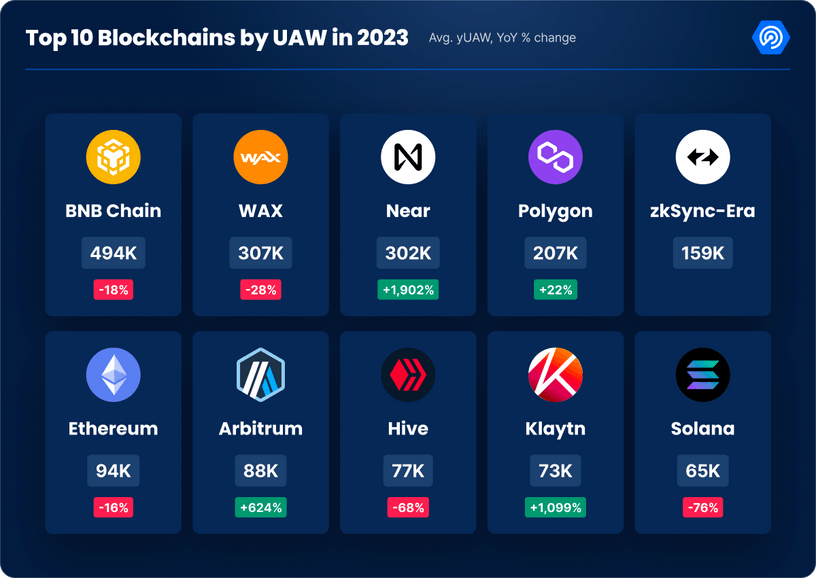

In 2023, web3 saw a 124% surge in Unique Active Wallets, with Near, Klaytn, and Arbitrum leading growth, while others declined.

In a recent report by blockchain analytics platform DappRadar on January 11, 2024, the web3 landscape witnessed substantial growth, with a 124% increase in Unique Active Wallets (UAW) engaging with decentralized applications (DApps) throughout 2023.

The data spotlighted Near, Klaytn, and Arbitrum as the frontrunners in growth, while Harmony, Solana, and Hive experienced declines in user engagement.

On average, 4.2 million UAW interacted daily with web3 apps, doubling the previous year’s figures. Nonfungible token (NFT) products dominated growth, boasting a 166% increase, followed by defi with a 112% surge. Social media apps, buoyed by leading protocols like Friend.tech, Lens Protocol, and Galxe, reported a 29% gain.

Near, Klaytn, and Arbitrum emerged as the standout performers, exhibiting growth rates of 1,902%, 1,099%, and 624%, respectively. Key DApps on these networks, such as KAI-CHING, SuperWalk, and Uniswap V3, contributed significantly to their success.

Conversely, Harmony, Solana, and Hive faced setbacks, experiencing declines of 96%, 76%, and 68%, respectively. Harmony’s struggles were linked to a bridge exploit in June 2022, while Solana grappled with challenges tied to its association with FTX.

The report acknowledged Solana’s impressive recovery in the latter part of 2023. Hive’s loss of users was speculated to stem from missing financial targets and reporting significant losses.

Overall, the report underscores the vibrancy of blockchain networks, citing instances like Stars Arena driving 10,000 UAW to the Arbitrum network in October and Ethereum collecting over $54.3 million in fees in a single week in November.

Hardware wallet manufacturer Ledger has responded to a recent security breach resulting in the theft of $600,000 worth of user assets.

The company has pledged to enhance its security protocols by eliminating Blind Signing, a process where transactions are displayed in code rather than plain language, by June 2024.

Ledger Takes Responsibility For ConnectKit Attack

In a statement, Ledger emphasized its focus on addressing the recent security incident and preventing similar occurrences in the future.

The company acknowledged the approximately $600,000 in assets that were impacted by the ConnectKit attack, particularly affecting users blind signing on Ethereum Virtual Machine (EVM) decentralized applications (dApps).

