The numbers: A closely-watched index that measures U.S. manufacturing activity fell 0.7 percentage points to 50.2 in October, according to the Institute for Supply Management on Tuesday.

Economists surveyed by the Wall Street Journal had forecast the index to inch down to 50. Any number below 50% reflects a shrinking economy.

It is the lowest level since May 2020.

Key details: The index for new orders remained in contraction territory, rising 2.1 points to 47.1. The production index rose 1.7 points to 52.3.

The employment index rose 1.3 points to 50 in October.

Supplier deliveries fell 5.6 points to 46.8 in October. This is the first time that deliveries were in a “faster” territory since February 2016.

The price index dropped 5.1 points to 46.6., also the lowest reading since the pandemic. Pricing power is shifting back to the buyer, the ISM said.

Only 8 of the 18 manufacturing industries reported growth in October.

Big picture: Manufacturing has been slowing recently led by softening business spending and fading demand for consumer goods. Economists think it is inevitable the index slips below the 50 threshold.

In a separate data, the S&P global U.S. manufacturing PMI inched up to 50.4 in its “final” reading in October from the “flash” reading of 49.9. This is down from a reading of 52 in September.

What ISM said: Manufacturing is slowing down and could soon enter contraction territory, but that doesn’t mean there will be a recession in the U.S., said Timothy Fiore, chair of the ISM factory business survey.

“I don’t see a collapse of new orders. I don’t see a collapse of the PMI,” Fiore said.

Looking ahead: “Recession jitters among manufacturers won’t disappear any time soon…manufacturing will endure more pain as demand weakens at home and abroad while prices stay high and interest rates remain fairly elevated,” said Oren Klachkin, economist at Oxford Economics.

The Chicago Business Barometer, also known as the Chicago PMI, dropped to 45.2 in October from 45.7 in the prior month, according to data released Monday.

Economists polled by the Wall Street Journal forecast a 47 reading.

Readings below 50 indicate contraction territory.

The index is produced by the ISM-Chicago with MNI. It is released to subscribers three minutes before its release to the public at 9:45 am Eastern.

The Chicago PMI is the last of the regional manufacturing indices before the national factory data for October is released on Tuesday.

Economist polled by the Wall Street Journal expect the closely-watched Institute for Supply Management’s factory index to barely remain above the 50 breakeven level in October.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.046%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.030%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

Economists polled by the Wall Street Journal had expected manufacturing to rise to 51.8 in October and for the service sector to rise to 49.7.

Key details: In the service sector, the downturn was fueled by the rising cost of living and tightening financial conditions.

New orders in the manufacturing sector fell back into contraction territory in October. Output remained resilient due to firms eating into backlogs of previously placed orders, S&P Global said.

While price pressures picked up a bit in the service sector, the pace of the gain in inflation in the manufacturing sector was the slowest in almost two years.

Big picture: Talk of a recession sometime in 2023 has picked up in the last week. Many economists are sounding more bearish on the outlook, especially since the Federal Reserve is now seen raising its benchmark rate to 5%. However, on Monday, economists at Goldman Sachs said that talk over a recession was overblown.

What S&P Global said: “The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

“Although price pressures picked up slightly in the service sector due to high food, energy and staff costs, as well as rising borrowing costs, increased competitive forces meant average prices charged for services grew at only a fractionally faster rate. Combined with the easing of price pressures in the goods-producing sector, this adds to evidence that consumer price inflation should cool in coming months,” he added.

Some investors are on edge that the Federal Reserve may be overtightening monetary policy in its bid to tame hot inflation, as markets look ahead to a reading this coming week from the Fed’s preferred gauge of the cost of living in the U.S.

“Fed officials have been scrambling to scare investors almost every day recently in speeches declaring that they will continue to raise the federal funds rate,” the central bank’s benchmark interest rate, “until inflation breaks,” said Yardeni Research in a note Friday. The note suggests they went “trick-or-treating” before Halloween as they’ve now entered their “blackout period” ending the day after the conclusion of their November 1-2 policy meeting.

“The mounting fear is that something else will break along the way, like the entire U.S. Treasury bond market,” Yardeni said.

Treasury yields have recently soared as the Fed lifts its benchmark interest rate, pressuring the stock market. On Friday, their rapid ascent paused, as investors digested reports suggesting the Fed may debate slightly slowing aggressive rate hikes late this year.

Stocks jumped sharply Friday while the market weighed what was seen as a potential start of a shift in Fed policy, even as the central bank appeared set to continue a path of large rate increases this year to curb soaring inflation.

