Amazon.com Inc.’s AMZN, -0.79%

layoffs will affect more than 18,000 employees, the highest reduction tally revealed in the past year at a major technology company as the industry pares back amid economic uncertainty.

The Seattle-based company in November said that it was beginning layoffs among its corporate workforce, with cuts concentrated on its devices business, recruiting and retail operations. At the time, The Wall Street Journal reported the cuts would total about 10,000 people. Thousands of those cuts began last year.

Looking at the worst-performing sectors, you might wonder why the consumer discretionary and communication services sectors have fared worse than information-technology, the core tech sector. One reason is that S&P Dow Jones Indices can surprise investors with its sector choices. The consumer discretionary sector includes Tesla Inc. TSLA, +0.70%

and Amazon.com Inc. AMZN, -1.17%,

which has fallen nearly 50% this year. The communications sector includes Meta Platforms Inc. META, -1.21%,

along with Match Group Inc. MTCH, +0.50%,

which is down 69% for 2022, and Netflix Inc. NFLX, -0.44%,

which is down 52% this year.

There have been many reasons easy to cite for Big Tech’s decline, such as a questionable change in strategy for Facebook’s holding company, Meta, as CEO Mark Zuckerberg has put so much of the company’s resources into developing a new world that most people don’t wish to enter, at least yet. Meta’s shares were down 64% for 2022 through Dec. 29.

You might also blame the Twitter-related antics and sales of Tesla shares by CEO Elon Musk for the 65% decline in the electric-vehicle maker’s stock this year. But Tesla had a forward price-to-earnings ratio of 120.3 at the end of 2021, while the S&P 500 SPX, -0.72%

traded for 21.4 times its weighted forward earnings estimate, according to FactSet. Those P/E ratios have now declined to 21.7 and 16.4, respectively. So Tesla no longer appears to be a very expensive stock, especially for a company that increased its vehicle deliveries by 42% in the third quarter from a year earlier.

Click on the tickers for more information about the companies.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Another way of measuring the biggest stock-market losers of 2022

It is one thing to have a large decline based on the share price, but that doesn’t tell the entire story. How much of a decline have investors seen in the holdings of their shares during the year? The S&P 500’s total market capitalization declined to $31.66 trillion as of Dec. 28 (the most recent figure available) from $40.36 trillion at the end of 2021, according to FactSet.

Shareholders of these companies have suffered the largest declines in market cap during 2022.

Restaurants are set to become the biggest winners of a holiday season that could turn out to be the most normalized since the onset of the pandemic.

That’s according to a new Mastercard SpendingPulse survey released on Monday, which showed spending at dining establishments surging 15.1% over the 2021 holiday period. Total retail expenditures for the Nov. 1–to–Dec. 24 period in 2022 rose 7.6%, with in-store spending up 6.8% and online spending up 10.6%.

Restaurant spending beat out several other categories, such as apparel, where spending was up 4.4% from 2021, and electronics and jewelry, where a respective 5.3% and 5.4% less were spent, and department stores, which saw spending rise 1%.

“This holiday retail season looked different than years past,” said Steve Sadove, senior adviser for Mastercard and former CEO and chairman of Saks Inc. “Retailers discounted heavily but consumers diversified their holiday spending to accommodate rising prices and an appetite for experiences and festive gatherings postpandemic.”

Government data for November showed consumer spending was up just 0.1%, reflecting cautiousness among households and price cutting by retailers to lure those hesitant shoppers in. But the data also showed more spending on holiday recreation and travel, expected to go in the books as a busy season even if deadly winter storm may have wreaked havoc on the plans of many Americans over the Christmas weekend.

Of course, even as some merrymakers felt confident enough to make more plans and see more friends and family this year, the virus of course continues to cause illness and death. The U.S. reported 70,000 newly diagnosed cases for the first time since September on Thursday, while 422 people died of COVID-19 on Wednesday.

The Mastercard SpendingPulse data measure in-store and online retail sales for all payment forms and are not inflation-adjusted.

As for the companies that might be benefiting from that increased traffic, the year-end cheer probably won’t be enough to make a dent in what has been a difficult year with would-be consumers juggling worries over inflation, rising interest rates and a war in Europe.

The Invesco Dynamic Leisure & Entertainment exchange-traded fund PEJ, +0.79%,

whose holdings include Chipotle Mexican Grill CMG, +0.32%,

McDonald’s MCD, +0.68%

and First Watch Restaurant Group FWRG, +0.42%,

has gained 6.5% to date in the fourth quarter and is down 20% for the year as of Thursday. The broad benchmark S&P 500 SPX, +0.59%

is poised for a nearly 20% loss in 2022.