Furthermore, Ledger pledged to make sure affected victims are fully compensated, including non-Ledger customers, with CEO & Chairman Pascal Gauthier personally overseeing the restitution process.

According to the statement, Ledger has already initiated contact with affected users and is actively working with them to resolve their specific cases.

In addition, by June 2024, blind signing will no longer be supported on Ledger devices, contributing to a “new standard of user protection” and advocating for “Clear Signing,” which refers to a process that allows users to verify transactions on their Ledger devices before signing them across dApps.

On this matter, Ledger’s CEO Pascal Gauthier stated:

My personal commitment: Ledger will dedicate as much internal and external resources as possible to help the affected individuals recover their assets.

Heightened dApp Security Measures

According to an incident report released by the hardware wallet manufacturer, the attack exploited the Ledger Connect Kit, injecting malicious code into dApps utilizing the kit.

This malicious code redirected assets to the attacker’s wallets, tricking EVM dApp users into “unknowingly signing transactions” that drained their wallets.

Ledger addressed the attack by deploying a genuine fix for the Connect Kit within 40 minutes of detection. The compromised code remained accessible for a limited time due to the nature of content delivery networks (CDNs) and caching mechanisms.

Ledger acknowledged the risks faced by the entire industry in safeguarding users and emphasized the need to continually raise the bar for security in dApps.

The company plans to strengthen its access controls, conduct audits of internal and external tools, reinforce code signing, and improve infrastructure monitoring and alerting systems.

Additionally, Ledger will educate users on the importance of Clear Signing and the potential risks associated with blind signing transactions without a secure display.

Notably, with Clear Signing, users are presented with a clear and readable representation of the transaction details, enabling them to review and validate the transaction before providing their signature.

This added layer of transparency and verification helps users mitigate the risks associated with front-end attacks or malicious code injected into decentralized applications

The 1-day chart shows the total crypto market cap’s valuation at $1.59 trillion. Source: TOTAL on TradingView.com

Featured image from Shutterstock, chart from TradingView.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

DappBay, a web3 dApp store for users on the BNB Chain, has flagged over 100 risky decentralized applications (dapps) in its recent update.

BNB Chain shared the findings on X (formerly Twitter). See below.

BNB Chain launched DappBay in July 2022, allowing users to discover new web3 projects while being kept abreast of their risk levels in real-time.

At the heart of DappBay is its Red Alarm component, a risk screening tool that can help identify possible rug pulls and scam projects by checking logic flaws or fraud risks in smart contracts.

This tool regularly updates its list with dapps and smart contracts that have been assessed as scams or deemed to carry an extraordinarily high level of risk.

Risky dapps

One of the prominent names on DappBay’s list of risky dapps is Genesis Universe, a non-fungible token (NFT) card exploration game built on the BNB Smart Chain. In this game, players explore and fight in a new world, following the increasingly popular play-to-earn approach.

However, its presence on the Red Alarm list points to possible risks in its operation, therefore advising caution for both users and investors.

Another notable addition to DappBay’s Red Alarm list is DeXe DAO Studio, categorized under tools and utilities and marked with a “significant risk” level.

This dapp reportedly supports the development of decentralized autonomous organizations (DAOs), highlighting the importance of active, valuable member involvement and expertise. However, despite its ambitious goals, the assigned risk level indicates possible drawbacks or issues that users need to consider.

Web3 Pilot, a first-in-first-out defi investment platform, was identified as a high-risk dapp. Per Red Alarm’s indication, the platform’s main risk revolves around it being a possible Ponzi scheme, misleadingly enticing investors with the allure of unusually high returns.

Other decentralized applications highlighted in Red Alarm’s list include QuickPay, Silo, and Defi Ujm. The first two are categorized as Ponzi schemes, while the third is suspected to be a phishing website.

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Web3, akin to numerous groundbreaking innovations, has been crafted with the explicit goal of improving and enriching our daily lives. It stands at the forefront of technological advancements that promise to reshape how we interact with digital systems and services.