The stock market’s reaction to The Wall Street Journal’s report that the central bank appears set to raise the fed funds rate by three-quarters of a percentage point next month – and that Fed officials may debate whether to hike by a half percentage point in December — seemed overly enthusiastic to Anthony Saglimbene, chief market strategist at Ameriprise Financial.

“It’s wishful thinking” that the Fed is heading toward a pause in rate hikes, as they’ll probably leave future rate hikes “on the table,” he said in a phone interview.

“I think they painted themselves into a corner when they left interest rates at zero all last year” while buying bonds under so-called quantitative easing, said Saglimbene. As long as high inflation remains sticky, the Fed will probably keep raising rates while recognizing those hikes operate with a lag — and could do “more damage than they want to” in trying to cool the economy.

“Something in the economy may break in the process,” he said. “That’s the risk that we find ourselves in.”

‘Debacle’

Higher interest rates mean it costs more for companies and consumers to borrow, slowing economic growth amid heightened fears the U.S. faces a potential recession next year, according to Saglimbene. Unemployment may rise as a result of the Fed’s aggressive rate hikes, he said, while “dislocations in currency and bond markets” could emerge.

U.S. investors have seen such financial-market cracks abroad.

The Bank of England recently made a surprise intervention in the U.K. bond market after yields on its government debt spiked and the British pound sank amid concerns over a tax cut plan that surfaced as Britain’s central bank was tightening monetary policy to curb high inflation. Prime minister Liz Truss stepped down in the wake of the chaos, just weeks after taking the top job, saying she would leave as soon as the Conservative party holds a contest to replace her.

“The experiment’s over, if you will,” said JJ Kinahan, chief executive officer of IG Group North America, the parent of online brokerage tastyworks, in a phone interview. “So now we’re going to get a different leader,” he said. “Normally, you wouldn’t be happy about that, but since the day she came, her policies have been pretty poorly received.”

Meanwhile, the U.S. Treasury market is “fragile” and “vulnerable to shock,” strategists at Bank of America warned in a BofA Global Research report dated Oct. 20. They expressed concern that the Treasury market “may be one shock away from market functioning challenges,” pointing to deteriorated liquidity amid weak demand and “elevated investor risk aversion.”

“The fear is that a debacle like the recent one in the U.K. bond market could happen in the U.S.,” Yardeni said, in its note Friday.

“While anything seems possible these days, especially scary scenarios, we would like to point out that even as the Fed is withdrawing liquidity” by raising the fed funds rate and continuing quantitative tightening, the U.S. is a safe haven amid challenging times globally, the firm said. In other words, the notion that “there is no alternative country” in which to invest other than the U.S., may provide liquidity to the domestic bond market, according to its note.

YARDENI RESEARCH NOTE DATED OCT. 21, 2022

“I just don’t think this economy works” if the yield on the 10-year Treasury TMUBMUSD10Y, 4.228%

note starts to approach anywhere close to 5%, said Rhys Williams, chief strategist at Spouting Rock Asset Management, by phone.

Ten-year Treasury yields dipped slightly more than one basis point to 4.212% on Friday, after climbing Thursday to their highest rate since June 17, 2008 based on 3 p.m. Eastern time levels, according to Dow Jones Market Data.

Williams said he worries that rising financing rates in the housing and auto markets will pinch consumers, leading to slower sales in those markets.

“The market has more or less priced in a mild recession,” said Williams. If the Fed were to keep tightening, “without paying any attention to what’s going on in the real world” while being “maniacally focused on unemployment rates,” there’d be “a very big recession,” he said.

Investors are anticipating that the Fed’s path of unusually large rate hikes this year will eventually lead to a softer labor market, dampening demand in the economy under its effort to curb soaring inflation. But the labor market has so far remained strong, with an historically low unemployment rate of 3.5%.

George Catrambone, head of Americas trading at DWS Group, said in a phone interview that he’s “fairly worried” about the Fed potentially overtightening monetary policy, or raising rates too much too fast.

The central bank “has told us that they are data dependent,” he said, but expressed concerns it’s relying on data that’s “backward-looking by at least a month,” he said.

The unemployment rate, for example, is a lagging economic indicator. The shelter component of the consumer-price index, a measure of U.S. inflation, is “sticky, but also particularly lagging,” said Catrambone.

At the end of this upcoming week, investors will get a reading from the personal-consumption-expenditures-price index, the Fed’s preferred inflation gauge, for September. The so-called PCE data will be released before the U.S. stock market opens on Oct. 28.

Meanwhile, corporate earnings results, which have started being reported for the third quarter, are also “backward-looking,” said Catrambone. And the U.S. dollar, which has soared as the Fed raises rates, is creating “headwinds” for U.S. companies with multinational businesses.

