Comparing these ETFs is mostly about assessing the potential of dividend growth versus a high-yield strategy.

The Vanguard ETF’s methodology currently emphasizes tech at the top (for better or worse), while Schwab’s looks for durable companies with healthy balance sheets.

I’ve always liked Schwab’s strategy, which considers dividend growth history, yield, and balance sheet quality.

Dividend income investing usually isn’t as simple as just picking the best dividend stocks. Your personal goals and income requirements can have a big impact on whether you focus on dividend growth or high yield.

Dividend growth stocks tend to have greater durability and sustainability, but can come with low yields. High yield stocks can help solve the income problem, but they can also turn into yield traps that damage total returns. That makes the argument between the Vanguard Dividend Appreciation ETF(NYSEMKT: VIG) and the Schwab U.S. Dividend Equity ETF(NYSEMKT: SCHD) an interesting one.

Is the current market environment built more for classic dividend growth or one that focuses on high yield with a quality tilt?

Image source: Getty Images.

The Vanguard Dividend Appreciation ETF tracks the S&P U.S. Dividend Growers Index. It targets large-cap stocks that have grown their annual dividend for at least 10 consecutive years. It eliminates the top 25% of yields in order to avoid some of those potential yield traps and weights the final portfolio by market cap.

There’s good and bad in this strategy. On the plus side, the elimination of high-yielders makes this more of a pure dividend growth play, even if it comes at the expense of income. On the downside, the market cap-weighting gives preference to the biggest companies regardless of yield or dividend history.

The Schwab U.S. Dividend Equity ETF follows the Dow Jones U.S. Dividend 100 Index. It targets companies of all sizes that have paid (but not necessarily grown) dividends over the past decade and scores them using metrics such as return on equity (ROE), cash flow to debt, dividend growth rate, and yield. The 100 stocks with the best combination of these factors make the final cut.

This methodology produces a portfolio heavily tilted toward the yield factor, but filled with higher-quality stocks. This is, in my opinion, an advantageous way of building the portfolio. Selecting purely by yield can be dangerous because it gives no consideration to sustainability. By selecting stocks only backed by quality balance sheets helps address that problem.

The Vanguard Dividend Appreciation ETF has benefited from its market-cap-weighting strategy because it’s made Broadcom, Microsoft, and Apple its top three holdings. That’s helped past performance relative to other dividend ETFs, but what happens if the market keeps rotating away from tech as it’s begun to do in 2026?

The Schwab U.S. Dividend Equity ETF has lagged mightily over the past three years, but that’s a function of its strategy being out of favor, not the strategy itself. Overall, I really like that it incorporates dividend growth history, dividend quality, and high yield into its strategy. That really helps it identify a portfolio of top-tier stocks.

I believe that the Schwab ETF is the better buy right now. With questions surrounding the direction of the economy, the health of the labor market, and the geopolitical backdrop, we could see a continuation of the current rotation away from tech and into more defensive issues. Its portfolio is much better positioned for that type of scenario.

Before you buy stock in Vanguard Dividend Appreciation ETF, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vanguard Dividend Appreciation ETF wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

David Dierking has positions in Apple and Vanguard Dividend Appreciation ETF. The Motley Fool has positions in and recommends Apple, Microsoft, and Vanguard Dividend Appreciation ETF. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Bristol Gate Capital Partners, an investment management company, published its Q3 2025 investor letter for the “US Equity Strategy”. A copy of the letter can be downloaded here. The strategy underperformed the benchmark, the S&P 500® Total Return Index, this quarter, but still surpassed the index in dividend growth. The underperformance was due to a lack of significant exposure to the AI/TMT sector or the Value sector, which provides advantages stemming from the Federal Reserve’s rate cut. The portfolio returned 15% dividend growth over the trailing 12 months, driven by the strong underlying fundamentals. In addition, please check the fund’s top five holdings to know its best picks in 2025.