Following a sharp and sustained rise in interest rates, U.S. stocks have taken a broad beating this year.

But 2023 may bring very different circumstances.

Below are lists of analysts’ favorite stocks among the benchmark S&P 500 SPX,

the S&P 400 Mid Cap Index MID

and the S&P Small Cap 600 Index SML

that are expected to rise the most over the next year. Those lists are followed by a summary of opinions of all 30 stocks in the Dow Jones Industrial Average DJIA.

Stocks rallied on Dec. 13 when the November CPI report showed a much slower inflation pace than economists had expected. Investors were also anticipating the Federal Open Market Committee’s next monetary policy announcement on Dec. 14. The consensus among economists polled by FactSet is for the Federal Reserve to raise the federal funds rate by 0.50% to a target range of 4.50% to 4.75%.

A 0.50% increase would be a slowdown from the four previous increases of 0.75%. The rate began 2022 in a range of zero to 0.25%, where it had sat since March 2020.

A pivot for the Fed Reserve and the possibility that the federal funds rate will reach its “terminal” rate (the highest for this cycle) in the near term could set the stage for a broad rally for stocks in 2023.

Wall Street’s large-cap favorites

Among the S&P 500, 92 stocks are rated “buy” or the equivalent by at least 75% of analysts working for brokerage firms. That number itself is interesting — at the end of 2021, 93 of the S&P 500 had this distinction. Meanwhile, the S&P 500 has declined 16% in 2022, with all sectors down except for energy, which has risen 53%, and the utilities sector, which his risen 1% (both excluding dividends).

Here are the 20 stocks in the S&P 500 with at least 75% “buy” or equivalent ratings that analysts expect to rise the most over the next year, based on consensus price targets:

Most of the companies on the S&P 500 list expected to soar in 2023 have seen large declines in 2022. But the company at the top of the list, EQT Corp. EQT,

is an exception. The stock has risen 69% in 2022 and is expected to add another 62% over the next 12 months. Analysts expect the company’s earnings per share to double during 2023 (in part from its expected acquisition of THQ), after nearly a four-fold EPS increase in 2022.

Shares of Amazon.com Inc. AMZN

are expected to soar 50% over the next year, following a decline of 46% so far in 2022. If the shares were to rise 50% from here to the price target of $136.02, they would still be 18% below their closing price of 166.72 at the end of 2021.

You can see the earnings estimates and more for any stock in this article by clicking on its ticker.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Mid-cap stocks expected to rise the most

The lists of favored stocks are limited to those covered by at least five analysts polled by FactSet.

Among components of the S&P 400 Mid Cap Index, there are 84 stocks with at least 75% “buy” ratings. Here at the 20 expected to rise the most over the next year:

Among companies in the S&P Small Cap 600 Index, 91 are rated “buy” or the equivalent by at least 75% of analysts. Here are the 20 with the highest 12-month upside potential indicated by consensus price targets:

One of the main advertising gimmicks of tonight’s Game Awards was a promotion being run by Valve that would see a viewer win one of the company’s prized Steam Deck handhelds every minute.

As we reported last week, to be eligible you had to be watching the show on Valve’s own Steam.TV website:

As announced November 30, Valve is celebrating The Game Awards with a massive Steam Deck giveaway. The company will be giving out a free handheld PC to a single person every minute for the entire run of The Game Awards. (Never in history has someone wanted The Game Awards to run long, until now…) To have a chance, you’ll need to first register for the drawing, which you can do now, then watch The Game Awards via Valve’s Steam.TV website.

During Christopher Judge’s acceptance speech, which, yes, did run long but was also incredibly emotional and heart-warming, the winners of Steam Decks started popping up. So while Judge was up there, pouring out his heart, the rest of us were witness to:

G/O Media may get a commission

People who were either disappointed (a minority) or who found it incredibly funny (the majority) began tweeting their congratulations to Mr or Mrs Hunter, which led at one point to “Milf Hunter” becoming a trending topic in the United States across all of Twitter.

Given “Milf Hunter” is also the name of a porn outlet, and The Game Awards have almost zero cultural penetration outside this bubble, you can understand some people’s confusion:

If you missed this, or any other Game Awards stuff, we’ve got you covered with this roundup, which includes everything from a Death Stranding 2 reveal, to a Hades 2 announcement, to Al Pacino.

