[ad_1]

Ben Harburg of Core Values Alpha says deflation is so entrenched in China that “numbers don’t show the amount of consumption that is truly going on.”

[ad_2]

[ad_1]

Ben Harburg of Core Values Alpha says deflation is so entrenched in China that “numbers don’t show the amount of consumption that is truly going on.”

[ad_2]

[ad_1]

Market optimism over the potential for interest rate cuts next year is dangerously overdone, according to former FDIC Chair Sheila Bair.

Bair, who ran the FDIC during the 2008 financial crisis, suggests Federal Reserve Chair Jerome Powell was irresponsibly dovish at last week’s policy meeting by creating “irrational exuberance” among investors.

“The focus still needs to be on inflation,” Bair told CNBC’s “Fast Money” on Thursday. “There’s a long way to go on this fight. I do worry they’re [the Fed] blinking a bit and now trying to pivot and worry about recession, when I don’t see any of that risk in the data so far.”

After holding rates steady Wednesday for the third time in a row, the Fed set an expectation for at least three rate cuts next year totaling 75 basis points. And the markets ran with it.

The Dow hit all-time highs in the final three days of last week. The blue-chip index is on its longest weekly win streak since 2019 while the S&P 500 is on its longest weekly win streak since 2017. It’s now 115% above its Covid-19 pandemic low.

Bair believes the market’s bullish reaction to the Fed is on borrowed time.

“This is a mistake. I think they need to keep their eye on the inflation ball and tame the market, not reinforce it with this … dovish dot plot,” Bair said. “My concern is the prospect of the significant lowering of rates in 2024.”

Bair still sees prices for services and rental housing as serious sticky spots. Plus, she worries that deficit spending, trade restrictions and an aging population will also create meaningful inflation pressures.

“[Rates] should stay put. We’ve got good trend lines. We need to be patient and watch and see how this plays out,” Bair said.

[ad_2]

[ad_1]

China’s consumer prices fell at the steepest pace in three years while producer costs dropped even further into negative territory, underscoring the challenges facing the economic recovery.

The consumer price index fell 0.5% last month from a year earlier, the national statistics bureau said in a statement Saturday. That’s the biggest drop since November 2020 and is weaker than the 0.2% drop projected by economists in a Bloomberg survey.

Producer prices declined 3%, compared with a forecast of a 2.8% fall. Factory-gate costs have been mired in deflation territory for 14 consecutive months.

China has struggled with falling prices much of this year, contrasting with many other parts of the world where central banks are focused on taming inflation instead. Bloomberg Economics expects deflationary risks to persist into 2024, as there aren’t enough catalysts to counter the housing slump, which has suppressed demand and prices.

Deflationary pressures have increased because of weak domestic demand, said Zhang Zhiwei, chief economist at Pinpoint Asset Management Ltd. “This highlights the importance of more supportive fiscal policy.”

Deflation is dangerous for China because it can lead to a downward spiral of economic activity. Consumers may hold off purchases on expectations prices will keep falling, further weighing on overall consumption. Businesses might lower production and investment due to uncertain future demand.

Deflation can also make monetary policies to stimulate the economy less effective, as declining prices lower corporate income and make it more difficult for companies to service their debt. The central bank has sought to downplay the risks of deflation this year, with an adviser to the People’s Bank of China saying last month that those pressures are “temporary.”

Beijing recently turned to fiscal policy to spur domestic demand, unexpectedly increasing its budget deficit and encouraging banks to help local governments refinance debt at lower interest rates to help increase their spending capacity.

There are indications that fiscal support will strengthen in the coming year to help the recovery: China’s top leaders on Friday announced such policies will be stepped up “appropriately” and emphasized the importance of economic “progress,” suggesting next year’s growth goal may be ambitious.

But it has been difficult for additional government spending to offset declines in demand coming from other sectors. The value of new home sales among China’s 100 biggest developers fell 29.6% on-year in November.

