Johnson & Johnson reported adjusted earnings and revenue that topped Wall Street’s expectations on Tuesday, and lifted its full-year forecast.

J&J, whose financial results are considered a bellwether for many health companies, said its first-quarter sales grew 5.6% over the same quarter last year.

The consumer staples giant reported a net loss of $68 million, or 3 cents per share, due to a special one-time charge. That’s compared to a net income of $5.2 billion, or $1.93 per share, for the same period a year ago. Excluding certain items, adjusted earnings per share were $2.68for the period.

Here’s how J&J results compared with Wall Street expectations based on a survey of analysts by Refinitiv:

Earnings per share: $2.68 adjusted, vs. $2.50 expected

Revenue: $24.75 billion, vs. $23.67 billion expected

J&J is now forecasting 2023 sales of $97.9 billion to $98.9 billion, about $1 billion higher than the guidance provided in January. The company raised its full-year adjusted earnings outlook to $10.60 to $10.70 per share, from a previous forecast of $10.45 to $10.65.

CFO Joseph Wolk told CNBC on Tuesday that J&J raised its guidance due to strong growth across all three business sectors — consumer health, pharmaceuticals and medtech.

“If you think about how we started the year and guidance in January, we were responsibly cautious,” he said on “Squawk Box.” “First-quarter growth was much stronger than even fourth-quarter growth for all three business units, and our positions kind of change to responsibly optimistic at this point. We feel very good about 2023.”

The company’s shares rose nearly 2% in premarket trading. The stock is down more than 6% for the year through Monday’s close, putting the company’s market value at roughly $430 billion.

But the New Brunswick, New Jersey-based company entered this earnings season with its shares on the rise after it offered more clarity on the long-running legal fight over its talc-based baby powder products. Earlier this month, J&J proposed to pay nearly $9 billion over the next 25 years to settle thousands of allegations that its baby powder and other talc products caused cancer.

During a period of high interest rates, it might be more difficult to impress investors with dividend stocks. But the stocks can have an important advantage over the long term. The dividend payouts can increase over the years, helping to push share prices higher over time.

When considering stocks for dividend income, yield shouldn’t be the only thing you consider. If a stock’s price has tumbled because investors are worried about the company’s business prospects, the dividend yield might be very high. A double-digit yield might mean investors expect to see a cut to the dividend soon.

There are many ways to look at companies’ expected ability to maintain or raise their dividend payouts. But one can also take a simple approach to begin researching stock choices.

For investors who would rather aim for long-term growth to go along with dividend income, or take a relatively conservative approach to growth while reinvesting dividends, a screen of stocks in the S&P 500 SPX, +0.33%

produces only 10 stocks with dividend yields of 4.5% or higher with majority “buy” or equivalent ratings among analysts polled by FactSet. Here they are, sorted by dividend yield:

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

The dividend yields for this group of 10 companies are based on current annual regular payout rates, with all paying quarterly except for Realty Income Corp. O, +1.30%,

which pays monthly.

These two oil and natural gas producers would have passed the above screen based on their most recent dividend payments and analysts’ sentiment, however, they pay a combined fixed-plus-variable dividend every quarter, with the fixed portion relatively low:

Shares of Pioneer Natural Resources Co. PXD, -0.77%

closed at $230 on April 14. Among analysts polled by FactSet, 59% rate the stock a “buy” or the equivalent, and the consensus price target is $257.42. The company pays a fixed quarterly dividend of $1.10 a share, which would make for a dividend yield of only 1.91%. However, the most recent variable quarterly dividend was $4.48 a share, for a combined quarterly dividend of $5.58, which would translate to an annualized dividend yield of 9.70%. The consensus estimate for dividends in 2025 is $4.63 — the analysts are only estimating the fixed portion of the dividend. Pioneer has held preliminary merger discussions with Exxon Corp. XOM, -1.16%,

according to a Wall Street Journal report.

Devon Energy Corp.’s DVN, -0.72%

stock closed at $55.70 on April 14. The shares are rated “buy” or the equivalent by 55% of analysts and the consensus price target is $67.66. The fixed portion of Devon’s quarterly dividend is 20 cents a share, for an annualized dividend yield of 1.44%. The variable portion of the most recent quarterly dividend was 69 cents a share. The total payout of 89 cents would make for an annual dividend yield of 6.39%. Analysts expect the fixed portion of annual dividends to total $3.61 in 2025, according to FactSet.

After a long period of underperformance when compared with the U.S. equity market, stocks in other countries are holding their own this year. One way to lower your overall risk with real diversification is to add exposure to an active international management style that doesn’t mirror a broad stock index.

One example is the $2.7 billion Columbia Overseas Value Fund COSZX, which is rated four stars out of five by Morningstar in its Foreign Large Value category. Fred Copper and Daisuke Nomoto co-manage the fund and described…

If you invest in dividend stocks, you are probably looking for long-term growth to go with the income. Otherwise you might be content to hold one-month U.S. Treasury bills, which yield 4.5% or park your money in an online savings account for a yield close to 4%.

Below is screen of stocks with current dividend yields ranging from 4.14% to 8.46%. What sets these apart from other stocks with high dividend yields is that their payout increases are expected to accelerate in 2023 and 2024 from those in 2022.

On Tuesday, S&P Dow Jones Indices said in a press release that it expected dividend payments by publicly traded U.S. companies to continue to hit record levels in 2023. But Howard Silverblatt, a senior index analyst with the firm, said that the pace of dividend increases in the first quarter had slowed and that he expected this year’s increases to be “at half the pace of the double-digit 2022 growth.”

Silverblatt also said current events in the banking industry were “expected to negatively impact future spending from both consumers and companies, which in turn may curtail corporate dividend growth.”

For many banks, there’s another big item on the table. A focus on share buybacks in recent years is very likely to end — this is a use of cash that can raise earnings per share if the share count is reduced, but there can be consequences, especially after a year of rising interest rates that pushed down the market value of banks’ investments in bonds.

In a note to clients on March 16, Dick Bove, a senior research analyst with Odeon Capital, predicted that stock repurchases in the banking industry would be “meaningfully cut back if not flat out eliminated.” He made three general points about buybacks in the banking industry:

Buybacks remove working capital that would otherwise provide returns to a bank.

Buybacks mean a bank’s board of directors is “in favor of flat-out giving capital away to investors that want nothing to do with the bank — they are selling its stock.”

Buybacks do “nothing to increase bank stock prices – many bank stocks are selling at below their prices of five years ago.”

A company might find it much easier to curtail or stop buying back shares to preserve cash than it is to cut regular dividends. Preserving and increasing the dividend over time has been correlated with good performance for stocks over time. These articles provide examples of how dividend compounding is correlated with long-term growth as income streams build up:

The S&P Dow Jones Indices report raises the question of which stocks might buck the trend.