What worked well during the years-long bull market through 2021 — a focus on growth, regardless of price — has ground to a halt this year. The rebirth of the value style of investing — and modest valuations overall — has taken hold.

The approach taken by the Invesco S&P 500 GARP ETF has paid off through both bull and bear markets.

Let’s begin with a 10-year chart comparing total returns with dividends reinvested for the Invesco S&P 500 GARP ETF SPGP, +0.67%

and the SPDR S&P 500 ETF Trust SPY, +0.78%,

which tracks the benchmark S&P 500:

FactSet

So far this year, SPGP is down 12%, while SPY is down 16%. But the long-term chart shows significant and consistent outperformance for SPGP, even during the bull market.

The S&P 500 GARP Index

GARP stands for “growth at a reasonable price.” SPGP tracks the S&P 500 GARP Index, which is reconstituted and rebalanced twice a year, on the third Fridays of June and December. The next change occurs Dec. 16.

S&P Dow Jones Indices assigns a growth score to each component of the S&P 500 by averaging the three-year compound annual growth rate (CAGR) for earnings and sales per share.

The top 150 components of the S&P 500 by growth score are eligible for inclusion in the GARP index. Those 150 are ranked by “quality/value composite score,” which is the average of these three ratios:

Financial leverage — total debt to book value.

Return on equity — trailing 12 months’ earnings per share divided by book value per share.

Earnings-to-price — 12 months’ earnings per share divided by the share price.

The top 75 of the 150 by QV rankings are then included in the GARP index and weighted by the growth score, with portfolio weightings ranging from 0.5% to 5%.

There is a weighting limitation of 40% to any one of the 11 S&P sectors.

Addressing concentration risk

The benchmark S&P 500 Index SPX, +0.75%

is weighted by market capitalization, which means it is more heavily concentrated than you might expect — success is rewarded, with rising stocks more heavily weighted over time.

That can backfire during a bear market, with Amazon.com Inc. AMZN, +2.14%

down 47% and Tesla Inc. TSLA, -0.34%

down 51% this year, to name two prominent examples.

Looking at the SPDR S&P 500 ETF Trust SPY, +0.78%,

which is the first and largest exchange traded fund and tracks the benchmark index by holding all of its components, six companies (Apple Inc. AAPL, +1.21%,

Microsoft Corp. MSFT, +1.24%,

Amazon, both common share classes of Alphabet Inc. GOOGL, -1.30%

That percentage has come down this year, but a lot of risk remains concentrated in a handful of companies. (Apple alone makes up 6.4% of the SPY portfolio. Tesla is now the ninth-largest holding, making up 1.4% of the portfolio.)

One way to address high concentration in an index fund is to use an equal-weighted approach, which Mark Hulbert recently discussed.

For the Invesco S&P 500 GARP ETF, the underlying index’s selection methodology has resulted in much less portfolio concentration than we see in SPY, with the top five holdings making up 10.9% of the portfolio.

Stock futures traded lower Monday as investors remained keyed on interest rate policy from the Federal Reserve and as a surge in China stocks over a loosening of Covid-19 restrictions in the country failed to boost U.S. equities.

Here are some stocks that could make moves Monday:

NEW YORK—Expressing skepticism about the unproven technology’s potential in the lead-up to the holiday season, Cyber Monday retailers reportedly worried this week that Americans were simply not ready to buy goods over the World Wide Web. “While there may be a few fringe dedicated Netizens interested in online holiday shopping, we’re not sure the average joe has the understanding or, frankly, interest needed to purchase goods in cyberspace,” said Best Buy vice president Scott Evans, echoing thousands of web retailers who noted that Americans have always enjoyed the atmosphere and experience of brick-and-mortar stores, and the rise of the information superhighway did not seem poised to change that. “I’ll admit I’m a bit in the dark on how it even works. People type ‘http://www.bestbuy.com’ into their web browser, sure, but what happens after that? Do they just send us a check in the mail? Plus, after they buy their item, who drives it to their house? Me? Our IT guy showed the whole thing to me, and it just went way over my head. So I can’t imagine how the average consumer feels. Computers are great for playing solitaire, but I think using them to buy goods is just more of a headache than it’s worth for most Americans.” Evans added that all of this was obviously purely hypothetical, given that the company only expected to get a few dozen online shoppers during the holidays.

