It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index SPX, -2.80%

tumbled 2.8% on Friday, the Dow Jones Industrial Average DJIA, -2.11%

fell 630.15 points, or 2.1%, and the Nasdaq Composite Index COMP, -3.04%

dropped 3.8%. An early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

The S&P 500 is down about 24% for the year, while the Dow is off 19% and the Nasdaq nearly 32%.The 10-year Treasury rate TMUBMUSD10Y, 3.889%

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

U.S. stocks finished sharply lower Friday, but still booked their best weekly gains in a month, after September jobs data showed an unexpected fall in the unemployment rate that’s anticipated to reinforce the Federal Reserve’s resolve to keep tightening monetary policy.

Investors also weighed a profit warning at a leading microchip maker ahead of next week’s increase in quarterly earnings results.

What happened

The Dow Jones Industrial Average DJIA, -2.11%

fell 630.15 points, or 2.1%, ending at 29,296.79, but off the session low of 29,142.66.

The S&P 500 SPX, -2.80%

dropped 104.86 points, or 2.8%, closing at 3,639.66.

The Nasdaq Composite COMP, -3.80%

shed 420.91 points, or 3.8%, to finish at 10,652.40.

Stocks posted back-to-back losses, trimming weekly gains, but recorded their best weekly gains since Sept. 9, according to Dow Jones Market Data.

Stocks recorded sharp losses Friday after the Labor Department said the U.S. economy added 263,000 jobs in September, while the unemployment rate declined to 3.5% from an August reading of 3.7%. Average hourly earnings rose 0.3%.

Still, a powerful rally earlier in the week boosted all three major stock indexes to weekly gains, a departure from three straight weekly losses, according to Dow Jones Market Data.

“It’s manic. We are all on edge,” said Kent Engelke, chief economic strategist at Capitol Securities Management, of the sharp market swings.

“Any piece of good news is a cause for an explosive rally,” Engelke said by phone. On the flip side, he pegged technology-based trading “in an illiquid and emotional market” as exacerbating Friday’s selloff.

“It’s a reflection that people have re-entered the mind-set that the Fed is going to be raising rates at a rapid clip, probably for longer than what they might have suspected at the start of the week,” said Robert Pavlik, a senior portfolio manager at Dakota Wealth Management, by phone.

Pavlik expects the Fed to keep tightening financial conditions to try to head off inflation. “But once we turn the corner, and the economy slows down, the Fed probably will be more aggressive in cutting rates on the way down.”

In addition, the Fed has been “draining liquidity from the system at a remarkable pace,” wrote Rick Rieder, BlackRock’s chief investment officer of global fixed income, in a Friday client note, while pointing to an astounding $1.3 trillion decline in the central bank’s balance sheet since the December 2021 peak.

Pavlik at Dakota Wealth said he anticipates the Fed will start slowing interest rate hikes by mid-next year, which likely means continued pressure for the stock market, particularly with a backdrop of big oil-price CL00, +5.37%

gains this week after global crude producers voted to cut monthly production and with the U.S. dollar’s DXY, +0.44%

surge this year against a basket of rival currencies.

U.S. crude oil prices climbed for a fifth day in a row on Friday to settle at $92.64 a barrel, while booking at 16.5% weekly gain.

New York Fed President John Williams said Friday that benchmark interest rates likely need to hit 4.5% over time. The Fed’s policy rate now sits in a 3%-3.25% range, up from a zero-0.25% range a year ago.

The benchmark 10-year Treasury rate TMUBMUSD10Y, 3.889%

climbed to 3.883% Friday, as the key metric used to gauge the affordability of credit for businesses, household and the economy posted 10 straight weeks of gains, according to Dow Jones Market Data.

Investors continued to hope for relief on the inflation front and will be monitoring next week’s release of the September consumer-price index, as well as corporate earnings season as it picks up.

