Systems reports financial results after the close of trading on Thursday, but the stock is more likely to move on any tidbits the company shares about its push into artificial intelligence—and the status of its pending $20 billion acquisition of the collaborative design software company Figma.

STOCKHOLM–Sweden’s H&M Hennes & Mauritz on Thursday reported fiscal second-quarter sales that were slightly below expectations.

The fashion retailer said sales for the quarter ended May 31 increased by 6% on year to 57.62 billion Swedish kronor ($5.38 billion), while net sales in local currencies were “flattish”.

Bud Light as the nation’s top-selling beer, punctuating the impact of a boycott that followed the brand’s controversial promotion by a transgender activist.

Shares of Oracle Corp. rose after hours Monday after the IT and cloud infrastructure provider reported fiscal fourth-quarter results that topped expectations, helped by a jump in cloud revenue that executives said positioned the company well for the year to come.

The company reported fourth-quarter net income of $3.32 billion, or $1.19 a share, compared with $3.19 billion, or $1.16 a share, in the same quarter last year. Revenue rose 17% to $13.84 billion, compared with $11.84 billion in the prior-year quarter.

Excluding stock-based compensation, amortization and other charges, Oracle earned $1.67 a share, compared with $1.54 a year ago.

Analysts polled by FactSet expected Oracle to report adjusted earnings per share of $1.58, on revenue of $13.74 billion.

Oracle also declared a quarterly cash dividend of 40 cents a share. Revenue from Oracle’s cloud software and infrastructure services rose 54% during the quarter.

“So, both of our two strategic cloud businesses are getting bigger — and growing faster,” Chief Executive Safra Catz said in a statement. “That bodes well for another strong year in FY24.”

Oracle shares ORCL, +5.99%

were up 4.8% after hours on Monday. The stock closed regular trading up 5.8% to $116.43, putting it at a record high.

Earlier on Monday, Wolfe Research upgraded Oracle, saying its cloud business could double its market share by 2025 “on the backs of architectural advantages, partnerships” and generative AI.

UBS analysts also said they expected Oracle to highlight its cloud-AI partnership with chip maker Nvidia Corp. NVDA, +1.84%,

which analysts say is set to benefit from more AI development. Those expectations were confirmed on Monday, when Oracle management name-checked Nvidia in its earnings release.

“Nvidia themselves are using our clusters, including one with more than 4,000 GPUs, for their AI infrastructure,” Larry Ellison, Oracle’s co-founder and chief technology officer, said in the release.

Shares of Oracle have marched 81.7% higher over the past 12 months. The S&P 500 Index SPX, +0.93%

has risen 15.7% over that period.

Shares of Tesla Inc. rose Thursday to a 10th straight gain, as data out of China showed that the electric vehicle giant sold more cars in May than the previous month.

The stock TSLA, +4.58%

surged 4.6% to $234.86, for its highest close since Oct. 6, when it closed at $238.13, and its largest one-day percentage increase since May 30, when it rose 4.14%. Shares continued rising around 3% in after-hours trading Thursday.

It has charged up 27.3% over the past 10 days, its longest win streak since the 11-day streak that ended Jan. 8, 2021.

The China Passenger Car Association reported overnight that May retail sales of new-energy vehicles, which includes electric and plug-in hybrids, jumped 60.9% from a year ago to 580,000 vehicles, or 33.3% of the total passenger cars sold of 1.74 million, according to a Dow Jones Newswires report.

Meanwhile, shares of other China-based EV makers were mixed, as Nio Inc.’s stock NIO, +0.39%

dropped 1.5%, but Xpeng Inc. shares XPEV, +0.95%

climbed 0.9% and Li Auto Inc.’s stock LI, +0.66%

tacked on 0.7%.

Tesla generated $4.89 billion in sales from China during the first quarter, or 21.0% of total sales. In 2022, the company’s China sales totaled $18.15 billion, or 22.2% of total sales for the year.

Separately, the Associated Press reported that late Wednesday that Tesla may face a class-action lawsuit after 240 Black factory workers described racism and discrimination at the company’s plant in the San Francisco Bay Area.

Tesla’s stock has soared 91% year to date, while the Global X Autonomous and Electric Vehicles exchange-traded fund DRIV, +0.77%

has run up 25.4% and the S&P 500 index SPX, +0.62%

has advanced 11.6%.