What makes web3 particularly noteworthy is its ability to transcend the boundaries of traditional financial institutions, as many of them have already discerned the potential for symbiosis with these cutting-edge technologies. Consequently, they are proactively delving into collaborative efforts and seeking ways to seamlessly integrate web3 into their core operations.

This intriguing interplay between web3 and traditional finance is shaping a new landscape that is bound to influence the global economy in profound ways. In 2024, we stand on the cusp of a transformative era, and it’s imperative that we dive into the exciting opportunities web3 holds for our world and the broader economic framework.

Amidst the backdrop of global economic and political uncertainties, there exists a palpable optimism surrounding the persistent growth of blockchain and decentralized applications (dapps). In an illuminating report from DappRadar, we observe a striking 15% surge in the average number of daily unique active wallets (dUAW) actively participating in decentralized applications, a figure that has soared to an average of 2.2 million dUAW since the second quarter of 2023.

Industry dominance by UAW in the dapp ecosystem | Source: DappRadar

While this growth paints a promising picture of the future, it’s essential to recognize the pressing concerns related to identity and privacy that loom large. The digital landscape is evolving rapidly, and the need for heightened security and accountability has never been more apparent. Fortunately, a significant shift within primary markets is discernible, with a pronounced emphasis on enhancing transparency. This concerted effort holds the potential to substantially curtail the illicit use of cryptocurrencies, evade sanctions and taxes, and mitigate similar issues that have challenged the integrity of the financial world.

For web3 technologies to thrive and gain widespread acceptance, a critical element is the collective embrace of transparency by users and the establishment of a robust regulatory framework that prioritizes the protection of all participants within the ecosystem. Regulators, too, find themselves in uncharted territory as they navigate the swiftly evolving innovation landscape. This necessitates a realization that adapting existing regulations will yield outcomes different from what we’ve known, ultimately shaping a future where trust, security, and accountability hold sway.

The embrace of decentralized finance protocols has captured the attention and intrigue of both investors and regulators, establishing itself as the newest and potentially transformative innovation within the cryptocurrency domain.

At the present juncture, the real-world applications of defi, especially in the context of cross-border transactions, serve as compelling testaments to its distinct advantages over conventional systems. These use cases underscore the efficiency and security that defi brings to the table, paving the way for a financial landscape that needs to be addressed by geographical constraints and costly intermediaries.

However, while defi’s potential is undeniably promising, its broader adoption hinges on our ability to identify and champion additional use cases that provide tangible, real-world benefits. The impetus for this shift towards defi is particularly pronounced in developing economies, where inefficiencies and limited accessibility have historically plagued the legacy financial systems, making them ripe for the innovations that defi offers.

The intriguing relationship between traditional finance institutions and the emerging web3 landscape is a dynamic that warrants a closer examination. While on the surface, they might appear as rivals, the realization of web3’s full potential is intricately tied to the collaboration and integration of traditional finance.

In the fast-evolving realm of emerging technologies, established incumbents often find it advantageous to seek partnerships with specialized providers rather than embarking on entirely new ventures. This approach allows them to tap into the innovative strengths of these specialized players. An illustrative case is E-Gates, which is strategically positioned to harness the advancements within the realms of cryptocurrency and blockchain, and which plays a pivotal role in enabling traditional entities, including financial institutions and e-commerce merchants, to seamlessly incorporate these transformative features into their existing operations while upholding regulatory compliance and reliability.

These progressive developments carry the potential to be a genuine game-changer, effectively bridging web3 with the familiar landscape of traditional financial systems fostering innovation and inclusivity in the ever-evolving financial ecosystem.

As we gaze into the future, the landscape of web3 finance beckons with boundless potential. Its transformative power extends far beyond the mere transfer of value, offering us a comprehensive reimagining of finance itself. In this forthcoming era, the doors to financial services are thrown wide open, promising widespread access and inclusivity like never before.