Exports also remain weak, rising just 0.5% last month, far below the pace seen in recent years. Economists have said it’s too early to call a bottom for growth, with some predicting further pressure on the economy in 2024 because of ongoing challenges from the property sector.

The weak CPI figures have been partly due to slumping pork prices. An ample supply of hogs and sluggish consumption have weighed on the market, prompting the government to take steps to support prices. The meat has a large share in China’s CPI basket due to its popularity among local diners.

The so-called core CPI, which strips out volatile food and energy costs, rose 0.6% on year in November, repeating the previous month’s performance.

China has set an annual inflation target of around 3% this year, which it is nearly certain to miss. Economists have mixed views on the outlook for 2024, with some arguing that consumer prices could grow at a pace of around 1% as sentiment improves, and others arguing deflation will persist into the first half.

Proactive fiscal stimulus will be a vital part of China’s policy objectives next year, according to Bruce Pang, chief economist for Greater China at Jones Lang LaSalle Inc. The measures will “have to strike a balance between juicing investment and consumption, and capping debt risks of local governments.”

— With assistance from Tom Hancock, Jasmine Ng, Jill Disis, and Yujing Liu

[ad_2]

Bloomberg

Source link

[ad_1]

Shaun Rein of China Market Research Group discusses his outlook on the Chinese economy and shares why he thinks it is unlikely to see the government implement a major stimulus program.

[ad_2]

[ad_1]

Tan Min Lan of UBS Global Wealth Management says structural changes have been positive drivers for the Japanese markets and discusses the sectors she finds attractive investment opportunities.

[ad_2]

[ad_1]

David Rosenberg honestly doesn’t want to be bearish on stocks or bash the Federal Reserve. The veteran market strategist will get no satisfaction if he’s right about Americans having to slog through recession and consequently endure deflation, job losses and a wallop to the stock market.

“As I play the role of economic detective, I can see the smoking gun,” says Rosenberg, a former chief North American economist at Merrill Lynch and now president of Toronto-based Rosenberg Research.

Who’s…

[ad_2]

[ad_1]

This is an opinion editorial by Ansel Lindner, an economist, author, investor, Bitcoin specialist and host of “Fed Watch.”

Ghost money has a long history but only recently became part of the bitcoin vernacular via premier eurodollar expert, and bitcoin skeptic, Jeff Snider, Chief Strategist at Atlas Financial. We’ve interviewed him twice for the Bitcoin Magazine podcast “Fed Watch” — you can listen here and here, where we talked about some of these topics.

In this post, I will define the concept of ghost money, discuss the eurodollar and bitcoin as ghost money, examine currency shortages and their role in monetary evolution, and finally, place bitcoin in its place among currencies.

Ghost money is an abstracted ideal currency unit, used primarily as a unit of account and medium of exchange, but whose store-of-value function is a derivative of a base money. Other terms for ghost money include: political money, quasi-money, imaginary money, moneta numeraria or money of account.

To many economic historians the most famous era of ghost money is the Bank of Amsterdam starting in the early 17th century. It was a full reserve bank, used double-entry bookkeeping (shared ledgers) for transactions, and redeemed balances at a fixed amount of silver. Ghost money existed on their books, and the money in their vaults.

The financial innovation of an abstracted ideal currency unit evolved because coins are never the same weight or fineness. Coins in circulation tended to get worn quickly, dented or clipped and even if the coins were in mint condition, sovereigns tended to debase the coins on a regular basis (by the year 1450, European coins only had 5% silver content). Ghost money is a currency abstraction based on a fixed measurement of a money (its store-of-value), but does not need to reference actual coins in circulation, just an official measurement.

To put it in terms Bitcoiners are familiar with, this layer of abstraction gave commodity money new security properties and payment features.

Security wise, ghost money avoids the problem of debasement to a degree (we could call this debasement resistance), because the unit-of-account is a fixed weight and fineness set by a bank, not the sovereign. For example, the Bank of Amsterdam set the guilder at 10.16 g fine silver in 1618. Coins in circulation at the time tended to differ widely, coming from all over Europe. There were even direct attacks on banks in the form of flooding the local economy with debased coins, as happened in the 1630s with the importation of coins of less silver content from Spanish Netherlands north to Amsterdam.