Companies in focus

Twitter Inc. TWTR, -0.43%

shares fell 0.4% Friday after a judge delayed a looming trial between the company and Elon Musk to allow the Tesla Inc. TSLA, -6.32%

CEO more time to close his $44 billion acquisition of the social media platform.

Besides the jobs report, investors weighed a profit warning from microchip maker Advanced Micro Devices Inc.AMD, which said the PC market weakened significantly during the quarter. AMD shares fell 13.9%, and rivals including Nvidia Corp. NVDA and Intel Corp. INTC also closed lower.

U.S. cannabis stocks were choppy Friday, with the AdvisorShares Pure US Cannabis ETF MSOS, -2.80%

ending lower, following steep gains earlier in the week after President Joe Biden said the U.S. would consider de-scheduling cannabis from its current position as a Schedule 1 narcotic under federal law.

—Steven Goldstein contributed reporting to this article

It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index SPX, -3.03%

tumbled 1.9% on Friday, the Dow Jones Industrial Average DJIA, -2.39%

was down 1.5% and the Nasdaq Composite Index COMP, -3.89%

was off 2.6%. And early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

The S&P 500 is down about 23% for the year, the Dow off 19% and the Nasdaq off 31% since January. The 10-year Treasury rate TMUBMUSD10Y, 3.884%

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

U.S. stock indexes ended modestly lower on Wednesday, despite briefly turning positive in the final hour of trading, while data showed steady growth in private-sector jobs and in the service sector, indicating more scope for the Federal Reserve to continue to raise interest rates.

How stocks traded?

The Dow Jones Industrial Average DJIA, +0.03%

lost 42.45 points, or 0.1%, to finish at 30,273.87

The S&P 500 SPX, +0.21%

was off 7.65 points, or 0.2%, ending at 3,783.28

The Nasdaq Composite COMP, +18.82%

shed 27.77 points, or 0.2%, to end at 11,148.64

On Tuesday, the Dow jumped 825 points, or 2.8%, while the S&P 500 increased 3.1% and the Nasdaq Composite rallied 3.3%.

What drove markets?

Wall Street stocks finished in the red after three main indexes bounced back from earlier losses in the final hour of trade, following a strong September private employment report in the morning.

Data released Wednesday showed that private-sector payrolls rose by 208,000 in September, indicating steady growth and supporting the view that the Fed has enough scope to keep raising interest rates. Economists surveyed by The Wall Street Journal had expected a rise of 200,000.

The report came two days before the closely watched nonfarm payrolls data issued by the Bureau of Labor Statistics. Investors are eying on it for important guidance on the Fed’s policy stance in the November meeting.

Friday’s employment report is expected to show the economy added 275,000 jobs in September, compared with 315,000 new positions added in August, according to a survey polled by Dow Jones.

“That certainly could move the needle,” said Kristina Hooper, chief global market strategist at Invesco. “Again, it doesn’t mean that it actually is going to change the market, but it could be the catalyst for short term rally if we get a disappointing jobs report.”

“But keep in mind, that’s just the anticipation of a Fed pivot based on data. But that does not ensure a Fed pivot. And so it could be one of those short-term rallies like the one we saw earlier this week,” Hooper said.

In other data Wednesday, an ISM barometer of U.S. business conditions in the service sector dipped to 56.7% in September but still showed steady growth and rising employment in a sign the economy is still expanding.

The U.S. trade deficit in August fell to $67.4 billion, the lowest level since mid 2021, paving the way for a resumption of growth in gross domestic product in the third quarter.

The S&P 500 had just enjoyed its largest two day percentage gain since April 2020 on Monday and Tuesday, and the best start to a quarter since 1938, according to Dow Jones Market data.

The bounce followed three quarters of declines, the worst such run since 2008, during which time the S&P 500 fell 24.8% to a near two-year trough as investors worried that the Federal Reserve’s interest rate hikes to crush inflation would harm the economy.