“Because of the lag that the Fed is operating under, you’re not going to know until it’s too late that you’ve gone too far,” said Catrambone. “This is what happens when you’re moving with such speed but also such size, he said, referencing the central bank’s string of large rate hikes in 2022.

“It’s a lot easier to tiptoe around when you’re raising rates at 25 basis points at a time,” said Catrambone.

‘Tightrope’

In the U.S., the Fed is on a “tightrope” as it risks over tightening monetary policy, according to IG’s Kinahan. “We haven’t seen the full effect of what the Fed has done,” he said.

While the labor market appears strong for now, the Fed is tightening into a slowing economy. For example, existing home sales have fallen as mortgage rates climb, while the Institute for Supply Management’s manufacturing survey, a barometer of American factories, fell to a 28-month low of 50.9% in September.

Also, trouble in financial markets may show up unexpectedly as a ripple effect of the Fed’s monetary tightening, warned Spouting Rock’s Williams. “Anytime the Fed raises rates this quickly, that’s when the water goes out and you find out who’s got the bathing suit” — or not, he said.

“You just don’t know who is overlevered,” he said, raising concern over the potential for illiquidity blowups. “You only know that when you get that margin call.”

U.S. stocks ended sharply higher Friday, with the S&P 500 SPX, +2.37%,

Dow Jones Industrial Average DJIA, +2.47%

and Nasdaq Composite each scoring their biggest weekly percentage gains since June, according to Dow Jones Market Data.

Still, U.S. equities are in a bear market.

“We’ve been advising our advisors and clients to remain cautious through the rest of this year,” leaning on quality assets while staying focused on the U.S. and considering defensive areas such as healthcare that can help mitigate risk, said Ameriprise’s Saglimbene. “I think volatility is going to be high.”

Stock-market investors have been adjusting to the jump in interest rates amid high inflation, but they have yet to cope with profit headwinds faced by the S&P 500, according to Morgan Stanley Wealth Management.

“While a rate peak may solidify estimates for the equity risk premium and valuation multiples, equity investors still face the bear market’s second act — the earnings outlook,” said Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management, in a note Monday.

“They have been slow to recognize that pricing power and operating margins, which hit all-time highs in the past two years, are unsustainable,” she said. “Even without a recession, the mean reversion of profits in 2023 translates to a 10%-to-15% decline from current estimates.”

MORGAN STANLEY WEALTH MANAGEMENT NOTE DATED OCT. 17 2022

Unprecedented monetary and fiscal stimulus during the throes of the pandemic had led to the largest U.S. companies booking record operating margins that were 150 to 200 basis points above norms seen in the past decade, according to Shalett.

She said that company profits may now be imperiled by slowing growth, with “demand skewing toward services” after pulling forward toward goods earlier in the pandemic, and a likely reversal in “extremely strong” pricing power as the Fed fights surging inflation with interest-rate hikes.

“Such risks are not discounted in 2023 consensus yet, constituting a material risk to stocks for the remainder of the year,” Shalett said.

While many sectors have discounted the potential drop in 2023 profits from current estimates that could stir headwinds even with no recession, “the megacap secular growth stocks that dominate market-cap indexes have not,” she warned. “And those indexes are where risk gets repriced in the bear market’s final stages.”

Morgan Stanley’s chief U.S. equity strategist Mike Wilson estimates as much as 11% downside from consensus estimates, with his base-case, earnings-per-share forecast for the S&P 500 for 2023 being $212, according to Shalett’s note.

U.S. stocks were bouncing Monday, with major stock benchmarks trading sharply higher in the afternoon, after sinking Friday amid inflation concerns as earnings season got under way. The S&P 500 SPX, +2.65%

was up 2.7% in afternoon trading, while the Dow Jones Industrial Average DJIA, +1.86%

gained 1.9% and the technology-heavy Nasdaq Composite surged 3.5%, FactSet data show, last check.

In the bond market, Treasury rates were trading slightly lower Monday afternoon, after the 2-year yield hit a 15-year high and the 10-year yield notched a 14-year high on Friday, according to Dow Jones Market Data. Two-year yields ended last week at 4.507%, the highest level since August 8, 2007 based on 3 p.m. Eastern time levels, while the 10-year rate climbed to 4.005% for its highest rate since Oct. 15, 2008.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.992%

was down about 1 basis point Monday afternoon at around 4%, while two-year yields TMUBMUSD02Y, 4.439%

fell about five basis points to around 4.45%, FactSet data show, at last check.

Meanwhile, as investors capitulated to higher inflation, “peak policy rates moved up aggressively in the fed funds futures market, with the terminal rate now at nearly 5%, an aggressive stance that smacks of ‘peak hawkishness,’” according to the Morgan Stanley note.

