Strategist Savita Subramanian called the dividend trade a “pain trade,” meaning the bulk of investors are not properly positioned for the potential upside gains in dividend-paying stocks.

“Over $6 trillion sits in US money market funds as the Fed is poised to start cutting rates,” Subramanian said in a note this week. “Bond funds have seen record flows YTD, but we see more opportunities within equities for investors searching for yield.”

There are more than 200 S&P 500 stocks that offer a higher real return potential than the 2% offered by the 10-year Treasury yield, according to the note, and about 75% of those stocks are under-owned by professional investors.

Some of the highest-yielding S&P 500 companies include Walgreens Boot Alliance, Altria, Verizon, Ford, and AT&T. And while the S&P 500 as a whole offers a dividend yield of about 1.25%, there are nearly 300 S&P 500 stocks that offer a higher yield.

“Overall, we expect dividends to make up a larger proportion of returns than the outsized price returns and multiple expansion of the past decade,” Subramanian said.

BMO’s Brian Belski is another Wall Street strategist who expects big gains to be had from dividend paying stocks, especially after their lackluster performance since the October 2022 stock market bottom.

“We believe these stocks have turned the corner and recent relative strength is likely to persist in the coming months,” Belski said in a note on Tuesday. “With the Fed now likely to cut rates sooner than previously anticipated, the likely drop in longer-term yields in response should provide a boost.”

As investors hunt for yield at a time when interest rates are about to fall, dividend-paying stocks could be the underloved area of the stock market that is set to boom.

Biden’s withdrawal soothes bond market, deflates “Trump trade”

Compared to the way U.S. President Joe Biden’s decision not to run for a second term shook the political world, the markets seemed nonplussed—on the surface, at least.

Biden’s U-turn took some air out of the “Trump trade” in stock, bond and cryptocurrency markets. Stock markets overall rebounded the day after the announcement, with mega-cap technology stocks leading the way. But oil and gas stocks and cryptocurrencies—foreseen to fare better under a Donald Trump administration—retrenched.

The Republican nominee is seen as a bigger deficit spender than whomever the Democrats might settle on, so a Trump/Vance administration is expected to usher in higher inflation. That recently translated into a steeper yield curve for bonds as polls showed him ahead of Biden. However, that expectation of Trump as an inevitable shoo-in has now deflated and bond yields have flattened somewhat.

However, Kristina Hooper, chief global market strategist at Invesco, warned investors to stay braced for more short-term volatility, “as the significant uncertainty about the new Democratic ticket might not be resolved until the party’s convention in August.” She also suggested that investors should pay closer attention to the U.S. Federal Reserve moves with respect to interest rates. (More on Canada’s recent rate cut below.)

Something for Canadians and investors to ponder: As a senator, Vice President and Democratic front-runner Kamala Harris voted against the U.S.-Canada-Mexico trade agreement (USMCA), the successor to NAFTA (North American Free Trade Agreement) that was concluded by the Trump administration in 2020. At the time, she cited the lack of environmental protections for her decision.

Bank of Canada cuts rates again

Speaking of monetary policy, on Wednesday Bank of Canada (BoC) governor Tiff Macklem announced a second quarter-point cut to interest rates in as many months bringing the overnight lending rate down to 4.5%. Further, Macklem hinted there would be more cuts to come this year; provided inflation continues to subside towards the Bank’s 2% target. The country’s Consumer Price Index (CPI) increased 2.7% year-over-year in June, down from a 21st-century high of 8.1% two years earlier.

The rate cut was widely expected by markets.

“Today’s decision to cut was consistent with our call, and that of broader market consensus which had upped the odds of reduction following a cascade of recent data which showed decelerating inflation, slack in the labour market and underperforming economy.”

– Brian Yu, AVP and chief economist for Central1 Credit Union.

The BoC is forecasting 1.2% GDP growth this year, 2.1% in 2025 and 2.4% in 2026, which sounds OK until you consider population growth is currently running at 3%. Regardless, the rate cut provides some relief to mortgage holders and support for bond markets.

As we’re moving through summer’s dog days and heat records are being broken around the world, Canadian inflation is moving in the opposite direction. Statistics Canada released that the year-over-year Consumer Price Index (CPI) increase cooled to 2.7% in June. As inflation continues its downward trend, it generally indicates that the Bank of Canada’s monetary policy is working.

The main takeaways from the monthly CPI report are:

Core CPI (excluding food and energy) stayed stubbornly higher than the headline CPI, coming in at an annualized 2.9%.

Shelter continues to dominate the overall inflation picture, as prices were up 6.2%.

Services, another major inflation concern, were up 4.8%.

Durable good prices have substantially deflated, as they fell at an annualized rate of 1.8%.

Similarly, prices for clothes and shoes were down 3.1%.

Gas prices were down 3.1% from May to June, and have been pretty stable over the last year.

Grocery prices went up at an annualized rate of 2.1%, lower than the overall CPI figure.

The business and individual sentiment surveys point to decreasing inflation expectations going forward, and are significant indicators that the Bank of Canada (BoC) has succeeded in curbing the scariest runaway inflation scenarios. The early 1980s saw the rise of denim and ultra-high interest rates. While ’80s fashion might be back, it’s pretty clear that the era’s monetary policy isn’t.

Decreased inflation is welcomed news by many Canadians, but it’s probably cold comfort to those with mortgages due for renewal this month. The country as a whole might be happier that demand-pull inflation is down, but that just really means: “People have way less money to spend on most things because their mortgage or rent payments just went through the roof.”

The lower inflation rates and decreased inflation sentiments should empower the BoC to continue to slowly but surely cut interest rates in the coming months. It would be shocking if the BoC didn’t lower interest rates by 0.25% when it makes its decision next week.

To check out the effects of inflation rates right now, use this table.

Netflix subscribers must be nostalgic for TV commercials

Earnings day went largely as predicted for Netflix last Thursday, as earnings and revenues were quite close to the company’s guidance last quarter.

Netflix earnings highlights

Currency figures in this section are reported in USD.

• Netflix (NFLX/NASDAQ): Earnings per share of $4.88 (versus $4.74 predicted). Revenue of $9.56 billion (versus $9.53 billion estimate).

Netflix sold more memberships than was predicted (277.65 million versus 274.40 million). The bulk of that subscriber growth was in its advertising-supported platform. The markets seemed to take the news in stride, as share prices were largely flat in after-market trading.

Netflix co-CEO Ted Sarandos highlighted the company’s focus on ads going forward, saying that the streamer would no longer partner with Microsoft. Instead, it’s investing in its own platform. He also mentioned that Netflix’s push into live sports would attract more ad dollars, specifically mentioning the NFL games on Christmas Day as important opportunities. He summed up the company’s push into live sports saying, “We’re in live [TV] because our members love it, and it drives a ton of engagement and a ton of excitement… and the good thing is advertisers like it for the exact same reason.”

With Netflix up over 43% this year, and at a price to earnings (P/E) ratio of over 44, one could make the argument the stock is priced appropriately, and that it will have to expertly execute future growth plans to have any chance of justifying that high price tag.