GoKwik, which is India’s largest e-commerce enabler start-up, expects to onboard over 10,000 digital-first brands and ecommerce players on its platform by 2023 – a huge jump from around 500 brands that are currently part of the platform.

Currently, well-known brands like Limeroad, Mama Earth, Man Matters, Boat, The Man Company, Neemans, Lenskart, Shoppers Stop and Hopscotch among several others are part of GoKwik platform, which also boasts of more than 80 million shoppers in its network.

The platform had recently announced that it had successfully processed over $1 billion worth of orders in its network, and has seen a 520 per cent increase in number of transactions on an annual basis.

For the next phase of growth, GoKwik is aiming to bring over 10,000 brands under its network with an aim to create a unified ecommerce ecosystem by supporting small, medium, large and enterprise level brands.

It is specially building efficient models to cater to small merchants. These models include customisable WhatsApp commerce, robust address verification systems, easy and insightful dashboard offering uber level analytics, etc.

It is also strategically venturing into newer product categories, business segments and partnerships.

Founded in 2020 by industry veterans Chirag Taneja, Ankush Talwar and Vivek Bajpai, GoKwik helps solve problems that ecommerce brands face throughout the shopping experience, including enhancing customer experience, abandoned cart recovery, increasing conversions, boosting gross merchandise value (GMV) and reducing instances of return to origin (RTO).

GoKwik’s solutions have helped brands reduce RTO by 30 per cent and improve conversion rates by over 35 per cent. Incidentally, RTO happens due to a failed delivery of goods and directly impacts the revenues and profits of a brand.

“The last two years have been amazing, and we are even more excited for the next leg of our journey. As we grow further, we want to be even more committed to helping merchants realize more GMV, especially in the current macro-economic environment,” says Taneja, Co-Founder & CEO, GoKwik.

“We want to create products for ecommerce businesses of all sizes and provide solutions across the shopping funnel which can further their growth. From WhatsApp commerce, personalised payments stack, conversion optimisation solutions to evolved RTO protection models, we want to continue building products that solve ecommerce problem statements end to end,” he adds.

Amazon.com Inc. plans more layoffs, but employees will have to wait until 2023 to see if their jobs are affected.

Chief Executive Andy Jassy said Thursday that while Amazon AMZN, -2.34%

already confirmed that it was eliminating jobs in its devices and books businesses, an unknown number of layoffs impacting other teams are still to follow.

“Our annual planning process extends into the new year, which means there will be more role reductions as leaders continue to make adjustments,” he said in a blog post on the company’s corporate site. “Those decisions will be shared with impacted employees and organizations early in 2023.”

While Jassy doesn’t know “exactly how many other roles will be impacted,” he does know “that there will be reductions in our Stores and PXT organizations.” The company already announced a “voluntary reduction offer for some employees” working in PXT, or People Experience and Technology Solutions.

Jassy took over as Amazon’s CEO in July 2021 and said Thursday that “without a doubt,” the move to cut staff is “the most difficult decision we’ve made” since he’s been in the role.

“It’s not lost on me or any of the leaders who make these decisions that these aren’t just roles we’re eliminating, but rather, people with emotions, ambitions and responsibilities whose lives will be impacted,” Jassy said.

He added that Amazon “has weathered uncertainty and difficult economies in the past, and we will continue to do so.” Jassy emphasized that Amazon will continue to plug away on more established areas like stores, advertising and cloud computing, as well as newer initiatives like Prime Video, the Alexa voice assistant and healthcare.

Billionaire Jeff Bezos, who founded the e-retail behemoth Amazon, has some spending tips as Americans gear up for a holiday shopping season — amid four-decade high inflation and recession worries.

Here’s what he said:

“‘If you’re an individual and you’re thinking about buying a large-screen TV, maybe slow that down, keep that cash, see what happens. Same thing with a refrigerator, a new car, whatever. Just take some risk off the table.’”

Why did Bezos offer the tip for consumers and small business to go easy on big-ticket items? He gave one big reason.

“If we’re not in a recession right now, we’re likely to be in one very soon,” he said in the interview, picking up on his cautionary tweet last month that “the probabilities in this economy tell you to batten down the hatches.”

Bezos is currently executive chair at Amazon AMZN, -2.34%,

transitioning to the role last year as Andy Jassy took the reins as CEO.

“Critics have taken aim at these words of thrift coming from a man — now worth approximately $120 billion — who built Amazon into the online shopping bonanza.”

To be sure, Bezos is not alone is his worries about a potential recession as the Federal Reserve and other central banks fight higher costs by hiking interest rates.