Brian Mulberry, client portfolio manager at Zacks Investment Management, believes the volatility in the stocks will continue because markets are getting a very “consistent message” from the Fed.

“Given what has happened over the last five trading sessions alone, we would be basically telling our clients to tighten your seatbelt a little bit because it’s definitely going to continue to be a bumpy ride,” Mulberry told MarketWatch in a phone interview on Wednesday. “If we get a ‘Goldilocks’ (jobs) report, that would mean decent economic activity is going on. That’s good for earnings overall in the market, but it’s not growing to a point where interest rates would have to be ratcheted up another 125 basis points by the end of the year.”

One major reason behind the rise early this week was the view that the Fed would pivot away from its aggressive monetary tightening.

Johanna Chua, chief Asia economist at Citi, said that though U.S economic growth remained in better shape than other countries and Fed officials continued to sound hawkish, the market risked being wrongfooted by any signs that interest rates could soon peak.

“Even as the overall fundamental setup has not changed… trimming of bearish risk/bearish rates/bullish USD positions has driven a sharp reversal,” Chua said.

Mary Daly, president of the Federal Reserve Bank of San Francisco said Wednesday that the Federal Reserve needs to keep raising its benchmark interest rate in order to cool inflation that hit a 40-year high earlier this year and has shown little signs of cooling. Atlanta Fed President Raphael Bostic will speak at 4 p.m. Eastern.

CLX22,

rose $1.24, or 1.4%, to settle at $87.76 a barrel on the New York Mercantile Exchange.

The S&P 500’s energy sector SP500.10, -0.07%

rose 2.1% following the news, up 12.6% over the last three trading days. According to Dow Jones Market Data, it was the best three-day percentage gain since November 2020 when it gained 16.1%. Shares of Schlumberger SLB, +0.77%

gained 6.3% at the close, while Exxon Mobil XOM, +1.32%

shares advanced 4%.

Companies in focus

Shares of Helen of Troy Ltd. HELE, -2.75%

finished 3.4% higher Wednesday, after the consumer products company, with brands including OXO, Hydro Flask and Braun, reported fiscal second-quarter earnings that beat expectations but cut its full-year outlook, as rising inflation has prompted consumers to change their spending patterns.

Shares of Monopar Therapeutics Inc. MNPR, +6.36%

gained 1.8% after the company said it completed enrollment in a Phase 2b clinical trial evaluating its experimental therapy aimed at preventing severe oral mucositis in patients undergoing chemoradiotherapy for oropharyngeal cancer.

Shares of Eiger BioPharmaceuticals Inc. EIGR, +0.85%

tumbled 5% after the company said it will not pursue emergency authorization of its experimental treatment for mild and moderate COVID-19 infections.

Shares of Lamb Weston Holdings Inc. LW, +2.45%

ended 4.2% higher Wednesday, after the potato supplier reported fiscal first-quarter profit that beat expectations, higher prices helped offset a volume decline.

Billionaire investor Ray Dalio is having a change of heart about cash. The founder of Bridgewater Associates, one of the world’s largest hedge funds, had been calling it “trash” since the purchasing power of cash diminishes amid rising inflation. Late Monday, he tweeted about his shift in thinking. “The facts have changed and I’ve changed my mind about cash as an asset: I no longer think cash is trash,” he wrote. “At existing interest rates and with the Fed shrinking the balance sheet, it is now about neutral—neither a very good or very bad deal. In other words, the short-term interest rate is now about right.” Cash as an asset has started to come back into focus as higher interest rates have led to it finally providing some return. The market turmoil also has investors looking for a safer bet. The Dow Jones Industrial Average and S & P 500 notched their biggest monthly losses in September since 2020. The Dow ended the quarter down 6.66%, finishing its third consecutive negative quarter for the first time since the third quarter of 2015. The S & P 500, meanwhile, hit a three-quarter losing streak for the first time since 2009. While stocks started October off with a rally, experts expect the turbulence to continue as the Federal Reserve continues to hike rates and fears about a possible recession grow. In September, Dalio predicted a rise in rates to about 4.5% will drag the economy down and result in a 20% plunge in equity prices.