Target Corp.’s stock is up 0.1% Friday after snapping its longest losing streak in 23 years amid an anti-LGBTQ+ backlash against the retail giant.

The stock ended Thursday’s session up 0.2% to snap the losing streak. Target TGT, +1.57%

shares had ended Wednesday’s session down 2.2%, marking their ninth consecutive decline, and the stock’s longest losing streak since an 11-day stretch that ended Feb. 24, 2000, according to Dow Jones data. Wednesday also marked the stock’s lowest close since Aug. 11, 2020.

Bud Light’s recent troubles should worsen in the summer, to the benefit of its competition’s brands, enough to turn Roth MKM analyst Bill Kirk bullish on the stocks of Constellation Brands Inc. and Boston Beer Co. Inc.

Kirk raised on Tuesday his rating on Modelo, Corona, Pacifico beer parent Constellation Brands to buy, after being at neutral since January 2021, while boosting his stock price target to $270 from $216.

Kirk said a lot of the market share Anheuser-Busch InBev SA’s Bud Light lost, amid backlash from the beer brand’s partnership with trans influencer Dylan Mulvaney, went to other premium light products, but he expects that to shift to Constellation’s favor.

“As the weather warms, we expect the share gains for Modelo Especial and Corona to accelerate,” Kirk wrote in a note to clients.

Constellation Brands’ stock STZ, +1.79%

rose 1.5% in afternoon trading Tuesday toward the highest close since Dec. 12, 2022, while Anheuser-Busch shares BUD, -4.71%

slumped 4.5% toward the lowest close since Nov. 10.

He noted that weekly scanner data has shown that Constellation’s beer portfolio outperformed the broader beer market by seven percentage points in early 2023, and that outperformance improved to 10 percentage points at the beginning of Bud Light’s market-share losses in April.

“With temperatures warming and substitutability with Bud Light increasing, recent weeks have seen 13 [percentage points] of outperformance,” Kirk wrote. “This trend should continue as Bud Light [declines/peak] over summer holidays.”

For Samuel Adams, Truly, Twisted Tea parent Boston Beer, Kirk raised his rating to buy, after being at neutral for at least the past three years. He raised his stock price target to $386 from $274.

Boston Beer’s stock SAM, +5.37%

jumped 6.8% toward the highest close since Feb. 15.

Earlier this year, Kirk was concerned that Truly hard seltzer’s weakness continued, offsetting Twisted Tea’s success, and that gross margins weren’t improving even after moving more production in-house.

“Now, we believe seltzer and Truly will benefit in the summer from Bud Light share losses (occasion overlap increases with warmer weather) and gross margin lift from production shift will be realized in 2Q (given inventory days timing),” Kirk wrote.

He believes that will shift investor focus away from Truly’s weakness and toward Boston Beer’s brands that are growing.

And while Wall Street expects the trends Boston Beer saw in the first quarter to continue throughout 2023, Kirk now believes the company will beat expectations for shipments and depletions, and sees opportunities for margins to also beat forecasts.

“While we had written at 1Q that the ‘timing of upside surprises remains unclear,’ we now believe the timing is Summer 2023,” Kirk wrote.

Constellation Brands’ stock has gained 5.7% over the past three months and Boston Beer shares have advanced 4.8%, while Anheuser-Busch’s stock has dropped 10.1% and the S&P 500 index SPX, +0.00%

has gained 5.9%.

Atmus Filtration Technologies Inc.’s stock soared 14% Friday in its trading debut, after the Cummins Inc. spinoff priced its initial public offering in the middle of its proposed price range.

The Nashville, Tenn.-based company sold 14.1 million shares priced at $19.50 each to raise $275 million. With 83.3 million shares to be outstanding after the deal, the company’s valuation is $1.6 billion.

The stock ATMU, +11.90%

is trading on the New York Stock Exchange under the ticker ATMU. Goldman Sachs and JPMorgan Chase were lead book-running managers on the deal, with 10 other banks acting as co-managers.

Although the company is issuing primary shares, Atmus will not receive any of the IPO proceeds; all of the proceeds will go to debt-for-equity exchange parties, namely underwriters Goldman Sachs and JPMorgan, and will indirectly pay down parent Cummins’ CMI, +1.03%

debt, according to the filing documents.

