billion.

Chief Financial Officer Akash Palkhiwala told analysts there is about eight to 10 weeks of elevated in the channel. In the meantime, Qualcomm was instituting a hiring freeze, and looking into cost-saving measures, execs told analysts.

While handset-chip sales surged 40% to a record $6.57 billion from a year ago, topping the Street’s expectation of $6.55 billion, the company’s forecast indicates a big glut in inventory in Qualcomm’s CDMA Technologies unit, the one that includes handset and RF chips as well as chips for autos and Internet of Things.

Qualcomm expects QCT sales of $7.7 billion to $8.3 billion, and sales from Qualcomm’s technology licensing, or QTL, segment of $1.45 billion to $1.65 billion. Analysts had forecast forecast $10.42 billion in QCT sales and QTL revenue of $1.71 billion.

Qualcomm reported fourth-quarter QCT revenue of $9.9 billion, a 28% gain from a year ago. Analysts had estimated $9.84 billion, based on the company’s forecast of $9.5 billion to $10.1 billion.

Fourth-quarter auto-chip sales zoomed up 58% to a record $427 million, and Internet of Things, or IoT, sales rose 24% to a record $1.92 billion. The Street was expecting auto sales of $362.4 million, and IoT sales of $1.82 billion.

Revenue from the QTL segment fell 8% to $1.44 billion compared with Wall Street estimates of $1.58 billion, based on a company forecast of $1.45 billion to $1.65 billion.

The company reported fiscal fourth-quarter net income of $2.87 billion, or $2.54 a share, compared with $2.8 billion, or $2.45 a share, in the year-ago period. The chip maker reported adjusted earnings, which exclude stock-based compensation expenses and other items, of $3.13 a share, compared with $2.55 a share in the year-ago period. Total revenue for the third quarter rose to $11.4 billion from $9.34 billion in the year-ago period.

Analysts had estimated earnings of $3.13 a share on revenue of $11.32 billion, based on Qualcomm’s forecast of $3 to $3.30 a share on revenue of $11 billion to $11.8 billion.

Year to date, Qualcomm shares are down 38%, compared with a 41% decline for the PHLX Semiconductor Index SOX, -3.09%,

a 21% decline by the S&P 500 index SPX, -2.50%

and a 33% drop by the tech-heavy Nasdaq Composite Index COMP, -3.36%.

Vicki Hollub’s Occidental Petroleum controls the biggest piece of the most important area for oil production in the United States. Not so long ago, an oilman in a position like that—and it would’ve been a man, before Hollub came along—would have gone for broke, turning up production to its physical limits.

Not Hollub. Occidental produces on average the equivalent of about 1.15 million barrels of oil a day, and that’s more than enough to turn a profit. The company can make money as long as oil prices are above $40 a barrel. They’ve been above $80 for almost all of this year, as the war in Ukraine takes a toll on global markets and the Saudi-led oil cartel OPEC now slashes production.

“We don’t feel like we’re in a national crisis right now,” Hollub told MarketWatch in an interview. And that means Hollub can keep executing on her plans: making shareholders happy by paying down debt and buying back shares. “When you have such a low break-even, to me there’s no pressure to increase production right now, when we have these other two ways that we can increase shareholder value,” Hollub said.

That market-focused logic puts her at odds with President Biden, who is acting like there is a national energy crisis ongoingprecisely because of what oil CEOs like Hollub are doing. The size of oil companies’ profits is outrageous, Biden said Monday. They’re raking in cash not because of innovation or investment but as a windfall from the war in Ukraine, Biden said. “Rather than increasing their investments in America or giving American consumers a break, their excess profits are going back to their shareholders and to buying back their stock, so the executive pay is — are going to skyrocket,” Biden said. He has ordered releases from the Strategic Petroleum Reserve to keep down gas prices and asked Congress to tax oil-company profits.

But Hollub is single-mindedly focused on seizing the moment to improve the company’s financial position. Occidental still has significant debt left over from a challenging acquisition Hollub spearheaded before the pandemic. In the second quarter alone, the company used its windfall to repay $4.8 billion in debt. If Biden called, she’d listen, but she hasn’t spoken to him one-on-one. Hollub said she’d spoken to the administration through Energy Secretary Jennifer Granholm. (“She doesn’t know the industry very well right now, but it’s because she hasn’t been in her job very long,” Hollub said.) The White House and the Department of Energy did not return requests for comment.

Hollub says she’s just following the market. “If demand goes down, we reduce production, if it goes up, we increase.” Oil prices have fluctuated rapidly over the year, and with a recession widely anticipated in the near future, demand could drop, Hollub said. Biden’s releases of oil from the SPR, she added, may have reduced gasoline prices, but at a cost to national security. “The SPR should be reserved for emergency situations, and you never know when those might come,” Hollub said.

Hollub’s message may not be politically convenient, but it’s exactly what her shareholders want to hear. Occidental OXY, -2.29%

is America’s hottest stock and has returned 150% this year, making it the top-performing company in the S&P 500 SPX, -0.65%.

Investors who bought shares of Occidental in January and held them through today would have more than doubled their money, even as the broader market has crashed. Warren Buffett’s Berkshire Hathaway has gone on a buying spree this year, and now owns more than 20% of Occidental’s shares. How Hollub got here constitutes America’s greatest corporate saga in recent years, from her 2019 debt-fueled decision to buy bigger rival Anadarko Petroleum over the vocal objections of activist investor Carl Icahn, to the pandemic-induced collapse in oil prices that almost bankrupted Occidental, and Buffett’s extension, removal, and re-extension of support.

With Occidental now on solid financial footing, Hollub is continuing to leave a mark on the oil industry and the world, landing her on the MarketWatch 50 list of the most influential people in markets. Hollub’s tangles with the wise men of Wall Street have left her savvier about how to manage her business. Stung by previous boom-and-bust cycles, Hollub has helped lead America’s oil frackers away from being “swing producers” that could counter the war-driven increase in energy prices, as she paid down debt and returned cash to shareholders through dividends and stock buybacks instead of plowing some of that money into shale oil fields. She is also pushing investment into Occidental’s massive new carbon-capture effort.

More than anything, Hollub is focused on guys like Bill Smead, founder of Smead Capital Management, who is a long-term investor in Occidental and a Hollub fan. “She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us,” he said.