Starting with the S&P 500 SPX, -0.50%,

there are 71 companies stocks with current dividend yields of at least 4.00% indicated by annual payout rates. Among these companies, 68 increased dividends during 2022, according to data provided by FactSet.

Then we looked at the pace of dividend increases in 2022 and the consensus estimates for dividends paid during 2023 and 2024, among analysts polled by FactSet. Among the remaining 68 companies, there are 29 for which the estimated 2023 dividend increase is higher than the 2022 dividend increase. Narrowing further, there are 14 for which the estimated 2024 dividend increases are higher than the estimated 2023 dividend increases.

Here are the 14 stocks that passed the screen, sorted by current dividend yield:

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Any stock screen is limited, but can be useful as a starting point or supplement to your own research. If you see any companies of interest, do some research to form your own opinion of how likely they are to remain competitive over the next decade, at least.

Forget about Treasury bills or certificates of deposit. Just look at the fat dividend yields now on offer among regional banks after the March meltdown triggered by the failure of Silicon Valley Bank, Signature Bank and Silvergate Capital. KeyCorp , an $11 billion market cap bank based in Cleveland, yielded 6.4% as of the Tuesday market close. Atlanta’s Truist Financial ($41 billion) now yields 6.2% while Minneapolis’s U.S. Bancorp ($53 billion) pays 5.1% on its common stock. The list goes on and on. Comerica of Dallas pays out the annual equivalent of 5.8%. Columbus, Ohio’s Huntington Bancshares wires to investors’ accounts or cuts checks equal to 5.5%. Cincinnati’s Fifth Third Bancorp pays 4.8%. Will the dividends be cut? Might some be omitted all together? After all, high dividend yields are often a sign of financial or business distress, or a red flag that the payments so many mom-and-pop investors depend on are unsustainable. That’s what happened during the Global Financial Crisis of 2008-2009, when bank after bank either passed the dividend or cut it to a token penny a share. It was just last week that embattled First Republic Bank, facing the withdrawal of a reported $70 billion in deposits , suspended its 27 cents quarterly dividend. Not this time But not this time. Wall Street just doesn’t think most payouts will be cut — so long as any recession this year stays on the mild side. Why’s the Street so sanguine? Because earlier banking crises were mostly caused by credit events. In 2008, Bear Stearns was lost in towers of mortgage-backed securities, while Lehman Brothers went belly up thanks to large positions in subprime mortgages. Years before, more than 1,000 savings and loans went bust in the S & L crisis , thanks to lax regulation, bad investments in commercial real estate and junk bonds, and a helping of fraud. In the 1980s, Continental Illinois National Bank and Trust loans to the oil patch went bad (creating the term “too big to fail”). So did Citigroup loans to Latin American sovereign governments. The challenge banks face today centers instead on the fastest rise in interest rates in two generations. Banks that hold Treasury bonds yielding 2% or mortgages at 4% suddenly find themselves in a higher-rate environment, and those bonds and mortgages held as capital have declined in price. “Unlike [2008-2009] or even 1990, those were credit debacles that crushed the banks, forced them to cut and eliminate dividends, pull back buybacks,” RBC Capital bank analyst Gerard Cassidy said on CNBC’s “Fast Money” on Monday. “This is an interest rate problem” and, in this environment, “banks know that if they maintain the dividends through the next cycle, which is maybe what we’re in right now, they will rerate coming out of the cycle. So dividend cuts I think [are] the last thing they need to do. Plus they’ve got strong capital levels today, unlike in 2007, plus they have plenty of liquidity, among the biggest banks.” As a reality check, CNBC ran a screen on the stocks in the Invesco KBW Bank ETF (KBWB), ranking them by the lowest dividend payout ratios , which measures dividends as a percentage of net income. We also looked at the yields themselves, plus the percentage of sell-side analysts rating the bank a buy and the potential upside if the stock hit the average analyst’s share price target. Looking outside that group of banks, New York Community Bancorp ‘s yield is more secure now after it bought most of the assets of Signature Bank earlier this week, according to Jenny Harrington, portfolio manager at Gilman Hill. Speaking on CNBC’s “Halftime Report” on Monday, Harrington argued that one bank’s loss is often another’s gain, saying that NYCB earnings will rise 20% as a result of the acquisition, and its book value expand by 15%. NYCB yielded 7.4% at Tuesday’s close. Little to no dividend growth The conventional wisdom today is that the pressure on bank profits makes the outlook for dividend growth in the sector more dicey, rather than jeopardizing the safety of current payouts. “Our dividend growth expectations have come down,” due to the fallout from Silicon Valley, Signature and First Republic, “as well as the economic impact of the Fed’s efforts to quell inflation via sharply higher rates over the past year,” Daniel Peris, head of the Strategic Value Dividend team at Federated Hermes, recently wrote. “Despite these lower dividend growth expectations, we believe these bank holdings still have attractive dividends,” Peris added. “Given a slowing economy we expect our banks to run their balance sheets more conservatively (and could be forced to via tougher regulation over the coming years); this would likely put a further damper on dividend growth.” A final straw in the wind: Wall Street has issued dozens of research reports since Silicon Valley Bank went under. Almost none of them so much as mention the word dividend. Take that as a sign most investors are confident the dividend checks will still roll.

Bank of America BAC, Citigroup C, JPMorgan Chase JPM and Wells Fargo WFC said Thursday that they are each making $5 billion in uninsured deposits into First Republic Bank FRC as part of a $30 billion backstop by 11 banks against the ravaged banking landscape of the past week.

However, First Republic stock fell 14.7% in after-hours trading after the bank said it would suspend its dividend to conserve cash. The bank last paid a quarterly dividend of 27 cents a share on Feb. 9 to shareholders of record as of Jan. 26.

(AMD) and has struggled to meet Wall Street’s earnings targets. Weighing on earnings is weak PC demand, with year-over-year declines in sales. A dividend cut this large may partly reflect the economic environment, but also the company’s own problems.