But his advice prompted some guffaws on social media. In a nutshell, critics say these are words of thrift coming from a man — now worth approximately $120 billion — who built Amazon into the online shopping bonanza that lets consumers seamlessly spend money.

As Joshua Becker, a proponent of minimalism wrote on Twitter: “I didn’t hear him mention refraining from Amazon’s Prime Day deals or Black Friday offers, but I recommend adding those items to your list as well.”

Regardless of how anyone feels about hearing spending advice, particularly from one of the world’s richest people, there are some things to consider as events like Black Friday and Cyber Monday approach.

For one thing, maybe there are discretionary expenses where people can cut back. Many Americans are still spending briskly, as Walmart WMT, -0.34%

third-quarter earnings and October’s retail-sales numbers recently affirmed. Holiday-spending projections paint the same picture.

Americans will spend between $942.6 billion and $960.4 billion on holiday-season sales this year, according to projections from the National Retail Federation. Last year’s holiday sales totaled $889.3 billion, the trade association said.

“During the third quarter, Americans’ credit-card balances climbed to $930 billion, the biggest annual increase in more than 20 years, according to the National Retail Federation.”

But Americans are planning for the holidays while credit-card balances are increasing — likely because credit cards are helping them keep up with rising costs.

During the third quarter, Americans’ credit-card balances climbed to $930 billion, the biggest annual increase in more than 20 years, according to Federal Reserve Bank of New York data.

While balances grow, so do credit-card interest rates. The annual percentage rate (APR) on new credit-card offers averaged 19.14% in mid-November, according to Bankrate.com. That beats the old record on APRs for new cards, set at 19% three decades ago.

The holiday shopping season is typically when Americans accumulate credit-card debt, pay the debts in the early part of the coming year and repeat the holiday-season debt the following year.

This year, the stakes could be higher if high credit-card bills arrive and a recession-induced job loss follows.

“It’s not the time to overspend and have a problem with paying your bills later,” Michele Raneri, vice president of financial services research and consulting at TransUnion TRU, -4.94%,

one of the country’s three major credit bureaus, previously told MarketWatch. “We know the economy is sending mixed messages.”

HONG KONG (AP) — Chinese e-commerce company Alibaba Group on Thursday posted net losses and missed market expectations for revenue in its quarter ended September amid a slowing economy and depressed consumer sentiment.

The company reported net losses of 20.6 billion yuan ($2.87 billion) that it said was due to falling market prices of its equity investments in listed companies.

Revenue grew 3% compared to the same time last year to 207.2 billion yuan ($29 billion), as the company saw decreased consumer spending as China continued its strict COVID-19 policies with lockdowns and mass-testing.

“Consumer appetite was weak and we saw a drop in purchasing frequency,” said Alibaba chairman and CEO, Daniel Zhang on an investor call, adding that there was a drop in demand for categories such as consumer electronics and apparel.

The company also said that it would extend a share repurchase program to its 2025 fiscal year and will buy an additional $15 billion shares on top of an existing $25 billion share buyback program aimed at shoring up investor confidence. Zhang described the expansion of the buyback program as “tangible action towards enhancing shareholder return.”

Alibaba said it has so far bought back about $18 billion of its U.S.-listed shares.

The Hangzhou-based company reported its third-quarter financial results just days after the conclusion of its annual Singles’ Day online shopping festival, the world’s largest in terms of sales.

However, for the first time since it pioneered the festival in 2009, Alibaba did not disclose the final sales results for the shopping festival, suggesting a lower-than-expected result. Rival JD.com also did not release sales numbers this year.

Alibaba’s NYSE-listed stock was down about 2.8% in premarket trading.

Alibaba’s U.S.-listed stock has plunged over 70% since a regulatory crackdown on the technology industry in November 2020 that saw regulators halt the initial public offering of its financial arm Ant Group and crack down on anticompetitive practices across the technology industry.

The e-commerce firm is also facing increased competition from short-video platforms such as Douyin and Kuaishou which also offer e-commerce services on their platforms.

Alibaba is preparing for a primary listing in Hong Kong, making its shares more accessible to Chinese investors. The company said Thursday that the primary listing will not be completed by the end of 2022 as initially planned, and that it will keep investors updated in due course.

Shares of Chinese internet giants jumped in Hong Kong, after official data showed better-than-expected October retail sales in the world’s second-largest economy.