With that kind of backing, Hollub is planning to put Occidental in the driver’s seat of the massive national economic transition induced by climate change. She is positioning Occidental to be the company of the energy transition, one geared not to the free-for-all economy of the last century or some carbonless vision of the next, but the oil company for right now. She might even stop drilling new oil wells entirely.

“Now we feel like we control our own destiny,” Hollub said.

For the chief executive of a company that’s having a banner year on Wall Street while investors choke down generational losses, Hollub seems to constantly be on the alert for threats. Talking through the company’s prospects, she repeats a certain phrase: “I know that this will ultimately get me in trouble, but…”

Trouble? Hollub and Occidental have known their share.

The drama surrounding Occidental’s 2019 acquisition of Anadarko would make for a good boardroom thriller—or at least a lively business-school case study. Anadarko had big assets in the crucial Permian Basin region of Texas and New Mexico, where horizontal drilling in shale rock had reinvigorated an aging oil field into the nation’s biggest production zone.

Hollub and her team made an offer to buy Anadarko after months of research. She thought she had a deal locked, only to hear on the radio that Anadarko had announced plans to combine with Chevron. She nearly drove off the road, Texas Monthly recounts.

Hollub turned to Buffett for help. He agreed to what was effectively a $10 billion loan at 8% interest, in the form of preferred shares, along with warrants that allow Berkshire Hathaway, Buffett’s company, to buy more common stock. That got Hollub what she wanted, but many on Wall Street hated it. “The Buffett deal was like taking candy from a baby and amazingly she even thanked him publicly for it!” Icahn wrote in a letter to his fellow shareholders. Icahn had bought a slug of Occidental’s shares and, in the ensuing months, the billionaire investor led a shareholder campaign against Hollub, insisting that she needed stronger board oversight. Icahn allies were made Occidental directors.

In 2020, as COVID-19 flattened the global economy, deeply indebted Occidental was forced to cut its dividend for the first time in decades. Buffett sold his stock. At Icahn’s urging, the company issued 113 million warrants to its shareholders, allowing them to buy shares at $22, at a time when the stock was trading at $17. Gary Hu, one of the Icahn directors on Occidental’s board, pointed to those warrants as evidence of their success. “Our involvement in Occidental represented activism at its finest,” said Hu.

Hollub flatly disagrees. Icahn saw an opportunity to make an easy profit in derailing the Anadarko deal, Hollub said. “And what he expected is that we would lose and he would benefit from that. Since that didn’t happen, he managed to maneuver his way onto the board.” Icahn’s representatives on the board came to Hollub with a number of plans, including the warrants. She felt that one wouldn’t do any harm. “So that’s what we agreed to, but yeah, the other 10 or so weird things, we didn’t do.”

““She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us.””

— Bill Smead, founder of Smead Capital Management

Former Occidental CEO Stephen Chazen returned to chair the board at Icahn’s insistence. Icahn and Occidental ultimately reached a settlement. His board members left, and the activist sold his common shares earlier this year. Chazen passed away in September. The experience embittered both sides, but there is one point of agreement: Hollub will do as she sees fit. “We were clearly wrong about the board’s ability to restrain Vicki’s ambitions,” Hu said.

Icahn made a $1.5 billion profit. At a MarketWatch event in September, Icahn said he still holds the warrants. But he hasn’t let go of the issues that motivated him to push into Occidental in the first place, though he insists he has no problem with Hollub personally. He likened her to a kid who got lucky gambling in Vegas. “The system allowed her to do it. And she’s just one small example of what is wrong with corporate governance.”

But as Icahn has himself shown, the system of corporate money in America is malleable. Its players can learn the rules of the game and adapt. Quarter after quarter since the dark days of the pandemic, Hollub turned up on corporate earnings calls pledging to keep cash flows strong, to invest in the highest-returning assets, and not to fall into the trap of overinvesting in debt-fueled or expensive production capacity, as so many failed shale producers have done in the past. She’s driven the company’s debt from nearly $40 billion following the Anadarko acquisition to less than $20 billion today. She increased the company’s dividend earlier this year. Along the way she transformed from market pariah to textbook CEO.

Hollub and other CEOs who run America’s biggest shale-oil producers have learned from the industry’s past mistakes. After proving a decade ago they could successfully extract shale oil, many U.S. oil producers were cheered on by growth and momentum stock investors as they borrowed billions to ramp up production, only to have those same investors abandon them after Saudi Arabia induced a plunge in oil prices. In the years that followed, U.S. shale-oil producers cultivated a new set of more value-oriented shareholders by promising they would share in profits through dividends and stock buybacks. Hollub and many of those other CEOs are not interested in chasing unrestrained growth again.

The world’s most famous value investor is now also on board. For Buffett, an earnings call Hollub led in February was the turning point. “I read every word, and said this is exactly what I would be doing. She’s running the company the right way,” Buffett told CNBC. Berkshire Hathaway BRK.A, +0.15%

started buying Occidental stock soon after. In August, federal regulators gave Buffett’s company permission to buy up to half of the company. (Asked for comment, a representative of Berkshire Hathaway asked for questions by email but did not respond to them.)

The markets are rife with speculation that Buffett will go all the way and purchase the entire company, though neither Hollub nor Berkshire have said as much. Hollub said simply that Buffett is bullish on oil, so she expects him to invest for the long haul. A Buffett buyout wouldn’t necessarily be a win for the investors who’ve hung on as Occidental’s stock price has recovered. “I’d probably make more money if he doesn’t buy it,” said Smead.

Warren Buffett is back to betting on Hollub and bought 20% of Occidental’s stock this year.

Johannes Eisele/Agence France-Presse/Getty Images

Where Hollub might cause real trouble is in the fight to keep carbon dioxide out of the earth’s atmosphere. That’s not because she’s a climate-denier. Far from it. Like many of her fellow oil-and-gas CEOs in recent years, Hollub has come to see climate change not as a threat to the business, but as an opportunity to be managed.

“I know some people don’t want oil to be produced for very long, but it’s going to be,” Hollub said. For that to change, people have to start using less oil. “It’s not that the more supply we generate, then the more that people are gonna use. It’s all driven by demand,” she said. And even with an electric vehicle in every driveway, we’d still need to extract oil to produce plastics and to create airplane fuel, among other projects that fall under the category of hard-to-abate emissions.