Dividend stocks have long been a way for investors to earn income, but recent cuts may have some concerned about what to do next. On Wednesday, Intel announced it was slashing its dividend by nearly 66%, to 12.5 cents per share from 36.5 cents. The new annualized dividend yield is 4.20%, down from 7.13%. The latest dividend is payable June 1 to shareholders on record as of May 7. Intel’s move comes after VF Corp cut its dividend by 41% to 30 cents from 51 cents earlier this month, causing it to be dropped from the S & P 500 Dividend Aristocrats Index . The index is made up of stocks that have increased their dividends in each of the past 25 years or more. The companies said the cuts were meant to best position them to create long-term value. However, those recent decreases are unusual, said Howard Silverblatt, senior index analyst at S & P Dow Jones Indices. Over the last 12 months, ending Jan. 31, five companies in the S & P 500 decreased their dividend, while 362 increased it, he said. In fact, dividends “are going to easily set a record this year,” Silverblatt said. He’s anticipating about a 5% to 6% increase in cash in investors’ pockets, even with Intel’s cut. In 2022, U.S. common dividend increases were up 5% to $82.5 billion from $78.6 billion in 2021, S & P Dow Jones Indices data show. Decreases were up 63% to $14.3 billion in 2022, compared with $8.8 billion in 2021. Where to look for income Corporate dividends are just one source of income, and that income should be just one part of your overall portfolio, said certified financial planner Jamie Hopkins, managing partner of wealth solutions at Carson Group. “When you’re looking at income from your investments you should consider all the available sources — CD ladders, bond ladders, dividend-paying equities and other fixed-income products like annuities — and figure out what is the cheapest way to buy that income,” he said. When looking for dividend stocks, history can be a guide. “Companies that tend to increase over time don’t cut them back as much during downturn times,” Hopkins said. However, as VF Corp’s and Intel’s recent cuts show, past performance does not guarantee future results. Some sectors have dividends that are more sensitive to earnings and therefore more susceptible to downward revisions, UBS wrote in a note Wednesday. Those include financials, real estate, media and entertainment, and tech hardware and equipment, the firm said. Sectors with dividends less cyclical to earnings include energy, health-care equipment and services, semiconductors and transportation, according to UBS. Grant suggests looking at utility stocks, which generally pay a pretty good dividend. Preferred stocks and real estate investment trusts are another area to consider, although there may be some volatility, he said. Dividend funds Another option is an exchange-traded fund composed of dividend stocks. There are all different types of funds available, from those that track the S & P 500 Dividend Aristocrats Index to high-yielders. There are also funds that stick to a certain sector, like utilities. However, not all will cut a stock if the company slashes its dividend. Therefore, if income is your goal, look for those that focus on names that have a history of raising dividends. “In general, companies that have increased their dividends five to six years in a row, it is part of their culture,” said Silverblatt. “It is in their cash flow.” For instance, the SPDR S & P Global Dividend ETF is composed of 100 high-dividend yielding stocks and measures the performance of the S & P 500 Dividend Aristocrats Index. It currently has a dividend yield of 5.14%, according to FactSet. WDIV YTD mountain SPDR S & P Global Dividend ETF’s year-to-date performance The ProShares S & P 500 Dividend Aristocrats ETF , also tracks the index. Holdings are equal-weighted and the ETF is rebalanced at the same time as the index. It currently has a dividend yield of 2.42%, according to FactSet. For Mike Moray, Integrity Viking Funds’ chief investment officer, a history of raising dividends is a key metric his team uses when deciding to keep a name in their Dividend Harvest Fund . There have been two times since the fund’s inception in 2012 that companies have been removed for dividend cuts, he said. The fund’s managers try to be proactive in assessing companies, which means some have been removed before they decrease their dividends. “We haven’t been 100% immune,” Morey said. “Strong free cash flow and a history of consecutive dividend raises have made us much more buffered from dividend cuts.” Laddering bonds and CDs Another way to earn income is through bonds, which have been enjoying high yields. The rate on the 10-year Treasury hit its highest level since November on Tuesday, briefly trading 3.95%. One strategy to capture that income and manage interest rate risk is to build a ladder of bonds of varying maturities. As each issue matures, you can decide to reinvest the proceeds into new bonds. The same thing can be done with certificates of deposit, or CDs, said CFP Don Grant, an investment advisor with Sabre Wealth. Interest rates on CD could hit 5.5% this year, Morgan Stanley recently predicted. However, don’t just go to your local bank. Instead, shop the entire country either through a broker or online, Grant advised. “Different regions will pay different interest rates based on their regional demand for money and their real estate,” he said. Depending on your income needs, he suggests a ladder of 3-month duration CDs to two years. Annuities Purchasing an annuity , which is issued by an insurance company, can also provide income. Just pay attention to fees, advised Grant. A fixed-index annuity links its potential return to market indices. A multiyear guaranteed annuity, or MYGA, offers a guaranteed fixed interest rate for a set period of time. “They are paying pretty good income streams now,” said Carson Group’s Hopkins. Take some profits If you need cash, there’s nothing wrong with taking some profits, Grant said. “Let’s say you have some appreciated stock. Go ahead and sell some of it and take off what you’ve earned,” he said. “Strip some growth. Use that as income.” — CNBC’s Michael Bloom contributed reporting.

beat earnings and revenue estimates in the fourth quarter, driven by higher prices. It increased its annual dividend, sending the stock higher in premarket trading Thursday.

The beverages and snacks giant (ticker:PEP) reported adjusted earnings per share (EPS) of $1.67 on sales of $28 billion. Analysts were expecting EPS of $1.65 on sales of $26.8 billion.

Intel Corp. continues to cut costs for everything except payments to investors.

Intel INTC, +3.03%,

which is already in the process of cutting what is believed to be thousands of jobs amid steep declines in profit and revenue, is reducing Chief Executive Pat Gelsinger’s base salary by 25% and trimming other salaries at a descending rate based on seniority, down to 5% cuts for midlevel positions, a person familiar with the matter told MarketWatch. While nonexempt workers and junior positions face no pay cuts, Intel is trimming its 401(k) contributions to 2.5% from 5% and will suspend merit raises and quarterly performance bonuses, the person said. Annual performance bonuses and stock grants will remain.

In an emailed statement, an Intel spokesperson confirmed “several adjustments to our 2023 employee compensation and rewards programs.”

“As we continue to navigate macroeconomic headwinds and work to reduce costs across the company, we’ve made several adjustments to our 2023 employee compensation and rewards programs,” the statement said. “These changes are designed to impact our executive population more significantly and will help support the investments and overall workforce needed to accelerate our transformation and achieve our long-term strategy. We are grateful to our employees for their commitment to Intel and patience during this time as we know these changes are not easy.”

Intel has not touched its dividend, though, even as its free cash flow fell into the red during 2022 and is expected to be negative again this year. The chip maker paid out roughly $1.5 billion in dividends in the fourth quarter, completing $6 billion in annual payments, and maintained the same level of payments for the first quarter despite analysts questioning whether the company can afford it.

“The board [and] management, we take a very disciplined approach to the capital allocation strategy and we’re going to remain committed to being very prudent around how we allocate capital for the owners, and we are committed to maintaining a competitive dividend,” Chief Financial Officer David Zinsner said when asked directly about the dividend during Intel’s earnings call last week.

Intel shares have declined 42.1% in the past 12 months, as the S&P 500 SPX, +1.30%

has dropped 10.3% and the Dow Jones Industrial Average DJIA, +0.36%

— which counts Intel as one of its 30 components — has fallen 3.7%.

Most investors want to keep things simple, but digging a bit into details can be lucrative — it can help you match your choices to your objectives.

The JPMorgan Equity Premium Income ETF JEPI, +0.20%

has been able to take advantage of rising volatility in the stock market to beat the total return of its benchmark, the S&P 500 SPX, +1.19%,

while providing a rising stream of monthly income.