Defi is a central pillar of this transformation, with its profound impact evident across borrowing, lending, trading, and income generation. It introduces a new dimension of financial freedom and flexibility, rewriting the traditional rulebook.

Smart contracts, another cornerstone of the web3 revolution, ushering in an era of efficient and secure agreements and transactions, stripping away the need for intermediaries and offering newfound trust in digital interactions.

Not to be overshadowed, NFTs emerge as trailblazers, fundamentally redefining the concept of digital ownership and propelling the creative economy into uncharted territory.

The evolution of web3 is not in isolation; it adapts to regulatory frameworks and boldly explores cross-chain operations, diligently paving the path for further innovation. During this transformative journey, 2024 promises to be a year of groundbreaking advancements and fresh horizons within this dynamic field. Ready to join us in anticipating 2024’s exciting developments?

Sarah Clark

Sarah Clark, CEO at E-Gates, is a seasoned executive with broad international experience in various industries, including travel, retail, financial services, fintech, and e-commerce across Europe, the US, the Middle East, and Africa. Sarah grew PayPal’s business across three continents to deliver the highest revenue growth in the company despite a challenging regulatory environment. She also launched and ran the European operations of two venture-backed businesses—LootCrate and Clearco—delivering double-digit revenue growth.

A large number of recent Ponzi schemes have used decentralized finance (DeFi) infrastructure to defraud their customers. This article explores the DeFi ecosystem and how fraudsters are able to exploit it to steal from crypto newbies.

Representation of cryptocurrency and the word ‘DeFi’ displayed on a screen in the background are … [+] seen in this illustration photo taken in Poland on November 6, 2021. (Photo by Jakub Porzycki/NurPhoto via Getty Images)

NurPhoto via Getty Images

DeFi is a broad term for financial infrastructure and financial services provided on public blockchains via smart contract technology. Ether ETH eum, Binance Chain, Cardano ADA , and Solana SOL are among the most popular smart contract blockchains, allowing developers to create dApps (decentralized applications) on their network. These dApps can be used for a variety of purposes, but the majority of them are financial in nature, giving rise to the term “DeFi.”

DeFi development has progressed to the point where token creation templates exist, allowing anyone to create a token in a matter of minutes without any programming knowledge or experience. This opens the door to a Pandora’s box in which token creators can create great decentralized applications while malicious people can use the technology to create malicious dApps such as Ponzi schemes.

Ponzi schemes are illegal in practice. Some blockchains, however, are decentralized, and there is no single jurisdiction in charge of enforcing compliance with local laws. Some centralized blockchains are based in areas with little or no oversight over their operations. This opens the door for fraudsters to set up Ponzi schemes on these chains.

Most blockchains that allow for the development and deployment of dApps do not require a know-your-customer (KYC) process. This means that people can create dApps anonymously.

So, what exactly are Ponzi schemes, and how do they function in the DeFi space? A Ponzi scheme, named after the Italian con artist Charles Ponzi, is an investment fraud that pays existing investors with funds collected from new investors. It does not necessarily invest the funds of the investors, but it promises existing investors high returns in a short period of time, which are frequently higher than all other mainstream yields.

(Original Caption) Charles Ponzi, the “financial wizard” of Boston who succeeded in amassing a … [+] fortune through his endless chain of sales of Foreign Exchange following the World War, later went to Florida where he hoped to recoup his losses of $2,000,000 owing to investors from his former scheme. In this photo, he is shown in an interesting attitude, as he rests at Jacksonville, Florida.

Bettmann Archive

Ponzi schemes rely on the number of new investors increasing indefinitely. If a Ponzi scheme fails to attract new investors, it will collapse quickly. Furthermore, if a large number of investors rush to withdraw their funds, the Ponzi schemers realize they are losing money and close shop because they are unable to honor the debts. In other cases, authorities may raid a Ponzi scheme office and, upon discovering that it is an illegal enterprise, it collapses immediately.