“Critically, although the market is still pricing 1.5 cuts in 2023, the January 2024 fed-funds rate is estimated at 4.5%, a comfortable 100 basis points above our forecast” for core inflation measured by the consumer-price index, Shalett wrote.

“Consider locking in solid short-term yields in bonds and shoring up positions in high growth, dividend-paying stocks,” she said. “Short-duration Treasuries look attractive, especially because the yield is more than 2.5 times that of the dividend yield on the S&P 500.”

The whipsaw action wasn’t limited to stocks, and was described by Rick Rieder, the chief investment officer for global fixed income at BlackRock, as “one of the craziest days” of his career.

The bond market’s warning

Some investors who focus on stocks might not realize that the bond market is much larger, and that its movements can cause government and central-bank policies to shift. Larry McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, explained just how bad the action was in the U.K. bond market over the past few weeks, when 30-year government bonds issued in December traded as low as 24 cents on the dollar. He also predicted what will happen if the Federal Reserve continues on its current course of interest-rate increases.

Michael Brush argues the Federal Reserve is moving too quickly to raise interest rates and cool the U.S. economy. He expects a rapid decline in inflation and a new bull market for stocks. In a column, he shares five sentiment indicators that suggest it is time to buy stocks — especially this group of companies.

Time for a refreshing COLA if you are on Social Security

Getty Images

The Social Security Administration has announced that its cost-of-living adjustment (COLA) for 2023 will be 8.7%, the largest increase in four decades. There is more to the story, including tax implications and changes to Medicare, as Jessica Hall and Alessandra Malito explain.

Freddie Mac said interest rates on 30-year mortgage loans averaged 6.92% on Oct. 13, up from 3.05% a year earlier. Mortgage Daily said rates had hit 7.10% — the highest in 20 years — and economists are warning these levels could be a “new normal.”

A homeowner locked-in with a low interest rate on their mortgage loan will be reluctant to sell. And some would-be buyers may now be priced out of the market because of much higher loan payments. Here’s what economists expect for home prices in 2023.

This is why Florida’s insurance market is such a mess

Florida insurers are not only suffering from storm-damage payouts.

Joe Raedle/Getty Images

Hurricanes are nothing new to Floridians, but insurers in the state are losing money even though premiums have doubled over the past five years. Shahid S. Hamid, the director of the Laboratory for Insurance at Florida International University, explains why the Florida insurance market is so distorted.

Here’s a travel option you may never have heard of — home swapping

Villefranche-sur-mer on the French Riviera.

istock

Home swapping can give you an opportunity to live as a local in a faraway place while spending much less than you would as a tourist. Here’s how it works.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

U.K. bond yields continued to drop on Friday, on expectations the U.K. government will further backtrack on its tax cut plans and that U.K. Prime Minister Liz Truss will fire Chancellor of the Exchequer Kwasi Kwarteng.

Kwarteng was photographed entering Downing Street after flying home early from the International Monetary Fund meeting in Washington, D.C. Truss’s office has announced a press conference. Both The Times and the Financial Times newspapers reported Kwarteng will be fired.

The yield on the 30 year gilt TMBMKGB-30Y, 4.265%

— which was high as 5.1% as recently as Wednesday — fell 28 basis points to 4.27%.

The yield on the 10-year gilt TMBMKGB-10Y, 3.947%

dropped 25 basis points to 3.95%. Yields move in the opposite direction to prices.

The pound GBPUSD, -0.75%

fetched $1.1273, down from $1.1331 on Thursday.

Kwarteng in recent interviews has done nothing to douse speculation the U.K. government will further pare its tax-cut plans.

Speculation of further U-turns has centered around corporate tax cuts in particular. Other tax cuts that could be reversed include the planned personal income-tax reduction to 19% from 20%.

The government has already relented on a planned cut for those making above £150,000. Financial markets gyrated after Kwarteng announced its mini-budget, which called for some £45 billion in tax cuts on top of capping energy prices. Investec Securities estimates the total cost of the stimulus to be on the order of £150 billion.

A medium-term fiscal plan, as well as an independent forecast from the Office of Budget Responsibliitiy, is due at the end of October.

The Bank of England’s emergency bond-buying plan — designed to ease tensions for pension funds — is due to expire on Friday.

The central bank says it’s purchased £17.8 billion in securities.

Don’t assume the worst is over, says investor Larry McDonald.

There’s talk of a policy pivot by the Federal Reserve as interest rates rise quickly and stocks keep falling. Both may continue.

McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, expects more turmoil in the bond market, in part, because “there is $50 trillion more in world debt today than there was in 2018.” And that will hurt equities.