Atmus makes products for on-highway commercial vehicles and off-highway agriculture, construction, mining and power-generation vehicles and equipment, mostly under the Fleetguard brand. The company had pro forma net income of $34.9 million in the first quarter on sales of $418.6 million.

About 16% of its 2022 sales went to original-equipment manufacturers, where its filters are used for new vehicles and equipment, and about 84% were aftermarket sales.

The company was created by Cummins, a maker of diesel and natural-gas engines, in 1958.

The IPO comes in a thin year for deals. There have been just 44 IPOs this year to raise $7.3 billion in proceeds, according to Renaissance Capital, a provider of IPO exchange-traded funds and institutional research.

That’s up 29.4% from the same period in 2022, when deal flow slowed to its lightest in decades.

“Deal flow started at a decent pace but failed to pick back up after the February lull, as hawkish signals from the Fed, renewed recession fears, and turmoil within the banking industry caused a spike in volatility,” Renaissance wrote in April commentary.

The biggest deal of the year to date was that of Kenvue Inc. KVUE, -0.11%,

a spinoff from Johnson & Johnson JNJ, +0.14%,

which is parent to a number of household brands, including Tylenol, Band-Aid, Listerine and Benadryl.

Chip stocks experienced a significant surge Thursday in the wake of Nvidia Corp.’s upbeat commentary on AI-fueled demand — with one notable exception.

Shares of Intel Corp. INTC, -5.52%

were down more than 5% in afternoon trading Thursday, leading Dow Jones Industrial Average DJIA, -0.11%

laggards by a wide margin, on a day when Nvidia Corp.’s NVDA, +24.37%

stock was up 26% and the PHLX Semiconductor Index SOX, +6.81%

was ahead 6%.

Nvidia delivered a stratospheric beat on its quarterly revenue outlook Wednesday afternoon, with executives discussing how spending on artificial intelligence is already starting to drive sizable financial benefits for the company. That discussion has Wall Street thinking that many other chip makers will also be able to capitalize on the same wave of interest in the hot technology — shares of Monolithic Power Systems Inc. MPWR, +17.46%,

Advanced Micro Devices Inc. AMD, +11.16%

and Taiwan Semiconductor Manufacturing Co. 2330, +3.43%

TSM, +12.00%

all joined Nvidia in gaining by double-digit percentages in Thursday’s session.

Intel, though, was a key outlier. Nvidia’s commentary seemed to make investors more worried that Intel is behind the curve on what some see as a massive technological revolution.

Intel’s revenue and profits from central processing units look “even more at risk” after Nvidia’s report, while Intel doesn’t have “any real” competitive position in graphics processing units or generative-AI compute, wrote Mizuho’s Jordan Klein, a desk-based analyst associated with the company’s sales team and not its research arm.

Nvidia’s earnings call “will reinforce the negative view that [Intel] and all their CPU share is a major loser and share donor to GPU, ASICs and lower power ARM design chips on the way,” Klein added.

While Nvidia GPUs typically would run alongside CPUs from either Intel or AMD, Nvidia has been making inroads in CPUs. Chief Financial Officer Colette Kress said on Nvidia’s call that the company has seen “growing momentum for Grace with both CPU-only and CPU-GPU opportunities across AI and cloud and supercomputing applications.”

Nvidia is perceived to be ahead of the pack in AI-related computing technology, but AMD is at least in a better position than Intel, with more of a one-stop shop across CPUs and GPUs. That’s likely why AMD’s stock is riding on Nvidia’s coattails Thursday, up more than 10% in afternoon action.

AMD is “the only other real GPU supplier,” Klein wrote, though the company “could lose CPU spend in process and [has] a far way to go to catch [Nvidia].”

In his view, it “will take some time for more advanced and higher performance GPU and software platform to ramp and really drive upside potential” at AMD. “But seeing how fast and much [Nvidia] benefited, few will want to wait and see how long that takes for AMD.”

A more clear beneficiary, he noted, is Taiwan Semiconductor, whose stock was up more than 12% Thursday. You “cannot get any of these GPUs, inference, etc. without their fabs,” according to Klein.