While Canada’s inflation rate is obviously at the forefront around decision making for the Bank of Canada (BoC) in setting the key interest rate, inflation below the border is also a major consideration. Arguably, policymakers are loath to devalue the Canadian dollar beyond a certain level. Consequently, if U.S. inflation stays high—and U.S. interest rates correspondingly stay high—it will likely impact just how quickly the BoC can cut our interest rates.

“The Canadian and American economies are very closely intertwined, especially when it comes to the cost of borrowing. Historically the BoC and the Fed have mirrored each other in terms of monetary policy (the act of cutting, holding, or hiking their benchmark interest rates).”

Markets were mostly flat on Thursday after the U.S. Bureau of Labor Statistics announced that headline CPI was down 0.1% from May, and the 12-month inflation reading was now 3%.

Core CPI (excluding food and energy) increased 0.1% and up 3.3% from a year ago.

Gas prices were down 3.8%.

Food prices were up 0.2%.

Shelter prices were up 0.2%.

Used vehicles prices were down 1.5%.

Real hour earnings were up 0.4% for the month.

Overall, the down-trending inflation rate, as well as Fed Chairman Jerome Powell’s comments about holding interest rates too high for too long this week, both seem to indicate a probable rate cut in September. CME Group’s FedWatch tracker uses futures contracts to predict the likelihood of interest rate movements, and it currently shows a strong likelihood of two interest rate cuts before the end of 2024. There is even a 40% probability of three cuts before year end.

Obviously this is welcome news to indebted Americans, but also to Canadian consumers who want to see interest rates come down here sooner rather than later.

—Kyle Prevost

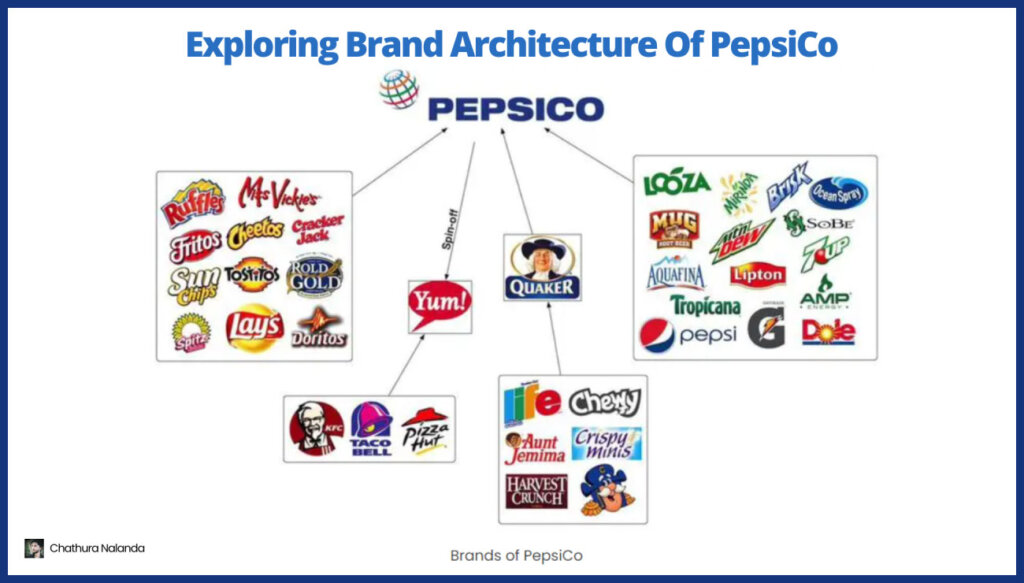

Pepsi’s revenues taste flat

Beverage-and-snack behemoth PepsiCo released lukewarm earnings news on Thursday. For those who aren’t familiar with Pepsi’s corporate structure, it long ago ceased to be a single-beverage entity. With brands ranging from numerous snack and soft drink choice to breakfast cereals, Pepsi is a diversified food conglomerate, including FritoLay and Quaker.

PepsiCo (PEP/NASDAQ): Earnings per share came in at $2.28 (versus $2.16 predicted) on revenues of $22.50 billion (versus $22.57 billion predicted). Shares were down nearly 2% in early trading on Thursday.

The company cited a declining demand in North America as the main factor in slowing revenue growth. Company executives explained that North American consumers were becoming more price conscious after failing to “push back” on significant price increases over the last few years. Low-income shoppers were highlighted as being the most willing consumer group to shift to cheaper private-label options. As well, increasing agricultural commodity costs were cited as an increasing operating expense. It’s worth noting that some market watchers believe weight-loss drugs, such as Ozempic and Wegovy, may curb demand for snack foods in the North American market.

FritoLay’s North America sales were down 4% year over year, while North American beverages were down 3%. Those sales declines were offset by international revenue increasing by 7% year to date. Management highlighted that this was the 13th straight consecutive quarter with at least mid-single-digit organic revenue growth for international operations.

Let’s wait and see how this one goes. If I wrote this column a week ago, I would have said Tesla looked like an excellent bet to be down 30% by year end. But shares jumped more than 10% this week on its positive second-quarter news. Despite the high numbers for vehicle deliveries, it has been a volatile year for Tesla shareholders, with prices down 42% at one point. Our central thesis was that decreased profit margins and increased competition would lead to lower profit projections. That still feels solid to me.

Prediction: Crypto might be volatile, but could finish 2024 up 50%

This one hit the bullseye. After going on a tear in February, bitcoin was down almost 20% between mid-March and the beginning of May.

Overall, bitcoin only has to go up slightly over the next six months to meet that 50% return prediction. Of course, I believe the asset will be ultimately worth very little in the long term. Admittedly, I’m quite skeptical about crypto.

Prediction: U.S. election in November will be chaotic

We also predicted that this election year would be more chaotic than most, even though U.S. election years are historically quite positive for U.S. stock markets. We shied away from making too many specific predictions about how a Biden/Trump victory would impact stock-market prices, but said many market-watchers would be cheering for a split government.

Well, it’s certainly been chaotic in the headlines. As the rest of the world watches in disbelief, the 2024 U.S. election has so far proven to be the most volatile campaign in recent memory—and maybe of all time. At this point, betting markets think it’s a coin toss as to whether Biden even makes it as the Democratic Party nominee. Ordinarily, a political candidate running against a convicted felon would be an easy win. Then again, ordinarily, a candidate running against an incumbent whose own party isn’t sure he’s still right for the job would be an easy win as well.

Given all the variables, we don’t even know how to measure the degree of accuracy of this prediction. We did reluctantly predict a very slim Biden victory, and that doesn’t look like such a great prognostication now that Trump is a fairly strong betting favourite. However, our strong feeling was that a split government would lead to a robust end of the year for U.S. stocks. That scenario could still be very much in play. We’re going to wait to fully assess this one.

What’s left of 2024?

After a very accurate round of 2023 predictions, we were statistically unlikely to repeat the feat in 2024. While we may have called it wrong about U.S. tech, I think there’s a good chance we’re going to get the big picture stuff right—by the end of the year. Despite a ton of negative headlines and general “bad vibes” over the last six months, one of my big takeaways is that the world’s stock markets (and especially America’s) should continue to reward patient Canadian investors.

Kyle Prevost is a financial educator, author and speaker. He is also the creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course.

If the summer heat doesn’t get you, inflation will

Canadians hoping for interest rate relief will likely have to wait a bit longer. The Consumer Price Index (CPI) reading for May came in at 2.9%, according to Statistics Canada.