Hollub’s plan for Occidental is to wrap the company around that lingering stream of demand for hydrocarbons. She says Occidental is now in the business of carbon management, a euphemism that glides over the messiness of the climate transition and companies’ role in it. Companies need to show anxious shareholders that they’re serious about reducing their carbon emissions, but they also need to keep operating in an economy that is still seriously short on meaningful alternatives to fossil fuels. Occidental is here to help, spurred along by a series of state and federal incentives that the company lobbied for over years, culminating in the passage this year of the Inflation Reduction Act.

Climate advocates have for years tried to make the use of fossil fuels reflect their full cost on the environment. That has put them deeply at odds with oil-and-gas executives like Hollub, who opposes carbon taxes. It’s also left U.S. climate policy stalled as the planet warms. But the IRA tries something else. “I do not see the IRA as a handout to the energy industry,” said Sasha Mackler, executive director of the energy program at the Bipartisan Policy Center, a D.C. think tank. Rather than making dirty energy more expensive, the IRA tries to make clean energy cheaper, Mackler said. And that’s something Hollub can get on board with. She’s selling the idea that a barrel of oil can be clean.

Getting to a net-zero barrel of oil, as Hollub calls it, involves literally rerouting the route carbon dioxide takes through the world. For companies like Occidental, CO2 isn’t just a planet-destroying waste product. It’s a critical input to the process of oil production. Engineers can use CO2 to essentially juice aging oil wells by pumping it underground to displace hydrocarbons. The process is called enhanced oil recovery, or EOR. Occidental is the industry leader, producing the equivalent of 130,000 barrels per day of EOR oil and gas as of 2020. And that oil can, in theory, be less impactful on the climate. “We have it documented that it takes more CO2 injected into the reservoir than what the incremental barrels from that CO2 that are produced will emit when they’re used,” she said.

The trick is where that injected CO2 comes from. The Permian is crisscrossed with thousands of miles of pipelines that bring CO2 to oil fields from as far away as Colorado. At the moment, the vast majority comes from naturally occurring reservoirs or as a byproduct of the production of methane. One of the strangest ironies of modern oil production is that companies like Occidental don’t actually have enough CO2. “There’s two billion barrels of resources remaining to be developed in our conventional reservoirs using CO2,” Hollub said.

So she and her team went out looking for more. Eventually they hit on the idea that’s encapsulated in the IRA. Instead of pulling CO2 out of the ground only to put it back, Occidental could divert some of the CO2 that’s being produced by so-called industrial sources, companies that would otherwise be dumping it into the atmosphere because, of course, there’s no business reason not to.

Finding companies that wanted to do the right thing with their waste CO2 turned out to be harder than Hollub thought. “We knocked on the doors of a lot of emitters,” Hollub said. They found one taker—a Texas ethanol producer that was willing to try a pilot. It was a decent start but not enough to unlock all those buried barrels.

That may soon change, driven by the IRA. The law puts new financial incentives behind those conversations Occidental was having with CO2 emitters. The IRA significantly beefed up the so-called 45Q tax incentive for companies to put CO2 permanently in the ground. Occidental can get $60 a ton in tax credits if the CO2 is stored in the process of pumping more oil for EOR, or $85 if the company just buries it.

There’s also a higher tier of incentives if companies obtain that CO2 using an experimental technology called direct air capture. Occidental is spending $1 billion to build what would be the world’s largest direct-air-capture facility in Texas, which you can loosely think of as a giant fan to suck ambient CO2 directly out of the atmosphere. Hollub plans to build as many as 70 by 2035.

The problem some see with this plan, and with Hollub and others’ efforts to shape legislation around it, is it tightens the economy’s dependence on fossil fuels rather than loosening it. Americans will now effectively pay Occidental to pursue more enhanced oil recovery. Those net-zero barrels of oil—should they materialize—might be better in climate terms than a traditional barrel. But that’s not the only alternative. Dollar for dollar, public money would be better spent on solar energy and other low-carbon options than on EOR, said Kurt House, who knows as much because he’s tried it. House got a Ph.D. at Harvard in the science of carbon capture and storage more than a decade ago and co-founded a company to put the idea into practice. “It is bad, bad economics,” he said. “If you pay people a million dollars a ton of CO2 sequestering, they will sequester a lot of CO2. But it’ll cost us. It’ll make solving global warming much, much, much, much, much more expensive.”

But Hollub isn’t likely to change course. “I would say to those who don’t like what we’re doing, who do they want to do this? Tell me who have they gotten to, that will commit to take CO2 out of the atmosphere?” she said. “This climate transition cannot happen as fast as some people want it to happen because the world can’t afford it,” Hollub said. “We’re looking at, you know, $100 to $200 trillion for this climate transition. We cannot spend that kind of money to make this transition happen without help from diverting some of the CO2 to enhanced oil recovery, which enables then the technology to be developed and to be built at a faster pace.” And in the meantime, Occidental can sell carbon offsets to companies like United Airlines, which is supporting the direct-air-capture facility.

Those companies can choose whether they want the CO2 Occidental is capturing to be buried, full stop, or used for more oil production. But it’s clear Hollub thinks EOR is a big part of the future for Occidental. She has often said that the last barrel of oil should come from EOR. “I think there could be a world where we do stop drilling new wells,” she said. “To increase recovery from the remaining conventional reservoirs is something that’s kind of like a best kept secret for the United States. Nobody very much realizes that, but that is there. And that gives us that longevity beyond what some people are forecasting,” Hollub said.

Hollub is well-aware of her critics. Perhaps that’s why she keeps looking around for signs of trouble. But even if it finds her, she doesn’t plan to change much. “I have no regrets,” she said.

In June 2020, Warner Music Group Corp. (NASDAQ:WMG) made some noise when it announced its arrival as a publicly traded music player. Press the fast-forward button and two years later, the company’s stock dipped below IPO levels.

MarketBeat.com – MarketBeat

As the music industry conglomerate slid into the low-20’s, the market tuned out talk of a comeback tour and volume dried up big time. That changed dramatically last week.

The trading volume was on full blast after Apple announced a plan to raise its prices on Apple Music and Apple TV+ (as well as the Apple One bundle which includes both services).

Warner Music Group shares jumped more than 8% on the news and continued to see elevated activity throughout the week. Spotify also moved higher.