For example, the most recent Ponzi scheme involved Eddy Alexandre, CEO of EminiFX, who promised investors a weekly 5% return on investment. The FBI apprehended him last week for allegedly defrauding his clients out of more than $59 million. He claimed to have a “Robo-Advisor Assisted account” system that would invest the monies in crypto and Forex. Beware of such scams and practice due diligence before investing in such a product.

Ponzi schemes in the DeFi space may take a different approach to defrauding customers. This can range from promising the next 100x ZRX moonshot (a token sold at a low price in exchange for a legitimate coin/token with the promise that the new token value will increase 100 times) to promising high staking rewards for new token holders. In other cases, DeFi Ponzi scammers will sell tokens to unsuspecting buyers while promising high staking rewards.

Staking rewards and yield farming are the two most appealing features in DeFi ecosystems. DeFi users will deposit and lock their tokens on the platform to earn a huge annual percentage yield because DeFi ecosystems rely on staked tokens for consensus. This means that if you stake your tokens on a DeFi platform that pays out, say, 1000 percent (yes, they can get that high) annually, you will have 10 times more tokens in a year.

However, because the majority of participants are also staking, the staking rewards amount to token inflation, which drives the price down. This means that in order for you to sell your staked tokens for a profit after a year, the ecosystem must experience a significant increase in new investors to offset the increasing supply. Because it relies on new investors to maintain its value, it is similar to other Ponzi schemes.

Of course, not everyone will agree with me, but the similarities are striking. If a DeFi protocol with high staking rewards does not attract new investors and is unable to burn excess supply, its price often crumbles.

Fraudsters who sold tokens for Bitcoin, Ethereum, Binance Coin, or any other seemingly valuable token make the most profit. Simply put, the con artists sell their clients an asset that they can inflate for an asset that they cannot, promise high returns, and then flood the market with more tokens in exchange for more tokens that they cannot inflate after the DeFi protocol goes live.

Yield farming, on the other hand, is dependent on the community providing liquidity for participants to buy newly minted tokens on a decentralized exchange. A yield farmer will technically purchase an equal dollar amount of two assets. Half of it goes to the newly minted token, and the other half to a counter token/coin like Ethereum or USDT.

Following that, the new liquidity is added to a pool on an automated market maker (AMM) platform (Often described as a decentralized exchange). New entrants to this pool can automatically convert their tokens such as Ethereum or USDT for the newly minted token. The fees charged on transactions in this pool are distributed automatically to the liquidity providers (yield farmers).

To consistently earn high yields from yield farms, fraudsters may charge high transaction fees, and future growth is heavily reliant on a massive increase in new users. Most yield farm rewards will be denominated in the newly minted token. As the DeFi Ponzi scheme expands, fraudsters frequently attack this automated liquidity by exchanging newly minted tokens for the counter coin/token, driving the price down to zero or close to it. Yield farmers and stakers in most DeFi Ponzi schemes are often left holding billions of worthless tokens.

There is a good number of DeFi protocols that provide value and utility to their investors. Others prevent fraud by going through audit certifications while others plan periodic token burns to reduce inflation.

As a new crypto trader looking to invest in DeFi, it is critical to ensure that the token you are purchasing does not rely on the growth of new users, as this has a strong correlation with Ponzi schemes. Furthermore, if the high returns promised by a DeFi protocol are not the result of value creation and utility, they are most likely the result of new investors, raising the correlation with Ponzi schemes.

Almost all DeFi scams attribute the theft of client funds to “unknown scammers.” For example, the founding brothers of the South African Africrypt DeFi Ponzi scheme allegedly stole $3.6 billion in what is considered the largest DeFi heist in history. Before defrauding over a quarter million customers and claiming that they were hacked, the two brothers claimed to have an AI-driven trading system that was earning above-market returns.

If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.