The money markets predict a 45% chance that the Bank of Canada (BoC) will cut rates at its July 24 meeting. Lowering interest rates after a month of renewed inflation worries would carry a large credibility risk for the BoC, after it raised rates so quickly to restore faith that it would tame inflation over the long term.

CPI May 2024 highlights

Here are some notable takeaways from the CPI report:

May’s overall 2.9% CPI increase was 0.2% higher than April’s 2.7% CPI increase.

Renters in Canada continue to get slammed, as the year-over-year increase in rent was 8.9%.

Mortgage interest costs also massively grew, by 23.3%.

Core CPI (stripping out volatile items such as gas and groceries) was 2.85%.

The cost of travel also jumped, with airfare up 4.5% and tours up 6.9%.

Gasoline costs were up 5.6%.

In slightly better news, grocery prices were only up 1.5% year-over-year, but they’re up 22.5% since May 2020.

Cell phone services continue to be a bright spot for deflation, as they are down 19.4% since May 2023.

We’re sure the BoC was hoping for inflation to be closer to 2.5%, which would allow it to justify cutting interest rates and point to a stronger downward trend for inflation. Continuing to balance long-term growth and full employment versus controlled inflation isn’t going to get easier anytime soon for BoC governor Tiff Macklem and his team.

It was a tale of two extremes in U.S. earnings this week as FedEx shareholders became quite happy, while Nike investors were down in the dumps.

U.S. earnings highlights

This is what came out of the earnings reports this week. Both Nike and FedEx report in U.S. dollars.

Nike (NKE/NYSE): Earnings per share of $1.01 (versus $0.83 predicted). Revenue of $12.61 billion (versus $12.84 predicted).

FedEx (FDX/NYSE): Earnings per share of $5.41 (versus $5.35 predicted). Revenue of $22.11 billion (versus $22.08 billion predicted).

Nike finance chief Matthew Friend found himself in an odd position on his earnings call with analysts on Thursday. On one hand, Nike’s effort to reduce costs by shedding 1,500 jobs is paying off, and earnings per share came in substantially higher than experts predicted. On the other hand, declining sales in China and “increased macro uncertainty” were cited as reasons for a predicted sales drop of 10% in the next quarter. Investors chose to see the half-empty part of the glass, as shares plunged more than 12% in after-hours trading.

Friend attempted to put the downward forecast in perspective: “While our outlook for the near term has softened, we remain confident in Nike’s competitive position in China in the long term.” Nike highlighted running, women’s apparel and the Jordan brand as growth areas to watch going forward.

FedEx had a much better day, as shares were up more than 15% after it announced earnings on Tuesday. Future earnings projections were up on the news of increased cost-cutting efforts that will save the company about $4 billion over the next two years. FedEx announced possible increased profit margins as a result of consolidating its air and ground services.

Cash-strapped consumers pinch Couche-Tard

Canada’s 13th-largest company, the gas and convenience store empire known as Alimentation Couche-Tard, announced its earnings on Tuesday.

The focus on acquisitions comes as the Quebec-based chain behind the Couche-Tard and Circle K banners is preparing for only its second CEO shuffle in its almost 45-year history and battling an economic landscape where customers are proving cash-strapped and less likely to spend.

When is Couche-Tard’s new CEO taking over?

The company said Wednesday that Hannasch, who has been with the firm for 10 years, will retire on Sept. 6. When chief operating officer Alex Miller takes over the top job, Hannasch will become a special adviser to his successor and the executive chair of the company’s board, tasked with assisting with mergers and acquisitions.

News of Hannasch’s future came the same day the company hosted a call to discuss its fourth-quarter performance with analysts. During the period ended April 28, the chain saw its net earnings attributable to shareholders tumble to $453 million from $670.7 million a year earlier.

RBC Capital Markets analyst Irene Nattel described the results as “not a quarter for the history books,” but said it was “a better outcome” than the company had seen in its prior quarter.

Couche-Tard blamed the results on lower gross margins on fuel, the quarter being a week shorter than last year, and expenses and depreciation related to investments and acquisitions, but said the period was also marked with economic headwinds.

The effects of less consumer spending

“No doubt, this was another challenging quarter with persistent inflation and continued pressure on consumers who are carefully watching their spending,” Hannasch said.

On the fuel front, he has noticed customers buying lower amounts per visit. Inside stores, there’s been a gravitation toward private label products and shoppers trading down from premium to lower tier brands in categories like alcohol.

Cigarette sales have also been “an issue,” he said.

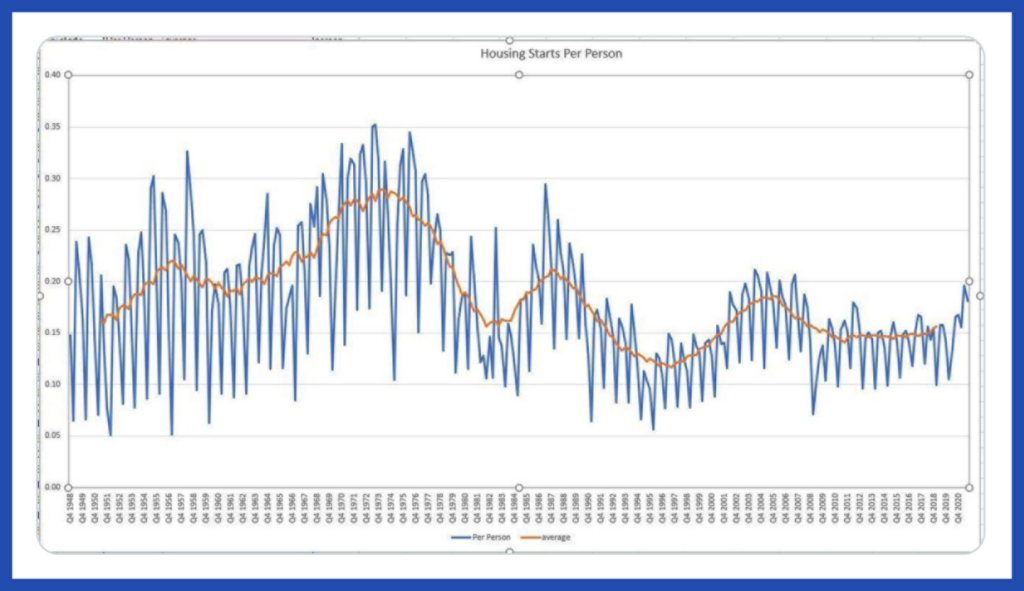

On Monday, the Canada Mortgage and Housing Corporation announced housing starts rose from 241,111 units in April to 264,506 units in May: good for a 10% increase. The pace was highest in Montreal, where starts were up 104%, and in Toronto, they were notably up 47%. That’s a pretty good clip, considering how high interest rates are at the moment.

While it would be statistically correct to say that this level of housing starts is near historically high levels, that doesn’t quite tell the whole story.

To get a more accurate historical perspective, we should consider the housing starts per capita over the years. After all, Canada’s higher population should mean more capital, carpenters, electricians and other factors of production that go into housing creation, right?