Let’s listen in to why this is a potential catalyst for the group.

Why is Apple’s Price Increase Good For Warner Music Group?

Like everything else, consumers are paying more to listen to their favorite artists and binge-watch their favorite shows these days. Last week, Apple became the latest to hike the cost of its streaming services following Netflix, Disney+ and others.

Monthly subscriptions to Apple Music and Apple TV+ are going up by $1 and $2 respectively. This brings Apple Music to $10.99 per month and the Apple One bundle to $16.95 for individual plans.

Why? With licensing fees on the rise, content creation is getting more expensive. Meanwhile, ad spending is slowing. As a result, the consumer is asked to pay more and the streamers potentially make more.

Apple’s move impacts music services like WMG, Spotify, and Universal Music Group because these competitors are likely to raise their own prices. Spotify hasn’t budged from its $9.99 rate for over 10 years but management hinted at U.S. price hikes in its Q3 earnings call.

Warner Music Group is a special case. In addition to its digital music offerings, the company sells a full slate of old school vinyl, cassettes and CDs across music genres. All of these prices along with those of the clothing and accessories available at the Warner Music Store stand to trend higher. And absent a parallel increase in costs, WMG stands to rake in greater profits.

Near-term inflationary pressures aside, Apple’s decision signals that the streaming music industry has pricing power and a positive growth outlook. The company wouldn’t bump prices if it didn’t anticipate consumers will pay up, which suggests streaming demand will persevere over the long haul.

The ripple effect of the Apple increase is also a boon to content creators themselves. When prices go up, artists and songwriters bank more when their stuff gets streamed.

What is Warner Music Group’s Growth Strategy?

When you own four top record labels as WMG does, the growth can come from anywhere. Atlantic Records, Warner Records, Elektra and Parlophone make the company a greatest hits collection for all things music. Add in all the other music labels under the Warner umbrella and you get a catalog of more than 1.4 million copyrights, including classic and modern hits alike.

It is the diversified revenue streams that make WMG intriguing from an investment perspective. The below industry P/E and 2.4% dividend aren’t too shabby either.

Even though Warner Music covers all music mediums, digital is the clear growth driver. It’s no secret the world is shifting to streaming music platforms, leaving nostalgic physical music playing second fiddle.

In fiscal Q3, revenue increased 12% and profits more than doubled. The consolidated streaming business was a solid contributor and is expected to be leaned on going forward.

So too is international expansion. New music service launches like The Music Station creative hub in Spain and Warner Music Israel stand to augment growth. The company also recently partnered with Polish concert promoter BIG Idea.

And no media conglomerate would be complete without NFT exposure. A collaboration with Bose on the Stickmen Toys NFT collection peaked at the number two spot on Open Sea for 24-hour volume and topped the one thousand Ethereum milestone.

Will Warner Music Group Stock Keep Going Up?

Price increases seem likely to happen at Warner Music Group. Given the popularity of its artist portfolio and streaming services, this could send growth to higher decibels in 2023.

Prior to the Apple news, Wall Street was mostly bullish on WMG’s long-term prospects. Price increases that are absorbed by loyal music fans should only support this.

In fact, the last six research firms’ opinions of the stock have been bullish. A few weeks back, Goldman Sachs started coverage with a buy rating. This set the stage for others to chime in with buy ratings and similar targets, which imply at least 10% upside from here.

This would bring the stock back to its IPO level and a potential new base to build on. Yes, it’s been a rocky Nasdaq debut for WMG, but the band of buyers may be getting back together.

AMD shares rose as much as 6% in extended trading on Tuesday after the chipmaker indicated its server chip business will grow in the quarters ahead, even as earnings and quarterly guidance failed to meet Wall Street’s expectations.

Here’s how the company did:

Earnings: 67 cents per share, adjusted, vs. 68 cents per share as expected by analysts, according to Refinitiv.

Revenue: $5.57 billion, vs. $5.62 billion as expected by analysts, according to Refinitiv.

Overall, AMD’s revenue grew by 29% year over year in the fiscal third quarter, which ended Sept. 24, according to a statement. Net income fell 93% to $66 million, mainly because of AMD’s $49 billion acquisition in February of Xilinx, a maker of chips called field-programmable gate arrays.

On Oct. 6, AMD issued preliminary results for the fiscal third quarter that lagged guidance it provided in August, because of fewer chip shipments in a weaker PC market than expected. The stock fell almost 14%, its largest decline since March 2020. AMD has been preparing for the PC market to be lackluster in the fiscal fourth quarter, CEO Lisa Su said on a conference call with analysts.

For the full year, AMD said it sees $23.5 billion in revenue, down from the $26.3 billion forecast the company gave in August. Analysts polled by Refinitiv had expected $23.88 billion. The company contracted its adjusted gross margin outlook to 52% from 54% in August.

AMD said its Data Center segment generated $1.61 billion in revenue in the fiscal third quarter, up 45% and slightly below the StreetAccount consensus of $1.64 billion. The unit includes contributions from Xilinx and distributed computing startup Pensando, which AMD bought for $1.9 billion.

The chipmaker has seen healthy demand for shipments of its server chips that carry the code name Genoa. AMD plans to launch Epyc data center chips on Nov. 10.

“We’ve had very good progress at the North American cloud vendors and we continue to believe that although there may be some near-term, let’s call it optimization, of, let’s call it individual footprints and efficiencies at individual cloud vendors, over the medium term,” Su said. “As we go into 2023, we expect growth in that market, particularly customers moving more workloads to AMD, just given the strength of our product portfolio and overall general coming forward.”

Su said cloud revenue more than doubled and increased sequentially, while revenue from server makers targeting big companies was down sequentially. She said AMD has seen enterprise customers taking longer to make decisions and being slightly more conservative on capital expenditures.

The data center business “at least for now, looks decent, and quite a bit better than what’s going on with Intel,” said Stacy Rasgon, senior semiconductor analyst at Bernstein, in an interview on CNBC’s “Closing Bell: Overtime” after AMD announced its results. “There’s a lot of uncertainty about what they were going to say about data center, particularly in the wake of Intel’s report where Intel had called for the market to decline in Q4. This is probably why the stock is up now. The guide itself is quite weak, but it seems likely that it’s isolated to PCs.”