While September lived up to its reputation as a brutal month for stocks, October tends to be a “bear-market killer,” associated with historically strong returns, especially in midterm election years.

Skeptics, however, are warning investors that negative economic fundamentals could overwhelm seasonal trends as what’s traditionally the roughest period for equities comes to an end.

Rough stretch

U.S. stocks ended sharply lower on Friday, posting their worst skid in the first nine months of any year in two decades. The S&P 500 SPX, -1.51%

recorded a monthly loss of 9.3%, its worst September performance since 2002. The Dow Jones Industrial Average DJIA, -1.71%

fell 8.8%, while the Nasdaq Composite COMP, -1.51%

on Friday pushed its total monthly loss to 10.5%, according to Dow Jones Market Data.

October’s track record may offer some comfort as it has been a turnaround month, or a “bear killer,” according to the data from Stock Trader’s Almanac.

“Twelve post-WWII bear markets have ended in October: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002 and 2011 (S&P 500 declined 19.4%),” wrote Jeff Hirsch, editor of the Stock Trader’s Almanac, in a note on Thursday. “Seven of these years were midterm bottoms.”

According to Hirsch, Octobers in the midterm election years are “downright stellar” and usually where the “sweet spot” of the four-year presidential election cycle begins (see chart below).

“The fourth quarter of the midterm years combines with the first and second quarters of the pre-election years for the best three consecutive quarter span for the market, averaging 19.3% for the DJIA and 20.0% for the S&P 500 (since 1949), and an amazing 29.3% for NASDAQ (since 1971),” wrote Hirsch.

SOURCE: STOCKTRADERSALMANAC

‘Atypical period’

Skeptics aren’t convinced the pattern will hold true this October. Ralph Bassett, head of investments at Abrdn, an asset-management firm based in Scotland, said these dynamics could only play out in “more normalized years.”

“This is just such an atypical period for so many reasons,” Bassett told MarketWatch in a phone interview on Thursday. “A lot of mutual funds have their fiscal year-end in October, so there tends to be a lot of buying and selling to manage tax losses. That’s kind of something that we’re going through and you have to be very sensitive to how you manage all of that.”

An old Wall Street adage, “Sell in May and go away,” refers to the market’s historical underperformance during the six-month period from May to October. Stock Trader’s Almanac, which is credited with coining the saying, found investing in stocks from November to April and switching into fixed income the other six months would have “produced reliable returns with reduced risk since 1950.”

Strategists at Stifel, a wealth-management firm, contend the S&P 500, which has fallen more than 23% from its Jan. 3 record finish, is in a bottoming process. They see positive catalysts between the fourth quarter of 2022 and the start of 2023 as Fed policy plus S&P 500 negative seasonality are headwinds that should subside by then.

“Monetary policy works with a six-month lag, and between the [Nov. 2] and [Dec. 14] final two Fed meetings of 2022, we do see subtle movement toward a data-dependent Fed pause which would bullishly allow investors to focus on (improving) inflation data rather than policy,” wrote strategists led by Barry Bannister, chief equity strategist, in a recent note. “This could reinforce positive market seasonality, which is historically strong for the S&P 500 from November to April.”

