Kellanova (NYSE:K – Get Free Report) will be posting its quarterly earnings results before the market opens on Thursday, October 31st. Analysts expect Kellanova to post earnings of $0.85 per share for the quarter. Kellanova has set its FY24 guidance at $3.65-3.75 EPS and its FY 2024 guidance at 3.650-3.750 EPS.Persons that are interested in participating in the company’s earnings conference call can do so using this link.

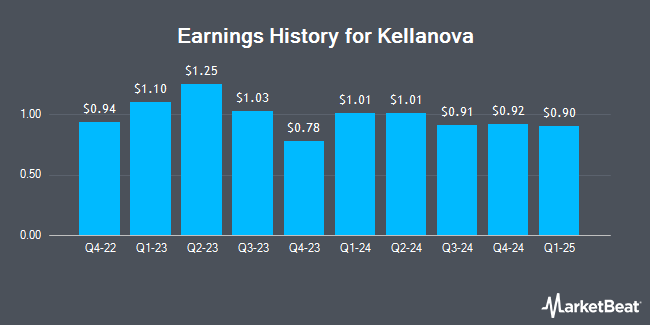

Kellanova (NYSE:K – Get Free Report) last posted its quarterly earnings results on Thursday, August 1st. The company reported $1.01 earnings per share for the quarter, topping analysts’ consensus estimates of $0.90 by $0.11. The firm had revenue of $3.19 billion for the quarter, compared to analyst estimates of $3.15 billion. Kellanova had a net margin of 6.72% and a return on equity of 36.74%. Kellanova’s quarterly revenue was down 4.7% on a year-over-year basis. During the same period in the previous year, the business posted $1.25 earnings per share. On average, analysts expect Kellanova to post $4 EPS for the current fiscal year and $4 EPS for the next fiscal year.

Kellanova Stock Performance

K opened at $80.60 on Tuesday. The firm has a market capitalization of $27.56 billion, a PE ratio of 30.19, a PEG ratio of 2.60 and a beta of 0.39. Kellanova has a twelve month low of $49.79 and a twelve month high of $81.26. The firm’s 50-day moving average price is $80.62 and its 200 day moving average price is $67.65. The company has a current ratio of 0.73, a quick ratio of 0.48 and a debt-to-equity ratio of 1.46.

Kellanova Dividend Announcement

The company also recently announced a quarterly dividend, which will be paid on Friday, December 13th. Shareholders of record on Monday, December 2nd will be issued a $0.57 dividend. This represents a $2.28 annualized dividend and a yield of 2.83%. Kellanova’s payout ratio is 85.39%.

Insider Activity

In other news, major shareholder Kellogg W. K. Foundation Trust sold 77,800 shares of the company’s stock in a transaction on Wednesday, August 7th. The shares were sold at an average price of $74.01, for a total value of $5,757,978.00. Following the completion of the transaction, the insider now owns 50,830,838 shares in the company, valued at approximately $3,761,990,320.38. This represents a 0.00 % decrease in their position. The sale was disclosed in a filing with the SEC, which is accessible through this link. In other news, major shareholder Kellogg W. K. Foundation Trust sold 77,800 shares of the company’s stock in a transaction on Wednesday, August 7th. The shares were sold at an average price of $74.01, for a total value of $5,757,978.00. Following the completion of the transaction, the insider now owns 50,830,838 shares in the company, valued at approximately $3,761,990,320.38. This represents a 0.00 % decrease in their position. The sale was disclosed in a filing with the SEC, which is accessible through this link. Also, major shareholder Kellogg W. K. Foundation Trust sold 114,583 shares of the stock in a transaction on Monday, September 16th. The stock was sold at an average price of $80.65, for a total transaction of $9,241,118.95. Following the sale, the insider now owns 50,368,272 shares of the company’s stock, valued at approximately $4,062,201,136.80. This represents a 0.00 % decrease in their position. The disclosure for this sale can be found here. In the last quarter, insiders sold 1,227,864 shares of company stock worth $98,438,243. Corporate insiders own 1.80% of the company’s stock.

Analyst Ratings Changes

K has been the topic of several recent analyst reports. Bank of America upgraded shares of Kellanova from a “neutral” rating to a “buy” rating and boosted their target price for the company from $62.00 to $70.00 in a report on Friday, August 2nd. Royal Bank of Canada lowered shares of Kellanova from an “outperform” rating to a “sector perform” rating and boosted their target price for the company from $76.00 to $83.50 in a report on Thursday, August 15th. Argus lowered shares of Kellanova from a “buy” rating to a “hold” rating in a report on Wednesday, October 2nd. DA Davidson lowered shares of Kellanova from a “buy” rating to a “neutral” rating and upped their price objective for the stock from $80.00 to $83.50 in a report on Monday, August 26th. Finally, Evercore ISI upgraded shares of Kellanova to a “hold” rating in a report on Friday, August 2nd. Fifteen analysts have rated the stock with a hold rating and two have given a buy rating to the stock. According to MarketBeat.com, Kellanova has a consensus rating of “Hold” and an average target price of $74.32.

Get Our Latest Analysis on K

About Kellanova

(Get Free Report)

Kellanova, together with its subsidiaries, manufactures and markets snacks and convenience foods in North America, Europe, Latin America, the Asia Pacific, the Middle East, Australia, and Africa. Its principal products include crackers, crisps, savory snacks, toaster pastries, cereal bars, granola bars and bites, ready-to-eat cereals, frozen waffles, veggie foods, and noodles.

Read More

Receive News & Ratings for Kellanova Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Kellanova and related companies with MarketBeat.com’s FREE daily email newsletter.