Ghost money also allows new features, like the ability to transact over long distances, in large sums, carrying only a letter, greatly reducing transaction costs. It also allowed longer-term bonds at lower interest rates because the unit-of-account is more stable. The pricing of shares (a new innovation at the time), also could be valued in stable currency units.

In general, ghost money leads to thinking of value in a stable abstract unit. This has far reaching effects that are hard to overstate when it comes to large long-term investments, like massive infrastructure projects, that just so happened to get going in the preindustrial era as well. Eventually, the thinking in stable abstract currency units would lead to all the financial and banking innovation we see today.

Ghost money is rightly thought of as a derivative to the money itself, one which replaced the insecure aspects of the physical coins, without getting rid of the underlying form of money. It would more properly be called “ghost currency,” because it is simply a stable derivative, an idealized currency, used for accounting.

Everything has a trade off, and ghost money is no exception. Abstracting the currency away provided debasement resistance from the sovereign, but it also enabled the banks to more easily create credit denominated in that idealized unit (fractional reserve lending), shifting the money printing task from sovereigns to banks. Expanding credit in the private sector according to market desires can lead to economic booms, but the trade off is the following bust.

In an article from Jeff Snider, he pairs the use of ghost money with the concept of monetary shortage to explain the rise of modern banking, and the beginning of the evolutionary process toward the current eurodollar financial system and even bitcoin.

“Any money-of-account [ghost money] alternative is the resourceful yet natural human response to these specific conditions.”

He sees ghost money as a natural market-driven practice, with a primary driving force being monetary shortage. Ghost money can add elasticity to the money supply as I stated above through credit expansion. He points to the 15th century’s Great Bullion Famine and the 1930’s Great Depression as two very important epochs in ghost money’s history. These were periods of inelasticity in the supply of currency, which incentivized efforts to search out new supplies via financial innovation (ghost money) or searching for new sources of money itself (silver and gold in the Age of Exploration and the eurodollar credit expansion in the 1950s and 1960s).

More than anything, though, what might have driven money-of-account forward to its preeminent position was something called the Great Bullion Famine. Just as the 20th century seemed to pivot in one direction then the other, from the deflationary money shortages of the Great Depression to decades later the overwhelming monetary changes underneath the Great Inflation, so, too, did Medieval economics suffer one to then pivot into its opposite.

Ghost money’s Golden Age, forgive the pun, coincided with the Bullion Famine. Quasi-money is often one solution to inelasticity; commercial pressures are not easily surrendered to something like a lack of medium of exchange. People want to do business because business, not money, is real wealth.

“The role of money, separated from any store of value desire, is nothing more than to facilitate such business[.]” — Jeff Snider

Snider frames ghost money as a market tool that happens to also provide a route to increasing the elasticity of money in times of currency shortage. In other words, when the supply of money does not expand at a sufficient rate, the ensuing economic difficulties will drive people to find ways to expand that money supply, and ghost money is a ready-made solution via fractional reserve.

Snider’s views put him squarely in the monetarist camp, along with Milton Friedman and others. They see in “the quantity of money the major source of economic activity and its disruptions.” Inelasticity is both the primary culprit of depression and the primary mover of financial innovation.

“Necessity, basically, the mother of invention even when it comes to money […]But if the eurodollar was the private (global) economy’s response to restrictive gold, what then of the eurodollar’s post-August 2007 restrictions upon the very same? Where’s the ghost money of the 21st century to replace the preeminent ghosts of the 20th?” — Jeff Snider

Snider frames the eurodollar system as a natural innovation response to the inelasticity that prevailed in the Great Depression. In the 1950’s when Robert Triffin began speaking about this paradox, the market was busy solving it through ghost money and credit. The eurodollar system is simply a network of double-entry bookkeeping and balance sheets, using the global idealized currency unit at the time, U.S. dollars (backed by $35/oz of gold).