The Gaming segment produced $1.63 billion in revenue. That was up about 14% and in line with the $1.63 billion consensus among analysts surveyed by StreetAccount. The company touted healthy demand for console chips for Microsoft and Sony as the holidays approach.

The Embedded segment that includes some Xilinx sales delivered $1.3 billion, up from $79 million in the year-ago quarter and in line with the $1.3 billion StreetAccount consensus.

AMD’s Client unit, which the chipmaker had warned about in October, generated $1.02 billion in revenue. That was down nearly 40% but in excess of the $1.17 billion StreetAccount consensus. Four days after AMD gave preliminary results, technology industry researcher Gartner said third-quarter PC shipments fell 19.5%, the steepest decline the company has seen since it started following the market in the mid-1990s. During the quarter AMD announced Ryzen 7000 desktop PC chips, and the company pointed to positive reviews of the products.

AMD “worked closely with our customers to reduce downstream inventory,” Su said.

All four of the segments delivered slightly more revenue than AMD had said to expect in its October warning.

“We will continue to invest in our strategic priorities around the data center, embedded and commercial markets, while tightening expenses across the rest of the business,” Su said. The company will control operating expenses and headcount growth, said Devinder Kumar, AMD’s finance chief.

Notwithstanding the after-hours fluctuation, AMD stock has plummeted 58% so far this year, while the S&P 500 is down 19% over the same period.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

Low-volatility stocks are working in 2022

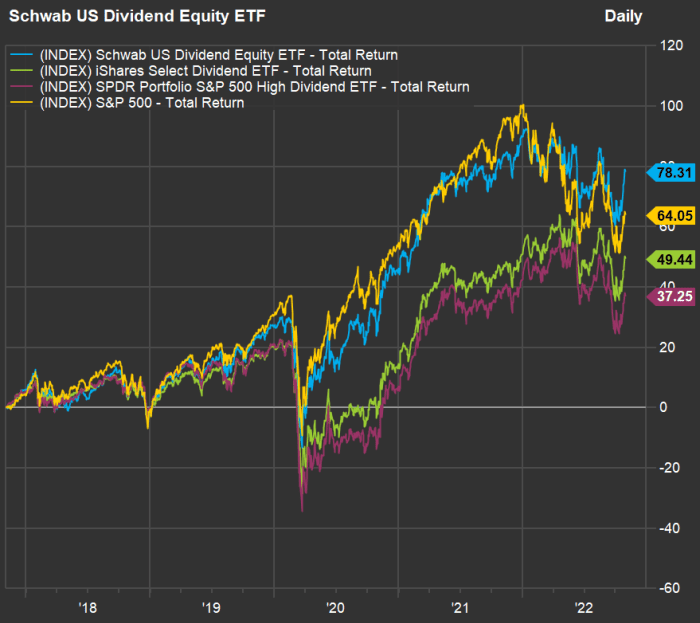

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

Oil and gas giant BP on Tuesday reported stronger-than-expected third-quarter profits, supported by high commodity prices and robust gas marketing and trading.

The British energy major posted underlying replacement cost profit, used as a proxy for net profit, of $8.2 billion for the three months through to the end of September. That compared with $8.5 billion in the previous quarter and marked a significant increase from a year earlier, when net profit came in at $3.3 billion.

Analysts polled by Refinitiv had expected third-quarter net profit of $6 billion.

BP announced another $2.5 billion in share repurchases and said net debt had been reduced to $22 billion, down from $22.8 billion in the second quarter.

It reported a net loss for the quarter of $2.2 billion, compared with a profit of $9.3 billion in the previous quarter. BP said this third-quarter result included inventory holding losses net of tax of $2.2 billion and a charge for adjusting items net of tax of $8.1 billion.

The world’s largest oil and gas majors have reported bumper earnings in recent months, benefitting from surging commodity prices following Russia’s invasion of Ukraine.

Combined with BP, oil majors Shell, TotalEnergies, Exxon and Chevron have posted third-quarter profits totaling nearly $50 billion.

This has renewed calls for higher taxes on record oil company profits, particularly at a time when surging gas and fuel prices have boosted inflation around the world.

U.S. President Joe Biden on Monday called on oil majors to stop “war profiteering” and threatened to pursue higher taxes if industry giants did not work to cut gas prices.

Oil and gas industry groups have previously condemned calls for a windfall tax, warning it would fail to resolve a sharp upswing in energy prices and could ultimately deter investment.

Read more about energy from CNBC Pro

“This quarter’s results reflect us continuing to perform while transforming,” BP CEO Bernard Looney said in a statement.

“We remain focused on helping to solve the energy trilemma – secure, affordable and lower carbon energy. We are providing the oil and gas the world needs today – while at the same time – investing to accelerate the energy transition,” Looney said.

Shares of London-listed BP rose nearly 1% during morning deals. The firm’s stock price is up over 45% year-to-date.

Environmental campaign groups said BP’s third-quarter results underscored the need for a windfall tax, describing the results as “a slap in the face” for the millions of Britons facing a deepening cost-of-living crisis.

“The case for a bigger, bolder windfall tax is now overwhelming,” said Sana Yusuf, energy campaigner at Friends of the Earth. “This must address the ridiculous loophole that undermines the levy by enabling companies to pay the bare minimum if they invest in more planet-warming gas and oil projects.”

“Some of the billions of pounds raised should be used to pay for a street-by-street, home insulation programme to cut energy bills and reduce emissions,” Yusuf said.

“A proper windfall tax on the profits of big polluters is no longer a far cry, it is now a necessity,” said Jonathan Noronha-Gant, senior fossil fuels campaigner at Global Witness.

“But the new U.K. Government must also urgently put us on track for a rapid transition away from dirty fossil fuels and onto renewables and decent home insulation, so we can fix this broken energy system once and for all.”

Speaking at the ADIPEC conference in the United Arab Emirates on Monday, BP CEO Bernard Looney said on a panel moderated by CNBC that he understood the public scrutiny on oil majors’ record profits, but sought to defend the firm’s record when it comes to investing and paying taxes.

“We are facing a very difficult winter ahead in the U.K., in Europe and right across the world,” Looney said.

“Our job is to pay our taxes; our job is to invest. We just announced a $4 billion acquisition in the United States just last week in renewable natural gas so that’s what our job is to do. We will continue to do that and do the very best that we can,” he added.