The bond market dwarfs the stock market — both have fallen this year, although the rise in interest rates has been worse for bond investors because of the inverse relationship between rates (yields) and bond prices.

About 600 institutional investors from 23 countries participate in chats on the Bear Traps site. During an interview, McDonald said the consensus among these money managers is “things are breaking,” and that the Federal Reserve will have to make a policy change fairly soon.

Pointing to the bond-market turmoil in the U.K., McDonald said government bonds that mature in 2061 were trading at 97 cents to the dollar in December, 58 cents in August and as low as 24 cents over recent weeks.

When asked if institutional investors could simply hold on to those bonds to avoid booking losses, he said that because of margin calls on derivative contracts, some institutional investors were forced to sell and take massive losses.

And investors haven’t yet seen the financial statements reflecting those losses — they happened too recently. Write-downs of bond valuations and the booking of losses on some of those will hurt bottom-line results for banks and other institutional money managers.

Interest rates aren’t high, historically

Now, in case you think interest rates have already gone through the roof, check out this chart, showing yields for 10-year U.S. Treasury notes TMUBMUSD10Y, 3.898%

over the past 30 years:

The yield on 10-year Treasury notes has risen considerably as the Federal Reserve has tightened during 2022, but it is at an average level if you look back 30 years.

FactSet

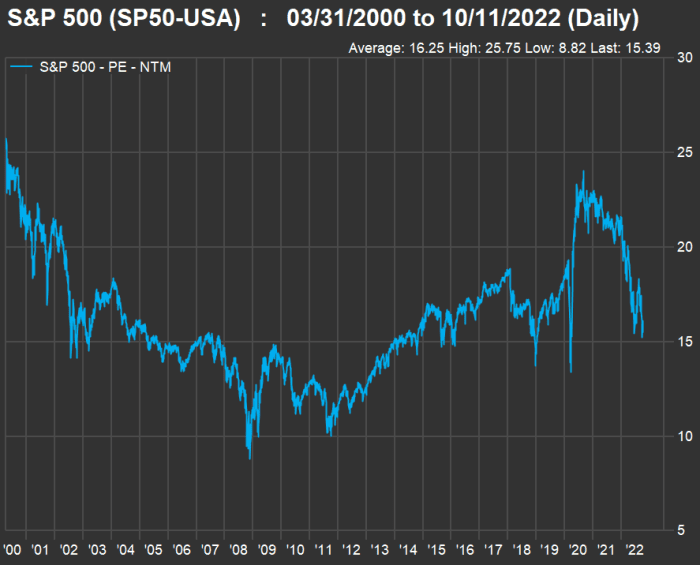

The 10-year yield is right in line with its 30-year average. Now look at the movement of forward price-to-earnings ratios for S&P 500 SPX, -0.03%

since March 31, 2000, which is as far back as FactSet can go for this metric:

FactSet

The index’s weighted forward price-to-earnings (P/E) ratio of 15.4 is way down from its level two years ago. However, it is not very low when compared to the average of 16.3 since March 2000 or to the 2008 crisis-bottom valuation of 8.8.

Then again, rates don’t have to be high to hurt

McDonald said that interest rates didn’t need to get anywhere near as high as they were in 1994 or 1995 — as you can see in the first chart — to cause havoc, because “today there is a lot of low-coupon paper in the world.”

“So when yields go up, there is a lot more destruction” than in previous central-bank tightening cycles, he said.

It may seem the worst of the damage has been done, but bond yields can still move higher.

Heading into the next Consumer Price Index report on Oct. 13, strategists at Goldman Sachs warned clients not to expect a change in Federal Reserve policy, which has included three consecutive 0.75% increases in the federal funds rate to its current target range of 3.00% to 3.25%.

The Federal Open Market Committee has also been pushing long-term interest rates higher through reductions in its portfolio of U.S. Treasury securities. After reducing these holdings by $30 billion a month in June, July and August, the Federal Reserve began reducing them by $60 billion a month in September. And after reducing its holdings of federal agency debt and agency mortgage-backed securities at a pace of $17.5 billion a month for three months, the Fed began reducing these holdings by $35 billion a month in September.

Bond-market analysts at BCA Research led by Ryan Swift wrote in a client note on Oct. 11 that they continued to expect the Fed not to pause its tightening cycle until the first or second quarter of 2023. They also expect the default rate on high-yield (or junk) bonds to increase to 5% from the current rate of 1.5%. The next FOMC meeting will be held Nov. 1-2, with a policy announcement on Nov. 2.

McDonald said that if the Federal Reserve raises the federal funds rate by another 100 basis points and continues its balance-sheet reductions at current levels, “they will crash the market.”