The objective of the fund is “to deliver a significant portion of the returns associated with the S&P 500 Index with less volatility,” while paying monthly dividends, according to JPMorgan Asset Management. It does this by maintaining a portfolio of about 100 stocks selected for high quality, value and low price volatility, while also employing a covered-call strategy (described below) to increase income.

This strategy might underperform the index during a bull market, but it is designed to be less volatile while providing high monthly dividends. This might make it easier for you to remain invested through the type of downturn we saw last year.

JEPI was launched on May 20, 2020, and has grown quickly to $18.7 billion in assets under management. Hamilton Reiner, who co-manages the fund with Raffaele Zingone, described the fund’s strategy, and its success during the 2022 bear market and shared thoughts on what may lie ahead.

Outperformance with a smoother ride

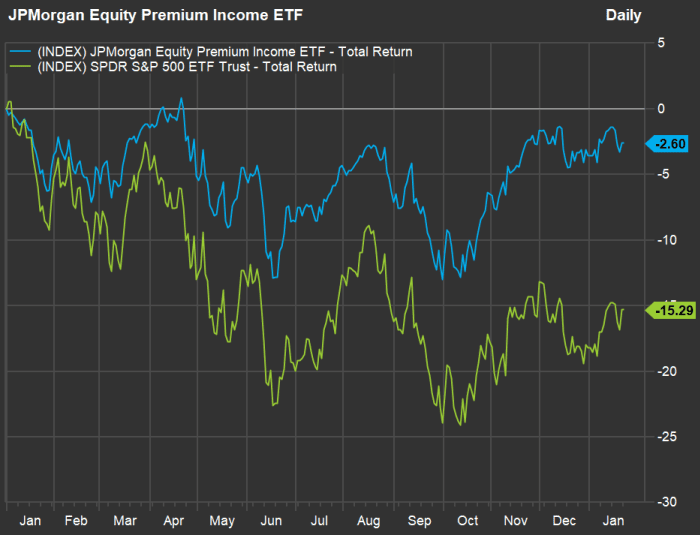

First, here’s a chart showing how the fund has performed from when it was established through Jan. 20, against the SPDR S&P 500 ETF Trust SPY, +1.20%,

both with dividends reinvested:

JEPI has been less volatile than SPY, which tracks the S&P 500.

FactSet

Total returns for the two funds since May 2020 pretty much match, however, JEPI has been far less volatile than SPY and the S&P 500. Now take a look at a performance comparison for the period of rising interest rates since the end of 2021:

Rising stock-price volatility during 2022 helped JEPI earn more income through its covered call option strategy.

FactSet

Those total returns are after annualized expenses of 0.35% of assets under management for JEPI and 0.09% for SPY. Both funds have had negative returns since the end of 2021, but JEPI has been a much better performer.

““Income is the outcome.””

— Hamilton Reiner

The income component

Which investors JEPI is designed for? “Income is the outcome,” Reiner responded. “We are seeing a lot of people using this as an anchor tenant for income-oriented portfolios.”

The fund quotes a 30-day SEC yield of 11.77%. There are various ways to look at dividend yields for mutual funds or exchange-traded funds and the 30-day yield is meant to be used for comparison. It is based on a fund’s current income distribution profile relative to its price, but the income distributions that investors actually receive will vary.

It turns out that over the past 12 months, JEPI’s monthly distributions have ranged between 38 cents a share and 62 cents a share, with a rising trend over the past six months. The sum of the past 12 distributions has been $5.79 a share, for a distribution yield of 10.53%, based on the ETF’s closing price of $55.01 on Jan. 20.

JEPI invests at least 80% of assets in stocks, mainly selected from those in the S&P 500, while also investing in equity-linked notes to employ a covered call option strategy which enhances income and lowers volatility. Covered calls are described below.

Reiner said that during a typical year, investors in JEPI should expect monthly distributions to come to an annualized yield in the “high single digits.”

He expects that level of income even if we return to the low-interest rate environment that preceded the Federal Reserve’s cycle of rate increases that it started early last year to push down inflation.

JEPI’s approach may be attractive to investors who don’t need the income now. “We also see people using it as a conservative equity approach,” Reiner expects the fund to have 35% less price volatility than the S&P 500.

Getting back to income, Reiner said JEPI was a good alternative even for investors who were willing to take credit risk with high-yield bond funds. Those have higher price volatility than investment-grade bond funds and face a higher risk of losses when bonds default. “But with JEPI you don’t have credit risk or duration risk,” he said.

An example of a high-yield bond fund is the iShares 0-5 Year High Yield Corporate Bond ETF SHYG, -0.10%.

It has a 30-day yield of 7.95%.

When discussing JEPI’s stock selection, Reiner said “there is a significant active component to the 90 to 120 names we invest in.” Stock selections are based on recommendations of JPM’s analyst team for those that are “most attractively priced today for the medium to long term,” he said.

Individual stock selections don’t factor in dividend yields.

Covered call strategies and an example of a covered-call trade

JEPI’s high income is an important part of its low-volatility total-return strategy.

A call option is a contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

A covered call option is one an investor can write when they already own a security. The strike price is “out of the money,” which means it is higher than the stock’s current price.

Here’s an example of a covered call option provided by Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev.

You bought shares of 3M Co. MMM, +1.63%

on Jan. 20 for $118.75.

You sold a $130 call option with an expiration date of Jan. 19, 2024.

The premium for the Jan. 24, $130 call was $7.60 at the time that MMM was selling for $118.75.

The current dividend yield for MMM is 5.03%.

“So the maximum gain for this trade before the dividend is $18.85 or 15.87%. Add the divided income and you’ll get 20.90% maximum return,” Roberts wrote in an email exchange on Jan. 20.

If you had made this trade and 3M’s shares didn’t rise above $130 by Jan. 19, 2024, the option would expire and you would be free to write another option. The option alone would provide income equivalent to 6.40% of the Jan. 20 purchase price in the period of a year.

If the stock rose above $130 and the option were exercised, you would have ended up with the maximum gain as described by Roberts. Then you would need to find another stock to invest in. What did you risk? Further upside beyond $130. So you would have written the option only if you had decided you would be willing to part with your shares of MMM for $130.

The bottom line is that the call option strategy lowers volatility with no additional downside risk. The risk is to the upside. If 3M’s shares had doubled in price before the option expired, you would still wind up selling them for $130.

JEPI pursues the covered call options strategy by purchasing equity-linked notes (ELNs) which “combine equity exposure with call options,” Reiner said. The fund invests in ELNs rather than writing its own options, because “unfortunately option premium income is not considered bona fide income. It is considered a gain or a return of capital,” he said.

In other words, the fund’s distributions can be better reflected in its 30-day yield, because option income probably wouldn’t be included.