Perhaps we’re moving in the right direction, but we’ll need a major uptick in housing starts before we have proportionately the same housing creation numbers as we did back in the heyday of the 1970s. Many young Canadians are hoping recent government incentives will spur more housing development sooner rather than later.

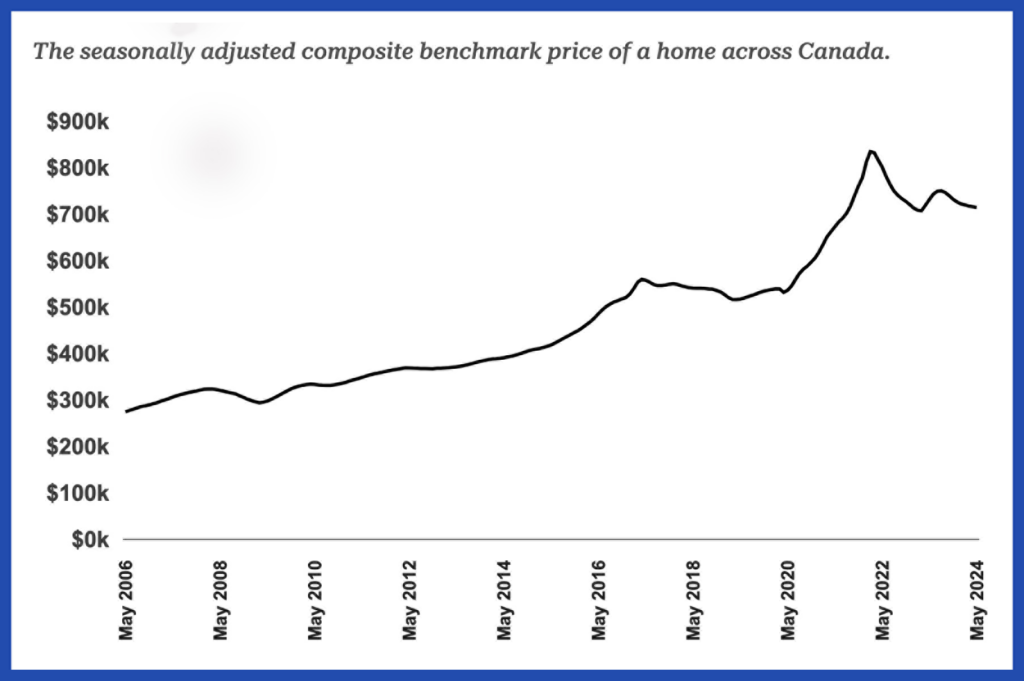

While there is more housing supply on the way, it appears that high interest rates continue to affect the current market. This week, the Canadian Real Estate Association released data that revealed total Canadian home sales were down nearly 6% in May on a year-over-year basis. The average home price slipped to $699,117, down 4% from May 2023 and about 14.4% from its peak in February 2022.

While the small interest rate cut earlier this month may spark some renewed appetite in the real estate market, it’s notable that the number of newly listed properties has jumped 28.4% from this time last year. As more mortgage renewals start to come up, it will be interesting to see which force is stronger: the increase in demand as mortgage rates decrease, or the continued softening of the market as more folks are forced to list houses they can no longer afford (as well as more new units being added).

What does the average Canadian buy?

Each month, Statistics Canada produces an inflation report based on the consumer price index (CPI), a representative “basket” of goods and services across eight categories (food, shelter, transportation, etc.) whose prices are tracked over time. Most of us simply accept that the CPI is a good measurement to go by, while others think it’s out of touch with reality. This week, the CPI got its annual update, after the Statistics Canada team looked at how average consumer preferences have changed over the last 12 months.

The CPI can’t stay the same from year to year because what we buy changes significantly over time. Consequently, measuring inflation with exactly the same goods from years ago doesn’t make much sense. For example, compact discs and videocassettes would have been part of the CPI basket back in my childhood—probably not so much today. Here are some of the more notable changes:

It appears the rising AI tide continues to lift all boats in the U.S. tech sector.

Deal-seeking customers power Dollarama

It was a quiet week for Canadian earnings announcements, with Dollarama (DOL/TSX) being the only large company to release quarterly results. Some Canadian investors might not realize that this humble dollar store is actually the 33rd biggest company in Canada, making it larger than Telus, Rogers or Fortis.

Dollarama earnings highlights

Here’s what the thrifty retailer announced this week:

Dollarama (DOL/TSX): Earnings per share of $0.77 (versus $0.75 predicted), and revenues were identical to the $1.41 billion expert prediction.

Comparable store sales were up 5.6%, and there are plans to add 60 to 70 new stores to the list of 1,551 existing Canadian stores.

“As anticipated, we are seeing a progressive normalization in comparable store sales, with growth primarily driven by persistent higher than historical demand for core consumables and other everyday essentials.”

– Neil Rossy, Dollarama CEO

Despite the positive news, share prices dropped on the heel of news for an aggressive expansion under the Dollarcity subsidiary in Latin America. The $761.7 million investment grows Dollarama’s total equity from 50.1% to 60.1%.

“We look forward to preparing for entry in Mexico in the near term, a large and dynamic market with untapped potential in the value retail space, guided by the same careful and disciplined approach as with our successful entries in Colombia in 2017 and in Peru in 2021.”

– Neil Rossy, Dollarama CEO

Long-term Dollarama shareholders are probably quite happy despite the pullback, as the stock is up a scorching 26% year to date, and 42% over the last 12 months.

Stock splits for Nvidia and Canadian Natural Resources

If you were recently looking at the stock prices of Canada’s sixth largest company, Canadian Natural Resources (CNQ/TSX), and the world’s third largest company, Nvidia (NVDA/NASDAQ), you might be alarmed to see steep price declines. No need to panic; this is simply the result of stock splits. (Read: “What does Nvidia’s stock split mean for Canadian investors?”)

Early this week, CNQ executed a 2-for-1 stock split, and Nvidia executed a 10-for-1 stock split. (Broadcom also announced that it too would be undertaking a 10-for-1 stock split in the near future.)

While The Big Short film is a riveting watch, “The Big Cut” may be even more enthralling.

The Bank of Canada (BoC) made the decision to cut its key interest rate to 4.75% on Wednesday. It’s the first rate cut since March 2020. With about $700 million worth of mortgages coming up for renewal in Canada this year, “The Big Cut” is going to affect a lot of Canadians.

“We’ve come a long way in the fight against inflation. And our confidence that inflation will continue to move closer to the 2% target has increased over recent months.”

– BoC Governor Tiff Macklem

Macklem also said: “Total consumer price index inflation has declined consistently over the course of this year, and indicators of underlying inflation increasingly point to a sustained easing.”

However, in the tradition of central bankers the world over, Macklem was also careful to speak using neutral language, pointing out that the BoC was going to take things “one meeting at a time.” He added “We don’t want monetary policy to be more restrictive than it needs to be to get inflation back to target. But if we lower our policy interest rate too quickly, we could jeopardize the progress we’ve made.”

While the BoC was the first G7 country to begin cutting interest rates, the European Central Bank followed suit on Thursday, cutting its key interest rate from 4% to 3.75%. Market experts are speculating that the BoC will cut interest rates three or four more times in 2024. (There are four announcements left on the BoC interest rate schedule).