The sector’s sharp upturn came after China’s National Bureau of Statistics said online retail sales of physical goods rose 7.2% in the first 10 months of the year. The number, closely watched by investors as an indicator of the country’s consumption trends, outpaced a 6.1% rise in the January-to-September period.

Jefferies analysts estimate that online retail sales grew more than 15% in October, accelerating from the three consecutive months of below-10% growth seen since July.

The was once a golden age of PC gaming where you could open up Steam (or even just launch an executable yourself!), boot up a game and the next thing you would see would be the game itself. For many big (and small) releases those days are now long gone, replaced by an era of launchers that are, at best, a nuisance. Now, they’re even infecting indie projects like Kerbal Space Program.

If you want to play a Rockstar game on PC you need to install the company’s own launcher, which boots before you play the game you clicked to play, then makes you click another play button so you can finally play it. And that’s how it works when it’s working; when it’s not you simply can’t play any Rockstar games that you own, sorry!

Want to play a Total War game? You get a launcher. Paradox game? A launcher. Blizzard game? Battle.net. Fortnite? Epic Games Store. An EA game? Origin. Ubisoft? Hey, guess what, you gotta launch Ubisoft Connect, a launcher. Even Kalypso has a launcher.

While publishers have clear reasons to dump these things on us (from DRM to $$$), these launchers are wildly unpopular among players, in part because of the connectivity hassles (see Rockstar’s example above), but mostly because they’re just a pain in the ass, a speed bump on your way to the place you actually want to go.

G/O Media may get a commission

Things have hit a new level of absurdity this week, though, with news that Kerbal Space Program—yes, the one with the little aliens building rockets—now has its own launcher for the Steam version of the game, announced as “a resource for news and updates about KSP & KSP 2 Early Access.”

Publishers, please, we’re begging you. This sucks. As the best comment in that Steam discussion says, “GAMES ON STEAM DO NOT NEED A LAUNCHER. STEAM IS THE LAUNCHER.”

How good is a company’s chief executive officer at investing your money most efficiently? This is an important question for long-term investors. It may underline the difference between a steady long-term performer and a flash in the pan.

And Apple Inc. AAPL, -4.24%

now makes up 7% of the SPDR S&P 500 ETF Trust SPY, -1.03%,

the first and largest exchange-traded fund (with $360 billion in assets), which tracks the benchmark S&P 500 SPX, -1.06%.

That’s close to an all-time record, and the iPhone maker has a whopping 14.1% position in the Invesco QQQ Trust QQQ, -1.95%,

which tracks the Nasdaq-100 Index NDX, -1.98%.

Looking at the full Nasdaq Index COMP, -1.73%,

which has 3,747 stocks, Apple takes a 13.5% position.

Apple now makes up 7.3% of the S&P 500 by market capitalization, close to the 8% record it set late in September.

FactSet

This is very much an Apple stock market, with the company topping the broad indexes that are weighted by market capitalization. You are likely to be invested in the company indirectly. You also might be feeling Apple’s impact in other ways. Apple’s App Store ecosystem drives more than $600 billion in annual revenue for developers.

Tim Cook’s tenure as Apple’s CEO has been nothing short of breathtaking when measured by the company’s financial performance. Apple is not one of the fastest-growing companies when measured by sales or earnings — it is too big for that. But its excellent stock performance has reflected Cook’s ability to deploy invested capital with improving efficiency. Cook has also been a market trendsetter in other important ways. He has Apple repurchasing $90 billion of its shares annually, setting the pace for stock buybacks in the market. Cook’s steady hand has also helped Apple withstand the market’s tech wreck and remain a stable pillar for the teetering Nasdaq Composite index generally. For all these reasons, Cook has earned a spot on the MarketWatch 50 list of the most influential people in markets.

Apple keeps improving by this important measure

Investors in the stock market are looking for growth over the long term. The best measure of that is whether or not a company’s share price goes up or down. But Cook isn’t just managing Apple’s stock. Digging a bit deeper into the company’s actual operating performance can provide some insight into what a good job Cook has done.

What should a corporate manager focus on? The stock price? How about the most efficient and most profitable way to provide goods and services? There are different ways to do this, and Apple has focused on quality, reliability and excellent service to build customer loyalty.

Apple’s commitment can be experienced by anyone who calls the company for customer service. It is easy to get through to a well-trained representative who will solve your problem. How many companies can say that at a time when it seems many companies cannot even handle answering the phone?