As for Intel, Klein likes that the company is approaching a second-quarter bottom and positioned to capitalize on a personal-computer refresh, but he said its stock “feels totally stuck at best and could get shorted.”

“‘Icahn’s favorite Wall Street saying: “If you want a friend, get a dog.” Over his storied career, Icahn has made many enemies. I don’t know that he has any real friends. He could use one here.’”

— Bill Ackman, Pershing Square Capital Management

That was billionaire hedge-fund manager Bill Ackman, founder and chief executive of Pershing Square Capital Management, resurrecting his longstanding feud with billionaire activist investor Carl Icahn in a tweet Wednesday.

Ackman was referencing the fallout from the recent report by short-selling firm Hindenburg Research that accused Icahn’s publicly traded investment vehicle, Icahn Enterprise Partners LP IEP, -13.83%,

of inflating asset values and causing his company to trade at a large premium. The report from May 2 has cost IEP about $10.9 billion in lost market cap, after the stock tumbled another 21% on Thursday.

Ackman said he is neither long or short IEP but merely “watching from a distance.”

But he seemed to agree with Hindenburg’s founder and CEO, Nate Anderson, who questioned margin loans extended to Icahn using his roughly 85% stake in IEP as collateral. Icahn has not disclosed the terms of those loans although he recently told the Financial Times that he used the money to make additional investments outside of his publicly traded vehicle.

“Over the years I have made a great deal of money with money,” he was quoted as having said. “I like to have a war chest, and doing that gave me more of a war chest.”

Ackman said the margin lender or lenders “must be extremely concerned with the situation,” particularly after IEP has disclosed a federal investigation of its business and corporate governance.

For his part, Icahn has called Hindenburg’s analysis “misleading and self-serving” and said it was designed solely to hurt long-term IEP shareholders.

Ackman compared the situation to that of failed investment fund Archegos, “where the swap counterparties were comforted by each having relatively smaller exposures to the situation.”

“The problem is that multiple lenders make for a more chaotic situation. All it takes is for one lender to break ranks and liquidate shares or attempt to hedge, before the house comes falling down. Here, the patsy is the last lender to liquidate.”

Ackman also expressed his surprise that Icahn has not disclosed the margin-loan terms, or even said who provided them. “My understanding of 13D SEC rules is that they require disclosure of sources of financing and even copies of financing agreements, although many investors ignore these requirements.”

Ackman also questioned how IEP’s large dividend yield is feasible, as it’s not supported by operating cash flows.

“The yield is generated by returning capital to outside shareholders, which is in turn funded by the company selling stock to investors,” said Ackman.

Icahn’s problem now is that his system has been outed by the short seller, Ackman wrote.

“Transparency is not the friend of $IEP having caused a more than 50% decline in the shares, which has caused Icahn to post more shares, now more than 65% of his holdings,” he said in the tweet.

The bad blood between Icahn and Ackman goes back to a business dispute the two had over a 2003 deal involving Hallwood Realty. The litigation between them went on for years.

But their animosity for one another hit a crescendo in 2013, when Bill Ackman publicly waged a $1 billion short-selling campaign against Herbalife. Sensing weakness, Icahn took a long position in Herbalife’s stock HLF, -5.21%

and helped deal Ackman significant losses on his bet over time.

The two claimed they had made up in 2014, sharing a stage at a conference broadcast by CNBC.

Ackman had previously had taken a soft shot at Icahn over the Hindenburg report, saying there was a “karmic quality” to it. But now their battle of Wall Street titans appears to be back in full force.

Nvidia Corp. headed toward market-capitalization gains of nearly $200 billion in after-hours trading Wednesday, which could put the chip maker within sight of becoming only the seventh U.S. company to top a valuation of $1 trillion.

Nvidia ended Wednesday’s session with a market cap — the total value of all shares in existence — of roughly $754.3 billion, according to FactSet. A 25% increase would add nearly $189 billion to that total, putting the company within striking distance of $1 trillion. Only six U.S. companies have ever attained a $1 trillion market cap: Apple Inc. AAPL, +0.16%

and Microsoft Corp. MSFT, -0.45%

are currently worth more than $2 trillion apiece; Google parent Alphabet Inc. GOOGL, -1.35%

and Amazon.com Inc. AMZN, +1.53%

have valuation of more than $1 trillion; and Facebook parent Meta Platforms Inc. META, +1.00%

and Tesla Inc. TSLA, -1.54%

have both touched the $1 trillion plateau previously.