A pivot may not prevent pain

McDonald expects the Federal Reserve to become concerned enough about the market’s reaction to its monetary tightening to “back away over the next three weeks,” announce a smaller federal funds rate increase of 0.50% in November “and then stop.”

He also said that there will be less pressure on the Fed following the U.S. midterm elections on Nov. 8.

Investors are bracing for some choppiness on Wall Street, with oil prices falling as growth worries rattle around the globe. That’s as the clock ticks down to CPI and the start of a earnings season later this week, and in the backdrop a war is intensifying in Europe.

Tough times don’t last, but tough investors do right? Maybe, hopefully. In any case, focusing on the distant future might offer some comfort right now.

And that’s where we’re headed with our call of the day from Citigroup, whose strategists have stock ideas to play what they expect will be one of the ten fastest-growing markets through 2040.

They are talking about the global fuel cell industry, a direct play on the green energy debate, and “reaching the part that batteries cannot.”

“Fuel cells enable both de-carbonization and energy resilience, and we see them as crucial in harder-to-abate sectors like commercial vehicles and marine,” a Citi team led by research analyst Martin Wilkie told clients in a note on Tuesday.

Their base case sees this market reaching 50 gigawatts (GW) and $40 billion by 2030, offering a compound average growth rate of more than 35% in dollar terms, with further acceleration to 500GW/$180 billion by 2040.

They admit they’re on the bullish side with these projections, and note fuel cell stocks are on average down around 70% since their January 2021 peaks .

“The fuel cell equity story has had false starts before, but we see the impetus from emissions policy as well as announced hydrogen plans as creating attractive opportunities,” said the Citi analysts, highlighting policies such as the U.S. Inflation Reduction Act, which aims at beefing up renewable energy and a recent EU move to offer more green-energy research and development subsidies.

While passenger cars were a big source of demand for the growing fuel cell market in 2021, they don’t think it can be a big competitor to battery electric. However, stationary power, such as distributed and backup power generation and heavy-duty transport, think commercial vehicles, off-road and later marine are set to become key fuel-cell markets.

VOLV.A, +0.12%,

which are working with Germany’s Traton 8TRA, -2.09%

on a joint venture called Cellcentric that aims to develop that technology for trucks, with a production goal of 2025. Others are outsourcing fuel-cell tech, such as Italy’s Iveco Group IVG, +0.10%,

which has teamed up with South Korea’s Hyundai 005380, -4.27%,

and U.S.-based Paccar PCAR, +0.23%

with Toyota TM, -0.73%.

Shares of the world’s biggest chip maker, TSMC 2330, -8.33%, fell 8% in Taiwan Y9999, -4.35%,

where stocks dropped more than 4% following new limits by the U.S. imposed on exports of semiconductors and chip-making equipment to China.

The National Federation of Independent Business small-business index showed confidence rising in September, but inflation a nagging problem. At noon Eastern we’ll hear from Cleveland Fed President Loretta Mester.

Subscription-based private aviation company Flexjet plans to go public through a merger with SPAC Horizon Acquisition HZON,

valuing it at $3.1 billion.

The U.S.’s third-biggest railroad union will be back at the negotiating table with employers on Tuesday, after rejecting a deal and raising the possibility of crippling strikes.

The Kremlin’s war hawks were thrilled at the devastating strikes across Ukraine on Monday. Now they want more. G-7 leaders are holding an emergency meeting to discuss the ramping up of the war.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index SPX, -2.80%

tumbled 2.8% on Friday, the Dow Jones Industrial Average DJIA, -2.11%

fell 630.15 points, or 2.1%, and the Nasdaq Composite Index COMP, -3.04%

dropped 3.8%. An early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

The S&P 500 is down about 24% for the year, while the Dow is off 19% and the Nasdaq nearly 32%.The 10-year Treasury rate TMUBMUSD10Y, 3.889%

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index SPX, -3.03%

tumbled 1.9% on Friday, the Dow Jones Industrial Average DJIA, -2.39%

was down 1.5% and the Nasdaq Composite Index COMP, -3.89%

was off 2.6%. And early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

The S&P 500 is down about 23% for the year, the Dow off 19% and the Nasdaq off 31% since January. The 10-year Treasury rate TMUBMUSD10Y, 3.884%

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

Treasury yields rose Friday after the U.S. September payrolls report showed a surprise decline in unemployment as well as strong growth in wages, making a pivot in Fed policy less likely.

What’s happening

The yield on the 2-year Treasury TMUBMUSD02Y, 4.307%

rose 5 basis points to 4.31%

The yield on the 10-year Treasury TMUBMUSD10Y, 3.894%

rose 5 basis points to 3.89%.

The yield on the 30-year Treasury TMUBMUSD30Y, 3.858%

increased 3 basis points to 3.82%.