But is the eurodollar in its current form, still ghost money? No — it is credit-based money, but it looks almost identical.

Remember, ghost money is an idealized unit of money (in the past it was silver or gold). Credit is also denominated an idealized unit-of-account, a second order derivative, if you will. Through the dominance of ghost money, thinking in an abstract currency unit became common, and the psychology of the market changed to center around this new financial tool.

The difference between the current eurodollar, which is a pure credit-based system, and credit in a ghost money system is found in the store-of-value function. Ghost money’s store of value is from a base money (silver or gold or bitcoin). The eurodollar today, on the other hand, is divorced from base money completely, and backed by something new. A dollar today is an idealized measurement of debt denominated in dollars. It’s a circular, self-referential definition in the place of base money:

“Money-of-account [ghost money] was one such alternative which also blurred the lines between money and credit; in one sense, using ledgers to settle transactions even between merchants was under the strictest definition credit rather than a monetary substitute. But that was the case only insofar as eventually this paper IOU would have to be disposed of by bullion or specie.

Subprime mortgages and their ancient equivalents became possible where specie was in overabundance, yet perhaps counterintuitively far less likely if not completely impractical using only ghosts untethered to hard money.” — Jeff Snider

In other words, untethering ghost money from its hard money can simulate the overabundance of money. We are wrong though to continue to call this untethered money, ghost money. What is it a ghost of? Once you remove the store-of-value/hard-money tether, it is now a new form of money.

I also must add that if untethered ghosts can simulate overabundance of currency, it can also simulate a currency shortage at the other extreme, which is exactly what we see today.

The eurodollar started out as ghost money until 1971 when the gold peg was severed, either by market evolution or official declaration. It became a new form of money, pure credit-based money.

Snider stated that “quasi-money is often one solution to inelasticity,” not that all solutions to inelasticity are quasi-money. Yet, that is what he’s doing when he extrapolates that because bitcoin is providing new monetary liquidity in a time of eurodollar shortage, that bitcoin is ghost money.

Currency shortages can be solved by introducing a whole new money, and as the old money suffers from shortage, the new money, with an all-new store-of-value anchor, can become the primary unit-of-account. This is not a ghost money process, it’s a money replacement process, something the Monetarists’ model cannot contend with.

“This forms the basic argument of so-called Bitcoin maximalists who see particularly the Federal Reserve but really all central banks as having set loose to ‘money printing’ excesses. They’re killing their currencies by creating too much, and cryptos are the offered antidote to ‘devaluation.’ No.It is, point of fact, the opposite.

Just like the bullion famine, what crypto enthusiasts of all kinds are reacting to — and basing their buying of digital currencies on — is the central bank response to an otherwise severe and constraining monetary shortage.” — Jeff Snider

Snider is right. I have to give him props on opening a lot of people’s eyes on this. We do have deflationary pressures today, but bitcoin is a hedge against inflation and deflation as a counterparty-free asset. It just so happens the overriding force in the economic environment today is a deflationary pressure of a credit collapse, which simulates currency shortage. While more quantity but increasingly less productive debt is money printing, meaning there is inflation, it also increases the debt burden relative to circulating currency. It creates a debt-to-income problem that manifests as a monetary shortage.

“Digital ghost money for a new age of shortfalls.” — Jeff Snider

Snider sees bitcoin as a new ghost money, where I see new money. Ghost money is no threat to replace the monetary standard, because it is a derivative of that standard, like stablecoins. U.S. dollar stablecoins will not replace U.S. dollars. They are a perfect example of ghost money.

As Snider said above, quasi-money (ghost money) is only one solution to a currency shortage, yet he labels all solutions as ghost money regardless of makeup.

Snider offers evidence in the form of his eurodollar cycles and their timing with bitcoin cycles.