DUBAI, United Arab Emirates — Oil giant Saudi Aramco on Tuesday reported a $42.4 billion profit in the third quarter of this year, buoyed by the higher global energy prices that have filled the kingdom’s coffers but helped fuel inflation worldwide.

The oil firm’s profits will help fund the kingdom’s assertive Crown Prince Mohammed bin Salman’s plans for a futuristic city on the Red Sea coast, but also comes as the U.S. grows increasingly frustrated by higher prices at the pump chewing into American consumer’s wallets.

Those tensions yet again have chilled relations between Riyadh and Washington before the Nov. 8 midterm elections.

In a note to investors, the predominantly state-owned oil company said its average barrel of crude sold for $101.70 in the third quarter — up from $72.80 at the same point last year. It’s Aramco’s second-largest quarterly profit in its history, just before its second-quarter results this year saw a profit of $48.4 billion.

It put its profits so far in 2022 at $130.3 billion, compared to $77.6 billion in 2021.

“While global crude oil prices during this period were affected by continued economic uncertainty, our long-term view is that oil demand will continue to grow for the rest of the decade given the world’s need for more affordable and reliable energy,” Aramco CEO Amin H. Nasser said in a statement.

Aramco will keep its dividend this quarter at $18.8 billion, the world’s highest.

Benchmark Brent crude traded just shy of $95 a barrel Tuesday. The sliver of Aramco that the kingdom has put on Riyadh’s Tadawul stock market stood at $9.29 a share before trading Tuesday — putting its valuation at just over $2 trillion. Only Apple’s valuation, at $2.44 trillion, is higher.

OPEC and a loose confederation of other countries led by Russia agreed in early October to cut its production by 2 million barrels of oil a day, beginning in November.

OPEC, led by Saudi Arabia, has insisted its decision came from concerns about the global economy. Analysts in the U.S. and Europe warn a recession looms in the West from inflation and subsequent interest rate hikes, as well as food and oil supplies being affected by Russia’s war on Ukraine.

In Washington, anger has grown with Saudi Arabia, particularly from President Joe Biden, who traveled to the kingdom in July and shared a fist bump with Crown Prince Mohammed. Biden recently warned the kingdom that “there’s going to be some consequences for what they’ve done.”

Saudi Arabia lashed back, publicly claiming the Biden administration sought a one-month delay in the OPEC cuts that could have helped reduce the risk of a spike in gas prices ahead of the U.S. midterm elections.

Biden on Monday separately accused oil companies of “war profiteering” as he raised the possibility of imposing a windfall tax on American energy companies if they don’t boost domestic production.

———

Follow Jon Gambrell on Twitter at www.twitter.com/jongambrellAP.

A customer waits for his car at the garage of Avis Budget Group at the San Francisco airport.

David Paul Morris | Bloomberg | Getty Images

Check out the companies making headlines in after-hours trading.

Avis Budget Group – Shares of the budget care rental company jumped 2% following its quarterly results. Avis reported adjusted per-share earnings of $21.70, compared to expectations of $14.64 per share, according to Refinitiv.

Stryker – The medical technology company fell 5.5% after it reported a miss on the top line in its latest quarterly results. Stryker posted adjusted earnings per share of $2.12, compared to estimates of $2.23, according to Refinitiv. The company narrowly beat expectations on revenue.

Hologic – Shares of the medical supplier added 7.5% as it beat expectations of analysts’ expectations on top and bottom lines for the latest quarter, according to Street Account. For the fiscal year ending September 2023, the company expects earnings per share between $3.30 and $3.60 compared to FactSet’s expectation of $3.43, while revenue is expected by the company between $3.7 billion and $3.9 billion against the anticipated $3.81 billion.

Goodyear Tire & Rubber Company – Shares of the tire company tumbled more than 8%. Goodyear posted quarterly earnings per share of 40 cents on revenue of $5.31 billion. Analysts expected per-share earnings of 55 cents on revenue of $5.36 billion, according to Street Account.

IDEXX Laboratories – The science company with a focus on animals and water added 2.8% in post-market trading as investors looked to earnings coming Tuesday ahead of the market’s open.

Uber Technologies Inc. is scheduled to release third-quarter earnings Tuesday morning before trading begins in the U.S.

Analysts expect Uber UBER, -3.27%

to report a revenue increase of nearly 70% from a year ago, while the company’s losses are expected to narrow. Growth is largely expected to come from the company’s ride-hailing business, while its food-delivery business is expected to see slower growth after a pandemic-influenced boom.

What to expect

Earnings: According to FactSet, analysts on average expect Uber to post a loss of 18 cents a share, a strong improvement from the $1.28-a-share loss that the company reported in the same quarter a year ago — though that loss was influenced by a drop in shares of DiDi Global Inc. DIDIY, -3.03%,

and executives said adjusted losses in the third quarter last year were 17 cents a share. Estimize, which gathers estimates from analysts, hedge-fund managers, executives and others, expects the company to post a loss of 24 cents a share.

Revenue: Analysts on average expect revenue of $8.11 billion, according to FactSet, up from $4.85 billion a year ago. Estimize is expecting $8.37 billion.

Stock movement: In two of the past three quarters, Uber stock has fallen after the company reported earnings; it has risen after seven of the 14 reports the company has made since going public. Shares are down about 36% so far this year through Friday’s session, while the S&P 500 index SPX, -0.75%

has fallen about 19% year to date.

What analysts are saying

Analysts see a continued upside in both Uber’s ride-hailing and delivery businesses, but slower growth in delivery.

Aaron Kessler, an analyst for Raymond James who has an outperform rating on Uber’s stock, wrote in a note to clients that he estimates mobility bookings of $13.8 billion, up 40% year over year and 3.5% quarter over quarter.

Jason Heffstein, an analyst for Oppenheimer, also has an outperform rating on Uber shares. He wrote in a note that Oppenheimer has received numerous requests about the company’s long-term prospects, so he updated his total-addressable market analysis, which includes the following: “U.S. Mobility [is less than] 3% of [the] annual cost of car ownership, representing a compelling value proposition in a weakening macro environment.”

As for delivery, Kessler estimates bookings of $13.85 billion, which would be up 8% year over year and flat from the previous quarter. Heffstein estimates bookings to be up 9% year over year.