October crashes

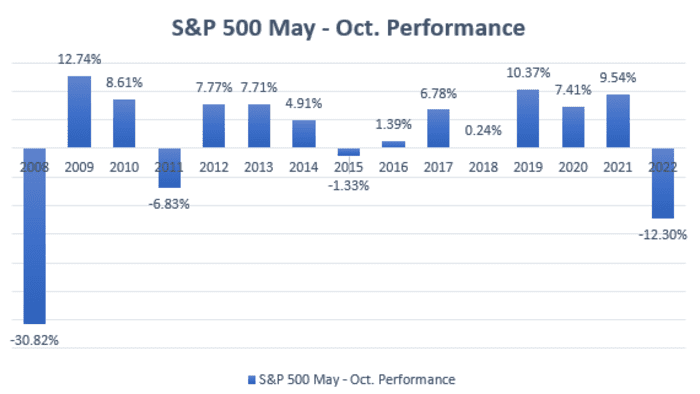

Seasonal trends, however, aren’t written in stone. Dow Jones Market Data found the S&P 500 recorded positive returns between May and October in the past six years (see chart below).

SOURCE: FACTSET, DOW JONES MARKET DATA

Anthony Saglimbene, chief markets strategist at Ameriprise Financial, said there are periods in history where October could evoke fear on Wall Street as some large historical market crashes, including those in 1987 and 1929, occurred during the month.

“I think that any years where you’ve had a very difficult year for stocks, seasonality should discount it, because there are some other macro forces [that are] pushing on stocks, and you need to see more clarity on those macro forces that are pushing stocks down,” Saglimbene told MarketWatch on Friday. “Frankly, I don’t think we’re going to see a lot of visibility at least over the next few months.”

It was a September investors will remember — and not in a good way.

A Friday drop left the S&P 500 and Dow Jones Industrial Average with their biggest monthly losses since March 2020. And it was the worst September performance for both indexes since 2002. Seasonally inclined investors may wonder what that means for October.

Dow Jones Market Data took a look at how equities have done in the wake of particularly brutal Septembers.

But first, how does the month just ended stack up? The S&P 500 SPX, -1.51%

fell 9.34%, while the Dow DJIA, -1.71%

dropped 8.84% and the Nasdaq Composite COMP, -0.43%

declined 10.5%. The Nasdaq’s drop marked its worst September performance since 2008.

Sample size is limited. Not counting the current month, the S&P 500 has seen a September decline of 7% or more 11 times, according to data going back to 1928. The Dow has dropped 7% or more in September 13 times based on data back to 1928. The Nasdaq Composite has suffered a fall of 9% or more in September six times going back to 1986.

Dow Jones Market Data found that in Octobers that follow a 7% or larger fall in September, the S&P 500 rises 0.53% on average in October and sees a median gain of 1.81%. That’s better than the average for all Octobers at 0.47% and the median at 1.03%. October is positive in years following an outsize September loss 54.55% of the time, versus 57.45% for all Octobers (see table below).

S&P 500

Category

7% or worse

All

Average

0.53%

0.47%

Median

1.81%

1.03%

Worst Performance

-16.94%

-21.76%

Best Performance

16.30%

16.30%

% of October’s higher

54.55%

57.45%

Seasonal patterns, however, are only a guide. As MarketWatch’s Isabel Wang noted in a Friday report, many strategists are skeptical of October’s reputation as “bear killer.” They argued that a macroeconomic environment dominated by central banks aggressively tightening monetary policy in a bid to wring out inflation is likely to overshadow favorable seasonal factors.

October is also associated with historical market crashes, including those in 1987 and 1929. The S&P 500 plunged nearly 17% in October 2008 following a 9.1% fall in September in the wake of the collapse of Lehman Brothers.

Dow Jones Market Data, meanwhile, found that in Octobers following a September drop of 7% or more, the Dow has seen an average fall of 1.51% and a median drop of 1.46%. That compares with an average rise of 0.37% for all Octobers and a median gain of 0.79%. The S&P 500 has risen 46.15% of the time in Octobers that follow a 7% or more September decline, versus a rise 57.6% of the time for all Octobers (see table below).