Nvidia’s market cap was ahead of both Meta and Tesla as of Wednesday’s close, with both worth less than $650 billion, showing the potential fleeting nature of such a valuation. Nvidia’s record market cap is $834.4 billion, established on Nov. 29. 2021, according to Dow Jones Market Data.

If Nvidia’s gains hold through Thursday’s trading session, the company could challenge for the largest one-day market-cap gain in history. The biggest currently on record was Amazon’s $191.2 billion increase on Feb. 4, 2022, according to Dow Jones Market Data, followed closely by a $190.9 billion gain by Apple on Nov. 10, 2022. Nvidia also stands to gain more than rival Advanced Micro Devices Inc. AMD, +0.14%

is worth in total — AMD ended Wednesday’s session with a market cap of $174.4 billion.

Nvidia is closing in on the rare $1 trillion plateau because of huge gains in its stock this year, as hopes and hype about generative AI have flooded the tech sector. After OpenAI debuted its ChatGPT AI offering, and investor Microsoft quickly integrated the chatbot into many of its services, expectations for the technology have exploded.

Despite the hype, most companies have avoided providing hard figures for revenue gains expected from AI. Nvidia’s fiscal second-quarter forecast — which calls for roughly $11 billion in sales, nearly 33% higher than Nvidia’s previous quarterly record of $8.28 billion — could be seen as the first sign of a wave of fresh spending coursing through the tech sector.

Other companies have indicated that they will be forced to spend to develop their technology before reaping large financial rewards from it. Microsoft, for example, disclosed to investors last month that capital expenditures are increasing as it builds AI capabilities into its Azure cloud-computing platform — spending that is largely going toward Nvidia.

That is a rather typical path for large jumps in tech spending: Companies that make the necessary hardware see gains before the companies that use that gear can develop offerings that take advantage of it. Other gear makers joined Nvidia in the sharp move higher in after-hours trading Wednesday, including AMD, which gained more than 10%; chip maker Marvell Technology Inc. MRVL, -1.31%,

which increased more than 5%; and networking specialist Arista Networks Inc. ANET, +0.53%,

which added about 5%.

Alphabet and Microsoft stocks both increased around 2% in after-hours trading, and software companies that have made AI a core part of their offerings also saw gains. Palantir Technologies Inc. PLTR, -3.24%

and C3.ai Inc. AI, +2.54%

shares both increased more than 8%, for example.

Nvidia Corp. executives predicted record revenue well beyond anything the company has experienced Wednesday, pushing shares toward all-time highs, as margins improve with AI-driven data-center sales.

Nvidia NVDA, -0.49%

guided for second-quarter revenue of $11 billion, plus or minus 2%; the chip maker has never before reported quarterly revenue higher than $8.29 billion, which it hit in the fiscal first quarter a year ago. Analysts on average were expecting $7.17 billion, according to FactSet, a gain from the $6.7 billion in sales Nvidia put up in the fiscal second quarter last year.

On the conference call with analysts, Huang said the simple way to think about it is that the world has “a trillion dollars of data center installed and it used to be 100% CPU,” or central processing units, as opposed to Nvidia’s graphics processors that data centers and AI models have embraced in recent years. And while the world’s data-center budget is strapped, at the same time larger and larger AI models require more and more computing power, he said.

“The easiest way to think about that is over the next four or five, 10 years, most of that trillion dollars, and compensating adjusting for all the growth in data center still, it will be largely generative AI,” Huang said.

“What happened is, when generative AI came along, it triggered a killer app for this computing platform that’s been in preparation for some time,” he added.

The company forecast adjusted gross margins of 70% for the second quarter, after reporting 66.8% for the first quarter, not only as higher data-center margins counter the deficit in gaming, but as Nvidia Chief Financial Officer Colette Kress said on the call: ” We believe the channel inventory correction is behind us.”