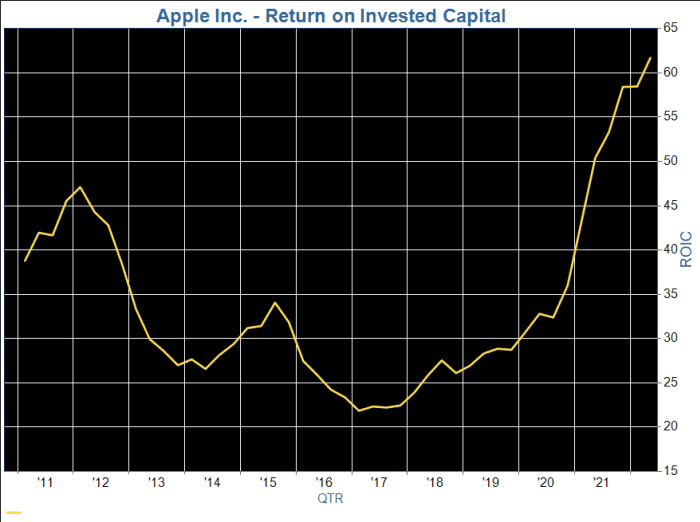

Apple’s returns on invested capital have increased markedly over the past six years.

FactSet

A company’s return on invested capital (ROIC) is its profit divided by the sum of the carrying value of its common stock, preferred stock, long-term debt and capitalized lease obligations. ROIC indicates how well a company has made use of the money it has raised to run its business. It is an annualized figure, but available quarterly, as used in the chart above.

The carrying value of a company’s stock may be a lot lower than its current market capitalization. The company may have issued most of its shares long ago at a much lower share price than the current one. If a company has issued shares recently or at relatively high prices, its ROIC will be lower.

A company with a high ROIC is likely either to have a relatively low level of long-term debt or to have made efficient use of the borrowed money.

Among companies in the S&P 500 that have been around for at least 10 years, Apple placed within the top 20 for average ROIC for the previous 40 reported fiscal quarters as of Sept. 1.

As you can see on the chart, Apple’s ROIC has improved dramatically over the past five years, even as the wide adoption of the company’s products and services has led to an overall slowdown in sales growth.

A quick comparison with other giants in the benchmark index

It might be interesting to see how Apple stacks up among other large companies, in part because some businesses are more capital-intensive than others. For example, over the past four quarters, Apple’s ROIC has averaged 52.9%, while the average for the S&P 500 has been a weighted 12.1%, by FactSet’s estimate.

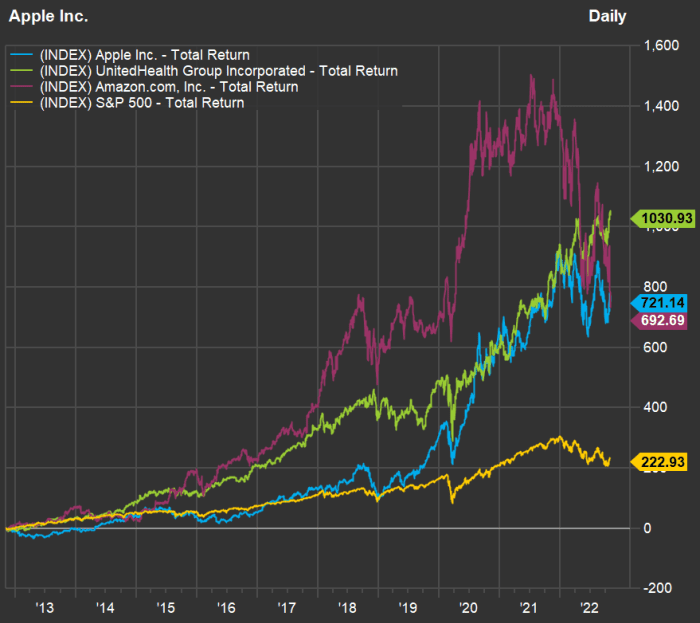

Here are the 10 companies in the S&P 500 reporting the highest annual sales for their most recent full fiscal years, with a comparison of average ROIC over the past 40 reported quarters:

Among the largest 10 companies in the S&P 500 by annual sales, Apple takes the top ranking for average ROIC over the past 10 years, while ranking second for total return behind UnitedHealth Group Inc. UNH, +0.03%

and ahead of Amazon.com Inc. AMZN, -3.06%.

UnitedHealth has been able to remain at the forefront of managed care during the period of transition for healthcare in the U.S., in the wake of President Barack Obama’s signing of the Affordable Care Act into law in 2010.