DJIA

Category

7% or worse

All

Average

-1.51%

0.37%

Median

-1.46%

0.79%

Worst Performance

-20.36%

-23.22%

Best Performance

10.60%

10.65%

% of October’s higher

46.15%

57.60%

And here are the numbers for the Nasdaq in October following a September drop of 9% or more:

Category

9% or worse

All

Average

2.19%

0.73%

Median

4.26%

2.16%

Worst Performance

-17.73%

-27.23%

Best Performance

17.17%

17.17%

% of October’s higher

50.00%

54.90%

Since 1950, September has been the worst performing month of the year for the Dow Jones Industrial Average, S&P 500 and Russell 1000 and the worst for the Nasdaq Composite since 1971 and the small-cap Russell 2000 since 1979, according to the Stock Trader’s Almanac.

U.S. stocks dropped sharply Friday, with major indexes posting their lowest finishes since 2020 and logging a third straight quarterly decline as investors grew more fearful that aggressive interest rate hikes by the Federal Reserve will drive the economy into a downturn in an attempt to quell inflation.

What’s happening

The Dow Jones Industrial Average DJIA, -1.71%

dropped 500.10 points, or 1.7%, to close at 28,725.51.

The S&P 500 SPX, -1.51%

dropped 54.85 points, or 1.5%, to end at 3,585.61.

The Nasdaq Composite COMP, -0.43%

shed 161.88 points, of 1.5%, finishing at 10,575.61.

The drop left the Dow and S&P 500 at their lowest since November 2020, while the Nasdaq posted its lowest close since July 29, 2020. The Dow dropped 8.8% in September, while the S&P 500 tumbled 9.3% and the Nasdaq lost 10.5%.

For the quarter, the Dow dropped 6.7%, the S&P 500 declined 5.3% and the Nasdaq gave up 4.1%.

What’s driving the market

In keeping with the historical pattern, U.S. stocks suffered during the month of September as an assertive Federal Reserve helped push Treasury yields and the dollar higher, which in turn undermined equity valuations.

Investors on Friday digested a reading from the personal consumption expenditure inflation index for August, which showed that core consumer prices climbed by 0.6% last month, more than Wall Street’s forecast of 0.5%. The core inflation measure excludes volatile food and energy prices.

“That means the Fed will remain hell-bent on killing inflation. And the best way to do that is to increase rates, kill the housing market, and get rental costs down. The PCE doesn’t have housing and rents as a big component as the CPI does, so the fact that it is rising is a warning sign,” said Louis Navellier, founder of Navellier & Associates, in emailed comments.

The reading largely confirmed similar data from the consumer-price index, another closely watched inflation barometer, which sent stocks lower earlier this month. Since that report was released just over two weeks ago, the S&P 500 has fallen more than 10%.

Helping to underscore this point, data out of the eurozone showed inflation accelerated at a record pace last month.

In other news, investors also heard from Fed Vice Chair Lael Brainard, who reiterated that the central bank would keep interest rates elevated to combat inflation, even if it harms the economy.

Since it will take time for high interest rates to bring inflation down, Brainard said the Fed is “committed to avoiding pulling back prematurely.”

Investors were also keeping an eye on megacap tech stocks. Apple Inc. AAPL fell 3% on Friday after leading markets lower a day earlier following a downgrade by Bank of America.

A final reading on the University of Michigan consumer-sentiment index for September showed consumers’ view of the economy improved somewhat during the month due to falling gas prices, even as their outlook remained broadly pessimistic.

Investors are now facing “what may be one of the most important earning seasons in a very long time, with a major rally in the cards if earnings don’t disappoint, and if the bears are right, lead to a further leg down if earnings disappoint and 4th quarter estimates are cut,” Navellier said.

Micron Technology MU, +0.18%

stock rose 0.2% after a report that Japan will grant it a $320 million subsidy to make advanced memory chips at its Hiroshima plant. That came a day after Micron posted quarterly earnings that included a forecast for a loss in the coming quarter and plans to scale back a build out of capacity.

— Steve Goldstein and Barbara Kollmeyer contributed to this article