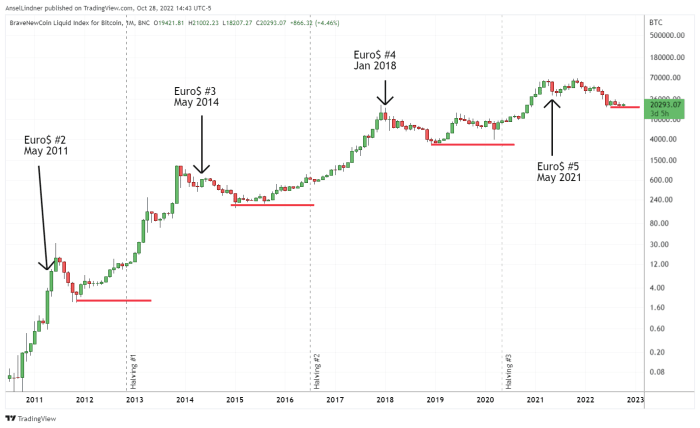

“In 2017’s bitcoin bubble, exactly the same. Its price in dollars went parabolic along with a clear bubble in digital offshoots, now-forgotten ICO’s, the frenzy never lasted long because the premise behind its price surge was entirely faulty. Once the dollar instead caught its Euro$ #4 bid, renewed acute shortage, bitcoin’s price sunk like a rock.” — Jeff Snider

They do match pretty well with bitcoin tops. Below is the best chart I could find of his with dates. However, many of his other charts have different dates for these cycles.

Source: Jeff Snider

Source: TradingView

Pretty convincing, but it shouldn’t be a surprise — demand for bitcoin is a part of the larger global market for money. Bitcoiners would definitely agree. When dollar supply is tight during these eurodollar events, bitcoin loses a bid. However, if bitcoin truly were just a ghost money derivative of the eurodollar, it would not set higher highs and higher lows each cycle.

The reason bitcoin can set those new highs each time is because bitcoin is a new money, and is slowly becoming entrenched next to the eurodollar not as a ghost money of it.

Turning back to the Great Bullion Famine, it was followed by the explosion of ghost money, but what followed that expansion is even more interesting. What happened in the 18th century in regards to ghost money and new money? Britain went to a gold standard in 1717 (officially in 1819). It changed money from which the store-of-value function was derived.

The gold guinea (7.6885 grams of fine gold) was not a new ghost money. As I argued above, the eurodollar itself, initially a response to the currency shortage in the first half of the 20th century, evolved eventually into a new store-of-value in a pure credit-based money.

But what if we bring Snider’s position full circle, when he claims that the eurodollar is still ghost money today, a position gold bugs have argued for years. What if we are still on a quasi-gold standard, because central banks hold most of the gold. (Ron Paul famously asked Ben Bernanke why the Federal Reserve held gold if it was demonetized. His response, “it’s tradition, long-term tradition.”)

This interpretation of the current eurodollar system would then make it a ghost of a ghost, ultimately based on the same store of value. It would also make the current incarnation of the eurodollar just the end-phase of another ghost money experiment, ready to be replaced by a new money, the same way the British gold standard replaced the international silver standard.

Either way you take it, that the current eurodollar is a new money because it is a pure credit-based money, or that it is the ghost of a ghost still connected psychologically to a gold standard, both these positions support one conclusion. The ultimate end of the process Snider outlines — starting from a currency shortage, to dealing with inelasticity through ghost money, and finally back to economic health — is a new form of money.

Bitcoin is a new store of value to undergird the financial system as it desperately tries to throw off the currency shortage restraints at the end of an epic global credit cycle. Bitcoin is not a ghost of the old, it is the unconstrained new.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

[ad_2]

Ansel Lindner

Source link

[ad_1]

“Dell has too many computers, Nike is swimming in summer clothes. And Gap is flooded with basics like t-shirts and shorts.” So wrote Washington Post reporter Abha Bhattarai last week. Bhattarai perhaps didn’t know it, but he was revealing something to readers bigger than the headline of the article that read “Overstocked retailers make deep price cuts.”