Shares soared more than 25% in after-hours trading, following a 0.5% decline in the regular session to $305.38. Nvidia’s record closing price is $333.76 and the all-time intraday high is $346.47, according to FactSet data. After-hours “prices” topped both of those marks, reaching more than 14% beyond all-time highs for the regular session, as shares registered as high as $395, according to FactSet. The last time Nvidia shares rallied as much in a single session was Nov. 11, 2016, when shares surged 29.8% after the company reported that profit more than doubled.

Meanwhile, shares of rival Advanced Micro Devices Inc. AMD, +0.14%

rallied 6% after hours.

Nvidia did not provide full-year guidance, but Chief Executive Jensen Huang has been effusive in his predictions that increased focus on AI from Big Tech partners such as Microsoft Corp. MSFT, -0.45%

and Alphabet Inc. GOOGL, -1.35% GOOG, -1.34%

will lead to revenue gains in the near future. Speaking to the media at Nvidia’s developers conference in March, he said that generative AI has only accounted for a “tiny, tiny, tiny” single-digit percentage of revenue over the past 12 months, but predicted that in the next year, revenue from generative AI will grow to be “quite large — exactly how large, it’s hard to say.”

Nvidia reported fiscal first-quarter earnings of $2.04 billion, or 82 cents a share, on sales of $7.19 billion, a decline from $8.29 billion a year ago but well ahead of expectations. After adjusting for stock compensation and other effects, the chip maker reported earnings of $1.09 a share, a decline from $1.36 a share a year ago. Analysts on average were expecting adjusted earnings of 92 cents a share on sales of $6.53 billion, according to FactSet.

Gaming sales for the first quarter fell 38% to $2.24 billion, while data-center sales at Nvidia rose 14% to a record $4.28 billion, “led by growing demand for generative AI and large language models using GPUs based on our Nvidia Hopper and Ampere architectures.”

“The revenue growth reflects strong demand from large consumer internet companies and cloud service providers,” the company said in a statement. “Enterprise demand for GPU platforms was strong, although general purpose networking solutions declined both sequentially and from a year ago.”

Analysts had expected gaming sales of $1.97 billion — nearly half of last year’s $3.62 billion — and data-center sales of $3.9 billion, a 4% increase from a year ago. Auto chip sales soared 114% to $296 million from a year ago.

Nvidia’s profit and sales have declined in recent quarters as the company deals with oversupply in the market, a result of pandemic-era shortages flipping to a glut after demand for personal computers and gaming gear waned. Analysts expect that trend to end with this report, however, as demand for gear that can power artificial intelligence kicks into higher gear amid a bevy of promises from tech companies about the power of generative AI.

PacWest Bancorp.’s stock jumped 3% premarket Monday, after the bank announced asset sales that would allow it to focus on its core community banking business.

The regional bank PACW, -1.88%

said it has entered an agreement to sell a portfolio of 74 real estate construction loans with a principal balance of about $2.6 billion to a unit of real-estate investment company Kennedy Wilson Holdings.

“Kennedy Wilson or its designees will also assume all remaining future funding obligations under the acquired loans of approximately $2.7 billion,” PacWest said in a regulatory filing.

The bank has also agreed to sell an additional six real estate construction loans to Kennedy Wilson with a principal balance of about $363 million.

The sale of the loans is subject to Kennedy Wilson’s satisfactory due diligence. The company will place $20 million into a third-party escrow account that will be refundable.

The deal is expected to close in several tranches in the second and third quarters. “There can be no assurance that the transaction will be completed in part or at all,” said the filing.

PacWest shares are down 75% in the year to date, after being caught up in the regional-bank stock rout that followed the collapse of Silicon Valley Bank in March.

The bank said it lost 9.5% of deposits during the week ending May 5 amid market volatility following JPMorgan’s JPM, -0.23%

rescue of First Republic Bank.

Shares of Target Corp. seesawed to a gain early Wednesday, after the discount retailer reported fiscal first-quarter results that beat expectations and reiterated its full-year outlook, but provided a downbeat second-quarter profit view due to “softening sales trends.”

Net income for the quarter to April 29 fell to $950 million, or $2.05 a share, from $1.01 billion, or $2.16 a share, in the same period a year ago. Excluding nonrecurring items, adjusted earnings per share fell to $2.05 from $2.19 but beat the FactSet consensus of $1.77.