The BoC (as well as many other central banks) have taken a lot of flak over the last couple of years. But if they manage to cut interest rates, get the economy growing again, and avoid resurgent interest rates, then they deserve a hand. Such a Goldilocks scenario would certainly qualify as a “soft landing” by most economists’ definitions.

If the BoC manages to slowly cut interest rates, while managing to get the economy growing again—all without supercharging inflation—that would certainly qualify as a “soft landing” by most economists’ definitions.

Lululemon stops its share price slide, Nvidia skips past Apple

It was a relatively slow week for earnings news, but Canadian retailers Lululemon and the North West Company let investors know how they did last quarter. Note: Lululemon releases its earnings numbers in U.S. dollars, while the North West Company releases its earnings in CAD. You might remember the North West Company from your history textbooks, as the Winnipeg-based grocery chain is significantly older than Canada (1779 versus 1867).

Retail earnings highlights

The latest share prices and revenue for Lulu and NWC.

Lululemon (LULU/NASDAQ): Earnings per share of USD$2.54 (versus USD$2.40 predicted) on revenues of USD$2.21 (versus USD$2.20 billion predicted)

North West Company (NWC/TSX): Earnings per share of $0.61 (versus $0.58 predicted) and revenues of $617.50 million (versus $626.31 million predicted).

Lulu shared a mostly positive earnings report and saw its share price rise 8% on Wednesday. This was welcome news for shareholders who have watched the stock go down over 36% year to date. Shares of the North West Company were flat the day after announcing earnings that were in line with expectations. (Read more about Lululemon’s earning report.)

Corporations, it seems, are just really, really good at making larger-than-ever profits. There are many reasons for fatter margins. It could be innovative new products and services, lower taxation, decreasing competition, willingness of consumers to pay higher prices, and so on. The bottom line is that the stock market will certainly pull back at some point (as it did this week). And there are solid reasons why companies are worth more now than they were, say, a few years ago.

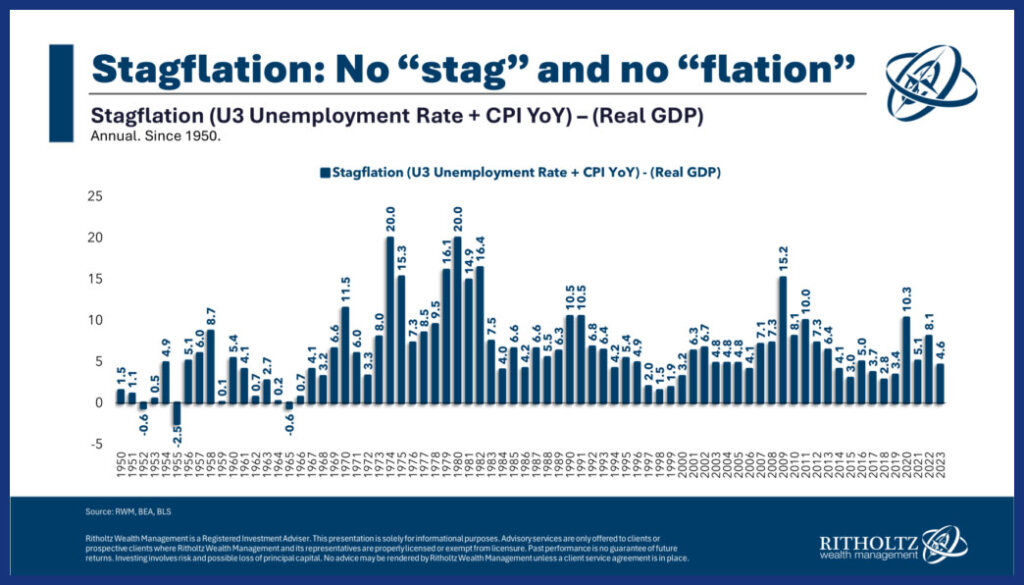

Back in spring/summer of 2022, all the “cool” writers were predicting a scary-sounding future of stagflation. We, on the other hand, were a bit more skeptical. We felt that these worst-case economic scenarios were just around the corner.

So, two years later, are we fearing unemployment rates may shoot through the roof? Are we fearing a shrinking GDP? (Gross domestic product, that is.)

Barry Ritholtz doesn’t think so. He’s the co-founder, chairman and chief investment officer of Ritholtz Wealth Management LLC, in New York City.

The above chart illustrates what economists call the “misery index.” It’s a rough approximation of measuring stagflation.

You’ll notice that while things weren’t exactly great in 2020 and 2022, they weren’t historically bad either. Last year was downright tame, and (spoiler alert!) we’re probably in for another not-so-miserable year for 2024.

Note, though, that this features American data. While Canada’s misery index isn’t quite as upbeat as the USA’s, Canada still sits below long-term averages.

Sure, the cost of living is up in for Canadians and Americans. But so are wages. And unemployment in the USA is at 60-year lows. While growth in Canada has been “anemic,” we haven’t experienced the deep recession folks were worried about over the last couple of years. Growth in the U.S. has been excellent. And inflation has steadily trended downward in both countries.

The bank said Thursday it will now pay a quarterly dividend of $1.42 per share, an increase of four cents. It also said it plans to buy back up to 30 million of its shares.

The moves came as RBC said it earned $3.95 billion or $2.74 per diluted share for the quarter ended April 30, up from $3.68 billion or $2.60 per diluted share a year earlier, helped in part by record capital markets revenue.

“This quarter, we saw strong growth across diversified revenue streams,” said chief executive Dave McKay on an earnings call.

He said the bank’s capital generation means it has options ahead for growth, including potential acquisitions, even as the bank returns more money to shareholders.

“This enormous capital that we are generating gives us significant strategic flexibility inorganically.”

The bank also has a wide range of growth options within the bank now, including making the most of its $13.5-billion HSBC Canada acquisition.

End of uncertainty for former HSBC employees

The roughly 4,500 employees RBC took on with the acquisition are now free from the uncertainty around the deal, and the barriers it posed to bringing on clients, he said.

“They’ve been on the defence for 18 months, and now we’re on the offence and you can see the excitement in their eyes to get back,” said McKay.

Investing in high-yield dividend stocks is an easy way to turn idle cash sitting in your portfolio into a lucrative income stream. High-quality income producers can provide you with a steadily rising stream of dividend income.

Pipeline giants Enbridge(NYSE: ENB) and Enterprise Products Partners(NYSE: EPD) are no-brainers among high-yield dividend stocks. They have superior track records of increasing their already sizable payouts. With low share prices, they’re ideal for those with less than $200 to invest right now.

Lots of fuel to grow its payout

Canadian pipeline and utility operator Enbridge has a forward dividend yield approaching 7.5%. That implies you can earn nearly $7.50 of annual dividend income for every $100 invested in the energy infrastructure company. While U.S. investors are subject to a 15% withholding tax (unless held in an individual retirement account, or IRA), they’d likely pay dividend taxes anyway for companies owned in a regular brokerage account.

Enbridge pays a very sustainable dividend. The company generates extremely durable cash flow (98% comes from stable cost-of-service agreements or long-term contracts) and pays out 60% to 70% of that steady income in dividends. It retains the rest to help fund expansion projects. Enbridge also has a strong balance sheet, with its leverage ratio well within its target range. That gives it additional financial flexibility to fund its growth.