Here’s a chart showing 10-year total returns for Apple, UnitedHealth Group, Amazon and the S&P 500:

FactSet

Apple is only slightly ahead of Amazon’s 10-year total return. But what is so striking about this chart is the volatility. Apple has had a smoother ride. During the bear market of 2022, Apple’s stock has declined 18%, while the S&P 500 has gone down 20%, the Nasdaq has fallen 32% (all with dividends reinvested) and Amazon has dropped 45%.

The broad indexes would have fared even worse so far this year without Apple.

The swift recent decline in Amazon.com Inc.’s stock has brought the company’s closing market value below $1 trillion for the first time in more than two years.

Amazon shares AMZN, -0.82%

fell 5.5% in Tuesday action, finishing with a market value of $987 billion. This marked the first time since April 6, 2020 that Amazon closed out of trillion-dollar territory, according to Dow Jones Market Data.

Amazon’s valuation fell below the trillion-dollar milestone Tuesday.

Dow Jones Market Data

Amazon shares have tumbled 19.74% over the most recent five-session stretch. That five-day decline was the worst five-day loss for Amazon since its 22.03% plunge during the period that ended Nov. 20, 2008.

The e-commerce giant has come under recent pressure after the company’s latest earnings report highlighted a slowdown in AWS cloud-computing revenue growth. Additionally, Amazon disappointed with the forecast it offered for the holiday quarter.

“Combined with wobbles on revenue momentum for both AWS and retail, and suddenly the Amazon hiding place doesn’t look good,” Bernstein analyst Mark Shmulik wrote following Amazon’s earnings report last Thursday. “The good news here is that the story isn’t broken, it’s just pushed out into 2023, while Q4 may get worse before it gets better.”

When looking at companies worth more than $200 billion, Amazon is currently closest to seeing its stock hit its pandemic-era low, according to Dow Jones Market Data. Amazon shares closed Thursday at $96.79, 15.5% above their pandemic low of $83.83. Only shares of Meta Platforms Inc. META, -2.30%

have actually plunged below their pandemic low, among this grouping of the largest U.S. companies.

Uber Technologies Inc. is scheduled to release third-quarter earnings Tuesday morning before trading begins in the U.S.

Analysts expect Uber UBER, -3.27%

to report a revenue increase of nearly 70% from a year ago, while the company’s losses are expected to narrow. Growth is largely expected to come from the company’s ride-hailing business, while its food-delivery business is expected to see slower growth after a pandemic-influenced boom.

What to expect

Earnings: According to FactSet, analysts on average expect Uber to post a loss of 18 cents a share, a strong improvement from the $1.28-a-share loss that the company reported in the same quarter a year ago — though that loss was influenced by a drop in shares of DiDi Global Inc. DIDIY, -3.03%,

and executives said adjusted losses in the third quarter last year were 17 cents a share. Estimize, which gathers estimates from analysts, hedge-fund managers, executives and others, expects the company to post a loss of 24 cents a share.

Revenue: Analysts on average expect revenue of $8.11 billion, according to FactSet, up from $4.85 billion a year ago. Estimize is expecting $8.37 billion.

Stock movement: In two of the past three quarters, Uber stock has fallen after the company reported earnings; it has risen after seven of the 14 reports the company has made since going public. Shares are down about 36% so far this year through Friday’s session, while the S&P 500 index SPX, -0.75%

has fallen about 19% year to date.

What analysts are saying

Analysts see a continued upside in both Uber’s ride-hailing and delivery businesses, but slower growth in delivery.

Aaron Kessler, an analyst for Raymond James who has an outperform rating on Uber’s stock, wrote in a note to clients that he estimates mobility bookings of $13.8 billion, up 40% year over year and 3.5% quarter over quarter.

Jason Heffstein, an analyst for Oppenheimer, also has an outperform rating on Uber shares. He wrote in a note that Oppenheimer has received numerous requests about the company’s long-term prospects, so he updated his total-addressable market analysis, which includes the following: “U.S. Mobility [is less than] 3% of [the] annual cost of car ownership, representing a compelling value proposition in a weakening macro environment.”

As for delivery, Kessler estimates bookings of $13.85 billion, which would be up 8% year over year and flat from the previous quarter. Heffstein estimates bookings to be up 9% year over year.

“We believe Uber’s superior network liquidity and leading logistics technology are well positioned to capture additional market share in ride-sharing … and online food delivery,” Heffstein wrote.