What’s driving markets

The U.S. created 263,000 nonfarm jobs in September — roughly in line with expectations — with the unemployment rate falling to 3.5% from 3.7%, while the year-over-year growth rate in hourly wages was 5%.

The unemployment decline was a surprise to economists who had anticipated a steady jobless picture.

Federal Reserve Gov. Christopher Waller late on Thursday said he didn’t expect the jobs report to change anyone’s thinking at the central bank. New York Fed President John Williams will have the opportunity to comment on the data when he speaks at 10 a.m. Eastern.

Ahead of the release, strategists at ING said the price action this week suggests the market has moved away from the early Fed policy pivot idea. “We may well have seen the structural top at 4% for the 10 year, or thereabouts, but we also feel we’re liable to see it at least one more time. There is a large fall in market rates to come, but we’re not at that point just yet,” they added.

When the stock market has jumped two days in a row, as it has now, it is easy to become complacent.

But the Federal Reserve isn’t finished raising interest rates, and recession talk abounds. Stock investors aren’t out of the woods yet. That can make dividend stocks attractive if the yields are high and the companies produce more cash flow than they need to cover the payouts.

Below is a list of 21 stocks drawn from the S&P Composite 1500 Index SP1500, +3.12%

that appear to fit the bill. The S&P Composite 1500 is made up of the S&P 500 SPX, +3.06%,

the S&P 400 Mid Cap Index MID, +3.18%

and the S&P Small Cap 600 Index SML, +3.80%.

The purpose of the list is to provide a starting point for further research. These stocks may be appropriate for you if you are looking for income, but you should do your own assessment to form your own opinion about a company’s ability to remain competitive over the next decade.

Cash flow is key

One way to measure a company’s ability to pay dividends is to look at its free cash flow yield. Free cash flow is remaining cash flow after planned capital expenditures. This money can be used to pay for dividends, buy back shares (which can raise earnings and cash flow per share), or fund acquisitions, organic expansion or for other corporate purposes.

If we divide a company’s estimated annual free cash flow per share by its current share price, we have its estimated free cash flow yield. If we compare the free cash flow yield to the current dividend yield, we may see “headroom” for cash to be deployed in ways that can benefit shareholders.

For this screen, we began with the S&P Composite 1500, then narrowed the list as follows:

Dividend yield of at least 5.00%.

Consensus free cash flow estimate available for calendar 2023, among at least five analysts polled by FactSet. We used calendar-year estimates, even though fiscal years for many companies don’t match the calendar.

Estimated 2023 free cash flow yield of at least double the current dividend yield.

For real-estate investment trusts, dividend-paying ability is measured by funds from operations (FFO), a non-GAAP figure that adds depreciation and amortization back to earnings. Adjusted funds from operations (AFFO) takes this a step further, subtracting cash expected to be used to maintain properties. So for the two REITs on the list, the FCF yield column makes use of AFFO.

For many companies in the financial sector, especially banks and insurers, free cash flow figures aren’t available, so the screen made use of earnings-per-share estimates. These are generally considered to run close to actual cash flow for these heavily regulated industries.

Here are the 21 companies that passed the screen, with dividend yields of at least 5% and estimated 2023 FCF yields at least twice the current payout. They are sorted by dividend yield:

Any stock screen has its limitations. If you are interested in stocks listed here, it is best to do your own research, and it is easy to get started by clicking the tickers in the table for more information about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

For the “estimated FCF yields,” consensus free cash flow estimates for calendar 2023 were used for all companies except the following:

For the REITs, (Uniti Group Inc. UNIT, +7.36%

and Macerich Co. MAC, +8.18%

), consensus AFFO estimates were used.

Consensus EPS estimates were used for Prudential Financial Inc. PRU, +5.66%,

Invesco Ltd. IVZ, +6.76%

and Franklin Resources Inc. BEN, +4.37%.

The U.S. stock market is heading higher again Tuesday, with the S&P 500 index continuing to climb above its 2022 low, but Bespoke Investment Group cautions that history shows its recent bounce may not signal the bear market’s end.

Bespoke’s research on first-day gains from bear-market lows found that bear markets typically end with even bigger moves than the one seen Monday, when the S&P 500 jumped 2.6%. The average move higher is “actually above 4%!” the firm wrote in an Oct. 3 note.

BESPOKE INVESTMENT GROUP NOTE DATED OCT. 3, 2022

U.S. stocks are trading up this week as Treasury yields fall and the soaring U.S. dollar loses some of its strength. The market moves come as investors look for any hints that the Federal Reserve might back off from its aggressive tightening of monetary policy.