Prediction Market powered by

In its third-quarter 2025 investor letter, Bristol Gate US Equity Strategy highlighted stocks such as Broadcom Inc. (NASDAQ:AVGO). Broadcom Inc. (NASDAQ:AVGO) is a leading technology company that designs and develops various semiconductor and infrastructure software solutions. The one-month return of Broadcom Inc. (NASDAQ:AVGO) was -8.31%, and its shares gained 50.90% of their value over the last 52 weeks. On December 30, 2025, Broadcom Inc. (NASDAQ:AVGO) stock closed at $349.85 per share, with a market capitalization of $1.659 trillion.

Bristol Gate US Equity Strategy stated the following regarding Broadcom Inc. (NASDAQ:AVGO) in its third quarter 2025 investor letter:

“Broadcom Inc. (NASDAQ:AVGO) reported its third quarter results on September 4, which beat analyst expectations for both revenue and earnings per share. However, the highlight of the quarter was the addition of a fourth significant customer for its XPU (custom AI accelerator) products, who has placed over $10 billion in orders to be shipped in Q326. The combination of continued growth from the existing three customers and the addition of this fourth major customer will drive a material improvement in Broadcom’s AI revenue growth in fiscal 2026 compared to the previous outlook. Management now expects 2026 AI revenue growth to exceed fiscal 2025’s 50-60% rate. In addition to the four customers for which it has secured orders, the company is working on projects with three other hyperscalers. Our “NVDA’s demand today is AVGO’s opportunity tomorrow” thesis continues to play out in the hyperscaler market where demand for custom AI accelerators continues to grow as each of them journeys towards compute self-sufficiency. The company’s overall backlog now stands at $110B, with over 50% from semiconductors.”

AVGO Stock: A Strong Buy Pick Backed by Robust Cash Flow and Dividend Growth

Broadcom Inc. (NASDAQ:AVGO) is in the 12th position on our list of 30 Most Popular Stocks Among Hedge Funds. As per our database, 183 hedge fund portfolios held Broadcom Inc. (NASDAQ:AVGO) at the end of the third quarter, which was 156 in the previous quarter. In the fiscal third quarter of 2025, Broadcom Inc. (NASDAQ:AVGO) reported record revenue of $16 billion, up 22% year-over-year. While we acknowledge the potential of Broadcom Inc. (NASDAQ:AVGO) as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on thebest short-term AI stock.

There’s increasing uncertainty these days. The economy is starting to show some signs of slowing, and the possibility of an escalating conflict in the Middle East is creating anxiety. On top of that is the upcoming presidential election.

All this uncertainty has investors rattled, with the market recently having its worst day since early last year.

These factors might have you fearing that another bear market could be around the corner. One potential way to help shelter your portfolio against a future market storm is to insulate it with high-quality, high-yielding dividend stocks. WEC Energy(NYSE: WEC), Enbridge(NYSE: ENB), and Northwest Natural Holding (NYSE: NWN) stand out to these Motley Fool contributors as great safe havens.

A boring utility with impressive dividend growth

Reuben Gregg Brewer (WEC Energy): One of the most attractive things about WEC Energy is that it flies under the radar. As a fairly traditional regulated electric and natural gas utility serving around 4.7 million customers in parts of Wisconsin, Illinois, Michigan, and Minnesota, its business is very straightforward.

And because of the importance of energy to modern life (and the monopoly WEC has been granted in the regions it serves), its customers are going to keep using power no matter what the market is doing.

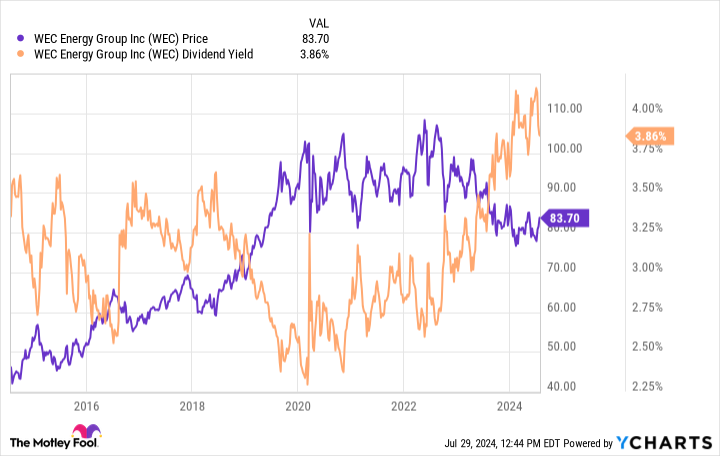

Sure, interest rates are high, and that’s going to be a headwind for WEC Energy, which like most utilities makes heavy use of debt to fund its business. And it is dealing with an adverse regulatory ruling in Illinois with regard to natural gas. But these problems have depressed the share price and increased the attractiveness of the stock for income investors, given that it now yields a historically high 4% or so.

