[ad_1]

If there were no tax cheats in America, there would be no Social Security crisis. Benefits could be paid, and payroll taxes kept the same, for the next 75 years.

That’s not me talking. That’s math. It comes from the number crunchers at the Social Security Administration and the Internal Revenue Service.

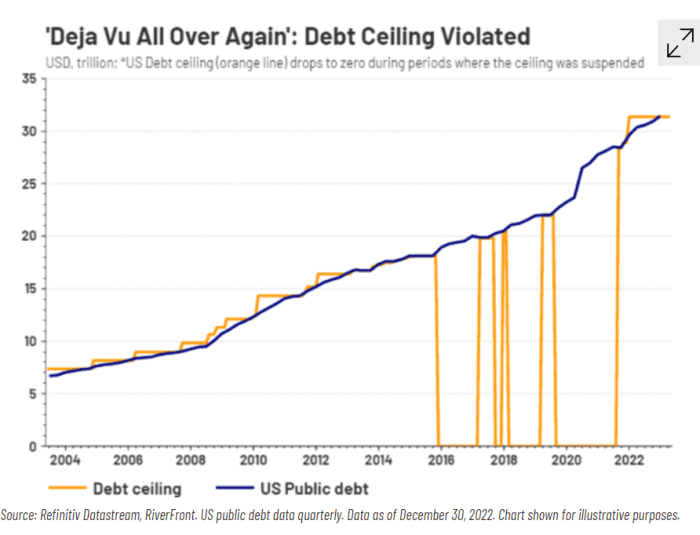

And it explains why those of us who support Social Security should be pounding the table in outrage over one clause of the Biden-McCarthy debt ceiling deal: The part where the president has to retreat from his crackdown on tax cheats just so McCarthy and the House Republicans would agree to prevent America defaulting on its debts.

It’s just two years since the administration got into law an extra $80 billion for the IRS to beef up enforcement. That was supposed to include hiring an estimated 87,000 IRS agents.

OK, so nobody likes paying taxes and nobody likes the IRS. Cue the inevitable critiques of an IRS tax “army,” and so on. But this isn’t about whether taxes should be higher or lower. It’s about whether everyone should pay the taxes that they owe.

After all, if we’re going to cut taxes, shouldn’t they apply to those of us who obey the laws as well as those who don’t? Or do we just support the “Tax Cuts for Criminals” Act?

Why would any voter rally around a platform of “I stand with tax cheats?”

The Congressional Budget Office calculated that the extra funding for the IRS would have reduced the deficit, because it would more than pay for itself. But it’s now been cut by an estimated $21 billion out of $80 billion.

If this seems abstract, consider the context and how it affects you and your retirement — and the retirements of everyone you know.

Social Security is now running at an $80 billion annual deficit. That’s the amount benefits are expected to exceed payroll taxes this year. (So say the Social Security Administration’s trustees.)

Next year, that deficit is expected to top $150 billion. By 2026, we’re looking at $200 billion and rising. The trust fund will run out of cash by 2034, and without extra payroll taxes will have to slash benefits by a fifth or more.

Over the next 75 years, says the Congressional Budget Office, the entire funding gap for the program will average about 1.7% of gross domestic product per year.

Meanwhile, how much are tax cheats stealing from the rest of us? A multiple of that.

According to the most recent estimates from the IRS, tax cheats steal about $470 billion a year. And that figure is four years out of date, relating to 2019. That’s the figure after enforcement measures.

Oh, and the Treasury Inspector General for Tax Administration says that’s a lowball number.

But it still worked out at around 12% of all the taxes people were supposed to pay (including payroll taxes). And around 2.3% of GDP.

Over the next 10 years, based on similar ratios to GDP, that would come to another $3.3 billion.

Sure, Social Security’s trust fund is theoretically separate from the rest of Uncle Sam’s finances. But that’s an accounting issue: A distinction without a difference.

Social Security is America’s retirement plan. Few could retire in dignity without it. Yet it is facing a fiscal crisis. By 2034, without changes, the program will be forced to cut benefits — drastically.

Some people want to cut benefits. Others want to raise the retirement age, which also means cutting benefits. Others want to raise taxes on benefits — which also means cutting benefits. Others want to hike payroll taxes, either on all of us or (initially) only on very high earners.

At last — just 40 or so years out of date — some are starting to talk about investing some of the trust fund like nearly every other pension plan in the world, in high-returning stocks instead of just low-returning Treasury bonds.

(It is hard for me to believe that it’s now almost 16 years since I first wrote about this ridiculously obvious fix And, yes, I’ve been boring readers on the subject ever since, including here and most recently here, and, no, I have no plans to stop.)

But if investing some of the trust fund in stocks is a no-brainer, so, too, is insisting everyone obey the law and pay the taxes they actually owe each year. I mean, shouldn’t we do that before we think about raising taxes even further on those who abide by the law?

How could anyone object? Any party that believes in law and order would support enforcing, er, law and order on tax evasion. And any party of fiscal conservatism would support measures, like tax enforcement, to narrow the deficit.

And, actually, any party that truly supported lower taxes for all would be tough on tax evasion: It is precisely this $500 billion in evasion by a small, scofflaw minority that forces the rest of us to pay more. We have, quite literally, a tax on obeying the law.

One of the many arguments in favor of taxing assets or wealth, instead of just income, is that enforcement would be easier and evasion much harder.

Washington, D.C., seems to be a place where people come up with complex proposals just so they can avoid the simple, fair ones.

[ad_2]