Total revenue increased 0.6% to $25.32 billion, above the FactSet consensus of $25.26 billion, while same-store sales grew 0.7% to exceed the FactSet consensus for a 0.2% rise, as traffic rose 0.9%.

The stock rose 0.9% in premarket trading, but has swung from a loss of as much as 3.6% to a gain of as much as 2.4% after the results were reported.

“We came into the year clear-eyed about the challenges consumers are facing, and we were determined to build on the trust we’ve established with our guests,” said Chief Executive Officer Brian Cornell. “It’s required agility and the ability to flex across our multi-category portfolio as we lean into value and the product categories our guests need most right now.”

Cost of sales declined 0.4% to $18.39 billion, as gross margin improved to 27.4% from 26.7%.

The value of inventory fell 6.5% from the sequential fourth quarter, and dropped 16.4% from a year ago, to $12.62 billion as of April 29.

“[W]e now expect shrink will reduce this year’s profitability by more than $500 million compared with last year,” said CEO Cornell. “While there are many potential sources of inventory shrink, theft and organized retail crime are increasingly important drivers of the issue.

Looking ahead, Target said it was planning for a wide range of sales outcomes, given “softening sales trends” in the first quarter.

For the second quarter, the company expects same-store sales to be down in the low-single digit percentage range, compared with the FactSet consensus for a 0.1% increase. And adjusted EPS for the current quarter is expected to be $1.30 to $1.70, below expectations of $1.95.

For the full year, Target reiterated its guidance for same-store sales growth of 0.7% and for adjusted EPS of $7.75 to $8.75. That compares with the FactSet consensus for same-store sales growth of 0.6% and for adjusted EPS of $8.36.

The stock has gained 5.3% year to date through Tuesday, while the Consumer Discretionary Select Sector SPDR exchange-traded fund XLY, -0.41%

has run up 14.1% and the S&P 500 index SPX, -0.64%

has advanced 7.0%.

Eli Lilly & Co.’s market cap neared Johnson & Johnson’s market cap on Friday, as the stock has benefited from a slew of positive data in trials for key treatments.

Earlier Friday, Lilly stock LLY, +0.00%

was on track to close with a greater market capitalization than J&J JNJ, -0.13%,

which would have marked the first time since 1997. Lilly stock ended flat, however, for the session at $434.43.

The stock has been steadily rising since the release of positive data from a trial of a treatment for Alzheimer’s disease in early May, showing significant slowing of cognitive and function decline in patients with early symptomatic Alzheimer’s disease.

Nearly half, or 7% of participants, had no clinical progression at one year, compared to 29% on placebo. The drug, called donanemab slowed clinical decline by 35% compared to a placebo and resulted in 40% less decline in the ability to perform activities of daily living, including managing finances, driving, engaging in hobbies and conversing about current events, the company said.

The company is planning to proceed with global regulatory submissions as quickly as possible and expects to make a submission to the U.S. Food and Drug Administration this quarter.

That’s not all. In April, Eli Lilly released data on its new obesity drug tirzepatide that showed patients in a trial losing up to 15.7% of their body weight, or about 34.4 pounds.

More than 80% of people taking tirzepatide lost at least 5% of their body weight, the company said, compared with about 30% of those taking a placebo.

The degree of average weight reduction seen in the trial “has not been previously achieved” in similar Phase 3 trials, Dr. Jeff Emmick, senior vice president for product development at Lilly, said in a statement.

Source: FactSet, Dow Jones Market Data

The company is planning regulatory submissions for that drug later this year. Tirzepatide was approved by the FDA last year as Mounjaro, a treatment for Type 2 diabetes.

Lilly has several other pipeline prospects, including lebrikizumab, a treatment for atopic dermatitis; mirikizumab for ulcerative colitis; empagliflozin, a treatment for chronic kidney disease; and pirtobrutinib for relapsed/refractory mantle cell lymphoma.

Lilly’s stock is up about 20% in the year to date and up 50% in the past 12 months.

Johnson & Johnson’s stock, meanwhile, has fallen 9% in the year to date and is down roughly the same over the past 12 months.

The company swung to a first-quarter loss as it booked a multibillion-dollar charge to settle lawsuits stemming from its talc-containing powders.