The company currently has a massive backlog of expansion projects under construction, primarily lower-carbon energy infrastructure, like gas pipelines and renewable energy projects. Enbridge also has additional investment capacity to make acquisitions. Those drivers help fuel its view that it can grow its cash flow per share by around 3% annually through 2026 before accelerating to 5% per year after that.

That growing cash flow should give Enbridge the fuel to continue increasing its dividend. The company has raised its payout for 29 straight years, including by more than 3% late last year.

A rock-solid income stream

Master limited partnership (MLP) Enterprise Products Partners currently has a forward yield of more than 7%. As an MLP, its income is largely tax-deferred, making it an excellent way to generate passive income. However, there’s a caveat: MLPs send Schedule K-1 tax forms each year (often later in the filing season), which can complicate your taxes.

The MLP’s sustainable and growing distribution payments can make those tax complications well worth it, though. Enterprise has increased its payout every year for a quarter century, including by more than 5% over the past year.

Enterprise Products Partners generates very stable cash flow, with the bulk coming from assets backed by long-term contracts and government-regulated rate structures. The MLP currently produces enough cash to cover its high-yielding payout by a comfy 1.7 times. That enables it to retain some money to fund expansion projects. It also has a very strong balance sheet (it has the highest credit rating in the midstream sector), giving it even more financial flexibility to fund its continued expansion.

The MLP has several billion dollars of expansion projects under construction, which should come online by the first half of 2026. It has several other projects under development as well, including a potentially needle-moving offshore oil export facility, giving it lots of visibility into future growth. The company also has the financial flexibility to opportunistically make acquisitions.

With a strong financial profile and visible growth ahead, Enterprise Products Partners should be able to continue increasing its high-yielding distribution.

High-quality, high-yielding dividend stocks

Enbridge and Enterprise Products Partners have exceptional track records of increasing their dividend payments. With more growth likely, they’re no-brainer buys for those seeking to turn some idle cash into a lucrative and growing income stream.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Matt DiLallo has positions in Enbridge and Enterprise Products Partners. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

A stock split divides existing shares into smaller pieces. So, if you previously had one share of Nvidia worth $1,000, you would now have 10 shares of Nvidia each worth $100, for an unchanged total value of $1,000. Stock splits are a way for companies to ensure that investors can easily buy and sell single shares.

The massive hype behind Nvidia has resulted in a price-to-earnings ratio of over 55x. By comparison, tech giants Microsoft and Apple currently have ratios of 36x and 29x, respectively. Conventional logic says Nvidia’s growth has to fall back into line at some point—but this sustained period of record earnings is tough to argue with for the moment. Nvidia made 18% more money in Q1 2024 than it did in Q4 2023, and it made a whopping 262% more money than it did in Q1 2023.

Founder and CEO Jensen Huang sounded appropriately upbeat in stating, “The next industrial revolution has begun—companies and countries are partnering with Nvidia … to produce a new commodity: artificial intelligence.”

Nvidia bought back $7.7 billion worth of its shares in Q1 and announced it was increasing its dividend from four cents to 10 cents per share (on a pre-split basis).

Frankly, I think it’s just a matter of time until competitors start to close the gap with Nvidia and some of those juicy profit margins start to shrink. That said, there is a whole lot of money to be made while that process plays out. Clearly, investors are willing to pay a premium for Nvidia’s future earnings.

Target (TGT/NYSE): Earnings per share of $2.03 (versus $2.06 predicted), and revenue of $24.53 billion (versus $24.52 billion estimated).

Macy’s (M/NYSE): Earnings per share of $0.27 (versus $0.15 predicted), and revenue of $4.85 billion (versus $4.86 billion estimated).

Lowe’s (LOW/NYSE): Earnings per share of $3.06 (versus $2.94 predicted), and revenue of $21.36 billion (versus $21.12 billion estimated).

All three of these retail heavy hitters cited a stretched consumer as the main reason for mediocre quarterly earnings reports. Target CEO Brian Cornell explained that low sales numbers reflected “continued soft trends in discretionary categories.” Compared to its rival Walmart, Target has substantially fewer customers coming into its stores to buy groceries, so the consumer shift to necessities appears to be hitting it harder.

Lowe’s CEO Marvin Ellison had similar thoughts on the current retail scene, saying, “Interest rates can go down, but you still need consumer confidence to come up.” Macy’s CFO and COO Adrian Mitchell went so far as to say that its team expects consumers “will remain under pressure for the balance of the year.”

Rainey went on to comment on the state of American consumers. While “wallets are still stretched,” it was also the case that “even the low-income consumer seems to be holding in there pretty well,” he said. He also added that shoppers were still coming to Walmart to buy necessities like food and health-related items, along with less general merchandise (such as home goods and electronics).

Going forward, Walmart is banking for growth on new revenue drivers, such as its subscription program, Walmart+. Global advertising grew 24% in Q1 and will be an interesting supplemental line of business for the company going forward—as it has been for retail rival Amazon.

In less celebratory news, Walmart has plans to streamline its store offerings by shuttering Walmart health clinics in American locations.

Given that consumers continue to cut back on home renovations after the massive COVID reno-boom, it stands to reason that Home Depot shareholders might be in for a bit of a sideways run for a while.

On Monday, the company revealed that while it was reporting its worst revenue miss in two decades, its bottom line was still holding up pretty well. Shares were mostly flat on the week.

For those who haven’t watched Dumb Money or Eat The Rich (excellent airplane flicks btw), GameStop stock is the iconic “meme stock.”

What is a meme stock?

A meme stock is an equity that sees growth instigated by internet memes—usually not based on earnings or value. To sum it up: GameStop is a semi-dying company that appears unlikely to make a profit in the foreseeable future. Consequently, it doesn’t make a lot of sense (according to traditional investing metrics) to pay a high price for GameStop stock. However, speculative bets on where its price could move can quickly make investors money (or make them lose it) quite quickly. Investors who short sell GameStop’s stock are essentially betting that the price will continue to go down. If enough people buy shares of GameStop, those short bets against its share price can cost those investors a ton of money.

When countries look to attract the attention of big financial funds, they often attempt to brand themselves in a manner that will bring much-needed foreign investment to their shores. For example, you might see buzzwords such as:

Innovative

Efficient

Attractive

Shareholder-friendly

But given Canada’s stagnating economy, I think it’s appropriate to get excited about this Warren Buffett quote:

“We do not feel uncomfortable in any shape or form putting our money into Canada.”

When Buffett takes the stage at his annual “Woodstock for capitalists” in Omaha each year, the investing world sits up to take notice. So, it was noteworthy to hear his lukewarm notes about Canada, including:

“There are a lot of countries we don’t understand at all. So, Canada, it’s terrific when you’ve got a major economy, not the size of the U.S., but a major economy that you feel confident about operating there. … Obviously, there aren’t as many big companies up there as there are in the United States. There are things we actually can do fairly well that Canada could benefit from Berkshire’s participation.”

He went on to reveal his company’s possible Canadian strategy, saying, “In fact, we’re actually looking at one thing now.” While most other investors are cool on Canadian stocks, it’s interesting to see Buffett warm (again).