“We believe Uber’s superior network liquidity and leading logistics technology are well positioned to capture additional market share in ride-sharing … and online food delivery,” Heffstein wrote.

Apparently it’s Apple Inc. AAPL, +7.56%,

which is set to become the only mega-cap technology company not to see a sharp post-earnings decline in its stock price this week, after the smartphone giant delivered a somewhat mixed earnings report but seemed to reassure Wall Street just enough about the state of its demand.

The stock was up 7.6% in Friday morning trading and on track to log its largest single-day percentage gain since July 31, 2020, when it increased 10.5%, according to Dow Jones Market Data.

Apple is “the bright spot amid mega-cap carnage,” wrote Wells Fargo analyst Aaron Rakers, as Apple topped expectations with its headline results despite the backdrop of “a lot of macro/geopolitical uncertainties” as well as foreign-exchange pressures.

While Apple fell short with its iPhone sales numbers for the September quarter, Rakers noted that the company has been constrained by supply for its Pro models. At the same time, he noted that Mac revenue easily exceeded the consensus view, which supported his thesis that “Apple is solidly positioned as share taker in PCs.”

He further pointed out that Apple results were burdened by a deeper-than-expected impact from foreign exchange. But “look past the FX headwinds & you’ll see why everyone is hiding in Apple,” he said.

Rakers rates the stock at overweight with a $185 price target.

Evercore ISI’s Amit Daryanani called Apple “the last FAANG standing.”

“Overall, revenue and EPS estimates will shift higher from current levels and given the broadly disappointing EPS calls from big tech this was an impressive set of numbers and guide,” he wrote in his note to clients.

Though Apple didn’t give formal financial guidance, it offered various pieces of commentary around the December quarter, including that it could see a 10-point headwind from foreign exchange in the period and recognize a “few hundred” basis points of impact from an extra week being added to the quarter, even as Mac revenue is set for a substantial decline.

“All this results in our assessment that revenue growth will be mid-single digits (our model is at 5% vs. Street was at 2%),” Daryanani wrote.

Admittedly, it’s not just about the December quarter, he noted.

“Eventually the question will be on durability of demand beyond Dec-qtr and the impact from macro not just on iPhones but also services,” Daryanani wrote, though he likes Apple’s long-term potential to grow sales at a mid- or high-single-digit clip and grow earnings at a mid- to low-teens rate.

He rates the stock at outperform with a $190 target.

Wedbush’s Dan Ives wrote that Apple was “the one bright spot” amid “a horror show week for Big Tech earnings.”

“Given the perfect storm of currency/macro this quarter, we would characterize Apple’s results and commentary around the December quarter as net bullish around underlying demand and help throw out the noise that iPhone 14 upgrades are slowing in this cycle,” he wrote, while keeping an outperform rating but cutting his price target to $200 from $220 to reflect a lower multiple.

The latest results could help change what Citi Research analyst Jim Suva said was a relatively negative attitude towards Apple’s stock when compared to the rest of Big Tech.

“The amount of investor negativity on mega-cap tech stocks, especially Apple, is well known as recent surveys show Apple as the least favored stock amongst its peers,” he wrote. “Yes there are valid concerns of electronic retailers working down inventory and consumers having less disposable income given inflation but we believe consumers will adjust their spending allocations and continue to spend on Apple’s growing platform of products and services.”

He rates the stock a buy with a $175 price target, down from $185 before.

Barclays analyst Tim Long stayed more cautious.

“Stepping back from the print, things get tougher heading into Dec-Q and beyond and we maintain our [equal-weight] rating, mainly on headwinds sustaining current demand levels as high-end consumers potentially weaken, tougher comps on Mac, Services weakening further, regulatory overhang (App Store, Google TAC), macro impacting digital advertising as well as a rich valuation,” he wrote as he bumped his price target up by a dollar to $156.

Whether that plays out in the shares is another question.

“Near term, we expect heightened macro uncertainty to remain an overhang for the stock, although some may view AAPL as a relative safe haven in the macro storm,” Long continued.

Apparently it’s Apple Inc. AAPL, +7.56%,

which is set to become the only mega-cap technology company not to see a sharp post-earnings decline in its stock price this week, after the smartphone giant delivered a somewhat mixed earnings report but seemed to reassure Wall Street just enough about the state of its demand.

The stock was up 7.6% in Friday morning trading and on track to log its largest single-day percentage gain since July 31, 2020, when it increased 10.5%, according to Dow Jones Market Data.

Apple is “the bright spot amid mega-cap carnage,” wrote Wells Fargo analyst Aaron Rakers, as Apple topped expectations with its headline results despite the backdrop of “a lot of macro/geopolitical uncertainties” as well as foreign-exchange pressures.

While Apple fell short with its iPhone sales numbers for the September quarter, Rakers noted that the company has been constrained by supply for its Pro models. At the same time, he noted that Mac revenue easily exceeded the consensus view, which supported his thesis that “Apple is solidly positioned as share taker in PCs.”

He further pointed out that Apple results were burdened by a deeper-than-expected impact from foreign exchange. But “look past the FX headwinds & you’ll see why everyone is hiding in Apple,” he said.

Rakers rates the stock at overweight with a $185 price target.

Evercore ISI’s Amit Daryanani called Apple “the last FAANG standing.”

“Overall, revenue and EPS estimates will shift higher from current levels and given the broadly disappointing EPS calls from big tech this was an impressive set of numbers and guide,” he wrote in his note to clients.

Though Apple didn’t give formal financial guidance, it offered various pieces of commentary around the December quarter, including that it could see a 10-point headwind from foreign exchange in the period and recognize a “few hundred” basis points of impact from an extra week being added to the quarter, even as Mac revenue is set for a substantial decline.

“All this results in our assessment that revenue growth will be mid-single digits (our model is at 5% vs. Street was at 2%),” Daryanani wrote.

Admittedly, it’s not just about the December quarter, he noted.

“Eventually the question will be on durability of demand beyond Dec-qtr and the impact from macro not just on iPhones but also services,” Daryanani wrote, though he likes Apple’s long-term potential to grow sales at a mid- or high-single-digit clip and grow earnings at a mid- to low-teens rate.

He rates the stock at outperform with a $190 target.

Wedbush’s Dan Ives wrote that Apple was “the one bright spot” amid “a horror show week for Big Tech earnings.”