On Monday, “markets clearly benefitted from huge declines in yields, which benefitted from Richmond Fed President Barkin echoing Governor Brainard’s speech Friday with concerns about the impact of dollar strength,” Bespoke said in its note. The reversal of the U.S. dollar, along with lower yields and higher stocks, showed investors “clearly bought that concern as the latest source of potential Fed dovishness.”

Bespoke was referring to comments by Fed Vice Chair Lael Brainard and Thomas Barkin, president of the Federal Reserve Bank of Richmond.

While the U.S. dollar’s strength has eased this week, the ICE US Dollar index DXY, -1.20%

is still up around 15% so far this year, according to FactSet data, at last check. The dollar has climbed as the Fed tightens monetary policy to combat high inflation.

“On balance, dollar appreciation tends to reduce import prices in the United States,” Brainard said in her speech Friday addressing global financial stability considerations. “But in some other jurisdictions, the corresponding currency depreciation may contribute to inflationary pressures and require additional tightening to offset.”

The Fed is “attentive to financial vulnerabilities that could be exacerbated by the advent of additional adverse shocks,” Brainard said in her speech. “For instance, in countries where sovereign or corporate debt levels are high, higher interest rates could increase debt-servicing burdens and concerns about debt sustainability, which could be exacerbated by currency depreciation.”

As for the decline in Treasury yields, the 10-year Treasury note dropped 15.2 basis points Monday to 3.650%, while two-year Treasury yield fell 10.3 basis points to 4.103%, according to Dow Jones Market Data. Treasury yields continued to dip on Tuesday, with the two-year TMUBMUSD02Y, 4.104%

at 4.08% and the 10-year TMUBMUSD10Y, 3.621%

falling to 3.60%, FactSet data show, at last check.

Meanwhile, the ICE US Dollar index, a measure of the dollar’s strength against a basket of rival currencies, was down more than 1% around midday Tuesday.

The U.S. stock market was moving sharply higher again on Tuesday, with the Dow Jones Industrial Average DJIA, +2.17%

jumping 2.6%, the S&P 500 SPX, +2.40%

climbing 2.9% and the Nasdaq Composite COMP, +2.66%

surging 3.3%, FactSet data show, at last check.

But after this week’s bounce, the S&P 500 remains down more than 20% this year, based on trading around midday Tuesday.

“It’s easy to read-in to very high two-way volatility across assets as signaling a Fed pivot is finally here, but we just haven’t seen any reason for that,” Bespoke said. “Until the Fed durably shifts away from their concern over inflation, headwinds for stocks and bonds alongside tailwinds for the dollar will continue.”

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.

The rising dollar lowers prices on imported goods for Americans and can also lower their international travel costs. But Michael Wilson, Morgan Stanley’s chief equity strategist, warns that earnings for the S&P 500 SPX, -1.51%

would decline as a direct result of the strong dollar and called the current foreign-exchange backdrop an “untenable situation” for the stock market.

This is what happens when bearish sentiment runs high

Michael Brush interviews David Baron, co-manager of the Baron Focused Growth Fund BFGFX, -0.76%,

who describes opportunities cropping up as institutional investors dump stocks. He also explains his winning long-term strategy, which has included a very long-term investment in Tesla Inc. TSLA, -1.10%.

When interest rates rise, bond prices fall. But it also means that if you have money to put to work, bond yields have become much more attractive.

Khuram Chaudhry, a European equity quantitative strategist at JPMorgan in London, makes the case for buying bonds now.

What about preferred stocks?

Getty Images/iStockphoto

Preferred stocks feature stated dividend yields and prices that move the same way bond prices do. That means prices for many issues are now heavily discounted to face value and that current yields are much higher than they were at the end of 2021. Here’s an in-depth guide on how to research preferred stocks and make your own selections.

Stanley Druckenmiller predicted a “hard landing” in 2023 for the U.S. economy while speaking at CNBC’s Delivering Alpha Investor Summit on Sept. 28.

Bloomberg

Stanley Druckenmiller predicted a U.S. recession in 2023 as a result of monetary policy tightening by the Federal Reserve. That may not be much of a stretch, considering that the U.S. economy contracted during the first half of 2022, according to revised GDP figures from the Bureau of Economic Analysis.

After the new U.K. government of Prime Minister Liz Truss announced a massive tax cut along with a new spending program to help counter rising fuel costs and new borrowing, the pound hit a new low against the dollar on Sept. 26 as investors and money managers panicked and sold-off U.K. government bonds. Steve Goldstein explains how and why the Bank of England came tot the rescue.

After Tesla CEO Elon Musk said the upcoming Cybertruck would be sufficiently waterproof to “serve briefly as a boat,” the San Francisco Bay Ferry offered this advice to patrons.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.