Buffett’s last major foray into Canada generated a massive 70% gain in a single year back in 2017 when he invested in Home Capital Group, so he may know a thing or two about making money in the Great White North.

Other highlights from the annual general meeting included (all figures in U.S. dollars):

Buffett’s company, Berkshire Hathaway (BRK.A/NYSE) is currently benefiting from high interest rates, as it sits on a massive cash hoard of $189 billion.

Berkshire sold about $39 billion worth of Apple stock during the quarter. Berkshire remains Apple’s single biggest shareholder with over $135 billion still invested.

In the absence of big deals, Berkshire continues to reward its shareholders by buying back its own shares to the tune of $2.6 billion for the quarter. When asked why he hadn’t used the cash to make big, flashy investments, Buffett responded, “I don’t think anyone sitting at this table has any idea how to use it effectively, and therefore we don’t use it. We only swing at pitches we like.”

Berkshire’s operating profit rocketed up 39% on a year-over-year basis.

Underwriting profits at Buffett’s insurance companies were up 185% year-over-year to $2.6 billion.

Buffett told the audience that he had sold all of Berkshire’s remaining Paramount Global shares and was refreshingly honest in admitting, “It was 100% my decision, and we’ve sold it all and we lost quite a bit of money.”

Buffett wrapped up the annual meeting by saying humbly, “I not only hope you come next year, [but] I hope I come next year.” He later added, “I know a little about actuarial tables,” in reference to his insurance expertise.

This insight was made particularly relevant given the absence of long-time friend and partner Charlie Munger at this year’s event. Munger passed away at age 99 in November 2023.

My number-one investing hero has to be Brandon Beavis. His YouTube videos taught me everything I know about investing. My money hero is Adrian Bar, Canadian in a T-Shirt on YouTube. He taught me how to optimize taxes and keep more money in my pocket. Third, my finance hero is Maxwell Nicholson, the CEO of Blossom. He built an app that shows you what your favourite influencers and friends are investing in, and transparency is truly what Gen Z needs nowadays.

How do you like to spend your free time?

Free time is such a luxury for me. While working two to three jobs from the ages of 19 to 25, I never had free time. I’ve been self-employed for six months now, and I’ve been travelling a lot recently. I also love going on solo dates, taking myself out for breakfasts, dinners, spa treatments and window shopping.

If money were no object, what would you be doing right now?

I would definitely be travelling and doing all the excursions, like swimming with dolphins, scuba diving, ziplining, paragliding and so on.

What was your first memory about money?

Buying snacks at the grocery store. I learned that money allows me to purchase items that I want.

What’s the first thing you remember buying with your own money?

The first thing I bought with my first paycheque was a silver ring at Swarovski. I wanted to buy something that would remind me of my independence and something that would never go out of style.

What was your first job?

I got my first job at age 16, as a sales associate at Old Navy.

What was the biggest money lesson you learned as an adult?

The biggest money lesson I learned was the importance of putting every single dollar of mine to work. I wish I’d researched all the available investment vehicles, like high-interest savings accounts, the stock market and GICs, when I was 19. I missed out on potential gains because I was unaware that such investment vehicles exist. It was important for me to go through that, because now I love exploring more ways to put my money to work, and now I have a platform to share my findings.

What’s the best money advice you’ve ever received?

Diluted bitumen started flowing through the expanded Trans Mountain Pipeline on Wednesday (even at a brisk walking pace, it’ll take weeks to reach its destination). This is raising hopes that at last Canada’s oil sands producers will be able to narrow the discount paid by a now-larger cohort of refiners for their product. Meanwhile, two of the largest shippers on the pipeline reported first-quarter earnings sans that hoped-for revenue bump.

Oilsands earnings highlights

Two producers released their financials this week.

Cenovus Energy (CVE/TSX): Earnings per share rose to $0.62 (versus $0.54 predicted) on revenues of $13.4 billion.

Canadian Natural Resources (CNQ/TSX): Earnings per share of $1.37 (versus $1.48 predicted) on revenues of $8.244 billion.

Cenovus output and profits both surprised on the upside, and the company further sweetened the pot by hiking its base dividend by 29% and announcing a variable dividend of 13.5¢ a share for this quarter. Production for the quarter exceeded 800,000 barrels of oil equivalent per day. At the same time the company modestly reduced its overall debt level.

Results for Canadian Natural Resources suffered from lower-than-expected production and realized prices, especially on the natural gas side. Output came in at 1.33 million barrels of oil equivalent per day.

Amazon, Apple still magnificent

Two more technology mega-caps reported first-quarter results this week, helping keep the Magnificent 7 bandwagon rolling.

U.S. earnings highlights

All amounts in U.S. dollars

Amazon (AMZN/NASDAQ): Adjusted earnings per share were $0.98, exceeding the consensus estimate of 83¢, while revenue of $143.3 billion outstripped the $142.6 billion predicted.

Apple (AAPL/NASDAQ): Earnings per share hit $1.53 (beating the estimate of $1.50) on revenue of $90.8 (versus expectations of $90.3 billion).

Amazon reported continued strong demand for its Web Services, as corporate customers signed longer-term deals with bigger commitments. Generative artificial intelligence (AI) components added to the overall spend, the company said. Advertising revenue also enjoyed strong growth, although there are signs consumers are turning more cautious with retail spending. Following the earnings release, the stock rose 3% Wednesday morning.

Amazon rival Walmart, meanwhile, opted to close 51 health clinics at U.S. stores and discontinue its virtual health services, the company announced Tuesday. It blamed high operating costs and “a challenging reimbursement environment” for poor profitability in the division first launched in 2020.

Apple’s revenues fell less than expected and earnings surpassed Wall Street estimates. The company also said it would boost its dividend to 25¢ a share and authorize $110 billion worth of share buybacks. Services revenue grew to nearly $24 billion, offsetting declines in sales of iPhones and other devices. Sales fell 8% in Greater China (including Taiwan, Singapore and Hong Kong), but that drop-off was not as severe as analysts anticipated. Apple shares surged nearly 6% before markets opened Friday, and more than a dozen analysts raised their target price on Apple.

Tipping on fast food

There’s no accounting for taste as fast-food purveyors moved in divergent ways in the first quarter; some were squeezed between cost inflation and consumer austerity while others continued to super-size their sales.

The high interest rates over the last few years have led to the explosive growth of cash holdings, including certificates of deposit (like guaranteed investment certificates (GICs) in Canada) and money market funds. Cash holdings in the fourth quarter of 2023 increased by $270 billion to $18 trillion. Despite that relatively small increase, the rise in value of U.S. equities has led to American households to hold more of their wealth in equities than at any point in history (save the dot-com boom in 2000).

There are likely many reasons for this shift, but these factors could likely be the most prominent influences:

It’s just simple math, since U.S. stocks are on such a long “winning streak” post-2008, the value of those assets is going to be worth more relative to other assets.

As companies complete the shift from defined-benefit pension plans to defined-contribution plans, it’s possible more stocks are being purchased at the individual level.

The average investor got smarter thanks to much more accessible information. Consequently, they now understand the long-term wealth-creating potential of owning large companies (both domestically and internationally).

Millennials and older Gen Zers are sticking around in the stock market after being introduced to it during the meme-stock and pandemic world of 2021.