One obvious question for a fund manager whose portfolio has increased quickly to almost $19 billion is whether or not the fund’s size might make it difficult to manage. Some smaller funds pursuing narrow strategies have been forced to close themselves to new investors. Reiner said JEPI’s 2% weighting limitation for its portfolio of about 100 stocks mitigates size concerns. He also said that “S&P 500 index options are the most liquid equity products in the world,” with over $1 trillion in daily trades.

Summing up the 2022 action, Reiner said “investing is about balance.” The rising level of price volatility increased options premiums. But to further protect investors, he and JEPI co-manager Raffaele Zingone also “gave them more potential upside by selling calls that were a bit further out of the money.”

The stock of a Singapore-based ed-tech and education company called Genius Group Ltd. rallied more than 200% on Thursday, after it said it appointed a former F.B.I. director to lead a task force investigating alleged illegal trading in its stock that it first disclosed in early January.

The stock was last up 264% to mark its biggest-ever one-day percentage gain. Volume of 197.76 million shares traded crushed the 65-day average of just 634,17. Genius Group GNS, +290.29%

also said it would issue a special dividend to shareholders to help expose the wrongdoing and is considering a dual listing that would make illegal naked short selling more difficult.

The task force will be led by Timothy Murphy, a former deputy director of the F.B.I. who is also on the board. It will include Richard Berman, also a Genius Group Director and chair of the company’s Audit Committee, and Roger Hamilton, the chief executive officer of Genius Group.

“The company has been in communication with government regulatory authorities and is sharing information with these authorities to assist them,” the company said in a statement.

Genius Group said it has proof from Warshaw Burstein LLP and Christian Levine Law Group, with tracking from Share Intel, that certain individual and/or companies sold but failed to deliver a “significant” amount of its shares as part of a scheme seeking to artificially depress the stock price.

It will now explore legal action and will hold an extraordinary general meeting in the coming weeks to get shareholder approval for its planned actions.

Genius’ IPO priced at $6 a share in April of 2022, he wrote in a blog. The company, which aims to develop an entrepreneur education system, then completed five acquisitions of education companies to build out its portfolio and reported more than 60% growth in its last earnings report.

Analysts at Diamond Equity assigned it an $11.28 stock price target, while Zacks assigned it a $19.20 stock price target.

“By all measures, we believed we were doing all the right things to justify a rising share price,” said Hamilton.

The company then announced two funding rounds totaling $40 million to grow its balance sheet to more than $60 million, yet its stock fell to under 40 cents, or less than 25% of the cash raised and less than 20% of its net assets.

“This didn’t happen gradually,” the executive wrote. “It happened in two month intervals from our IPO, in June, August, October and December. Each time, over a period of a few days, massive selling volume that was a multiple of our float (As most of our shares are on lock up, only around 4 million are tradeable) was sold into the market, making our share price drop by 50% or more.”

The company has since drawn on Wes Christian, a short-selling litigator from Christian Levine Law Group, who has helped it understand how naked short selling works, and then Share Intel helped find the proof that that’s what has happened.

Individuals or groups get together and sell shares in a target company that they don’t own, with the aim of getting the share price to fall 50% in a short period. They use small-cap firms that have low buying volume, allowing them to scare off buyers.

“The broker doesn’t bother to find shares to borrow,” said Hamilton. “They simply sell shares they don’t have and after a few days book them as FTDs (failure to deliver) or hide them as long sales instead of short sales. The people who bought the shares have no idea they bought a fake share, and suddenly there’s plenty more shares in the market than there should be.”

If these groups sell 6 million shares from $12 to $6 each, and then buy back over two months at under $6, they double their money. That allows them to make up to $30 million out of thin air. They can then repeat the whole process a few months later.

“If they don’t buy back all the shares, they simply leave them as FTDs or hide them in offshore accounts,” he wrote. “At no point do they need to put up any cash to make this happen, as they’re making money from the moment they start selling fake shares.”

The ultimate goal is to push a company into bankruptcy, where the equity will be wiped out, meaning they never have to cover the short position on the fake shares.

By issuing a special dividend, Genius is hoping to find who is responsible, as all brokers are forced to disclose to the Depository Trust & Clearing Corp. (DTCC) how many shares their clients hold and how many dividends will be paid. Theoretically, that should expose the oversold shares and dishonest brokers will be forced to cover their position, said Hamilton.

In practice, dishonest brokers will not declare the fake shares and just pay the dividend out of their own pockets.

“If you issue a dividend that isn’t straight cash—such as a spinoff of a company so you are issuing shares, or a blockchain based asset, then the brokers can’t do that are a forced to either cover or be exposed,” he wrote.

Many people are good at saving up money for retirement. They manage expenses and build up their nest eggs steadily. But when it comes time to begin drawing income from an investment portfolio, they might feel overwhelmed with so many choices.

Some income-seeking investors might want to dig deeply into individual bonds or dividend stocks. But others will want to keep things simple. One of the easiest ways to begin switching to an income focus is to use exchange-traded funds. Below are examples of income-oriented exchange-traded funds (ETFs) with related definitions further down.

First, the inverse relationship

Before looking at income-producing ETFs, there is one concept we will have to get out of the way — the relationship between interest rates and bond prices.

Stocks represent ownership units in companies. Bonds are debt instruments. A government, company or other entity borrows money from investors and issues bonds that mature on a certain date, when the issuer redeems them for the face amount. Most bonds issued in the U.S. have fixed interest rates and pay interest every six months.

Investors can sell their bonds to other investors at any time. But if interest rates in the market have changed, the market value of the bonds will move in the opposite direction. Last year, when interest rates rose, the value of bonds declined, so that their yields would match the interest rates of newly issued bonds of the same credit quality.

It was difficult to watch bond values decline last year, but investors who didn’t sell their bonds continued to receive their interest. The same could be said for stocks. The benchmark S&P 500 SPX, -0.20%

fell 19.4% during 2022, with 72% of its stocks declining. But few companies cut dividends, just as few companies defaulted on their bond payments.

One retired couple that I know saw their income-oriented brokerage account value decline by about 20% last year, but their investment income increased — not only did the dividend income continue to flow, they were able to invest a bit more because their income exceeded their expenses. They “bought more income.”

The longer the maturity of a bond, the greater its price volatility. Depending on the economic environment, you might find that a shorter-term bond portfolio offers a “sweet spot” factoring in price volatility and income.

And here’s a silver lining — if you are thinking of switching your portfolio to an income orientation now, the decline in bond prices means yields are much more attractive than they were a year ago. The same can be said for many stocks’ dividend yields.

Downside protection

What lies ahead for interest rates? With the Federal Reserve continuing its efforts to fight inflation, interest rates may continue to rise through 2023. This can put more pressure on bond and stock prices.

Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev., emphasizes the “downside protection” provided by dividend income in his discussions with clients.

“Diversification is the best risk-management tool there is,” he said during an interview. He also advised novice investors — even those seeking income rather than growth — to consider total returns, which combine the income and price appreciation over the long term.