That there are “deep price cuts” at a time of rising prices is really a statement of the obvious. A rising price by definition signals a falling price elsewhere. To see why, imagine $100 sitting in your pocket. If you’re suddenly paying $50 for the same groceries that used to cost $35, you logically have fewer dollars for other goods and services.

In the past year or so, the news has been the “inflation” that was allegedly caused by rising prices. Such reasoning reverses causation. To say that rising prices cause inflation is the same as saying collapsed houses and buildings cause hurricanes. Actually, what’s destroyed is an effect of the hurricane, not the instigator. Inflation is no different.

Inflation is a decline in the monetary unit of measure. Rising prices can be an effect of inflation, but they’re certainly not the cause of same. To presume otherwise is tantamount to pointing to wet sidewalks as the cause of rain.

Some reading this will reply that CPI and other price measures are up, thus inflation, but CPI is once again prices of goods. The basket used right now signals higher prices, but restock the basket with Dell computers, broadband access, Nike summer apparel, and Gap t-shirts and you have a different reading. Which is why “prices” are paradoxically such a lousy way of divining inflation.

That’s the case because prices can move for all sorts of reasons. Imagine if tangerines are suddenly discovered as a surefire way of curing the common cold. If so, demand for the fruit would almost surely exceed supply on the way to soaring prices of tangerines. Conversely, imagine if plant-based meat is revealed to cause jaundice. One guesses demand for same will decline, in concert with falling prices.

Or, just think about production overall. Businesses and entrepreneurs are endlessly in the market for capital in order to mass produce former luxuries. Henry Ford rather famously turned the automobile from an impossible-to-get luxury into a common good via assembly-line production advances. What was once costly was increasingly inexpensive. Deflation? Not at all. See above. Just as a rising price for one good implies a falling price elsewhere, so does a falling price for one market good imply rising prices for other goods.

The simple truth is that prices on their own are how a market economy organizes itself, and they rise and fall for all sorts of reasons that have nothing to do with inflation. Inflation is once again a decline in the monetary unit of measure.

Taking all of this into the present, this column has made a case from Day One that the “inflation” of the moment is not inflation. This is no revelation, or shouldn’t be. Inflation is yet again a decline in the monetary unit, but over the last two years the dollar has risen against the major foreign currencies, plus it’s risen against gold; the most objective measure of all. Gold generally doesn’t move in value as much as the currencies in which it’s priced move in value. The dollar price of gold has fallen in the past two years, which should have neo-inflationists wondering. Indeed, their contention is that we have a major inflation problem as the dollar is rising. Sorry, but that’s not inflation.

What we have right now is rising and sometimes nosebleed prices for certain goods. That we do should be a statement of the obvious. To see why, consider Henry Ford’s genius yet again. He was miraculously able to make automobiles affordable by dividing up their production among hundreds and thousands of specialized workers.

Please think of this with the last two years top of mind. As I point out in my new book The Money Confusion, every market good in the world is the result of remarkably sophisticated global cooperation among workers and machines. Yet this sophisticated global symmetry was eviscerated to varying degrees by lockdowns in 2020 and beyond. Economic activity divided up by billions of workers around the world was suddenly halted altogether, or limited in various ways. Workers once free to work, and businesses once free to operate, suddenly were not. That prices are higher in the aftermath of this hideous imposition of command-and-control is more than tautological.

What’s important is that higher prices born of force are hardly inflation, plus as we know from Bhattarai, the higher prices have logically reduced demand elsewhere. Bhattarai reports that there’s presently a record of $732 billion in unsold inventory among U.S. companies. Yes, it makes sense. We can’t have everything.

In short, this is not inflation. Don’t let it be called what it isn’t. To errantly refer to rising prices as inflation is to let politicians off the hook for their monumental errors in 2020 and beyond. Don’t let them off of the hook. “Dell has too many computers, Nike is swimming in summer clothes. And Gap is flooded with basics like t-shirts and shorts.” So wrote Washington Post reporter Abha Bhattarai last week. Bhattarai perhaps didn’t know it, but he was revealing something to readers bigger than the headline of the article that read “Overstocked retailers make deep price cuts.”