“Given the perfect storm of currency/macro this quarter, we would characterize Apple’s results and commentary around the December quarter as net bullish around underlying demand and help throw out the noise that iPhone 14 upgrades are slowing in this cycle,” he wrote, while keeping an outperform rating but cutting his price target to $200 from $220 to reflect a lower multiple.

The latest results could help change what Citi Research analyst Jim Suva said was a relatively negative attitude towards Apple’s stock when compared to the rest of Big Tech.

“The amount of investor negativity on mega-cap tech stocks, especially Apple, is well known as recent surveys show Apple as the least favored stock amongst its peers,” he wrote. “Yes there are valid concerns of electronic retailers working down inventory and consumers having less disposable income given inflation but we believe consumers will adjust their spending allocations and continue to spend on Apple’s growing platform of products and services.”

He rates the stock a buy with a $175 price target, down from $185 before.

Barclays analyst Tim Long stayed more cautious.

“Stepping back from the print, things get tougher heading into Dec-Q and beyond and we maintain our [equal-weight] rating, mainly on headwinds sustaining current demand levels as high-end consumers potentially weaken, tougher comps on Mac, Services weakening further, regulatory overhang (App Store, Google TAC), macro impacting digital advertising as well as a rich valuation,” he wrote as he bumped his price target up by a dollar to $156.

Whether that plays out in the shares is another question.

“Near term, we expect heightened macro uncertainty to remain an overhang for the stock, although some may view AAPL as a relative safe haven in the macro storm,” Long continued.

The Dow Jones Industrial Average rose nearly 600 points on Friday to its highest level in two months as the blue-chip gauge remained on track for a sixth straight session in the green in what would be its longest winning streak since May 27, according to Dow Jones Market Data.

All three major indexes were trading higher as expectations that the Federal Reserve will shift toward smaller interest-rate hikes after its November meeting have offset weak earnings this week from some of the market’s biggest megacap technology names.

How are stocks trading?

The S&P 500 SPX, +1.67%

gained 59 points, or 1.6%, to 3,866.

The Dow Jones Industrial Average DJIA, +1.98%

rose 589 points, or 1.8%, to 32,623.

The Nasdaq Composite COMP, +1.80%

advanced 181 points, or 1.7%, to 10,974.

Both the S&P 500 and Nasdaq were on track to cement their second weekly gain in a row on Friday, although the tech-heavy Nasdaq has substantially lagged after Thursday’s performance, where it was the only one of the major indexes to finish in the red following abysmal earnings from Meta Platforms Inc.

Barring an intraday turnaround, the Dow is on track to log its fourth straight weekly advance. It remains down just 10.2% so far this year.

The blue-chip gauge has risen 5% so far this week, while the S&P 500 is up 3.1% and the Nasdaq has risen 1.1%.

What’s driving markets?

All eyes were on the Dow Friday as the blue-chip gauge was the only major index to reach new notable highs late this week as its advance during the month of October has somewhat ameliorated its losses for the year so far.

The Dow has risen 13.5% since the start of the month, leaving it on track for its best October performance since it was created in the late 19th century.

Perhaps the biggest reason for the Dow’s rise this month is tied to its composition. The average is generally light on technology stocks, while including more of the energy and industrial stocks that have outperformed this year.

“The Dow just has more of the winners embedded in it and that has been the secret to its success,” said Art Hogan, chief market strategist at B.Reily Wealth.

Despite some volatility in the premarket session, all three major indexes turned higher after the open as investors remained fixated on expectations for the Fed to down shift to smaller interest rate hikes after next week’s policy meeting — an expectation that endured after the latest reports on inflation and wage growth released Friday.

Brad Conger, deputy chief investment officer at Hirtle, Callaghan & Co., said Friday’s data didn’t interfere with mounting expectations that the Fed might soon pause its campaign of aggressive rate hikes.

“Basically, the market is starting to price in a pause, not a pivot, but maybe a pause. The end is in sight,” Conger said.

The September core personal consumption expenditures price index — the Fed’s preferred gauge of inflation pressures — came in roughly in line with economists expectations, while a more modest 1.2% gain in private wages and salaries in the third quarter was interpreted as a sign that wage growth may have finally peaked, according to Andrew Hunter, senior U.S. economist at Capital Economics.

“The Federal Reserve has not yet broken the persistent trend in core inflation and so will likely stay aggressive at next week’s meeting. However, some areas of the economy show significant weakness and could build the case that the Fed downshifts to smaller rate hikes in 2023,” Jeffrey Roach, Chief Economist for LPL Financial in Charlotte, NC, said.

Since the start of the week, investors have digested a batch of disappointing numbers from some of America’s largest tech companies, which helped to sully the overall quality of S&P 500 earnings this quarter.

On Thursday night, Amazon.com AMZN, -9.29%

joined Microsoft Corp. MSFT, +2.75%,

Alphabet Inc. GOOGL, +2.76%

and Meta META, +0.34%

by publishing disappointing earnings for the quarter that ended Sept. 30.

But despite the disappointing results reported this week, in aggregate, S&P 500 firms are beating earnings expectations by 3.8%, according to Refinitiv data. That’s compared to a long-term average of 4.1% since 1994. However, if energy firms are excluded, the picture darkens substantially.

Shares of Amazon were off 10% after the e-commerce giant, which dominates the consumer-discretionary sector, predicted slower holiday sales and profit while also reporting slower-than-expected growth in its key cloud-computing business.

Peter Garnry, head of equity strategy at Saxo Bank, said investors were unnerved by Amazon’s guidance cut.

“The outlook for Q4 was what terrified investors with the retailer guidance operating income in the range $0-4 billion vs est. $4.7 billion and revenue of $140-148 billion vs est. $155.5 billion,” he said in a note.

One notable exception to the downbeat earnings news this week was Apple Inc. AAPL, +7.21%,

which proved a bright spot after the iPhone maker’s revenue and earnings topped forecasts, helped by record back-to-school sales of Macs. Shares were up nearly 0.9% in premarket trading.

Companies in focus

Oil giants Chevron Corp.CVX and Exxon Mobil Corp. XOM were climbing on Friday after reporting strong results. Chevron is a Dow component.

Intel Corp.INTC shares advanced more than 8% after reporting an earnings beat. The chip maker said it would cut costs by $3 billion next year, and lay off employees, as it trimmed its outlook again.