An ETF that holds bonds is designed to provide income in a steady stream. Some pay dividends quarterly and some pay monthly. An ETF that holds dividend-paying stocks is also an income vehicle; it may pay dividends that are lower than bond-fund payouts and it will also take greater risk of stock-market price fluctuation. But investors taking this approach are hoping for higher total returns over the long term as the stock market rises.

“With an ETF, your funds are diversified. And when the market goes through periods of volatility, you continue to enjoy the income, even if your principal balance declines temporarily,” Roberts said.

If you sell your investments into a declining market, you know you will lose money — that is, you will sell for less than your investments were worth previously. If you are enjoying a stream of income from your portfolio, it might be easier for you to wait through a down market. If we look back over the past 20 calendar years — arbitrary periods — the S&P 500 increased during 15 of those years. But its average annual price increase was 9.1% and its average annual total return, with dividends reinvested, was 9.8%, according to FactSet.

In any given year, there can be tremendous price swings. For example, during 2020, the early phase of the Covid-19 pandemic pushed the S&P 500 down 31% through March 23, but the index ended the year with a 16% gain.

Two ETFs with broad approaches to dividend stocks

Invesco Head of Factor and Core Strategies Nick Kalivas believes investors should “explore higher-yielding stocks as a way to generate income and hedge against inflation.”

He cautioned during an interview that selecting a stock based only on a high dividend yield could place an investor in “a dividend trap.” That is, a high yield might indicate that professional investors in the stock market believe a company might be forced to cut its dividend. The stock price has probably already declined, to send the dividend yield down further. And if the company cuts the dividend, the shares will probably fall even further.

Here are two ways Invesco filters broad groups of stocks to those with higher yields and some degree of safety:

The Invesco S&P 500 High Dividend Low Volatility ETF SPHD, -0.33%

holds shares of 50 companies with high dividend yields that have also shown low price volatility over the previous 12 months. The portfolio is weighted toward the highest-yielding stocks that meet the criteria, with limits on exposure to individual stocks or sectors. It is reconstituted twice a year in January and July. Its 30-day SEC yield is 4.92%.

The Invesco High Yield Equity Dividend Achievers ETF PEY, -0.70%

follows a different screening approach for quality. It begins with the components of the Nasdaq Composite Index COMP, +1.39%,

then narrows the list to 50 companies that have raised dividend payouts for at least 10 consecutive years, whose stocks have the highest dividend yields. It excludes real-estate investment trusts and is weighted toward higher-yielding stocks meeting the criteria. Its 30-day yield is 4.08%.

The 30-day yields give you an idea of how much income to expect. Both of these ETFs pay monthly. Now see how they performed in 2022, compared with the S&P 500 and the Nasdaq, all with dividends reinvested:

Both ETFs had positive returns during 2022, when rising interest rates pressured the broad indexes.

8 more ETFs for income (and some for growth too)

A mutual fund is a pooling of many investors’ money to pursue a particular goal or set of goals. You can buy or sell shares of most mutual funds once a day, at the market close. An ETF can be bought or sold at any time during stock-market trading hours. ETFs can have lower expenses than mutual funds, especially ETFs that are passively managed to track indexes.

You should learn about the expenses before making a purchase. If you are working with an investment adviser, ask about fees — depending on the relationship between the adviser and a fund manager, you might get a discount on combined fees. You should also discuss volatility risk with your adviser, to establish a comfort level and to try to match your income investment choices to your risk tolerance.

Here are eight more ETFs designed to provide income or a combination of income and growth:

Company

Ticker

30-day SEC yield

Concentration

2022 total return

iShares iBoxx $ Investment Grade Corporate Bond ETF

The following definitions can help you gain a better understanding of how the ETFs listed above work:

30-day SEC yield — A standardized calculation that factors in a fund’s income and expenses. For most funds, this yield gives a good indication of how much income a new investor can be expected to receive on an annualized basis. But the 30-day yields don’t always tell the whole story. For example, a covered-call ETF with a low 30-day yield may be making regular dividend distributions (quarterly or monthly) that are considerably higher, since the 30-day yield can exclude covered-call option income. See the issuer’s website for more information about any ETF that may be of interest.

Taxable-equivalent yield — A taxable yield that would compare with interest earned from municipal bonds that are exempt from federal income taxes. Leaving state or local income taxes aside, you can calculate the taxable-equivalent yield by dividing your tax exempt yield by 1 less your highest graduated federal income tax bracket.

Bond ratings — Grades for credit risk, as determined by ratings agencies. Bonds are generally considered Investment-grade if they are rated BBB- or higher by Standard & Poor’s and Fitch, and Baa3 or higher by Moody’s. Fidelity breaks down the credit agencies’ ratings hierarchy. Bonds with below-investment-grade ratings have higher risk of default and higher interest rates than investment-grade bonds. They are known as high-yield or “junk” bonds.

Call option — A contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

Covered call option — A call option an investor writes when they already own a security. The strategy is used by stock investors to increase income and provide some downside protection.

Preferred stock — A stock issued with a stated dividend yield. This type of stock has preference in the event a company is liquidated. Unlike common shareholders, preferred shareholders don’t have voting rights.

These articles dig deeper into the types of securities mentioned above and related definitions:

Investors love dividend stocks but there are different ways to look at them, including various “quality” approaches. Today we are focusing on high yields.

A high dividend yield can be a warning that investors have lost confidence in a company’s ability to maintain its dividend payout. But there are always exceptions, some of which can be brought about by market events — some investors remain skeptical of energy stocks, for example, after so much pain before this year’s outstanding performance for the sector.

Below is a screen of stocks that have high dividend yields and are favored by analysts. The screen has no financial quality filters.

For investors who are interested in dividend stocks but wish to focus on quality and total returns, this recent look at the S&P Dividend Aristocrats (companies that have raised dividends consistently for many years) might be of interest. For those looking for income but also worried about dividend cuts, here is a list of stocks with dividend yields of at least 5% whose payouts are expected to be well-covered by free cash flow in 2023.

Removing the filters for a high-yield dividend-stock screen

For a broad screen of stocks with high dividend yields that are favored by analysts, we began with the S&P Composite 1500 Index SP1500, +1.42%,

which is made up of the S&P 500 SPX, +1.42%,

the S&P 400 Mid Cap Index MID, +1.48%,

and the S&P 600 Small Cap Index SML, +1.49%.

The S&P indexes exclude energy partnerships, so we added the 15 stocks held by the Alerian MLP ETF AMLP, +1.81%

to the list. Energy partnerships tend to have high distribution yields, in part because they pass most earnings through to investors. But they also can make tax preparation more complicated. They can also be volatile as oil CL00, +2.96%

CL00 and natural-gas NG00, +1.58%

prices swing.

The S&P indexes also exclude business development companies, or BDCs, so we expanded our initial screen to include the 24 stocks held by the VanEck BDC income ETF BIZD, +0.76%.