That there are “deep price cuts” at a time of rising prices is really a statement of the obvious. A rising price by definition signals a falling price elsewhere. To see why, imagine $100 sitting in your pocket. If you’re suddenly paying $50 for the same groceries that used to cost $35, you logically have fewer dollars for other goods and services.

In the past year or so, the news has been the “inflation” that was allegedly caused by rising prices. Such reasoning reverses causation. To say that rising prices cause inflation is the same as saying collapsed houses and buildings cause hurricanes. Actually, what’s destroyed is an effect of the hurricane, not the instigator. Inflation is no different.

Inflation is a decline in the monetary unit of measure. Rising prices can be an effect of inflation, but they’re certainly not the cause of same. To presume otherwise is tantamount to pointing to wet sidewalks as the cause of rain.

Some reading this will reply that CPI and other price measures are up, thus inflation, but CPI is once again prices of goods. The basket used right now signals higher prices, but restock the basket with Dell computers, broadband access, Nike summer apparel, and Gap t-shirts and you have a different reading. Which is why “prices” are paradoxically such a lousy way of divining inflation.

That’s the case because prices can move for all sorts of reasons. Imagine if tangerines are suddenly discovered as a surefire way of curing the common cold. If so, demand for the fruit would almost surely exceed supply on the way to soaring prices of tangerines. Conversely, imagine if plant-based meat is revealed to cause jaundice. One guesses demand for same will decline, in concert with falling prices.

Or, just think about production overall. Businesses and entrepreneurs are endlessly in the market for capital in order to mass produce former luxuries. Henry Ford rather famously turned the automobile from an impossible-to-get luxury into a common good via assembly-line production advances. What was once costly was increasingly inexpensive. Deflation? Not at all. See above. Just as a rising price for one good implies a falling price elsewhere, so does a falling price for one market good imply rising prices for other goods.

The simple truth is that prices on their own are how a market economy organizes itself, and they rise and fall for all sorts of reasons that have nothing to do with inflation. Inflation is once again a decline in the monetary unit of measure.

Taking all of this into the present, this column has made a case from Day One that the “inflation” of the moment is not inflation. This is no revelation, or shouldn’t be. Inflation is yet again a decline in the monetary unit, but over the last two years the dollar has risen against the major foreign currencies, plus it’s risen against gold; the most objective measure of all. Gold generally doesn’t move in value as much as the currencies in which it’s priced move in value. The dollar price of gold has fallen in the past two years, which should have neo-inflationists wondering. Indeed, their contention is that we have a major inflation problem as the dollar is rising. Sorry, but that’s not inflation.

What we have right now is rising and sometimes nosebleed prices for certain goods. That we do should be a statement of the obvious. To see why, consider Henry Ford’s genius yet again. He was miraculously able to make automobiles affordable by dividing up their production among hundreds and thousands of specialized workers.

Please think of this with the last two years top of mind. As I point out in my new book The Money Confusion, every market good in the world is the result of remarkably sophisticated global cooperation among workers and machines. Yet this sophisticated global symmetry was eviscerated to varying degrees by lockdowns in 2020 and beyond. Economic activity divided up by billions of workers around the world was suddenly halted altogether, or limited in various ways. Workers once free to work, and businesses once free to operate, suddenly were not. That prices are higher in the aftermath of this hideous imposition of command-and-control is more than tautological.

What’s important is that higher prices born of force are hardly inflation, plus as we know from Bhattarai, the higher prices have logically reduced demand elsewhere. Bhattarai reports that there’s presently a record of $732 billion in unsold inventory among U.S. companies. Yes, it makes sense. We can’t have everything.

In short, this is not inflation. Don’t let it be called what it isn’t. To errantly refer to rising prices as inflation is to let politicians off the hook for their monumental errors in 2020 and beyond. Don’t let them off of the hook.

[ad_2]

John Tamny, Contributor

Source link