There hasn’t been a brutal bear market for U.S. stocks since 2008. Sure, there were substantial pullbacks at the start of the COVID-19 pandemic, and then again in 2022. But, those were relatively short-lived. When the stocks did come back, they returned in a massive way—thus, rewarding buy-and-hold investors.

A contrarian investor might say this indicates an oversold market. We’re not so sure that’s the case. Given the long-term track record of U.S. stocks, we’d be surprised to see stock allocations fall below 35% of household assets in the foreseeable future. That’s as low as it got during the worst days of the pandemic. There has been a durable paradigm shift in how investors see the stock market from a risk/reward perspective.

Canadian investors aren’t doing so bad either. We hit a record high last quarter for financial assets of $9.74 trillion, and overall net worth reached $16.4 trillion. Financial assets (shorthand for stocks and bonds) increased overall net worth by about half a trillion bucks, while residential real estate was down about $158 billion. Household debt was up 3.4%, but that’s actually the slowest rise in debt since 1990, and the debt-to-income ratio actually fell slightly.

Will new corporations spin off more value?

When big corporations buy new companies or dive into new lines of business they often tout the advantages of integration and synergies. The theory goes that the asset will be more valuable as a cog in the bigger machine. General Electric (GE/NYSE) and 3M (MMM/NYSE) are two of the world’s largest industrial companies and it was interesting to see them move in the opposite direction this week.

In contrast to the bigger-is-better theory, companies can sometimes get too big and be hindered by layers of bureaucracy. In that case, the spin-off idea is put forward, in which a part of the company will be separated into its own entity so it can focus on providing a narrower product or service. The more narrowly-focused company should, in theory, excel as it’s no longer distracted by the tangle of corporate machinery at the parent company.

GE completed its corporate restructuring last Wednesday, as the former parent company has now been divided into:

GE Vernova (GEV/NYSE): The energy assets of the old GE.

GE Aerospace (GE/NYSE): The old GE market ticker continues on as a pure aerospace company.

GE HealthCare (GEHC/NASDAQ): GEHC was successfully spun off in late 2022, and is up about 57% since it started trading.

GE Aerospace shares finished down 2.42% on their first day of trading, while GE Vernova was down 1.42%.

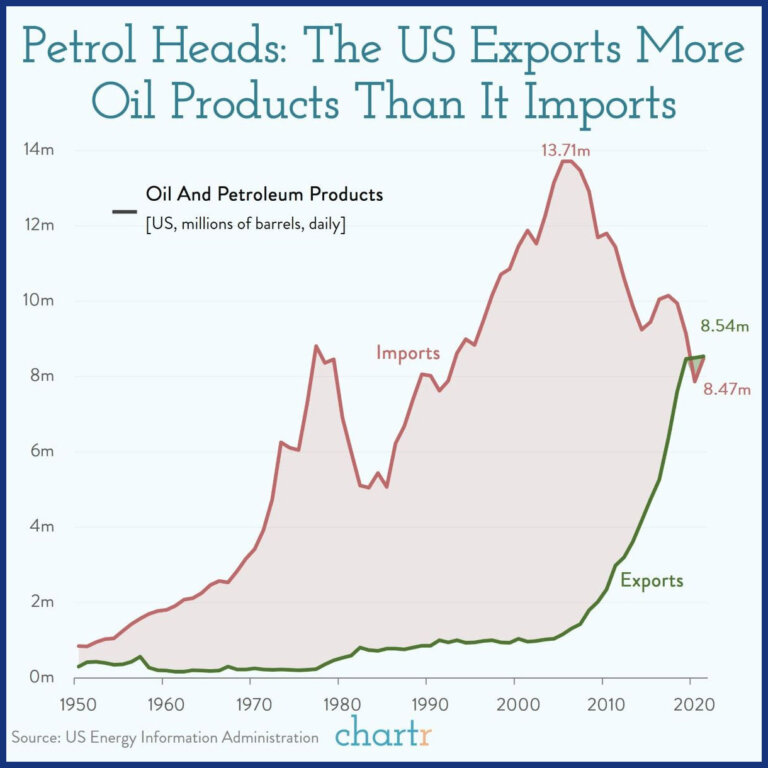

With so much going on in the world, it might have slipped past some Canadian investors that the U.S. fossil fuel industry just hit an interesting milestone. America now has the honour of producing more oil in a single day than any other country in the history of our planet. Yes, even more than Saudi Arabia.

When you consider that the USA has been a massive oil importer for much of the last 70 years, it’s pretty noteworthy that the U.S. exported four million barrels of oil per day last year.

It certainly appears that investors are not shying away from providing capital to American fossil fuel companies. It also means that Canadian efforts to turn away from natural gas (despite our allies essentially begging us for more yet again this week) may not add up to much in the great push against global warming.

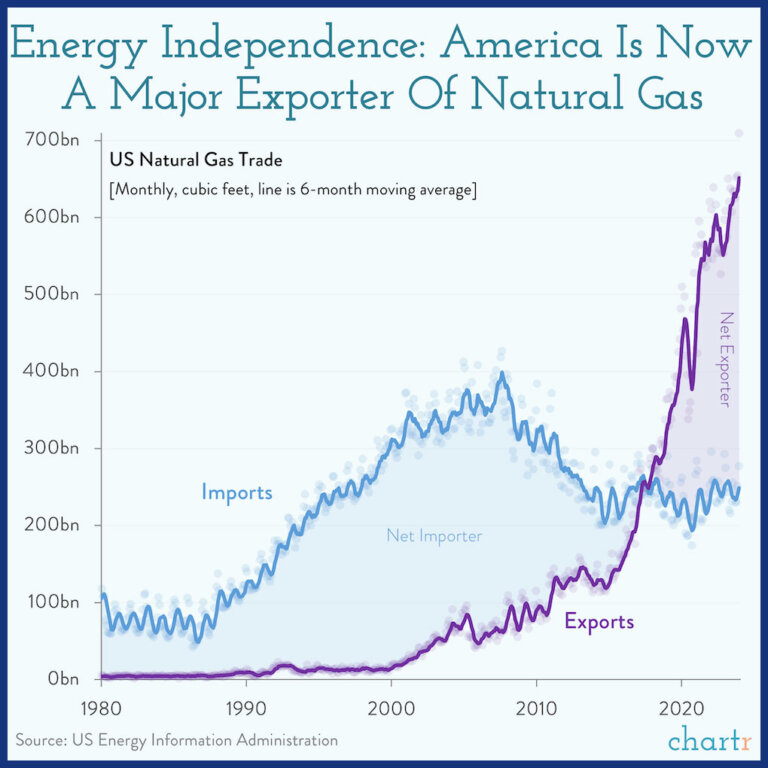

The USA is now the world’s largest exporter of natural gas, as well.

Wow, it’s a good thing the Keystone XL pipeline got cancelled, as it appears to have put a stop to all that American fossil fuel business—and at hardly any cost to the Canadian economy either!

Economists would argue that the best way, by far, to reduce the amount of fossil fuel being burned would be to put a tax on it. How popular is that tax on carbon these days anyway?

Clearly, the world has to decide on what sort of level playing field it wants to create in regards to the rules for carbon reduction efforts, as Canada’s attempt to go it alone doesn’t seem to be gaining much traction.