BDCs are specialized leveraged lenders that make loans with high interest rates, mainly to middle-market companies. They often take equity stakes in the companies they lend to, for a venture-capital-type of investment style. The BDC space features several stocks with very high dividend yields, but is also known for volatility.

You have been warned — this particular stock screen focuses only on high yields and favorable ratings among analysts working for brokerage firms. There is no look back at dividend cuts and no cash-flow analysis as featured in other dividend-stock articles. If you see anything of interest resulting from the screen, you need to do your own research to consider whether or not a long-term commitment to one or more of these companies is worth the risk as you seek high income.

The screen

Starting with the S&P Composite 1500 and the components of AMLP and BIZD, there are 68 stocks with dividend yields of at least 8%, according to data provided by FactSet.

Among the 68 companies, 55 made the first screen, because they are covered by at least five analysts polled by FactSet.

Among the 55 companies, 11 have “buy” or equivalent ratings among at least 70% of analysts.

Here they are, ranked by upside potential implied by analysts’ consensus price targets:

Income-seeking investors are looking at an opportunity to scoop up shares of real estate investment trusts. Stocks in that asset class have become more attractive as prices have fallen and cash flow is improving.

Below is a broad screen of REITs that have high dividend yields and are also expected to generate enough excess cash in 2023 to enable increases in dividend payouts.

REIT prices may turn a corner in 2023

REITs distribute most of their income to shareholders to maintain their tax-advantaged status. But the group is cyclical, with pressure on share prices when interest rates rise, as they have this year at an unprecedented scale. A slowing growth rate for the group may have also placed a drag on the stocks.

And now, with talk that the Federal Reserve may begin to temper its cycle of interest-rate increases, we may be nearing the time when REIT prices rise in anticipation of an eventual decline in interest rates. The market always looks ahead, which means long-term investors who have been waiting on the sidelines to buy higher-yielding income-oriented investments may have to make a move soon.

During an interview on Nov 28, James Bullard, president of the Federal Reserve Bank of St. Louis and a member of the Federal Open Market Committee, discussed the central bank’s cycle of interest-rate increases meant to reduce inflation.

When asked about the potential timing of the Fed’s “terminal rate” (the peak federal funds rate for this cycle), Bullard said: “Generally speaking, I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation.”

Fed’s Bullard says in MarketWatch interview that markets are underpricing the chance of still-higher rates

In August we published this guide to investing in REITs for income. Since the data for that article was pulled on Aug. 24, the S&P 500 SPX, -0.29%

has declined 4% (despite a 10% rally from its 2022 closing low on Oct. 12), but the benchmark index’s real estate sector has declined 13%.

REITs can be placed broadly into two categories. Mortgage REITs lend money to commercial or residential borrowers and/or invest in mortgage-backed securities, while equity REITs own property and lease it out.

The pressure on share prices can be greater for mortgage REITs, because the mortgage-lending business slows as interest rates rise. In this article we are focusing on equity REITs.

Industry numbers

The National Association of Real Estate Investment Trusts (Nareit) reported that third-quarter funds from operations (FFO) for U.S.-listed equity REITs were up 14% from a year earlier. To put that number in context, the year-over-year growth rate of quarterly FFO has been slowing — it was 35% a year ago. And the third-quarter FFO increase compares to a 23% increase in earnings per share for the S&P 500 from a year earlier, according to FactSet.

The NAREIT report breaks out numbers for 12 categories of equity REITs, and there is great variance in the growth numbers, as you can see here.

FFO is a non-GAAP measure that is commonly used to gauge REITs’ capacity for paying dividends. It adds amortization and depreciation (noncash items) back to earnings, while excluding gains on the sale of property. Adjusted funds from operations (AFFO) goes further, netting out expected capital expenditures to maintain the quality of property investments.

The slowing FFO growth numbers point to the importance of looking at REITs individually, to see if expected cash flow is sufficient to cover dividend payments.

Screen of high-yielding equity REITs

For 2022 through Nov. 28, the S&P 500 has declined 17%, while the real estate sector has fallen 27%, excluding dividends.

Over the very long term, through interest-rate cycles and the liquidity-driven bull market that ended this year, equity REITs have fared well, with an average annual return of 9.3% for 20 years, compared to an average return of 9.6% for the S&P 500, both with dividends reinvested, according to FactSet.

This performance might surprise some investors, when considering the REITs’ income focus and the S&P 500’s heavy weighting for rapidly growing technology companies.

For a broad screen of equity REITs, we began with the Russell 3000 Index RUA, -0.04%,

which represents 98% of U.S. companies by market capitalization.

We then narrowed the list to 119 equity REITs that are followed by at least five analysts covered by FactSet for which AFFO estimates are available.

If we divide the expected 2023 AFFO by the current share price, we have an estimated AFFO yield, which can be compared with the current dividend yield to see if there is expected “headroom” for dividend increases.

For example, if we look at Vornado Realty Trust VNO, +1.03%,

the current dividend yield is 8.56%. Based on the consensus 2023 AFFO estimate among analysts polled by FactSet, the expected AFFO yield is only 7.25%. This doesn’t mean that Vornado will cut its dividend and it doesn’t even mean the company won’t raise its payout next year. But it might make it less likely to do so.

Among the 119 equity REITs, 104 have expected 2023 AFFO headroom of at least 1.00%.

Here are the 20 equity REITs from our screen with the highest current dividend yields that have at least 1% expected AFFO headroom:

Click on the tickers for more about each company. You should read Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

The list includes each REIT’s main property investment type. However, many REITs are highly diversified. The simplified categories on the table may not cover all of their investment properties.

Knowing what a REIT invests in is part of the research you should do on your own before buying any individual stock. For arbitrary examples, some investors may wish to steer clear of exposure to certain areas of retail or hotels, or they may favor health-care properties.

Largest REITs

Several of the REITs that passed the screen have relatively small market capitalizations. You might be curious to see how the most widely held REITs fared in the screen. So here’s another list of the 20 largest U.S. REITs among the 119 that passed the first cut, sorted by market cap as of Nov. 28:

As many Americans fire up their furnaces for the winter months, they’ll also be eyeing their home heating bills. They’re going to be paying more, and several companies will be the beneficiary of those higher prices. Among them will be several midstream oil and gas companies that are responsible for keeping natural gas flowing across the country.

MarketBeat.com – MarketBeat

Midstream companies are among the most stable investments in the oil and gas industry. Many operate as master limited partnerships (MLPs). These companies aren’t known for generating significant capital growth. In fact, they’re known as the “utilities” of the natural gas sector.

Investing in MLPs isn’t for every investor as they do present some tax implications. But for investors who have wealth preservation and income as their most important goals, these stocks make up for that with generous dividends.

This article will look at three of the top companies that investors should be looking at right now. Each offers a healthy dividend, but also may be ready to deliver some share price appreciation. But first, let’s answer this question.