WEC Chart

That dividend, meanwhile, is backed by 21 consecutive annual increases. The average yearly increase over the past decade was roughly 7%, which is pretty attractive for a utility. Meanwhile, management expects earnings growth to fall between 6.5% and 7% a year for the foreseeable future.

If history is any guide, the dividend will follow earnings higher. And given the regulated nature of the business, the good news should continue to flow even through a bear market. But jump quickly or you might miss the opportunity here.

A model of stability and durability

Matt DiLallo (Enbridge): Enbridge has one of the lowest-risk business models in the energy sector. The Canadian pipeline and utility operator gets 98% of its earnings from stable cost-of-service or contracted assets, like oil and gas pipelines, natural gas utilities, and renewable energy facilities. These assets produce such predictable cash flow that Enbridge has achieved its financial guidance for 18 straight years.

The company took a notable step to further enhance the stability of its cash flow over the past year by acquiring three natural gas utilities. When it sealed the deal in late 2023, CEO Greg Ebel said, “These acquisitions further diversify our business, enhance the stable cash flow profile of our assets, and strengthen our long-term dividend growth profile.”

The transaction will increase its earnings from stable natural gas utilities from 12% to 22% of its total. The company partly funded that deal by selling Aux Sable, which operates extraction and fractionation facilities for natural gas liquids.

Enbridge also has a strong investment-grade balance sheet and a conservative dividend payout ratio. It has billions of dollars in annual investment capacity after paying its dividend (which yields an attractive 7%).

That gives it the flexibility to fund its roughly $18 billion backlog of secured capital projects. It also has the capacity to make opportunistic acquisitions and approve more expansion projects.

The company’s secured growth drivers and initiatives to reduce costs and optimize its assets should grow its cash flow per share by around 3% annually through 2026 and 5% per year after that. Its visible earnings growth and strong balance sheet suggest it should have no trouble increasing its dividend, which it has done for 29 straight years.

That high-yielding and steadily rising payout supplies a very strong base return, providing investors with some shelter amid a future financial storm.

68 consecutive years of dividend increases, and counting

Neha Chamaria(Northwest Natural Holding): If you haven’t heard about Northwest Natural, the company’s dividend track record will stun you. Utilities often pay regular and stable dividends, and Northwest Natural is no different.

What sets it apart, though, is that Northwest Natural has increased its dividend every year for the last 68 consecutive years. That’s one of the longest streaks among Dividend Kings.

Northwest Natural provides natural gas and water services through its subsidiaries, including NW Natural, NW Natural Water, and NW Natural Renewables.

NW Natural provides natural gas to nearly two million people in Oregon and southwest Washington State, while NW Natural Water serves around 180,000 people. As is typical with regulated utilities, Northwest Natural can earn and generate stable earnings and cash flows, which is why it not only can afford to pay a regular dividend but also grow it with time.

It’s a great dividend stock for several reasons. The utility expects to invest $1.4 billion to $1.6 billion in its natural gas business over the next five years, which could boost its rate base by 5% to 7%.

Management believes this investment, combined with its spending on water infrastructure, could boost its earnings per share by a compound annual growth rate of 4% to 6% between 2022 and 2027. Since the company prioritizes dividend growth, earnings growth should mean bigger dividends for shareholders year after year.

Its 68-year streak, of course, is the biggest testimony to how reliable Northwest Natural’s dividends are. With its high yield of 4.8%, this is the kind of stock that will let you sleep even during bear markets.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $657,306!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Matt DiLallo has positions in Enbridge. Neha Chamaria has no position in any of the stocks mentioned. Reuben Gregg Brewer has positions in Enbridge and WEC Energy Group. The Motley Fool has positions in and recommends Enbridge. The Motley Fool has a disclosure policy.