J&J booked a $6.9 billion one-time litigation charge relating to lawsuits filed by people alleging the company’s talc-containing powders caused cancers, asbestos poisoning and other illnesses. The company has offered to pay at least $8.9 billion to settle the suits, and remove an overhang on the stock.

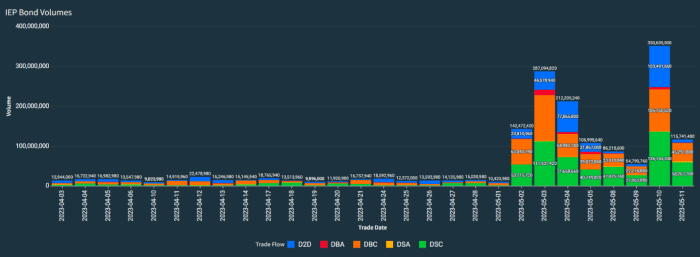

Icahn Enterprises LP’s stock was trading down 0.7% Thursday, after short seller Hindenburg Research intensified his bearish bet on Carl Icahn’s investing arm, and said he’s now taking aim at its bonds.

Hindenburg, run by Nate Anderson, said the latest disclosures made Wednesday by IEP raised more questions about Icahn’s personal margin loans, or debt, from the company as well as portfolio losses at IEP. The short seller also said disclosures, intended to counter Hindenburg’s May 2 report, failed to address the issues raised.

The original report raised questions about asset valuations and Icahn’s own borrowing from the company using his units as collateral.

Hindenburg Research, which typically aims to profit from the decline in value of the shares of companies that it writes negative reports about, kicked off such a bet against Icahn Enterprise earlier this month but has now also set its sights on the company’s debt.

“As noted in our earlier report, Icahn had not disclosed “basic metrics around his margin loans like loan to value (LTV), maintenance thresholds, principal amount, or interest rates.” This is still the case,” said Hindenburg.

IEP has not said why Icahn had borrowed against his holdings. The company didn’t respond to a request for comment on Thursday’s report.

On Wednesday, IEP disclosed a federal probe into its corporate governance and other issues. It is unclear if that investigation by the Southern District of New York is related to Hindenburg’s report and allegations, but the news put further pressure on the stock.

The bonds, which have been more active than usual since the first report, took another leg down on Thursday, as the attached charts from market-data company BondCliQ show, as Hindenburg said it has taken a short position in them.

The longest-dated bonds, the 4.375% notes that mature in February of 2029, were trading at around 75 cents on the dollar, as of midmorning.

On Wednesday, IEP IEP, -1.77%

said that pledge had increased to 202 million units, which Hindenburg estimates was valued at $6.5 billion as of Wednesday’s close, based on his calculations.

The battle between the iconic activist investor and the short seller has clobbered IEP’s stock, which has fallen 39% in the month to date at a cost of more than $6 billion of market cap.

IEP posted an unexpected loss on Wednesday of $270 million, or 75 cents per depositary unit, for the first quarter, after income of $323 million, or $1.06 a unit, in the year-earlier period. The FactSet consensus was for income of 19 cents.

Revenue fell to $2.758 billion from $2.968 billion a year ago, ahead of the $2.559 billion FactSet consensus. Analysts on its conference call didn’t pose any question of executives who briefly outlined the quarterly numbers.

The company on Wednesday also issued a rebuttal of the May 2 report from Hindenburg and said it would “take all appropriate steps to protect our unit holders and fight back.”

Icahn acknowledged that the investment segment has underperformed in recent years, which he blamed on its bearish view of the market and large net short position, which it has now scaled back.

IEP offers exposure to Icahn’s personal portfolio of public and private companies, including petroleum refineries, car-parts makers, food-packaging companies and real estate. Its unit holders are mostly individual investors, which means the market-cap loss prompted by the report has hurt those individual investors, said Icahn.

Palantir Technologies Inc. delivered a surprise profit for the second quarter in a row Monday, while also topping revenue expectations, sending shares more than 20% higher in after-hours trading.

The software company reported first-quarter net income of $17 million, or 1 cent a share, whereas Palantir PLTR posted a loss of $101 million, or 5 cents a share, in the year-earlier quarter. Analysts tracked by FactSet were expecting a loss of a penny a share on a GAAP basis. The stock closed with a 4.7% gain at $7.76 in Monday’s…