Is It Too Late to Invest in Natural Gas Stocks?

It wouldn’t seem to be the case. A poll conducted by Pew Research Center in March 2022 found that over two-thirds of Americans support the use of a diverse energy mix that includes natural gas.

Many of these respondents still want the United States to be carbon neutral by 2050. But most of the respondents were concerned about “unexpected problems” that could result from reducing fossil fuel production.

One of those unexpected problems is on full display since the Russian invasion of Ukraine. Europe relies on Russia for much of its natural gas needs. To meet that need this winter, many European Union nations are looking for natural gas from elsewhere. And the United States is a prime candidate.

Enterprise Products Partners

With a $54 billion market cap, Enterprise Products Partners (NYSE: EPD) is one of the largest midstream companies. In its most recent quarter, the company’s natural gas pipelines transported a record $17.5 trillion BTUs per day which speaks to the ongoing demand for natural gas.

Many analysts note that over 30% of the company’s shares (or “units” since it’s an MLP) are owned by company insiders. The thesis is that this level of ownership means that management has a personal stake in making sure the business is run in a prudent manner. And that is reflected in the company’s balance sheet which keeps a significant amount of cash on hand.

Some of that cash is used to support the dividend which currently has a yield of over 7.6%. Plus, the company just increased its dividend for its 25th consecutive year making it part of the dividend aristocrat club.

As of this writing, EPD stock has just crossed above both its 50- and 200-day simple moving averages after a period of consolidation. This may create an opportunity for investors to capture a little share price growth to end the year.

Enbridge

Enbridge (NYSE: ENB) has a market cap of over $81 billion. I could list many of the same positives for Enbridge as I did for Enterprise Products Partners. This is a very fundamentally sound company with a secure dividend that currently yields over 6%.

One differentiating factor for Enbridge is its ability to capitalize on the growing liquefied natural gas (LNG) market. As mentioned above, Europe is looking to the West for natural gas which will have to be transported as LNG. Enbridge has several projects that are near liquefication terminals. The company expects this will allow it to garner a fair share of this business, which adds growth potential to the solid dividend offered by Enbridge.

Magellan Midstream Partners

The third midstream company to watch is Magellan Midstream Partners (NYSE: MMP). It checks in with the smallest market cap of the three companies. At just over $10 billion, it could be considered a mid-cap company.

MMP stock is up over 10% for the year and is trading above its 50- and 200-day moving averages at the time of this writing. But investors are really buying a stock like this for secure income. The company does have a dividend yield of just over 8%. And the company has increased that dividend for 19 consecutive years.

Beyond Meat “Beyond Burger” patties made from plant-based substitutes for meat products sit on a shelf for sale in New York City.

Angela Weiss | AFP | Getty Images

Beyond Meat on Wednesday reported a wider-than-expected loss for its third quarter as demand for its meat substitutes tumbled.

Shares of the company bounced around in after-hours trading. The stock closed down 9% on Wednesday.

Here’s what the company reported compared with what Wall Street was expecting, based on a survey of analysts by Refinitiv:

Loss per share: $1.60 vs. $1.14 expected

Revenue: $82.5 million vs. $98.1 million expected

Beyond reported a third-quarter net loss of $101.7 million, or $1.60 per share, wider than its net loss of $54.8 million, or 87 cents per share, a year earlier.

SEATTLE — A judge in Washington state has temporarily blocked Albertsons from paying a $4 billion dividend to investors as part of the grocery retailer’s proposed merger with rival Kroger.

On Thursday, King County Superior Court Commissioner Henry Judson approved a motion by state Attorney General Bob Ferguson to temporarily block the dividend until the court can more fully consider whether the payment violates antitrust laws, The Seattle Times reported.

The dividend was scheduled to be paid Monday.

The proposed merger would combine two of the nation’s largest grocery chains. Some critics worry that could mean reduced competition, higher food prices and the closure of under-performing locations, including some in Washington state. Albertsons, which owns Safeway, and Kroger, which owns QFC and Fred Meyer, are among the biggest players in Washington.

“Putting the brakes on this $4 billion payment is a huge win for consumers nationwide,” Ferguson said Thursday afternoon on Twitter.

Next Thursday, King County Superior Court Judge Ken Schubert is scheduled to more closely review arguments in the case.

“There is obviously further information and evidence that needs to be presented,” Judson noted.

In a lawsuit filed Tuesday, Ferguson argues the dividend is illegal because it potentially undercuts the ability of Albertsons to keep all its locations open in the several years needed to complete the merger.

Those arguments were echoed by attorneys general in Illinois, California and the District of Columbia, which on Wednesday jointly sued to block the dividend in federal court in Washington, D.C.

Boise, Idaho-based Albertsons said this week that both lawsuits are without merit.

One major concern of the dividend is the potential impact of such a large payment on Albertsons. To win regulatory approval for the merger, Albertsons and Kroger must sell hundreds of locations in areas where they have too much market overlap. So-called divestiture could have a major impact in Seattle and throughout Washington, where Kroger and Albertsons collectively have about 350 locations.

Kroger and Albertsons have agreed to put the divested locations in a standalone company, managed by Albertsons, and then sell them to a competing retailer or retailers as part of the approval process.

However, some antitrust and business experts question whether locations chosen for divesture might already be struggling financially. They worry that a cash-strapped Albertsons might fail to keep all those locations open while it finds a willing buyer and that some divested stores could close, as happened after the 2015 merger between Albertsons and Safeway.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

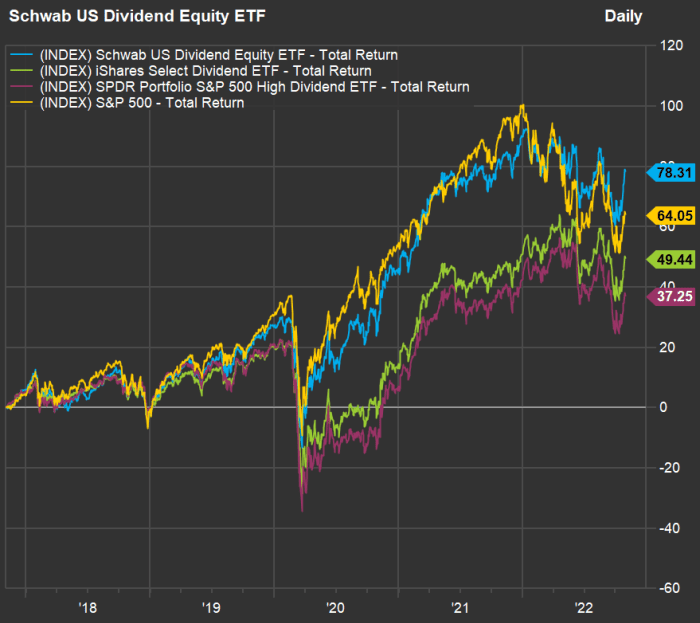

Low-volatility stocks are working in 2022

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.